The U.S. federal tax system includes several elements. Income taxes are the primary component, and the United States has an income tax that applies to the income of individuals and a separate tax for corporations. The United States also levies payroll taxes on employment earnings, with most of this revenue used to finance social insurance programs. The U.S. tax system also includes an estate and gift tax, as well as several excise taxes.

At the end of 2017, President Trump signed into law P.L. 115-97, which substantially changed the U.S. federal tax system. Consequently, the federal tax system in effect for 2018 differs from what was in effect for 2017.1 Most of the changes to the individual income tax system in P.L. 115-97 are temporary and scheduled to expire at the end of 2025. Thus, under current law, after 2025, the individual income tax system is slated to look like the system that was in effect for 2017. In contrast, many of the changes affecting corporations are permanent.

This report provides an overview of the federal tax system, including the individual income tax, corporate income tax, payroll taxes, estate and gift taxes, and federal excise taxes, as in effect for 2018. Information on changes to the tax system enacted in the 2017 tax revision (P.L. 115-97) can be found in CRS Report R45092, The 2017 Tax Revision (P.L. 115-97): Comparison to 2017 Tax Law, coordinated by [author name scrubbed] and [author name scrubbed].

The Federal Income Tax System

The federal income tax system has several components. The largest component, in terms of revenue generated, is the individual income tax. For fiscal year (FY) 2018, an estimated $1.7 trillion, or 50% of the federal government's revenue, will come from the individual income tax.2 The corporate income tax is estimated to generate another $218 billion in revenue in FY2018, or just under 7% of total revenue. Social insurance or payroll taxes will generate an estimated $1.2 trillion, or 35% of revenue in FY2018. Estimates indicate that the remainder of federal revenue collected in FY2018 will come from excise taxes (3%) or other sources (6%).3

The Individual Income Tax4

The individual income tax is the largest source of revenue in the federal income tax system. Most of the income reported on individual income tax returns is wages and salaries. The Joint Committee on Taxation (JCT) estimates that in 2018, 68% of individuals' gross income will come from wages and salaries.5 However, a large portion of business income in the United States is also taxed in the individual income tax system. Pass-through businesses, including sole proprietorships, partnerships, S corporations, and limited liability companies, generally pass business income through to the business's owners, where that income is taxed at individual income tax rates.6 Projections indicate that in 2018, 10% of income reported by individual taxpayers will be business, farm, or Schedule E income.7

Gross Income and Adjustments

To levy an income tax, income must first be defined. As a benchmark, economists often turn to the Haig-Simons comprehensive income definitions, which can differ from the measure of income used in computing a taxpayer's taxes. Under the Haig-Simons definition, taxable resources are defined as changes in a taxpayer's ability to consume during the tax year.8 Using this definition of income, an employer's contributions toward employee health insurance, for example, would be counted toward the employee's income. This income, however, is not included in the employee's taxable income under current tax law.

In practice, the individual income tax is based on gross income individuals accrue from a variety of sources. Included in the individual income tax base are wages, salaries, tips, taxable interest and dividend income, business and farm income, realized net capital gains, income from rents, royalties, trusts, estates, partnerships, and taxable pension and annuity income.

Gross income for tax purposes excludes certain items, which may deviate from the Haig-Simmons definition of income. For example, employer-provided health insurance, pension contributions, and certain other employee benefits are excluded from income subject to tax.9 Employer contributions to Social Security are also excluded from wages. Amounts received under life insurance contracts are excluded from income. Another exclusion from income is the interest received on certain state and local bonds. Some forgiven debts and various other items are also excluded from income for tax purposes.

There are special rules for income earned as capital gains or dividends.10 Capital gains (or losses) are realized when assets are sold.11 The tax base excludes unrealized capital gains.12 There are reduced tax rates for certain capital gains and dividends (discussed below in the "Tax Rates" section).13 As with ordinary income, there may be exclusions. For example, certain capital gains on sales of primary residences are excluded from income.

Income from operating a business through a proprietorship, partnership, or small business corporation that elects to be treated similarly to a partnership (Subchapter S corporation), or income from rental property, is also subject to the individual income tax.14 This income is the net of gross receipts reduced by such deductible costs as payments to labor, depreciation, costs of goods acquired for resale and other inputs, interest, and taxes.

A taxpayer's adjusted gross income (AGI), the basic measure of income under the federal income tax, is determined by subtracting "above-the-line" deductions from gross income.15 Above-the-line deductions are available to taxpayers regardless of whether they itemize deductions or claim the standard deduction.16 Above-the-line deductions may be claimed for, among other items, contributions to qualified retirement plans by self-employed individuals, contributions to individual retirement accounts (IRAs), interest paid on student loans, higher education tuition expenses, and contributions to health savings accounts.

