The Economic Effects of Trade: Overview and Policy Challenges

During the Obama Administration, the United States negotiated two comprehensive and high-standard mega-regional free trade agreements: the Trans-Pacific Partnership (TPP) among the United States and 11 other countries, and the U.S.-European Transatlantic Trade and Investment Partnership (T-TIP). The 12 TPP countries signed the agreement in February 2016, but the agreement required ratification by each country before it could enter into force. In the United States this requires implementing legislation by Congress. Upon taking office, President Trump withdrew the United States from the TPP and halted further negotiations on the T-TIP, but may reengage in the TPP under different terms. The remaining 11 partners to the TPP concluded, without U.S. participation, a revised TPP, now identified as the Comprehensive and Progressive Agreement for Trans-Pacific Partnership (CPTPP). The Trump Administration is also attempting to revise the two largest existing U.S. FTAs, through the ongoing renegotiation of the North American Free Trade Agreement (NAFTA), and modification talks regarding the U.S.-South Korea (KORUS) FTA. For Members of Congress and others, international trade and trade agreements offer the prospect of improving national economic welfare, while also raising questions about the potential cost to the economy. Congress plays an important role in shaping and considering legislation to implement U.S. trade agreements.

Discussions of trade and trade agreements often focus on a number of issues, including the role that trade plays in the U.S. economy, the impact of trade agreements on employment gains and losses, and the size of the U.S. trade deficit. This report focuses on some of the major issues associated with trade and trade agreements and the impact of trade on the U.S. economy. The key findings include the following:

From the perspective of the U.S. economy as a whole, trade is one among a number of forces that drive changes in employment, wages, the distribution of income, and ultimately the standard of living. Most economists argue that broad macroeconomic forces, including technological advances, are generally considered to be more important than trade.

Economists generally conclude that trade provides net overall positive benefits to economies. Changes in trading patterns associated with changes in trading partners and composition or with new trade agreements, however, may entail certain adjustment costs, including changes in employment, which can be highly concentrated with some workers, firms, and communities affected disproportionately.

In discussions of trade agreements, both proponents and opponents use the results of a variety of trade models and underlying assumptions to estimate the impact on the U.S. economy. Such models have various strengths and weaknesses, although not always in equal proportion. Most economists argue that such estimates represent a partial accounting of the total economic effects and, therefore, are not representative of the overall impact of trade agreements on the U.S. economy.

Some argue that trade, trade agreements, and globalization more broadly contributed to growing wealth and income equality within countries. Growing income inequality domestically is not unique to the United States, or even to developed countries, but is found in both developed and developing countries. Despite intense focus in the academic literature, there is no consensus on the direct impact that trade or trade agreements have on income inequality.

Congress faces a number of challenging policy issues relative to trade and the impact of trade agreements on the U.S. economy. These challenges include assessing the quality of data on trade and what, if any, additional resources should be devoted to collecting trade data and analyzing the role of trade in the economy. Congress also has legislative and oversight responsibility over various government programs that assist workers and firms adjust to increased competition from trade.

The Economic Effects of Trade: Overview and Policy Challenges

Jump to Main Text of Report

Contents

- Introduction

- Background

- Trade and Employment

- Job Churning

- Worker Dislocation

- U.S. Trade With China

- Adjustment Policies

- U.S. Jobs Supported by Exports

- Goods and Services Jobs Supported by Exports

- Earnings for Workers in Jobs Supported by Exports

- Industry Distribution of Jobs Supported by Exports

- Jobs Supported by State Exports

- U.S. Jobs, Exports, and Trade Deficits

- ITA Clarification and Disclaimer

- Trade Agreements and Employment Estimates

- Trade Models

- Other Domestic Effects of Trade

- General Assumptions and Limitations of Trade Models

- General Assumptions

- Full Employment Assumption

- Consumer Indifference Assumption

- Differences in Firm Behavior

- Trade Creation and Trade Diversion

- Other Complications

- Value Chains

- Macroeconomic Relationships

- Unemployment and Trade Deficits

- Savings and Investment Balance

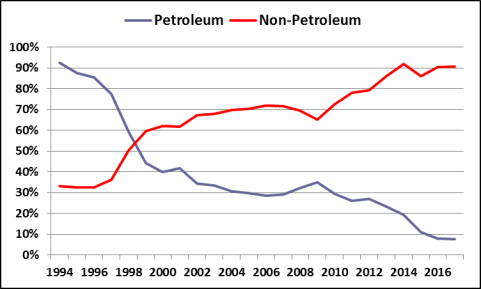

- Oil Prices and the Trade Deficit

- Capital Inflows and the U.S. Economy

- Foreign Investment and Outsourcing

- International Trade and Income Inequality

- International Trade Theory and Income Distribution

- OECD Analyses of Trade Liberalization and Income Inequality

- Issues for Congress

Figures

- Figure 1. Employment and Real Output in the U.S. Manufacturing Sector, 1980-2017

- Figure 2. Estimated Number of Jobs Supported by Exports in the Goods and Services Sectors in the U.S. Economy, 1993-2016

- Figure 3. Estimated Export Earnings Premium by Industry for Blue Collar and White Collar Workers, 2013

- Figure 4. Estimated Distribution by Industry of U.S. Jobs Supported by Exports, 2010

- Figure 5. U.S. Jobs Supported by Exports, Top 15 States, 2014

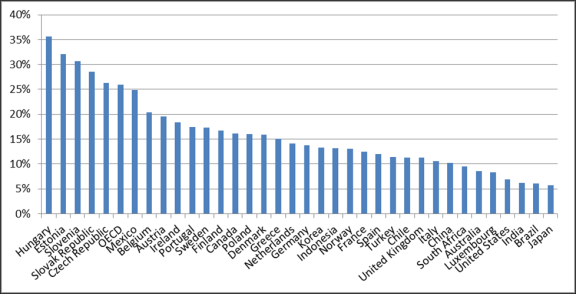

- Figure 6. Share of Foreign Value Added in Exports, by Country, 2010

- Figure 7. U.S. Merchandise Trade Deficit and Rate of Unemployment 2005-2017

- Figure 8. U.S. Net Saving Balances by Major Sector and Current Account Deficit

- Figure 9. Petroleum and Non-Petroleum Shares of the Annual U.S. Merchandise Trade Deficit

- Figure 10. Offshore Production as a Share of Total Manufacturing Production, 2005

Summary

During the Obama Administration, the United States negotiated two comprehensive and high-standard mega-regional free trade agreements: the Trans-Pacific Partnership (TPP) among the United States and 11 other countries, and the U.S.-European Transatlantic Trade and Investment Partnership (T-TIP). The 12 TPP countries signed the agreement in February 2016, but the agreement required ratification by each country before it could enter into force. In the United States this requires implementing legislation by Congress. Upon taking office, President Trump withdrew the United States from the TPP and halted further negotiations on the T-TIP, but may reengage in the TPP under different terms. The remaining 11 partners to the TPP concluded, without U.S. participation, a revised TPP, now identified as the Comprehensive and Progressive Agreement for Trans-Pacific Partnership (CPTPP). The Trump Administration is also attempting to revise the two largest existing U.S. FTAs, through the ongoing renegotiation of the North American Free Trade Agreement (NAFTA), and modification talks regarding the U.S.-South Korea (KORUS) FTA. For Members of Congress and others, international trade and trade agreements offer the prospect of improving national economic welfare, while also raising questions about the potential cost to the economy. Congress plays an important role in shaping and considering legislation to implement U.S. trade agreements.

Discussions of trade and trade agreements often focus on a number of issues, including the role that trade plays in the U.S. economy, the impact of trade agreements on employment gains and losses, and the size of the U.S. trade deficit. This report focuses on some of the major issues associated with trade and trade agreements and the impact of trade on the U.S. economy. The key findings include the following:

- From the perspective of the U.S. economy as a whole, trade is one among a number of forces that drive changes in employment, wages, the distribution of income, and ultimately the standard of living. Most economists argue that broad macroeconomic forces, including technological advances, are generally considered to be more important than trade.

