Major Agricultural Trade Issues in the 116th Congress

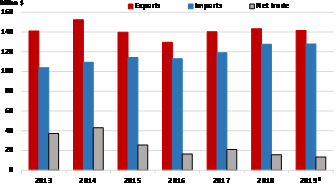

Sales of U.S. agricultural products to foreign markets absorb about one-fifth of U.S. agricultural production, thus contributing significantly to the health of the farm economy. Farm product exports, which totaled $143 billion in FY2018 (see chart below), make up about 9% of total U.S. exports and contribute positively to the U.S. balance of trade. The economic benefits of agricultural exports also extend across rural communities, while overseas farm sales help to buoy a wide array of industries linked to agriculture, including transportation, processing, and farm input suppliers.

U.S. Agricultural Trade, FY2013-FY2019

/

Source: USDA, Outlook for U.S. Agricultural Trade, AES-107, February 2019.

Notes: *denotes forecast. Data is not adjusted for inflation.

Congress has traditionally displayed a keen interest in agricultural trade issues given their importance to farmers and ranchers and to the overall economy. A major area of interest for the 116th Congress has been the loss of overseas export market shares for agricultural products due to the direction of the Trump Administration’s trade policy, which places increased emphasis on reducing the overall U.S. trade deficit. In March 2018, the Trump Administration imposed Section 232 tariffs on U.S. imports of steel and aluminum from most countries and additional Section 301 tariffs on a number of imports from China. Following these actions, Canada, China, Mexico, the European Union (EU), and Turkey imposed retaliatory tariffs on more than 800 U.S. agricultural and food product exports. In response, USDA authorized $12 billion in short-term assistance to the affected agricultural producers and commodities under its Market Facilitation Program to help mitigate the economic impact on farmers.

A number of policy developments undertaken by the Trump Administration in bilateral and regional trade agreements may affect agricultural markets as well. On the Administration’s initiative, the North American Free Trade Agreement (NAFTA) has been renegotiated and signed as the U.S.-Mexico-Canada Agreement (USMCA). This agreement is subject to legislative ratification by Canada and Mexico and approval by U.S. Congress. President Trump withdrew the United States from the Trans-Pacific Partnership (TPP) in January 2017. In March 2018, the remaining 11 countries concluded a revised version of TPP, the Comprehensive and Progressive Agreement for the Trans-Pacific Partnership (CPTPP). Signatories of CPTPP have begun to reduce tariffs and provide greater agricultural market access for imports from CPTPP signatory countries, actions that could potentially erode U.S. agricultural market shares in the region. At the bilateral level, the Trump Administration has notified Congress of its intent to begin trade negotiations with Japan (a CPTPP member), the EU, and the United Kingdom.

At the global level, and at the initiative of the United States, the World Trade Organization (WTO) recently ruled that China has subsidized its agricultural production beyond the level permitted under its WTO obligations and that China’s administration of its agricultural market access policies are inconsistent with its WTO obligations. The United States has also filed a counter notification against India at the WTO stating that India has underreported its agricultural domestic subsidies.

Several other agricultural trade issues may be of interest to Congress. For example, the proposed USMCA does not address all the issues that restrict U.S. agricultural exports to Mexico and Canada, and Southeastern U.S. produce growers have been seeking changes to trade remedy laws to address imports of seasonal produce. A key objective of U.S. trade negotiations continues to be the establishment of a common framework for approval, trade, and marketing of the products of agricultural biotechnology. U.S. farm and food interests see the potential for market expansion opportunities in Cuba, but a prohibition on private U.S. financing is generally viewed as a major obstacle to this end. Moreover, the United States has announced its intention to withdraw eligibility for the Generalized System of Preference (GSP)—which provides duty-free tariff treatment for certain products from developing countries—from Turkey and India. On another front, U.S. exports of beef, pork, and chicken continue to face bans and trade restrictions over disease outbreaks even though the bans are inconsistent with international trade protocols, among which are China’s ongoing bans on imports of U.S. beef and poultry and restrictions imposed by several foreign markets on U.S. ractopamine-fed pork.

Major Agricultural Trade Issues in the 116th Congress

Jump to Main Text of Report

Contents

- Introduction

- Overview of U.S. Agricultural Trade

- Trump Administration Trade Policy

- Retaliatory Tariffs on U.S. Agricultural Exports

- USDA's Trade-Aid Package in Response to Trade Retaliation

- U.S. Withdrawal from Trans-Pacific Partnership (TPP)

- Agricultural Trade Issues with Canada and Mexico

- U.S.-Mexico-Canada Agreement (USMCA)

- U.S. Dairy Exports to Canada

- U.S.-Canada Dispute Regarding the Sale of Wine in Grocery Stores

- Other North American Trade Issues

- Import Competition of Seasonal Produce from Mexico

- Withdrawal of the U.S.-Mexico Tomato Suspension Agreement

- U.S.-Mexico Sugar Suspension Agreements

- Other Major Trade Issues

- Agricultural Biotechnology

- Geographical Indications (GIs)

- U.S. Farm Trade with Cuba

- Generalized System of Preferences (GSP)

- U.S.-EU Agricultural Trade Issues

- U.S.-EU Agricultural Trade Negotiations

- U.S.-EU Dispute over U.S. Olive Imports

- U.S.-EU Beef Hormone Dispute

- U.S.-EU Dispute over Pathogen Reduction Treatments (PRTs)

- EU Regulation of Edible Gelatin and Collagen

- Issues Related to Livestock Trade

- Export Bans on U.S. Meat and Poultry

- U.S. Meat and Poultry Imports

- Imports of Chicken from China

- Fresh Beef Imports from Brazil and Argentina

- Trade Restrictions on Ractopamine Use

- Country-of-Origin Labeling (COOL)

- WTO and U.S. Agriculture

- 2018 Farm Bill and WTO Compliance

- U.S. Challenges of Farm Support Spending of WTO Members

- U.S. Challenges of China's Agricultural Domestic Support

- U.S. Challenges of China's Agricultural Market Access Policy

- U.S. Challenges of India's Domestic Agricultural Support

Summary

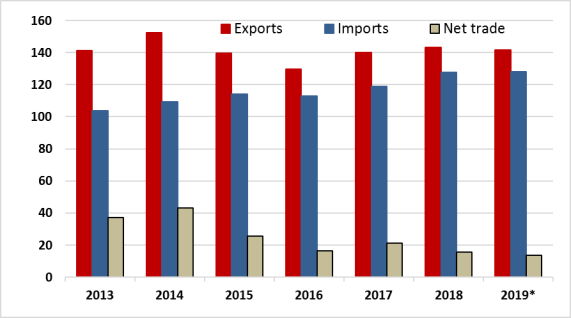

Sales of U.S. agricultural products to foreign markets absorb about one-fifth of U.S. agricultural production, thus contributing significantly to the health of the farm economy. Farm product exports, which totaled $143 billion in FY2018 (see chart below), make up about 9% of total U.S. exports and contribute positively to the U.S. balance of trade. The economic benefits of agricultural exports also extend across rural communities, while overseas farm sales help to buoy a wide array of industries linked to agriculture, including transportation, processing, and farm input suppliers.

|

U.S. Agricultural Trade, FY2013-FY2019 |

|

|

Source: USDA, Outlook for U.S. Agricultural Trade, AES-107, February 2019. Notes: *denotes forecast. Data is not adjusted for inflation. |

Congress has traditionally displayed a keen interest in agricultural trade issues given their importance to farmers and ranchers and to the overall economy. A major area of interest for the 116th Congress has been the loss of overseas export market shares for agricultural products due to the direction of the Trump Administration's trade policy, which places increased emphasis on reducing the overall U.S. trade deficit. In March 2018, the Trump Administration imposed Section 232 tariffs on U.S. imports of steel and aluminum from most countries and additional Section 301 tariffs on a number of imports from China. Following these actions, Canada, China, Mexico, the European Union (EU), and Turkey imposed retaliatory tariffs on more than 800 U.S. agricultural and food product exports. In response, USDA authorized $12 billion in short-term assistance to the affected agricultural producers and commodities under its Market Facilitation Program to help mitigate the economic impact on farmers.

