Tax Deductions for Individuals: A Summary

Every tax filer has the option to claim deductions when filing their income tax return. Deductions serve four main purposes in the tax code: (1) to account for large, unusual, and necessary personal expenditures, such as extraordinary medical expenses; (2) to encourage certain types of activities, such as homeownership and charitable contributions; (3) to ease the burden of taxes paid to state and local governments; and (4) to adjust for the expenses of earning income, such as unreimbursed employee expenses.

Some tax deductions can be taken by individuals even if they do not itemize. These deductions are commonly referred to as above-the-line deductions, because they reduce a tax filer’s adjusted gross income (AGI, or the line). In contrast, itemized and standard deductions are referred to as below-the-line deductions, because they are applied after AGI is calculated to arrive at taxable income.

Tax filers have the option to either claim a standard deduction or itemize certain deductions. The standard deduction, which is based on filing status, is, among other things, intended to reduce the complexity of paying taxes, as it requires no additional documentation. Alternatively, tax filers claiming itemized deductions must list each item separately on their tax return and be able to provide documentation that the expenditures being deducted have been made. Only tax filers with deductions that can be itemized in excess of the standard deduction find it worthwhile to itemize. Whichever deduction the tax filer claims—standard or itemized—the amount is subtracted from AGI.

Deductions differ from other tax provisions that can reduce a tax filer’s final tax liability. Deductions reduce final tax liability by a percentage of the amount deducted, because deductions are calculated before applicable marginal income tax rates. In contrast, tax credits generally reduce an individual’s tax liability directly, on a dollar-for-dollar basis, because they are incorporated into tax calculations after marginal tax rates are applied.

Some deductions can only be claimed if they meet or exceed minimum threshold amounts (usually a certain percentage of AGI) in order to simplify tax administration and compliance. In addition, some deductions are subject to a cap (also known as a ceiling) in benefits or eligibility. Caps are meant to reduce the extent that tax provisions can distort economic behavior, limit revenue losses, or reduce the availability of the deduction to higher-income tax filers.

Because some tax filers and policymakers may not have detailed knowledge of tax deductions, this report first describes what they are, how they vary in their effects on reducing taxable income, and how they differ from other provisions (e.g., exclusions or credits). Next, a discussion concerning the rationale for deductions as part of the tax code is provided. Because some deductions are classified as tax expenditures, or losses in federal revenue, they might be of interest to Congress from a budgetary perspective. The final section of this report includes tables that summarize each individual tax deduction, under current law. Many of these deductions are part of the permanent income tax code. The Consolidated Appropriations Act (P.L. 114-113) extended several temporary provisions through 2016 (for the 2017 tax filing season).

Tax Deductions for Individuals: A Summary

Jump to Main Text of Report

Contents

- Calculating the Individual Income Tax

- What Are Tax Deductions?

- Above-Versus-Below-the-Line Deductions

- Itemized Versus Standard Deductions

- Standard Deduction

- Itemized Deductions

- Pease Limit on Itemized Deductions for Higher-Income Tax Filers

- Summary of Individual Tax Deductions

Figures

Summary

Every tax filer has the option to claim deductions when filing their income tax return. Deductions serve four main purposes in the tax code: (1) to account for large, unusual, and necessary personal expenditures, such as extraordinary medical expenses; (2) to encourage certain types of activities, such as homeownership and charitable contributions; (3) to ease the burden of taxes paid to state and local governments; and (4) to adjust for the expenses of earning income, such as unreimbursed employee expenses.

Some tax deductions can be taken by individuals even if they do not itemize. These deductions are commonly referred to as above-the-line deductions, because they reduce a tax filer's adjusted gross income (AGI, or the line). In contrast, itemized and standard deductions are referred to as below-the-line deductions, because they are applied after AGI is calculated to arrive at taxable income.

Tax filers have the option to either claim a standard deduction or itemize certain deductions. The standard deduction, which is based on filing status, is, among other things, intended to reduce the complexity of paying taxes, as it requires no additional documentation. Alternatively, tax filers claiming itemized deductions must list each item separately on their tax return and be able to provide documentation that the expenditures being deducted have been made. Only tax filers with deductions that can be itemized in excess of the standard deduction find it worthwhile to itemize. Whichever deduction the tax filer claims—standard or itemized—the amount is subtracted from AGI.

Deductions differ from other tax provisions that can reduce a tax filer's final tax liability. Deductions reduce final tax liability by a percentage of the amount deducted, because deductions are calculated before applicable marginal income tax rates. In contrast, tax credits generally reduce an individual's tax liability directly, on a dollar-for-dollar basis, because they are incorporated into tax calculations after marginal tax rates are applied.

Some deductions can only be claimed if they meet or exceed minimum threshold amounts (usually a certain percentage of AGI) in order to simplify tax administration and compliance. In addition, some deductions are subject to a cap (also known as a ceiling) in benefits or eligibility. Caps are meant to reduce the extent that tax provisions can distort economic behavior, limit revenue losses, or reduce the availability of the deduction to higher-income tax filers.

Because some tax filers and policymakers may not have detailed knowledge of tax deductions, this report first describes what they are, how they vary in their effects on reducing taxable income, and how they differ from other provisions (e.g., exclusions or credits). Next, a discussion concerning the rationale for deductions as part of the tax code is provided. Because some deductions are classified as tax expenditures, or losses in federal revenue, they might be of interest to Congress from a budgetary perspective. The final section of this report includes tables that summarize each individual tax deduction, under current law. Many of these deductions are part of the permanent income tax code. The Consolidated Appropriations Act (P.L. 114-113) extended several temporary provisions through 2016 (for the 2017 tax filing season).