- Economists generally conclude that trade provides net overall positive benefits to economies. Changes in trading patterns associated with changes in trading partners and composition or with new trade agreements, however, may entail certain adjustment costs, including changes in employment, which can be highly concentrated with some workers, firms, and communities affected disproportionately.

- In discussions of trade agreements, both proponents and opponents use the results of a variety of trade models and underlying assumptions to estimate the impact on the U.S. economy. Such models have various strengths and weaknesses, although not always in equal proportion. Most economists argue that such estimates represent a partial accounting of the total economic effects and, therefore, are not representative of the overall impact of trade agreements on the U.S. economy.

- Some argue that trade, trade agreements, and globalization more broadly contributed to growing wealth and income equality within countries. Growing income inequality domestically is not unique to the United States, or even to developed countries, but is found in both developed and developing countries. Despite intense focus in the academic literature, there is no consensus on the direct impact that trade or trade agreements have on income inequality.

- Congress faces a number of challenging policy issues relative to trade and the impact of trade agreements on the U.S. economy. These challenges include assessing the quality of data on trade and what, if any, additional resources should be devoted to collecting trade data and analyzing the role of trade in the economy. Congress also has legislative and oversight responsibility over various government programs that assist workers and firms adjust to increased competition from trade.

Introduction

The United States historically has led the global economic order that evolved after World War II. This economic order established multilateral economic institutions to advance rules-based commercial economic engagement, open markets, and transparent, nondiscriminatory treatment of all economic players. In turn, these efforts supported overall domestic and global economic growth and the nation's broader strategic interests. This agenda was broadly supported by successive Congresses and Administrations over seven decades. Congress plays a key role in U.S. trade policy by approving trade agreements, overseeing trade-oriented government agencies and adjustment assistance programs, and setting the terms for U.S. engagement with the global economy.

Congress plays a major role in formulating and implementing U.S. trade policy through its legislative and oversight responsibilities. Under the U.S. Constitution, Congress has the authority to regulate foreign commerce, while the President has the authority to conduct foreign relations. In 2015, Congress reauthorized Trade Promotion Authority (TPA) through the Bipartisan Congressional Trade Priorities and Accountability Act of 2015 (P.L. 114-26), which (1) sets trade policy objectives for the President to negotiate in trade agreements; (2) requires the President to engage with and keep Congress abreast of negotiations; and (3) provides for congressional consideration of implementing legislation on an expedited basis, e.g., guaranteed consideration, up-or-down vote, no amendments, limited time period.1

The United States concluded the Trans-Pacific Partnership (TPP) among the United States and 11 other countries and negotiated the U.S.-European Transatlantic Trade and Investment Partnership (T-TIP).2 The 12 TPP countries signed the agreement in February 2016, but it required ratification by each country before it could enter into force. In the United States, this requires implementing legislation by Congress. Upon taking office, President Trump withdrew the United States from the TPP and halted further negotiations on the T-TIP, but may reengage in the TPP under different terms. The remaining 11 partners to the TPP concluded, without U.S. participation, a revised TPP, now identified as the Comprehensive and Progressive Agreement for Trans-Pacific Partnership (CPTPP). The Trump Administration is also attempting to revise the two largest existing U.S. FTAs, through the ongoing renegotiation of the North American Free Trade Agreement (NAFTA), and modification talks regarding the U.S.-South Korea (KORUS) FTA. For Members of Congress and others, international trade and trade agreements offer the prospect of improving national economic welfare, while also raising questions about the potential cost to the economy. Congress plays an important role in shaping and considering legislation to implement U.S. trade agreements. Other countries also are participating in, or currently negotiating, a variety of FTAs.3

These proposed trade agreements raise questions and concerns over the role of trade in a country's economy and how increased trade, or globalization more generally, affects its employment, the distribution of income, and its standard of living. For some observers, these negotiations hold the potential to open markets further and establish new trade rules and disciplines, and they may reenergize the World Trade Organization (WTO), whose broad Doha Round negotiations have been stalled for over a decade. For Members of Congress and others, however, international trade and trade agreements offer not only the prospect of improved national economic welfare, but also the potential for lost jobs in some sectors.

This report focuses on a number of major issues concerning the role of trade and trade agreements in the economy and issues that are particular to FTAs, including

- the role of trade in the economy and the macroeconomic forces that drive the trade deficit;

- the impact of trade on employment and the adjustment costs experienced by firms and workers;

- estimates of the number of jobs in the economy that are supported by trade and economic models used to estimate the impact of FTAs on employment;

- the impact of FTAs on foreign investment and employment; and

- the relationship between trade and the distribution of income.

Background

Discussions of trade broadly and trade agreements in particular often focus on potential effects on economic growth, the distribution of income, and employment gains or losses.4 Most economists argue that liberalized trade results in both economic costs and benefits, but that the long-run net effect on the economy as a whole is positive. They contend that the economy as a whole operates more efficiently as a result of competition through international trade and that consumers benefit by having available a wider variety of goods and services at varying levels of quality and price than would be possible in an economy closed to international trade. They also contend that trade may have a long-term positive dynamic effect on an economy and enhance production and employment. According to the World Bank, liberalizing trade and foreign investment have reduced the number of people in the world living in extreme poverty (under $1 per day) by half, or 600 million, over the past 25 years, transforming the global economy.5

The United States International Trade Commission (ITC) released a study in June 2016 on the economic impact of trade agreements on the United States, based on the 14 trade agreements the United States has signed with 20 countries.6 The report concluded that these trade agreements increased U.S. aggregate trade by about 3% and U.S. real GDP and U.S. employment by, respectively, less than 1%, or $32.2 billion, and 159.3 thousand fulltime equivalent employees. In response to the report, however, Representative Sander Levin indicated in a statement:

....the ITC fails to adequately and innovatively address the real economic impact of previous U.S. free trade agreements. The ITC claims a small increase in GDP based on traditional economic models. The ITC fails to address the costs associated with workers losing their jobs or factories leaving communities as a result of trade agreements. Those transition costs are largely ignored in this report. They focus on the long-term benefit of lower tariffs in other countries and cheap imports coming into the United States, failing to capture the impact – which they may call short term – which can have a dramatic impact on jobs in America.7

Most economists also argue that macroeconomic forces within an economy are the dominant factors that shape trade and foreign investment relationships. In particular, the prominent role of these macroeconomic forces complicates efforts to disentangle the distinct impact that trade has on the economy. According to standard economic theory, macroeconomic conditions within an economy determine capital flows, which in turn affect exchange rates and the overall size of the trade deficit. In addition, economic theory holds that trade agreements between countries alter trade relationships and thus the composition of the trade deficit, but have little impact on the trade deficit's overall size.

Changes at the microeconomic level of the economy, such as new technologies, also can affect particular industries or sectors of the economy in ways that are unrelated to international trade.8 In addition, changes in currency exchange rates, productivity, economic policies, and the business cycle can affect the overall performance of the economy in ways that may outweigh the effects of trade agreements, given the already open nature of the U.S. economy. For instance, the decline in the value of the peso in late 1994, followed by a financial crisis in Mexico and severe economic recession,9 had a major impact on U.S.-Mexico trade, arguably greater than anything anticipated by the completion of the North American Free Trade Agreement (NAFTA).