A number of policy developments undertaken by the Trump Administration in bilateral and regional trade agreements may affect agricultural markets as well. On the Administration's initiative, the North American Free Trade Agreement (NAFTA) has been renegotiated and signed as the U.S.-Mexico-Canada Agreement (USMCA). This agreement is subject to legislative ratification by Canada and Mexico and approval by U.S. Congress. President Trump withdrew the United States from the Trans-Pacific Partnership (TPP) in January 2017. In March 2018, the remaining 11 countries concluded a revised version of TPP, the Comprehensive and Progressive Agreement for the Trans-Pacific Partnership (CPTPP). Signatories of CPTPP have begun to reduce tariffs and provide greater agricultural market access for imports from CPTPP signatory countries, actions that could potentially erode U.S. agricultural market shares in the region. At the bilateral level, the Trump Administration has notified Congress of its intent to begin trade negotiations with Japan (a CPTPP member), the EU, and the United Kingdom.

At the global level, and at the initiative of the United States, the World Trade Organization (WTO) recently ruled that China has subsidized its agricultural production beyond the level permitted under its WTO obligations and that China's administration of its agricultural market access policies are inconsistent with its WTO obligations. The United States has also filed a counter notification against India at the WTO stating that India has underreported its agricultural domestic subsidies.

Several other agricultural trade issues may be of interest to Congress. For example, the proposed USMCA does not address all the issues that restrict U.S. agricultural exports to Mexico and Canada, and Southeastern U.S. produce growers have been seeking changes to trade remedy laws to address imports of seasonal produce. A key objective of U.S. trade negotiations continues to be the establishment of a common framework for approval, trade, and marketing of the products of agricultural biotechnology. U.S. farm and food interests see the potential for market expansion opportunities in Cuba, but a prohibition on private U.S. financing is generally viewed as a major obstacle to this end. Moreover, the United States has announced its intention to withdraw eligibility for the Generalized System of Preference (GSP)—which provides duty-free tariff treatment for certain products from developing countries—from Turkey and India. On another front, U.S. exports of beef, pork, and chicken continue to face bans and trade restrictions over disease outbreaks even though the bans are inconsistent with international trade protocols, among which are China's ongoing bans on imports of U.S. beef and poultry and restrictions imposed by several foreign markets on U.S. ractopamine-fed pork.

Introduction

This report identifies selected current major trade issues for U.S. agriculture that may be of interest to the 116th Congress. It provides background on individual trade issues and attempts to bring perspective on the significance of each for U.S. agricultural trade. Each trade issue summary concludes with an assessment of its current status.

The report begins by examining a series of overarching issues. These issues include U.S. agricultural trade and its importance to the agricultural sector, a brief description of the trade policy being pursued by the Trump Administration and its ramifications for U.S. agricultural exports, the Administration's actions to mitigate the economic impact on agriculture from retaliatory actions by trading partners against its trade policies, and the implications for U.S. agriculture of the U.S. withdrawal from the Trans-Pacific Partnership (TPP) agreement. The report then reviews a number of ongoing trade disputes and trade negotiations while also examining a series of narrower trade issues of importance to the agricultural sector. The format for these more focused trade issues is similar, consisting of background and perspective on the issue at hand and an assessment of their current status.

Overview of U.S. Agricultural Trade1

U.S. agricultural exports have long been a bright spot in the U.S. balance of trade, with exports exceeding imports in every year since 1960. In recent years, the value of farm exports have experienced a downturn from the record level recorded in FY2014. The U.S. Department of Agriculture (USDA) forecasts U.S. agricultural exports in FY2019 at $141.5 billion (see Figure 1). If realized, this total would represent a decline from FY2018, when exports totaled $143 billion. Exports in FY2018 were $3 billion above the FY2017 total but almost $11 billion below the peak of $152.3 billion in FY2014.2 The decline in the value of farm exports since FY2014 initially reflected lower market prices for bulk commodities, such as soybeans and corn. Agricultural prices and U.S. exports of certain bulk commodities such as soybeans were further affected in 2018 by retaliatory tariffs imposed on selected U.S. agricultural imports by China, Canada, Mexico, the European Union (EU), and Turkey.3 The retaliatory tariffs were in response to the Trump Administration's imposition of Section 301 tariffs on certain imports from China and Section 232 tariffs on U.S. imports of steel and aluminum.

U.S. agricultural imports are forecast to total $128 billion in FY2019, slightly up from $127.6 billion in FY2018, resulting in an agricultural trade surplus of $13.5 billion. This would be below the surplus of $15.8 billion in FY2018 and below the record high in nominal dollars of $43.1 billion in FY2014.

Agricultural exports are important both to farmers and to the U.S. economy. During the calendar years 2017 and 2018, the value of U.S. agricultural exports accounted for 8% and 9% of total U.S. exports, respectively, and 5% of total U.S. imports, according to the U.S. Census data.4 As for the contribution of U.S. agricultural exports to the overall U.S. economy, USDA's Economic Research Service (ERS) estimates that in 2017 each dollar of U.S. agricultural exports stimulated an additional $1.30 in business activity. Moreover, that same year, U.S. agricultural exports generated an estimated 1,161,000 full-time civilian jobs, including 795,000 jobs outside the farm sector.5

With the productivity of U.S. agriculture growing faster than domestic demand, farmers and agriculturally oriented firms rely on export markets to sustain prices and revenue. Within the agricultural sector itself, the importance of exports account for around 20% of total farm production by value.6 Export markets are a major outlet for many farm commodities, absorbing over one-half of U.S. output for cotton and about half of total U.S. production for wheat, soybeans, and some specialty crops.7

Within the overall mix of agricultural exports, soybeans, corn, other feed crops, and wheat continue to rank at or near the top of the list of farm exports by volume. The high-value product (HVP) category—which includes such products as live animals, meat, dairy products, fruits and vegetables, nuts, fats, hides, manufactured feeds, sugar products, processed fruits and vegetables, and other processed food products—comprises the largest share of exports in value terms. In FY2018, the HVP share of the value of U.S. agricultural exports represented 66% of the total.8

All U.S. states export agricultural commodities, but a minority of states account for a majority of farm export sales. In calendar year 2017, the 10 leading agricultural exporting states based on value—California, Iowa, Illinois, Texas, Minnesota, Nebraska, Kansas, Indiana, North Dakota, and Missouri—accounted for 57% of the total value of U.S. agricultural exports that year.9

Status: In December 2018, Congress reauthorized major agricultural export promotion programs through FY2023 with the passage of the so-called 2018 farm bill (P.L. 115-334).10 Title III of the farm bill includes provisions covering export credit guarantee programs, export market development programs, and international science and technical exchange programs that are designed to develop agricultural export markets in emerging economies.

Trump Administration Trade Policy11

In establishing policy for U.S. participation in international trade, the Trump Administration has placed increased emphasis on trade deficits,12 which it views as an indicator of "unfair" foreign trade practices,13 with potential implications for U.S. industry and jobs. With the objective of reducing trade deficits, the Administration's trade policy has focused on withdrawing from or renegotiating existing trade agreements that the Administration views as being "unfair;" initiating new bilateral agreements; and responding to the trade practices of U.S. trade partners (whether geopolitical ally or adversary) that it views as unfair, illegal, or threatening to U.S. industry, with punitive14 trade actions.15 The punitive actions have included the imposition of Section 232 tariffs on U.S. imports of steel and aluminum and Section 301 tariffs on U.S. imports of products from China. The direction of the Administration's trade policy—for example, withdrawing from the Trans-Pacific Partnership (TPP) agreement with Japan and 10 other Pacific-facing nations and engaging in trade disputes with important agricultural trading partners that have resulted in retaliatory tariffs on U.S. agricultural products—has coincided with market share losses for certain U.S. agricultural exports.16

The Trump Administration has taken the position that current trade agreements to which the United States is a party and where the U.S. has a trade deficit or where the Administration perceives that the United States is being treated unfairly must be renegotiated or the United States will withdraw from them.17 Furthermore, the Administration questions the benefits of multi-party agreements, viewing them in some instances as improper vehicles for achieving meaningful negotiations.18 The Administration has also threatened to withdraw from the World Trade Organization (WTO) if it fails to undergo certain reforms.19 In January 2017, the Trump Administration withdrew from the TPP, which was subsequently concluded by the remaining TPP signatories under a modified framework renamed the Comprehensive and Progressive Agreement for Trans-Pacific Partnership (CPTPP) in March 2018.20 Under U.S. initiative, the North American Free Trade Agreement (NAFTA) was renegotiated as the U.S.-Mexico-Canada Agreement (USMCA).21 USMCA was signed by the leaders of the three nations in November 2018 but requires legislative ratification to enter into force.

