The Impact of the Federal Income Tax Code on Poverty

Changes from October 17, 2019 to October 19, 2020

This page shows textual changes in the document between the two versions indicated in the dates above. Textual matter removed in the later version is indicated with red strikethrough and textual matter added in the later version is indicated with blue.

The Impact of the Federal Income Tax on Poverty: Before and After the 2017 Tax Revision ("TCJA"; P.L. 115-97)

Contents

- Introduction

- Key Concepts, Conventions, and Terms Used in this Report

- How Major Federal Income Tax Provisions Apply to the Poor

- Calculating Income Tax Liability

- Exclusion of Public Assistance

- The Standard Deduction and Personal Exemptions

- Marginal Tax Rates

- Refundable Tax Credits

- The Pre-TCJA Income Tax and Poverty

- Poor Families with Positive, Negative, and Zero Tax Liabilities Under the Pre-TCJA Income Tax

- The Impact of Pre-TCJA Income Tax on Poverty Rates

- The Impact of Pre-TCJA Income Tax on the Poverty Gap

- The Post-TCJA Income Tax and Poverty

- Poor Families with Positive, Negative, and Zero Tax Liabilities Under the Post-TCJA Income Tax

- The Impact of the Post-TCJA Income Tax on Poverty Rates

- The Impact of the Post-TCJA Income Tax on the Poverty Gap

- A Comparison of the Impact of the Post-TCJA Income Tax and Selected Low-Income Assistance Programs on Poverty Rates and the Poverty Gap

- Conclusion

Figures

- Figure 1. Estimated Share of Families with Positive, Zero, and Negative Income Tax Liabilities Under the Pre-TCJA Income Tax by Family After-Tax Poverty Status, 2016

- Figure 2. Estimated Share of Poor Families with Positive, Zero, and Negative Income Tax Liabilities Under the Pre-TCJA Income Tax by Family Type, 2016

- Figure 3. Estimated Before-Tax and After-Tax Poverty Rates Under the Pre-TCJA Income Tax, 2016

- Figure 4. Estimated Share of Families with Positive, Zero, and Negative Income Tax Liabilities Under the Pre- and Post-TCJA Income Tax by After-Tax Family Poverty Status, 2016

- Figure 5. Estimated Share of Poor Families with Positive, Zero, and Negative Income Tax Liabilities Under the Pre- and Post-TCJA Income Tax by Family Type, 2016

- Figure 6. Estimated After-Tax Poverty Rates Under the Pre- and Post-TCJA Income Tax, 2016

- Figure 7. Estimated Percentage-Point Reduction in the Poverty Rate from the Post-TCJA Income Tax and Selected Low-Income Assistance Programs, 2016

- Figure 8. Estimated Dollar Reduction in the Aggregate Poverty Gap from the Post-TCJA Income Tax and Selected Low-Income Assistance Programs, 2016

- Figure C-1. Child Tax Credit Amounts by Income Under the Pre- and Post-TCJA Income Tax for a Married Couple with Two Children, 2018

- Figure C-2. Child Tax Credit Amounts Under the Pre- and Post-TCJA Income Tax and the Difference in These Amounts for Married Couple with Two Children and Less Than $36,000 in Income, 2018

Tables

- Table 1. Estimated Before-Tax and After- Tax Poverty Rates Under the Pre-TCJA Income Tax for Selected Individuals Living in Families With and Without Workers, 2016

- Table 2. Estimated Aggregate Poverty Gap Before and After the Pre-TCJA Income Tax by Family Type, 2016

- Table 3. Estimated Before-Tax and After-Tax Poverty Rates Under the Post-TCJA Income Tax for Selected Individuals Living in Families With and Without Workers, 2016

- Table 4. Estimated Aggregate Poverty Gap Before and After the Pre- and Post-TCJA Income Tax by Family Type, 2016

- Table A-1. Selected Post-TCJA Income Tax Provisions in 2018 and 2016 Dollars

- Table B-1. Estimated Number of Individuals in Poverty Before the Income Tax for Selected Individuals Living in Families With and Without Workers, 2016

- Table B-2. Estimated Number of Families in Poverty Before the Income Tax by Family Type, 2016

- Table C-1. Combined Standard Deduction and Personal Exemption for Hypothetical Taxpayers Under the Pre- and Post- TCJA Income Tax, 2018

- Table C-2. Marginal Tax Rates Under the Pre- and Post-TCJA Income Tax, 2018

- Table C-3. Overview of Changes to the Child Tax Credit Under the TCJA

Summary

The Impact of the Federal Income Tax Code

October 19, 2020

on Poverty

Margot L. Crandall-Hollick

The federal individual income tax is structured so that the poor owe little or no income

Acting Section Research

tax. In addition, the federal individual income tax (hereinafter referred to simply as the income tax

Manager

income tax code or income tax) increases the disposable income of many poor families

via refundable tax credits—primarily the earned income tax credit (EITC) and the

Gene Falk

refundable portion of the child tax credit, referred to as the additional child tax credit, or ACTC

Specialist in Social Policy

(ACTC). These credits are explicitly designed to benefit low-income families with

workers and children and can significantly boost families'’ disposable income, lifting

Jameson A. Carter

many of these families above the poverty line.

Research Assistant

Using the federal government'’s Supplemental Poverty Measure (SPM), CRSthe Congressional Research Service (CRS) estimates that under current law, the income tax

reduced total poverty by 15% (from 14.5% 7% of individuals in poverty to 12.3% 5% of individuals in poverty). The impact of the income tax on the overall poverty rate was larger than the impact of many needs-tested benefits programs targeted toward the poor. In contrast, the income tax'’s ability to lift the poorest Americans out of poverty—to reduce the "“poverty gap"”—was limited in comparison to many needs-tested programs. (The poverty gap is the difference between the poverty threshold and a family'’s disposable income, aggregated over all poor families, and is a measure of the degree of poverty.) CRS estimates that under current law, the income tax reduced the poverty gap by about $13.910.3 billion annually (from $150.8154.0 billion to $136.9$143.6 billion), approximately half the effect of other needs-tested programs.

Virtually all of the poverty reduction from the income tax—both in terms of reducing poverty rates and the poverty gap—was concentrated among families with children and workers. For example, CRS estimates that poverty among children who lived in families with workers fell by almost 40% (from 14.7%15.3% of children in poverty to 8.9%9.4% of children in poverty) as a result of the income tax. For nonaged (i.e., nonelderly) adults in families with children and workers, poverty fell by almostroughly a third (from 12.3% 2% of nonaged adults in poverty to 8.1% of nonaged adults 8.3% in poverty). (In contrast, CRS estimates that the poverty rates among individuals who lived in families with no workers were unchanged by the income tax.) Similarly, all of the estimated $13.910.3 billion in poverty gap reduction from the current income tax occurred among families with children and workers.

.

The current income tax includes the effects of legislative changes made by P.L. 115-97, commonly referred to as the Tax Cuts and Jobs Act (TCJA). The TCJA made numerous changes to the federal income tax system, including many that affect individuals and families. A comparison of the effect of the current income tax (i.e., the post-TCJA income tax) and the pre-TCJA income tax on poverty rates and the poverty gap (assuming all else unchanged) provides one measure of the law'’s impact on poverty. CRS estimates suggestindicate that the TCJA marginally reduced poverty rates and the poverty gap, with the impact of the post-TCJA income tax similar to the impact of the pre-TCJA income tax. This suggests the law provided relatively small benefits to poor families.

Insofar as policymakers are interested in expanding the antipoverty impact of the income tax, they could expand or modify the EITC or ACTC, or create new refundable tax credits targeted toward the poor. However, refundable tax credits are subject to several limitations as a poverty reduction policy: the current credits primarily benefit those who work (and have children), limiting their ability to reduce poverty among those who do not or cannot work; they are received only once a year when income tax returns are filed, limiting their ability to help the poor meet ongoing basic needs; and they are difficult for the IRSInternal Revenue Service (IRS) to administer, subjecting the credits and their recipients to additional scrutiny.