Filing Status and Deductions

Tax liability depends on the filing status of the taxpayer. There are four main filing categories: married filing jointly, married filing separately, head of household, and single individual. The computation of taxpayers' tax liability depends on their filing status, as discussed further below. The amount of the standard deduction also depends on filing status. Deductions are subtracted before determining taxable income.

Taxpayers have a choice between claiming the standard deduction or claiming the sum of their itemized deductions. The standard deduction amount depends on filing status. The 2018 standard deduction for single filers is $12,000, while the standard deduction for married taxpayers filing jointly is twice that amount, or $24,000. The standard deduction for a head of household is $18,000. There is an additional standard deduction for the elderly (taxpayers age 65 and older) and the blind.17 The standard deduction amount is indexed for inflation.18

When the sum of taxpayers' itemized deductions exceeds the standard deduction, taxpayers may choose to itemize. Deductions may be allowed for mortgage interest19 and charitable contributions.20 Taxpayers may also claim up to $10,000 ($5,000 for married taxpayers filing separately) in total deductions for state and local taxes (income, sales, or property taxes).21

|

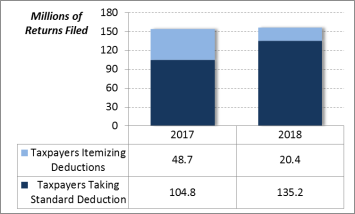

Recent Changes in Personal Exemptions and Deductions The 2017 Tax Revision (P.L. 115-97) substantially changed the individual income tax system by eliminating personal exemptions and nearly doubling the standard deduction. Before 2018, taxpayers deducted personal exemptions from their AGI when calculating taxable income. Personal exemptions were allowed for taxpayers, their spouse, and any dependents. For 2018, the personal exemption amount would have been $4,150 per exemption, had the exemption not been temporarily eliminated in P.L. 115-97. Standard deduction amounts for 2018 would have been $6,500 for single filers, and $13,000 for married taxpayers filing jointly, had P.L. 115-97 not been enacted. Nearly doubling the standard deduction means that fewer taxpayers will itemize deductions. Additional limitations imposed on the deduction for state and local taxes and mortgage interest deduction in P.L. 115-97 may also contribute to fewer taxpayers claiming these deductions. The share of taxpayers itemizing deductions is expected to fall substantially between 2017 and 2018 (see Figure 1). For 2017, the JCT estimated that 48.7 million (32%) tax filers will itemize deductions.22 For 2018, the JCT estimates that 20.4 million (13%) tax filers will itemize deductions.23

|

Some deductions can only be itemized and claimed in excess of a floor. For example, medical expenses can be deducted to the extent they exceed 7.5% of AGI.24 Casualty and theft losses attributable to federally declared disasters can also be deducted in excess of 10% of AGI.

The JCT estimates that for 2018, 135.2 million tax returns filed will use the standard deduction, while 20.4 million returns will elect to itemize deductions (see Figure 1).

Deduction for Qualified Business Income

The deduction for qualified business income is also taken in determining taxable income. Individual taxpayers can deduct 20% of qualified business income from a partnership, S corporation, or sole proprietorship. Individual taxpayers can also deduct 20% of qualified Real Estate Investment Trust (REIT) dividends, publicly traded partnership income, and cooperative dividends. Above threshold amounts, the deduction begins to phase out for income from certain services, including health, law, accounting, actuarial science, performing arts, consulting, athletics, financial services, brokerage services, or investing and investments management services. These threshold amounts are $315,000 for married taxpayers filing joint returns, and $157,500 for all other taxpayers. The deduction is also subject to limitation based on the taxpayer's allocable share of W-2 wages paid and the taxpayer's allocable share of capital investment above these threshold amounts. Specifically, the deduction is limited to the greater of 50% of W-2 wages, or 25% of W-2 wages plus 2.5% multiplied by qualified property.

Tax Rates

The income tax system is designed to be progressive, with statutory marginal tax rates increasing as income increases.25 At a particular statutory marginal tax rate, all individuals subject to the regular income tax, regardless of their overall level of earnings, pay the same tax rate on taxable income within the bracket. Once taxpayers' incomes surpass a threshold level, placing them in a higher marginal tax bracket, the higher marginal tax rate is only applied on income that exceeds that threshold value. In 2018, the individual income tax system has seven marginal income tax rates: 10%, 12%, 22%, 24%, 32%, 35%, and 37%.26 These marginal income tax rates are applied to taxable income to arrive at a taxpayer's gross income tax liability.27 Threshold levels associated with the rate brackets depend on filing status. Tax rates for 2018 are summarized in Table 1.