In contrast to the Trump Administration's view of regional or multilateral negotiations, the Administration believes that greater potential gains can be achieved under bilateral negotiations where two countries can negotiate directly in the absence of group consensus.22 The Administration has sought to update some existing bilateral trade agreements and open new bilateral negotiations:

- The Administration negotiated selected modifications to the U.S.-South Korea free trade agreement.23

- The Administration has notified Congress of its intent to begin negotiations under Trade Promotion Authority (TPA)24 with trading partners including Japan, the EU, and the United Kingdom (UK).

- The Administration is currently engaged in bilateral trade negotiations with China in an attempt to resolve the current trade dispute that has resulted in retaliatory tariffs on a wide range of U.S. agricultural products.25

Status: The Administration's trade policy actions have in some cases resulted in retaliatory tariffs against U.S. agricultural product exports, while the status of new agreements with several important agricultural trading partners, such as Canada and Mexico, remains uncertain. U.S. agricultural exports continue to be subject to retaliatory tariffs imposed by trading partners in response to the Administration's imposition of Section 232 tariffs on steel and aluminum and Section 301 tariffs on China. The signed USMCA awaits consideration by Congress and ratification by Canada and Mexico. Numerous stakeholders have raised concerns that U.S. agriculture will lose export market shares to competitors due to U.S. withdrawal from TPP and its absence from CPTPP. Some stakeholders wonder whether agriculture will be prioritized in all planned bilateral negotiations.26 The Office of the U.S. Trade Representative (USTR) had indicated that it may pursue negotiations with Japan in stages, declaring that the automobiles sector will be a priority.27At the same time, both President Trump and the Secretary of Agriculture have stated that U.S.-Japan negotiations would occur in stages with a "very quick" deal on agriculture.28 However, the Japanese economy minister has stated that the United States and Japan would not reach an agreement in any one sector before other sectors.29

Elsewhere, the EU negotiating mandate for conducting trade negotiations with the United States articulates that a key EU goal is "a trade agreement limited to the elimination of tariffs for industrial goods only, excluding agricultural products."30 As for the UK, it cannot formally negotiate or conclude a new trade agreement with the United States until it exits the EU.31

Retaliatory Tariffs on U.S. Agricultural Exports32

On March 23, 2018, the Trump Administration applied a 25% tariff to certain U.S. steel imports and a 10% tariff to certain U.S. aluminum imports under Section 232 of the Trade Expansion Act of 1962. This action followed Department of Commerce (DOC) investigations that determined that current imports threaten U.S. national security. Citing objections to China's policies on intellectual property, technology, and innovation, the Administration also implemented three rounds of tariff increases under Section 301 on a total of $250 billion worth of Chinese products.

Canada, China, Mexico, the EU, and Turkey—whose exports were affected by the steel and aluminum tariffs—retaliated with tariffs on imports of a range of U.S. agricultural and food products and other goods. India has proposed retaliatory tariffs on a number of U.S. agricultural products, but it has delayed implementation pending ongoing negotiations with the Trump Administration.33

In all, the retaliatory tariffs imposed by these trading partners have targeted more than 800 U.S. agricultural and food products. Exports of those products to these five trading partners amounted to $26.9 billion in calendar year 2017, or about 18% of global U.S. agricultural and food product exports of $150.8 billion that year.

Retaliatory tariffs by China affect 99% of U.S. agricultural products exported to China. With a combination of Section 301 and Section 232 retaliations, China has levied retaliatory tariffs ranging from 5% to 50%, in addition to existing most-favored nation (MFN) tariffs, on more than 800 U.S. food and agricultural products that were worth about $20.6 billion in calendar year 2017. The products, subject to retaliatory tariffs, span all agricultural and food categories, including grains, meat and animal products, fruits and vegetables, seafood, and processed foods. The U.S. agricultural imports into China with the largest loss of markets since the tariffs were imposed in 2018, compared with 2017, are soybeans, cotton, sorghum, and hides and skins.

Canada has levied retaliatory tariffs of 10% on more than 20 U.S. agricultural and food products that are otherwise duty free under NAFTA. U.S. exports most affected by these tariffs are roasted coffee, ketchup, various beverage waters, licorice and toffee, and orange juice. U.S. exports of the products subject to Canada's retaliatory tariffs were valued at $2.6 billion in 2017.

Mexico has placed retaliatory tariffs of 15%-25% on a range of U.S. products that are otherwise duty free under NAFTA. U.S. exports to Mexico of these products amounted to approximately $2.5 billion in 2017. U.S. exports of cheese and pork have been the commodities most affected by Mexico's retaliatory tariffs as measured by reduced exports in 2018 compared with 2017.

The EU has levied a 25% tariff on certain U.S. exports of prepared vegetables and legumes, grains, fruit juice, peanut butter, and whiskey, which together amounted to $1 billion in sales in 2017. Turkey has imposed retaliatory tariffs on U.S. tree nuts, rice, prepared foods, whiskey, and unmanufactured tobacco. U.S. exports of these products to Turkey totaled $250 million in 2017.

A study from Purdue University found that the retaliatory tariffs could result in a reduction of U.S. agricultural exports by as much as $8 billion annually (in inflation adjusted values) after the markets have adjusted in the near future.34 The study also projects that the reduction in U.S. agricultural exports could lower agricultural land prices and result in the reallocation of 45,000 farm, ranch, and processing workers. Additionally, the authors suggest that U.S. soybean producers would see the most change in the wake of tariff retaliation, with exports potentially falling by 21% and land prices declining by about 18%. The impact estimated by the model would be affected over time by other policy shocks and technological and population changes that are not accounted for in the model. A recent United Nations study states that extended imposition of retaliatory tariffs will erode U.S. market share in favor of export competitors in the longer term.35

Status: U.S. agricultural exports continue to face retaliatory tariffs in response to the Administration's 2018 trade actions. The USDA forecasts U.S. agricultural exports for FY2019 at $141.5 billion compared with $143.4 billion in FY2018, reflecting its expectation that increased trade with other regions that are not involved in the tariff dispute will partially offset tariff-related trade losses, particularly with China. U.S. agricultural exports to China are forecast to decline in FY2019 by over $7 billion from $16 billion in FY2018.36 The United States and China are engaged in bilateral discussions to resolve the current trade dispute. USMCA—the proposed successor to NAFTA—does not address the Section 232 tariffs that led Canada and Mexico to impose retaliatory tariffs. Representatives of the U.S. business community, agriculture interest groups, other congressional leaders, and Canadian and Mexican government officials have stated that the Section 232 tariff issues must be resolved before USMCA enters into force.37

USDA's Trade-Aid Package in Response to Trade Retaliation38

On July 24, 2018, Secretary of Agriculture Sonny Perdue announced that the USDA would take several temporary actions to assist farmers in response to trade-related consequences from what the Administration characterized as "unjustified retaliation" against several U.S. agricultural products in 2018.39 Specifically, the Secretary said that the USDA would authorize up to $12 billion in financial assistance—referred to as a trade aid package—for certain agricultural commodities using the authority provided under Section 5 of the Commodity Credit Corporation (CCC) Charter Act (15 U.S.C. §714c).40

The Secretary initially stated that there would be no further trade-related financial assistance beyond this $12 billion package. However, on May 10, 2019, Secretary Perdue tweeted that the White House had directed USDA to work on a new aid package.41 The 2018 trade aid package includes (1) a Market Facilitation Program (MFP) of direct payments (valued at up to $10 billion) to producers of commodities most affected by the trade retaliation, (2) a Food Purchase and Distribution Program to partially offset lost export sales of affected commodities ($1.2 billion), and (3) an Agricultural Trade Promotion program to expand foreign markets ($200 million).

