U.S. Sugar Program Fundamentals

The U.S. sugar program provides a price support guarantee to producers of sugar beets and sugarcane and to the processors of both crops. The U.S. Department of Agriculture (USDA), as program administrator, is directed to administer the program at no budgetary cost to the federal government by limiting the amount of sugar supplied for food use in the U.S. market. To achieve both objectives, USDA uses four tools—as reauthorized without change by the 2014 farm bill (P.L. 113-79) and found in chapter 17 of the Harmonized Tariff Schedules of the United States—to keep domestic market prices above guaranteed levels. These are:

price support loans at specified levels—the basis for the price guarantee;

marketing allotments to limit the amount of sugar that each processor can sell;

import quotas to control the amount of sugar entering the U.S. market;

a sugar-to-ethanol backstop—available if marketing allotments and import quotas are insufficient to prevent a sugar surplus from developing, which in turn could result in market prices falling below guaranteed levels.

To supplement these policy tools in supporting sugar prices above government loan levels, while avoiding costly loan forfeitures, important administrative changes were adopted in late 2014. These included imposing limits on U.S. imports of Mexican sugar and establishing minimum prices for Mexican sugar imports, actions that fundamentally recast the terms of bilateral trade in sugar. A U.S. sugar refiner is pursuing a legal challenge to the U.S. government’s finding that these changes have eliminated the harm to the U.S. sugar industry, so although this new regime is in effect, a measure of uncertainty about its future remains.

Under the U.S. sugar program, nonrecourse loans that may be taken out by sugar processors, not producers themselves, provide a source of short-term, low-cost financing until a raw cane sugar mill or beet sugar refiner sells sugar. The “nonrecourse” feature of these loans means that processors—to meet their repayment obligation—can exercise the legal right to forfeit sugar offered as collateral to USDA to secure the loan, if the market price is below the effective support level when the loan comes due.

Sugar marketing allotments limit the amount of domestically produced sugar that processors can sell each year. In a 2008 farm bill provision, retained by the 2014 farm bill, USDA each year must set the overall allotment quantity (OAQ) at not less than 85% of estimated U.S. human consumption of sugar. The OAQ is intended to ensure that permitted sales of domestic sugar, when added to imports under U.S. trade commitments, do not depress market prices below loan forfeiture levels for refined beet sugar and raw cane sugar.

The United States imports sugar in order to meet total food demand. The amount of foreign sugar supplied to the U.S. market reflects U.S. commitments made under various trade agreements. The most significant import obligation is the World Trade Organization (WTO) quota commitment, which requires the United States to allow not less than 1.256 million tons of sugar (almost all raw cane) to enter the domestic market from 40 countries. The United States also grants much smaller import quotas to nine countries covered by four free trade agreements. At the same time, a 2008 farm bill provision, also retained in the 2014 farm bill, directs USDA to manage overall U.S. sugar supply, including imports, so that market prices do not fall below effective support levels.

If market prices fall below levels guaranteed by the sugar program, USDA must administer a sugar-for-ethanol program in which it buys domestically produced sugar from the market and sells it to ethanol producers as feedstock for fuel ethanol. A source of controversy over the sugar program is the balance it strikes between the interests of the sugar industry and sugar users.

U.S. Sugar Program Fundamentals

Jump to Main Text of Report

Contents

- Sugar Policy Overview

- Price Support Loans

- Tools for Balancing Supplies and Supporting Prices

- Marketing Allotments

- Import Quotas

- Suspension Agreements Recast Sugar Trade with Mexico

- Potential Effects on Government Outlays and Sugar Prices

- Two Sugarcane Refiners Challenging Suspension Agreements

- Mechanisms Aimed at Countering Low Prices

- Sugar Purchases and Exchanges for Import Rights

- Feedstock Flexibility Program for Bioenergy Producers

- Sugar Program Draws Sharply Differing Views

- Administrative Year in the Sugar Program

Figures

- Figure 1. Price Support Loan Making Process for Raw Cane Sugar

- Figure 2. Price Support Loan Making Process for Refined Beet Sugar

- Figure 3. Raw Cane Sugar Prices Have Been Above Loan Forfeiture Level Since the 2008 Farm Bill Except in Early FY2009, Late FY2013, and Early FY2014

- Figure 4. Refined Beet Sugar Prices Have Stayed Above Loan Forfeiture Range Since the 2008 Farm Bill Until February 2016

- Figure 5. Overall Allotment Quantity Compared to Total U.S. Sugar Supply

- Figure 6. U.S. Sugar Imports, by Trade Agreement

Summary

The U.S. sugar program provides a price support guarantee to producers of sugar beets and sugarcane and to the processors of both crops. The U.S. Department of Agriculture (USDA), as program administrator, is directed to administer the program at no budgetary cost to the federal government by limiting the amount of sugar supplied for food use in the U.S. market. To achieve both objectives, USDA uses four tools—as reauthorized without change by the 2014 farm bill (P.L. 113-79) and found in chapter 17 of the Harmonized Tariff Schedules of the United States—to keep domestic market prices above guaranteed levels. These are:

- price support loans at specified levels—the basis for the price guarantee;

- marketing allotments to limit the amount of sugar that each processor can sell;

- import quotas to control the amount of sugar entering the U.S. market;

- a sugar-to-ethanol backstop—available if marketing allotments and import quotas are insufficient to prevent a sugar surplus from developing, which in turn could result in market prices falling below guaranteed levels.

To supplement these policy tools in supporting sugar prices above government loan levels, while avoiding costly loan forfeitures, important administrative changes were adopted in late 2014. These included imposing limits on U.S. imports of Mexican sugar and establishing minimum prices for Mexican sugar imports, actions that fundamentally recast the terms of bilateral trade in sugar. A U.S. sugar refiner is pursuing a legal challenge to the U.S. government's finding that these changes have eliminated the harm to the U.S. sugar industry, so although this new regime is in effect, a measure of uncertainty about its future remains.

Under the U.S. sugar program, nonrecourse loans that may be taken out by sugar processors, not producers themselves, provide a source of short-term, low-cost financing until a raw cane sugar mill or beet sugar refiner sells sugar. The "nonrecourse" feature of these loans means that processors—to meet their repayment obligation—can exercise the legal right to forfeit sugar offered as collateral to USDA to secure the loan, if the market price is below the effective support level when the loan comes due.

