The Financial CHOICE Act in the 115th Congress: Selected Policy Issues

The Financial CHOICE Act (FCA; H.R. 10) was introduced on April 26, 2017, by Representative Jeb Hensarling, chairman of the House Committee on Financial Services. It passed the House on June 8, 2017. Selected provisions of H.R. 10 were then added to the appropriations bill passed by the House (H.R. 3354).

H.R. 10, as passed, is a wide-ranging proposal with 12 titles that would alter many parts of the financial regulatory system. Much of the FCA is in response to the Dodd-Frank Wall Street Reform and Consumer Protection Act (Dodd-Frank Act; P.L. 111-203), a broad package of regulatory reform following the financial crisis that initiated the largest change to the financial regulatory system since at least 1999. Many of the provisions of the FCA would modify or repeal provisions from the Dodd-Frank Act, although others would address long-standing or more recent issues.

This report highlights major proposals included in the FCA but is not a comprehensive summary. In general, the bill proposes changes that can be divided into two categories: (1) changes to financial policies and regulations and (2) changes to the regulatory structure and rulemaking process.

Major policy-related changes proposed by the FCA include the following:

Leverage Ratio—allowing a banking organization to choose to be subject to a higher, 10% leverage ratio in exchange for being exempt from risk-weighted capital ratios, liquidity requirements, enhanced prudential regulation (if the bank has more than $50 billion in assets), and other regulations.

Regulatory Relief—providing regulatory relief throughout the financial system to banks, consumers, and capital market participants, including by repealing the Volcker Rule, fiduciary rule, and risk retention requirements for nonmortgage asset-backed securities. Some provisions are targeted at small financial institutions or issuers, whereas others provisions are applied across the board.

Too Big To Fail—repealing the designation of systemically important nonbank financial institutions, repealing or restricting authority to provide emergency assistance to financial markets, and replacing an option for winding down systemic institutions with a new chapter in the Bankruptcy Code that is tailored to financial firms.

Structural and procedural changes that affect the balance between regulator independence from and accountability to Congress and the judiciary include the following:

Funding—subjecting regulators that currently set their own budgets to the traditional congressional appropriations process.

Rulemaking—requiring regulators to perform more detailed cost-benefit analysis when issuing new rules and to use cost-benefit analysis to review existing rules, as well as requiring congressional approval for a major rule to come into effect.

Judicial Review—requiring courts to apply a heightened judicial review standard for agency actions taken by financial regulators rather than applying varying levels of deference to the agencies’ interpretations of the law.

Enforcement—increasing the maximum civil penalties that could be assessed for violations of certain banking and securities laws and restraining certain agency enforcement powers.

CFPB—replacing the Consumer Financial Protection Bureau with the Consumer Law Enforcement Agency and modifying its powers, leadership, mandate, and funding. The new agency would not have the CFPB’s examination or supervisory powers, but would have similar enforcement powers. Its director would be removable at-will by the President.

Federal Reserve—requiring a GAO audit of the Fed, restricting emergency lending, and requiring the Fed to compare its monetary policy decisions to a mathematical rule.

The Financial CHOICE Act in the 115th Congress: Selected Policy Issues

Jump to Main Text of Report

Contents

- Introduction

- Regulatory Relief

- Leverage Ratio as an Alternative to Current Bank Regulation

- Volcker Rule

- Relief for Small Capital Issuers

- Fiduciary Rule

- Risk Retention

- Executive Compensation

- Systemically Important ("Too Big To Fail") Financial Institutions

- Regulating Systemically Important Financial Institutions and Limiting Their Size

- Resolving a Failing TBTF Firm and Preventing "Bailouts"

- Changes to Regulatory Authority

- Appropriations

- Consumer Financial Protection Bureau

- Federal Reserve

- Rulemaking

- Cost-Benefit Analysis

- Congressional Review of Federal Financial Agency Rulemaking

- Judicial Review of Administrative Rulemakings

- Enforcement Powers

Tables

- Table 1. Overview of Federal Financial Regulators Discussed in this Report

- Table 2. Institutions Designated by FSOC as Systemically Important

- Table 3. Current Funding for Financial Regulatory Agencies

- Table A-1. Selected Changes to the Dodd-Frank Act in the Financial CHOICE Act

- Table B-1. Provisions of the Financial CHOICE Act in the Appropriations Omnibus

- Table C-1. CRS Contact Information

Summary

The Financial CHOICE Act (FCA; H.R. 10) was introduced on April 26, 2017, by Representative Jeb Hensarling, chairman of the House Committee on Financial Services. It passed the House on June 8, 2017. Selected provisions of H.R. 10 were then added to the appropriations bill passed by the House (H.R. 3354).

H.R. 10, as passed, is a wide-ranging proposal with 12 titles that would alter many parts of the financial regulatory system. Much of the FCA is in response to the Dodd-Frank Wall Street Reform and Consumer Protection Act (Dodd-Frank Act; P.L. 111-203), a broad package of regulatory reform following the financial crisis that initiated the largest change to the financial regulatory system since at least 1999. Many of the provisions of the FCA would modify or repeal provisions from the Dodd-Frank Act, although others would address long-standing or more recent issues.

This report highlights major proposals included in the FCA but is not a comprehensive summary. In general, the bill proposes changes that can be divided into two categories: (1) changes to financial policies and regulations and (2) changes to the regulatory structure and rulemaking process.

Major policy-related changes proposed by the FCA include the following:

- Leverage Ratio—allowing a banking organization to choose to be subject to a higher, 10% leverage ratio in exchange for being exempt from risk-weighted capital ratios, liquidity requirements, enhanced prudential regulation (if the bank has more than $50 billion in assets), and other regulations.

- Regulatory Relief—providing regulatory relief throughout the financial system to banks, consumers, and capital market participants, including by repealing the Volcker Rule, fiduciary rule, and risk retention requirements for nonmortgage asset-backed securities. Some provisions are targeted at small financial institutions or issuers, whereas others provisions are applied across the board.

- Too Big To Fail—repealing the designation of systemically important nonbank financial institutions, repealing or restricting authority to provide emergency assistance to financial markets, and replacing an option for winding down systemic institutions with a new chapter in the Bankruptcy Code that is tailored to financial firms.

Structural and procedural changes that affect the balance between regulator independence from and accountability to Congress and the judiciary include the following:

- Funding—subjecting regulators that currently set their own budgets to the traditional congressional appropriations process.

- Rulemaking—requiring regulators to perform more detailed cost-benefit analysis when issuing new rules and to use cost-benefit analysis to review existing rules, as well as requiring congressional approval for a major rule to come into effect.

- Judicial Review—requiring courts to apply a heightened judicial review standard for agency actions taken by financial regulators rather than applying varying levels of deference to the agencies' interpretations of the law.

- Enforcement—increasing the maximum civil penalties that could be assessed for violations of certain banking and securities laws and restraining certain agency enforcement powers.

- CFPB—replacing the Consumer Financial Protection Bureau with the Consumer Law Enforcement Agency and modifying its powers, leadership, mandate, and funding. The new agency would not have the CFPB's examination or supervisory powers, but would have similar enforcement powers. Its director would be removable at-will by the President.

- Federal Reserve—requiring a GAO audit of the Fed, restricting emergency lending, and requiring the Fed to compare its monetary policy decisions to a mathematical rule.