The largest component of the trade aid package, the MFP, provides direct financial assistance to producers of commodities that are most impacted by actions of foreign governments resulting in the loss of traditional exports. Affected commodities include soybeans, corn, cotton, sorghum, wheat, hogs, dairy, fresh sweet cherries, and shelled almonds. USDA announced MFP per-unit payment rates to be applied to certified production of eligible commodities in 2018.

USDA's Farm Service Agency administers the MFP. Eligible participants had to sign up for payments from September 2018 to February 2019. They also had to meet additional criteria, including being "actively engaged in farming," having an average adjusted gross income of less than $900,000, meeting conservation compliance provisions, and certifying their 2018 production with USDA by May 1, 2019.

USDA determined the MFP per-unit payment rate based on the estimated "direct trade damage"—the difference in expected trade value for each affected commodity with and without the retaliatory tariffs.42 The estimated "trade damage" for each affected commodity was then divided by the crop's production in 2017 to derive a per-unit payment rate. Indirect effects—such as any decline in market prices for affected commodities that were used domestically rather than exported—were not included in the payment calculation. Based on 2017 production data, USDA estimated that approximately $9.6 billion would be distributed in MFP payments to eligible producers, with over three-fourths ($7.3 billion) of MFP payments provided to soybean producers.

By linking MFP commodity payments only to the trade loss associated with each named MFP commodity, the payment formula favored commodities that relied more heavily on export markets than on domestic markets. Soybean growers and most farm-advocacy groups have generally been supportive of the payments, but some commodity groups—most notably associations representing corn, wheat, milk, and specialty crops—argued that the MFP payment formulation was inadequate to fully compensate their industries.43 For example, the National Corn Growers Association states that the 2018 trade disputes lowered corn prices by $0.44 per bushel for a potential total loss of $6.3 billion. Similarly, the National Association of Wheat Growers estimates a $0.75 per bushel decrease in domestic wheat prices that resulted in nearly $2.5 billion in lost value, while the National Milk Producers Federation has calculated that the retaliatory tariffs resulted in a $1.10 per hundredweight decline in domestic milk prices and over $1.2 billion in losses for milk producers based on milk futures prices. Similarly, many specialty crop groups contend that their tariff-related export losses were not fully compensated by the trade aid programs. To this point, a 2018 study by researchers at the University of California-Davis stated that, in California alone, specialty crops may suffer trade-related losses of over $3.3 billion on their 2018 production.44

Status: In March 2019, USDA estimated that a total of $8.7 billion in outlays would be made available under the MFP program, including $5.2 billion in 2018 and $3.5 billion in 2019.45 The large volume of payments could attract international attention about whether they are consistent with WTO rules and commitments on domestic support.46 The trade aid package raises a number of potential questions. For instance, if the United States and China do not reach an agreement in their ongoing tariff-driven trade negotiations, should another trade aid package, or some alternative compensatory measure, be provided in 2019, and possibly beyond? If MFP payments are to be repeated in the future, should USDA revise its payment formulation to provide a broader distribution of payments across the U.S. agricultural sector?

U.S. Withdrawal from Trans-Pacific Partnership (TPP)47

The TPP was concluded on October 4, 2015, among 12 countries: the United States, Australia, Brunei, Canada, Chile, Japan, Malaysia, Mexico, New Zealand, Peru, Singapore, and Vietnam. The agreement had not yet entered into force when President Trump signed an executive order withdrawing the United States from TPP on January 23, 2017. On March 8, 2018, the remaining 11 countries concluded a revised agreement—the CPTPP. On December 30, 2018, the CPTPP entered into force among the first six countries to ratify the agreement—Canada, Australia, Japan, Mexico, New Zealand, and Singapore. On January 14, 2019, the CPTPP entered into force for Vietnam.

With the United States, the TPP would have become the world's largest trade agreement, covering 40% of the global economy and providing comprehensive market access through the elimination and reduction of tariff and non-tariff barriers. The TPP provisions would have significantly increased the overseas markets to which U.S. farm and food products would have preferential access.48 The CPTPP provisions are based on the TPP. The agricultural provisions of the CPTPP seek to liberalize trade through lower tariffs, expanded tariff-rate quotas (TRQs),49 and agreements for reducing non-tariff barriers, including laws and regulations pertaining to products of agricultural biotechnology.50

In 2016, the U.S. International Trade Commission (USITC) had assessed the potential economic benefits from TPP ratification, projecting that by 2032 U.S. agricultural exports would be higher by $7.2 billion, or 2.6%, under TPP than without the agreement.51 Most of the increase in U.S. exports would have been concentrated in Japan (up $3.6 billion) and Vietnam (up $3.3 billion).

CPTPP countries represent a major component of U.S. farm and food trade, providing markets for 42% of U.S. farm exports between 2015 and 2018 while also supplying 52% of U.S. agricultural imports. By one estimate, U.S. absence from CPTPP will lead to a decline in U.S. agricultural exports of about $1.8 billion (1.2% of FY2018 U.S. agricultural exports of $143 billion) per year.52 The combination of U.S. absence from CPTPP, retaliatory tariffs on U.S. farm and food exports, and the possibility of the United States withdrawing entirely from NAFTA—as President Trump has threatened in the absence of USMCA ratification—could lead to a potential annual drop in U.S. agricultural exports of $21.8 billion, according to a study commissioned by the Farm Foundation.53 As the CPTPP agreement is relatively new, the possible range of impact on U.S. agriculture is uncertain because of limited studies that are available.

A broad cross-section of agricultural groups and food and agribusiness interests are concerned about losing potential export markets given U.S. absence from CPTPP. Under CPTPP, for example, Japanese tariffs on wheat imports will face a 50% reduction by 2025, which will put U.S. wheat exports to Japan at a competitive disadvantage.54 Similarly, the U.S. dairy industry estimates that by 2027, almost half of the U.S. dairy exports to Japan are likely to be replaced by dairy products from CPTPP and other countries with preferential trading agreements with Japan.55 Japan has historically accounted for more than a quarter of the total value of U.S. beef and pork exports. The U.S. share of Japan's imports of these commodities is expected to decline, because CPTPP competitors receive more favorable access to the Japanese market for beef and pork. U.S. Meat Export Federation states that annual beef export losses could reach $550 million by 2023 and more than $1.2 billion by 2028. Annual U.S. pork export losses are estimated to exceed $600 million by 2023 and reach $1 billion by 2028.56 USDA officials and representatives of the U.S. wheat and barley industries assert that U.S. wheat and barley exports are rapidly losing market share in Japan to CPTPP member countries and the EU.57

Status: U.S. agricultural exports appear to be at an increasing disadvantage in the CPTPP member country markets as these countries have begun to expand market access and reduce tariffs on imported products from CPTPP signatory countries. On October 16, 2018, under the TPA procedures, the Trump Administration gave Congress its official 90-day advance notification of intent to enter into trade negotiations with Japan, a CPTPP member country. In view of the Trump Administration's expressed objectives to "achieve fairer, more balanced trade," including in auto trade, stakeholders are uncertain about the prospects of reaching a quick deal with Japan.58 At the same time, both President Trump and the Secretary of Agriculture have stated that U.S.-Japan negotiations would occur in stages with a "very quick" deal on agriculture.59 However, the Japanese economy minister has stated that the United States and Japan would not reach an agreement in any one sector before other sectors.60

Agricultural Trade Issues with Canada and Mexico

Since 2002, Canada has been the United States' top agricultural export market, with U.S. agricultural exports averaging over $20 billion between FY2016 and FY2018. In FY2018, Canada accounted for 14% of the total value of U.S. agricultural exports to all destinations. Mexico has been the third-largest market for U.S. agricultural exports since FY2010. U.S. agricultural exports to Mexico averaged over $18 billion between FY2016 and FY2018, accounting for 13% of the total value of U.S. agricultural exports to all destinations in FY2018.