Congressional Research Service

link to page 32 The Impact of the Federal Income Tax Code on Poverty

Overview of the Estimated Antipoverty Impact of the Federal Income Tax

Estimated Before-Tax and After-Tax Poverty Rates for Selected Individuals

After Tax

Current-Law

Prior-Law

Before

Income Tax

Income Tax

Individual by Family Type

Tax

(Post-TCJA)

(Pre-TCJA)

All Individuals Living in Families of All Types

14.7%

12.5%

12.8%

Children

18.2%

12.6%

13.1%

Nonaged Adults in Families with Children

14.3%

10.4%

10.8%

Individuals Living in Families with Workers

10.9%

8.2%

8.5%

Children

15.3%

9.4%

9.9%

the credits and their recipients to additional scrutiny.

Overview of the Estimated Antipoverty Impact of the Federal Income Tax

Estimated Before-Tax and After-Tax Poverty Rates for Selected Individuals | ||||

|

After Tax |

||||

|

Individual by Family Type |

Before Tax |

(Post-TCJA) |

(Pre-TCJA) | |

|

All Individuals Living in Families of All Types |

14.5% |

12.3% |

12.5% |

|

|

Children |

17.5% |

12.0% |

12.3% |

|

|

Nonaged Adults in Families with Children |

14.5% |

10.6% |

10.8% |

|

|

Individuals Living in Families with Workers |

10.8% |

8.1% |

8.3% |

|

|

Children |

14.7% |

8.9% |

9.2% |

|

|

Nonaged Adults in Families with Children |

12.3% |

8.3% |

8.5% |

|

|

Individuals Living in Families with No Workers |

34.7% |

34.7% |

34.7% |

|

|

Children |

64.1% |

64.1% |

64.1% |

|

|

Nonaged Adults in Families with Children |

64.3% |

64.3% |

64.3% |

|

Nonaged Adults in Families with Children

12.2%

8.1%

8.5%

Individuals Living in Families with No Workers

35.1%

35.1%

35.1%

Children

66.2%

66.2%

66.2%

Nonaged Adults in Families with Children

61.6%

61.6%

61.6%

Estimated Before-Tax | ||||

|

After Tax |

||||

|

Family Type |

|

|

| |

|

All Poor Families |

150.8 |

136.9 |

138.1 |

|

|

Poor Families with Children |

52.3 |

38.3 |

39.1 |

|

|

With Workers |

37.8 |

23.9 |

24.7 |

|

|

With No Workers |

14.5 |

14.5 |

14.5 |

|

|

Poor Families with Aged Adults, but no Children |

29.5 |

29.6 |

29.6 |

|

|

Poor Families without Children or Aged Adults |

69.1 |

69.0 |

69.4 |

|

Source: CRS estimates using TRIM3 and the ASEC 2017. For methodology, see Appendix A.

)

(Pre-TCJA)

Family Type

($ in bil ions)

($ in bil ions)

($ in bil ions)

All Poor Families

154.0

143.6

145.1

Poor Families with Children

49.9

39.4

40.4

With Workers

34.7

24.2

25.2

With No Workers

15.3

15.3

15.3

Poor Families with Aged Adults, but no Children

31.1

31.3

31.4

Poor Families without Children or Aged Adults

73.0

72.9

73.3

Source: CRS estimates using TRIM3 and the ASEC 2018. For methodology, see Appendix B. Note: The 2018 parameters of the current-law income tax (post-TCJA) and the prior-law income tax (pre-TCJA) are modeled. Due to data limitations, the impacts of the federal income tax in effect in 2018 (both pre- and post-TCJA) are modeled as if they were in effect in 2016. 2017. Items may not sum to totals due to rounding.

Introduction

Congressional Research Service

link to page 6 link to page 7 link to page 8 link to page 9 link to page 10 link to page 11 link to page 13 link to page 16 link to page 17 link to page 18 link to page 18 link to page 18 link to page 18 link to page 19 link to page 20 link to page 10 link to page 10 link to page 11 link to page 11 link to page 12 link to page 12 link to page 12 link to page 13 link to page 13 link to page 13 link to page 14 link to page 14 link to page 16 link to page 16 link to page 19 link to page 19 link to page 20 link to page 20 link to page 29 link to page 29 link to page 30 link to page 30 link to page 30 The Impact of the Federal Income Tax Code on Poverty

Contents

Introduction ..................................................................................................................................... 1 How Major Provisions of the Income Tax Code Affect the Poor .................................................... 2

Comparison to the Pre-TCJA Income Tax ................................................................................ 3

The Income Tax and Poverty ........................................................................................................... 4

The Share of Families with Positive, Negative, and Zero Tax Liabilities ................................. 5

Comparison to the Pre-TCJA Income Tax .......................................................................... 6

The Impact of the Income Tax on Poverty Rates ...................................................................... 8

Comparison to the Pre-TCJA Income Tax ......................................................................... 11

The Impact of the Income Tax on the Poverty Gap................................................................. 12

Comparison to the Pre-TCJA Income Tax ........................................................................ 13

Impact of the Income Tax on Poverty Compared to Selected Low-Income Assistance

Programs..................................................................................................................................... 13

Poverty Rate ...................................................................................................................... 13 Poverty Gap ...................................................................................................................... 14

Conclusion ..................................................................................................................................... 15

Figures Figure 1. Estimated Share of All Families with Positive, Zero, and Negative Income Tax

Liabilities Under the Current Income Tax by Family After-Tax Poverty Status, 2017 ................ 5

Figure 2. Estimated Share of Poor Families with Positive, Zero, and Negative Income Tax

Liabilities Under the Current Income Tax by Family Type, 2017 ................................................ 6

Figure 3. Estimated Share of Families with Positive, Zero, and Negative Income Tax

Liabilities Under the Current Income Tax and Pre-TCJA Income Tax by Family Poverty Status, 2017 ..................................................................................................................... 7

Figure 4. Estimated Share of Poor Families with Positive, Zero, and Negative Income Tax

Liabilities Under the Current Income Tax and Pre-TCJA Income Tax by Family Type, 2017 .............................................................................................................................................. 8

Figure 5. Estimated Before-Tax and After-Tax Poverty Rates Under the Current Income

Tax, 2017 ...................................................................................................................................... 9

Figure 6. Estimated After-Tax Poverty Rates Under the Current and Pre-TCJA Income

Tax, 2017 ..................................................................................................................................... 11

Figure 7. Estimated Percentage-Point Reduction in the Poverty Rate from the Income Tax

and Selected Low-Income Assistance Programs, 2017 .............................................................. 14

Figure 8. Estimated Dollar Reduction in the Aggregate Poverty Gap from the Income Tax

and Selected Low-Income Assistance Programs, 2017 .............................................................. 15

Figure A-1. Child Tax Credit Amounts by Income Under the Pre- and Post-TCJA Income

Tax for a Married Couple with Two Children, 2018 .................................................................. 24

Figure A-2. Child Tax Credit Amounts Under the Pre- and Post-TCJA Income Tax and

the Difference in These Amounts for Married Couple with Two Children and Less Than $36,000 in Income, 2018 ............................................................................................................ 25

Congressional Research Service

link to page 15 link to page 15 link to page 17 link to page 17 link to page 25 link to page 25 link to page 26 link to page 28 link to page 35 link to page 37 link to page 37 link to page 38 link to page 38 link to page 23 link to page 23 link to page 32 link to page 37 link to page 37 link to page 38 The Impact of the Federal Income Tax Code on Poverty

Tables Table 1. Estimated Before-Tax and After- Tax Poverty Rates for Selected Individuals

Living in Families With and Without Workers, 2017 ................................................................. 10

Table 2. Estimated Aggregate Poverty Gap Before and After the Current and Pre-TCJA

Income Tax by Family Type, 2017 ............................................................................................. 12

Table A-1. Combined Standard Deduction and Personal Exemption for Hypothetical

Taxpayers Under the Pre-TCJA and Current-Law (Post- TCJA) Income Tax, 2018 ................. 20

Table A-2. Marginal Tax Rates Under the Pre- and Post-TCJA Income Tax, 2018 ...................... 21 Table A-3. Overview of Changes to the Child Tax Credit Under the TCJA.................................. 23 Table B-1. Selected Post-TCJA Income Tax Provisions in 2018 and 2017 Dollars ...................... 30 Table C-1. Estimated Number of Individuals in Poverty Before the Income Tax for

Selected Individuals Living in Families With and Without Workers, 2017 ............................... 32

Table C-2. Estimated Number of Families in Poverty Before the Income Tax by Family

Type, 2017 .................................................................................................................................. 33

Appendixes Appendix A. How Major Provisions of the Federal Income Tax Affect the Poor and How