Introduction

In the 114th Congress, the Financial CHOICE Act of 2016 (H.R. 5983) was sponsored by Representative Jeb Hensarling, chairman of the House Committee on Financial Services. The bill was reported by the House Committee on Financial Services on December 20, 2016. In the 115th Congress, a modified version of the CHOICE Act was introduced as the Financial CHOICE Act of 2017 (H.R. 10, FCA) on April 26, 2017. It passed the House on June 8, 2017. This report describes the FCA as passed in the 115th Congress.1 The Congressional Budget Office estimated that a similar version of the bill would reduce budget deficits by $33.6 billion over the next 10 years.2

|

The Financial CHOICE Act and FY2018 Appropriations Selected provisions of the Financial CHOICE Act were included in the FY2018 Financial Services and General Government Appropriations Act (H.R. 3280), which was reported by the House Appropriations Committee on July 18, 2017. For more information, see Appendix B. H.R. 3280 was then combined with other appropriation bills in H.R. 3354, which passed the House on September 14, 2017. |

The FCA is a wide-ranging proposal with 12 titles that would alter many parts of the financial regulatory system. Many of the provisions can be categorized as providing regulatory relief to financial firms, investors, or borrowers. Other provisions alter the financial regulatory architecture or change the relationship between financial regulators and Congress or the judiciary. For background and reference, Table 1 lists the federal financial regulators and their general responsibilities.

|

Name/Acronym |

Composition/General Responsibilities |

|

Regulator |

|

|

Commodity Futures Trading Commission (CFTC) |

Regulation of derivatives markets |

|

Consumer Financial Protection Bureau (CFPB) |

Regulation of financial products for consumer protection |

|

Federal Deposit Insurance Corporation (FDIC) |

Provision of deposit insurance, regulation of banks, receiver for failing banks |

|

Federal Housing Finance Agency (FHFA) |

Regulation of housing government sponsored enterprises |

|

Federal Reserve System (Fed)a |

Monetary policy; regulation of banks, systemically important financial institutions, and the payment system |

|

National Credit Union Administration (NCUA) |

Provision of deposit insurance, regulation of credit unions, receiver for failing credit unions |

|

Office of the Comptroller of the Currency (OCC) |

Regulation of banks |

|

Securities and Exchange Commission (SEC) |

Regulation of securities markets |

|

Other Federal Financial Entities |

|

|

Financial Stability Oversight Council (FSOC) |

Council of financial regulators and state and industry representatives accountable for financial stability |

|

Office of Financial Research (OFR) |

Provides research support to FSOC |

Source: Table compiled by the Congressional Research Service (CRS).

Notes: The Financial CHOICE Act of 2017 (FCA) would replace the CFPB with the newly created Consumer Law Enforcement Agency (CLEA). For more information on the roles, duties, and responsibilities of the federal financial regulators, see CRS Report R44918, Who Regulates Whom? An Overview of the U.S. Financial Regulatory Framework, by Marc Labonte.

a. The Federal Reserve System is composed of the Board of Governors and 12 regional Federal Reserve banks. Unless otherwise noted, provisions of the FCA involving the Fed affect the Board of Governors.

Many parts of the FCA would repeal or amend provisions of the Dodd-Frank Wall Street Reform and Consumer Protection Act (Dodd-Frank Act),3 a broad package of regulatory reform legislation passed following the 2007-2009 financial crisis that initiated the largest change to the financial regulatory system since at least 1999 (see Appendix A). President Trump has called for the Dodd-Frank Act to be "dismantled," and Chairman Hensarling has characterized the FCA as "work(ing) with the president to end and replace the Dodd-Frank mistake."4 The minority on the House Financial Services Committee stated that the FCA "dismantles critical safeguards included in the Dodd-Frank Wall Street Reform and Consumer Protection Act (Dodd-Frank), the law that was put in place to protect the American economy from another financial crisis. Dodd-Frank improves accountability in the financial system and protects consumers, investors, and the economy from abusive Wall Street practices."5 Although many of the provisions of the bill focus on parts of the Dodd-Frank Act, others would address long-standing or more recent issues.

This report highlights major policy proposals in the version of the bill as passed in the 115th Congress, but it is not a comprehensive summary of the bill. It provides context for these proposals in the form of background and policy debate. This report also includes an experts' contact list for FCA topics in Appendix C.

Regulatory Relief

As financial regulators have implemented the Dodd-Frank Act and other reforms, some Members of Congress argue that the pendulum has swung too far toward excessive regulation. As a result, they argue that additional regulatory burden—the cost associated with government regulation and its implementation—has stymied economic growth and restricted consumer and business access to credit. Other Members, however, contend the current regulatory structure has appropriately strengthened financial stability and increased protections for consumers and investors. They are concerned that regulatory relief for financial institutions could negatively affect consumers and market stability.

In determining whether to provide regulatory relief, a central question is whether an appropriate trade-off has been struck between the benefits and costs of regulation. In other words, can relief be provided while maintaining the stability of the financial system and ensuring taxpayers, consumers, and investors are protected, or would relief undermine those goals? Regulatory relief is generally focused on the financial services providers—such as banks, broker-dealers, and other institutions—but what effect would relief have on consumers, investors, particular markets, and market stability more broadly? The answers to these and other policy questions will vary based on the particulars of the relief being proposed.

The FCA would provide regulatory relief to two broad categories—banks and securities markets' participants.

The FCA would provide regulatory relief to banks through more than two dozen provisions. Some of the proposals are aimed at assisting community banks, whereas others would apply to all banks, regardless of size. Some provisions provide relief from regulations, whereas others target supervisory practices. Many would modify or repeal rules stemming from the Dodd-Frank Act, whereas others target long-standing regulatory practices. This report highlights two provisions providing relief to banks—the Volcker Rule and the leverage ratio.

Many of the securities-related provisions in the FCA provide regulatory relief with the aim of facilitating capital formation. Among the over three dozen securities-related provisions in the FCA are provisions that relax restrictions on who is eligible to invest in certain types of securities, including venture capital investors; provisions that relax regulatory requirements on licensed professionals in the securities industry, including private equity advisers, private funds, municipal advisors, investment fund researchers, and credit rating agencies; and provisions that relax regulatory requirements for firms that issue capital or securities, including emerging growth companies, risk retention requirements for nonmortgage securitizers, firms subject to disclosures on conflict minerals, and companies raising funds via crowdfunding or from angel investors. Many of these issues are discussed in further detail below.

Leverage Ratio as an Alternative to Current Bank Regulation6

Background

With more than 500 banks failing between 2007 and 2014,7 strengthening prudential regulation has been a major goal of postcrisis financial reforms. Prudential regulation covers a broad set of a bank's activities, including assessing whether a bank will be able to meet its obligations during a market downturn, evaluating the quality of its assets and management team, and other factors. One of the main areas of focus is bank capital adequacy.

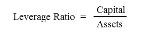

Capital is the difference between the value of a bank's assets and its liabilities and is an indicator of a bank's ability to absorb losses. For example, if a bank has $100 worth of assets and $90 of liabilities, then the bank has capital of $10. If the value of the assets decreases by $5 to $95 and the bank still has $90 in liabilities, then the $5 decline in asset value would be absorbed by the capital, which would decrease from $10 to $5.

Capital requirements are stated as the ratio of capital to the bank's assets. Banks are required to satisfy several different capital ratios, but the ratios fall into two main categories: (1) a leverage ratio and (2) a risk-weighted asset ratio. Failure to satisfy the required ratios could lead to regulators taking corrective action against a bank, including ultimately shutting the bank down.