Sugar marketing allotments limit the amount of domestically produced sugar that processors can sell each year. In a 2008 farm bill provision, retained by the 2014 farm bill, USDA each year must set the overall allotment quantity (OAQ) at not less than 85% of estimated U.S. human consumption of sugar. The OAQ is intended to ensure that permitted sales of domestic sugar, when added to imports under U.S. trade commitments, do not depress market prices below loan forfeiture levels for refined beet sugar and raw cane sugar.

The United States imports sugar in order to meet total food demand. The amount of foreign sugar supplied to the U.S. market reflects U.S. commitments made under various trade agreements. The most significant import obligation is the World Trade Organization (WTO) quota commitment, which requires the United States to allow not less than 1.256 million tons of sugar (almost all raw cane) to enter the domestic market from 40 countries. The United States also grants much smaller import quotas to nine countries covered by four free trade agreements. At the same time, a 2008 farm bill provision, also retained in the 2014 farm bill, directs USDA to manage overall U.S. sugar supply, including imports, so that market prices do not fall below effective support levels.

If market prices fall below levels guaranteed by the sugar program, USDA must administer a sugar-for-ethanol program in which it buys domestically produced sugar from the market and sells it to ethanol producers as feedstock for fuel ethanol. A source of controversy over the sugar program is the balance it strikes between the interests of the sugar industry and sugar users.

Sugar Policy Overview

The U.S. sugar program is singular among major agricultural commodity programs in that it combines a price support guarantee with a supply management structure that encompasses both domestic production for human use and sugar imports. The sugar program provides a price guarantee to the processors of sugarcane and sugar beets, and by extension, to the producers of both crops. The U.S. Department of Agriculture (USDA) is directed to administer the program at no budgetary cost to the federal government by limiting the amount of sugar supplied for food use in the U.S. market. To achieve both objectives, USDA uses four tools to keep domestic market prices above guaranteed levels. Measures one through three below were reauthorized through crop year 2018 without change by the 2014 farm bill (P.L. 113-79). The fourth measure is found in long-standing trade law. The four are:

- 1. price support loans at specified levels—the basis for the price guarantee;

- 2. marketing allotments to limit the amount of sugar that each processor can sell;

- 3. a sugar-to-ethanol (feedstock flexibility) backstop—available if marketing allotments and import quotas fail to prevent a price-depressing surplus of sugar from developing (i.e., fail to keep market prices above guaranteed levels);

- 4. import quotas to control the amount of sugar entering the U.S. market.

In addition to the foregoing policy tools, two agreements signed by the U.S. Department of Commerce (DOC) in late 2014—one with the government of Mexico and another with Mexican sugar producers and exporters—impose annual limits on Mexican sugar exports to the United States and establish minimum prices for imported Mexican sugar.

The current sugar program has its roots in the Agriculture and Food Act of 1981 (P.L. 97-98), according to the USDA.1 The sugar program that Congress enacted in the 1981 farm bill required the Secretary of Agriculture to support prices of U.S. sugarcane and sugar beets at minimum levels—initially through purchases of processed sugar, and subsequently by offering nonrecourse loans. The legislation also encouraged the President to impose duties, fees or quotas on foreign sugar to prevent domestic prices from moving below established support levels to avoid imposing budgetary costs on the government. In its report on the 1981 farm bill, the Senate Committee on Agriculture, Nutrition and Forestry cited the importance of sugar imports to U.S. sugar supplies, pointing out that volatile world market prices of sugar contributed to sharp fluctuations in U.S. sugar prices, while adding that the United States was alone among sugar producing nations in being without an effective government price support program.2

The sugar program has long been a source of political controversy over the degree of government support and market intervention it involves with sharply differing perspectives on the balance of benefits and drawbacks to the program. Critics of the program, including the Coalition for Sugar Reform, which represents consumer, trade and commerce groups, manufacturing associations and food and beverage companies that use sugar, argue the sugar program acts to keep domestic prices far above world sugar prices. In so doing, the Coalition contends the sugar program imposes a hidden tax on consumers and has led to the loss of jobs in the food manufacturing sector by encouraging imports of sugar-containing products and by providing manufacturers with an incentive to move facilities abroad to gain access to lower priced sugar. The American Sugar Alliance, consisting of sugarcane and sugar beet producers, including farmers, processors, refiners, suppliers and sugar workers, is a leading advocate for the U.S. sugar program. It points out that the price support feature of the sugar program fosters a reliable supply of sugar at reasonable prices at no cost to the government. The sugar program, it argues, is necessary to shield the domestic sugar industry from unfair competition from sugar imports at world market prices that it contends are distorted by heavily subsidized foreign sugar that is dumped on the world market at prices that are below production costs (see "Sugar Program Draws Sharply Differing Views" below).

For background on sugar policy debate, see CRS Report R42551, Sugar Provisions of the 2014 Farm Bill (P.L. 113-79), by Mark A. McMinimy.