More open markets globally and other changes have subjected a larger portion of the domestic workforce to international competition. According to the International Monetary Fund (IMF), the effective global labor market quadrupled over the past two decades through the opening of China, India, and the former East European bloc countries.10 In particular, the entry of China into the global economy is an unprecedented development given the size of the Chinese economy and the speed with which it became a major participant in the global economy. The global economy experienced this transformation initially through a rapid increase in trade of goods and services that were produced through labor-intensive processes. It also occurred secondarily, through a major disruption in global commodity markets as China's economy experienced slower growth and it began shifting its economy away from dependence on exports to an economy focused more on domestic consumption.11

According to the IMF, the internationalization of labor contributed to rising labor compensation in the advanced economies by increasing productivity and output, while emerging market economies benefited from rising wages.12 Increased exports from labor-intensive developing economies would be expected to push down wages, adjusted for productivity, for relatively unskilled workers in developed economies, thereby reducing labor's share of income.13

At the same time, most economists argue that workers in developed economies are better off if the net effects of increased trade and productivity on the economy are positive. Rising employment and wages in developing economies would increase living standards in those economies and increase demand for imports from developed economies, which would place upward pressure on wages and employment. The IMF concludes that globalization is only one of several factors that have acted to reduce the share of income accruing to labor in advanced economies and that technological change likely has played a larger role in affecting the distribution of income in the economy, especially for workers in lower-skilled sectors.14

Another development that has upended global trade and capital and labor markets is the impact of the digital revolution. In particular, the digital revolution, as a form of technological advancement, is a new variant of the long-term trend of labor-saving technologies that improve productivity and provide opportunities for labor to shift from labor-intensive activities to more knowledge-intensive activities. According to one economist, the new technologies, termed labor-linking, are transforming the global job landscape by linking labor with demand in faraway places and creating opportunities for small and medium-sized firms to participate in the global economy.15 In describing this new technology, this economist writes:

What this new technology has done is to make it possible for nations that are not yet rich and industrialized, such as the low-income economies and lower middle-income economies, to connect workers with corporations in industrialized nations. If these nations are moderately well-organized and have basic infrastructure such as power and digital connectivity, their workers can do well by working for companies and customers in rich and upper-middle-income nations. This in turn is creating new competition for workers in rich and some middle-income countries, dragging their salaries down and exacerbating unemployment. In brief, while the rise of labor-saving technology is tending to curb labor demand all over the world, some emerging economies and developing economies are able to offset the decline by taking advantage of labor-linking technologies.16

Trade and Employment

The effects that trade and trade agreements such as the TPP have on economic growth and employment are often among the most controversial issues. Economic theory concludes that the economy as a whole benefits over the long run from a more open trade environment and greater competition, because such an environment pushes an economy to use its resources more efficiently. Standard economic theory also recognizes that some workers and producers in the economy may experience a disproportionate share of the short-term adjustment costs that are associated with shifts in resources stemming from greater international competition. Although the attendant adjustment costs for businesses and labor are difficult to measure, some estimates suggest they may be significant over the short run and can entail dislocations for some segments of the labor force, for some companies, and for some communities. Closed plants can result in depressed commercial and residential property values and lost tax revenues, with effects on local schools, local public infrastructure, and local community viability.17

Many research organizations, academics, and others are analyzing the impact of trade on employment. A group of 10 international organizations, including the Asian Development Bank, the International Labor Organization, the World Bank, the Organization of American States (OAS), Organization for Economic Cooperation and Development (OECD), World Trade Organization (WTO), and the United Nations Conference on Trade And Development (UNCTAD), among others, joined together to form the International Collaborative Initiative on Trade and Employment (ICITE) to analyze the relationship between trade and employment.

A study published by ICITE surveyed the economic literature on trade and employment and restated the general position that over the long run higher levels of international trade are associated with positive rates of economic growth, rising wages, and higher levels of employment.18 Similarly, higher levels of economic growth are associated with higher levels of international trade, which complicates efforts to disentangle cause and effect relationships between economic growth and trade. The study also concluded that countries that experienced greater trade liberalization also experienced higher levels of investment, higher levels of productivity, and improvements in both physical and human capital. In addition, the study indicated that the positive correlation between trade and economic growth seems to be predicated on companion policies that countries adopted, including policies to create a positive investment climate and labor market as well as social protection systems that support trade liberalization.

The study concluded that forces within the economy that support trade competitiveness, primarily shifts in capital and labor to more internationally competitive sectors with higher productivity, also may result in frictional unemployment and income losses for displaced workers in the short run. According to the authors, for those countries that experience greater income inequality, factors other than trade are likely to be more important. The authors concluded that

....working conditions in developing countries, contrary to the assertions of some, have not deteriorated with trade openness. Indeed the positive effect of trade on investment and incomes carries with it important implications for reduced child labor, workplace injuries, and informality, while offering new opportunities for female entrepreneurs. However, trade, as with changes in technology, does entail reallocation of resources, so policies that help workers to move more quickly into new, higher productivity jobs can help attenuate human costs of normal job transitions and unemployment arising from economic shocks as well as lay the foundations for more rapid growth.19

In addition, the authors concluded

....trade liberalization may (sooner or later) be a necessary but not a sufficient condition for attaining more rapid growth. Whether countries realize the potential gains from trade liberalization depends heavily on companion policies and the general economic environment. These supportive policies—stable macroeconomic policies, adequate property rights, effective regulation, and well-designed public investments—can determine the difference between a trade reform that helps catapult trend growth to a higher level or one that produces little.20

Job Churning

Another factor that complicates efforts to equate gains or losses of jobs in the economy with trade or with a specific trade agreement is the constant turnover in jobs, referred to as "churn," that is continuously taking place in the U.S. economy. At the plant level, job openings may come from new businesses or from expansions at existing facilities, including those that support increased exports. Job losses may come from voluntary departures, involuntary discharges, or from business closures for any reason, including bankruptcy, personal choice, an inability to compete in the domestic market, import competition, or production shifts.

In a dynamic economy like that of the United States, jobs are constantly being created and replaced as some economic activities expand, while others contract. As part of this process, various industries and sectors evolve at different speeds, reflecting differences in technological advancement, productivity, and efficiency. Those sectors that are the most successful in developing or incorporating new technological advancements generate greater economic rewards and are capable of attracting larger amounts of capital and labor. In contrast, those sectors or individual firms that lag behind attract less capital and labor and confront ever-increasing competitive challenges. Indeed, to avoid economic stagnation, some sectors may need to relinquish some capital and labor so that others sectors can grow. Also, advances in communications, transportation, and technology have facilitated a global transformation of economic production into sophisticated supply chains that span national borders and defy traditional concepts of trade. This expanded reach of trade means that economic activities potentially can involve a greater share of the labor force in trade-related activities. How firms respond to these challenges likely will determine their long-term viability in the marketplace.

As indicated in Table 1, there was an annual average of 144.4 million jobs in the U.S. economy in 2016, up from the 141.8 million jobs recorded in 2015. During this same period, jobs supported by exports were estimated at 10.7 million jobs, or about 7.4% of employment in 2016. The data also indicate that in 2016 there were 13.1 million gross jobs gained in the economy and 10.6 million gross jobs lost, accounting for 9.1% and 7.4%, respectively, of the number of jobs in the economy, or amounts that bracket the total number of jobs in the economy that were supported by exports. The combined share of 16.5% (the combined shares of gross jobs gained and lost) reflects the process of job turnover during the year, or the churning in the labor market.

