International Trade and Finance: Overview and Issues for the 115th Congress

The U.S. Constitution grants authority to Congress to regulate commerce with foreign nations. Congress exercises this authority in numerous ways, including through oversight of trade policy and consideration of legislation to implement trade agreements and authorize trade programs. Policy issues cover areas such as U.S. trade negotiations, U.S. trade and economic relations with specific regions and countries, international institutions focused on trade, tariff and nontariff barriers, worker dislocation due to trade liberalization, enforcement of trade laws and trade agreement commitments, import and export policies, international investment, economic sanctions, and other trade-related functions of the federal government. Congress also has authority over U.S. financial commitments to international financial institutions and oversight responsibilities for trade- and finance-related agencies of the U.S. government.

Issues in the 115th Congress

During the 2016 presidential campaign, U.S. trade policy and trade agreements received significant attention, particularly regarding the impact of trade agreements on the U.S. economy and workers. Among the more potentially prominent international trade and finance issues the 115th Congress is considering, or may consider, are:

the status of Trade Promotion Authority (TPA), which is authorized through 2021, provided the President requests an extension and Congress does not enact an extension disapproval resolution before July 2018;

the Administration’s renegotiation of the North American Free Trade Agreement (NAFTA) and efforts to modify the U.S.-South Korea (KORUS) free trade agreement (FTA);

U.S.-China trade relations, including investment issues, intellectual property rights (IPR) protection, forced technology transfer, currency issues, and market access liberalization;

proposals to launch new bilateral FTAs, such as with the United Kingdom, Japan, or possibly with countries in Africa;

the future of U.S.-Asia trade and economic relations, given President Trump’s withdrawal of the United States from the Trans-Pacific Partnership (TPP) and China’s expanding Belt and Road Initiative;

the future status of trade negotiations launched under the Obama Administration, including for the proposed Transatlantic Trade and Investment Partnership (T-TIP) FTA with the European Union (EU) and the Trade in Services Agreement (TiSA);

oversight of World Trade Organization (WTO) agreements and negotiations, including the completed Trade Facilitation Agreement (TFA) and expansion of the Information Technology Agreement (ITA), as well as potential agreements on environmental goods and the WTO’s future overall direction;

the Administration’s enforcement of U.S. trade laws;

the effects of trade on the U.S. economy, jobs, and manufacturing, as well as policies that support U.S. workers and industries adversely affected by trade agreements;

international finance and investment issues, including U.S. funding for and oversight of international financial institutions (IFIs), the creation of development and infrastructure banks by emerging economies, and U.S. negotiations on new bilateral investment treaties (BITs), notably with China and India; and

oversight of international trade and finance policies to support development and/or foreign policy goals, including trade preferences for sub-Sahara Africa and sanctions on Iran, North Korea, Russia, and other countries.

International Trade and Finance: Overview and Issues for the 115th Congress

Jump to Main Text of Report

Contents

- Overview

- The United States in the Global Economy

- The Role of Congress in International Trade and Finance

- Policy Issues for Congress

- Trade Promotion Authority (TPA)

- The World Trade Organization (WTO)

- U.S. Bilateral and Regional Trade Agreements

- North American Free Trade Agreement (NAFTA) Renegotiation

- U.S.-South Korea (KORUS) FTA Modifications

- Trans-Pacific Partnership (TPP)

- Transatlantic Trade and Investment Partnership (T-TIP)

- Brexit and a Potential U.S.-UK Free Trade Agreement (FTA)

- Trade in International Services Agreement (TiSA)

- U.S.-China Commercial Relations

- Economic Effects of Trade

- Trade and U.S. Jobs

- Trade Adjustment Assistance (TAA)

- Intellectual Property Rights (IPR)

- IPR in Trade Agreements & Negotiations

- Other IPR Trade Policy Tools

- International Investment

- Foreign Investment and National Security

- U.S. International Investment Agreements (IIAs)

- Promoting Investment in the United States

- Trade Enforcement

- Dispute Settlement

- Trade Remedies

- National Security and Section 232

- Digital Trade

- New Barriers

- EU-U.S. Data Flows

- Exchange Rates

- Labor and Environment

- Labor Provisions in FTAs

- Environment Provisions in FTAs

- Export Controls and Sanctions

- Export Controls

- Economic Sanctions

- Miscellaneous Tariff Bills (MTBs)

- Trade and Development

- Trade Preferences

- Trade Capacity Building

- U.S. Trade Finance and Promotion Agencies

- Export-Import Bank of the United States (Ex-Im Bank)

- Overseas Private Investment Corporation (OPIC)

- International Trade Administration (ITA) of U.S. Department of Commerce

- U.S. Trade and Development Agency (TDA)

- International Financial Institutions (IFIs) and Markets

- International Economic Cooperation (G-7 and G-20)

- International Monetary Fund (IMF)

- Multilateral Development Banks (MDBs)

- The Asian Infrastructure Investment Bank (AIIB)

- Economic Crisis in Venezuela

- Looking Forward

Figures

- Figure 1. Global Economy: Snapshot

- Figure 2. Existing and Proposed U.S. Free Trade Agreements

- Figure 3. U.S. Trade with South Korea

- Figure 4. U.S. International Investment Agreements

- Figure 5. Global FDI Stock and ISDS Cases

- Figure 6. Trade Weighted U.S. Dollar Index

- Figure 7. Evolution of Labor Commitments

- Figure 8. Evolution of Environment Commitments

- Figure 9. G-20 Members

Summary

The U.S. Constitution grants authority to Congress to regulate commerce with foreign nations. Congress exercises this authority in numerous ways, including through oversight of trade policy and consideration of legislation to implement trade agreements and authorize trade programs. Policy issues cover areas such as U.S. trade negotiations, U.S. trade and economic relations with specific regions and countries, international institutions focused on trade, tariff and nontariff barriers, worker dislocation due to trade liberalization, enforcement of trade laws and trade agreement commitments, import and export policies, international investment, economic sanctions, and other trade-related functions of the federal government. Congress also has authority over U.S. financial commitments to international financial institutions and oversight responsibilities for trade- and finance-related agencies of the U.S. government.

Issues in the 115th Congress

During the 2016 presidential campaign, U.S. trade policy and trade agreements received significant attention, particularly regarding the impact of trade agreements on the U.S. economy and workers. Among the more potentially prominent international trade and finance issues the 115th Congress is considering, or may consider, are:

- the status of Trade Promotion Authority (TPA), which is authorized through 2021, provided the President requests an extension and Congress does not enact an extension disapproval resolution before July 2018;

- the Administration's renegotiation of the North American Free Trade Agreement (NAFTA) and efforts to modify the U.S.-South Korea (KORUS) free trade agreement (FTA);

- U.S.-China trade relations, including investment issues, intellectual property rights (IPR) protection, forced technology transfer, currency issues, and market access liberalization;

- proposals to launch new bilateral FTAs, such as with the United Kingdom, Japan, or possibly with countries in Africa;

- the future of U.S.-Asia trade and economic relations, given President Trump's withdrawal of the United States from the Trans-Pacific Partnership (TPP) and China's expanding Belt and Road Initiative;

- the future status of trade negotiations launched under the Obama Administration, including for the proposed Transatlantic Trade and Investment Partnership (T-TIP) FTA with the European Union (EU) and the Trade in Services Agreement (TiSA);

- oversight of World Trade Organization (WTO) agreements and negotiations, including the completed Trade Facilitation Agreement (TFA) and expansion of the Information Technology Agreement (ITA), as well as potential agreements on environmental goods and the WTO's future overall direction;

- the Administration's enforcement of U.S. trade laws;

- the effects of trade on the U.S. economy, jobs, and manufacturing, as well as policies that support U.S. workers and industries adversely affected by trade agreements;

- international finance and investment issues, including U.S. funding for and oversight of international financial institutions (IFIs), the creation of development and infrastructure banks by emerging economies, and U.S. negotiations on new bilateral investment treaties (BITs), notably with China and India; and

- oversight of international trade and finance policies to support development and/or foreign policy goals, including trade preferences for sub-Sahara Africa and sanctions on Iran, North Korea, Russia, and other countries.