Under a leverage ratio, all assets regardless of riskiness are treated the same and the ratio is calculated by dividing capital by assets. A 10% leverage ratio, for example, would imply $10 of capital for every $100 of assets. Under a risk-weighted asset ratio, each asset is assigned a risk weight to account for the fact that some assets are more likely to lose value than others. Riskier assets receive a higher risk weight, which requires banks to hold more capital—and so be better able to absorb losses—to meet the ratio requirement.

|

Leverage Ratio and Risk-Weighted Ratio Sample Calculations

|

|

|

The specifics of the capital ratios—what the minimum levels are, what qualifies as capital, what the asset risk weights are, what is included in total assets—were proposed by the Basel Committee on Bank Supervision and then implemented by the U.S. financial regulators.8 The Basel Committee "is the primary global standard-setter for the prudential regulation of banks and provides a forum for cooperation on banking supervisory matters."9 The most recent comprehensive reform proposal is referred to as Basel III.

The capital ratios that a bank must satisfy and how those levels are computed varies based on a bank's size and complexity. The largest banks are required to hold more capital than smaller, less complex banks.10 In regard to the simple leverage ratio, most banks are required to meet a 4% leverage ratio.11 Large banks must also comply with a supplementary leverage ratio ranging from 3% to 6% depending on their size and the organizational unit within the bank.12 The supplementary leverage ratio is more expansive than the leverage ratio because it takes into account certain off-balance-sheet assets and exposures.

Policy Issues

Some economists argue that it is important to have both a risk-weighted ratio and a leverage ratio because the two complement each other.13 A basic tenet of finance is that riskier assets have a higher expected rate of return to compensate the investor for bearing more risk. Without risk weighting, banks would have an incentive to hold riskier assets because capital is costly and the same amount of capital must be held against riskier and safer assets. For example, banks might decide to shift out of certain lines of business that involve holding large amounts of safe assets, such as cash, if risk-weighted ratios were replaced by a higher leverage ratio. But relying solely on risk-weighted ratios could be problematic, because the weight assigned to an asset may in fact be an inaccurate measure of its riskiness and therefore distort bank behavior. For example, banks held highly rated mortgage-backed securities (MBSs) before the crisis, in part because those assets had a higher expected rate of return than other assets with the same risk weight. The crisis revealed that MBSs were more risky than their risk weights indicated, and banks holding them suffered unexpectedly large losses. Thus, the leverage ratio can be thought of as a backstop to ensure that incentives posed by risk-weighted capital ratios do not result in a bank holding insufficient capital.

Others argue that the risk-weighted system provides "needless complexity" and is an example of "central planning." The complexity generally benefits those largest banks that have the resources to absorb the added regulatory cost. They contend that the risk weights in place prior to the financial crisis were poorly calibrated and "encouraged financial firms to crowd into these" unexpectedly risky assets, exacerbating the downturn. Risk weighting may encourage regulators to set the weights so as "to provide a cheaper source of funding for governments and projects favored by politicians," which can lead to a distortion in credit allocation. Better, they argue, to eliminate the risk-weighted system for those banks that agree to hold more capital and satisfy a higher, simpler leverage ratio.14

In addition to the issue of whether it is better to have both a risk-weighted ratio and a leverage ratio or only a leverage ratio is the broader issue of the role of capital in bank regulation. Those who argue in favor of having only a higher leverage ratio also generally support eliminating some other forms of prudential regulation, such as liquidity requirements, asset concentration guidelines, and counterparty limits. They argue that, so long as sufficient capital is in place in case of losses, banks should not be subject to excessive regulatory micromanagement.15 Others, however, contend that the different components of prudential regulation each play an important role in ensuring the safety and soundness of financial institutions and are essential complements to bank capital.16 In other words, capital can absorb losses, but unlike other forms of prudential regulation, it cannot make losses less likely.

Provision in the FCA

Under the FCA, a banking organization could choose to be subject to a higher, 10% leverage ratio,17 and in exchange would be exempt from risk-weighted capital ratios; liquidity requirements; stress-test requirements; certain merger, acquisition, and consolidation restrictions; limitations on dividends; and other regulations.18 A bank would have the option to follow current regulatory requirements or this new regulatory approach.

Some of the regulations from which a bank could receive relief are regulations that apply to all banks, such as the risk-weighted capital ratios set by Basel III. Other regulations from which a bank could receive relief under the FCA would only apply to larger banks (with an asset threshold of $50 billion to $700 billion, depending on the provision). For example, banks opting in to the new leverage ratio approach would be exempt from the Dodd-Frank Act's enhanced prudential regulations for banks with $50 billion or more in assets and other regulations based on financial stability considerations (discussed in "Regulating Systemically Important Financial Institutions and Limiting Their Size").

Although a 10% leverage ratio is significantly more capital than what banks are currently required to hold, it is not necessarily more capital than they are currently holding. For example, under the current definition of the leverage ratio, banks except those with more than $250 billion in assets had an average leverage ratio above 10% at the end of 2016.19 For traditional banks, as defined in the FCA, the bill uses a slightly different definition of leverage ratio than found in regulatory filings, however, making a direct comparison to the bill's requirement difficult. For traditional banks that are already above a 10% ratio, the FCA would provide them with regulatory relief without requiring them to hold more capital.

Predicting which banks would elect to hold the 10% leverage ratio involves a degree of uncertainty, but CBO did make such an estimate when scoring the bill. In general, the CBO estimates that larger banks would be less likely to elect to be subject to the 10% leverage ratio than smaller banks and expects none of the eight U.S. globally systemically important banks would make the election. One source of uncertainty the CBO had to address is that some banks that hold enough capital to meet the requirement would not necessarily make the election. CBO estimated that half the banks whose leverage ratio (as defined by the bill) currently exceeds 10%—most of which are banks with less than $50 billion in assets—would make the election. As a result, the CBO estimated that the banks that would make the election would account for roughly 9% of total bank industry assets.20

Volcker Rule21

Background

Section 619 of the Dodd-Frank Act, also known as the Volcker Rule, has two main parts—it prohibits banks from proprietary trading of "risky" assets and from "certain relationships" with risky investment funds, including acquiring or retaining "any equity, partnership, or other ownership interest in or sponsor[ing] a hedge fund or a private equity fund."22 The statute carves out exemptions from the rule for trading activities that Congress viewed as legitimate for banks to participate in, such as risk-mitigating hedging and market making related to broker-dealer activities. It also exempts certain securities, including those issued by the federal government, government agencies, states, and municipalities, from the ban on proprietary trading.23

Policy Issues

The Volcker Rule is named after Paul Volcker, former chair of the Federal Reserve (Fed) and former chair of President Obama's Economic Recovery Advisory Board. Volcker proposed this rule on the grounds that

adding further layers of risk to the inherent risks of essential commercial bank functions doesn't make sense, not when those risks arise from more speculative activities far better suited for other areas of the financial markets…. Apart from the risks inherent in these activities, they also present virtually insolvable conflicts of interest with customer relationships, conflicts that simply cannot be escaped by an elaboration of so-called Chinese walls between different divisions of an institution. The further point is that the three activities at issue—which in themselves are legitimate and useful parts of our capital markets—are in no way dependent on commercial banks' ownership.24

Volcker also pointed out that in the presence of deposit insurance, banks are implicitly backed by taxpayers, which presents moral hazard problems. Thus, support for the Volcker Rule has often been posed as preventing banks from "gambling" in securities markets with taxpayer-backed deposits.25 In Volcker's view, moving these activities out of the banking system reduces moral hazard and systemic risk concerns.

Although proprietary trading and hedge fund sponsorship pose risks, it is not clear whether they pose greater risks to bank solvency and financial stability than traditional banking activities, such as mortgage lending. They could be viewed as posing additional risks that might make banks more likely to fail, but alternatively those risks might better diversify a bank's risks, making it less likely to fail. Further, the Volcker Rule bans these activities from any subsidiary within a bank holding company, including nonbank subsidiaries. Proprietary trading in nonbank subsidiaries would be less likely to pose concerns about moral hazard and taxpayer risk unless the firm poses too big to fail problems.