This report provides an overview of income tax deductions for individuals. A tax deduction reduces the amount of a tax filer's income that is subject to taxation, ultimately reducing the tax filer's tax liability. Every tax filer has the option to claim deductions when filing their income tax return. However, some tax filers and policymakers may not have detailed knowledge of tax deductions, including future changes in the requirements to claim certain deductions. In addition, tax deductions may be of interest to Congress from a budgetary perspective, as some deductions are classified as tax expenditures, and result in losses in federal revenue.

This report first describes what tax deductions are, how they vary in their effects on reducing taxable income, and how they differ from other provisions (e.g., exclusions or credits). Next, it discusses the rationale for deductions as part of the tax code. The final section includes tables that summarize each individual tax deduction, under current law.

This report focuses on the standard treatment of tax deductions for individuals under the individual income tax code. As such, the following are beyond the scope of this report:

- the different treatment of deductions under the alternative minimum tax for individuals,1

- tax deductions for businesses under the individual income tax code,2 and

- options for reforming itemized deductions.3

Calculating the Individual Income Tax

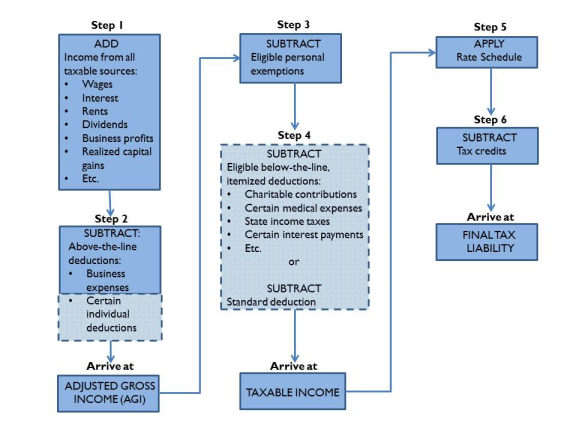

To understand what tax deductions are, it is helpful to first understand how a tax filer calculates individual income tax liability. Figure 1 provides an overview of how a tax filer calculates his or her federal tax liability.4 To calculate taxes owed (tax liability), tax filers first add up all of their forms of income (see step 1 in Figure 1) to calculate their gross income. Next, the tax filer subtracts any above-the-line deductions to calculate their adjusted gross income, or AGI (step 2). AGI is often referred to as "the line." Then, the tax filer subtracts personal exemptions, or fixed dollar amounts per spouse and dependent child (step 3). The tax filer then subtracts the greater of either the sum of all of their below-the-line, or itemized deductions, or the standard deduction, which is a fixed amount based on filing status, in order to arrive at taxable income (step 4). The marginal tax rates are applied to taxable income (step 5) to arrive at a preliminary tax liability. Finally, tax credits are subtracted from preliminary tax liability (step 6) to arrive at final tax liability. The provisions in Figure 1 surrounded by dotted lines are covered in this report.

|

Figure 1. Computation of Federal Personal Income Tax Liability |

|

|

Source: Harvey S. Rosen, Public Finance, 7th ed. (New York, NY: McGraw-Hill Irwin, 2005), p. 360. |

What Are Tax Deductions?

Simply stated, deductions reduce taxable income. Each deduction reduces tax liability by the amount of deduction times the tax filer's marginal tax rate. In contrast, a tax credit reduces tax liability on a dollar-for-dollar basis because it would be applied after the marginal tax rate schedule. An individual in a 35% tax bracket would receive a reduction in taxes of $35 for each $100 deduction while an individual in a 25% tax bracket would receive a reduction in taxes of $25 for each $100 deduction. Hence, the same deduction can be worth different amounts to different tax filers depending on their marginal tax bracket. The tax savings from deductions are generally equal to the tax filer's marginal tax rate times the amount of the deduction. So higher-income tax filers typically benefit more than lower-income tax filers from deductions.

Deductions serve four main purposes in the tax code.5 First, they can account for large, unusual, and necessary personal expenditures, such as the deduction for extraordinary medical expenses. Second, they are used to encourage certain types of activities, such as homeownership and charitable contributions. Third, they account for and ease the burden of paying for nonfederal forms of taxes, such as state and local taxes. Fourth, deductions adjust for the expenses of earning income, such as deductions for work-related employee expenses.

The following sections define each form of deduction and explain in greater detail how deductions are used in the calculation of an individual's tax liability.