|

Married Filing Jointly |

|||

|

If taxable income is: |

Then, tax is: |

||

|

$0 |

to |

$19,050 |

10% of the amount over $0 |

|

$19,050 |

to |

$77,400 |

$1,905 plus 12% of the amount over $19,050 |

|

$77,400 |

to |

$165,000 |

$8,907 plus 22% of the amount over $77,400 |

|

$165,000 |

to |

$315,000 |

$28,179 plus 24% of the amount over $165,000 |

|

$315,000 |

to |

$400,000 |

$64,179 plus 32% of the amount over $315,000 |

|

$400,000 |

to |

$600,000 |

$91,379 plus 35% of the amount over $400,000 |

|

$600,000 |

plus |

$161,379 plus 37% of the amount over $600,000 |

|

|

Single |

|||

|

If taxable income is: |

Then, tax is: |

||

|

$0 |

to |

$9,525 |

10% of the amount over $0 |

|

$9,525 |

to |

$39,700 |

$952.50 plus 12% of the amount over $9,525 |

|

$39,700 |

to |

$82,500 |

$4,453.50 plus 22% of the amount over $39,700 |

|

$82,500 |

to |

$157,500 |

$14,089.50 plus 24% of the amount over $82,500 |

|

$157,500 |

to |

$200,000 |

$32,089.50 plus 32% of the amount over $157,500 |

|

$200,000 |

to |

$500,000 |

$45,689.50 plus 35% of the amount over $200,000 |

|

$500,000 |

plus |

$150,689.50 plus 37% of the amount over $500,000 |

|

|

Heads of Households |

|||

|

If taxable income is: |

Then, tax is: |

||

|

$0 |

to |

$13,600 |

10% of the amount over $0 |

|

$13,600 |

to |

$51,800 |

$1,360 plus 12% of the amount over $13,600 |

|

$51,800 |

to |

$82,500 |

$5,944 plus 22% of the amount over $51,800 |

|

$82,500 |

to |

$157,500 |

$12,698 plus 24% of the amount over $82,500 |

|

$157,500 |

to |

$200,000 |

$30,698 plus 32% of the amount over $157,500 |

|

$200,000 |

to |

$500,000 |

$44,298 plus 35% of the amount over $200,000 |

|

$500,000 |

plus |

$149,298 plus 37% of the amount over $500,000 |

|

Source: Internal Revenue Code.

Certain higher-income individuals may be subject to the alternative minimum tax (AMT). There are two marginal tax rates under the AMT, 26% and 28%, that are applied to an expanded income base. The AMT is discussed in further detail below.

|

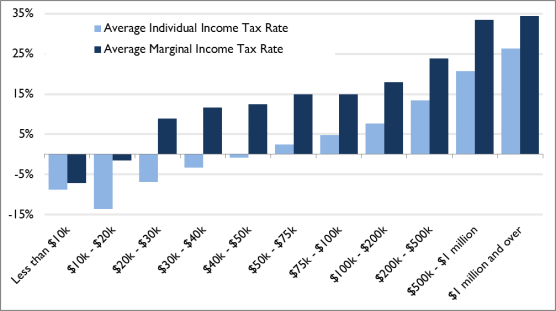

Average and Marginal Tax Rates, by Income Group For most taxpayers, their average tax rate (individual income taxes paid divided by income) is less than their statutory tax rate. This is due to the progressive nature of the tax system, coupled with a variety of tax preference items (credits, deductions, exclusions, etc.). Many taxpayers, particularly lower-income taxpayers, have negative average tax rates. Refundable tax credits, such as the earned income tax credit (EITC) (discussed below), can lead to negative average tax rates.28 As illustrated in Figure 2, the average of average tax rates is projected to be negative for all income groups below $50,000 in 2018.29 Marginal tax rates are the amount of tax paid on the next dollar of earnings.30 Marginal tax rates are determined by (1) a taxpayer's statutory tax bracket; and (2) interactions with other credits, deductions, exemptions, and special provisions in the tax code. These interactions, particularly phase-ins and phaseouts of various provisions, mean that an individual's marginal tax rate can be higher than or lower than their statutory rate. On average, marginal tax rates are negative for taxpayers in the lowest income groups (those below $20,000) (see Figure 2).31 The average of marginal tax rates tends to rise with income, and exceeds the average of average tax rates for all income groups. Projections for 2018 indicate that, on average, for taxpayers in the highest income group ($1 million and above), the average marginal tax rate (34%) will be less than the highest statutory rate of 37%.

|

Tax Rates on Capital Gains and Dividends

As was noted above, income earned from long-term capital gains and qualified dividends may be taxed at lower rates. The rate on long-term capital gains and qualified dividends can be 0%, 15%, or 20%, depending on the taxpayer's taxable income and filing status. The rates are linked to the statutory rate brackets that were in effect before P.L. 115-97 was enacted, such that the 20% rate applies to taxpayers that would have been in the 39.6% bracket (under the pre-P.L. 115-97 rate structure). Taxpayers that would have been in the 25%, 28%, 33%, and 35% tax brackets under the former rate structure face a 15% tax rate on long-term capital gains and qualified dividends, whereas the rate is 0% for taxpayers that would have been in the 10% and 15% tax brackets under the former rate structure. The taxable income thresholds for long-term capital gains and qualified dividends in 2018 are summarized in Table 2.