They Were Modified by the TCJA ............................................................................................. 18

Appendix B. Methodology and Data Sources ............................................................................... 27 Appendix C. Estimated Number of Individuals and Families in Poverty Before the

Income Tax, 2017 ....................................................................................................................... 32

Contacts Author Information ........................................................................................................................ 33

Congressional Research Service

The Impact of the Federal Income Tax Code on Poverty

Introduction The federal individual income tax is structured so that the poor owe little or no income tax (although they may pay other federal taxes, like payroll taxes as well as state and local taxes).11 In addition, the federal income tax increases the disposable income of many poor families via refundable tax credits. These tax credits—primarily the earned income tax credit (EITC) and the refundable portion of the child tax credit, called the additional child tax credit (ACTC)—increase the disposable income of many low-income taxpayers who work and have children, and have been shown to reduce poverty.2

2

P.L. 115-97, commonly referred to as the Tax Cuts and Jobs Act3Act3 (TCJA), made numerous temporary changes to the federal income tax systemcode, including many that affect individuals and families.4 Analysesfamilies.4 Preliminary analyses of the TCJA found that the law provides larger benefits to higher-income individuals and families.55 This report'’s analyses findindicate that overall the law had a relatively small impact on poverty compared to. In other words, poverty levels under the current income tax code (i.e., post-TCJA) are similar to those under the pre-TCJA federal individual income tax.

Recent tax

Tax legislation considered in the 116th116th Congress—including the Economic Mobility Act of 2019 ((H.R. 3300)H.R. 3300) ordered reported by the House Ways and Means Committee on June 20, 2019—would target additional tax benefits to lower-income families. H.R. 3300 would temporarily increase the amount of the EITC for "childless" workers,6“childless” workers;6 allow all eligible taxpayers to receive the full amount of the ACTC, irrespective of a taxpayer'’s earned income,7 and make the child and dependent care tax credit refundable. To provide context for the consideration of new tax legislation, this report examines the relationship between the federal individual income tax and poverty. Given some policymakers' continued interest in using the tax system to reduce poverty and boost the incomes of low-income working families with children, understanding the impact of the income tax in reducing poverty—pre- and post-TCJA—may help inform future policy debates and legislative proposals.

This report is structured to first provide a brief overview of the major federal income tax provisions that affect lower-income individuals and families, including a comparison of how these provisions changed under the TCJA. The report then provides an analysis of how the pre-TCJA federal income tax affected poverty, followed by a comparison of how the post-TCJA federal income tax affected poverty. The report concludes with some observations on the benefits and limitations of the federal income tax system and refundable tax credits in reducing poverty.

Key Concepts, Conventions, and Terms Used in this Report

Several major concepts, conventions, and terms used throughout this report are briefly described below. The information in this report provides some insights into how the federal income tax affects families' poverty status, specifically the immediate, short-term impact of the TCJA on poverty. The report does not estimate how the impacts of the TCJA will change over time or how people may change their behavior (e.g., choices between working and not working) in response to the TCJA.

The family is the unit of analysis. While federal income tax provisions affect taxpayers, the impact of these provisions is analyzed in terms of families. A taxpayer is generally composed of all individuals listed on a federal income tax return (IRS Form 1040) and includes an individual, his or her spouse (if married), and any dependents. Descriptions of the tax system pre- and post- TCJA will generally refer to how these changes applied to taxpayers (i.e., the below section titled, "How Major Federal Income Tax Provisions Apply to the Poor"). In contrast, poverty analysis is done at the family level since families can share many resources and expenses. Hence, in this report analyses of the impact of the income tax, pre- and post-TCJA, are generally done at the family level. In this report, a family is composed of people living together related by blood or marriage (the family), cohabiting partners, and foster children. In some cases, like multigenerational families, a family is composed of multiple taxpayers. In these cases, tax liabilities and/or benefits for all taxpayers are aggregated to determine the impact of the income tax on the family's resources. If a family is determined to be poor, all members of that family are counted as poor.

The Supplemental Poverty Measure (SPM) is used to measure the poverty impact of the federal income tax. This report examines the impact of the pre- and post-TCJA federal income tax on poverty, using the federal government's Supplemental Poverty Measure (SPM). Unlike the official poverty measure, the SPM was developed in part to help assess the effects of tax and government benefit policies on the economic well-being of low-income individuals.8 For more information on the SPM, see Appendix A and CRS Report R45031, The Supplemental Poverty Measure: Its Core Concepts, Development, and Use.

The impacts of the federal income tax (pre- and post-TCJA) are estimated using the TRIM3 model and are modeled as if they were in effect in 2016. To estimate the impact of the federal income tax on poverty—in both the pre- and post-TCJA cases—income taxes owed (or the net benefit from refundable credits received) are subtracted from (or added to) the family's other resources, which are then assessed against an SPM poverty threshold. Other taxes that a family may pay—including payroll and excise taxes—are unchanged in these analyses.9 All poverty estimates in this report are calculated using a computer simulation model called the Transfer Income Model, version 3 (TRIM3). TRIM3 uses data from the 2017 Annual Social and Economic Supplement (ASEC) to the Current Population Survey (CPS), representing income received and tax liabilities or benefits accrued during calendar year 2016. As such, the poverty estimates under the old and new income tax systems are estimated as if they were in effect in 2016. Hence, for ease of reading, the estimates in this report are described in the past tense. Details on this methodology, including how the TCJA was modeled in TRIM3, can be found in Appendix A.

How Major Federal Income Tax Provisions Apply to the Poor

The federal income tax can increase or decrease a taxpayer's disposable income, which may affect a family';7 and make

1 The principle that poor families should not owe federal income taxes can be found in the enactment of the Tax Reform Act of 1986 (P.L. 99-514). The Joint Committee on Taxation, in its explanation of the act, stated: “In addition to ensuring that high-income taxpayers pay their share of the Federal tax burden, the Act provides tax relief to low-and middle-income wage earners. To achieve this goal, the Act substantially increases the standard deduction (the prior-law zero bracket amount) and almost doubles the personal exemption. Together with the greatly expanded earned income credit, these provisions relieve approximately six million low-income individuals from income tax liability and ensure that no families below the poverty level will have Federal income tax liability.” Joint Committee on Taxation, General Explanation of the Tax Reform Act of 1986, committee print, 99th Cong., May 4, 1987, JCS-10-87, p. 8.

2 For example, see CRS Report R44057, The Earned Income Tax Credit (EITC): An Economic Analysis. 3 The original title of the law, the Tax Cuts and Jobs Act, was stricken before final passage because it violated what is known as the Byrd rule, a procedural rule that can be raised in the Senate when bills, like the tax bill, are considered under the process of reconciliation. The actual title of the law is “To provide for reconciliation pursuant to titles II and V of the concurrent resolution on the budget for fiscal year 2018.” For more information on the Byrd rule, see CRS Report RL30862, The Budget Reconciliation Process: The Senate’s “Byrd Rule”.

4 Most of the changes that affect individuals are temporary. The temporary changes are generally scheduled to be in effect from 2018 through the end of 2025. For an overview of all changes made in the law, see CRS Report R45092, The 2017 Tax Revision (P.L. 115-97): Comparison to 2017 Tax Law.

5 For example, the Joint Committee on Taxation found in 2019 that on average, the law would reduce income taxes for all taxpayers, although to a greater extent for higher-income taxpayers. See Joint Committee on Taxation, Distributional Effects of the Conference Agreement for H.R. 1, the “Tax Cuts and Jobs Act,” 115th Cong., December 18, 2017. Similarly, the Tax Policy Center found that the TCJA increased after-tax income in 2018 by 0.4% for households in the lowest quintile, compared with 2.9% for those in the top quintile and even more for the top few percent of households. For more information, see Tax Policy Center, Distributional Analysis of the Conference Agreement for the Tax Cuts and Jobs Act, December 18, 2017.

6 The bill would expand the EITC for workers without qualifying children, commonly referred to as the “childless” EITC. While some workers eligible for this credit may indeed have no children, others may have children who do not reside with them for more than half the year, and others may live with children whom for various reasons they cannot claim for the EITC (e.g., an individual living with but not married to a mother with children from another relationship).