Overview1

During the first session of the 115th Congress, Congress faced numerous international trade and finance policy issues. A major focus was examining and responding to the Trump Administration's evolving trade policy. U.S. trade policy under President Trump to date arguably represents a significant shift from recent past Administrations under both Republicans and Democrats. In particular, the Administration has displayed a more critical view of U.S. trade agreements, made greater use of various U.S. trade laws with the potential to restrict U.S. imports, and placed increased emphasis on bilateral trade balances as a key metric of the health of U.S. trading relationships. Another major issue before Congress involved growing interest in whether and in what ways the U.S. process for determining the national and economic security implications of foreign investment in the United States should be reformed. Continued focus on the U.S.-China economic relationship, and economic sanctions against Iran, Cuba, North Korea, Russia, and other countries also have been of interest to Congress.

President Trump's withdrawal of the United States from the Trans-Pacific Partnership (TPP) free trade agreement (FTA) among 12 Asia-Pacific nations, alongside a stated preference for negotiating bilateral rather than multi-party trade agreements were notable developments in the Trump Administration's policy approach to U.S. trade agreements. Also significant are Administration initiatives to potentially revise the two largest existing U.S. FTAs, through the ongoing renegotiation of the North American Free Trade Agreement (NAFTA), and modification talks regarding the U.S.-South Korea (KORUS) FTA. These decisions, in addition to the evolving global landscape on trade agreements, including a recently-concluded, revised TPP (now called the Comprehensive and Progressive Agreement for Trans-Pacific Partnership (CPTPP)) among the 11 parties, without the United States, raise potentially significant legislative and policy issues for Congress, including: (1) potential congressional consideration of legislation to implement a revised NAFTA, (2) the economic and strategic rationale for U.S. participation in multi-party and other FTAs, (3) the extent to which past U.S. FTAs should be modernized or revised and, if so, in what manner, (4) how much priority should be placed in U.S. trade policy on new FTA and multilateral trade agreements, and (5) the effect of FTAs not including the United States on U.S. economic and broader interests, and the appropriate U.S. response to the proliferation of agreements.

Another major issue is the role of the United States in the multilateral, rules-based trading system under the World Trade Organization (WTO), historically led by the United States. The WTO has served as the foundation of the international trading system and WTO agreements serve as the floor of commitments in U.S. FTAs, but the institution has languished for decades in terms of achieving new multilateral trade disciplines and liberalization in important areas, such as digital trade. President Trump may formally request and justify to Congress an extension of current U.S. Trade Promotion Authority (TPA) until 2021, to provide authority for expedited consideration of future trade agreements if they meet specific conditions and criteria. This process would present Congress a significant opportunity to examine the U.S. role in the WTO and current and future trade agreement negotiations, particularly in how they meet TPA's congressionally-mandated U.S. trade negotiating objectives.

The United States under the Trump Administration has renewed the use of specific trade laws that have not been used in several years, such as Section 232, designed to investigate the national security impact of specific imports. It has also placed greater emphasis on "fair" and "reciprocal" trade. For example, with respect to China, a Section 301 case was launched involving China's policies on intellectual property rights and forced technology transfer, among other measures. China continues to be viewed as a growing main competitor of the United States in the global economy, as recognized in the recently-released U.S. National Security Strategy.2

The policy implications for Congress of potential action under various trade investigations may depend on a number factors such as: how firms, industries and workers are affected by measures, such as increased tariffs, that may be taken; what other countries' reactions may be (such as possible retaliation); and how future actions are in line with core U.S. commitments and obligations under the WTO and other trade agreements. The U.S.-China trade and economic relationship is complex and wide-ranging. It will likely entail continued close examination by Congress in terms of current and future policy issues. In addition to specific trade practices of concern, Congress may undertake closer scrutiny of the economic and geopolitical implications of China's sizable Belt and Road Initiative to finance and develop infrastructure across multiple countries and regions, as well as the proliferation of China's industrial policies in high technology industries that may challenge U.S. firms and potentially disrupt global markets if fully implemented.

International trade and finance issues have been important to Congress because they can affect the overall health of the U.S. economy and specific sectors, the success of U.S. businesses and workers, and Americans' standard of living. They also have implications for U.S. geopolitical interests. Conversely, geopolitical tensions, risks, and opportunities can have major impacts on international trade and finance. These issues are complex and at times controversial, and developments in the global economy often make policy deliberation more challenging, because they involve balancing many competing interests.

Congress is in a unique position to address these and other issues, particularly given its constitutional authority for legislating and overseeing international trade and financial policy. This report provides a brief overview of select trade and finance issues that may be of interest to the 115th Congress.

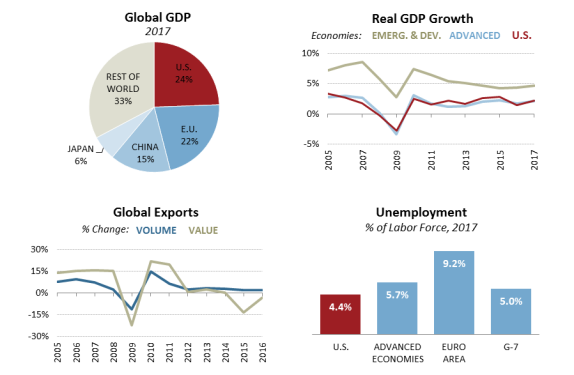

The United States in the Global Economy

Since the end of World War II, the United States has served as the chief architect of an open and rules-based international economic order that has been characterized by trade expansion and growing economic integration. Some see this global economic order fragmenting and becoming less governable. The U.S. leadership role is being challenged both from abroad by rising economic powers such as China and from within the United States by groups that have been adversely affected by U.S. integration in the global economy.

Overall, the global economy in 2017 began to display signs of a synchronized recovery among major economies from the 2008-2009 financial crisis and deep economic recession. Similarly, international financial markets improved and are expected to continue growing, despite recent signs of increased volatility. Nevertheless, uncertainty over the direction of monetary policy among major central banks, some concerns about rates of inflation, slower growth in real wages and productivity, and demographic challenges are among the issues that could restrain the recovery.

The International Monetary Fund (IMF) estimates that global real annual GDP growth increased by 3.7% in 2017, and will increase by 3.9% in 2018, up slightly from previous estimates.3 This forecast is based on the U.S. economy growing at a rate of 2.7%, as a result of a return to a more normal monetary policy stance and a temporary boost arising from the macroeconomic impact of tax reform and cuts. The U.S. Bureau of Economic Analysis (BEA) reported that the rate of U.S. economic growth slowed in the fourth quarter of 2017 to 2.6%, compared to an annualized rate of 3.2% in the third quarter.4 Of broader potential significance is the movement of the dollar against other major currencies. Since the start of 2017, the dollar has depreciated 9% against other major currencies, following a large appreciation over the previous three years. Depreciation in the value of the dollar generally makes imports more expensive reducing the purchasing power of U.S. consumers, and may worsen the U.S. trade deficit in the short term depending on the price sensitivity of import consumption. However, a weaker dollar also generally makes U.S. exports more competitive.

The IMF forecasts that developed economies as a group will grow at 2.3% in 2018. Although the economic recovery in the EU is progressing, the growth rate is projected to remain low in comparison with other economic recoveries, reflecting high levels of corporate debt and non-performing loans that are restraining business investment. Emerging market and developing economies are projected by the IMF to grow by 4.9%, up from 4.7% in 2017, while China's economy is projected to grow at 6.6% in 2018, down slightly from the 6.8% rate experienced in 2017. Commodity exporters are projected to experience a stronger rate of economic growth as a result of a partial recovery in commodity prices, which also would support a higher rate of growth in global trade volumes. Increased global manufacturing activity and investment in infrastructure and equipment are also projected to support higher levels of global trade.

Despite these positive signs, the World Economic Forum (WEF) notes a number of risks that could limit the strength and pace of the projected recovery and rate of global economic growth.5 These risks include: cybersecurity risks in both the private and government sectors; economic risks, including rising trade protectionism; environmental risks; and geopolitical risks (such as conflict over North Korean nuclear development). Other risks include savings and investment relative to GDP, which serve as building blocks for future growth, but continue to lag behind pre-financial 2008 crisis levels in the advanced economies. Similarly, global trade is growing, but lags behind historical levels.