U.S.-Mexico-Canada Agreement (USMCA)61

On September 30, 2018, the Trump Administration announced an agreement with Canada and Mexico, USMCA, which it is promoting as a replacement for the NAFTA.62 Under NAFTA, all agricultural tariffs were phased out to zero except for certain products traded between the United States and Canada. These included U.S. imports from Canada of dairy products, peanuts, peanut butter, cotton, sugar, and sugar-containing products and Canadian imports from the United States of dairy products, poultry, eggs, and margarine. Quotas that once governed bilateral trade in these commodities were redefined as TRQs to comply with WTO commitments. Under a TRQ, a lower tariff rate is levied on import quantities within the quota amount, while a higher tariff rate is imposed on quantities in excess of the quota. The United States and Mexico agreement under NAFTA did not exclude any agricultural products from trade liberalization.

The proposed USMCA would expand upon the agricultural provisions of NAFTA. All food and agricultural products that have zero tariffs under NAFTA would remain at zero under USMCA. Under USMCA, market access would be expanded for the agricultural products traded between Canada and the United States that were exempt from tariff elimination under NAFTA. Canada agreed to create new U.S.-specific TRQs for U.S. dairy products63 and to replace the existing NAFTA poultry TRQs with new USMCA TRQs.64 All U.S. exports within the set TRQ volume limit would be subject to zero tariffs rates, but U.S. over-quota exports would still face the higher levels of tariffs currently in place under Canada's WTO commitment. The United States, in turn, agreed to improve access for imports of Canadian dairy, sugar, peanuts, and cotton. Canada and the United States also agreed to grade each other's like varieties of wheat as if they were produced domestically, a long-standing request of the U.S. wheat industry.

Under USMCA, provisions are made for textiles and apparel to promote greater use of North American origin products, which may support domestic U.S. cotton production. Also, each country would offer the same treatment for distributing another USMCA country's spirits, wine, beer, and other alcoholic beverages as it would its own products. USMCA's Sanitary and Phytosanitary (SPS) chapter calls for greater transparency in SPS rules and improved regulatory alignment among the three countries. Under USMCA, the United States, Canada, and Mexico agreed to provide procedural safeguards for recognition of new geographic indications, which are place names used to identify products that come from certain regions or locations. The agricultural chapter of USMCA also lays out provisions for addressing the products of agricultural biotechnology, an issue NAFTA does not address.

In April 2019, USITC released its report that provides an assessment of the likely effects of USMCA on the overall U.S. economy and its component sectors.65 Because NAFTA has already eliminated duties on most goods and reduced most non-tariff barriers, USITC's quantitative assessment includes changes that are not easily quantifiable. These provisions of trade negotiations were excluded from past USITC quantitative analyses. The provisions included in USMCA assessment by USITC—such as intellectual property rights, future commitments to open flows of data, and strengthening labor standards and rights—may reduce uncertainty in future trading regimes. Uncertainty reducing provisions are part of most free-trade agreements, including NAFTA, even if past assessments excluded them in the analyses. The USITC report finds that U.S. agricultural exports would increase by 1.1% in year 6 of USMCA implementation compared to its 2017 baseline export levels. In inflation-adjusted dollars, U.S. dairy exports to NAFTA countries would increase by $314.5 million (7.1%), and U.S. poultry exports would increase by $183.5 million (1%) compared to exports in 2017.

A 2018 study commissioned by the Farm Foundation performs an economy-wide analysis, but the analysis takes into consideration only the changes in agricultural tariffs and TRQs proposed under USMCA. The market access changes are introduced as shocks into a multi-region, economy-wide model. The impacts of these changes are analyzed after the economy has adjusted to the shocks after full implementation of USMCA—year 6. The adjustment process can include changes in production and consumption structure, including production costs and changes in the volume of agricultural outputs. This study estimates, in 2014 dollars, a net increase in annual U.S. agricultural exports of $450 million under USMCA, or about 1% of U.S. agricultural exports under NAFTA—$41 billion in FY2014.66 It projects the export losses from the retaliatory tariffs imposed by Canada and Mexico in response to U.S. Section 232 tariffs on steel and aluminum imports to be $1.8 billion per year (in 2014 dollars), which would more than offset the projected export gain of $450 million from USMCA. These losses include changes in production decisions and volumes resulting from higher production costs. This study does not consider changes in other sectors of the economy that would result from the implementation of USMCA provisions in these other sectors. Moreover, the impact estimated by the model would be affected over time by other policy shocks and technological and population changes that are not accounted for in the model.

According to an updated version of the Farm Foundation study, under the possible scenario of a complete withdrawal from NAFTA without ratification of USMCA, tariffs on U.S. exports to Canada and Mexico would be expected to return to the higher WTO MFN rates. Under this scenario, the study finds that, in 2014 dollars, U.S. agricultural and food exports to Canada and Mexico would decline by about $12 billion annually.67

A study conducted by researchers at the International Monetary Fund assesses the potential impacts of USMCA on North America as a region taking into consideration the following provisions of the proposed USMCA: (1) higher vehicle and auto parts regional value content requirement; (2) new labor value content requirement for vehicles; (3) stricter rules of origin for USMCA textile and apparel trade; (4) agricultural trade liberalization that increases U.S. access to Canadian supply-managed markets and reduces U.S. barriers on Canadian dairy, sugar and sugar products, and peanuts and peanut products; and (5) trade facilitation measures.68

The results describe a medium-term adjustment five to seven years after full implementation of USMCA—year 6. By this time, labor and capital would have been reallocated among sectors, but new investment spending would not yet have increased productive capacity. The study compares base period with what may happen five to seven years after full implementation of USMCA. This study finds that increasing higher regional vehicle and labor requirements would contribute to an economic loss for all three USMCA countries, with a decline in the production of vehicles and parts, shifts toward greater sourcing of both vehicles and parts from outside of the region, and higher prices for consumers. Regarding agricultural provisions of USMCA, the report highlights that Canada would stand to gain more than the United States. The study also highlights that the trade facilitation provisions of USMCA would potentially provide the largest gain to the region. Another researcher reiterates the findings of the International Monetary Fund study that the new domestic content provisions in USMCA would increase input costs for U.S. farmers who would end up paying more for trucks and machinery.69 As few studies have analyzed the potential impacts of USMCA, the diversity in the findings regarding the impacts from the implementation of USMCA is limited.

Stakeholder groups have expressed mixed responses to USMCA. A broad coalition representing more than 200 U.S. companies and industry associations has advocated for USMCA's approval.70 The American Farm Bureau Federation, which is the largest general farm organization, expressed satisfaction that USMCA not only locks in market opportunities previously developed but also builds on those trade relationships in several key areas.71 On the other hand, the National Farmers Union and the Institute for Agriculture and Trade Policy have expressed concern that the proposed agreement does not go far enough to institute a fair trade framework that benefits family farmers and ranchers.72

Status: The proposed USMCA does not enter into force unless approved by the U.S. Congress and ratified by Canada and Mexico. A report by USITC that assesses the impact of USMCA on U.S. economy was submitted to Congress on April 18, 2019.73 The timeline for congressional approval of USMCA would likely be governed by the TPA procedures established under the Bipartisan Congressional Trade Priorities and Accountability Act of 2015 (P.L. 114-26) but would not be initiated until the President submits the draft implementing bill to Congress.74

Some policymakers have stated that the path to ratifying USMCA by Congress is uncertain, in part because the three countries have yet to resolve disputes over U.S. Section 232 tariffs on imports of steel and aluminum and over the retaliatory tariffs that Canada and Mexico have imposed on U.S. agricultural products.75 Senator Chuck Grassley is reported to have called on the Trump Administration to lift tariffs on steel and aluminum imports from Canada and Mexico before Congress begins considering legislation to implement USMCA.76 House Speaker Nancy Pelosi has reportedly stated that she wants "stronger enforcement language" and that USMCA talks should be reopened to tighten enforcement provisions for labor and environmental protections.77

For more information, see CRS Report R45661, Agricultural Provisions of the U.S.-Mexico-Canada Agreement.

U.S. Dairy Exports to Canada78

The Canadian dairy sector limits production, sets prices, and restricts imports. Canadian imports of dairy products are restricted through TRQs, with over-quota tariffs in excess of 200% for some products. Although Canada is the second-largest market for U.S. dairy product exports, U.S. exports would likely be higher but for Canadian import restrictions.