Net Investment Income

Certain higher-income individuals may be subject to an additional 3.8% tax on net investment income. Specifically, the tax applies to the lesser of (1) net investment income, or (2) the amount by which modified AGI exceeds fixed threshold amounts.32 The fixed threshold amounts are $250,000 for taxpayers filing jointly and $200,000 for other filers.33 The net-investment-income tax increases the maximum tax rate on capital gains and dividends to 23.8%. The maximum rate on other investment income, including interest, annuities, royalties, and rent, is 40.8%.

|

Married Filing Jointly |

Single |

Heads of Households |

||||||

|

Taxable Income |

Tax Rate |

Taxable Income |

Tax Rate |

Taxable Income |

Tax Rate |

|||

|

Less than $77,200 |

|

Less than $38,600 |

|

Less than $51,700 |

|

|||

|

$77,200 to $479,000 |

|

$38,600 to $425,800 |

|

$51,700 to $452,400 |

|

|||

|

Above $479,000 |

|

Above $425,800 |

|

Above $452,400 |

|

|||

Source: Internal Revenue Code.

Tax Credits

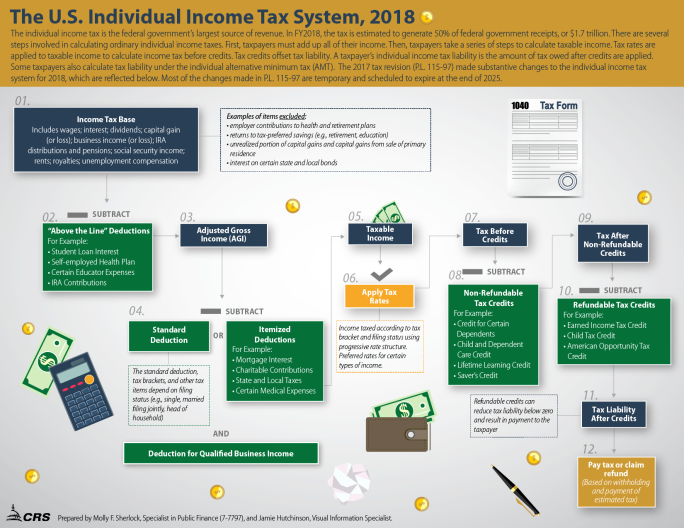

After a taxpayer's tax liability has been calculated, tax credits are subtracted from gross tax liability to arrive at a final tax liability (see Figure 3). Tax credits offset tax liability on a dollar-for-dollar basis. There are two different types of tax credits: refundable and nonrefundable. If a tax credit is refundable, and the credit amount exceeds tax liability, a taxpayer receives the credit (or a portion of the credit) as a refund. If credits are not refundable, then the credit is limited to the amount of tax liability. In some cases, unused credits can be carried forward to offset tax liability in future tax years. Some credits are phased out as income rises to limit or eliminate benefits for higher-income taxpayers.

Tax credits that are refundable or have a refundable portion include the earned income tax credit (EITC)34 and the child tax credit (CTC).35 The American Opportunity Tax Credit (AOTC), a tax credit for tuition expenses, also has a refundable portion.36

A nonrefundable tax credit can be claimed for child and dependent care expenses.37 There are also tax credits for other purposes, such as education38 and certain health insurance premiums.39

Tax credits add to the complexity of the tax system for various reasons. For one, tax credits can cause effective marginal tax rates to differ from statutory marginal tax rates for many taxpayers.40 For example, the earned income tax credit (EITC) phases in as income increases, reducing a taxpayer's marginal tax rate. At higher income levels, as the credit phases out, the taxpayer faces a higher marginal tax rate during that phaseout range. Thus, effective marginal tax rates can be less than or greater than statutory rates. Tax credits can also pose administrative challenges.41

Alternative Minimum Tax

Individuals may also pay tax under the alternative minimum tax (AMT). The AMT applies lower tax rates to a broader income base. The policy goal of the AMT is to prevent certain higher-income taxpayers from using the graduated personal income tax rate structure and tax preferences to avoid paying sufficient amounts of taxes.42

To calculate the AMT, an individual first adds back various tax items, including certain itemized deductions and business tax preferences, to regular taxable income.43 This grossed-up amount becomes the income base for the AMT.

The AMT exemption is subtracted from the AMT's income base. For 2018, the AMT exemption is $109,400 for married taxpayers filing a joint return, $54,700 for married taxpayers filing separate returns, and $70,300 for all other individual tax filers.44 These exemption amounts are indexed for inflation. The AMT exemption is reduced by 25% of the amount by which a taxpayer's AMT taxable income exceeds certain threshold amounts. In 2018, the AMT exemption amount begins to phase out at $1,000,000 for married taxpayers filing a joint return and $500,000 for all other individual tax filers.