Job churning in the United States was more pronounced from 2008 to 2010, during the deepest part of the economic recession, when job turnover averaged over 18% of the jobs in the economy. High rates of job turnover also can occur during periods of strong economic growth, when demand for labor can prompt greater shifts in employment between growing and declining sectors of the economy. During 2008-2010, job turnover was more pronounced in the goods-producing sector of the economy, the sector most closely tied to international trade, where rates of job turnover ranged between 25% and 30%. Also, as the United States was experiencing a sharp decline in its trade deficit in 2009 and 2010, job turnover in the goods-producing sector recorded rates of 31.6% and 27.5%, respectively, rates that were much higher than the rate of job turnover in the overall economy. This likely reflected the sharp reduction in consumer spending during this period and a sharp drop in global trade due to the financial crisis and economic recession. Since 2011, job gains have been greater than job losses, helping to drive down the U.S. rate of unemployment. Also, since 2011, the share of jobs in the economy supported by exports has maintained a share of total employment between 10.7% and 11.2%, total goods-producing employment (6.3% and 6.7%), and services (4.1 and 4.8%).21

Table 1. Jobs Gained or Lost Annually and Job Turnover in the U.S. Economy, 2011-2016

(in millions of jobs; and percentage share of jobs in the respective sectors)

|

Year |

2011 |

2012 |

2013 |

2014 |

2015 |

2016 |

||||||

|

Jobs |

% share |

Jobs |

% share |

Jobs |

% share |

Jobs |

% share |

Jobs |

% share |

Jobs |

% share |

|

|

Total Employment |

||||||||||||

|

Total |

131.9 |

100.0% |

134.2 |

100.0% |

136.4 |

100.0% |

139.0 |

100.0% |

141.8 |

100.0% |

144.4 |

100.0% |

|

Gross job gains |

11.6 |

8.8% |

12.2 |

9.1% |

12.0 |

8.8% |

12.3 |

8.8% |

12.8 |

9.1% |

13.1 |

9.1% |

|

Gross job losses |

9.7 |

7.4% |

9.5 |

7.1% |

9.9 |

7.3% |

10.0 |

7.2% |

10.1 |

7.1% |

10.6 |

7.4% |

|

Net change |

1.9 |

1.4% |

2.7 |

2.0% |

2.1 |

1.6% |

2.3 |

1.6% |

2.7 |

1.9% |

2.5 |

1.7% |

|

Jobs supported by exports |

10.7 |

8.1% |

11.2 |

8.4% |

11.2 |

8.2% |

11.3 |

8.1% |

10.9 |

7.7% |

10.7 |

7.4% |

|

Goods Producing Sector |

||||||||||||

|

Total |

18.0 |

100.0% |

18.4 |

100.0% |

18.7 |

100.0% |

19.2 |

100.0% |

19.6 |

100.0% |

19.8 |

100.0% |

|

Gross job gains |

2.2 |

12.4% |

2.4 |

12.8% |

2.2 |

11.9% |

2.2 |

11.6% |

2.3 |

11.6% |

2.2 |

11.3% |

|

Gross job losses |

2.0 |

11.0% |

1.8 |

10.0% |

1.9 |

10.1% |

1.8 |

9.6% |

1.8 |

9.4% |

2.1 |

10.6% |

|

Net change |

0.2 |

1.4% |

0.5 |

2.8% |

0.3 |

1.8% |

0.4 |

2.0% |

0.4 |

2.3% |

0.1 |

0.7% |

|

Jobs supported by exports |

6.6 |

36.5% |

6.7 |

36.6% |

6.7 |

35.6% |

6.8 |

35.2% |

6.4 |

32.8% |

6.3 |

32.0% |

|

Services Sector |

||||||||||||

|

Total |

91.8 |

100.0% |

93.8 |

100.0% |

95.8 |

100.0% |

97.9 |

100.0% |

100.2 |

100.0% |

102.4 |

100.0% |

|

Gross job gains |

9.4 |

10.2% |

9.9 |

10.5% |

9.8 |

10.2% |

10.0 |

10.3% |

10.6 |

10.5% |

10.9 |

10.6% |

|

Gross job losses |

7.7 |

8.4% |

7.7 |

8.2% |

8.0 |

8.4% |

8.2 |

8.3% |

8.3 |

8.2% |

8.5 |

8.3% |

|

Net change |

1.7 |

1.8% |

2.2 |

2.3% |

1.8 |

1.9% |

1.9 |

1.9% |

2.3 |

2.3% |

2.3 |

2.3% |

|

Jobs supported by exports |

4.1 |

4.5% |

4.5 |

4.8% |

4.4 |

4.6% |

4.5 |

4.6% |

4.4 |

4.4% |

4.4 |

4.3% |

Sources: Business Employment Dynamics-Second Quarter 2017, Bureau of Labor Statistics, January 26, 2018, and Employment Situation-March 2018, Bureau of Labor Statistics, April 6, 2018; Jobs Supported by Exports 2016, An Update, International Trade Administration, August 2, 2017.

Worker Dislocation

As previously discussed, trade can have different effects on workers in different occupations, which some economists have termed the occupational exposure to international trade. As a result, trade liberalization not only can have a different effect between sectors of the economy on workers and firms, but also within the same industry. Some estimates indicate that the short-run costs to workers who attempt to switch occupations or switch industries in search of new employment opportunities as a result of dislocations related to international trade agreements may be "substantial."22 In a study of the impact of trade liberalization on occupations, a number of economists concluded that trade liberalization has had a small effect on wages and jobs at the industry level, but that trade liberalization has provided an additional impetus within the economy for workers to shift their employment among sectors of the economy, particularly from the manufacturing sector to the services sector.23 The study also concluded that workers who switched jobs as a result of trade liberalization generally experienced a reduction in their wages, particularly in occupations where workers performed routine tasks. These negative income effects were especially pronounced in occupations exposed to imports from low-income countries. In contrast, occupations associated with exports experienced a positive relationship between rising incomes and growth in export shares.24

U.S. Trade With China

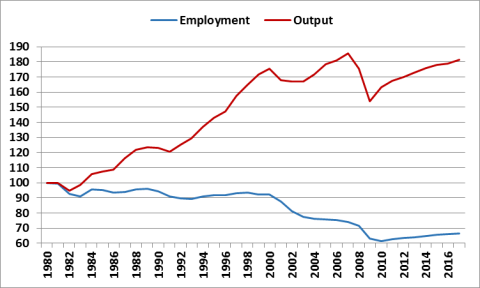

Changes in trade patterns can affect the types of goods that are traded and, therefore, the types of industries and workers that are directly exposed to trade. Some economists argue that U.S. and global trade patterns were altered by the approval of permanent normal trade relations (PNTR) for China in 2000 by the United States and by China's accession to the WTO in December 2001.25 In particular, these economists estimate that these developments increased U.S. imports from China at the expense of exporters in other Asian countries and had a major impact on U.S. manufacturing employment from 2001 to 2007. While the impact of increased Chinese imports on the U.S. economy is multifaceted and, in some cases, disruptive, the analysis also points to features and rigidities in U.S. labor markets, particularly at the local level, that hamper the adjustment process. Also, the U.S. manufacturing sector had been undergoing a fundamental restructuring for more than two decades prior to China joining the WTO and opening its economy. As Figure 1 indicates, U.S. manufacturing employment has slowly declined since at least 1980, falling by more than one-third between 1980 and 2014. During the same period, real output in the manufacturing sector nearly doubled, reflecting the increase in productivity in the U.S. manufacturing sector. During the economic recession of 2009, both employment and output in the manufacturing sector declined, along with most sectors of the U.S. economy. Between 2010 and 2017, U.S. manufacturing sector employment has increased by about 8% and output has increased by more than 11%.

|

Figure 1. Employment and Real Output in the U.S. Manufacturing Sector, 1980-2017 (1980 = 100) |

|

|

Source: Bureau of Labor Statistics; Bureau of Economic Analysis. |

Some estimates indicate that imports from China have been concentrated in a relatively small number of product areas in ways that have magnified the economic impact of Chinese imports on certain U.S. economic sectors and localities. According to a recent widely cited study, the local impact of increased import competition from China was associated with increased unemployment in manufacturing, decreased labor force participation, and increased use of disability and other transfer payments in certain localities.26 In part, these effects on local labor markets may persist over time because noncollege-educated workers, who experience the lowest levels of mobility between geographical areas or sectors, are overrepresented in manufacturing.27 These economists argue that a combination of demand and supply factors accounts for the growth in Chinese exports, including reform-induced changes within China, rising productivity, greater movement in labor-intensive export sectors, and a lowering of trade barriers.28

According to this analysis, Chinese imports appear to have little effect on average U.S. manufacturing wages, in part because the most productive workers retained their manufacturing jobs and manufacturing plants accelerated technological and organizational innovations. The authors argue that wages in the U.S. nonmanufacturing sector fell because the decline in the number of workers employed in manufacturing reduced demand for local services while increasing the supply of workers.29 The authors also indicate that Chinese productivity grew at a faster rate than U.S. productivity from 1997 to 2007. Such a difference by itself is not unusual since Chinese productivity was growing from a lower level than that of the U.S. economy and China was importing technology and technical know-how. U.S. productivity, however, grew at a pace that was consistent with historical trends and at a faster rate than other similarly highly developed economies, which may have necessitated the shifting of some resources from import-competing manufacturing industries to other sectors of the economy, even in the absence of increased trade with China.