7 Under current law, the ACTC phases in for low-income taxpayers based on their earned income, and the maximum amount of the ACTC is $1,400 per qualifying child. Under H.R. 3300, the earned income phase-in of the credit is effectively eliminated in 2019 and 2020, and hence all eligible low-income taxpayers with children would be able to receive $2,000 per qualifying child ($3,000 for a child under four years old) for those years. The $3,000 credit for

Congressional Research Service

1

link to page 23 The Impact of the Federal Income Tax Code on Poverty

the child and dependent care tax credit refundable. Similar tax law changes have been included in the Heroes Act (H.R. 6800), which passed the House on May 15, 2020, and a revised version of the Heroes Act (H.R. 8406), which passed the House on October 1, 2020. To provide context for the consideration of new tax legislation, this report examines the impact of the current federal individual income tax code on poverty. Given some policymakers’ continued interest in using the tax system to reduce poverty and boost the disposable incomes of low-income working families with children, understanding the impact of the income tax in reducing poverty—both under current law and pre-TCJA—may help inform future policy debates and legislative proposals.

This report first provides a brief summary of how the federal income tax affects the poor. The report then provides an analysis of how the current-law federal income tax affects poverty, including comparisons to the pre-TCJA income tax. A brief comparison of the income tax’s antipoverty impact to those of other needs-tested programs is also provided. The report concludes with some observations on the benefits and limitations of the federal income tax system and refundable tax credits in reducing poverty.

How Major Provisions of the Income Tax Code Affect the Poor The federal income tax code can increase or decrease a taxpayer’s disposable income, which in turn affects a family’s poverty status. Broadly, when a taxpayer receives refundable tax credits greater than the income taxes they owe, they have a negative tax liability, and an increase in disposable income, all else being equal.108 Conversely, if a taxpayer owes federal income tax, they have a positive tax liability, and reduced disposable income, all else being equal. (If a taxpayer has zero tax liability, their disposable income is unchanged by the income tax.) Unless otherwise mentioned, the term tax liability will refer to federal income tax liability in this report.

In order to understand how the individual income tax can affect tax liabilities, it can be helpful to broadly understand how income taxes are calculated, and in particular, how major components of the income tax affect poor taxpayers. Importantly, the description below summarizes only the major aspects of the federal income tax calculation that are particularly relevant for poor families. For a more detailed overview of the federal income tax calculation, see CRS Report R45145, Overview of the Federal Tax System in 2018; and CRS Infographic IG10014, The U.S. Individual Income Tax System, 2019.11 For a more detailed description of the tax provisions summarized below, how they affect income tax liability, and how they were modified by the TCJA, see CRS Report R45092, The 2017 Tax Revision (P.L. 115-97): Comparison to 2017 Tax Law.

The TCJA substantially modified the federal tax code, including changing many provisions that affect individuals. Most of these changes are temporary, and are scheduled to expire ("sunset") at the end of 2025. The major changes made by the TCJA that are likely to affect many low-income taxpayers are highlighted below.12

Calculating Income Tax Liability

The first step for taxpayers in calculating their income tax liability is to add up their income from various sources to calculate their gross income.

Exclusion of Public Assistance

The income tax code excludes certain types of income received by lower-income individuals from gross income. For example, public assistance payments (cash assistance from the Supplemental Security Income program or the Temporary Assistance for Needy Families [TANF] Block Grant) and the value of certain noncash benefits (food benefits from the Supplemental Nutrition Assistance Program [SNAP] or the subsidy value of housing benefits) are excluded from gross income under the income tax system, and hence are not taxable. The TCJA did not make any changes to the exclusion of public assistance.

The taxpayer then subtracts from gross income various deductions and exemptions to calculate the amount of income that is taxable—their taxable income. Most low-income taxpayers will subtract from their gross income the standard deduction (and before 2018, personal exemptions) to calculate their taxable income.

The Standard Deduction and Personal Exemptions

The standard deduction is a fixed dollar amount all taxpayers may deduct from their income, with the amount varying by the taxpayer's tax filing status.13 In 2018, before enactment of the TCJA, the standard deduction would have ranged from $6,500 to $13,000, depending on the taxpayer's filing status. The TCJA almost doubled the standard deduction. The personal exemption is a per-person subtraction from gross income for the taxpayer and, if applicable, his or her spouse and dependents. Before enactment of the TCJA, the personal exemption would have equaled $4,150 per person in 2018. The TCJA effectively eliminated the personal exemption (reduced the amount to $0). When combined, the personal exemptions and the standard deduction represent an amount of income that is not subject to income taxation. As a result of these provisions, many low-income taxpayers have little or no taxable income and hence have little or no income tax liability. (Taxable income cannot be reduced below zero.)

After taxpayers have calculated their taxable income, they then apply marginal tax rates to calculate their tax liability before credits.

Marginal Tax Rates

A marginal tax rate is the tax incurred on each additional dollar of taxable income. Marginal tax rates in the individual income tax code are graduated, meaning the rate increases over successive ranges of taxable income. Many low-income taxpayers who do have taxable income pay taxes at the lowest marginal rate of 10%. The ranges of taxable income and their associated rate are often referred to as tax brackets. Taxpayers determine their tax liability before credits by applying marginal tax rates to their taxable income. Then taxpayers can subtract tax credits to determine their final tax liability. The 10% tax bracket (the lowest tax bracket) was unchanged by the TCJA. In general, marginal tax rates above the 10% rate were reduced under the TCJA. See Table C-2.

Refundable Tax Credits

Tax credits reduce the amount a taxpayer owes dollar-for-dollar the value of the credit. Credits can be nonrefundable or refundable. Nonrefundable credits cannot exceed tax liability, and therefore can only reduce tax liability to zero. In other words, "the maximum value of a nonrefundable credit is capped at a taxpayer's tax liability."14 For example, if a taxpayer owes $1,000 in income taxes and is eligible to receive $4,000 in nonrefundable tax credits, the taxpayer will receive only $1,000 in nonrefundable tax credits, reducing their income

Key aspects of the current income tax code that affect the poor are described below. These features tend to result in many poor families not owing income taxes, and receiving a net increase in disposable income from the income tax system. A more in-depth discussion can be found in Appendix A.

Public assistance is not taxed. The income tax code excludes certain types of income received by lower-income individuals from gross income. For example, public assistance payments (cash assistance from the Supplemental Security Income program or the Temporary Assistance for Needy Families [TANF] Block Grant) and the value of certain noncash benefits (food benefits from the Supplemental Nutrition Assistance Program [SNAP] or the subsidy value of housing benefits) are excluded from gross income under the income tax system, and hence are not taxable.

Poor taxpayers often have no taxable income. As a result of the standard deduction, many low-income taxpayers have zero taxable income. The standard deduction is a fixed dollar amount that

children under four years old was added as an amendment during the Ways and Means Committee’s consideration of H.R. 3300. This amendment passed by a roll call vote of 22 yeas to 19 nays in the committee. For more information, see House Committee on Ways and Means, Markup of Tax Legislation, 116th Cong., 1st sess., June 20, 2019, https://waysandmeans.house.gov/legislation/markups/markup-hr-3298-child-care-quality-and-access-act-2019-hr-3299-promoting-respect.

8 By definition, the value of a refundable tax credit received can be greater than a taxpayer’s income tax liability. For example, if a taxpayer has a $1,000 income tax liability, but is eligible to receive $3,000 in refundable tax credits, those credits will first reduce their income tax liability to zero and they will receive a net benefit of $2,000. In other words, the taxpayer will have a negative tax liability of $2,000.

Congressional Research Service

2

link to page 25 The Impact of the Federal Income Tax Code on Poverty

taxpayers can subtract from their total income when determining the amount of their income subject to taxation (i.e., “taxable income”). In 2018 the standard deduction for unmarried single filers, head of household filers (i.e., single parents), and married joint filers was $12,000, $18,000, and $24,000, respectively.9 In other words, taxpayers with income at or below these levels had no taxable income and hence no income tax liability.

Poor taxpayers who do have taxable income are subject to low statutory marginal tax rates. Marginal tax rates in the individual income tax code are graduated, meaning the rate increases over successive ranges of taxable income. Many low-income taxpayers who do have taxable income are subject to the lowest marginal rate of 10%.