Price Support Loans

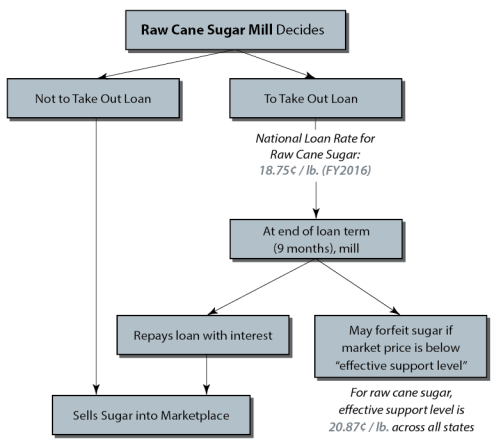

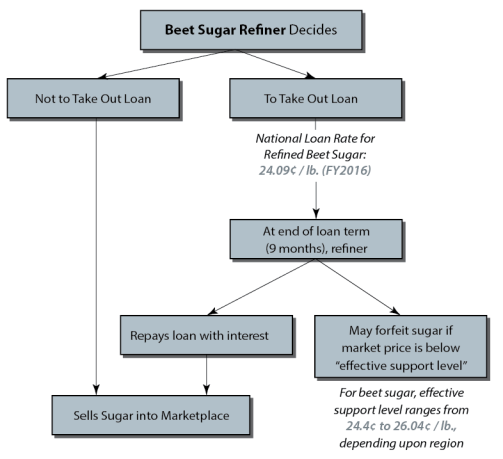

Nonrecourse loans taken out by a processor of a sugar crop, not producers themselves, provide a source of short-term, low-cost financing until a raw cane sugar mill or beet sugar refiner sells sugar. The "nonrecourse" feature means that processors—to meet their loan repayment obligation—can exercise the legal right to forfeit sugar offered as collateral to USDA to secure the loan, if the market price is below the effective support level when the loan comes due. Figure 1 and Figure 2 illustrate the repayment options available to raw cane sugar mills and beet sugar refiners, respectively, and show loan rates and effective support levels for FY2016.

The price levels at which processors can take out loans are referred to as "loan rates." The 2014 farm bill made no changes in the sugar program, so the current rates date from the 2008 farm bill, P.L. 110-246. The raw cane sugar loan rate (18.75¢/lb) is lower than the refined beet sugar loan rate (24.09¢/lb) to reflect its unprocessed state. The raw sugar loan rate is lower because raw sugarcane must be further processed by a cane refinery to have the same value and characteristics as refined beet sugar for food use. These loan rates are national averages. Actual loan rates are adjusted by region to reflect marketing cost differentials.

The minimum market price that a processor wants to receive in order to remove the incentive to forfeit sugar and instead repay a price support loan, though, is higher than the loan rate. This "effective support level," also called the loan forfeiture level, represents all of the costs that processors need to offset to make it economically viable to repay the loan. These costs equal the loan rate, plus interest accrued over the nine-month term of the loan, plus certain marketing costs. The effective support level for 2015-crop (FY2016) of raw cane sugar is 20.87¢/lb; for refined beet sugar, it ranges from 24.4¢ to 26.04¢/lb, depending on the region.

If market prices are below these loan forfeiture levels when a price support loan usually comes due (i.e., July to September), and a processor hands over sugar earlier pledged to obtain this loan rather than repaying it, USDA records a budgetary expense (i.e., an outlay). If this occurs, USDA gains title to the sugar and is responsible for disposing of this asset.

Two suspension agreements the DOC signed in December 2014—one with the Government of Mexico and another with Mexican sugar producers and exporters—have substantially modified the terms for importing sugar from Mexico and may have the practical effect of raising the effective support level.3 For one, Mexican sugar is an important source of the U.S. sugar supply, with imports of Mexican sugar averaging 15% of the sum of U.S. production plus imports during the three marketing years prior to the onset of the suspension agreements from 2011/2012 to 2013/2014.4 Imports of sugar from Mexico in 2014/2015, the year the suspension agreements took effect, represented 11% of the total of U.S. production plus imports.5 The agreements (see "Suspension Agreements Recast Sugar Trade with Mexico" below) establish minimum prices for Mexican sugar imports that are at, or above, effective U.S. support levels. These minimum prices are calculated at Mexican plants, so transportation costs to the U.S. processor or end user would add several cents per pound to the delivered cost of Mexican sugar. As a result, prices of imported Mexican sugar should track well above levels that would encourage U.S. loan forfeitures.

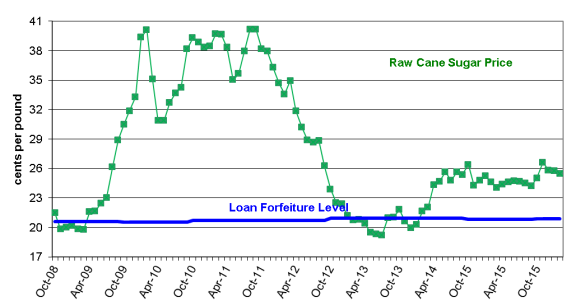

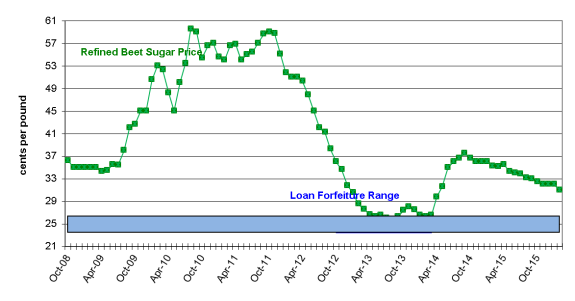

Market prices for raw cane sugar and refined beet sugar since the 2008 farm bill provisions took effect were higher than loan forfeiture levels until mid-year 2013 (Figure 3 and Figure 4, respectively). Toward the end of FY2013, market prices that were below these effective support levels prompted processors to forfeit, or hand over, to USDA 381,875 tons of sugar (4.3% of FY2013 U.S. sugar output valued at almost $172 million). USDA actions taken to avert these forfeitures, and then to dispose of sugar acquired as a result of these forfeitures, are detailed below in "Sugar Purchases and Exchanges for Import Rights" and "Feedstock Flexibility Program for Bioenergy Producers."

Tools for Balancing Supplies and Supporting Prices

The government sets annual limits on the quantity of domestically produced sugar that can be sold for human use. It also restricts the level of imports that may enter the domestic market through tariff-rate quotas and via an import limitation agreement with Mexico. This is done to avoid costs during times when an imbalance between sugar supplies and demand could lead to low prices and sugar forfeitures under the loan program.