Above-Versus-Below-the-Line Deductions

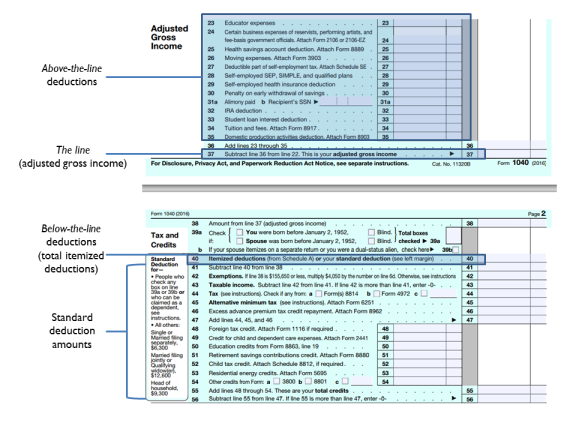

To arrive at final tax liability, all taxpayers may be able to claim above-the-line deductions whether they claim itemized deductions or the standard deduction. Each of these deductions has a specific line on the Form 1040 (e.g., line 23 for teacher classroom expenses). Figure 2 shows how tax deductions appear on the IRS Form 1040.

|

Figure 2. Above- Versus Below-the-Line Deductions on the IRS Form 1040 |

|

|

Source: Internal Revenue Service, 2016 Form 1040, at http://www.irs.gov/pub/irs-pdf/f1040.pdf. |

These deductions are commonly referred to as above-the-line deductions, because they reduce a tax filer's AGI (the line). Above-the-line deductions are sometimes also called adjustments to income, because they generally represent costs incurred to earn income. In contrast, itemized and standard deductions are sometimes referred to as below-the-line deductions, because they are applied after AGI is calculated to arrive at taxable income.

Above-the-line deductions may provide additional benefits to some tax filers seeking to claim certain tax preferences. A number of tax provisions have a phaseout of benefits as income increases. The higher the AGI, the less likely the tax filer will be able to claim a larger value of the tax preference. Tax deductions that lower AGI increase the likelihood that the tax filer will be able to claim a larger value of the tax preference.

Itemized Versus Standard Deductions

As previously discussed, tax filers have the option to claim either a standard deduction or the sum of their itemized deductions. Whichever deduction the tax filer claims—standard or itemized—the deduction amount is subtracted from AGI to arrive at final tax liability.

Standard Deduction

The standard deduction is a fixed amount, based on filing status, available to all taxpayers. In contrast to those itemizing their deductions, tax filers do not have to provide additional documentation in order to claim the standard deduction.

The standard deduction was introduced into the federal tax code with the passage of the Individual Income Tax Act of 1944 (P.L. 78-315) primarily to simplify tax administration and compliance. At the time of passage, it was noted that taxpayers generally had little idea about what deductions were allowable and few taxpayers kept accurate records. Thus, the enactment of the standard deduction reduced excessive unsupportable claims of deductions, although at the same time it permitted many taxpayers to take a deduction in excess of what they would have been allowed if they had been required to itemize their deductions.

Today it is also viewed as performing a social welfare purpose. The social welfare purpose of the standard deduction was introduced with the minimum standard deduction in the Revenue Act of 1964 (P.L. 88-272). Under this minimum standard deduction provision, a taxpayer was assured a minimum amount of deductions from his or her income. The personal exemptions combined with the standard deduction amount are designed to remove low-income households from the tax rolls.

The calculation of the standard deduction has changed over time. In 1944, it was equal to 10% of AGI, up to a maximum of $1,000. In 1964, a minimum standard deduction was introduced as a fixed value of $200 plus $100 for each exemption with a ceiling of $1,000 if married filing jointly.6 The value of the standard deduction, including both the percent of AGI and the maximum value, was increased multiple times from 1969 to 1975. The minimum standard deduction and the deduction were merged in 1977 into a flat standard deduction of $2,200 (single) and $3,200 (married filing jointly).7 The Economic Recovery Tax Act of 1981 (P.L. 97-34) indexed standard deduction amounts for inflation, beginning in 1985.8 The standard deduction has been increased over time, such as with the Tax Reform Act of 1986 (TRA86; P.L. 99-514).

The Economic Growth and Tax Relief Reconciliation Act of 2001 (EGTRRA; P.L. 107-16) phased out part of the so-called marriage penalty associated with the federal tax code, where the standard deduction for joint filers was less than twice the single filer amount. EGTRRA increased the deduction for joint filers to 200% of singles. This provision, most recently extended by Tax Relief, Unemployment Insurance Reauthorization and Job Creation Act of 2010 (P.L. 111-312), expired in 2012. Under current law, the standard deduction for married couples filing jointly will be equal to 167% of the upper limit for singles for the 2013 tax year and beyond.9

The standard deduction amount varies depending on the filing status of the tax unit (i.e., single, married filing jointly, married filing separately, or head of household), whether the tax filer is over the age of 65, and whether the tax filer is blind.

For the 2015 tax year (2016 filing season), the inflation-adjusted standard deductions are as follows:

- $12,600 married filing jointly or surviving spouses,

- $6,300 for single tax filers and married filing separately, and

- $9,250 for tax filers who qualify as the head of a household.10

For the 2016 tax year (2017 filing season), the inflation-adjusted standard deductions are as follows:

- $12,600 married filing jointly or surviving spouses,

- $6,300 for single tax filers and married filing separately, and

- $9,300 for tax filers who qualify as the head of a household.11

In addition, there is a standard deduction available for an individual who can be claimed as a dependent on another person's tax return. For tax year 2016 (2017 filing season), the standard deduction for a dependent is generally limited to the greater of (a) $1,050 or (b) the sum of the individual's earned income for the year plus $350 (but not more than the regular standard deduction amount of $6,300 for single tax filers).12

The additional standard deductions for those aged 65 or older and those who are legally blind are increased by $1,550 if single or head of household and $1,250 if married filing jointly for tax year 2016 (2017 filing season).13 These increases apply per classification and are added above the base standard deduction amounts listed above. Thus, a 70-year-old blind and single tax filer would be eligible for a $3,100 increase ($1,550 for being 65 or older, and $1,550 for being blind) in his or her standard deduction for tax year 2016. These amounts are adjusted annually for inflation.