The impact of increased U.S. imports from China on U.S. import-competing industries, however, represents only a partial accounting of the total economic impact of increased trade with China. Lower-priced goods from China would be expected to have a negative impact on import-competing industries, as consumers shifted their purchases toward the lower-priced imports and away from the relatively more expensive domestic products (the substitution effect). This substitution of imports for domestic products would negatively affect firms and workers in the import-competing industries, as indicated in the previous analysis. At the same time, lower-priced imports would increase the real incomes for all consumers in the economy (the income effect), improving consumer standards of living by increasing their purchasing power and allowing them to increase their consumption of additional goods and services. Lower prices also would be expected to spur increased production and employment in other sectors of the economy. In addition, increased exports by China would raise national income in China, which would increase Chinese consumption of both domestic and imported commodities, affording U.S. exporters more opportunities to increase their sales in China. The authors conclude their analysis by stating, "trade theory suggests that trade with China yields aggregate gains for the U.S. economy."30

Others experts argue that it was China's entry into the WTO, combined with extensive policy changes in China, that increased China's productivity and manufacturing capacity. China also removed barriers to investment by U.S. firms, which helped Chinese firms develop long-term trade and investment relationships with the United States.31 Other estimates indicate that increased trade with China has sped up technological innovation and the adoption of new technologies, both of which have contributed to productivity growth.32

Adjustment Policies

As a result of the differing impact of trade liberalization on workers and firms, some governments have adopted special safeguards and worker retraining and other social safety net policies to mitigate the potential adverse effects of trade liberalization or address certain trade practices that may cause or threaten to cause injury. For example, the United States established the Trade Adjustment Assistance (TAA) program to assist workers and firms adversely affected by trade agreements.33 The primary benefits of the program are funding for retraining and weekly income support payments while affected workers are enrolled in retraining.34 In negotiating trade agreements, governments are mindful of potential adjustment costs and address them in different ways, including negotiating longer transitional periods to phase out tariffs. At times, governments are constrained in their ability to liberalize trade due to opposition by groups within the economy that may bear a disproportionate share of the adjustment costs from such liberalization. These costs can be especially acute for older workers who may have a difficult time transitioning to other jobs and for workers who may lack advanced education and other skills. The length and impact of this adjustment process may vary greatly, depending on circumstances.35

The United States and its trading partners use trade remedies to mitigate the injury (or threat thereof) of various trade practices to domestic industries and workers. The three most frequently applied U.S. trade remedies are (1) antidumping (AD), which provides relief to domestic industries that have experienced, or are threatened with, material injury caused by the adverse impact of imports sold in the U.S. market at prices determined to be less than fair market value; (2) countervailing duties (CVD), which provide relief to domestic industries that are threatened with material injury due to the adverse impact of imported goods that have been subsidized by a foreign government or public entity; and (3) safeguards (also referred to as escape clause), which provide temporary relief from imports of fairly traded goods that cause or threaten to cause serious injury. Identified as Section 201 of the Trade Act of 1974, the safeguards clause may provide domestic industries with temporary relief from import competition through a temporary import duty, import quota, or a combination of both, based on a presidential decision.36

U.S. Jobs Supported by Exports

Various measures are used to estimate the role and impact of trade in the economy and of trade on employment. One such measure developed by the Department of Commerce's International Trade Administration (ITA) provides a unique estimate of the number of jobs in the U.S. economy that currently are supported directly and indirectly, not created, by exports. These estimates use available historical U.S. input-output data37 and projections in years when the input-output data are not updated. The 2007 benchmark input-output table was substantially revised and updated in February 2014.38 The benchmark input-output tables are revised every five years.

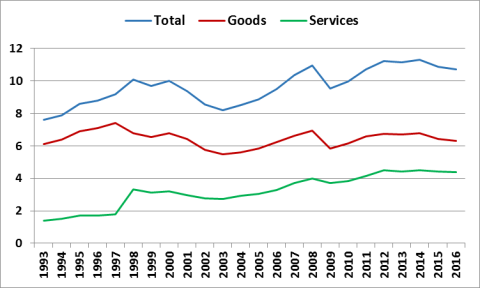

The ITA bases its approach on three economic relationships: (1) average relationships between the value of goods and services in the economy relative to the average number of jobs that are required to produce that output for each industry; (2) the value of inputs used in their production; and (3) the value of transportation and other marketing services required to bring goods and services to buyers.39 The agency does not develop a similar methodology to estimate the number of jobs related to imports, or any job gains or losses that may be due to imports. In its 2017 update, ITA estimated that U.S. exports of goods and services in 2016 supported 10.7 million jobs—6.3 million in the goods producing sector and 4.4 million in the services sector, as indicated in Figure 2.

ITA adjusted its methodology in 2011 to differentiate between changes in the prices of exports and changes in labor productivity. This methodology uses export price levels and a proxy estimator of U.S. export labor productivity to estimate the real value of U.S. exports (rather than the nominal value of exports reported in official sources) that support a given number of jobs as determined through input/output analysis and adjusted for changes in productivity.40

Goods and Services Jobs Supported by Exports

ITA projects that on average $1 billion of merchandise goods exports supported (not created) 5,223 jobs, and $1 billion of services exports supports 6,706 jobs, or an average of 5,744 jobs supported by goods and services exports combined. Expressed differently, $191,461 in merchandise goods exports, $149,120 in services exports, or an average of $174,095 in goods and services exports, supports one job in each respective sector.41 For the economy as a whole, the share of GDP associated with exports has increased since 1990. While the value of U.S. exports has grown, the number of jobs supported by exports is not significantly different from that estimated in 1990, suggesting that labor productivity in export sectors and export-supporting sectors has grown at a faster rate than that for the economy as a whole.42

|

Figure 2. Estimated Number of Jobs Supported by Exports in the Goods and Services Sectors in the U.S. Economy, 1993-2016 (in millions of jobs) |

|

|

Source: International Trade Administration. |

Earnings for Workers in Jobs Supported by Exports

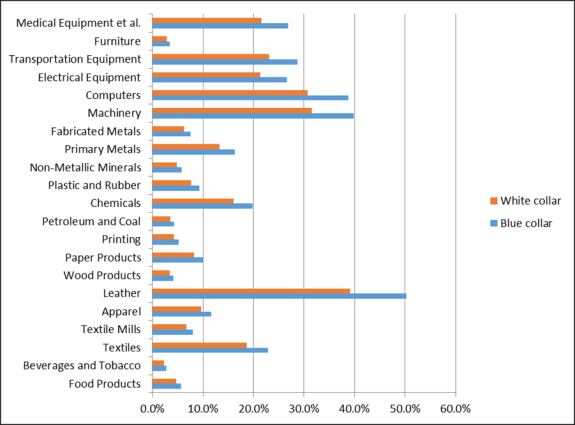

According to ITA estimates, jobs associated with international trade, especially jobs in export-intensive manufacturing industries, earn 18% more on a weighted average basis (termed the export earnings premium) than comparable jobs in other manufacturing industries, as indicated in Figure 3. ITA attributes this earning differential to several factors, including the observation that industries with greater access to international markets invest heavily in technology and capital in those areas where the United States has an international comparative advantage, which likely improves worker productivity. They also estimate that firms in export-oriented industries employ a more highly educated workforce on average, which also increases the average earnings of workers.43 Estimates indicate that U.S. labor productivity, particularly in the manufacturing sector, has been robust compared to other sectors in the U.S. economy. From 1993 to 2010, labor productivity in the U.S. manufacturing sector doubled, while U.S. nonfarm business labor productivity increased by about 50%.44 In addition, from 2002 to 2011, U.S. unit labor costs expressed in U.S. dollars fell by 15%, while unit labor costs rose in 18 other developed and developing countries.45