Marketing Allotments

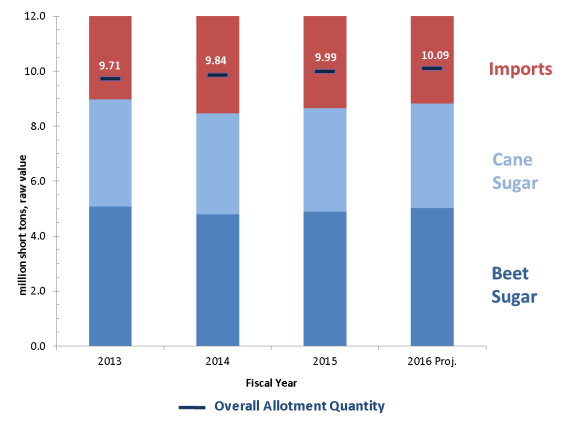

Sugar marketing allotments limit the amount of domestically produced sugar that processors can sell each year. They do not, however, limit how much beet and cane farmers can produce, nor do they limit how much sugar beets and sugarcane that beet refiners and raw sugar mills can process. In a 2008 farm bill provision that was retained in the 2014 farm bill, USDA is required each year to set the overall allotment quantity (OAQ) at not less than 85% of estimated U.S. human consumption of sugar for food. This task is carried out by the USDA's Commodity Credit Corporation (CCC) at the beginning of each fiscal year. The OAQ is intended to ensure that permitted sales of domestic sugar, when added to imports under U.S. trade commitments, do not depress market prices below loan forfeiture levels for refined beet sugar and raw cane sugar. Sugar production that is in excess of a processors' marketing allotment may not be sold for human consumption except to allow another processor to meet its allocation or for export.

In recent years, U.S. sugar production has consistently fallen short of the OAQ, averaging 88% of the OAQ threshold during the most recent three completed years from FY2013 through FY2015. Over this same period, U.S. sugar production has amounted to 74% of U.S. human use of sugar.

Figure 5 illustrates the persistent gap between domestic sugar production, the higher levels of the OAQ, and U.S. domestic consumption for human use. Substantial quantities of sugar have been imported to cover the shortfall between domestic output and human consumption. For this reason, market participants view USDA's decisions on setting import quotas rather than marketing allotments as having more of an impact on market price levels (see "Import Quotas").

The national OAQ is split between the beet and cane sectors and then allocated to processing companies based on previous sales and production capacity. If either sector is not able to supply sugar against its allotment, USDA has authority to reassign such a "shortfall" to imports.

Import Quotas

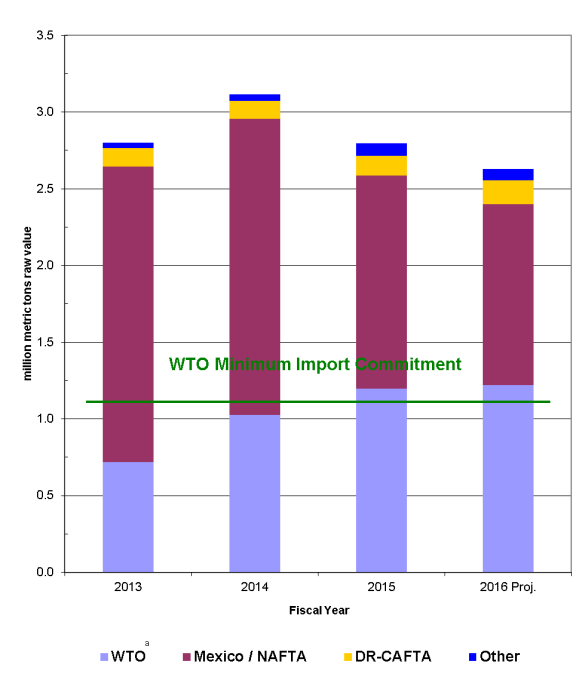

The United States imports sugar in order to meet total food demand. From FY2013 through FY2015, imports accounted for 30% of U.S. sugar used in food and beverages. The amount of foreign sugar supplied to the U.S. market reflects U.S. commitments made under various trade agreements. At the same time, a 2008 farm bill provision—one retained in the 2014 farm bill—directs USDA to manage overall U.S. sugar supply, including imports, so that market prices do not fall below effective support levels. The most significant import limit is the World Trade Organization (WTO) quota commitment, which requires the United States to allow not less than 1.256 million tons, raw value, of sugar (almost all raw cane) to enter the domestic market from 40 countries (equivalent to 1.139 million metric tons, raw value [MTRV]). The raw cane sugar tariff-rate quota (TRQ), representing 98% of the WTO minimum quota commitment of the United States, is allocated based on trade in sugar from 1975 to 1981, years during which this trade was relatively unrestricted.

The United States also grants much smaller import quotas to the six countries covered by the Dominican Republic-Central American Free Trade Agreement (DR-CAFTA), and to Colombia, Panama, and Peru under separate free trade agreements (FTAs). For calendar year 2016, the TRQ under these FTAs totals 140,580 MTRV for the DR-CAFTA countries, 53,000 tons for Colombia, 7,325 tons for Panama, and 2,000 tons for Peru.

Beyond these defined import commitments, unrestricted, duty-free access to Mexican sugar under the North American Free Trade Agreement (NAFTA) introduced uncertainty over how much sugar Mexico would ship north in any year. To illustrate, U.S. imports of Mexican sugar since 2008 have ranged from a low of about 800,000 tons in FY2010 to a high of almost 2.1 million tons in FY2013. This variability (Figure 6) in part reflects large swings in the amount of Mexican sugar available for export in any year, depending on the impact of drought in some years in Mexico's sugarcane-producing regions, and the degree to which U.S. exports of cheaper high-fructose corn syrup displace Mexican consumption of Mexican-produced sugar.

During the three most recently completed marketing years, FY2013-FY2015, Mexico was by far the largest source of U.S. sugar imports, supplying 55% of total U.S. sugar imports on average over this period. Reflecting Mexico's unique status as an unrestricted supplier up until December 2014, its annual shipments varied from a high of 2.1 million short tons, raw value (STRV)6, comprising 66% of U.S. sugar imports in FY2013, to a low of 1.5 million STRV, comprising 43% of U.S. imports in FY2015. Sugar entering the United States under tariff-rate quota programs during these three years amounted to 36% of all imports, with DR-CAFTA countries supplying a subtotal of nearly 4% of total U.S. sugar imports (Figure 6).