In recent years, U.S. milk producers began exporting increased quantities of ultra-filtered (UF) milk to Canada. UF milk is a high-protein liquid product made by separating and concentrating certain milk components (such as protein and fat) for use as ingredients in dairy products, such as cheese, yogurt, and ice cream. U.S. UF milk found a market among Canadian cheese makers in 2008 after Canada revised its compositional standards for cheese. This revision significantly reduced the use of several milk products that U.S. processors had been supplying to Canadian food manufacturers, including milk protein concentrates and dried protein products.

In recent years, growing demand for butterfat in Canada resulted in increased Canadian milk production and, consequently, surplus supplies of skim milk. To address the surplus, Canada adopted the Class 7 milk price classification in 2017 (Class 6 in Ontario). Milk classified as Class 7 comprises skim milk components—primarily milk protein concentrates (MPC) and skim milk powder (SMP)—used to process dairy products. Prices for Class 7 products were set at low levels. Once the Class 7 regime was implemented, Canadian skim milk products became cheaper. Canada expanded global exports of SMP with the consequence that U.S. producers lost exports of high-protein UF milk to Canadian cheese and yogurt processors.

According to USDA, the value of U.S. UF milk exports to Canada peaked at nearly $107 million in 2015 but declined after the Class 7 regime was implemented in 2017 to $49 million in 2017 and $32 million in 2018.79 At the same time, Canada's exports of SMP more than tripled in 2017 to $133 million, compared with $42 million in 2016 before the Class 7 price regime was implemented.80 Eliminating Canada's Class 7 pricing regime became a priority for the U.S. dairy industry when NAFTA renegotiations commenced in 2017.

Status: Under USMCA, Canada agreed to eliminate the Class 7 pricing regime six months after USMCA enters into force. Canada also agreed to reclassify Class 7 products according to their end use and base its selling price on a formula that takes into consideration the USDA reported nonfat dry milk price. Also under the agreement, Canada would be required to monitor its exports of MPC, SMP, and infant formula and report at the harmonized tariff schedule level monthly.

Although Canada would maintain its milk supply management system under USMCA, it would expand TRQs for U.S. exports of milk, cheese, cream, skim milk powder, condensed milk, yogurt, and several other dairy products. U.S. dairy products within the USMCA TRQs would enter Canada duty free, while U.S. exports above the TRQ quantities would be subject to the existing higher over-quota tariffs. Likewise, the United States would establish TRQs for imports of Canadian dairy products.

In total, under USMCA Canada would grant the United States duty-free access to nearly 17,000 metric tons (MT) of dairy products the first year of the agreement, 100,000 MT in the sixth year, and 109,000 MT in year 19. The USMCA quota is specific to the United States and would be in addition to the 93,648 MT of WTO global quota, which is available under NAFTA to exports from the United States as well as to exports from other WTO member countries.81 For more information, see CRS In Focus IF11149, Dairy Provisions in USMCA.

U.S.-Canada Dispute Regarding the Sale of Wine in Grocery Stores82

In Canada, the authority to import and distribute alcohol rests with the provincial governments. Starting in 2015, British Columbia (BC) initiated a series of policies and regulations that provide BC wine exclusive access to retail channels and grocery store shelves, while imported wine maybe sold in grocery stores only through a "store within a store"83 physically separated from the main retail outlet and with separate cash registers.84 Overall, the U.S.-based Wine Institute reports that Canada is the leading export market for California wine—the leading wine producing state in the United States—accounting for $444 million in sales in 2017.85

Status: In January 2017, the Obama Administration initiated trade enforcement action against Canada at the WTO regarding Canada's BC wine measures.86 Subsequent actions by the Trump Administration, in September 2017, led to the United States requesting formal consultations with Canada regarding BC wine measures.87 USTR states that "discriminatory regulations implemented by British Columbia are unfairly keeping U.S. wine off of grocery store shelves" and that the measures are inconsistent with Canada's commitments and obligations under the WTO.88 The Canadian wine industry estimates that wine imports account for nearly 70% of the Canadian wine market. It also points out that the BC Vintners Quality Alliance has been issuing store licenses for the industry since the 1980s.89 The United States reiterated its concerns as part of a second complaint issued in this case in July 2018. Argentina, Australia, New Zealand, and the EU have requested to join the consultation.

The proposed USMCA addresses U.S. concerns about Canada's BC wine measures as part of a side letter to the proposed agreement. As outlined in the side letter, Canada would modify certain measures that provide preferential grocery store shelf space to wines produced within the province and "implement any changes no later than November 1, 2019."90

Other North American Trade Issues

The proposed USMCA does not address all the issues that restrict U.S. agricultural exports to Mexico and Canada, nor does it include all of the changes sought by U.S. agricultural interest groups. For instance, Southeastern U.S. produce growers have been seeking changes to trade remedy laws to address imports of seasonal produce.

Import Competition of Seasonal Produce from Mexico91

Mexico's production of some fruits and vegetables—tomatoes, peppers, cucumbers, berries, and melons—has increased in recent years in part due to Mexico's investment in large-scale greenhouse production facilities and other types of technological innovations. Greenhouse production in Mexico continues to rise, with 2018 estimates of nearly 57,500 acres of produce grown under protection, up from an estimated 9,000 acres in 2017.92 USDA researchers reported that Mexico is the largest foreign supplier of U.S. imports of vegetables and fruits (excluding bananas).93

Representatives of the Florida Fruit and Vegetable Association (FFVA) claim that Mexico's investment in produce production is supported by government subsidies and should be addressed through countervailing duties (CVD) on U.S. imports of these products.94 They further state that these exports enter the United States at prices below the cost of production and should be countered by higher antidumping (AD) duties. FFVA also believes that Mexico's labor cost advantage in fruit and vegetable production gives Mexico a competitive advantage over U.S. produce growers.95 In general, trade concerns have centered on tomatoes, peppers, and berries.

One of the Trump Administration's initial agriculture-related objectives in the renegotiation of NAFTA included a proposal to establish new rules for seasonal and perishable products, such as fruits and vegetables.96 The proposal would have established a separate domestic industry provision for perishable and seasonal products in AD and CVD proceedings, making it easier for a group of regional producers to initiate an injury case and to prove injury, thereby implementing CVD or AD duties to be levied on the imported products responsible for the injury. This could protect certain U.S. seasonal fruit and vegetable products in some regions by making it easier to initiate trade remedy cases.97 USITC has previously reviewed trade remedy cases involving perishable agricultural products that have proven difficult to settle.98

Some Members of Congress supported including seasonal protections as part of NAFTA's renegotiation.99 Others opposed including such protections, contending that seasonal production complements rather than competes with U.S. growing seasons,100 while still others worried it could open the door to an "uncontrolled proliferation of regional, seasonal, perishable remedies against U.S. exports."101 Most U.S. food and agricultural sectors, including some fruit and vegetable producer groups, opposed including seasonal protections as part of the renegotiation.102 Some worried that efforts to push for seasonal protections would derail the renegotiation. Others claimed that such efforts would favor a few "politically-connected, wealthy agribusiness firms from Florida" at the expense of others in the U.S. produce industry103 and at the expense of both consumers and growers in other fruit and vegetable producing states, such as California.104 The Agricultural Technical Advisory Committee for Trade in Fruits and Vegetables (F&V ATAC) supported not including provisions in the NAFTA renegotiation, acknowledging that including such protections would generate "significant opposition from Mexican and Canadian negotiators, in addition to raising concern by many in the U.S. agricultural community, including many in the fruit and vegetable industry."105 In January 2018, F&V ATAC passed a resolution supporting the withdrawal of the seasonal and perishable trade remedy proposal from the U.S. negotiating objectives.106

Status: The proposed USMCA that might replace NAFTA does not include changes to U.S. trade remedy laws to address seasonal produce trade. As a result, some in Congress have taken additional steps to try to address this issue.107 Bills were introduced in both the House and Senate in the 115th Congress as part of the Agricultural Trade Improvement Act of 2018 (S. 3510; H.R. 7015). These bills would have provided for CVD and AD procedures for seasonal producers and defined core seasonal industry in U.S. trade remedy laws, among other changes. These two bills were reintroduced in the 116th Congress but renamed "Defending Domestic Produce Production Act of 2019" (S. 16; H.R. 101). Current law generally requires that an injury case be supported by at least 50% of the domestic industry.108 The House and Senate bills would allow regional groups representing less than 50% of nationwide seasonal growers to initiate an injury investigation. Such changes could make it easier for a group of regional producers to initiate trade remedy cases.