Itemized Deductions

Alternatively, tax filers claiming itemized deductions must list each item separately on their tax return and be able to provide documentation (i.e., in the event of an IRS audit) that the expenditures have been made.

Tax filers have been able to itemize their deductions since the Revenue Act of 1913 (P.L. 63-16), which created the first permanent federal income tax. Deductions for interest paid or unexpected casualty losses were early provisions in the federal income tax code because many businesses were sole proprietorships (i.e., pass-through entities) where the owner was personally liable for the costs of doing business. Itemized deductions have been reduced or limited in eligibility, most notably with TRA86. For example, TRA86 eliminated deductions for consumer interest and enacted more complex rules for deducting investment interest.14

Only individuals with aggregate itemized deductions greater than the standard deduction find it worthwhile to itemize. Itemized deductions are claimed on the IRS Schedule A form.15 Itemized deductions are allowed for a variety of purposes. A detailed summary of the requirements and limits for each of these provisions, and other itemized deductions, is included in Table 2, at the end of this report.

Some itemized deductions can only be claimed if they meet or exceed minimum threshold amounts (usually a certain percentage of AGI) in order to simplify tax administration and compliance. For example, a tax filer must meet a certain threshold (or a floor) to deduct a casualty, disaster, or theft loss.

Certain itemized deductions are treated as miscellaneous itemized deductions, which are allowed only to the extent that their total exceeds 2% of the individual tax filer's AGI. This floor makes it simpler for a tax filer to choose whether he or she would be better off itemizing the deductions or choosing to claim the standard deduction, and it helps to ensure that the IRS is only reviewing documentation of fewer, larger events rather than many, smaller events. Any restriction placed upon an itemized deduction generally applies prior to the 2% AGI floor.16 An example of an expense subject to the combined 2% of AGI floor for miscellaneous deductions is the 50% reduction for unreimbursed meals while traveling away from home on business.

In addition, some deductions are subject to a cap (also known as a ceiling) in benefits or eligibility. Caps are meant to reduce the extent that tax provisions can distort economic behavior, limit revenue losses, or reduce the availability of the deduction to higher-income tax filers. For example, the home mortgage interest itemized deduction is limited to mortgage debt in the amount of up to $1 million for married couples filing jointly ($500,000 for individuals or married filing separate).17 This ceiling is intended to limit incentives for higher-income tax filers to finance their home purchases with deductible interest.

Pease Limit on Itemized Deductions for Higher-Income Tax Filers

There is a limitation on the value of itemized deductions that certain, higher-income tax filers can claim. The limitation on itemized deductions was initially included in the Omnibus Budget Reconciliation Act of 1990 (P.L. 101-508), drafted by Representative Donald Pease of Ohio. Commonly referred to as "Pease" by tax analysts, it effectively increases taxes on high-income tax filers without explicitly increasing tax rates.

Pease's limitations are triggered by an AGI threshold.18 The number or total amount of itemized deductions claimed by a tax filer does not determine whether he or she is subject to Pease. Pease affects tax filers above the inflation-adjusted AGI thresholds who itemize deductions. For these tax filers, the total of certain itemized deductions is reduced by 3% of the amount of AGI exceeding the threshold.19 The total reduction, however, cannot be greater than 80% of the deductions (and the tax filer always has the option of taking the standard deduction). Consequently, the effective marginal tax rate for these tax filers will be 3% higher than their statutory marginal tax rate.20

Pease was in effect from 1991 to 2009, and was fully repealed from 2010 to 2012.21 The Economic Growth and Tax Relief Reconciliation Act of 2001 (P.L. 107-16) included the phased-in repeal of Pease between 2006 and 2009. Pease was scheduled to be reinstituted beginning with the 2011 tax year, but the reintroduction was postponed until the 2013 tax year by the Tax Relief, Unemployment Insurance Reauthorization, and Job Creation Act of 2010 (P.L. 111-312).

The American Taxpayer and Relief Act of 2012 (ATRA; P.L. 112-240) restored Pease for tax years 2013 and beyond.

For the 2016 tax year (2017 filing season), the Pease threshold amounts are adjusted to

- $259,400, if single and not married;

- $285,350, if head of household;

- $311,300, if married filing jointly or a surviving spouse; or

- $155,650, if married, filing separately.22

Summary of Individual Tax Deductions

|

Abbreviations Used in S: Single tax filer MFJ: Married, filing jointly MFS: Married, filing separately HOH: Head of household filer SS: Surviving spouse filer |

Table 1 and Table 2 provide a summary of above- and below-the-line tax deductions, respectively.23 The first column provides a reference to where the provision can be found on the Form 1040 (if an above-the-line deduction) or on the Schedule A form (if a below-the-line, itemized tax deduction). The provision column contains a reference to where the provision can be found in the Internal Revenue Code (IRC), which is Title 26 of the U.S. Code. A brief summary of the provision follows in the adjacent column. When applicable, annual limits (whether they are floors or ceilings) and income limits and phaseouts are provided.24 The last column provides the tax expenditure amount for FY2016 and FY2017.25