Refundable tax credits increase disposable income. Tax credits reduce the amount a taxpayer owes dollar-for-dollar the value of the credit.10 Generally, low-income taxpayers receive refundable tax credits (or the portion that remains after offsetting any income taxes owed) as a tax refund (or an increase in their tax refund, if they are already receiving a refund). The two major refundable tax credits claimed by low-income working taxpayers are the EITC and the additional child tax credit (the ACTC, which is the refundable portion of the child tax credit).11 Combined, these credits can boost incomes of working families with children by several thousand dollars, depending on their earned income, marital status, and number of children.

Comparison to the Pre-TCJA Income Tax The current income tax code includes the legislative changes made by P.L. 115-97, commonly referred to as the Tax Cuts and Jobs Act (TCJA). The TCJA made numerous changes to the federal income tax system, including many that affect individuals and families. The ultimate impact of the TCJA on a particular taxpayer’s tax liability depends on how the taxpayer’s individual circumstances interact with all of these provisions, not just one of them. Most of these changes are temporary, and are scheduled to expire (“sunset”) at the end of 2025.

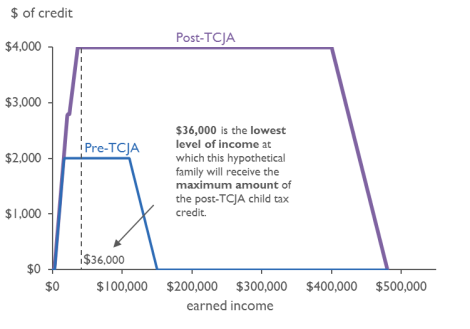

With respect to provisions of the income tax code that affect the poor, the TCJA made two main changes. First, the amount of income that is not subject to taxation may have changed for some taxpayers. Specifically, the law almost doubled the standard deduction amount to current levels, and effectively eliminated the personal exemption (a fixed dollar amount per person taxpayers subtracted from the income).12 For many taxpayers, these changes do not affect their amount of taxable income. However, for some taxpayers, especially larger families, more of their income may be subject to the federal income tax because of these changes (see Table A-1).13 Second, the law expanded the child tax credit, doubling the maximum amount, increasing the maximum amount of the ACTC, and increasing the income level at which the credit begins to phase out (see

9 These amounts are annually adjusted for inflation. In 2020, these amounts are $24,800 for married joint filers, $12,400 for single filers, and $18,650 for head of household filers. See Internal Revenue Service, Revenue Procedure 2019-44.

10 Credits can be nonrefundable or refundable. Nonrefundable credits cannot exceed tax liability, and therefore can only reduce tax liability to zero. By contrast, refundable credits are not limited by how much a taxpayer owes in income taxes, meaning those with little to no income tax liability, including may poor taxpayers, can receive the full value of the credit.

11 Some low-income taxpayers will receive both the ACTC and the nonrefundable portion of the child tax credit. The sum of the ACTC and the nonrefundable child tax credit cannot exceed the maximum credit per child.

12 The personal exemption is a fixed dollar amount per person listed on a tax return that is subtracted from total income to calculate taxable income. If in effect in 2020, it would have equaled $4,300. While the personal exemption remains in the income tax code under Section 151, the TCJA zeroed it out from 2018 through the end of 2025.

13 Even if these families may have more taxable income, other changes in the law, including a $500 nonrefundable tax credit for non-child credit eligible dependents, may offset any increases in tax liability.

Congressional Research Service

3

link to page 29 link to page 30 link to page 32 link to page 32 The Impact of the Federal Income Tax Code on Poverty

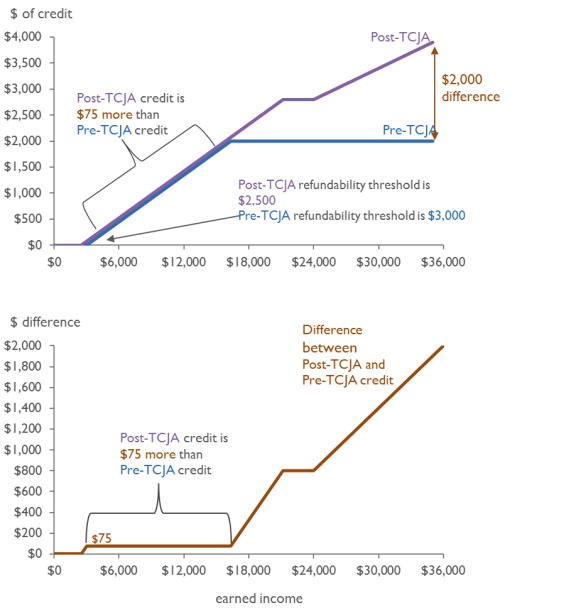

Figure A-1). These changes substantially increased the credit amount for many middle-income and high-income families. Many low-income families were eligible for a relatively modest increase of up to $75 (see Figure A-2).

Key Concepts, Conventions, and Terms Used in this Report

Several major concepts, conventions, and terms used throughout this report are briefly described below. The family is the unit of analysis. Although federal income tax provisions affect taxpayers, the impact of these provisions is analyzed in terms of families. A taxpayer is generally composed of all individuals listed on a federal income tax return (IRS Form 1040) and includes an individual, their spouse (if married), and any dependents. In contrast, poverty analysis is done at the family level because families can share many resources and expenses. Hence, in this report analyses of the impact of the income tax are generally done at the family level. In this report, a family is composed of people living together related by blood or marriage (the family), cohabiting partners, and

foster children. In some cases, like multigenerational families, a family is composed of multiple taxpayers. In these cases, tax liabilities and/or benefits for all taxpayers are aggregated to determine the impact of the income tax on the family’s resources. If a family is determined to be poor, all members of that family are counted as poor. The Supplemental Poverty Measure (SPM) is used to measure the poverty impact of the federal income tax. This report examines the impact of the federal income tax on poverty, using the federal government’s Supplemental Poverty Measure (SPM). Unlike the official poverty measure, the SPM was developed in part to help assess the effects of tax and government benefit policies on the economic well-being of low-income individuals. For more information on the SPM, see Appendix B and CRS Report R45031, The Supplemental Poverty Measure: Its Core Concepts, Development, and Use. The impacts of the federal income tax (under current law and pre-TCJA) are estimated using the TRIM3 model and are modeled as if they were in effect in 2017. To estimate the impact of the federal income tax on poverty—in both the pre- and post-TCJA cases—income taxes owed (or the net benefit from refundable credits received) are subtracted from (or added to) the family’s other resources, which are then assessed against an SPM poverty threshold. Other taxes that a family may pay—including payrol and excise taxes—are unchanged in these analyses.14 Al poverty estimates in this report are calculated using a computer simulation model called the Transfer Income Model, version 3 (TRIM3). TRIM3 uses data from the 2018 Annual Social and Economic Supplement (ASEC) to the Current Population Survey (CPS), representing income received and tax liabilities or benefits accrued during calendar year 2017. As such, the poverty estimates under the old and new income tax systems are estimated as if they were in effect in 2017. Hence, for ease of reading, the estimates in this report are described in the past tense. Details on this methodology, including how the TCJA was modeled in TRIM3, can be found in Appendix B.

Thethe credit. A refundable tax credit provides a net benefit to a taxpayer (i.e., after-tax income is greater than before-tax income) when the amount of the credit is greater than the taxpayer's income tax liability. For example, if a taxpayer owes $1,000 in income taxes but receives $4,000 in refundable tax credits, the taxpayer has a net benefit (and negative tax liability) of $3,000.15

The two major refundable tax credits claimed by low-income working taxpayers are the EITC and the additional child tax credit (the ACTC, which is the refundable portion of the child tax credit).16 The amount of the EITC is based on a taxpayer's earned income, marital status, and number of qualifying children. In 2018, before the TCJA, the maximum amount of the credit would have ranged from $520 to $6,444, depending on the number of qualifying children.17 The TCJA did not alter the EITC itself, though it did change the rules for adjusting it for inflation, which resulted in a slightly smaller EITC under the TCJA than under prior law (a difference of $1 to $13 in 2018, depending on the number of qualifying children claimed by a taxpayer).18 Before the TCJA the child tax credit equaled a maximum $1,000 per child, and up to the full amount ($1,000 per child) could be received as the ACTC. The ACTC was calculated as 15% of earned income over $3,000, not to exceed $1,000 per child. The TCJA increased the maximum child tax credit from $1,000 to $2,000 per child and increased the maximum amount of credit that could be claimed as the ACTC from $1,000 to $1,400 per child. The formula for calculating the ACTC was also modestly changed. Post-TCJA, the ACTC formula now equals 15% of earned income above $2,500, not to exceed $1,400 per child. While many low-income taxpayers did receive a larger benefit as a result of these changes, the poorest taxpayers received a more modest increase of up to $75 (see Figure C-1 and Figure C-2).