Emerging markets (EMs) as a group are expected to face fewer risks to sustainable rates of economic growth in 2018 due to a modest recovery in global trade and more stable exchange rates, inflation, commodity prices, and equity markets. Growth rates are projected to recover somewhat in Russia and Brazil, due to more stable oil and commodity prices, but increased uncertainty over political and policy direction could constrain the rate of growth in Brazil. Additionally, China is expected to experience slower growth rates as it attempts to navigate toward a more sustainable growth model that is more focused on boosting innovation and private consumption, rather than fixed investment and exporting, as sources of economic growth. In Venezuela, a major economic and financial crisis has surfaced that could cause the economy to continue to contract. The IMF projects that continued social turmoil in Venezuela will cause economic activity to fall by 15% in 2018. These and other developments, such as ongoing tension and concern over North Korea's nuclear arms policies, contribute to uncertainties that potentially could impact global markets.

|

|

Source: Data from International Monetary Fund, World Economic Outlook, October 2017 and World Trade Organization Trade Statistics, accessed February 2018. Figure created by CRS. Note: 2017 data is forecasted. |

Over the long term, developed and developing economies are struggling to find the right policy mix to address low growth, low inflation, and low levels of productivity growth, referred to as structural stagnation by some. Developed and some developing economies are experiencing declining or flat birth rates, which portend a smaller work force in the future and lower potential rates of economic growth. Aging work forces, a demographic unfolding everywhere except Africa and the Middle East, may also restrain economic growth. Under similar challenging conditions, nations in the past have turned to broad, multinational trade liberalization agreements to stimulate economic growth through improvements in productivity by removing market-distorting barriers.

The United States accounts for approximately a quarter of global gross domestic product (GDP) in nominal U.S. dollars and 9.1% of global trade (Figure 1). Although still recovering from the worst recession in eight decades, overall U.S. economic conditions have improved with the unemployment rate at 4.1% in December 2017 from a high of 10% in 2009. The stabilization in oil prices is affecting the U.S. economy. Relatively low energy prices are expected to raise consumers' real incomes, improve the competitive position of some industries, and stabilize employment and output in the energy sector.

With improvements in the economy as a whole, average U.S. real household incomes are slowly recovering from the 2008-2010 economic recession. The United States, similar to other economies, has experienced widening disparity in incomes that many view as fueling domestically-focused political movements and a backlash against globalization. The Trump Administration achieved a major goal by lowering corporate tax rates, a move that is projected to stimulate the economy. The Administration has indicated that it is also turning to infrastructure spending. It has also made reducing U.S. bilateral trade deficits a priority issue, as the U.S. trade deficit in 2017 reached its highest level since 2008. However, using a broader measure, the current account (which includes the trade balance, as well as unilateral transfers and income on overseas investments), the U.S. deficit has fallen significantly since its peak in 2006, as have the surpluses in China and Japan.

For many economists, an improving outlook for global trade and the potential role for the United States in supporting global growth as a major importer and overseas investor may overshadow potential concerns over global imbalances. The Euro and Japanese yen have experienced periods of volatility since the Brexit referendum vote during the summer of 2016. Policy actions by the Bank of England have led to a slight appreciation in the pound through early 2018. Renewed capital flows to developing economies have sustained a slight appreciation in some currencies, including the Chinese renminbi and the South African rand. In addition, the Mexican peso continued to depreciate in international foreign markets, reflecting uncertainties over the potential impact of a renegotiation of NAFTA. Stronger economic performance and still low interest rates and low rates of price inflation have provided impetus for the U.S. Federal Reserve to strengthen monetary policy by raising interest rates in small steps. In addition, other major economies in Europe and Japan have attempted to pursue more expansionary monetary policies. Reduced levels of uncertainty in global financial markets have reduced upward pressure on the dollar, as investors have been less prone to seek safe haven currencies and dollar-denominated investments.

The Role of Congress in International Trade and Finance

The U.S. Constitution assigns authority over foreign trade to Congress. Article I, Section 8, of the Constitution gives Congress the power to "regulate Commerce with foreign Nations" and to "lay and collect Taxes, Duties, Imposts, and Excises." For roughly the first 150 years of the United States, Congress exercised its power to regulate foreign trade by setting tariff rates on all imported products. Congressional trade debates in the 19th century often pitted Members from northern manufacturing regions, who benefitted from high tariffs, against those from largely southern raw material exporting regions, who gained from and advocated for low tariffs.

A major shift in U.S. trade policy occurred after Congress passed the highly protective "Smoot-Hawley" Tariff Act of 1930, which significantly raised U.S. tariff levels and led U.S. trading partners to respond in kind. As a result, world trade declined rapidly, exacerbating the impact of the Great Depression. Since the passage of the Tariff Act of 1930, Congress has delegated certain trade authority to the executive branch. First, Congress enacted the Reciprocal Trade Agreements Act of 1934, which authorized the President to enter into reciprocal agreements to reduce tariffs within congressionally pre-approved levels, and to implement the new tariffs by proclamation without additional legislation. Congress renewed this authority periodically until the 1960s. Subsequently, Congress enacted the Trade Act of 1974, aimed at opening markets and establishing nondiscriminatory international trade norms for nontariff barriers as well. Because changes in nontariff barriers in reciprocal bilateral, regional, and multilateral trade agreements may involve amending U.S. law, the agreements require congressional approval and implementing legislation. Congress has renewed or amended the 1974 Act five times, which includes granting "fast-track" trade negotiating authority. Since 2002, "fast track" has been known as trade promotion authority (TPA). In 2015, Congress authorized new TPA, through 2021, provided the President requests an extension and Congress does not enact an extension disapproval resolution before July 1, 2018.

Congress also exercises trade policy authority through the enactment of laws authorizing trade programs and measures to address unfair and other trade practices. It also conducts oversight of the implementation of trade policies, programs, and agreements. These include such areas as U.S. trade agreement negotiations, tariffs and nontariff barriers, trade remedy laws, import and export policies, economic sanctions, and the trade policy functions of the federal government.

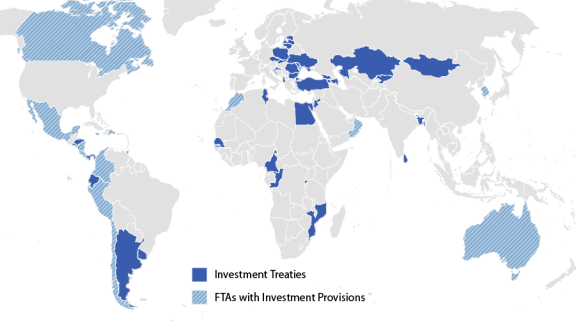

Additionally, Congress has an important role in international investment and finance policy. It has authority over bilateral investment treaties (BITs) through Senate ratification, and the level of U.S. financial commitments to the multilateral development banks (MDBs), including the World Bank, and to the International Monetary Fund (IMF). It also authorizes the activities of various agencies, such as the Export-Import Bank (Ex-Im Bank) and the Overseas Private Investment Corporation (OPIC). Congress also has oversight responsibilities over these institutions, as well as the Federal Reserve and the Department of the Treasury, whose activities affect international capital flows and short-term movements in the international exchange value of the dollar. Congress also closely monitors developments in international financial markets that could affect the U.S. economy.

Policy Issues for Congress

Trade Promotion Authority (TPA)6

Legislation to renew Trade Promotion Authority (TPA)—the Bipartisan Congressional Trade Priorities and Accountability Act of 2015 (P.L. 114-26)—was signed by President Obama on June 29, 2015, after months of debate and passage by both houses of Congress. TPA allows implementing bills for specific trade agreements to be considered under expedited legislative procedures ("fast track")—limited debate, no amendments, and an up or down vote—provided the President observes certain statutory obligations in negotiating trade agreements. These obligations include adhering to congressionally-defined U.S. trade policy negotiating objectives, as well as congressional notification and consultation requirements before, during, and after the completion of the negotiation process.