Withdrawal of the U.S.-Mexico Tomato Suspension Agreement109

The U.S.-Mexico Tomato Suspension Agreement is an agreement between DOC and signatory producers/exporters110 of fresh tomatoes grown in Mexico that suspends the U.S. AD investigation into whether Mexican fresh tomatoes were sold into the U.S. market at less than fair value.111 Fresh tomatoes imported from Mexico have been governed by suspension agreements since 1996.112 The first suspension agreement on fresh tomatoes from Mexico became effective in November 1996. The Mexican signatory growers and the United States entered into new agreements in 2002 and 2008. The most recent agreement became effective in March 2013. Under the current agreement, the signatories agree to suspend the AD investigation and monitor compliance with the agreement. The basis for the suspension agreement was a commitment by each signatory producer/exporter to sell tomatoes at or above the stated reference price in order to eliminate the injurious effects of exports of fresh tomatoes to the United States. Analysis commissioned by the Fresh Produce Association of the Americas (FPAA) found that terminating the agreement could "reduce the supply of tomatoes in the US market, and raise prices paid by consumers in the U.S., particularly during the winter tomato season (October-June)."113

The agreement sets different floor prices for Mexican fresh tomatoes during the summer and winter and specifies prices for open field/adapted-environment and controlled-environment production. These price floors cover all types of fresh or chilled tomatoes from Mexico, including common round, cherry, grape, plum, pear, and greenhouse tomatoes. The agreement does not cover tomatoes that are for processing.

In early 2018, DOC initiated consultations with the Mexican tomato growers and exporters to negotiate possible revisions to the 2013 agreement. In addition, DOC initiated its five-year sunset review of the suspended AD investigation and published the preliminary and final results of its analysis in late 2018. DOC's analysis indicated that dumping of fresh tomatoes was likely to occur or recur and calculated weighted-average dumping margins of up to 188%.114 In November 2018, the Florida Tomato Exchange requested that the United States withdraw from the suspension agreement, eliminate the reference prices, and resume the related initial 1996 AD investigation.115 Several Members of Congress in both the House and the Senate have expressed support for withdrawing from the suspension agreement.116 Among the groups that oppose withdrawal are the FPAA and other groups representing Mexican growers and exporters as well as businesses, various associations, and local and county governments.117

Status: On May 7, 2019, the United States terminated the 2013 Suspension Agreement on Fresh Tomatoes from Mexico but said it plans to continue negotiations regarding a possible revised agreement.118 DOC initially announced its intention to withdraw from the agreement in February 2019 following its periodic review of the agreement, which concluded that Mexican fresh tomatoes have been sold into the U.S. market at less than fair value.119 Without a suspension agreement, an AD order could be issued if USITC makes a determination of financial injury to U.S. growers. Reportedly, the DOC and Mexico have been unable to develop a revised agreement that is acceptable to both sides, despite ongoing negotiations since early 2018.120 In April 2019, Mexico's tomato growers proposed to eliminate a price distinction between winter and summer season tomatoes and increase the reference price for USDA-certified organic tomatoes.121 The government of Mexico has expressed its disappointment about the U.S. decision.122

U.S.-Mexico Sugar Suspension Agreements123

In December 2014, DOC signed suspension agreements with the government of Mexico and Mexican sugar producers and exporters that prevented the imposition of CVD and AD on U.S. imports of Mexican sugar. This was a consequence of U.S. government determinations that Mexican sugar was being subsidized by the government of Mexico and was being sold into the U.S. market at less than fair value.

The suspension agreements limit Mexico's sugar exports to the United States to the residual of U.S. needs for domestic human use in a given marketing year after subtracting U.S. production and imports from other countries. The agreements establish minimum reference prices for Mexican sugar that are above U.S. sugar program loan levels for domestically produced sugar. Another provision limits the share of Mexican sugar that can enter the United States as refined sugar.

After the suspension agreements took effect, a number of stakeholders in the U.S. sugar market asserted that the suspension agreements had not worked as intended and had not entirely eliminated the injury caused by the subsidization and dumping of Mexican sugar. One widely held criticism was that cane refiners who were dependent on imports of raw cane from Mexico had received an inadequate share of sugar from Mexico. Another criticism leveled at the agreements was that Mexican exporters were not always adhering to limits on the share of Mexican sugar imports that are refined sugar as compared with raw sugar nor to the specified minimum reference prices.124

In November 2016, the American Sugar Coalition—representing sugar cane and sugar beet producers and sugar processors, refiners, and workers—called on DOC to withdraw from the agreements, an action that could have caused AD and CVD duties to be imposed on Mexican sugar.125 Imperial Sugar Company, a U.S. cane refiner, also advocated for withdrawal. The Sweetener Users Association, which represents sugar-using businesses, recommended renegotiating the agreements to address their shortcomings and warned that terminating them would virtually eliminate Mexican sugar from the U.S. market. In November 2016, DOC issued results of a preliminary administrative review.126 In it, the DOC concluded that the agreements may not have entirely redressed the injury, and that certain import transactions may not have adhered to the terms in the agreements.

Status: In June 2017, the United States and Mexico agreed to amendments to the suspension agreements.127 Under the amendments, effective October 1, 2017, the price of imported Mexican raw sugar was increased from $0.2225 per pound to $0.23 per pound. The price of imported refined sugar was increased from $0.26 per pound to $0.28 per pound. The maximum share of refined sugar imports was limited to 30%, with raw sugar imports constituting at least 70% of the total, compared with 53% and 47%, respectively, under the 2014 agreement. The agreement also requires that imported raw sugar be loaded in bulk and free flowing—that is, not packaged. Any raw sugar imports that are packaged would be counted toward the refined sugar allotment. In addition, if USDA determines that the United States requires additional sugar imports to meet its needs, Mexico would be awarded the first opportunity to fill the need. For more information, see CRS In Focus IF10693, Amended Sugar Agreements Recast U.S.-Mexico Trade.

Other Major Trade Issues

Several other trade issues may be of interest to Congress. A key objective of U.S. trade negotiations has been to establish a common framework for approval, trade, and marketing of the products of agricultural biotechnology. Among other high-profile issues, geographical indications are increasingly becoming an agricultural trade issue. In addition, U.S. farm and food interests continue to see potential market expansion opportunities in Cuba, but interested exporters regard a prohibition on private U.S. financing as a major obstacle to this end. On the import side of the trade ledger, in March 2019, the United States initiated its review of the Generalized System of Preference (GSP), which provides duty-free tariff treatment for certain products imported from developing countries.

Agricultural Biotechnology128

Agricultural biotechnology refers primarily to the commercial use of recombinant DNA techniques to genetically modify or bioengineer plants and animals so that they have certain desired characteristics, primarily herbicide tolerance and pest resistance. More recently, the term has also come to encompass a range of new genetic technologies involving genomic editing (e.g., CRISPR-Cas9) rather than recombinant DNA techniques alone.129 U.S. soybean, corn, cotton, and sugar beet producers have rapidly adopted genetically engineered (GE) varieties of these crops since commercialization began in the mid-1990s. The United States is the leading country in cultivating GE crops, accounting for more than 40% of total acres growing GE crops worldwide.

Elsewhere in the world, the adoption and cultivation of GE crops by both producers and consumers has been mixed. In the EU, for example, the European Commission (EC) may approve of GE products for import and marketing, but individual member states may maintain bans. GE crop production in the EU accounts for about 1% of crop acreage—about 325,000 acres—all in a single variety of pest-resistant GE corn: MON810.130 This particular variety is cultivated predominantly in Spain and Portugal. Eighteen EU member states ban cultivation of GE crops and/or have specific rules on the trade of GE seeds.131 EU officials have been cautious in permitting GE products to be cultivated within the EU, but EU-approved varieties of GE commodities can be imported.132

All GE-derived food and feed imported to the EU must be labeled as such. The EU's regulatory framework regarding biotechnology is generally regarded as one of the most stringent worldwide. Many U.S. producers assert that EU labeling and traceability regulations for approving GE crops have effectively limited certain U.S. agricultural exports to the EU. The EU's approval process for GE products—effectively a de facto moratorium since 1998—has been a source of dispute since 2003 and continues to be a contentious issue in the current U.S.-EU agricultural trade negotiations.