ITA concludes that its estimate of export earnings premiums for 2013 likely understates the actual export earnings differential.46 It estimates that the earnings differential for blue collar workers in export industries, at 20%, was higher than the average for white collar workers. In such industries as leather, computers, and machinery, the average weekly earnings of workers that supported exports were more than 30% higher than their counterparts in similar activities that were not involved in exporting. ITA also estimates that foreign tariffs may reduce the earnings of U.S. workers in manufacturing by 12% annually in the beverages and tobacco, food products, and apparel industries. Some economists conclude, however, that other factors, such as technological change, could account for the observed relationship between exporting and worker incomes, and they question the ability to estimate a direct cause and effect relationship between exporting, or trade more generally, and workers' earnings.47

Industry Distribution of Jobs Supported by Exports

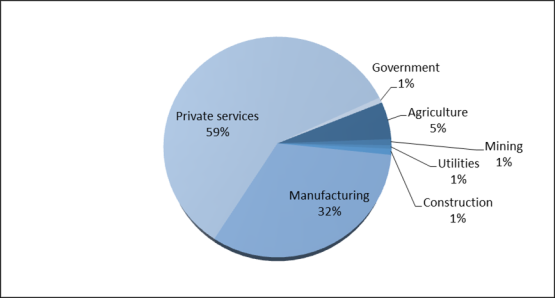

Additional estimates by ITA address the potential distribution of jobs by industry that were supported by exports in 2013, as indicated in Figure 4. Exports can support jobs directly and indirectly through industries that produce materials and services that serve as intermediate inputs to exports. According to ITA, jobs supported by exports in the manufacturing industry accounted for 32% of all jobs supported by exports. In addition, most of the jobs in the manufacturing sector that were supported by exports were in goods-producing activities. In contrast, jobs supported by exports in the services sector accounted for 59% of the total number of jobs that were supported by exports. Within the services sector, however, service-related jobs accounted for 40.5% of the jobs in the goods-producing sector that were supported by exports, reflecting the growing service component of merchandise exports. According to ITA, jobs supported by exports in the manufacturing sector have declined from 41.4% of the total number of jobs supported by exports in 1993 to 32.4% in 2010, also due to the relatively more rapid increase in labor productivity in the manufacturing sector.

|

Figure 4. Estimated Distribution by Industry of U.S. Jobs Supported by Exports, 2010 (percentage share) |

|

|

Source: International Trade Administration. |

Jobs Supported by State Exports

In addition to estimates of the total number of jobs in the United States that are supported by exports, ITA published estimates in 2015 of the number of jobs by state that are supported by the exports of goods, including manufactured goods, natural resources, and agricultural commodities, as indicated in Table 2.48 Estimating exports by state and, therefore, estimating the number of jobs in each state that are supported by exports, however, is hampered by a lack of detailed export data. Such state-level data are based on the Census Bureau's origin of movement (OM) data, or trade data based on the state in which a good began its journey to the port of export, which may not always be the state where the good was manufactured or from which it originated.49 These data are especially problematic for agricultural commodities when those commodities are shipped on the Mississippi River to New Orleans and are credited to Louisiana, instead of to the state where the commodities were produced. To improve its estimates, the ITA used a combination of OM data and export data from the Department of Agriculture, which uses a measure of state-level farm cash receipts to estimate each state's export value based on a state's share of the total cash receipts. These shares are applied to U.S. national export values to create state export values.50

In using the data, the ITA cautioned that

Given the data used to estimate jobs supported by state-level exports, care should be taken in the interpretation of the results. The figures should best be thought of as representing the number of jobs supported by the exports from a state as opposed to the number of jobs supported by exports within a state. As calculated, exports from a particular state are not necessarily produced in that state and, therefore, not all the labor embodied in the production of the export will be located in the state.51

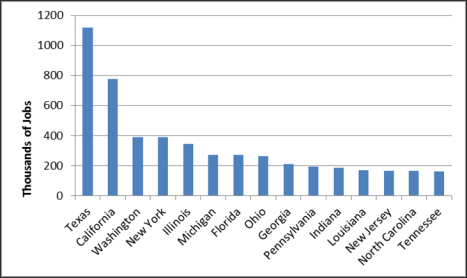

According to the ITA estimates, 15 states accounted for over 70% of the total number of U.S. jobs that were supported by exports in 2014. Exports from Texas and California accounted for nearly one-fourth of the total number of U.S. jobs supported by exports, as indicated in Figure 5.

|

Figure 5. U.S. Jobs Supported by Exports, Top 15 States, 2014 |

|

|

Source: International Trade Administration. |

|

State |

No. of jobs |

State |

No. of jobs |

State |

No. of jobs |

|

Alabama |

95,258 |

Kentucky |

137,138 |

North Dakota |

32,332 |

|

Alaska |

39,540 |

Louisiana |

170,200 |

Ohio |

263,356 |

|

Arizona |

93,354 |

Maine |

17,120 |

Oklahoma |

36,401 |

|

Arkansas |

50,490 |

Maryland |

59,650 |

Oregon |

86,157 |

|

California |

775,320 |

Massachusetts |

124,016 |

Pennsylvania |

191,779 |

|

Colorado |

43,615 |

Michigan |

270,927 |

Rhode Island |

13,459 |

|

Connecticut |

75,292 |

Minnesota |

128,863 |

South Carolina |

153,816 |

|

DC Washington |

4,114 |

Mississippi |

51,892 |

South Dakota |

24,407 |

|

Delaware |

23,278 |

Missouri |

86,602 |

Tennessee |

158,913 |

|

Florida |

270,473 |

Montana |

13,319 |

Texas |

1,117,318 |

|

Georgia |

209,071 |

Nebraska |

62,214 |

Utah |

50,578 |

|

Hawaii |

6,198 |

Nevada |

30,319 |

Vermont |

14,728 |

|

Idaho |

26,017 |

New Hampshire |

20,048 |

Virginia |

90,788 |

|

Illinois |

345,050 |

New Jersey |

165,695 |

Washington |

390,690 |

|

Indiana |

187,309 |

New Mexico |

16,546 |

West Virginia |

35,822 |

|

Iowa |

107,366 |

New York |

389,957 |

Wisconsin |

124,913 |

|

Kansas |

70,889 |

North Carolina |

164,023 |

Wyoming |

6,489 |

Source: International Trade Administration.

U.S. Jobs, Exports, and Trade Deficits

Both opponents and proponents of trade and trade agreements have used the numerical relationship developed by ITA on the number of jobs supported by exports in the economy to serve as a proxy for estimating the employment effects of FTAs. In some cases, various groups have used these data in reverse to argue that if a certain number of jobs were supported by $1 billion of exports, then that same number could be used to argue that a certain number of jobs would be "lost" by $1 billion of imports, represented by the trade deficit (the difference between exports of goods and services and imports of goods and services) so that any net increase in imports with countries that are associated with a trade agreement would necessarily result in a loss of employment for the economy.52 This approach also has been used by some to argue that the U.S. trade deficit implies a net loss of jobs in the economy; they contend that domestic production could be substituted for imports, which would boost both production and jobs in the U.S. economy.

While some imports and exports are substitutable, other imports represent items that are not available or are more costly to produce domestically. Also, demands on labor and capital markets vary substantially between export and import sectors. While some job losses associated with imports can be highly concentrated, imports also support a broad range of widely-dispersed service-sector jobs, including transportation, sales, finance, marketing, insurance, legal, and accounting.