A two-tiered rate structure of 26% and 28% is assessed against AMT taxable income.45 The taxpayer compares his AMT tax liability to his regular tax liability and pays the greater of the two. Most nonrefundable personal tax credits are allowed against the AMT. The JCT estimates that roughly 600,000 tax filers will pay the AMT in 2018.46

|

Figure 3. Visualization of the U.S. Individual Income Tax System |

|

|

Source: This graphic was previously published as CRS Infographic IG10011, The U.S. Individual Income Tax System, 2018, by [author name scrubbed]. |

The Corporate Income Tax47

The corporate income tax generally only applies to C corporations (also known as regular corporations). These corporations—named for Subchapter C of the Internal Revenue Code (IRC), which details their tax treatment—are generally treated as taxable entities separate from their shareholders.48 That is, corporate income is taxed once at the corporate level according to the corporate income tax system. When corporate dividend payments are made or capital gains are realized income is taxed again at the individual-shareholder level according to the individual tax system (discussed above). In contrast, noncorporate businesses, including S corporations49 and partnerships,50 pass their income through to owners who pay taxes. Collectively, these noncorporate business entities are referred to as pass-throughs. For these types of entities, business income is taxed only once, at individual income tax rates. As discussed above, taxpayers may be allowed to claim a 20% deduction from certain income earned by pass-through businesses.

The corporate income tax is designed as a tax on corporate profits (also known as net income). Broadly defined, corporate profit is total income minus the cost associated with generating that income.51 Business expenses that may be deducted from income include employee compensation; the decline in value of machines, equipment, and structures (i.e., depreciation); general supplies and materials; advertising; and interest payments (subject to certain limitations).52 Businesses may also be allowed 100% first-year depreciation or to expense the costs of certain property. The corporate income tax also allows for a number of other special deductions, credits, and tax preferences that reduce taxes paid by corporations. Oftentimes, these provisions are intended to promote particular policy goals (promoting charitable giving or encouraging investment in renewable energy, for example). A corporation's tax liability can be calculated as follows:

Taxes = [(Total Income – Deductible Expenses) × Tax Rate] – Tax Credits.

Some corporations experience net operating losses (NOLs), which occur when total income less expenses is negative. Losses arising after 2017 can generally be "carried forward" indefinitely, and used to offset future tax liability.53 The NOL deduction is generally limited to 80% of taxable income.54

The corporate income tax rate is a flat 21%. Thus, tax liability before applying tax credits is generally calculated as 21% of taxable income. Corporate tax liability can be reduced by claiming corporate tax credits. Credits claimed by corporations include the research credit,55 the low-income housing tax credit,56 certain energy credits,57 the new markets tax credit,58 the work opportunity tax credit,59 and an employer credit for paid family and medical leave (this provision expires in 2019).

In broad economic terms, the base of the corporate income tax is the return to equity capital. Income produced by corporate capital investment includes that produced by corporate investment of borrowed funds (debt), and that produced by investment of equity, or funds provided by stockholders. The deductibility of certain items makes it such that the corporate income tax applies largely to equity capital. Specifically, wages are tax deductible, so labor's contribution to corporate revenue is excluded from the corporate tax base. Additionally, profits from debt-financed investment are paid out as interest, which is partially deductible. To the extent that interest is deductible, the return to debt capital is excluded from the corporate tax base. Equity investments are financed by retained earnings and the sale of stock. The income equity investment generates is paid out as dividends and the capital gains that accrue as stock increases in value. Neither form of equity income is generally deductible. Thus, the base of the corporate income tax is largely the return to equity capital.

With the base of the corporate tax being largely equity income, the flow of capital out of the corporate sector and other economic adjustments probably cause the burden of the tax to spread to all owners of capital: owners of unincorporated business, bondholders, and homeowners. In analyzing the incidence of the corporate tax, the Congressional Budget Office (CBO) and JCT generally distribute most of the burden to owners of capital, with a smaller portion falling on labor income.60 Since owners of capital tend to be in higher income groups, and most of the corporate tax burden falls on capital, the corporate tax is widely viewed as being progressive.

Corporate Income Earned Abroad

The United States has a quasiterritorial tax system. In general, dividends received by U.S. corporate shareholders from their controlled foreign corporations (CFCs) are generally eligible for a 100% dividends-received deduction. However, certain forms of passive or easily shifted income are taxed in the year earned—under subpart F. In addition, global intangible low-taxed income (GILTI) is taxed at 10.5%.61 A deduction is allowed for the foreign derived intangible income (FDII)—roughly the share of intangible income that is attributed to foreign activity.