To address the market uncertainty expected from imports of Mexican sugar once it achieved unrestricted access in 2008, the 2008 farm bill introduced a new policy to regulate imports, and this policy was retained by the 2014 farm bill. The farm bill directed that at the beginning of each marketing year (October 1) USDA was required to set the WTO quotas for raw cane and refined sugar at the minimum level—1.256 million STRV—necessary to comply with this trade commitment (Figure 6). In case of an emergency shortfall of sugar prior to April 1, due to either weather or war, USDA was directed to increase these quotas. After April 1 (the midpoint of the marketing year), USDA may increase the WTO raw sugar quota consistent with the dual objectives of maintaining sugar prices above loan forfeiture levels and providing for adequate supplies of raw and refined sugar in the domestic market. Any increase in the import quota is temporary in that it applies only until the next marketing year, which begins on October 1.

|

TPP Agreement and U.S. Sugar Imports The Trans-Pacific Partnership (TPP) is a regional FTA that the United States concluded with 11 other Pacific Ocean–facing nations in October 2015 and was signed by the participating governments in February 2016. Among its provisions, the United States agreed to make available additional amounts of TRQ sugar exports to five countries. The total quantity involved amounts to 86,300 metric tons (MT) of sugar and sugar-containing products. Recipients of the additional TRQ sugar are Australia (65,500 MT), Canada (19,200 MT), Vietnam (1,500 MT), Malaysia (500 MT), and Japan (100 MT). If the agreement is implemented, this additional TRQ sugar would represent about 3% of U.S. sugar imports in FY2014/2015. Any additional sugar imports under TPP would not be expected to increase the likelihood of forfeitures under the U.S. sugar program; more likely, they would displace a portion of Mexican sugar exports to the United States. The reason for this outcome is that under the U.S.-Mexico bilateral suspension agreements of December 2014, Mexico has, in effect, become the "swing" (or residual) supplier of sugar to the U.S. market, so additional TRQ sugar would be expected to displace shipments of Mexican sugar. Importantly, the TPP agreement will not have the force of law for the United States unless Congress enacts implementing legislation.7 |

Suspension Agreements Recast Sugar Trade with Mexico

While the 2014 farm bill reauthorized the sugar program intact for five years through 2018 crops, events since enactment of the farm bill have materially altered the program. A major change with substantial repercussions for the U.S. sugar program in late 2014 concerned the treatment of imported sugar from Mexico. From 2008 until December 2014, Mexican sugar exports were accorded unrestricted, duty-free access to the U.S. market under NAFTA. Two suspension agreements that the U.S. government signed with the Government of Mexico and with Mexican sugar producers and exporters in December 2014 have fundamentally altered trade in sugar with Mexico while creating ripple effects for the sugar program and for sugar users. The two suspension agreements stem from parallel countervailing duty (CVD) and antidumping (AD) investigations initiated in the spring of 2014 by the International Trade Commission (ITC) and the International Trade Administration (ITA) of the DOC in response to a petition filed by the American Sugar Coalition (ASC). The ASC represents sugarcane and sugar beet producers, processors, refiners, and sugar workers. Sections 704 and 734 of the Tariff Act of 1930 (19 U.S.C. §1671(c) and §1673(c)), as amended, provide the legal authority for the CVD and AD suspension agreements.

Preliminary findings in the CVD investigation determined that the Mexican government was subsidizing Mexican sugar exports.8 The AD investigation concluded as a preliminary matter that Mexican sugar was being dumped into the U.S. market, that is, sold at less than fair value—defined as below the sale price in Mexico, or below the cost of production.9 The investigations determined these actions had injured the U.S. sugar industry, and based on these preliminary findings, the DOC imposed cumulative duties on U.S. imports of Mexican sugar to be deposited by U.S. importers of sugar, ranging from 2.99% to 17.01% under the CVD order, and from 39.54% to 47.26% under the AD order.

In December 2014, the U.S. Department of Commerce (DOC) entered into suspension agreements with the Government of Mexico and with Mexican sugar industry interests.10 Under the CVD agreement that DOC entered into with the Government of Mexico and the AD order that DOC signed with Mexican sugar producers and exporters, the DOC agreed to suspend both the CVD and AD investigations and to remove the duties it had imposed on imports of Mexican sugar. In return, the Government of Mexico agreed to relinquish the unrestricted access to the U.S. sugar market it had negotiated under NAFTA. Further, the Mexican government and Mexican producer groups and exporters also agreed to observe the certain restrictions on Mexican sugar exports to the United States.

The two suspension agreements have substantially recast U.S. sugar trade with Mexico by imposing three fundamental changes on Mexican sugar exports to the United States.

- Mexico's previously unlimited sugar exports to the U.S. market are henceforth limited to an assessment of U.S. needs, defined as the residual of projected U.S. human use less domestic production and imports from tariff-rate quota countries.

- Refined sugar exports from Mexico are limited to 53% of Mexico's allowable quantity in any given marketing year (October 1 to September 30), whereas previously no such restriction was in place.

- Mexican sugar is subject to minimum reference prices of $0.26 per pound for refined sugar and $0.2225 for all other sugar.11 Prior to the agreements, no floor price was imposed.

To determine the quantity of Mexican sugar that may be imported into the United States in a given marketing year under the suspension agreements, DOC is tasked with making an initial calculation of the domestic requirement for Mexican sugar in July. This quantity is subject to a recalculation in September, December, and March that may result in increases in quantity from the initial calculation. The agreement with the government of Mexico suspending countervailing duties states that Mexico's export limit is determined according to a calculation of U.S. needs that is based on a U.S. sugar carryover of 13.5%.12 The carryover, or stocks-to-use ratio (SUA), is the quantity of sugar available at the end of the marketing year (September 30) expressed as a percentage of annual usage. This formula has been a point of concern for some U.S. sugar users. The Sweetener Users Association, for one, has argued that an SUA of 13.5% is too restrictive of supplies and runs the risk of creating shortages in the domestic sugar market.13 In commenting on the draft suspension agreements, the Sweetener Users Association contended that an SUA of at least 14.5%, if not 15.5%, would be a more appropriate level.

In addition to imposing limits on the quantity of Mexican sugar that may be imported into the U.S. market, the agreements limit the concentration of Mexican sugar imports over the course of the marketing year to not more than 30% of the assessment of U.S. needs from October 1 through December 31 and not more than 55% from October 1 through March 31. For instance, in the wake of the agreement the initial export limit on Mexican sugar of 1,162,604.75 metric tons raw value for the 2014/2015 marketing year was subsequently increased to 1,383,969.68 metric tons raw value, which became effective on March 30, 2015.