A House Financial Services Committee majority report argues that the Volcker Rule is "a solution in search of a problem—it seeks to address activities that had nothing to do with the financial crisis, and its practical effect has been to undermine financial stability rather than preserve it."26

The Volcker Rule poses a practical challenge in differentiating between proprietary trading and permissible activities, such as hedging and market making. For example, how can regulators determine whether a broker-dealer is holding a security as inventory for market making, as a hedge against another risk, or as a speculative investment? Differentiating between these motives creates regulatory complexity, and if the benefits are not sufficient, the Volcker Rule might be unduly burdensome. The House Financial Services Committee report argues that banks will alter their behavior to avoid this regulatory burden, and this will reduce financial market efficiency:

The Volcker Rule will increase borrowing costs for businesses, lower investment returns for households, and reduce economic activity overall because it constrains market-making activity that has already reduced liquidity in key fixed-income markets, including the corporate bond market.27

Provision in the FCA

The FCA would repeal the Volcker Rule in its entirety.

Relief for Small Capital Issuers

Background

Some small and emerging companies may be interested in accessing funds for investment through issuing (or expanding their issuance of) securities that represent ownership in the firms. Such companies, however, may be disproportionally burdened by the costs of complying with the Securities and Exchange Commission's (SEC's) regime of securities registration and periodic disclosure aimed at protecting investors through the provision of material information.

Many existing securities requirements already have exemptions and tailoring for small capital issuers. For example, the Jumpstart Our Businesses Startup Act of 2012 (JOBS Act; P.L. 112-106) expanded on the regulatory relief that had historically been given to companies who issue unregistered securities called private placements when certain conditions (such as limitations on the issuance size or the types of eligible investors) are met.

Policy Issues

In a securities context, granting regulatory relief to boost capital formation may diminish the content and the efficacy of investor-based SEC disclosures, a potential trade-off between two of the SEC's statutory goals—investor protection and capital formation. This trade-off might also be informed by the fact that small and emerging firms are often described as risky investments.28

Conversely, some observers note that expanding the range of securities an investor can purchase will potentially allow them to increase risk diversification.29 Another potentially complicating dimension to the dynamic is the notion that some mandatory SEC corporate disclosures may not necessarily facilitate informed investing because they may be superfluous or may contribute to investor information overload. For example, in a 2013 speech, then-SEC Chair Mary Jo White observed that the agency would be examining whether investors' needs are served by the "detailed and lengthy disclosures about all of the topics that companies currently provide in the reports they are required to prepare and file with us … [and] whether information overload is occurring."30 In contrast, there is some evidence that giving small issuers exemptions from certain disclosure requirements reduces the price that investors are willing to pay when a firm issues equity—an example of how the goals of investor protection and capital formation sometimes reinforce each other.31

Provisions in the FCA

The FCA contains numerous provisions that would provide regulatory relief related to capital issuance by small firms, whether through public secondary markets or private placements (privately issued corporate securities). Examples of these provisions include the following:

Auditor Attestation. Internal controls are the policies and procedures that a company employs to maintain the accuracy of its financial reporting. Section 404(b) of the Sarbanes-Oxley Act of 2002 (SOX; P.L. 107-204) requires that a public company's outside auditor attest to its senior managers' assertions about the company's internal controls for its financial reporting (ICFR). In response to concerns over the burdens for small firms of complying with the auditor attestation provision, the Dodd-Frank Act included an exemption from Section 404(b) for public companies with a public float of less than $75 million. In 2011, the SEC reported that such companies represented about 60% of all public companies.32 The FCA would increase the exemption from Section 404(b) to nondepository corporate issuers with a public float from $75 million to $500 million.

Equity Crowdfunding. Traditionally, crowdfunding constituted the online donation of small amounts of capital from a large number of individuals to help finance a startup firm. It was initially illegal for donors to obtain an ownership stake through a debt or equity interest in the firms, however. The JOBS Act enabled firms to offer and sell securities conferring ownership through crowdfunding, known as equity crowdfunding, without SEC registration. To take advantage of the crowdfunding exemption, a crowdfunding issuer must conduct its offering solely through an online platform operated by an intermediary that is a SEC-registered broker-dealer or that is operated as a funding portal, subject to various requirements. Companies face limits on how much they can raise and investors face limits on how much they can invest.

The FCA would significantly loosen the regulation of the current equity crowdfunding regime. Among other things, it would subject crowdfunding issuers and investors to no limits in terms of the amount of securities that they could issue and invest in. Issuers would be allowed to offer securities directly to investors, provided that they complied with certain requirements. Equity crowdfunding firms would also be able to bypass broker-dealer or funding portal intermediaries and issue securities directly to the public.

General Solicitation and Demo Days. SEC Regulation D (Reg D) exempts certain securities offerings from SEC registration requirements, while also prohibiting issuers of Reg D securities from publicly marketing them via general solicitation.33 However, various members of the business community have criticized what they describe as the SEC policy's lack of clarity on whether general solicitation is permissible during promotional events, commonly known as "demo days." The FCA attempts to address such concerns by directing the SEC to revise Reg D to lift the prohibition on the use of general solicitation by issuers offering securities under Reg D in the context of a demo day as long as the demo day promotions do not specifically reference a given securities offering.

XBRL Exemptions for Emerging Growth Companies and Smaller Companies. Extensible Business Reporting Language (XBRL) is a freely available global standard developed to improve the way financial data are disseminated, compiled, and shared electronically. Historically, publicly traded companies were required to submit paper-based filings of mandatory financial statement disclosures to the SEC. Beginning in 2011, all publicly traded firms were required to submit disclosures to the agency in XBRL. A provision in the FCA would exempt emerging growth companies (EGCs) and other small public companies with annual revenues of less than $250 million from the requirement to use XBRL for SEC disclosures.34

Raising Venture Capital Funds' Investment Company Act Registration Threshold. One exception from SEC registration requirements is for a pooled investment entity whose outstanding stock is owned by 100 beneficial owners or fewer and is neither currently making nor intends to make a public securities offering.35

Organized and run by their general partners, venture capital funds are investment pools that manage the funds of their wealthy investors interested in acquiring private equity stakes in emerging small- and medium-sized firms and startup firms with perceived growth potential. Currently, within the business community, there are some concerns over the perceived behavioral impact of the 100-owner limit. Some say that to avoid registration and its potentially significant compliance costs, some venture capital funds are reluctant to add additional investors—potentially foregoing the opportunity to expand the capital to invest in various businesses.

A provision in the FCA attempts to address such concerns by creating a new subset of venture capital fund called a qualifying venture capital fund (QVCF). QVCFs are defined as venture capital funds with no more than $50 million in invested capital. They could be owned by up to 500 beneficial owners before triggering registration requirements.

Fiduciary Rule36

Background

Under federal securities laws, SEC-registered investment advisers are fiduciaries, a designation that carries a legal obligation to act in a client's best interest. By contrast, brokers and dealers who receive commissions are generally not subject to the fiduciary standard, and are instead required to make investment recommendations that are suitable for the customer—a comparatively less demanding standard of client duty. The Dodd-Frank Act authorized, but did not require, the SEC to promulgate rules to establish a uniform standard of client responsibility for broker-dealers and investment advisers, which it has not done to date. In 2016, the Department of Labor (DOL) finalized rules to amend the definition of investment advice to broaden the class of financial professionals (including broker-dealers and insurance agents) subject to the fiduciary obligation under the Employee Retirement Income Security Act of 1974,37 which governs investment advisers for private-sector retirement accounts.38

On February 23, 2017, President Donald Trump issued an executive memorandum directing the DOL to analyze the fiduciary rule's impact. If the study found that the rule would negatively affect investors in specified ways, the agency was then authorized to either rescind or revise the rule.39 Subsequent to the presidential memorandum, the DOL delayed the effective date of the fiduciary rule to June 9, 2017.40

Policy Issues

In announcing the fiduciary rule, DOL observed that investment advisers and consultants have increasingly assumed greater roles in managing retirement accounts.41 The services provided by broker-dealers and investment advisers often overlap—both can provide investment advice—and there are some concerns that customers may falsely assume that the person advising them is required to be acting in their best interests.