Tax expenditures are defined under the Congressional Budget and Impoundment Control Act of 1974 (P.L. 93-344) as "revenue losses attributable to provisions of the Federal tax laws which allow a special exclusion, exemption, or deduction from gross income or which provide a special credit, a preferential rate of tax, or a deferral of tax liability."26 Tax expenditure estimates are based on current law, which does not assume extensions of temporary provisions that are subject to expire within the time period observed. Not all tax deductions have JCT tax expenditure estimates, as some provisions are estimated to result in revenue losses less than $50 million per fiscal year (JCT's de minimus level). In addition, some tax deductions are not considered tax expenditures for various, other reasons.27 For example, the deduction for uncompensated employee expenses is considered an appropriate measure to adjust a tax filer's AGI.

|

1040 |

Provision |

Summary of |

Annual Deduction Limit |

Income Limits and Phaseouts |

Tax Expenditure, in Billionsb |

|

23 |

Educator expenses |

An eligible employee of a public (including charter) and private elementary or secondary school may deduct ordinary and necessary expenses paid in connection with books, supplies, equipment (including computers and software), and other materials used in the classroom. Professional development expenses are also considered eligible in 2016 and beyond. The annual deduction amount of $250 is indexed for inflation in 2016 and beyond. |

$250 ($500 if MFJ and both spouses are eligible educators, but not more than $250 each). |

None |

FY2016: $0.2 FY2017: $0.2 |

|

24 |

Certain reimbursed business expenses of reservists, performing artists, and fee-basis government officials |

Certain reimbursed business expenses of National Guard and Reserve members who traveled more than 100 miles from home to perform their services; performing arts-related expenses; and business expenses of fee-basis state or local government officials. |

None |

None |

FY2016: $0.1 FY2017: $0.1 |

|

25 |

Health savings account (HSA) contri-butions |

Eligible individuals can establish Health Savings Accounts (HSAs) and fund these accounts when they have qualifying high deductible health insurance (insurance with a deductible of at least $1,300 for single coverage and $2,600 for family coverage, plus other criteria) and no other health care coverage, with some exceptions. |

2015 and 2016: $3,350 for individual plans and $6,650 for family plans; individuals aged 55 or older can contribute an additional $1,000. |

None |

FY2016: $2.2 FY2017: $2.5 |

|

25 |

Archer medical savings account (MSA) contributions |

Contributions toward Archer medical savings account (MSAs). Archer MSAs are tax-exempt trust or custodial accounts, established with a U.S. financial institution, used to save money exclusively for future medical expenses. Individuals must meet the following requirements to be eligible for an Archer MSA, including: having a high deductible health plan (HDHP); having no other health or Medicare coverage; and being either a small employer or self-employed (or the spouse of a self-employed individual). |

(1) Cannot exceed a taxpayer's net earned income from the business in which the health insurance plan was established. |

None |

[dm] |

|

26 |

Work-related moving expenses |

Unreimbursed moving expenses incurred during the taxable year in connection with the commencement of work by the taxpayer as an employee or as a self-employed individual at a new principal place of work that is at least 50 miles farther from the prior residence. |

None |

None |

NA |

|

28 |

Retirement plan contributions for the self-employed |

A self-employed individual may deduct contributions to a Simplified Employment Plan (SEP), Savings Incentive Match Plan for Employees of Small Employers (SIMPLE), or Keogh plan. |

Contributions cannot exceed an amount equal to 25% of pay up to a maximum amount indexed to inflation: SEP and Keogh: $53,000 (2015 and 2016), SIMPLE: $12,500 (2015 and 2016). Participants aged 50 and older can make additional contributions of up to $3,000 (2015 and 2016). |

None |

NA |

|

29 |

Health insurance premiums for the self-employed |

A self-employed individual may deduct the premium costs of health insurance or long-term care insurance as long as he or she is not eligible to participate in a plan, in a given month, sponsored by his or her employer or the spouse's employer. |

(1) Cannot exceed a taxpayer's net earned income from the business in which the health insurance plan was established, less the deductions for 50% of the self-employment tax and any contributions to qualified pension plans. (2) If a self-employed individual claims an itemized deduction for medical expenses, those expenses must be reduced by any deduction for health insurance premiums. |

None |

FY2016: $5.7 FY2017: $5.9 |

|

31 |

Alimony paid |

Alimony and separate maintenance payments are income to the recipient and are deductible by the payor if certain requirements are met [U.S.C. §62(a)(10), 71, and 215]. Child support is not tax deductible. |

None |

None |

NA |

|

32 |

Retirement savings, including traditional individual retirement accounts (IRAs) |

Taxpayers may deduct qualified retirement contributions, such as a 401(k) plan or a traditional IRA, generally limited to $5,500 (increased by $1,000 of catch-up contributions for taxpayers aged 50 and over). ATRA permanently expanded the availability of "in-plan Roth conversions," allowing virtually all traditional employer-sponsored retirement account balances [like funds in a 401(k) plan] to be transferred to employer-sponsored Roth accounts [like Roth 401(k) plans]. By electing to convert a non-Roth account to a Roth account, an employee pays tax at the time the funds are rolled over or converted. However, when an employee ultimately withdraws funds from these Roth accounts they will not be subject to taxation.c |

The lesser of $5,500 or 100% of compensation. 2015 and 2016: $5,500 ($6,500 if over 50). |