Potential Effects on Government Outlays and Sugar Prices

In practice, the changes ushered in by the suspension agreements should greatly facilitate the USDA's task of operating the sugar program at no cost to the government, as Congress directed in the 2014 farm bill. Prior to the suspension agreements, imports of sugar from Mexico represented the only unmanaged source of supply under the sugar program. The USDA's ability to administer the sugar program at no net cost has been at issue since the 2012/2013 crop year, when net government outlays for the sugar program spiked to $259 million. That year, large quantities of domestic sugar under loan were forfeited in the face of excess supplies and low market prices. This obligated USDA to dispose of the forfeited sugar at a significant loss under the Feedstock Flexibility Program (FFP) and via exchanges in which the agency provided swapped forfeited domestic sugar for the right to import certain quantities of sugar.14

In an analysis issued in March 2015, the Food and Agricultural Policy Institute (FAPRI) at the University of Missouri projected net government outlays for the sugar program under two scenarios: with the suspension agreements, and without them. FAPRI concluded that under the suspension agreements net government outlays for sugar would be zero over marketing years 2016 through 2024. Without the agreements, FAPRI projected that annual outlays would average $16 million a year during marketing years 2016 through 2018, declining to $8 million a year on average from 2019 through 2024.15

In its March 2015 Baseline for Farm Programs, the Congressional Budget Office (CBO) projects government outlays for the sugar program at zero over the period FY2015 through FY2019. From FY2020 through FY2025 CBO projects outlays totaling $115 million, reflecting a likely re-examination of the agreement after five years and the potential for policy uncertainty over Mexican sugar imports thereafter.16 The USDA projects no sugar program costs through FY2026 based on the USDA Agricultural Projections to 2025 analysis, which assumes no changes in government agricultural policies and that existing trade arrangements remain in place.17

Assessing the potential for the suspension agreements to add to costs borne by sugar-using industries and consumers, the Coalition for Sugar Reform, representing consumer, trade, and commerce groups; manufacturing associations; and food and beverage companies that use sugar, contends that the suspension agreements will result in higher sugar prices for U.S. users and consumers. Following the signing of the suspension agreements in December 2014, the Coalition asserted, "These agreements will ensure that any Mexican sugar needed to adequately supply the U.S. market must be priced well above world market prices—prices that are even higher than mandated by the U.S. sugar program."18 The American Sugar Alliance, a coalition of sugar producers, including farmers, processors, refiners, sugar suppliers and workers, has expressed support for the agreements, contending they will foster free and fair trade in sugar, while benefiting U.S. sugar farmers, workers, consumers, and taxpayers.19

Considering that Mexican sugar is a significant source of U.S. sugar supplies that can vary in quantity from one year to the next, and considering also that minimum prices of Mexican sugar are at U.S. loan levels, or above them, without including transportation costs to U.S. destinations, it is evident that pricing on Mexican sugar should be well above U.S. loan levels as long as the suspension agreements remain in effect. Transportation from Mexican mills adds several cents per pound to the cost of sugar delivered to U.S. plants—as much as $0.03 to $0.06 per pound, according to FAPRI.

Two Sugarcane Refiners Challenging Suspension Agreements

Whether the new framework around trade in Mexican sugar imposed by the suspension agreements will remain in effect is not entirely certain. The agreements have no termination date, but the signatories may terminate them at any time. The suspended CVD and AD investigations are subject to a review after five years. Separately, two U.S. sugarcane refiners—Imperial Sugar Company and AmCane Sugar LLC—challenged the agreements in court. In January 2015, the two companies petitioned the U.S. International Trade Commission (ITC), contending the agreements do not eliminate completely the injurious effect of sugar imports from Mexico as the law permitting such agreements requires.20 In a unanimous decision issued in March 2015, the ITC concluded the agreements do eliminate entirely the injurious effect of Mexican sugar imports.21 In the wake of the ITC's determination, the two cane refiners filed petitions with the U.S. Court of International Trade, contending that the ITC's determination was not supported by the evidence and was not in accordance with the governing statute. The complaints were consolidated by the court, but AmCane's action was dismissed at the company's request in early April 2016, while the action brought by Imperial Sugar continued to be under review.

On a separate track, the two cane refining companies also petitioned the DOC to continue the CVD and AD investigations to final determinations. In early May 2015, the DOC determined the two sugar-refining companies had standing under the law to make such a petition and announced it would resume the CVD and AD investigations.22 Pending final determinations in these investigations, the terms of the suspension agreements remained in force. In September 2015, the DOC issued its final determinations, affirming its preliminary findings that, prior to the entry into force of the suspension agreements, Mexican sugar exports were being subsidized by the government and dumped into the U.S. market at prices below their fair market value. The DOC found that dumping margins on Mexican sugar ranged from 40.48% to 42.14%, depending on the producer/exporter, and that government subsidies on exported sugar ranged from 5.78% to 43.93%. Following these determinations, the ITC reaffirmed its earlier finding that the U.S. sugar industry was injured as a result of these practices.23 As a consequence, the suspension agreements remain in force pending a decision by the U.S. Court of International Trade.

Mechanisms Aimed at Countering Low Prices

In addition to domestic marketing allotments and import quotas and limits, USDA has two policy mechanisms to help prevent prices from slipping below effective loan forfeiture levels, thereby limiting program costs that might otherwise accrue to the government as a result of substantial loan forfeitures. These include offering CCC sugar to processors in exchange for surrendering rights to import tariff-rate quota sugar; purchasing sugar from processors in exchange for surrendering tariff-rate quota sugar; and removing sugar from the human food market by purchasing sugar from processors for resale to ethanol producers for fuel ethanol production.