Among other things, DOL said that the rule would help address instances in which plan advisers (1) steer Individual Retirement Account (IRA) owners into investments based on their—not the investors'—own financial interests; (2) have conflicts of interests with respect to the investment advice that they give; and (3) give imprudent investment advice.42 Critics of the rule, including some Members of Congress, have argued that it would have a negative impact on retirees43 and would result in higher costs for people who seek financial advice.44

Provisions in the FCA

The FCA would repeal the DOL's fiduciary rule. Additionally, before it promulgated any fiduciary standard rule, the SEC would have to report to Congress on whether

- 1. retail customers are being harmed because there is not a uniform standard;

- 2. alternative reforms would alleviate retail investor harm and confusion;

- 3. adoption of a uniform fiduciary standard would adversely impact the broker-dealers; and

- 4. the adoption of a uniform fiduciary standard would adversely affect retail investor access to personalized and cost-effective investment advice.

In addition, the DOL could not reissue a fiduciary rule until after the SEC publishes one.

Risk Retention

Background

Securitization is the process of turning mortgages, credit card loans, and other debt into securities that can be purchased by investors. Securitizers make or acquire a pool of many loans, then issue securities—called asset-backed securities (ABS)—which entitle the holder of the security to receive payments based on the flow of payments being made on the underlying loans. Banks can reduce their exposed risk on their retained portfolios by securitizing the loans they hold, spreading risks to other types of investors more willing to bear them. If risks are adequately managed and understood, this can enhance financial stability. In addition, securitization allows nonbank lenders with limited sources of long-term funding to make loans, and thus can increase the total amount of credit available to businesses and consumers.

In the years leading up to the financial crisis, securitization grew rapidly, driving loan origination and becoming an increasingly important source of funding for lenders. During the crisis, the value of ABS that were backed by residential mortgages—called residential mortgage backed securities (RMBS)—decreased significantly, precipitating systemic distress. The decline, and the general contraction in credit following the crisis, resulted in a sharp decline in new ABS issuance. Although ABS issuance has grown in the years since the crisis, it remains below precrisis levels.

The Dodd-Frank Act generally required securitizers to retain some of the risk if they issue ABS. The amount of risk required to be retained depends in part on the quality and type of the underlying assets. The act instructed regulators to require not less than 5% retention of risk unless the securitized assets meet underwriting standards prescribed by the regulators. Securitizers were prohibited from hedging the retained credit risk.

The act required securitizers to perform due diligence on the underlying assets of the securitization and to disclose the nature of the due diligence. In addition, ABS investors are to receive more information about the underlying assets.

Policy Issues

Securitization can create an incentive to originate loans without appropriate underwriting because lenders collect origination fees but are not exposed to losses from borrower defaults. These incentives likely contributed to deteriorating underwriting standards prior to the crisis, the housing bubble, and the turmoil experienced during the financial crisis. Private-label securitization was prevalent in the subprime mortgage market, the nonconforming mortgage market, and in regions where loan defaults were particularly severe. Losses and illiquidity in the RMBS market led to wider problems in the crisis, including a lack of confidence in financial firms because of uncertainty about their exposure to potential RMBS losses, through their holdings of RMBS or off-balance-sheet support to securitizers.

One approach to address incentive problems in securitization is to require loan securitizers to retain a portion of the long-term default risk. An advantage of this "skin in the game" requirement is that it may help preserve underwriting standards among lenders funded by securitization, because securitizers would share in their investors' securities risks.

One possible cost of risk retention is that it may make less credit available in markets in which loans are securitized. If securitizers must hold onto, rather than sell, a portion of their securities or underlying assets, a portion of their funding remains tied up in those assets, making less funding available for new loans.45 Reducing the availability of credit could also increase the cost to borrowers. Another possible disadvantage is that less risk may be shifted away from lenders and other securitizers and out to a broader sector of investors willing and able to bear it. Concentrating risk in certain financial sectors could increase financial instability. Finally, opponents of risk retention assert that certain loan types—including commercial real estate loans and certain corporate loans—feature characteristics and securitization practices that differ from residential mortgages and RMBS in ways that reduce the incentive problem. They note that nonresidential mortgage ABS performed relatively well during the crisis and were not a source of systemic risk, making the risk retention rule inappropriate for these markets.46

Provisions in the FCA

The FCA would amend the provision of Dodd-Frank Act mandating risk retention rules by applying those requirements only to securities that are wholly composed of residential mortgages. Under this definition, securities backed by assets that are not residential mortgages—such as commercial real estate mortgages, commercial loans, auto loans, or other types of debt—would not be subject to the risk retention rule.

Executive Compensation47

Background

In general, federal policy does not limit or regulate executive compensation levels. Instead, publicly listed companies are required to disclose certain information about their executive compensation levels and practices.

Two examples of the general approach to current disclosure requirements come from the Dodd-Frank Act. The "say-on-pay" provision requires public companies to conduct a nonbinding shareholder vote on executive compensation at least every three years. The "pay ratio" provision requires publicly traded companies to calculate and disclose the median annual total compensation of all employees excluding the chief executive officer (CEO), the annual total compensation of the CEO, and the ratio between the two.

One exception to this general approach on executive compensation is a Dodd-Frank Act requirement that federal financial regulators promulgate rules aimed at prohibiting incentive-based compensation (performance-based variable employee pay) that encourages "inappropriate risks" at financial institutions with greater than $1 billion in assets. In 2016, the regulators jointly released proposed rules to implement the requirement.48

Policy Issues

Proponents of greater disclosure believe that requiring transparency about executive compensation will help prevent outsized pay arrangements that are not in the interest of investors or in line with social values. Critics argue current disclosure requirements impose unnecessary costs that do not impart useful information that helps maximize shareholder return. For example, critics of the pay ratio have cited the compliance challenges and costs of building systems capable of generating the worker pay data needed to arrive at worker median pay data, particularly for large multinational or multisegmented firms with decentralized payroll systems.49

A key question in this debate is whether high executive compensation levels reflect executives' productivity or result from corporate governance shortcomings. Those who contend it is due to corporate governance shortcomings can point to research that found that executive pay has become decoupled from corporate financial performance.50 Critics of this view counter that, overall, the body of research on the issue has failed to convincingly make the case for such a decoupling.51

On the proposed rule prohibiting incentive-based compensation at financial firms, proponents have described the proposals as critically important to mitigating systemic risk.52 Critics, however, dispute that it would mitigate systemic risk, and argue it would result in an exodus of talent from various financial institutions.53

Provisions in the FCA

The FCA would amend the Dodd-Frank Act's say-on-pay provision by eliminating mandatory periodic shareholder votes on executive pay and limiting such votes to when a company has made a material change to the previous year's executive compensation. The FCA would repeal the Dodd-Frank Act requirement that companies calculate and disclose the CEO-worker pay ratio.54 The FCA would also repeal the Dodd-Frank Act's incentive compensation mandate.