The primary purpose of TPA is to preserve the constitutional role of Congress with respect to consideration of implementing legislation for trade agreements that require changes in domestic law, which includes tariffs, while also bolstering the negotiating credibility of the executive branch by ensuring that trade agreements will not be changed once concluded. Since the authority was first enacted in the Trade Act of 1974, Congress has renewed or amended TPA five times (1979, 1984, 1988, 2002, and 2015). The latest grant of authority expires on July 1, 2021, provided that the President requests its extension by April 1, 2018, and neither chamber introduces and passes an extension disapproval resolution by July 1, 2018. If legislation is introduced in Congress in the future to implement the results of negotiations to renegotiate or modernize the North American Free Trade Agreement, it may be eligible to receive expedited consideration under TPA.

The World Trade Organization (WTO)7

The WTO is an international organization that administers the trade rules and agreements negotiated by its 164 participating members to eliminate barriers and create non-discriminatory rules and principles to govern trade. It also serves as a forum for dispute settlement resolution and trade liberalization negotiations. The United States was a major force behind the establishment of the WTO on January 1, 1995, and the new rules and trade liberalization agreements that occurred as a result of the Uruguay Round of multilateral trade negotiations (1986-1994). The WTO succeeded the General Agreement on Tariffs and Trade (GATT), which was established in 1947.

In contrast to its predecessors, the Trump Administration has taken a more skeptical stance toward the institution. While the Administration thus far has largely concentrated on perceived shortcomings of the WTO dispute settlement system (see below), past U.S. leadership was critical to supporting and advancing a forward-looking multilateral trading system.

The WTO's future as an effective multilateral trade negotiating organization for broad-based trade liberalization remains in question. The current deadlock in major on-going negotiations is largely due to differences between leading emerging-market economies, such as India, China and Brazil, developing economies, and advanced countries. Most developing countries want to continue to link the broad spectrum of agricultural and non-agricultural issues under the Doha Round and have been reluctant to lower their tariffs on industrial goods. They maintain that unless all issues are addressed in a single package, issues important to developing countries will be ignored. Conversely, developed economies have pushed for change in the negotiating dynamics, arguing that the WTO needs to address new issues, such as e-commerce and digital trade, especially given the growth of major emerging markets, and that advanced developing countries should make commercially meaningful new commitments on market access to their markets. WTO members have been working to achieve consensus on future work plans, but were unable to announce major deliverables or negotiated outcomes at the 11th Ministerial Conference in Buenos Aires, Argentina in December 2017. While many were disappointed by the lack of progress, in the view of the United States, the ministerial outcome signaled that "the impasse at the WTO was broken," paving the way for like-minded countries to pursue new work in other key areas.8

The most recent round of multilateral trade negotiations, the WTO Doha Round, began in November 2001, but concluded with no clear path forward after the 10th Ministerial Conference in December 2015, in Nairobi Kenya. The Nairobi Declaration, issued at the Ministerial, underscored the importance of a multilateral rules-based trading system with regional and plurilateral agreements as a complement to, not a substitute for, the multilateral forum. Work to build on the current WTO agreements outside of the specific Doha agenda continues, including through sectoral or plurilateral agreements, for example, on services (see textbox). At the more recent 11th Ministerial, separate groups of WTO members committed to new work programs or open-ended plurilateral talks on e-commerce, investment facilitation, and micro, and small and medium-sized enterprises. The United States signed on to the declaration in support of e-commerce.

|

Agreements and Negotiations WTO Trade Facilitation Agreement (TFA) WTO Information Technology Agreement (ITA) WTO Government Procurement Agreement (GPA) WTO Environmental Goods Agreement (EGA) WTO Fisheries Subsidy Agreement Trade in Services Agreement (TiSA) |

U.S. Bilateral and Regional Trade Agreements

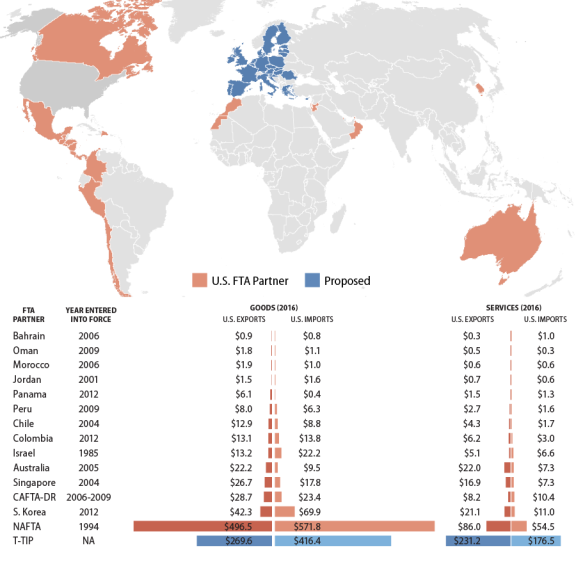

In addition to the WTO, the United States has worked to reduce and eliminate barriers to trade and create non-discriminatory rules and principles to govern trade through plurilateral, regional, and bilateral agreements. It has concluded 14 free trade agreements (FTAs) with 20 countries since 1985, when the first U.S. bilateral FTA was concluded with Israel (Figure 2).

The Trump Administration has signaled a shift on U.S. bilateral and regional trade agreements. President Trump withdrew the United States from the Trans-Pacific Partnership (TPP), an FTA negotiated during the Obama Administration between the United States and 11 other countries in the Asia-Pacific region. The Trump Administration has also initiated a renegotiation of the North American Free Trade Agreement (NAFTA), an FTA between the United States, Canada, and Mexico, as well as official talks to potentially modify the bilateral U.S.-South Korea (KORUS) FTA. The Trump Administration to date has not acted on other trade negotiations launched during the Obama Administration, including an FTA between the United States and the European Union (EU) on a potential Transatlantic Trade and Investment Partnership (T-TIP) and a potential Trade in Services Agreement (TiSA) with 23 WTO members. President Trump has expressed interest in negotiating bilateral trade agreements, including an FTA with the United Kingdom, Japan, and other TPP partners.

|

|

Source: Created by CRS using U.S. International Trade Commission and the Bureau of Economic Analysis data. |

|

U.S. Trade Agreement Basics

|

North American Free Trade Agreement (NAFTA) Renegotiation9

|

NAFTA Fast Facts

|

NAFTA, a comprehensive FTA among the United States, Canada, and Mexico, entered into force on January 1, 1994. NAFTA established trade liberalization commitments and set new rules and disciplines for future free trade agreements (FTAs) on issues important to the United States, including rules of origin, intellectual property rights (IPR), foreign investment, agriculture and services trade, dispute resolution, worker rights, and environmental protection. NAFTA's market-opening provisions gradually eliminated nearly all tariff and most nontariff barriers on goods produced and traded within North America. At the time of NAFTA, average applied U.S. duties on imports from Mexico were 2.07%, while U.S. producers faced average Mexican tariffs of 10%, in addition to nontariff and investment barriers in Mexico. The U.S.-Canada FTA had been in effect since 1989. Trade among NAFTA partners has tripled since the agreement entered into force, forming a more integrated North American market.

Many trade policy experts and economists give credit to NAFTA and other FTAs for expanding trade and economic linkages among countries, creating more efficient production processes, increasing the availability of lower-priced consumer goods, and improving living standards and working conditions. Other proponents contend that FTAs have political dimensions that create positive ties among member countries and improve democratic governance. However, some policymakers, labor groups and consumer advocacy groups argue that NAFTA has had a negative effect on the U.S. economy. They strongly oppose NAFTA and other FTAs, maintaining that trade agreements result in outsourcing, lower wages, and job dislocation.

The Trump Administration has made NAFTA renegotiation and modernization a prominent priority of its trade policy agenda. President Trump has viewed the agreement as the "worst trade deal," and has stated that he may seek to withdraw from the agreement. He has focused on the trade deficit with Mexico as a major reason for his critique. In May 2017, the Trump Administration sent a 90-day notification to Congress of its intent to begin talks to renegotiate NAFTA, as required by the 2015 Trade Promotion Authority (TPA) (P.L. 114-26), and negotiations started in August 2017. Negotiators were initially committed to concluding negotiations by the end of 2017 or early 2018. After a contentious fourth round of talks in October 2017, negotiators agreed to extend their timeline with a possible conclusion date in the spring of 2018 at the earliest. Subsequent rounds of negotiations have also remained contentious.