Impact of the TCJA on a Taxpayer's Tax Liability

The ultimate impact of the TCJA on a particular taxpayer's tax liability depends on how the taxpayer's individual circumstances interact with all of these provisions, not just one of them. For example, as a result of all the changes made by the TCJA, a taxpayer may have greater taxable income, but that income may be subject to lower marginal tax rates, and the taxpayer may also be eligible for a larger child credit. Hence, even though on average the TCJA lowered tax liabilities, individual taxpayers' tax liabilities may have been unchanged, increased, or decreased as a result of the law.19

The Pre-TCJA Income Tax and Poverty

Under the pre-TCJA income tax, Income Tax and Poverty Under the current income tax—that is, the income tax code as amended by the TCJA—many poor families did not owe federal income taxes (i.e., had zero tax liability), and a significant proportion received a net benefit from refundable credits. As previously discussed, the combination of personal exemptions and the standard deduction—subtracted from gross income to determine income subject to the tax—generally reduced most poor families' taxable income to zero. Additionally, some poor families with little or no income tax liability—particularly those with children and earned income—received refundable tax credits that resulted in their after-tax income being greater than their before-tax income. (CRS estimates that before (i.e., had a negative tax liability) that pushed them above the poverty line. Most of the antipoverty impact of the income tax was concentrated among families with children and workers, who are the major recipients of refundable tax credits.

This impact of the current income code on poverty rates is similar to the impact of the pre-TCJA income tax code. In addition, the current income tax system and the pre-TCJA income tax system had roughly the same impact on the poverty gap. These estimates suggest the TCJA changes to the tax code provided relatively small benefits to poor families.

14 In addition, state income tax liabilities are assumed to be unchanged in the TRIM3 model between the pre- and post-TCJA tax codes. In reality, for some taxpayers, changes made to the federal income tax code by the TCJA may affect their state income tax liabilities. See Richard C. Auxier and Elaine Maag, Post-TCJA, Your State Should Consider a Refundable Child Tax Credit, Tax Policy Center, November 15, 2018, at https://www.taxpolicycenter.org/taxvox/post-tcja-your-state-should-consider-refundable-child-tax-credit.

Congressional Research Service

4

link to page 37 link to page 10 link to page 10 link to page 32

The Impact of the Federal Income Tax Code on Poverty

The Congressional Research Service (CRS) estimates that before the income tax was subtracted from [(or added to, in the case of negative tax liabilities]) a family'’s resources, there were approximately 21.48 million families—equaling an estimated 4647.5 million individuals—in poverty. For more information, see Appendix B.)

PoorC.

The Share of Families with Positive, Negative, and Zero Tax Liabilities Under the Pre-TCJA Income Tax

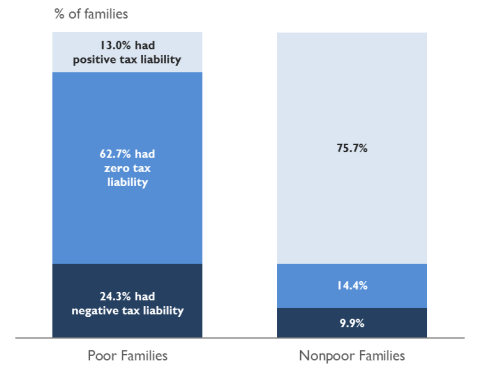

Figure 1 illustratesFigure 1 shows the estimated share of all families who owed income taxes (positive tax liability), owed no income taxes (zero tax liability), or owed no income taxes and received a net benefit from refundable tax credits (negative tax liability) by family poverty status. Under the pre-TCJA income tax, under the current income tax. These estimates of the current income tax are based on tax law in effect beginning in 2018, after the enactment of TCJA. Family poverty status was determined based on family income after applying the income tax code.

As illustrated in Figure 1, under the current income tax, CRS estimates that the majority of nonpoor families (75.774.6%) owed income taxes. In contrast, the majority of poor families (62.765.2%) owed no income taxes, and approximately a quarter (24.323.5%) owed no income taxes and received a net benefit from refundable tax credits.

Figure 1. Estimated Share of All Families with |

|

2017

Source: CRS estimates using TRIM3 and the ASEC B. Note: Poverty status is determined using the SPM. Estimates under the |

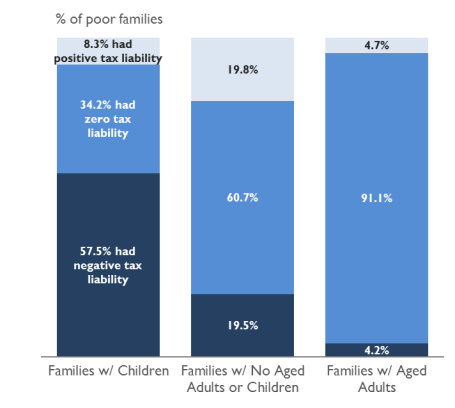

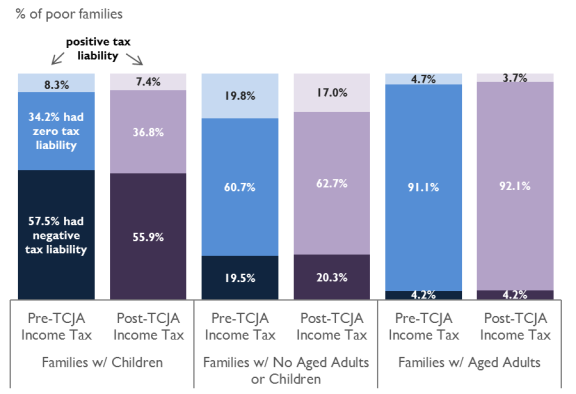

Figure 2 shows the estimated share of poor families with positive, zero, and negative tax liabilities under current law by the presence of children or aged family members. Nearly 6 in 10 poor families with children (57.5%) had a negative tax liability under the pre-TCJAcurrent income tax. In comparison, nearlyalmost 2 in 10 poor families without children or aged adults (19.518.8%) had a negative tax liability.

tax liability.

Figure 2. Estimated Share of Poor Families with |

|

2017

Source: CRS estimates using TRIM3 and the ASEC B. Notes: Poverty status is determined using the SPM. Estimates under the |

The Impact of Pre-TCJA Income Tax on Poverty Rates

Comparing poverty rates before and after a policy change is one way to assess a policy's impact on poverty. To calculate poverty rates under the pre-TCJA income tax, a family's poverty status must be determined before and after tax. A family's before-tax poverty status is based on the family's available financial resources before federal income tax liabilities are subtracted from (or added to, in the case of negative tax liabilities) their disposable income. In contrast, a family's after-tax poverty status is based on the family's financial resources after the federal income tax is subtracted from (or added to, in the case of negative tax liabilities) disposable income. If the income tax boosts income sufficiently to push a poor family above the poverty threshold, they are then counted as nonpoor as a result of the pre-TCJA income tax. As previously discussed, if a family is determined to be poor, all members of that family are counted as poor. Poverty rates are then calculated based on the number of individuals who are poor before and after the pre-TCJA income tax is applied.