Systemically Important ("Too Big To Fail") Financial Institutions

Although "too big to fail" (TBTF) has been a long-standing policy issue, it was highlighted by the near-collapse of several large financial firms in 2008, including Bear Stearns, Fannie Mae, Freddie Mac, Lehman Brothers, and AIG, which led to a worsening of the financial crisis. With the exception of Lehman Brothers (which filed for bankruptcy), all of these firms received government assistance under emergency authority to avoid insolvency. Financial firms are said to be TBTF when policymakers judge that the firms' failure would cause unacceptable disruptions to financial stability. Financial firms can be perceived as TBTF because of their size or interconnectedness. In addition to fairness issues, economic theory suggests that market expectations that the government will not allow a firm to fail create moral hazard—if the creditors and counterparties of a TBTF firm believe that the government will protect them from losses, they have less incentive to monitor the firm's riskiness (referred to as market discipline). If this is the case, a firm that is perceived to be TBTF could have a funding advantage, which some call an implicit subsidy, compared with other firms.

Regulating Systemically Important Financial Institutions and Limiting Their Size55

Background

The Dodd-Frank Act included a number of provisions to address TBTF, using several different policy approaches.56 The act's main approach was to create an enhanced regulatory regime mostly administered by the Federal Reserve to hold systemically important firms to stricter prudential standards than other financial firms. Prudential regulation is a concept from banking regulation that refers to monitoring an institution's financial safety and soundness; the concept was generally not applied federally to nonbank financial firms before the crisis, with limited exceptions. The enhanced regulatory regime can include capital standards, liquidity standards, counterparty limits, stress tests, risk-management standards, "living will" requirements, and early remediation requirements.

The Dodd-Frank Act applied enhanced prudential regulation to three sets of financial entities—banks; nonbank financial firms; and payment, clearing, and settlement systems (called financial market utilities, or FMUs).57 Bank holding companies (BHCs) are automatically subject to enhanced regulation if they have $50 billion or more in assets. More than 30 BHCs—which include most of the largest U.S. financial firms—meet this criterion. A BHC cannot "debank" to avoid enhanced regulation if it received funds under the Troubled Asset Relief Program (referred to as the "Hotel California" provision). A smaller subset of the largest U.S. BHCs also faces additional capital, leverage, and liquidity requirements through U.S. regulations implementing Basel III, an international accord. Nonbank financial firms and FMUs are subject to enhanced regulation only if they are designated as systemically important financial institutions (SIFIs) by the Financial Stability Oversight Council (FSOC). To date, eight FMUs and four nonbank financial firms, three of which are insurance companies, have been designated. Subsequently, one firm (GE Capital) has had its designation removed by FSOC and one designation (MetLife) has been overturned in court, subject to pending appeals.58

The Dodd-Frank Act included other approaches to coping with the TBTF problem, including provisions to limit the size of financial firms and narrow the scope of emergency authority to limit future bailouts. It gave the Federal Reserve the authority to restrict the size and activities of a financial firm that posed a grave threat to financial stability and prevented a nonbank financial firm from most mergers and acquisitions that would cause its liabilities to exceed 10% of total financial-sector liabilities. These powers could be used only in limited circumstances, however, and have not been exercised to date.

|

SIFIs |

FMUs |

|

Current |

Current |

|

AIG |

The Clearing House Payments Co. |

|

Prudential Financial |

CLS Bank International |

|

Former |

Chicago Mercantile Exchange |

|

GE Capitala |

The Depository Trust Company |

|

MetLifeb |

Fixed Income Clearing Corporation |

|

ICE Clear Credit |

|

|

National Securities Clearing Corp. |

|

|

The Options Clearing Corp. |

Source: FSOC at https://www.treasury.gov/initiatives/fsoc/designations/Pages/default.aspx.

Notes: See text for details.

a. On June 28, 2016, FSOC rescinded GE Capital's designation.

b. On March 30, 2016, the U.S. District Court for the District of Columbia struck down MetLife's designation.

Policy Issues

The fact that many large firms have grown in dollar terms since the enactment of the Dodd-Frank Act has led some critics to question whether the TBTF problem has been solved. Debate continues about whether the best policy approach to address excessive risk-taking from moral hazard is through enhanced prudential regulation or market discipline—the fear of losses curbing excessive risk-taking. Although these two approaches need not be at odds with one another in theory—and policymakers have tried to pursue both simultaneously—in practice they may be. Critics of enhanced prudential regulation fear that if the government explicitly designates specific firms as systemically important, investors will assume that the firms will not be allowed to fail, which will undermine market discipline. If enhanced regulation is not tough enough—critics point to regulatory failures during the crisis as evidence that it may not be—and market discipline is undermined, designated firms might take greater risks and the financial system could be less stable.

Proponents of enhanced regulation question how credible a pledge to let firms fail can be. They point to the excessive risk-taking leading up to 2008—when the government did not have a policy of aiding failing firms—and the subsequent decision to assist large firms to avoid a further deterioration in financial conditions as an example of the failure of market discipline. In addition, the fact that many large failing firms did receive government assistance in 2008 may have already undermined the viability of the market discipline approach going forward, by undermining the credibility of any subsequent pledge to allow firms to fail (regardless of current statutory limitations). Furthermore, systemic risk is a risk to the rest of society that investors do not internalize. From a policymaker's perspective, systemic risk may still be too high in the presence of perfect market discipline, because a TBTF firm's creditors have less to lose from its failure than the financial system as a whole. Another limit to market discipline is that creditors do not have access to the same confidential information as regulators.

Extending prudential regulation to nonbank SIFIs raises additional policy questions:

- Enhanced regulation. Can the Federal Reserve effectively adapt banking prudential regulation and supervision to nonbanks, tailoring regulation to match their business models and the risks that they pose?

- Designation process. Given the lack of consensus on how to measure systemic importance, is FSOC's discretion appropriate or is the existing designation process too opaque and arbitrary?

- Insurance and systemic risk. Given that all currently designated SIFIs are insurers, are large insurance firms a source of systemic risk and, if so, is it already adequately addressed by prudential regulation at the state level?

- Size vs. activities. Is the source of systemic risk for nonbanks caused mainly by firm size or by specific market practices by firms of all size? If the latter, then SIFI regulation is unlikely to contain systemic risk.

Provisions in the FCA

The FCA would repeal several provisions of the Dodd-Frank Act related to TBTF. Notably, it would repeal FSOC's ability to designate nonbank financial firms or FMUs as SIFIs and subject them to enhanced regulation, as detailed above. Firms and FMUs currently designated as SIFIs (see Table 2) would no longer be subject to enhanced regulation. The FCA also would repeal early remediation requirements for SIFIs and bank holding companies with more than $50 billion in assets. It would also reduce the frequency of and modify the frameworks for stress testing and living wills for large banks.

The FCA would leave in place enhanced regulation from the Dodd-Frank Act and Basel III for large BHCs. However, banks that qualify for regulatory exemptions under the 10% leverage ratio would no longer be subject to these enhanced regulations. The FCA would also repeal the Hotel California provision prohibiting a BHC from debanking to avoid enhanced regulation.

In addition, the FCA would repeal Dodd-Frank Act provisions that gave the Federal Reserve the ability to restrict the size and activities of a financial firm that posed "a grave threat to financial stability" and the limit on a nonbank financial firm exceeding 10% of total financial sector liabilities (the provision would still apply to banks).

Whether these changes would increase or decrease the riskiness of large financial firms and the financial system as a whole depends on whether the effect of potentially greater market discipline or reduced prudential regulation dominates. The effect on market discipline, in turn, will depend in part on what market participants believe will happen in the event of a failure, which is addressed in the next section.