Many economists argue that equating a trade deficit (whether on a bilateral basis or overall) with a specific amount of unemployment or job losses in the economy is questionable.53 According to standard economic theory, the overall size of the trade deficit arises from the imbalance of saving and investment in the economy as a whole, represented by the combined net savings or dissaving of households (individuals), firms, and the government sector relative to the amount of investment that takes place in the economy. This imbalance either increases capital inflows or outflows depending on whether the net amount of saving and investment is positive, which would tend to reduce domestic interest rates and increase capital outflows, or negative, which would tend to raise domestic interest rates and induce capital inflows. Such inflows and outflows affect the international exchange value of the dollar and, therefore, the prices of exports and imports.54

In contrast, trade agreements and other factors alter trading relationships by changing the composition of trade, or by changing the share of trade that is represented by different countries and a different mix of goods and services. As a result, most economists argue that, given the current composition of the U.S. economy, globalization, international trade, and trade agreements are not major determinants of the overall level of employment or wages in the U.S. economy, although trade can affect various sectors of the economy disproportionately.55 They assert that, for the U.S. economy, the total number of jobs and the overall level of production are determined by such macroeconomic factors as productivity growth, the growth rate of the population, and the pace of technological innovation.

ITA Clarification and Disclaimer

As indicated above, the methodology developed by ITA was unique to estimating a static number of jobs in the U.S. economy that were supported by exports, and ITA did not develop a similar methodology for linking imports or a trade deficit to jobs in the economy.56 The composition of U.S. imports is fundamentally different from that of U.S. exports. While some imports and exports represent clearly substitutable items, other imports represent inputs to further processing, or are items that either are not available or are not fully available in the economy. In addition, import-competing industries likely do not have the same mix of capital and labor in their production processes as do export-oriented industries, so that demands on capital and labor markets can vary substantially across industrial sectors.

ITA has issued various statements indicating that using the data on jobs supported by exports to estimate any relationship between imports and jobs (as has been done by some) is a misuse of the data.57 As ITA has stated, the employment estimate is a static relationship, or it reflects a relationship at a point in time, and is not a multiplier and should not be used to estimate changes in jobs associated with changes in exports or imports in a multiplier fashion; nevertheless, this has been done by both opponents and proponents of trade liberalization to estimate the number of U.S. jobs that have been lost or created as a result of trade agreements. In addition, the ITA estimates relate to the average number of jobs supported by exports across a broad section of the economy, which is not the same as estimating the number of jobs that would be added or lost as a result of a trade agreement. Such an estimate would need to focus on estimating the change in the composition of employment that would be associated directly with a change in trade as a result of a trade agreement. Also, most trade agreements incorporate provisions governing trade in services, investment, nontariff barriers, and a broad range of other issues that are not reflected in ITA's estimates.

ITA argues that its estimate of the number of jobs supported by exports should not be used with projected changes in trade to estimate potential employment effects from trade agreements. It says:58

Averages derived from IO [input-output]59 analysis should not be used as proxies for change. They should not be used to estimate the net change in employment that might be supported by increases or decreases in total exports, in the exports of selected products, or in the exports to selected countries or regions.

The averages are not proxies because the number of jobs supported by exports usually does not change at the same rate as export value. The rate is not the same because other factors, such as prices, resource utilization, business practices, and productivity, do not usually change at the same rate. In addition, the material and service inputs and the labor and capital inputs differ significantly across types of exports. For example, the labor requirements for an exported aircraft are significantly different from those of an exported agricultural product or an educational service.

Ideally, estimates of trade changes from tariff reductions would be multiplied by figures that reflect actual changes in employment (based on the mix of goods traded) that would occur at the margin as a result of changes in the volume of goods traded. According to ITA, though, such data do not exist. The only data that are available reflect the estimated average number of jobs supported across the U.S. economy by a given level of exports. Further, according to the ITA, "[a]s a result, multiplying trade estimates from the computable general equilibrium (CGE) models by employment averages would tend to overestimate the actual number of jobs potentially lost to trade changes."60

ITA also indicated that

In addition, estimates of the average number of jobs associated with exports cannot be adjusted for fluctuations in manufacturing capacity over the course of the business cycle. As explained by the USITC, the more slack capacity there is in the U.S. economy, the more potential there would be for job creation.61

During periods of slack business activity, increased output, including from export-oriented sectors, would tend to increase employment, lower unemployment, and increase labor force participation. Conversely, during periods of strong business activity, when industry operates at or near full capacity and employment, increased output, including output for exports, tends to raise employment less—if at all—and instead mainly shifts employment to industries that pay higher wages.

Trade Agreements and Employment Estimates

In contrast to ITA's estimates of the number of jobs in the economy currently supported by exports, some economists and others use various trade models to forecast the number of jobs that may be affected by FTAs. Most economists argue, however, that estimates of employment gains or losses represent a partial accounting of the total economic effects of FTAs and, therefore, are not representative of the overall impact of FTAs on the economy. In general, various economic models and approaches used to provide differing estimates of the magnitude of changes in U.S. employment that could arise from an FTA reflect different assumptions and conditions. Both proponents and opponents of FTAs cite results of these studies to support their respective positions. The various models and approaches have strengths and weaknesses, although not always in equal proportions, and they vary in the degree to which they reflect economic reality and are highly sensitive to the assumptions that are used.62

Trade models are different from macroeconomic models used to forecast GDP, employment, wages, taxes, and investment in the economy. Trade models are not structured to allow them to directly estimate changes in the number of job gains or losses in the economy that may arise from a trade agreement. Instead, trade models estimate changes in employment between sectors of the economy given certain baseline assumptions about changes in prices of traded goods and GDP. The models are hampered by data limitations and other theoretical and practical issues that make it difficult to derive precise estimates of the impact of a particular trade agreement on the economy. In response, some groups use various methods and proxy estimators to assess the potential impact of trade agreements on jobs, producing a wide range of estimates.

Some groups argue that in certain cases FTAs negatively affect employment in the United States, worsen the nation's trade deficit, and reduce wages for U.S. workers. Most economists acknowledge that international trade and FTAs can entail some negative effects, particularly job losses and lower wages, with the effects falling more heavily on some workers and some firms, but they also argue that the overall net effect is positive. Generally, the costs and benefits associated with FTAs do not accrue to the economy at the same speed; costs to the economy in the form of job losses are felt in the initial stages of the agreement, while benefits to the economy accrue over time. In addition, while research is ongoing, many economists conclude that there is little evidence indicating that trade liberalization, or international trade more broadly, is a major factor affecting income distribution, whether in the United States or in other economies, developed or developing. (See the section on "International Trade and Income Inequality" in this report.)

In comparison to the limited amount of data on nontariff barriers to trade in goods and services and the difficulties involved in translating nontariff barriers into tariff equivalents, the relative availability of data on trade in goods and tariff rates has tended to drive the policy dialogue concerning the impact that cuts in tariffs will have on employment, wages, and output in the economy. The rapid digitalization of the global economy, however, is reshaping global trade, as well as broader global value chains. As a result of these developments, global trade patterns arguably are being shaped more by nontariff activities than they are by traditional cuts in tariffs, due to successive rounds of trade negotiations that have lowered average tariff rates. Perhaps more importantly, the digital revolution is affecting the economy in unpredictable ways that are complicating efforts to collect data and to forecast the impact of the phenomenon in ways that capture their impact in trade models, thereby challenging the relevance of traditional trade models and some of the more common measures that often are used to assess the performance of trade agreements. As one study concluded, "globalization is being accelerated by flows of data that embody ideas, information, and innovation."63

Faced with pressure on jobs and wages from international trade, governments are tempted at times to protect domestic producers or vulnerable segments of the workforce. Such actions, however, have broader implications for the economy as a whole. Faced with these price pressures, firms can respond by upgrading their own production processes and improving their productivity. In lieu of making such structural changes, firms can also outsource production, fold, or attempt to alter the trade environment. Such attempts can include (1) negotiating with other producers to set a global price that is consistent with their own production costs, essentially creating a cartel price; (2) lobbying governments to raise the price of imported goods to match the domestic price through tariffs or nontariff measures, or some other form of a tax on imports; or (3) lobbying for subsidies to compensate domestic producers for the difference between the domestic and the international price. While the economic impact of these specific policies differs, they may impose costs on the economy as a whole by affecting the allocation of capital and labor. In almost all cases, efforts to protect a segment of the economy from international competition involve costs that are dispersed throughout the economy.