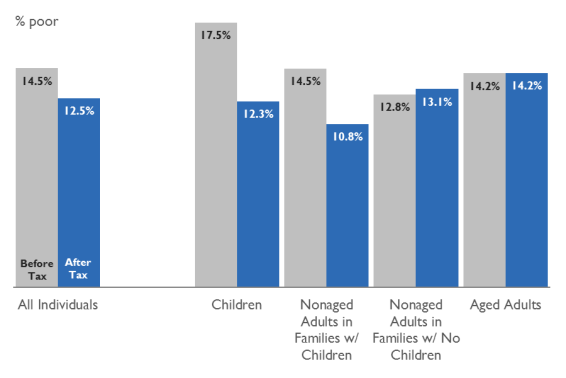

Figure 3 shows the effect of the pre-TCJA income tax system on the poverty rates of individuals based on the types of families in which individuals lived. Overall, the pre-TCJA income tax reduced poverty: the before-tax poverty rate was 14.5%, while the after-tax poverty rate was 12.5%, a net reduction of two percentage points. Figure 3 also indicates that the poverty reduction impact of the income tax was concentrated among individuals who lived in families with children. Specifically, the pre-TCJA income tax reduced child poverty by nearly 30% (from 17.5% in poverty to 12.3% in poverty) and reduced poverty among nonaged (i.e., nonelderly) adults in families with children by a quarter (from 14.5% in poverty to 10.8% in poverty).20 In contrast, the post-tax poverty rate for nonaged adults in families with no children was higher than the pre-tax poverty rate for this group (the poverty rate for individuals in this group rose from 12.8% to 13.1%).

|

|

Notes: Poverty status is determined using the SPM. Estimates under the pre-TCJA income tax are estimated as if they were in effect in 2016. Children are under 18 years old. Aged adults are 65 years old and older. |

Further examination of the impact of the pre-TCJA income tax on poverty rates indicates that all of the antipoverty effect of the federal income tax went to those individuals who lived in families with workers. As illustrated in Table 1, CRS estimates that among the subset of families who had no workers, poverty rates, including the poverty rates of children and nonaged adults who lived with children, were unchanged by the pre-TCJA income tax. In contrast, among those who lived with a worker, poverty fell by over 20% (from 10.8% in poverty to 8.3% in poverty), with larger reductions for children and nonaged adults who lived in families with children. In other words, the poverty reduction of the pre-TCJA income tax was concentrated among individuals who lived with workers and children.

Table 1. Estimated Before-Tax and After- Tax Poverty RatesUnder the Pre-TCJA Income Tax forSelected Individuals Living in Families With and Without Workers, 2016

|

Individuals by Family Type |

Before Tax |

After Tax |

|

All Individuals Living in Families of All Types |

14.5% |

12.5% |

|

Children |

17.5% |

12.3% |

|

Nonaged Adults in Families with Children |

14.5% |

10.8% |

|

Individuals Living in Families with Workers |

10.8% |

8.3% |

|

Children |

14.7% |

9.2% |

|

Nonaged Adults in Families with Children |

12.3% |

8.5% |

|

Individuals Living in Families with No Workers |

34.7% |

34.7% |

|

Children |

64.1% |

64.1% |

|

Nonaged Adults in Families with Children |

64.3% |

64.3% |

Source: CRS estimates using TRIM3 and the ASEC 2017. See Appendix A.

Notes: Poverty status is determined using the SPM. Estimates under the pre-TCJA income tax are estimated as if they were in effect in 2016. Children are under 18 years old. An aged adult is 65 years old and older. A family with workers is a family that includes at least one worker. Workers are individuals 18 years and older who work at least one week during the year. For estimates of the number of individuals in poverty before the income tax by their family type, see Table B-1.

The Impact of Pre-TCJA Income Tax on the Poverty Gap

The poverty gap is another metric that can be used to understand poverty and to examine the impact of a policy on poverty. The poverty gap is the difference between the poverty threshold (an amount of money below which a family is counted as poor) and a family's disposable income. (The poverty gap for a nonpoor family is $0.) Unlike the poverty rate, which is based on whether a family is below the poverty threshold, the poverty gap provides a way of examining the degree to which a family is below that threshold.

For example, assume there are two poor families who have the same poverty threshold of $25,000. The first family has $20,000 of disposable income, hence their poverty gap is $5,000. The second family has $10,000 of disposable income—they are poorer than the first family—and their poverty gap is $15,000. Hence the larger the poverty gap, the poorer the family.

For this analysis, poverty gaps are summed together across all poor families to determine the aggregate poverty gap. The aggregate poverty gap is calculated both before and after taxes (or refundable credits) are subtracted (or added) to disposable income as calculated under the pre-TCJA income tax. Changes to the aggregate poverty gap from the pre-TCJA income tax measure the degree to which the federal income tax reduced financial hardship among poor families.

Table 2 provides estimates of the aggregate poverty gap before and after the pre-TCJA income tax. The aggregate poverty gap before the pre-TCJA income tax was $150.8 billion. The poverty gap after the pre-TCJA income tax was $138.1 billion. Thus, the pre-TCJA income tax reduced the aggregate poverty gap by $12.7 billion, all of which went to families with children and at least one worker. For families without children (i.e., families with aged adults and families without children or aged adults), the aggregate poverty gap increased slightly as a result of the pre-TCJA income tax.

Table 2. Estimated Aggregate Poverty GapBefore and After the Pre-TCJA Income Tax by Family Type, 2016

|

Family Type |

|

|

|

| ||||||||

|

All Poor Families |

|

|

|

| ||||||||

|

Poor Families with Children |

|

|

|

| ||||||||

|

With Workers |

|

|

|

| ||||||||

|

With No Workers |

|

|

|

| ||||||||

|

Poor Families with Aged Adults, but no Children |

|

|

|

| ||||||||

|

Poor Families without Children or Aged Adults |

|

|

|

|

Source: CRS estimates using TRIM3 and the ASEC 2017. See Appendix A.

Notes: The poverty gap is estimated using the SPM. Estimates under the pre-TCJA income tax are estimated as if they were in effect in 2016. Families with children are families with or without an aged (i.e., elderly, or 65 years old and older) member who have at least one child. Families with no children or an aged member are as described. Families with aged adults are families with aged adults and no children. Children are under 18 years old. A family with workers is a family that includes at least one worker. Workers are individuals 18 years old and older who work at least one week during the year. For estimates of the number of families in poverty before the income tax by family type, see Table B-2. Items may not sum to totals due to rounding.

a. Less than $100 million.

The Post-TCJA Income Tax and Poverty

Under the post-TCJA income tax—similar to the pre-TCJA income tax—many poor families did not owe federal income taxes (i.e., had zero tax liability), and a significant proportion owed no income tax and received a net benefit from refundable credits (i.e., had a negative tax liability). The impact of the post-TCJA income tax system on poverty rates and the poverty gap suggests the TCJA provided relatively small benefits to poor families. (CRS estimates that before the income tax was subtracted from [or added to, in the case of negative tax liabilities] a family's resources, there were approximately 21.4 million families—equaling 46.5 million individuals—in poverty. For more information, see Appendix B.)

Poor Families with Positive, Negative, and Zero Tax Liabilities Under the Post-TCJA Income Tax

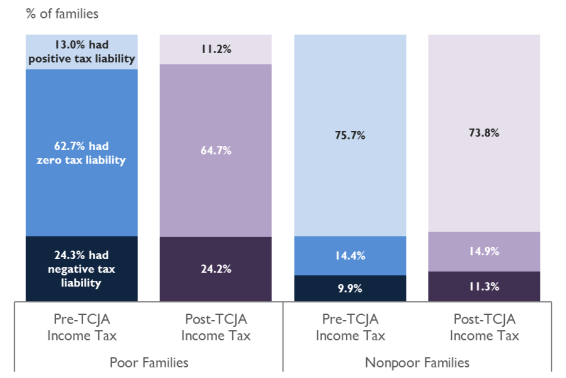

As illustrated in Figure 4, CRS analysis indicates that the shares of poor and nonpoor families with positive, negative, and zero income tax liabilities were similar pre- and post-TCJA. For both poor and nonpoor families, there is a relatively small decrease (less than 2 percentage points) in the number of families with a positive tax liability. For both poor and nonpoor families, there is a relatively small increase in the share of families with zero tax liability. The share of poor families with a negative tax liability is effectively unchanged, while the share of nonpoor families with a negative tax liability increased by a relatively small amount.

|

|

Notes: Poverty status is determined using the SPM. Estimates under the pre-TCJA and post-TCJA income tax are estimated as if they were in effect in 2016. Items may not sum to 100% due to rounding. |

Figure 5 compares the estimated share of poor families with positive, zero, and negative income tax liabilities under the pre-TCJA and post-TCJA income tax by family type. This analysis indicates that across all poor family types, the share of poor families that owed taxes (i.e., had positive tax liability) modestly fell as a result of the TCJA.21 Among poor families with children, CRS analysis indicates that share of these families who did not owe income taxes (i.e., had zero tax liability) increased as a result of the TCJA. In contrast, the share of poor families with children who received an increase in their disposable income from refundable tax credits (i.e., had a negative income tax liability) fell as a result of the TCJA.