For active participants in certain pension plans, the deduction amount is phased out proportionately over the following inflation-adjusted AGI ranges: MFJ: $98,000-$118,000 (2015 and 2016), Taxpayers whose spouses are active participants: $184,000-$194,000 (2016), Other taxpayers: $61,000-$71,000 (2015 and 2016). |

FY2016: $15.1 FY2017: $16.1 |

|

33 |

Interest on Education Loans |

Interest paid on a qualified student loan is deductible in the year that the interest was paid. |

$2,500 |

Inflation-adjusted phaseout: MFJ: $130,000-$160,000 (2015 and 2016), Other taxpayers: $65,000-$80,000 (2014 and 2015). |

FY2016: $2.2 FY2017: $2.3 |

|

34 |

Qualified Tuition and Related Expenses |

Includes costs related to qualified tuition, fees, room and board, books, and supplies. This "tax extender" provision expires after the 2016 tax year (2017 filing season). |

Up to $4,000 or $2,000, depending on AGI. |

Taxpayers can deduct up to $4,000 or up to $2,000 of qualified tuition and related expenses depending on their AGI fell between the following ranges in 2015 or 2016: $65,000 or less ($130,000 MFJ): $4,000. $65,001-$80,000 ($160,000 MFJ): $2,000. $80,000+ ($160,000+ MFJ): $0. |

FY2016: NA FY2017: NA |

Source: U.S. Congress, Joint Committee on Taxation, Estimates of Federal Tax Expenditures, For Fiscal Years 2016-2020, 114th Cong., 1st sess., January 30, 2017, JCX-3-17 (Washington: GPO, 2017), at https://www.jct.gov/publications.html?func=startdown&id=4971.; Internal Revenue Service (IRS), 1040 Instructions 2016, at https://www.irs.gov/pub/irs-prior/i1040gi—2016.pdf; IRS, 1040 Instructions 2015, at https://www.irs.gov/pub/irs-prior/i1040gi—2015.pdf; IRS, Internal Revenue Bulletin No. 2015-44, November 2, 2015, at https://www.irs.gov/pub/irs-drop/rp-15-53.pdf; and IRS, Internal Revenue Bulletin No. 2014-47, November 17, 2014, at http://www.irs.gov/pub/irs-drop/rp-14-61.pdf.

Notes:

a. Line numbers refer to the 2016 Form 1040.

b. Tax expenditures estimates are for individuals only, not corporations. Estimates below JCT's de-minimus amount of $50 million over FY2016-FY2020, as per its January 2017 estimates, are denoted by [dm]. Provisions without a JCT tax expenditure amount are denoted by NA.

c. For more information on changes to the tax treatment of IRAs, see the archived CRS Report R42894, An Overview of the Tax Provisions in the American Taxpayer Relief Act of 2012, by Margot L. Crandall-Hollick.

|

Schedule A Linea |

Provision |

Summary of |

Annual Deduction |

Income Limits and Phaseouts |

Tax Expenditure, in Billionsb |

|

1 |

Medical and dental expenses |

Includes the diagnosis, cure, mitigation, treatment, or prevention of disease, or for the purpose of affecting any structure or function of the body; lodging and transportation costs related to essential medical care; qualified long-term care services; insurance covering medical care for any qualified long-term care insurance contract; and prescribed drugs. |

Expenses are deductible only if they exceed the floor of 10% of adjusted gross income (AGI). |

None |

FY2016: $10.0 FY2017: $10.1 |

|

5 and 7 |

State and local nonbusiness, income, sales, and personal property taxes |

Taxpayers who itemize can choose between deducting either state and local income taxes or sales taxes, but not both. State and local income taxes are withheld from wages during the year, as they appear on Form W-2. Nonbusiness state or local property taxes are also deductible. |

None |

None |

FY2016: $65.4 FY2017: $69.3 |

|

6 |

Real estate taxes |

Tax filers can claim an itemized deduction for property taxes paid on owner-occupied residences. |

None |

None |

FY2016: $31.2 FY2017: $33.3 |

|

8 |

Federal estate tax on income in respect of a decedent (IRD) |

The IRS allows any recipient of current or future IRD to deduct any properly allocable expenses against the income that was not claimed on the decedent's final tax return for estate tax purposes. Common items include fiduciary fees, commissions paid to dispose of assets, and state income taxes. |

None |

None |

NA |

|

10 and 11 |

Home mortgage interest and other provisions related to home-ownership |

Interest paid on an eligible mortgage secured by a principal or secondary residence is deductible. Interest can also be deducted on home equity loans. The sum of the acquisition indebtedness and home equity debt cannot exceed the fair market value of the home(s). Home equity debt means any loan whose purpose is not to acquire, to construct, or substantially to improve a qualified home, or any loan whose purpose was to substantially improve a qualified home but exceeds the home acquisition debt limit. |

Mortgage interest paid on primary and secondary residences are deductible up to: MFJ: the first $1,000,000 of a mortgage. Other taxpayers: the first $500,000 of a mortgage. The deduction for interest on home equity debt is limited to interest associated with the first $100,000 in home equity debt combined from a primary and secondary residence. |

None |

FY2016: $59.0 FY2017: $63.6 |

|

13 |

Home mortgage insurance premiums |

Qualified mortgage insurance premiums are deductible if the insurance policy covers home acquisition debt on a primary or secondary residence. Qualified mortgage insurance means mortgage insurance obtained from the Department of Veterans Affairs (VA), the Federal Housing Authority (FHA), the Rural Housing Administration (RHA), and private mortgage insurance as defined by the Homeowners Protection Act of 1988. This "tax extender" provision expires after the 2016 tax year (2017 filing season). |