Current law also contains a general antiabuse provision whose focus is primarily on U.S. subsidiaries of foreign parents, although it applies in general to all related parties. Unlike Subpart F or the new GILTI provision, the base erosion and antiavoidance tax (BEAT) is not aimed at including income but at disallowing deductions for certain "base erosion" payments made by U.S. parents to their foreign subsidiaries that historically have been used to shift profits out of the United States. BEAT imposes a minimum tax which is equal to 5%, in 2018, of the sum of taxable income and base erosion payments on corporations with average annual gross receipts of at least $500 million over the past three tax years and with deductions attributable to outbound payments exceeding 3% of overall deductions.62

Social Insurance and Retirement Payroll Taxes

Payroll taxes are used to fund specific programs, largely Social Security and Medicare.63 Social Security and Medicare taxes are generally paid at a combined rate of 15.3% of wages, with 7.65% being paid by the employee and employer alike.64

The Social Security part of the tax, or the old age, survivors, and disability insurance (OASDI) tax, is 6.2% for both employees and employers (12.4% in total).65 In 2018, the tax applies to the first $128,400 in wages. This wage base is adjusted annually for inflation.

The Medicare portion of the tax, or the Medicare hospital insurance (HI) tax, is 1.45% for both employees and employers (2.9% in total).66 There is no wage cap for the HI tax (the Medicare HI tax applies to all wage earnings). Certain higher-income taxpayers may be subject to an additional HI tax of 0.9%. For married taxpayers filing jointly, combined wages above $250,000 are subject to the additional 0.9% HI tax.67 The threshold for single and head of household filers is $200,000. These threshold amounts are not indexed for inflation.

Employers may also be subject to a federal unemployment insurance payroll tax.68 This tax is 0.6% on the first $7,000 of wages.69 Federal unemployment insurance payroll taxes are used to pay for the administrative costs of the unemployment insurance (UI) program. State UI taxes generally pay for UI benefits.70

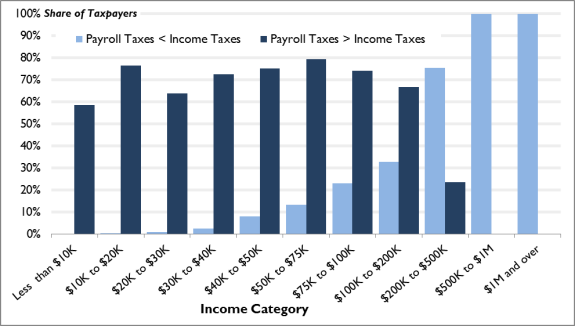

Most taxpayers pay more in payroll taxes than income taxes. The JCT projects that in 2018, 67% of tax units will pay more in payroll taxes than income taxes (see Figure 4).71 Most low- and middle-income taxpayers pay more in payroll taxes than in income taxes. Nearly all taxpayers with incomes of $30,000 or less pay more in payroll taxes than income taxes. Up through the $100,000 to $200,000 income category, the share of taxpayers paying more in payroll taxes than income taxes exceeds the share of taxpayers paying more in income taxes than payroll taxes.

Estate and Gift Taxes

Upon death, an individual's estate may be subject to tax.72 The base of the federal estate tax is generally property transferred at death, less allowable deductions and exemptions. An unlimited marital deduction is allowed for property transferred to a surviving spouse. Other allowable deductions include estate administration expenses and charitable bequests. The effective estate tax exemption is $11.2 million for 2018.73 The value of the estate over the exemption amount is generally taxed at a rate of 40%.74

The federal gift tax operates alongside the estate tax to prevent individuals from avoiding the estate tax by transferring property to heirs before dying. For 2018, the first $15,000 of gifts from one individual to another is excluded from taxation and does not apply to the lifetime exemption.75 Any amount over this annual exclusion lowers the effective lifetime estate tax exemption.

The gift tax and estate tax are unified in that the same lifetime exemption amount applies to both taxes ($11.2 million in 2018). Being unified, taxable gifts reduce the exemption amount that is available for estate tax purposes. The gift tax rate is 40%, the same as the top rate for the estate tax, for gifts beyond the exemption amount.

Few taxpayers pay the estate tax. Through 2025, an estimated 0.06% of decedents will pay the estate tax.76 The estate tax is also progressive, up to the very top of the income distribution. For taxpayers in the 95th to 99th percentile, the estate tax has been estimated to be 0.2% of cash income in 2016.77 For taxpayers in the top 1% and top 0.1% of the income distribution, the estate tax has been estimated to be 0.5% of cash income in 2016. The concentration in upper income categories will increase with the higher temporary exemption levels in effect in 2018.

Excise Taxes

Excise taxes are levied on the consumption of goods and services rather than income. Unlike sales taxes, they apply to particular commodities, rather than to broad categories. Historically, the federal government has levied excise taxes, but not a broad-based sales tax, instead leaving sales taxes to the states as a revenue source.