Sugar Purchases and Exchanges for Import Rights

To dispose of sugar owned by CCC without increasing the risk of loan forfeitures, the farm bill authorizes USDA to transfer ownership of CCC-owned sugar in exchange for rights to purchase tariff-rate quota sugar, or certificates of quota entry, which carry a low tariff rate or zero tariff. From July to September 2013, USDA completed four sugar "exchanges" in an effort to bolster market prices and forestall loan forfeitures of some 2012 crop sugar. Two exchanges involved bids made by refiners and brokers for sugar acquired by USDA from processors as a result of loan forfeitures in return for surrendering import rights. Two other exchanges involved USDA purchasing sugar from processors, which then was exchanged for import rights that cane refiners and brokers surrendered to USDA. The latter two initiatives were taken to reduce the amount of sugar expected to be supplied to the U.S. market and were implemented by USDA using 1985 farm bill authority. This cost reduction provision authorizes USDA to purchase a supported commodity deemed to be in surplus if such action results in program savings.

Feedstock Flexibility Program for Bioenergy Producers

If market prices fall to levels that threaten to result in loan forfeitures, the Secretary of Agriculture may purchase surplus sugar and sell it to bioenergy producers to avoid forfeitures. In the event that forfeitures of sugar loans do occur, the Secretary is required to administer a sugar-for-ethanol program using domestic sugar intended for food use. The objective of this Feedstock Flexibility Program (FFP) is to permanently remove sugar from the market for human consumption by diverting it into a non-food use—ethanol. When the Secretary activates this program, USDA will purchase surplus and other sugar acquired from processors and then sell that sugar to bioenergy producers for processing into fuel-grade ethanol and other biofuels. Competitive bids would be used by USDA to purchase sugar from processors and also to sell that sugar (together with any sugar forfeited by processors) to ethanol producers. An exception to the requirement to activate this program is that forfeited sugar may be sold back into the market for human food use in the event of an emergency shortfall of sugar. In August and September 2013, USDA activated this program as remaining loans came due and sugar prices headed below effective support levels (Figure 3 and Figure 4).

Sugar Program Draws Sharply Differing Views

The sugar program has long been the subject of controversy, both among lawmakers and among competing interests within the sugar market. In part, disagreement over the sugar program has centered on whether it strikes the right balance between government support for the domestic sugar industry in the face of subsidized foreign sugar and the cost this support may impose on sugar users and consumers in the form of marketplace distortions and potentially higher sugar prices than might otherwise prevail.

From one side of this controversy, the American Sugar Alliance (ASA), representing U.S. sugar industry interests, asserts that even though U.S. sugar producers are among the most efficient in the world, they cannot compete with foreign subsidies that encourage the production of surpluses that are dumped onto the world market at prices that are often below the cost of production.24 As to the competitiveness of U.S. sugar prices, ASA issued the results of a study from 2015 that indicated that U.S. retail prices of sugar in 2014 were below the average for developed countries and also below the average retail price in some major exporting countries, including Brazil and Australia.25

The Sugar Users Association, representing companies that use sweeteners in their business operations, has a very different perspective on this issue, contending that the sugar program is poorly designed. In particular, it argues that TRQ allocations are dated and that this has the effect of restricting export quotas to certain countries that in some cases either cannot fill their entire quotas or may not ship any sugar to the United States. As such, it asserts the TRQ program tends to distort and destabilize the U.S. sugar market, which it argues has led to job losses in sugar-using food industries.26

As to whether the sugar program harms consumers through higher sugar prices, an analysis issued in 2013 by the Center for Agricultural and Rural Development at Iowa State University concluded that eliminating the U.S. sugar program—including marketing allotments and import quotas and tariffs that restrict the availability of sugar for domestic human use—would increase U.S. consumers' welfare by between $2.9 billion and $3.5 billion each year while also supporting a modest increase in employment in the U.S. food processing industry.27 The paper was commissioned by the Sweetener Users Association.

The ITC took a narrower approach to this question in a report from 2013 that analyzed the potential effects of removing only the existing restrictions on U.S. sugar imports.28 The ITC concluded that removing sugar import restrictions would result in a meaningful decline in U.S. sugar production and employment within the sugar production and processing sectors in tandem with a substantial expansion in total U.S. sugar imports. As for sugar prices, the report projected that the elimination of import restrictions would produce welfare gains for U.S. consumers amounting to $1.66 billion over the period 2012-2017, equating to a yearly benefit of $277 million.

Administrative Year in the Sugar Program

The text box below sets out specific dates, and calendar windows, for undertaking key administrative actions that are integral to managing the U.S. sugar program.

|

U.S. Sugar Program Calendar of Administrative Actions In July, DOC is to calculate the "export limit" for Mexican sugar for the U.S. market for the upcoming marketing year (October-September), which is to be 70% of the projection of the "target quantity of U.S. needs" for Mexican sugar based on the USDA's July World Agricultural Supply and Demand Estimates (WASDE) report. The export limit becomes effective October 1. On September 1, the Secretary of Agriculture is to announce the amount of sugar (if any) that the Commodity Credit Corporation (CCC) is to purchase prior to the end of the current marketing year (September 30) to avoid loan forfeitures. Any purchases are to be resold for ethanol production under the Feedstock Flexibility Program (FFV). In September, a subsequent calculation of the target quantity of U.S. needs is to be carried out based on the September WASDE with the export limit to remain at 70% of the target quantity. The new export limit quantity cannot be below the export limit announced in July. By September 30, USDA must announce sugar loan rates for the year beginning October 1. By October 1, USDA is to establish domestic human consumption of sugar for the new marketing year (October-September) and also establish domestic marketing allotments for sugarcane and sugar beet processors. By October 1, the Secretary of Agriculture sets initial sugar import quotas for the new marketing year (October-September) at the minimum levels that are required to comply with international trade agreements, except for refined sugar. By October 1, USDA is to announce the amount of sugar, if any, the CCC is to purchase in current crop year that is to be made available for sale under the FFV, and to re-estimate this amount and provide notice by Jan. 1, April 1, and July 1. From October 1 to March 31, In the event of an emergency shortfall of sugar because of war or natural disaster, the Secretary of Agriculture is to act to increase the supply of sugar in a manner consistent with avoiding loan forfeitures and maintaining adequate supplies of raw and refined sugar—first by increasing the TRQ for raw cane sugar to allow a reassignment to imports and, secondly, if the shortage persists and if domestic raw cane sugar refining capacity has been maximized, by increasing the TRQ for refined sugars. In December, DOC is to recalculate the target quantity for Mexican sugar for the current marketing year based on the December WASDE report. The export limit is to be raised to 80% of target quantity as of January 1. The new export limit quantity cannot be below the September export limit. In March, DOC is to recalculate the target quantity for Mexican sugar based on the March WASDE report. The export limit is to be raised to 100% of target quantity as of April 1. The new export limit quantity cannot be below the December export limit. Prior to April 1, DOC may increase the export limit on Mexican sugar to address potential shortages in the U.S. market. From April 1, the Secretary may increase the Overall Allotment Quota and the tariff rate quotas that restrain imports of sugar in the event of an emergency shortfall of sugar. From April 1, tariff rate quotas on imported sugar may be increased as long as doing so will not threaten to result in forfeitures under the sugar loan program. After April 1, DOC may increase the export limit on Mexican sugar in response to a written request from USDA citing the need for additional imports of Mexican sugar. |