None |

Deduction is reduced by 10% for each $1,000 a filer's income is over the following AGI thresholds: MFJ: $100,000 And completely phases out by: |

FY2016: $1.0 FY2017: $0.8 |

|

14 |

Investment interest |

Tax filers can deduct investment interest, or money borrowed to purchase taxable interests. Leftover investment interest expenses can be carried over for use in future years, without expiration. |

Interest expenses are deductible up to the amount of any net investment income. |

None |

NA |

|

16 and 18 |

Charitable contributions |

Subject to certain limitations, charitable contributions may be deducted by individuals, corporations, and estates and trusts. The contributions must be made to specific types of organizations, including scientific, literary, or educational organizations [as specified by IRC §501(c)(3)]. |

Can deduct contributions up to 50% of AGI that go to 501(c)(3) organizations. For contributions to nonoperating foundations and organizations, deductibility is limited to the lesser of 30% of the taxpayer's contribution base, or the excess of 50% of the contribution base for the tax year over the amount of contributions which qualified for the 50% deduction ceiling (including carryovers from previous years). Gifts of capital gain property to these organizations are limited to 20% of AGI. |

None |

FY2016: $55.2c FY2017: $56.9 |

|

20 |

Casualty, disaster, or theft losses |

Applies to nonbusiness property lost due to fire, storm, shipwreck, or other casualty, or from theft. The cause of the loss should be considered a sudden, unexpected, and unusual event. The loss must be sustained (e.g., without expectation of being compensated). |

Limited to losses in excess of $100 per event and 10% of AGI combined for all events. |

None |

FY2016: $0.4 FY2017: $0.4 |

|

21 |

Unreimbursed employee expenses |

Includes miscellaneous job-related unreimbursed expenses, such as travel costs, union dues, job-related education, uniforms, and subscriptions to professional journals. |

Subject to the combined expenses floor in excess of 2% of AGI. |

None |

NA |

|

22 |

Tax preparation fees |

Tax preparation fees and expenses, including the cost of tax preparation software programs and tax publications, are deductible. |

Subject to the combined expenses floor in excess of 2% of AGI. |

None |

NA |

|

23 |

Other financial and investment expenses |

Includes expenses such as investment management fees, safe deposit box rental fees, and transportation to an investment broker's or advisor's office. |

Subject to the combined expenses floor in excess of 2% of AGI. |

None |

NAd |

|

28 |

Gambling losses that offset gambling winnings |

Wagering losses are deductible only to the extent of the taxpayer's gains from similar transactions (U.S.C. §165(d); Reg Sec 1.165-10). Nonbusiness gambling losses are deductible only as itemized deductions. If gambling is conducted as a business, the losses are deductible as business losses on form Schedule C. |

Gambling losses claimed as a deduction cannot exceed winnings in the same year. |

None |

NA |

|

28 |

Impairment-related work expenses of a person with disabilities |

Qualified impairment-related work expenses are deductible. These include expenses such as prosthetics, specialized office equipment, supplies, or an attendant during work hours. |

None |

None |

NA |

Source: U.S. Congress, Joint Committee on Taxation, Estimates of Federal Tax Expenditures, For Fiscal Years 2016-2020, 114th Cong., 1st sess., January 30, 2017, JCX-3-17 (Washington: GPO, 2017), at https://www.jct.gov/publications.html?func=startdown&id=4971.; Internal Revenue Service (IRS), 1040 Instructions 2016, at https://www.irs.gov/pub/irs-prior/i1040gi—2016.pdf; IRS, 1040 Instructions 2015, at https://www.irs.gov/pub/irs-prior/i1040gi—2015.pdf; IRS, Internal Revenue Bulletin No. 2015-44, November 2, 2015, at https://www.irs.gov/pub/irs-drop/rp-15-53.pdf; and IRS, Internal Revenue Bulletin No. 2014-47, November 17, 2014, at http://www.irs.gov/pub/irs-drop/rp-14-61.pdf.

Notes:

a. Line numbers refer to the 2016 Schedule A to the Form 1040.

b. Tax expenditures estimates are for individuals only, not corporations. Estimates below JCT's de-minimus amount of $50 million over FY2016-FY2020, as per its January 2017 estimates, are denoted by [dm]. Provisions without a JCT tax expenditure amount are denoted by NA.

c. This estimate is the sum of the three different categories of charitable giving included in JCT's tax expenditures estimates that were estimated in January 2017.

d. JCT did not provide a tax expenditure estimate for this provision, as it is considered to be a negative tax expenditure (i.e., revenue net-gain).