NAFTA is 24 years old and renegotiation provides parties opportunities to address issues not covered in the original text. Technology and industrial production processes have changed significantly and the widespread use of the internet has significantly affected economic activities and the use of e-commerce. A modernization could incorporate elements of more recent U.S. FTAs, such as provisions to address digital and newer services trade barriers and enhanced IPR protection. Many U.S. manufacturers, services providers, and agricultural producers oppose efforts to eliminate NAFTA and ask that the Trump Administration strive to "do no harm" in the negotiations because they have much to lose if the United States pulls out of the agreement. Other groups contend that NAFTA should be rewritten to include stronger and more enforceable labor protections, provisions on currency manipulation, and stricter rules of origin. Reported issues of contention in the negotiations include U.S. proposals for stronger rules of origin in the auto sector, a "sunset clause" in which NAFTA parties would re-evaluate the agreement every five years, modified dispute resolution provisions, and changes to government procurement provisions.

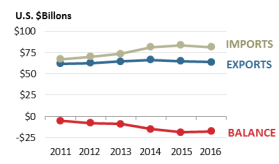

U.S.-South Korea (KORUS) FTA Modifications10

The U.S.-South Korea (KORUS) FTA has been the centerpiece of U.S.-South Korea economic relations since its entry into force in March 2012. KORUS was signed in 2007, but implementing legislation was not passed by Congress until 2011 after the United States exchanged side letters with the South Korean government effectively changing certain commitments on auto and agricultural trade in the original agreement. Like all U.S. FTAs, the agreement will eventually eliminate nearly all tariffs (over 99% of tariff lines) on imports into both countries. As one of the most recent U.S. FTAs in effect, it arguably includes the most extensive commitments on nontariff issues ranging from intellectual property rights (IPR) to labor and environmental protections.

|

|

Source: Data from Bureau of Economic Analysis. |

Trade between the two countries has grown modestly since the FTA's entry into force, but U.S. imports have risen faster than U.S. exports, leading to an increase in the bilateral trade deficit with South Korea (Figure 3). Given the myriad factors affecting trade flows, most economists argue that overall trade balances are a poor measure of the success of trade agreements, noting that other variables, including a slowdown in South Korea's economic growth during the period, were likely the key drivers of the trade deficit increase. Investment between the two countries also surged between 2011 and 2016.

Views on the KORUS FTA are mixed. Proponents argue it led to increased consumer choice, improved South Korea's regulatory process, and further opened markets for U.S. goods and services. Critics assert it has had negative effects on U.S. employment opportunities in industries competing with South Korean imports. Although the business community broadly supports the agreement, it has raised concerns with South Korea's implementation of certain commitments.

The Trump Administration has criticized the KORUS FTA, citing the growth in the U.S. trade deficit with South Korea. The Administration requested consultations with the South Korean government in August 2017 to address its concerns with the FTA. The two sides agreed to formal talks to potentially modify the pact, the first of which was held January 5, 2018. It is unclear what specific commitments the Trump Administration seeks to modify as it has neither notified Congress of its intent to negotiate nor provided negotiating objectives for the talks.

|

Trans-Pacific Partnership (TPP)11

In January 2017, President Trump withdrew the United States from the Trans-Pacific Partnership (TPP). The TPP was a proposed free trade agreement (FTA) among 12 countries in the Asia-Pacific region, including the United States. The Obama Administration cast TPP as a comprehensive and high standard agreement with economic and strategic significance for the United States. Some U.S. stakeholders argue the TPP withdrawal, coupled with ongoing FTA negotiations that do not involve the United States, may negatively affect U.S. export competitiveness and leadership in establishing new trade disciplines in Asia. Others in the United States supported the President's withdrawal, viewing certain TPP nontariff commitments as infringing on U.S. sovereignty and raising concerns that reduced import tariffs would negatively affect U.S. employment in import competing industries. The Trump Administration has expressed interest in negotiating bilateral FTAs with Japan and other TPP parties with which the United States does not already have FTAs.

The remaining 11 parties are moving forward to ratify the TPP without U.S. participation. In January 2018, the group announced the conclusion of negotiations on a new agreement—the Comprehensive and Progressive Agreement for Trans-Pacific Partnership (CPTPP)—expected to be signed in early March. U.S. withdrawal required certain modifications to the text, both logistically and as a result of a change in some countries' calculus on the appropriate balance of concessions given the withdrawal of the original pact's largest market. The 11 countries have agreed to maintain the vast majority of the original TPP text, however, including each country's market access commitments (i.e., tariff reduction schedules). Some provisions pushed by the United States, mostly on intellectual property rights and investment, have been suspended. The economic significance of a CPTPP agreement would be smaller without U.S. participation. However, it would provide those countries liberalized trade with Japan, the world's third largest economy. Japan is leading the CPTPP process.

The Regional Comprehensive Economic Partnership (RCEP), an Association of South-East Asian Nations (ASEAN)-led negotiation, may also take on increased significance in the wake of U.S. withdrawal from TPP. RCEP encompasses ASEAN members (Brunei, Cambodia, Indonesia, Laos, Malaysia, Myanmar, Philippines, Singapore, Thailand, and Vietnam), as well as China, Japan, South Korea, Australia, India, and New Zealand, but not the United States. The remaining TPP countries may also seek to solidify their trading relationship with China, whether within RCEP or bilaterally, as China is the largest trading partner for most TPP countries.

Transatlantic Trade and Investment Partnership (T-TIP)12

|

T-TIP Fast Facts Date negotiations started: 7/8/2013. Number of negotiating rounds: 15 rounds through October 2016 under the Obama Administration. Status: Negotiations currently inactive under the Trump Administration. U.S.-EU goods and services trade in 2016: $1.1 trillion (22% of U.S. global trade). U.S.-EU investment in 2016: $5.2 trillion (57% of U.S. world investment stock on historical-cost basis). Note: Data for EU-28, including the UK. |

The Transatlantic Trade and Investment Partnership (T-TIP) is a potential "comprehensive and high-standard" free trade agreement (FTA) between the United States and the European Union (EU). These economies are each other's largest overall trade and investment partner. T-TIP aims to liberalize U.S.-EU trade and investment and address tariff and nontariff barriers on goods, services, and agriculture. It also aims to set globally relevant rules and disciplines to support economic growth and multilateral trade liberalization. T-TIP negotiations began in 2013. With the 15th and latest negotiating round in October 2016, the two sides had consolidated texts in many areas. Yet, they face unresolved complex and sensitive issues on numerous fronts, raising questions about whether sufficient political momentum exists to overcome differences. Presently, negotiations are inactive as both sides evaluate T-TIP's status.13

In the EU, the UK withdrawal process (Brexit) adds complexity to T-TIP's prospects. Public opposition to T-TIP in the EU due to concerns over genetically modified organisms (GMOs), investor-state dispute settlement (ISDS), and data privacy has also added uncertainty, as have U.S. attempts to tighten Buy American policies. Some in the EU Parliament and European Commission (EC) are reportedly calling for a tougher EU approach against the Trump Administration's "America First" policies.14

On the U.S. side, T-TIP's outlook is also uncertain. Support for T-TIP remains high among some Members of Congress, yet trade remains a controversial issue. The Trump Administration is reportedly evaluating the status of T-TIP. U.S. Trade Representative (USTR) Lighthizer recently commented on the importance and size of the U.S.-EU trade relationship. According to press reporting of the 2018 World Economic Forum, Secretary of Commerce Wilbur Ross said that it was no accident that the United States withdrew from the TPP but not the T-TIP negotiations, while EC Trade Commissioner Cecelia Malmström noted that there are "lots of trade irritants" between the United States and the EU and that "parameters have changed" for the T-TIP negotiations.15

If T-TIP negotiations resume, potential issues for Congress include the level of priority both sides place on T-TIP, given the U.S. renegotiation of NAFTA and the EU's trade negotiations with other countries, and the shape of the future agreement on controversial issues. If T-TIP negotiations stall indefinitely or terminate, Congress may examine other ways to enhance U.S.-EU trade relations.