Federal excise taxes are levied on a variety of products.78 The collection point of the tax varies across products. For some goods, taxes are collected at the production level. Other excise taxes are collected on retail sales. In terms of receipts, the single largest tax is the excise tax on gasoline.79 Other prominent excise taxes are those on diesel and other fuels; trucks, trailers, and tractors; aviation-related taxes and fees;80 excise taxes on beer, wine, and distilled spirits;81 taxes on tobacco products; Affordable Care Act (ACA) taxes and fees82 (e.g., insurance provider fee,83 branded pharmaceuticals fee); and taxes on firearms and ammunition.84

Most federal excise taxes are paid into federal trust funds devoted to specific federal activities, as opposed to remaining in the federal budget's general fund. Estimates for 2018 indicate that of the $108 billion in anticipated excise tax revenue, approximately 61% will support trust funds, with the remainder being general fund revenue.85 The largest trust fund is the Highway Trust Fund. Devoted revenue sources include excise taxes on fuels, trucks, and tires. Aviation-related excise taxes support the Airport and Airway Trust Fund, the second largest of the excise-tax-supported trust funds.86 General fund excise taxes include taxes on alcohol and tobacco and ACA-related excise taxes.

Excise taxes can result in consumers paying higher prices for goods and services. Overall, households from the lower part of the income distribution tend to pay a larger share of their income in excise taxes than higher-income households.87 Thus, taken as a whole, federal excise taxes are generally believed to be regressive. The degree of regressivity can vary for different types of excise taxes. For example, tobacco excise taxes are estimated to be more regressive than aviation-related excise taxes.88

Tax Statistics

Taxes as a Share of the Economy

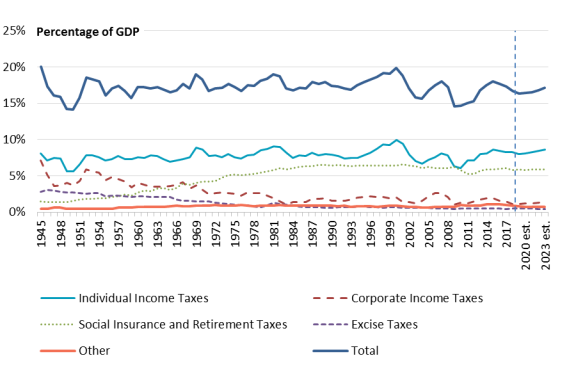

Federal revenues are derived from several sources and have collectively ranged from roughly one-fifth to one-seventh the size of the economy. Figure 5 displays total federal tax revenues and major sources of federal tax revenue as percentages of gross domestic product (GDP) since 1945. For 2018, it is estimated that revenues will be 16.7% of GDP, slightly below the post-World War II average of 17.2% of GDP.

Since the mid-1940s, the individual income tax has been the most important single source of federal revenue (business income may also be taxed under the individual income tax system, as discussed above in "The Individual Income Tax"). Between 2000 and 2010, however, the individual income tax receipts decreased relative to the size of the economy, falling from nearly 10% of GDP in 2000 to just over 6% in 2010. Individual income tax receipts have subsequently increased, and are estimated to be 8.3% of GDP in 2018. Over time, the corporate income tax has fallen from the second- to the third-most important source of revenue. In the late 1960s, corporate taxes were replaced by social insurance and retirement taxes as the second-leading revenue source. Excise taxes and estate and gift taxes have also decreased as a share of GDP over time.

Composition of Tax Revenue

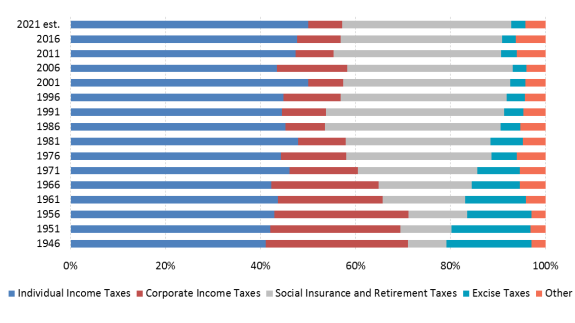

The changing shares of federal revenues over time are more clearly shown in Figure 6. For example, the corporate income tax accounted for roughly 30% of federal revenue in 1946, but 9% in 2016.89 As a share of total revenues, the corporate income tax is projected to decline further, to roughly 7%, by 2021. Excise tax revenue is roughly 3% of federal receipts, down from nearly 18% in 1946. In contrast, receipts for social insurance and retirement taxes have risen post-World War II with the enactment of Social Security and Medicare and are now the second-largest source of federal receipts at approximately 35% of federal revenue.