Trade Models

While the ITA provides annual estimates of the number of jobs in the economy that currently are supported by exports, the U.S. International Trade Commission (USITC) is directed to provide the official U.S. Government estimate of the impact of proposed trade agreements on the future course of the economy. The ITC uses an economic model known as the Global Trade Atlas Project (GTAP), located at Purdue University,64 to estimate changes in trade (exports and imports) that arise from changes in tariff rates and tariff rate quotas.65 This model is a long-run microeconomic model that has been used widely and tested to provide estimates of the distribution of potential gains and losses expressed as proportional effects (percentage increases or decreases in trade) for various sectors, relative to certain baseline economic projections.

Trade models used to analyze FTAs are part of a class of economic models referred to as computable general equilibrium models (CGE) that incorporate data on trade and a range of domestic economic variables from as many as 100 countries. These models generally operate with the assumption that the economy is operating at full employment and provide estimates of the distribution of potential gains and losses expressed as proportional effects (percentage increases or decreases in trade) for various sectors, relative to certain baseline economic projections. As a result of the large number of countries that often are included in trade models and the vast amounts of trade data that are used by the models, the models necessarily must sacrifice some level of precision in their estimating abilities. The models aim to provide insights into the mechanisms by which changes in tariffs or other parameters can affect changes in trade flows among a set of countries. Since such trade models originally were developed with the intent of analyzing the economic effects of such broad multilateral trade agreements as the Uruguay Round, this lack of precision was not considered to be an important drawback. However, this lack of precision may be an issue when the models are used to estimate the effects of bilateral trade agreements where the overall amount of trade, and therefore the impact of the agreement, is expected to be less than that of a comprehensive multilateral agreement.

Since tariff reductions and other provisions in trade agreements are phased in over a number of years, trade models must incorporate a number of assumptions that invariably compromise their ability to make accurate estimates. Trade agreements also attempt to strike a balance between commitment to an implementation schedule and flexibility to allow governments to adjust their commitment schedules due to events that may affect the length of time it takes for the agreement to be fully implemented. Such models also reflect various assumptions and subjective analysis that is used to estimate the economic impact of removing nontariff barriers, increasing foreign investment, and reducing or removing other barriers to trade. Nontariff measures have become an increasingly important component of trade agreements and may offer the greatest long-term benefits. Successive rounds of multilateral trade agreements have instituted across-the-board cuts in tariffs that have stimulated global trade among developed and developing economies and increased global economic welfare. What largely remain are higher tariffs on products that are the most politically sensitive.

Estimating the effect of trade agreements on employment is complicated further by two major economic forces. When import prices are lowered due to a trade agreement, the lower prices have two main effects: (1) they lower the prices of imported goods, which can stimulate a shift in domestic demand toward the comparably lower-priced imported goods (the substitution effect); and (2) they increase the real purchasing power of consumers and producers, which may increase demand for all goods and services (the income effect). For some goods, these two effects work in tandem to unambiguously increase demand, tending to increase production and employment. In some cases, however, the two effects work in opposite directions: the substitution effect has a negative impact on demand, while the income effect has a positive impact on demand. In these cases, the result of these two effects is ambiguous.

Other Domestic Effects of Trade

Beyond external forces that affect the economy, multi-directional interactions within the economy complicate efforts to determine cause and effect between trade and trade agreements and the gains or losses of jobs. International trade is not the primary force that creates jobs in the U.S. economy; exports account for about 13% of total U.S. annual GDP, compared with 45% in Germany and 30% in Canada.66 The total number of jobs and the overall level of production in the United States are determined by such macroeconomic factors as productivity growth, the growth rate of the population, and the pace of technological innovation.

Although trade agreements may have a limited impact on the U.S. economy as a whole, trade agreements with specific countries may have a concentrated impact on certain sectors of the economy due to the nature of the trade relationship. As indicated, it is difficult to determine beyond broad generalizations how a trade agreement will affect jobs in the economy, given the range of other factors that can affect job gains and losses in the U.S. economy, especially considering the extended phase-in period of most FTAs. Also, significant gaps in data, particularly relative to formal and informal barriers in the services sector, hinder the ability to model the effects of trade agreements that lower barriers to trade in services. These gaps are important for the United States, because the services sector accounts for 66% of output and 70% of full- and part-time employment in the U.S. economy, and increased trade in services offers the possibility of large gains for the U.S. economy.67 U.S. trade also is characterized by the extent of trade with developed economies that are similar to the United States. In 2015, for instance, 63% of U.S. exports and 57% of U.S. imports were from countries with similarly highly developed economies.68

In general, economists view trade agreements as a potential force in encouraging greater economic openness. Consequently, trade agreements potentially can serve as a driving force for economic change. This change, however, cannot always be quantified and, therefore, cannot always be represented in trade models. Comprehensive free trade agreements include a range of policy issues that have cross-border implications, including trade in goods and services, investment, regulatory and other nontariff trade barriers, government procurement, e-commerce, agricultural barriers, intellectual property rights, state-owned enterprises, worker rights, and the environment. As such, these trade agreements can serve as catalysts for economic growth and development that can have a significant impact on a nation's economy beyond what would be predicted from traditional trade models. This can be particularly important for developing countries; such countries may be trying to raise their own standards and see trade agreements as important tools for integrating themselves into regional and global economies, as well as for implementing domestic economic reforms. In addition, trade agreements may help standardize such matters as dispute resolution procedures and other governance issues.69

General Assumptions and Limitations of Trade Models

Beyond the general limitations discussed above, trade models incorporate a number of other, often unstated, assumptions that affect their forecasting accuracy. Despite these limitations, CGM trade models are widely used and have proven to be helpful in estimating the effects of trade liberalization in such sectors as agriculture and manufacturing where the barriers to trade are more easily identifiable and quantifiable. Barriers to trade in services and investment, however, have proven to be more difficult to identify and, therefore, to quantify in an economic model. In general, trade models attempt to estimate the impact on domestic economic activity as a result of changes in the volumes of exports and imports that would arise from changes in the prices of goods that, in turn, are affected by changes in tariff rates. These estimated changes in exports and imports are based on assumptions noted below.

General Assumptions

Trade models like the GTAP model noted above must aggregate vast amounts of data into a manageable size, for instance by reducing more than 17,000 individual commodities into about 50 categories. As a result, tariffs in the models represent weighted averages of tariffs for the commodities that are aggregated into these basic groups. This procedure tends to mask the importance of those products within the aggregate that have high tariff rates. This also means that products within a group may not be good substitutes for products in another country and imported products in a category may be quite dissimilar to a country's domestic product in that same category.

Trade models also generally do not incorporate assumptions about the speed with which tariff changes affect the relevant economies, leaving it to the modelers to make assumptions about how quickly changes in tariff rates will be passed along in goods prices and about the timing of any adjustments that occur. Also, these models make no assumptions about the basic input-output structure of the economy, and they do not attempt to adjust this structure to account for economic or technical changes that lead an industry to substitute one factor for another. This assumption is particularly important, since the basic economic theories that relate changes in the prices of goods, whether from changes in tariff rates or from some other source, to changes in the demand for such factors as labor and capital assume that price changes drive changes in the basic input-output structure of the economy.

Full Employment Assumption