Brexit and a Potential U.S.-UK Free Trade Agreement (FTA)16

In June 2016, the United Kingdom (UK) voted in favor of exiting the EU ("Brexit"), presenting issues about transatlantic trade relations. Trade is equivalent to about 60% of the UK economy, in large part due to reduced trade barriers through the EU's Single Market. At $2.7 trillion, the UK was the EU's second largest economy behind Germany and accounted for about 16% of EU GDP in 2016.17 Brexit confronts U.S. firms operating in the UK and benefiting from the UK's access to the Single Market with economic and financial uncertainties. The UK is a key U.S. trade and investment partner, and Brexit's impact on U.S.-UK trade relations depends on a number of variables, including the UK's negotiated terms of withdrawal from the EU, the UK's future trade relationship with the EU, and any redefinition of UK and EU terms of trade in the WTO.

|

U.S.-UK Trade Fast Facts

|

Following the Brexit referendum, some Members of Congress and the Trump Administration called for launching U.S.-UK FTA negotiations, though some Members have moderated their support with calls to ensure that such negotiations do not constrain promoting broader transatlantic trade relations. On January 27, 2017, President Trump and Prime Minister May discussed how the two sides could "lay the groundwork" for a future U.S.-UK FTA.18 In July 2017, the two sides launched a U.S.-UK Trade and Investment Working Group to explore a possible post-Brexit FTA. However, the UK cannot negotiate new trade agreements with other countries until it leaves the EU. Some experts view a potential U.S.-UK FTA as more politically feasible than other U.S. FTAs, given similarities in U.S. and UK trade policy approaches and the two countries' "special relationship;" others caution that, even among like-minded trading partners, domestic political interests can complicate trade negotiations.

Brexit raises questions about other aspects of U.S. trade policy as well. Some argue that Brexit could complicate the T-TIP negotiations, if resumed, given the UK's traditionally liberalizing role in the EU. Others say that a potential U.S.-UK FTA could add pressure to advance any further T-TIP negotiations. The UK's future status also could affect other U.S. trade policy interests, such as the Trade in Services Agreement (TiSA) negotiations (see below).

Trade in International Services Agreement (TiSA)19

TiSA is a potential agreement that would liberalize trade in services among its signatories. The term "services" refers to an expanding range of economic activities, such as construction, retail and wholesale sales, e-commerce, financial services, professional services (e.g., accounting and legal services), logistics, transportation, tourism, and telecommunications. The impetus for TiSA comes from the lack of progress in the WTO Doha Round on services trade liberalization. A subset of WTO members, led by the United States and Australia, launched informal discussions in early 2012 to explore negotiating a separate agreement focused on trade in services. The United States and the 22 other TiSA participants account for more than 70% of global trade in services.

|

TiSA Fast Facts

|

Negotiations began in April 2013, and 21 rounds of negotiations took place through 2016. The Trump Administration has not stated an official position on TiSA, and no negotiations were held in 2017. Negotiations on services present unique trade policy issues, such as how to construct trade rules that are applicable across a wide range of varied economic activities. The General Agreement on Trade in Services (GATS) under the WTO is the only multilateral set of rules on trade in services. GATS came into effect in 1995, and many policy experts have argued that the GATS should be updated and expanded if it is to liberalize services trade effectively.

The TiSA negotiations are of congressional interest given the significance of the services sector in the U.S. economy and TiSA's potential impact on domestic services industries seeking to expand internationally. Services account for almost 78% of U.S. gross domestic product (GDP) and for over 82% of U.S. private sector employment.20

U.S.-China Commercial Relations21

Since China embarked upon economic and trade liberalization in 1979, U.S.-Chinese economic ties have grown extensively. Total bilateral trade rose from about $2 billion in 1979 to $636 billion in 2017. China was the United States' largest trading partner, largest source of imports ($506 billion), and third largest merchandise export market ($130 billion).22 The U.S. merchandise trade deficit with China was $375 billion (up 8.1% over 2016 levels), by far the largest U.S. bilateral trade imbalance.

From 2008 to 2017, U.S. merchandise exports to China grew by 82.4%, the second fastest growth rate among the top 10 U.S. export markets in 2017 (after Hong Kong). The U.S.-China Business Council estimates that China is a $400 billion market for U.S. firms when U.S. exports of goods and services to China plus sales by U.S-invested firms in China are counted.23 China's large population, vast infrastructure needs, and rising middle class could make it an even more significant market for U.S. businesses, provided that new economic reforms are implemented and trade and investment barriers are lowered. According to the Rhodium Group, annual Chinese foreign direct investment (FDI) in the United States rose from $4.6 billion in 2010 to $46.2 billion in 2016.24 China is important to the global supply chain for many U.S. companies, some of which use China as a final point of assembly for their products. Low-cost imports from China help keep U.S. inflation low. As the world's largest economy and trading country, China's economic conditions and policies have a major impact on the U.S. and global economy, and thus have been of interest to Congress.

|

China's Economic Rise:

|

Despite growing U.S.-Chinese commercial ties, the bilateral relationship is complex and at times contentious. From the U.S. perspective, many trade tensions stem from China's incomplete transition to an open-market economy. While China has significantly liberalized its economic and trade regimes over the past three decades—especially since joining the World Trade Organization (WTO) in 2001—it continues to maintain (or has recently imposed) a number of policies that appear to distort trade and FDI flows, which, some policymakers argue, often undermine U.S. economic interests and cause U.S. job losses in some sectors. A 2018 American Chamber in China (AmCham China) business climate survey of its member companies found that while a majority of respondents felt optimistic about their investments in China, 81% said that foreign businesses in China were "less welcomed" in China than before, compared to 44% who felt that way in 2014.25

The United States has initiated more WTO dispute settlement cases (21 cases through February 15, 2018, though none so far by the Trump Administration) against China than any other WTO member. China has brought 12 WTO dispute settlement cases against the United States. In December 2016, it brought a WTO case over U.S. treatment of China as a non-market economy (NME) for the purposes of applying anti-dumping measures.26 In addition, on February 6, 2018, China initiated WTO cases against the United States over safeguard measures on imported washing machines and solar cells.

|

China-U.S. FDI U.S.-China FDI flows are relatively small given the high level of bilateral trade, although estimates of such flows differ. The Rhodium Group (RG), a private advisory firm, estimates the stock of China's FDI in the United States through 2015 at $62.9 billion and the stock of U.S. FDI in China at $227.9 billion. RG also estimated that annual Chinese FDI flows to the United States rose from $7.5 billion in 2012 to $15.3 billion in 2015, and that 2016 FDI flows were nearly triple 2015 levels, at $45.6 billion. Some Members of Congress have raised concerns that some Chinese FDI activities may threaten to harm U.S. economic security and the competitiveness of some industries, and have proposed revising the criteria of how the federal government reviews such investment. The United States has pressed China to reduce FDI restrictions and barriers, including through negotiations for a bilateral investment treaty (BIT). In 2013, China agreed that the BIT would include Chinese commitments to open up various sectors to FDI, based on a "negative list" basis—meaning only sectors specifically listed in the final agreement would be barred from FDI. A BIT was not concluded by the end President Obama's term and the Trump Administration has not indicated if it intends to restart BIT negotiations with China. |

Industrial Policies and State Capitalism

The Chinese government continues to play a major role in economic decision-making. For example, at the macroeconomic level, the Chinese government maintains policies that induce households to save a high level of their income, much of which is deposited in state-controlled Chinese banks. This enables the government to provide low-cost financing to Chinese firms, especially state-owned enterprises (SOEs) which dominate several economic sectors in China. Fortune's 2016 Global 500 list of the world's largest companies included 103 Chinese firms, 75 of which were classified as being 50% or more owned by the Chinese government.27 At the microeconomic level, the Chinese government (at the central and local government level) seeks to promote the development of industries deemed critical to the country's future economic development by using various means, such as subsidies, preferential loans, tax exemptions, and access to low-cost land and energy. Many analysts contend that such distortionary policies contribute to overcapacity in several Chinese industrial sectors, such as steel and aluminum. Additionally, the Chinese government imposes numerous restrictions on foreign firms seeking to do business in China, such as discriminatory regulations and standards, uneven enforcement of commercial laws (such as its anti-monopoly laws), FDI barriers and mandates, export restrictions on raw materials, technology transfer requirements imposed on foreign firms, and public procurement rules that give preferences to domestic Chinese firms.