Resolving a Failing TBTF Firm and Preventing "Bailouts"59

Background

The financial crisis raised issues about how to allow large financial firms to fail without triggering financial instability. In an attempt to quell the crisis, the Fed (under Section 13(3) of the Federal Reserve Act), FDIC, and Treasury (using the Exchange Stabilization Fund) used emergency authority to offer loans and guarantees to financial firms and markets. Broadly speaking, the Dodd-Frank Act (for the Fed and FDIC) and the Emergency Economic Stabilization Act (P.L. 110-343) (for Treasury) narrowed the scope of these authorities in an attempt to rule out "bailouts" to insolvent, failing firms, while preserving their authority to provide emergency liquidity to healthy but illiquid firms. The Dodd-Frank Act also extended access to the Fed's discount window to FMUs.

Policymakers at the time of the crisis argued that government intervention was unavoidable in the absence of a means to wind down systemically important firms without triggering financial instability.60 Some argued that these concerns were confirmed by the financial instability associated with the government's decision to allow the broker-dealer Lehman Brothers to enter the bankruptcy process rather than extending it assistance to remain solvent and.61 Critics, by contrast, argue that repeated ad hoc interventions by policymakers created uncertainty that contributed to financial instability.62

In response to these concerns, Title II of the Dodd-Frank Act created a special resolution regime (called Orderly Liquidation Authority or OLA) for liquidating failing financial firms only if federal policymakers determine that a firm's imminent failure poses a threat to financial stability. OLA is an administrative, rather than judicial, resolution forum modeled on how the FDIC resolves insured depository institutions. Should the failing firm's estate lack sufficient liquid assets to prevent creditor reactions from contributing to financial instability, the FDIC is empowered to contribute resources to the failing firm's estate. Any such payments would be recouped through the liquidation of the failed firm's assets or after-the-fact assessments on surviving firms in the financial industry. (Note that access to OLA is not limited to designated SIFIs and has not been used to date.)

OLA is statutorily structured as a fallback alternative to the normally applicable insolvency regimes;63 the failure of most nonbank financial institutions generally is dealt with under the Bankruptcy Code.64 The Bankruptcy Code consists of separate chapters designed to resolve a variety of failing entities through judicial processes.65 However, certain entities are not statutorily permitted to be resolved through the Bankruptcy Code. For example, FDIC insured depositories are not permitted to be debtors under the Bankrutpcy Code.66 Instead, the FDIC is statutorily authorized to resolve failing insured depositories through a largely nonjudicial, FDIC-administered conservatorship or receivership. Part of the policy justification for resolving insured depositories through this administrative regime, rather than the normally applicable Bankruptcy Code, is that the FDIC, as deposit insurer, guarantees payment to depositors even if such obligations exceed the resources of the failing firm's estate, but also due to the threat of financial instability accompanied by widespread failures of depositories.67

Policy Issues

Advocates of OLA highlight several specific characteristics of financial markets and the Bankruptcy Code at the time that may have magnified financial instability.68 First, some argue that the Lehman Brothers bankruptcy announcement was a negative shock to confidence because investors had assumed that Lehman was "too big to fail." By contrast, OLA has a statutory focus on maintaining financial stability, of which there is no statutory equivalent under the existing Bankruptcy Code. Second, some argue that the length of a typical judicial bankruptcy proceeding compared to an administrative agency resolution process would contribute to financial uncertainty. Proponents argue that OLA's administrative forum would allow the FDIC to move more quickly than generally is possible through a judicial bankruptcy proceeding, thus decreasing market uncertainty. Third, some argue that the treatment of some financial contracts, such as acceleration and netting of qualifying financial contracts (QFCs), under the Bankruptcy Code is done selectively by counterparties to the detriment of the bankruptcy estate.69

Critics say these three advantages of OLA could be replicated in a judicial forum by establishing a new chapter of the Bankruptcy Code designed specifically to address the unique characteristics of large financial institutions.

Fourth, supporters of OLA argue that the nature of financial intermediaries' continuous need to access credit (liquidity) makes a bankruptcy process impractical for large financial institutions.70 They view it as unlikely that markets will be able to provide sufficient private financing during the bankruptcy of a failing firm and, therefore, "it is not credible to suggest that a financial institution bankruptcy can work without standby government financing," like that which is provided by Title II.71

The FDIC's option to temporarily use government funds to meet creditor claims under OLA leads critics to argue that it "institutionalized bailouts" and that the FDIC's plan for implementing OLA has promoted "expectations that the government will come to the rescue of large financial institutions and insulate their creditors and counterparties from losses."72 OLA cannot be used to bail out failing firms in the sense that it can only be used to wind a firm down, but it could potentially be used to bail out a firm's creditors by making them whole or at least compensating them more than would be available through a bankruptcy proceeding. Although Title II instructs the FDIC to generally treat similarly situated creditors similarly, critics worry that the fact that, if necessary for financial stability, the FDIC has "authority to treat similarly situated creditors differently places far too much discretion in the hands of the government to pick winners and losers" during a resolution.73 The FDIC, in addressing these concerns, has noted that it "expects that disparate treatment of creditors would occur only in very limited circumstances and has, by regulation, expressly limited its discretion to treat similarly situated creditors differently."74

Provisions in FCA

The FCA would repeal Title II of the Dodd-Frank Act and would add a new subchapter to the Bankruptcy Code designed specifically to handle the arguably unique characteristics associated with the failure of certain financial firms. As such, the resolution process would be handled through the courts rather than through largely nonjudicial proceedings administered by the financial regulators. However, the relevant financial regulators would, under certain circumstances, have the right to "appear and be heard" in certain bankruptcy proceedings of covered financial institutions.

Similar to the current Bankruptcy Code, under the FCA there would be several resolution options available to covered financial institutions. The firm could be liquidated (Chapter 7) or reorganized (Chapter 11). However, the plan must meet a number of conditions, including that it is in the best interests of the creditors and must not pose a likely threat to the financial stability of the United States.

The FCA would add additional limits to the Fed's emergency lending authority and would eliminate FMU access to the discount window, the FDIC's emergency authority to guarantee bank debt and systemic risk exception to least cost resolution, and the use of the Exchange Stabilization Fund for government guarantees.

CBO projects that the elimination of the Orderly Liquidation Authority would reduce the budget deficit by $14.5 billion over 10 years based on the probability of a firm being resolved through OLA over the next 10 years multiplied by the net cost to the government of doing so. Eliminating OLA reduces the deficit mainly because of scoring conventions. Although the FDIC is required to assess fees on large financial firms after the fact sufficient to completely offset the costs of an OLA resolution, CBO assumes that some of these fees (and asset sales from the resolution) would be collected outside of the 10-year scoring window.75

Changes to Regulatory Authority

Conventional wisdom regarding regulators is that the structure and design of the organization matters for policy outcomes. These agencies have been given certain characteristics that enhance their day-to-day independence from the President or Congress, which may make policymaking more technical and less political or partisan, for better or worse.76 Independence also may make regulators less accountable to elected officials and can reduce congressional influence. From a practical perspective, independence and accountability take various forms and each regulator has a unique group of characteristics that, along with tradition, determine its relative independence and accountability. Two of the most independent regulators, the Fed and the CFPB, would see their independence reduced and congressional oversight increased by the FCA. The rest of this section discusses issues raised by the FCA related to independence and accountability, with added focus on the CFPB and the Fed.