The Distribution of the Tax Burden

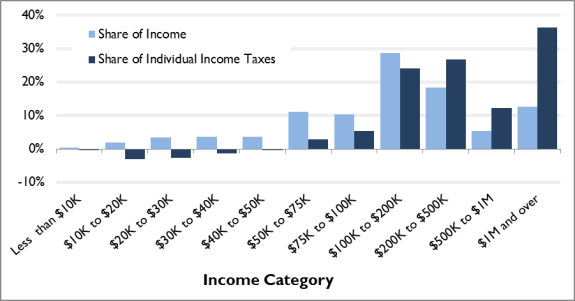

The U.S. individual income tax system is generally progressive. As shown in Figure 7, taxpayers with lower incomes tend to have a proportionally smaller share of the overall individual income tax burden. JCT projections indicate that in 2018, taxpayers in lower income categories will, on average, have a negative share of individual income taxes.90 Thus, on average, these groups receive more in refundable tax benefits than they pay in federal individual income taxes. For taxpayers in income groups above $200,000, projections for 2018 show that their share of taxes paid exceeds their share of income earned. About 50% of taxpayers fall into an income category below $50,000. In contrast, less than 7% of filers fall into an income category above $200,000. Since higher-income taxpayers pay a larger share of taxes than they earn in income, the system is generally progressive, and causes after-tax income to be more equally distributed than before-tax income.

The tax system as a whole is progressive, but not as progressive as the individual income tax system. Payroll taxes and excise taxes tend to be regressive, with higher average tax rates paid by taxpayers in lower income groups. Thus, taken together in evaluating the federal tax system as a whole, payroll taxes and excise taxes offset some of the progressivity of the individual income tax.91

|

Figure 7. Shares of Income and Individual Income Taxes by Income Category, |

|

|

Source: CRS and Joint Committee on Taxation. |

International Comparisons

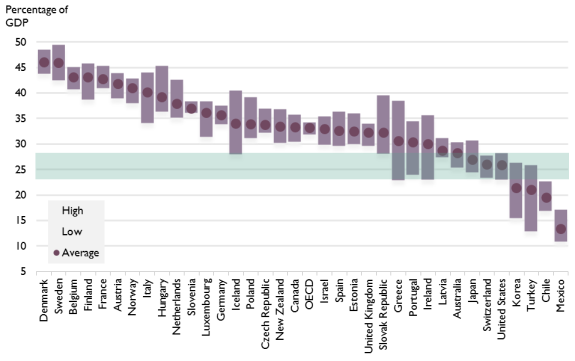

How the U.S. tax system compares to those in other countries is a perennial tax policy question. As shown in Figure 8, total U.S. taxes as a percentage of GDP has historically been below the average for OECD countries. Four countries have tended to have lower taxes as a percentage of GDP than the United States, with most others tending to have higher taxes relative to the size of the economy. Note that such a direct comparison can be difficult to interpret, as it does not take into account government spending that reflects each country's policy preferences or deficit/surplus levels that provide more context.

|

Figure 8. Government Tax Revenue as a Percentage of GDP OECD Countries, 1987-2016 |

|

|

Source: OECD Revenue Statistics. Note: Government revenue includes all federal, state, and local tax collections. |

Table 3 provides this additional context for the United States and the other major democratic countries in the G-7. Among the G-7 countries, the United States has both the lowest revenue and spending as a percentage of GDP and the second-highest deficit level in 2017.92

|

Government Revenues as a % of GDP |

Government Expenditures as a % of GDP |

Surplus/Deficit as a % of GDP |

|

|

Canada |

38.5 |

40.1 |

-1.6 |

|

France |

53.2 |

56.1 |

-2.9 |

|

Germany |

44.9 |

43.8 |

1.1 |

|

Italy |

47.0 |

49.2 |

-2.1 |

|

Japan |

33.9 |

38.8 |

-4.8 |

|

United Kingdom |

38.2 |

40.5 |

-2.3 |

|

United States |

33.0 |

37.6 |

-4.6 |

Source: OECD Economic Outlook Annex Tables.

Note: Government revenue and expenditures includes all federal, state, and local collections (tax and non-tax) and spending.

Concluding Remarks

The U.S. federal tax system in 2018 looks substantively different than it did in 2017. As taxpayers adjust to the federal tax system in place for 2018, Congress may consider further changes to the federal tax system. Given the scope and magnitude of the changes enacted in P.L. 115-97, tax policy for the remainder of the 115th Congress may build on or be related to this legislation. Over the longer term, as tax policies that were temporary in P.L. 115-97 expire, and delayed tax policies begin to phase in, Congress may choose to consider whether expirations, phase-ins, or other delayed policies in P.L. 115-97 should be modified.

This report provides an overview of the federal tax system, as in effect in 2018. Information on taxes relative to the size of the economy, the distribution of the tax burden, and how the U.S. tax system compares to tax systems globally may provide context for consideration of future tax policy changes.