Author Contact Information

Footnotes

| 1. |

USDA, ERS Sugar & Sweeteners at http://www.ers.usda.gov/topics/crops/sugar-sweeteners/policy.aspx. |

| 2. |

Report of the Senate Committee on Agriculture, Nutrition, and Forestry to accompany S. 884, May 27, 1981. |

| 3. |

See Agreement Suspending the Countervailing Duty Investigation on Sugar from Mexico at http://enforcement.trade.gov/agreements/sugar-mexico/CVD-Agreement.pdf; also, Agreement Suspending the Antidumping Duty Investigation on Sugar from Mexico at http://enforcement.trade.gov/agreements/sugar-mexico/AD-Agreement.pdf. |

| 4. |

The marketing year for U.S. sugar is the same as the U.S. government's fiscal year: October1-September 30. |

| 5. |

USDA, Economic Research Service, Sugar and Sweeteners Outlook, March 15, 2016. |

| 6. |

A short ton is equivalent to 2,000 pounds. Raw value is a factor of 1.07 of refined value, according to USDA, except for Mexican sugar for which raw value is a factor of 1.06 of the actual weight of the shipped product. |

| 7. |

For additional background on the TPP agreement, see CRS Report R44278, The Trans-Pacific Partnership (TPP): In Brief, by Ian F. Fergusson, Mark A. McMinimy, and Brock R. Williams. |

| 8. |

See U.S. Department of Commerce Fact Sheet of August 26, 2014, at http://enforcement.trade.gov/download/factsheets/factsheet-mexico-sugar-ad-prelim-082614.pdf. |

| 9. |

See U.S. Department of Commerce Fact Sheet of October 27 at http://enforcement.trade.gov/download/factsheets/factsheet-mexico-sugar-ad-prelim-102714.pdf. |

| 10. |

For the text of the two agreements suspending countervailing duties and antidumping duties, see http://enforcement.trade.gov/agreements/sugar-mexico/index.html. |

| 11. |

Prices are based on dry weight, commercial value, f.o.b. at Mexican plants. |

| 12. |

See agreement suspending countervailing duties at http://enforcement.trade.gov/agreements/sugar-mexico/index.html. |

| 13. |

See "Comments of Sweetener User Association on Draft Agreements Suspending Antidumping and Countervailing Duty Investigations on Sugar from Mexico of November 18, 2014," http://sugarreform.org/wp-content/uploads/2014/11/SUA-Comments-re-Draft-Agreements.pdf, |

| 14. |

See U.S. International Trade Commission publication 4467, Sugar from Mexico, p. 27, http://usitc.gov/publications/701_731/pub4467.pdf. |

| 15. |

Impacts of the U.S.-Mexico Antidumping and Countervailing Duty Suspension Agreement, FAPRI, March 27, 2015, at http://www.fapri.missouri.edu/wp-content/uploads/2015/03/FAPRI-MU-Bulletin-07-15.pdf. |

| 16. |

Telephone conversation of April 1, 2015, with Dave Hull, Congressional Budget Office. |

| 17. |

See USDA, Economic Research Service, Sugar and Sweeteners Outlook, March 15, 2016, http://www.ers.usda.gov/media/2030300/sss-m-331-mar2016-final.pdf. |

| 18. |

Coalition for Sugar Reform press release of December 22, 2014, at http://sugarreform.org/wp-content/uploads/2011/07/CSR-AD-CVD-Agreements-Signed-12-22-14-FINAL.pdf. |

| 19. |

American Sugar Alliance press release of March 19, 2015, at http://www.sugaralliance.org/itc-suspension-agreements-remove-the-injury-caused-by-unfairly-traded-mexican-sugar-5245/. |

| 20. |

CVD: 19U.S.C. §1671c(c); AD: 19 U.S.C. §1673c(c). |

| 21. |

See U.S. ITC press release of March 19, 2015, at http://www.usitc.gov/press_room/news_release/2015/er0319ll436.htm. |

| 22. |

Federal Register notice of May 4, 2015, at https://www.federalregister.gov/articles/2015/05/04/2015-10253/sugar-from-mexico-continuation-of-antidumping-and-countervailing-duty-investigations. |

| 23. |

See ITC, Sugar from Mexico, https://www.usitc.gov/publications/701_731/pub4577.pdf. |

| 24. |

See testimony of Jack Roney, American Sugar Alliance, before the House Committee on Agriculture, October 21, 2015, at http://agriculture.house.gov/uploadedfiles/10.21.15_roney_testimony.pdf. |

| 25. |

See Global Retail Sugar Prices, July 2015, https://sugaralliance.org/wp-content/uploads/2015/08/SIS-Global-Sugar-Price-Survey-2015-Summary.pdf. |

| 26. |

See Thomas Earley, oral statement on behalf of the Sweetener Users Association to the U.S. International Trade Commission, March 19, 2013, http://www.sweetenerusers.org/Tom%20Earley%20ITC%20SUA%20Oral%20statement%20-%203-19-13%20FINAL.pdf. |

| 27. |

See The Impact of the Sugar Program Redux, 2013, at http://www.card.iastate.edu/publications/synopsis.aspx?id=1183. |

| 28. |

See The Economic Effects of Significant U.S. Import Restraints (Publication 4440) at http://www.usitc.gov/publications/332/pub4440.pdf. |