Appropriations77

Background

The annual appropriations processes and periodic reauthorization legislation provide Congress with opportunities to influence the size, scope, priorities, and activities of an agency. Most financial regulators determine their own budgets and assess fees to cover expenditures, as shown in Table 3, typically subject to some general language regarding proportionality of budget and mission. Currently, the two financial regulators whose funding is primarily determined through the appropriations process and who are subject to periodic reauthorizations are the CFTC and the SEC.78 Most financial regulators generate income from various sources, particularly fees or assessments on entities that they oversee. The two financial regulators that do not largely raise their own revenues are the CFTC and the CFPB. The CFTC's funding comes from general revenues and CFPB funding is transferred from the Federal Reserve's revenues.

|

Regulator |

Subject to Annual Appropriations? |

Subject to Periodic Reauthorization? |

Primary Revenue Source |

|

Commodity Futures Trading Commission |

Yes |

Yes, latest authorization expired Sept. 30, 2013. |

Treasury general fund per congressional appropriation. |

|

Consumer Financial Protection Bureau |

No |

No |

Transfer from Federal Reserve System limited to 12% of the Fed's operating expenses. |

|

Federal Deposit Insurance Corporation |

No |

No |

Deposit insurance premiums determined by FDIC to meet a reserve ratio set by FDIC (with a statutory minimum of 1.35% of insured deposits). |

|

Federal Housing Finance Agency |

No |

No |

Fees and assessments on regulated institutions. Amounts determined by FHFA. |

|

Federal Reserve |

No |

No |

Income on securities and loans held by the Fed. The Fed also charges fees to cover the costs of business services it offers. |

|

National Credit Union Administration |

No |

No |

Deposit insurance premiums determined by NCUA to meet a reserve ratio set by NCUA (with a statutory minimum of 1.2% of insured deposits). |

|

Office of the Comptroller of the Currency |

No |

No |

Fees on regulated institutions. Amounts determined by OCC. |

|

Securities and Exchange Commission |

Yes, except for $100 million reserve fund. |

Yes, latest authorization expired September 30, 2015. |

Fees and assessments on regulated entities. Amounts set to meet congressional appropriation. |

Source: CRS analysis of federal statute.

Note: Both the SEC and CFTC have continued to operate since their authorizations expired.

Policy Issues

The appropriations and authorization processes provide Congress regular opportunities to evaluate an agency's performance. During these processes, Congress might also influence the activities of these agencies by legislating provisions that reallocate resources or place limitations on the use of appropriated funds to better reflect congressional priorities. Through line-item funding, bill text, or accompanying committee report text, Congress can encourage, discourage, require, or forbid specific activities at the agency, including rulemaking. Alternatively, Congress can adjust an agency's overall funding level if Congress is supportive or unsupportive of the agency's mission or conduct. Thus, congressional control over an agency's funding reduces its independence from (and increases its accountability to) Congress. To the extent that agency budget requests exceed appropriations in practice, bringing agencies into the appropriations process could result in lower agency funding levels, for better or worse.

Provisions in the FCA

The FCA would bring the rest of the financial regulators—the FDIC, FHFA, NCUA, OCC, Fed, and CLEA—as well as FSOC into the appropriations process. For the Fed, spending related to monetary policy would remain outside of the appropriation process.79 For the FDIC, the Deposit Insurance Fund would remain outside of the appropriations process. The CLEA, replacing the CFPB, would not receive transfers from the Federal Reserve and thus would not have a dedicated source of revenues. Fees and assessments that agencies currently collect to fund themselves would appear as offsetting collections in the federal budget with certain exceptions. Agencies that are currently permanently authorized would remain so. The FCA would also reauthorize the SEC through 2022 and the CLEA through 2018.

CBO estimates that moving these agencies to appropriations would reduce direct spending (and therefore decrease the deficit) by $18.4 billion over 10 years. To the extent that these agencies were funded through future appropriations acts, discretionary spending would rise and offset that reduction in the deficit.80

Consumer Financial Protection Bureau

Background81

Before Title X of the Dodd-Frank Act (entitled the Consumer Financial Protection Act) went into effect,82 federal consumer financial protection regulatory authority was split between five banking agencies—the OCC, Fed, FDIC, NCUA, and Office of Thrift Supervision (OTS)83—as well as the Federal Trade Commission (FTC) and the Department of Housing and Urban Development (HUD). These seven agencies shared (1) the authority to write rules to implement most federal consumer financial protection laws; (2) the power to enforce those laws; and (3) supervisory authority over the individuals and companies offering and selling consumer financial products and services. The jurisdictions of these agencies varied based on the type of institution involved and, in some cases, based on the type of financial activities in which institutions engaged.84

The regulatory authority of the banking agencies varied by depository charter. The OCC regulated depository institutions with a national bank charter.85 The Fed regulated the domestic operations of foreign banks and state-chartered banks that were members of the Federal Reserve System (FRS).86 The FDIC regulated state-chartered banks and other state-chartered depository institutions that were not members of the FRS.87 The NCUA regulated federally insured credit unions,88 and the OTS regulated institutions with a federal thrift charter.89

The banking agencies were charged with a two-pronged mandate to regulate depository institutions within their jurisdiction for safety and soundness, as well as consumer compliance.90 The focus of safety and soundness regulation is ensuring that institutions are managed in a safe and sound manner so as to maintain profitability and avoid failure.91 The focus of consumer compliance regulation is ensuring that institutions abide by applicable consumer protection and fair lending laws.92 To reach these ends, the banking agencies held broad authority to subject depository institutions to up-front supervisory standards, including the authority to conduct regular, if not continuous, on-site examinations of depository institutions.93 They also had flexible enforcement powers to redress consumer harm, as well as to rectify proactively compliance issues found in the course of examinations and the exercise of their other supervisory powers, potentially before consumers suffered harm.94

The FTC was the primary federal regulator for nondepository financial companies, such as payday lenders and mortgage brokers.95 Unlike the federal banking agencies, the FTC had little up-front supervisory or enforcement authority.96 For instance, the FTC did not have the statutory authority to examine nondepository financial companies regularly or impose reporting requirements on them as a way proactively to ensure they were complying with consumer protection laws.97 Instead, the FTC's powers generally were limited to enforcing federal consumer laws.98 However, because the FTC lacked supervisory powers, it generally initiated enforcement actions in response to consumer complaints, private litigation, or similar "triggering events [that] postdate injury to the consumer."99

Additionally, both depository institutions and nondepository financial companies were subject to the federal consumer financial protection laws.100 Together, these federal laws establish consumer protections for a broad and diverse set of activities and services, including consumer credit transactions,101 third-party debt collection,102 and credit reporting.103 Before the Dodd-Frank Act went into effect, the rulemaking authority to implement federal consumer financial protection laws was largely held by the Fed.104 However, the authority to enforce the federal consumer financial protection laws and regulations was spread among all of the banking agencies, the FTC, and HUD.105

Some scholars and consumer advocates contended that this arguably complex, fragmented federal consumer financial protection regulatory regime failed to protect consumers adequately and created market inefficiencies to the detriment of both financial companies and consumers.106 Some argued that these problems could be corrected if federal consumer financial regulatory powers were strengthened and consolidated in a single regulator with a consumer-centric mission and supervisory, rulemaking, and enforcement powers akin to those held by the banking agencies.107

The Dodd-Frank Act established the Consumer Financial Protection Bureau (CFPB, or Bureau), in part to address these concerns.108 The CFPB is established as an independent agency109 within the Federal Reserve System.110 The Bureau is headed by a single director who is appointed by the President of the United States, subject to the advice and consent of the Senate, and may only be removed from office "for inefficiency, neglect of duty, or malfeasance in office."111 The Bureau is funded primarily through transfers of nonappropriated funds from the Federal Reserve System's combined earnings in an amount "determined by the Director to be reasonably necessary to carry out the authorities of the Bureau," subject to specified caps.112