The Chinese government has outlined a number of policies to promote China's transition from a manufacturing center to a major global source of innovation and reducing the country's dependence on foreign technology by promoting "indigenous innovation" and a 2025 "Made in China" plan. In recent years, the Chinese government has proposed new regulations for banking and insurance, which, under the pretext of protecting national security, appear to impose new restrictions against foreign providers of information and communications products (ICT) and services.

Intellectual Property Rights (IPR) Protection and Cyber-Theft

American firms cite the lack of effective and consistent protection and enforcement in China of U.S. IPR as one of the largest challenges they face in doing business in China. Although China has significantly improved its IPR protection regime over the past few years, many U.S. industry officials view piracy rates in China as unacceptably high. While AmCham China's 2017 business survey found that 95% of respondents felt that IPR enforcement had improved over the past five years, 66% said the IPR enforcement of trade secrets was ineffective and 52% said protection of trademarks and brands was ineffective. The USTR's 2016 report on foreign trade barriers stated that over the past decade, China's internet restrictions have "posed a significant burden to foreign suppliers," and that eight out of the top 25 most globally visited sites (such as Yahoo, Facebook, YouTube, eBay, Twitter and Amazon) are blocked in China.28 Cyberattacks by Chinese entities against U.S. firms have raised concerns over the potential theft of U.S. IPR, especially trade secrets. According to the U.S. Customs and Border Protection China (including Hong Kong) accounted for 88% of the $1.4 billion in counterfeit goods seized by in FY2016.29

On April 1, 2015, President Obama issued an executive order authorizing certain sanctions against "persons engaging in significant malicious cyber-enabled activities." Shortly before Chinese President Xi's state visit to the United States in September 2015, some press reports indicated that the Obama Administration was considering imposing sanctions against Chinese entities over cyber-theft. After high-level talks between Chinese and U.S. officials on cybersecurity, President Obama and President Xi announced in September 2016 that they reached an agreement. The agreement stated that neither country's government will conduct or knowingly support cyber-enabled theft of intellectual property, including trade secrets or other confidential business information, with the intent of providing competitive advantages to companies or commercial sectors. They also agreed to set up a high-level dialogue mechanism to address cybercrime and to improve two-way communication when cyber-related concerns arise. The U.S.-China High-Level Joint Dialogue on Cybercrime and Related Issues met in December 2015 and June 2016, although it is unclear if the dialogue has produce concrete results.

The Trump Administration's Approach

At their first official meeting as heads of state in April 2017, President Trump and Chinese President Xi Jinping announced the establishment of a "100-day plan on trade" as well as a new high-level forum called the "U.S.-China Comprehensive Economic Dialogue" (CED). In May 2017, the two sides announced that China would open its markets to U.S. beef, biotechnology products, credit rating services, electronic payment services, and bond underwriting and settlement. The United States agreed to open its markets to Chinese cooked poultry and welcomed Chinese purchases of U.S. liquefied natural gas. Chinese officials also indicated their support for continuing the BIT negotiations, although the Trump Administration did not indicate its position. Following the meeting, President Trump in a series of tweets appeared to indicate that he would link U.S. trade policy towards China with China's willingness to pressure North Korea to curb its nuclear and missile programs.

In July 2017, the two sides held the first session of the CED in Washington, DC, which sought to build on the 100-day action plan through a new one-year action plan on trade and investment, seeking to achieve a more balanced economic relationship. The outcome of the meeting is unclear as, unlike past high-level meetings, no joint fact sheet was released. The U.S. side issued a short statement that said that "China acknowledged our shared objective to reduce the trade deficit which both sides will work cooperatively to achieve," which led some U.S. observers to claim that the CED was marred with high tensions and disagreements. China issued a four-page document on the "positive outcomes" of the CED, including the broad outline of a one-year plan covering broad economic and trade topics.30 The document also stated that the two sides discussed trade in services, steel, aluminum, and high technology.

In August 2017, the Trump Administration announced it would launch a Section 301 investigation into China's protection of U.S. IPR and forced technology transfer policies (see textbox). The Section 301 case against China could have significant implications for bilateral commercial ties, especially if the case is pursued unilaterally and not through the WTO dispute settlement process and if trade sanctions against China are ultimately imposed.

|

Section 301 Sections 301 of the Trade Act of 1974, as amended, is one of the principal statutory means by which the United States enforces U.S. rights under trade agreements and addresses "unfair" foreign barriers to U.S. exports. Section 301 procedures apply to foreign acts, policies, and practices that the USTR determines either (1) violates, or is inconsistent with, a trade agreement; or (2) is unjustifiable and burdens or restricts U.S. commerce. The measure sets procedures and timetables for actions based on the type of trade barrier(s) addressed. Section 301 cases can be initiated as a result of a petition filed by an interested party with the USTR or self-initiated by the USTR. Once the USTR begins a Section 301 investigation, it must seek a negotiated settlement with the foreign country concerned, either through compensation or an elimination of the particular barrier or practice. For cases involving trade agreements, such as those under the Uruguay Round (UR) agreements in the WTO, the USTR is required to utilize the formal dispute proceedings specified by the agreement. |

During President Trump's visit to China in November 2017, the U.S. Commerce Department announced it had facilitated $250 billion in deals between private U.S. businesses and Chinese entities. However, many analysts argued that some of the deals were already in the making, while others were non-binding. In remarks made at an event with Chinese President Xi, Trump stated that he was trying to make U.S.-China commercial ties "fair and reciprocal," noting China's trade barriers and IPR practices, which he cited as causes of the large U.S. trade deficit with China.

Overall, however, the Trump Administration appears to be taking a harder line against China on trade issues. Looking ahead, the executive order requiring the U.S. Department of Commerce and USTR to submit an Omnibus Report on Significant Trade Deficits will likely heavily focus on China. The Administration's Section 232 investigations on steel and aluminum imports (see below) are leading to the imposition of import restrictions against China. Finally, the Administration has made the enforcement and application U.S. anti-dumping and countervailing measures (where Chinese imports have been the largest target) a major priority. When President Trump announced and signed his Presidential Memorandum on China's IPR policies on August 14, he said that "this is only the beginning."

Some analysts argue that the Trump Administration's "America First" economic policies (such as the U.S. withdrawal from TPP) could undermine U.S. global leadership and weaken its ability to push China toward liberalizing its economy. The Office of the Director of National Intelligence stated in its 2018 World Threat Assessment report that "China and Russia will seek spheres of influence and check U.S. appeal and in their regions. Meanwhile, US allies' and partners' uncertainty about the willingness and capability of the United States to maintain its international commitments may drive them to consider reorienting their policies, particularly regarding trade, away from Washington."31

Economic Effects of Trade

Trade and trade agreements have wide-ranging effects on the economy, including on economic growth, the distribution of income, and employment gains or losses. For most economists, liberalized trade results in both economic costs and benefits, but they argue the long-run net effect on the economy as a whole is positive. It is argued that the economy as a whole operates more efficiently and grows more rapidly as a result of competition through international trade and investment, and consumers benefit by having available a wider variety of goods and services at varying levels of quality and price than would be possible in an economy closed to international trade. Trade also can have long-term positive dynamic effects on an economy and enhances production and employment. However, the costs and benefits associated with expanding trade and trade agreements do not accrue to the economy at the same speed; costs to the economy in the form of job and firm losses are felt especially in the initial stages of the agreement, while benefits to the economy accrue over time. According to the World Bank, liberalizing trade and foreign investment have reduced the number of people in the world living in extreme poverty (under $1 per day) by half, or 600 million, over the past 25 years, transforming the global economy.32