Author Contact Information

Footnotes

| 1. |

See CRS Report R44494, The Alternative Minimum Tax for Individuals: In Brief, by Donald J. Marples. |

| 2. |

Some of the deductions reported on the Internal Revenue Service Form 1040 relate to business expenses, as some businesses are organized as pass-through entities. Pass-through entities get their name from the fact that the business's income passes through to the owner, as opposed to being claimed separately by the business. However, the tax treatment of business income through the individual tax code is beyond the scope of this report. For more information on pass-through entities, see CRS Report R43104, A Brief Overview of Business Types and Their Tax Treatment, by Mark P. Keightley. |

| 3. |

For example, see CRS Report R44771, An Overview of Recent Tax Reform Proposals, by Mark P. Keightley; CRS Report RL33755, Federal Income Tax Treatment of the Family, by Jane G. Gravelle; and CRS Report R43079, Restrictions on Itemized Tax Deductions: Policy Options and Analysis, by Jane G. Gravelle and Sean Lowry. |

| 4. |

For a more detailed description of each of these tax terms, see CRS Report RL30110, Federal Individual Income Tax Terms: An Explanation, by Mark P. Keightley and Jeffrey M. Stupak. For a general explanation of the federal tax system, see CRS Report RL32808, Overview of the Federal Tax System, by Molly F. Sherlock and Donald J. Marples. |

| 5. |

Joseph A. Pechman, Federal Tax Policy, 3rd ed. (Washington, DC: Brookings Institution Press, 1977), pp. 85-88. |

| 6. |

CRS Report 80-31, Historical Summary of Selected Features of the Individual Income Tax, by George J. Leibowitz and Jane G. Gravelle. (This archived report, last updated by Cheryl Savage Newton in 1980, is available to congressional clients upon request.) |

| 7. |

Ibid. |

| 8. |

Jon Bakija and Eugene Steuerle, "Individual Income Taxation Since 1948," National Tax Journal, vol. 44, no. 4 (December 1991), p. 453. |

| 9. |

See CRS Report R42485, An Overview of Tax Provisions Expiring in 2012, by Margot L. Crandall-Hollick, available to congressional clients upon request. |

| 10. |

See Internal Revenue Service, Internal Revenue Bulletin No. 2014-47, November 17, 2014, at http://www.irs.gov/pub/irs-drop/rp-14-61.pdf. |

| 11. |

See Internal Revenue Service, Internal Revenue Bulletin No. 2015-44, November 2, 2015, at https://www.irs.gov/pub/irs-drop/rp-15-53.pdf. |

| 12. |

For tax year 2015 (2016 filing season), the standard deduction for a dependent is generally limited to the greater of (a) $1,050 or (b) the sum of the individual's earned income for the year plus $350 (but not more than the regular standard deduction amount of $6,200 for single tax filers). |

| 13. |

For the 2015 tax year (2016 filing season), these additional standard deduction amounts are the same as the 2016 tax year (2017 filing season). |

| 14. |

See Sally Wallace, "Itemized Deductions," in Encyclopedia of Taxation and Tax Policy, ed. Joseph J. Cordes, Robert D. Ebel, and Jane G. Gravelle (Washington, DC: Urban Institute Press, 2000), p. 215. For an explanation of reforms to particular itemized tax deductions in the Tax Reform Act of 1986, see U.S. Congress, Joint Committee on Taxation, General Explanation of the Tax Reform Act of 1986, committee print, 100th Cong., 1st sess., May 4, 1687, JCS-10-87 (Washington: GPO, 1987). |

| 15. |

Internal Revenue Service, 2014 Schedule A (Form 1040), at http://www.irs.gov/pub/irs-pdf/f1040sa.pdf. |

| 16. |

Internal Revenue Code (IRC) Section 162(a). |

| 17. |

IRC §163(h). |

| 18. |

Ibid. |

| 19. |

The deductions not subject to the Pease limitation are medical and dental expenses, investment interest, qualified charitable contributions, and casualty and theft losses. |

| 20. |

The statutory tax rate is the marginal tax rate a tax filer faces based on their AGI. In contrast, the effective marginal tax rate is the net rate a taxpayer pays on an increment of income that includes all forms of taxes, including the different rate for itemized deductions under Pease. The average effective tax rate is calculated by dividing total tax liability by total gross income. |

| 21. |

For more information on the Pease limitation and sample calculations, see CRS Report R41796, Deficit Reduction: The Economic and Tax Revenue Effects of the Personal Exemption Phaseout (PEP) and the Limitation on Itemized Deductions (Pease), by Thomas L. Hungerford, available to congressional clients upon request. |

| 22. |

Internal Revenue Service, Internal Revenue Bulletin No. 2015-44, November 2, 2015, at https://www.irs.gov/pub/irs-drop/rp-15-53.pdf. |

| 23. |

For more information about each provision, please refer to the latest IRS tax guide or the specific Internal Revenue Code provision within the U.S. Code. These summary tables are not meant to be a substitute for professional tax assistance. |

| 24. |

Some provisions in the tax code are phased out (i.e., their value is reduced as income rises) for higher-income taxpayers as a way to target tax benefits on middle- and lower-income households and to limit the loss of revenue. |

| 25. |

U.S. Congress, Joint Committee on Taxation, Estimates of Federal Tax Expenditures, For Fiscal Years 2016-2020, 114th Cong., 1st sess., January 30, 2017, JCX-3-17 (Washington: GPO, 2017), at https://www.jct.gov/publications.html?func=startdown&id=4971. |

| 26. |

P.L. 93-344, Section 3(3). |

| 27. |

For a discussion of the debate over what is and what is not a tax expenditure, see Leonard E. Burman, "Is the Tax Expenditure Concept Still Relevant?," National Tax Journal, vol. 56, no. 3 (September 2003), pp. 613-627, and Donald B. Marron, "Spending in Disguise," National Affairs, no. 8 (Summer 2011), at http://www.nationalaffairs.com/publications/detail/spending-in-disguise. |