While the EU as a policymaking entity generally supports GE production, public opinion remains strongly opposed to GE food and crops in most EU member states. This opposition in the EU has also been an important factor in the acceptance of GE crops in lesser developed countries. Most African countries have largely followed the EU in restricting or banning the cultivation of GE crops.

The U.S. Secretary of Agriculture stated that the United States will not regulate plants created through genomic editing so long as they are developed without using a plant pest as the donor or vector and are not plant pests themselves.133 In contrast, the EU Court of Justice ruled that organisms obtained by mutagenesis134 are genetically modified organisms (GMOs) and are in principle within the scope of the GMO Directive, which governs the deliberate release of GMOs into the environment.135 The EU Court considers that the risks posed by new mutagenesis techniques such as gene editing (CRISPR-Cas9) to be similar to crops created from transgenesis, wherein GE crops have genetic material introduced from other organisms.

China's reluctance to approve GE crops or GE imports is a source of frustration for U.S. agricultural interests. While GE crops are technically banned from China, U.S.-developed GMOs appear to be grown in China without authorization despite Chinese laws banning their cultivation.136 In September 2016, China agreed to improve its agricultural biotechnology approval process. That commitment did not include specific details, although China stated that they are committed to review eight long-pending applications of agricultural biotechnology in a "timely, ongoing, and science-based manner."137 On January 8, 2019, the Chinese Ministry of Agriculture and Rural Affairs announced approval of five new biotech traits in imported crops for processing, the first new approvals since June 2017.138 At the same time, the ministry amended the regulations on safety assessment, import approval, and labeling of agricultural GMOs without notifying the changes to the WTO nor soliciting comments from stakeholders.

With respect to the proposed USMCA, the agreement specifically includes provisions to improve transparency in approving and bringing to market products of agricultural biotechnology, something NAFTA did not cover. USMCA provisions cover crops produced with all biotechnology methods, including recombinant DNA and gene editing.

Trade negotiations concerning agricultural biotechnology also involve labeling issues and other provisions that address the unintended presence of GE products in non-GE shipments. As the United States implements its new "bioengineered food disclosure" standard, it may raise concerns among some trading partners—particularly the EU.139 The food disclosure standard, for example, will not mandate labeling of highly refined ingredients from any GE crop if "no modified genetic material" is detectable. This provision would exclude food products, for example, containing high-fructose corn syrup, refined soybean oil, and sugar from sugar beets.

Status: A key objective of U.S. trade negotiations, such as the U.S.-EU agricultural trade negotiations and U.S. negotiations with China, has been to establish a common framework for GE approvals. This includes labeling practices consistent with the U.S. guidelines and harmonized regulatory procedures concerning GE presence in products that are consistent with the Codex Alimentarius Commission Annex on Food Safety Assessment in Situations of Low-Level Presence of Recombinant-DNA Plant Material in Food. The proposed USMCA specifically includes provisions to improve transparency in approving and bringing to market products of agricultural biotechnology. For other negotiations, U.S. objectives on agricultural biotechnology, for the most part, remain aspirational. Additionally, the United States believes that U.S. export opportunities are being impaired due to EU pressure on lesser developed countries to adopt EU SPS measures that ban GE products.

Geographical Indications (GIs)140

GIs are geographical names that act to protect the quality and reputation of a distinctive product originating in a certain region. The term GI is most often applied to wines, spirits, and agricultural products. Some food producers benefit from the use of GIs by giving certain foods recognition for their distinctiveness, thereby differentiating them in the marketplace. In this manner, GIs can be commercially valuable. GIs may also be eligible for relief from acts of infringement or unfair competition. While the use of GIs may protect consumers from deceptive or misleading labels, they also have the potential to impair trade when the use of names that are considered common or generic in one market are protected in another. Examples of registered or established GIs include Parmigiano Reggiano cheese and Prosciutto di Parma ham from the Parma region of Italy, Toscano olive oil from the Tuscany region of Italy, Roquefort cheese from France, Champagne from the region of the same name in France, Irish whiskey, Darjeeling tea, Florida oranges, Idaho potatoes, Vidalia onions, Washington State apples, and Napa Valley wines.

GIs—along with other types of intellectual property such as patents, copyrights, trademarks, and trade secrets—are an example of intellectual property rights (IPR). The use of GIs has become a contentious international trade issue, particularly for U.S. wine, cheese, and sausage makers. In general, some consider GIs to be protected intellectual property, while others consider them to be generic or semi-generic terms. For example, in the United States, feta is considered the generic name for a type of cheese. However, it is protected as a GI in Europe. As such, feta cheese produced in the United States may not be exported for sale in the EU, since only feta produced in countries or regions currently holding GI registrations may be sold commercially.

Laws and regulations governing GIs differ markedly between the United States and EU, which further complicates this issue. In addition, registered products often fall under GI protections in certain third-country markets, and some EU GIs have been trademarked in some non-EU countries. This has become a concern for U.S. agricultural exporters following a series of recently concluded trade agreements among the EU and Canada, Japan, South Korea, South Africa, and other countries that in many cases are also trading partners of the United States. As a result, Canada has agreed to recognize a list of 143 EU GIs in Canada,141 and Japan has agreed to recognize 71 EU GIs in Japan.142 More than 4,500 product names are registered and protected in the EU for foods, wine, and spirits originating in both EU member states and other countries.

The EU's GI program remains a contentious issue for many in the U.S. Congress, particularly among Members with dairy constituencies. Some have long expressed their concerns about EU protections for GIs, which they claim are being misused to create market and trade barriers.143 A 2019 study commissioned by the U.S. dairy industry forecasts declining U.S. cheese exports due to expanding restrictions on the use of generic terms such as parmesan, asiago, and feta cheese.144 However, some U.S. agricultural industry groups are trying to create a system similar to the EU GI system for U.S. products to promote certain distinctive American agricultural products as part of the American Origin Products Association, which represents certain U.S. potato, maple syrup, ginseng, coffee, and chile pepper producers and certain U.S. winemakers, among other regional producer groups,145 and seeks to work with federal authorities to "create of a list of qualified U.S. distinctive product names, which correspond to the GI definition."

Status: GIs are included among other IPR issues in the current U.S. trade agenda.146 The proposed USMCA protects common names and limits the ability to register new GIs that some producers regard as common (generic) names. USMCA includes a side letter between the U.S. and Mexico regarding the use of 33 cheese names.147

GIs have been an active area of debate between the United States and EU in previous trade negotiations.148 GIs continue to be a trade issue for USTR, and the United States is working "to advance U.S. market access interests in foreign markets and to ensure that GI-related trade initiatives of the EU, its Member States, like-minded countries, and international organizations, do not undercut such market access," stating that the EU's GI agenda "significantly undermines the scope of trademarks and other [intellectual property] rights held by U.S. producers and imposes barriers on market access for American-made goods that rely on the use of common names."149 Previously, USDA officials have indicated that the United States would likely not agree to EU demands to reserve certain food names for EU producers and have expressed concerns about the EU's system of protections for GIs.150 GIs are also included in the United States' IPR negotiating objectives for the U.S.-EU and U.S.-Japan trade negotiations.151

U.S. Farm Trade with Cuba152

The U.S. embargo on trade and financial transactions with Cuba dates from 1962. The sanctions on Cuba were partially eased in 2000 with regard to U.S. exports of agricultural products with the enactment of the Trade Sanctions Reform and Export Enhancement Act of 2000 (P.L. 106-387). The law allows for one-year export licenses for selling agricultural commodities to Cuba but without the availability of U.S. government assistance, foreign assistance, export assistance, credits, or credit guarantees to finance the trade. The law also denies exporters of agricultural goods access to U.S. private commercial financing or credit, although U.S. private export financing is permitted for all other authorized export trade to Cuba.153 Moreover, all agricultural product transactions must be conducted on a cash-in-advance basis or with financing from third countries.