Trade and U.S. Jobs33

Trade is one among a number of forces that drive changes in employment, wages, the distribution of income, and ultimately the U.S. standard of living. Most economists argue that macroeconomic forces within an economy, including technological and demographic changes, are the dominant factors that shape trade and foreign investment relationships and complicate efforts to disentangle the distinct impact that trade has on the economy. Various measures are used to estimate the role and impact of trade in the economy and of trade on employment. One measure developed by the Department of Commerce concludes that exports support, directly and indirectly, 11.7 million jobs in the U.S. economy.34 According to these estimates, jobs associated with international trade, especially jobs in export-intensive manufacturing industries, earn 18% more on a weighted average basis than comparable jobs in other manufacturing industries.35

More open markets globally and other changes have subjected a larger portion of the domestic workforce to international competition. According to the International Monetary Fund (IMF), the effective global labor market quadrupled over the past two decades through the opening of China, India, and the former East European bloc countries.36 Standard economic theory recognizes that some workers and producers in the economy may experience a disproportionate share of the short-term adjustment costs as a result of such economic transformations. Although difficult to measure, some estimates suggest that adjustment costs may be significant over the short-run and can entail dislocations for some segments of the labor force, some companies, and some communities. Closed plants can result in depressed commercial and residential property values and lost tax revenues, with effects on local schools, local public infrastructure, and local community viability.37

In a dynamic economy like that of the United States, jobs are constantly being created and replaced as some economic activities expand, while others contract. As part of this process, various industries and sectors evolve at different speeds, reflecting differences in technological advancement, productivity, and efficiency. Those sectors that are the most successful in developing or incorporating new technological advancements usually generate greater economic rewards and are capable of attracting larger amounts of capital and labor. In contrast, those sectors or individual firms that lag behind generally attract less capital and labor and confront ever-increasing competitive challenges. In addition, advances in communications, transportation, and technology have facilitated a global transformation of economic production into sophisticated supply chains that span national borders, defy traditional concepts of trade, and effectively increase the number of firms and workers participating in the global economy.

Trade and trade liberalization can have a differential effect on workers and firms in the same industry. Some estimates indicate that the short-run costs to workers who attempt to switch occupations or switch industries in search of new employment opportunities may experience substantial effects. One study concluded that workers who switched jobs as a result of trade liberalization generally experienced a reduction in their wages, particularly in occupations where workers performed routine tasks.38 These negative income effects were especially pronounced in occupations exposed to imports from low-income countries. In contrast, occupations associated with exports experienced a positive relationship between rising incomes and growth in export shares. As a result of the differing impact of trade liberalization on workers and firms, some governments have adopted special safeguards and worker retraining and other social safety net policies to mitigate the potential adverse effects of trade liberalization or address certain trade practices that may cause or threaten to cause injury.

Trade Adjustment Assistance (TAA)39

Trade Adjustment Assistance (TAA) is a group of programs that provide federal assistance to parties that have been adversely affected by foreign trade. Reduced barriers to trade can offer domestic benefits, including increased consumer choice and new export markets, but trade can also have negative effects among domestic industries that face increased competition. TAA aims to mitigate some of these negative domestic effects. TAA programs are authorized by the Trade Act of 1974, as amended, and were last reauthorized by the Trade Adjustment Assistance Reauthorization Act of 2015 (TAARA; Title IV of P.L. 114-27).

The largest TAA program, TAA for Workers (TAAW), provides federal assistance to workers who have been separated from their jobs because of increases in directly competitive imports or because their jobs moved to a foreign country. The largest components of the TAAW program are (1) funding for career services and training to prepare workers for new occupations and (2) income support for workers who are enrolled in an eligible training program and have exhausted their unemployment compensation. The TAAW program is administered at the federal level by the Department of Labor and FY2017 appropriations were $849 million.

TAA programs are also authorized for firms and farmers that have been adversely affected by international competition. TAA for Firms supports trade-impacted businesses by providing technical assistance in developing business recovery plans and by providing matching funds to implement those plans. TAA for Firms is administered by the Department of Commerce and the FY2017 appropriation was $13 million. The TAA for Farmers program was reauthorized by TAARA, but the program has not received an appropriation since FY2011.

Intellectual Property Rights (IPR)40

Intellectual property (IP) is a creation of the mind that may be embodied in physical and non-physical (including digital) objects. IPR are legal, private, enforceable rights that governments grant to inventors and artists that generally provide time-limited monopolies to right holders to use, commercialize, and market their creations and prevent others from doing the same without their permission.

IP is a source of comparative advantage of the United States, and IPR infringement has adverse consequences for U.S. commercial, health, safety, and security interests. Protection and enforcement of IPR in the digital environment is of increasing concern, including cyber-theft. At the same time, lawful limitations to IPR, such as exceptions in copyright law for media, research, and teaching (known as "fair use"), also may have benefits.

|

Examples of IPR Patents protect new innovations and inventions, such as pharmaceutical products, chemical processes, new business technologies, and computer software. Copyrights protect artistic and literary works, such as books, music, and movies. Trademarks protect distinctive commercial names, marks, and symbols. Trade secrets protect confidential business information that is commercially valuable because it is secret, including formulas, manufacturing techniques, and customer lists. Geographical indications (GIs) protect distinctive products from a certain region, applying primarily to agricultural products. |

IPR in Trade Agreements & Negotiations

IPR protection and enforcement has been a long-standing objective in U.S. trade agreement negotiations. The United States generally seeks IP commitments that exceed the minimum standards of the World Trade Organization (WTO) Agreement on Trade-Related Aspects of Intellectual Property Rights (TRIPS Agreement), known as "TRIPS-plus." The 2015 Trade Promotion Authority (TPA) incorporated past trade negotiating objectives to ensure that U.S. free trade agreements (FTAs) "reflect a standard of protection similar to that found in U.S. law" ("TRIPS-plus") and to apply existing IPR protection to digital media through adhering to the World Intellectual Property Organization (WIPO) "Internet Treaties." The TPA also contained new objectives on addressing cyber-theft and protecting trade secrets and proprietary information.

Treatment of IPR may be a key issue in the NAFTA renegotiations.41 Updated or new provisions may include enhanced provisions on pharmaceutical patent protections, copyright protections, trademark protection, disciplines for geographic indicators (GIs), and enforcement measures, as well as new provisions on data exclusivity periods for biologics and criminal penalties for cyber-theft of trade secrets found in more recent U.S. FTAs.

Congress could examine whether the IPR outcomes in a possible revised NAFTA outcome are consistent with U.S. trade negotiating objectives in TPA. Additionally, U.S. government actions to enforce foreign trading partners' IPR obligations within the WTO and under existing U.S. FTAs could intensify. Possible oversight issues for Congress include approaches to, as well as prioritization of, potential future U.S. trade enforcement actions in the IPR context.

Other IPR Trade Policy Tools

The United States maintains other trade policy tools to advance IPR goals, including the "Special 301" and "Section 337." These tools may be particularly relevant in addressing U.S. issues with respect to emerging economies, such as China, India, and Brazil, which present significant IPR challenges but are not a part of existing U.S. trade agreements or negotiations. Additionally, with President Trump's expressed intent to focus on trade enforcement, such tools may take on greater prominence.

Special 301. The United States Trade Representative (USTR) publishes annually a "Special 301" report, pursuant to the Trade Act of 1974, as amended. This report identifies countries that do not offer "adequate and effective" IPR protection, for example for patents and copyrights, and designates them on various "watch lists." If the USTR designates a country as a Special 301 "Priority Foreign Country," a category reserved for the most egregious IPR offenders, the country could be subject to an investigation under Section 301 of the Trade Act of 1974, as amended; this could result in trade enforcement action. Reflecting the evolution of IPR issues, the Trade Facilitation and Trade Enforcement Act of 2015 (P.L. 114-125) required USTR to identify issues in countries' protection of trade secrets in the "Special 301" report. China has been a top country of concern, and continues to be identified on the Special 301 "Priority Watch List" (among other countries, such as India). While not designating China as a "Priority Foreign Country," in August 2018, USTR initiated a Section 301 investigation of China's IPR practices under separate authority in the Section 301 statute (see China section).