|

|

Notes: Poverty status is determined using the SPM. Estimates under the pre-TCJA and post-TCJA income tax are estimated as if they were in effect in 2016. Families with children are families with or without an aged (i.e., elderly, or 65 years old and older) member who have at least one child. Families with no children or an aged member are as described. Families with aged adults are families with aged adults and no children. Children are under 18 years old. Items may not sum to 100% due to rounding. |

The Impact of the Post-TCJA Income Tax on Poverty Rates

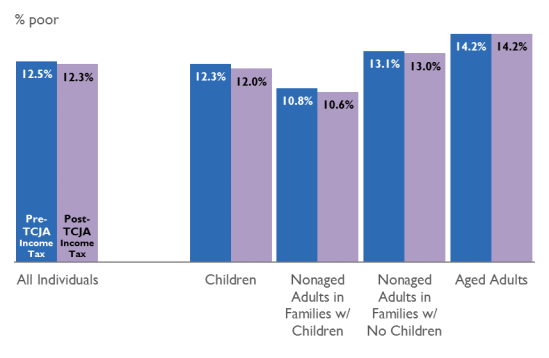

Figure 6 compares estimated after-tax poverty rates between the pre- and post-TCJA income tax. The difference in these poverty rates reflects the impact of the TCJA on poverty. These estimates indicate that the TCJA had a relatively small effect on poverty rates. CRS estimates that the TCJA reduced overall poverty by 1.6% (from 12.5% in poverty under the pre-TCJA income tax to 12.3% in poverty under the post-TCJA income tax). The impact of these changes was concentrated among individuals who lived in families with children. Specifically, the TCJA reduced poverty among children and nonaged adults living in families with children by about 2.4% and 1.9%, respectively (from 12.3% to 12.0% in poverty among children and from 10.8% to 10.6% in poverty among nonaged adults living in families with children).

|

|

Notes: Poverty status is determined using the SPM. Estimates under the pre-TCJA and post-TCJA income tax are estimated as if they were in effect in 2016. Children are under 18 years old. Aged adults are 65 years old and older. |

As with the pre-TCJA income tax, the impact of the post-TCJA income tax on poverty rates was concentrated among those who lived in a family with workers. As illustrated in Table 3, CRS estimates that among the subset of families who had no workers, the poverty rates of children and nonaged adults who lived with children were unchanged by the post-TCJA income tax. In contrast, among those who lived with a worker, poverty fell by nearly 25% (from 10.8% in poverty to 8.1% in poverty), with larger reductions for children and nonaged adults who lived in families with children. As with the pre-TCJA income tax, these estimates suggest that virtually all of the benefits of post-TCJA income tax go to individuals who live with workers and children.

Table 3. Estimated Before-Tax and After-Tax Poverty RatesUnder the Post-TCJA Income Tax forSelected Individuals Living in Families With and Without Workers, 2016

|

Individuals by Family Type |

Before Tax |

After Tax |

|

All Individuals Living in Families of All Types |

14.5% |

12.3% |

|

Children |

17.5% |

12.0% |

|

Nonaged Adults in Families with Children |

14.5% |

10.6% |

|

Individuals Living in Families with Workers |

10.8% |

8.1% |

|

Children |

14.7% |

8.9% |

|

Nonaged Adults in Families with Children |

12.3% |

8.3% |

|

Individuals Living in Families with No Workers |

34.7% |

34.7% |

|

Children |

64.1% |

64.1% |

|

Nonaged Adults in Families with Children |

64.3% |

64.3% |

Source: CRS estimates using TRIM3 and the ASEC 2017. See Appendix A.

Notes: Poverty status is determined using the SPM. Estimates under the pre-TCJA and post-TCJA income tax are estimated as if they were in effect in 2016. Children are under 18 years old. An aged adult is 65 years old and older. A family with workers is a family that includes at least one worker. Workers are individuals 18 years old and older who work at least one week during the year. For estimates of the number of individuals in poverty before the income tax by their family type, see Table B-1.

The Impact of the Post-TCJA Income Tax on the Poverty Gap

The post-TCJA income tax reduced the aggregate poverty gap from $150.8 billion to $136.9 billion. The pre-TCJA income tax reduced the aggregate poverty gap to $138.1 billion. Hence, CRS estimates that the changes made by the TCJA reduced the aggregate poverty gap by an additional $1.2 billion compared to the pre-TCJA income tax. Table 4 breaks down this $1.2 billion reduction by family type and indicates that the majority of the additional reduction in the poverty gap—approximately $800 million of the $1.2 billion—occurred among families with children. Almost all of that $800 million went to families with children and workers.

Table 4. Estimated Aggregate Poverty GapBefore and After the Pre- and Post-TCJA Income Tax by Family Type, 2016

|

Family Type |

|

|

|

| ||||||||

|

All Poor Families |

|

|

|

| ||||||||

|

Poor Families with Children |

|

|

|

| ||||||||

|

With Workers |

|

|

|

| ||||||||

|

With No Workers |

|

|

|

| ||||||||

|

Poor Families with Aged Adults, but no Children |

|

|

|

| ||||||||

|

Poor Families without Children or Aged Adults |

|

|

|

|

Source: CRS estimates using TRIM3 and the ASEC 2017. See Appendix A.

Notes: The poverty gap is estimated using the SPM. Estimates under the pre-TCJA and post-TCJA income tax are estimated. Children are under 18 years old. Aged adults are 65 years old and older.

As previously discussed, these relatively small effects were concentrated among individuals who lived in families with children. Specifically, as illustrated in Table 1, the TCJA reduced poverty among children and nonaged adults living in families with children by about 3.5% and 4.0%, respectively (from 13.1% to 12.6% in poverty among children and from 10.8% to 10.4% in poverty among nonaged adults living in families with children).

Congressional Research Service

11

link to page 18 link to page 32 The Impact of the Federal Income Tax Code on Poverty

The Impact of the Income Tax on the Poverty Gap The poverty gap is another metric that can be used to understand poverty and to examine the impact of a policy on poverty. The poverty gap is the difference between the poverty threshold (an amount of money below which a family is counted as poor) and a family’s disposable income. (The poverty gap for a nonpoor family is $0.) Unlike the poverty rate, which is based on whether a family is below the poverty threshold, the poverty gap provides a way of examining the degree to which a family is below that threshold.

For example, assume there are two poor families who have the same poverty threshold of $25,000. The first family has $20,000 of disposable income; hence their poverty gap is $5,000. The second family has $10,000 of disposable income—they are poorer than the first family—and their poverty gap is $15,000. Hence the larger the poverty gap, the poorer the family.

For this analysis, poverty gaps are summed together across all poor families to determine the aggregate poverty gap. The aggregate poverty gap is calculated both before and after taxes (or refundable credits) are subtracted (or added) to disposable income as calculated under the income tax.

The current income tax reduced the aggregate poverty gap from $154.0 billion to $143.6 billion. Thus, the income tax reduced the aggregate poverty gap by $10.4 billion, all of which went to families with children and at least one worker. For families without children (i.e., families with aged adults and families without children or aged adults), the aggregate poverty gap increased slightly as a result of the income tax.

Table 2. Estimated Aggregate Poverty Gap

Before and After the Current and Pre-TCJA Income Tax by Family Type, 2017

After Tax

Difference

Current-

Between

Law

Current-

Income

and Prior-

Tax

Prior-Law

Law

Income

Before

(Post-

Income

Tax

Tax

TCJA)

Tax

($ in

($ in

(Pre-TCJA)

Systems

Family Type

bil ions)

bil ions)

($ in bil ions) ($ in bil ions)

All Poor Families

154.0

143.6

145.1

-1.5

Poor Families with Children

49.9

39.4

40.4

-1.0

With Workers

34.7

24.2

25.2

-1.0

With No Workers

15.3

15.3

15.3

0.0a

Poor Families with Aged Adults, but no Children

31.1

31.3

31.4

0.0a

Poor Families without Children or Aged Adults

73.0

72.9

73.3

-0.4

Source: CRS estimates using TRIM3 and the ASEC 2018. See Appendix B. Notes: The poverty gap is estimated using the SPM. Estimates under the current income tax code model the tax law in effect beginning in 2018 (i.e., after the enactment of TCJA). However, due to data limitations (i.e., the 2018 ASEC data are for the 2017 calendar year), the current income tax code provisions are modeled as if they

were in effect in 2017. Estimates of the prior-law (pre-TCJA) income tax are also modeled as if they were in effect in 20162017. Families with children are families with or without an aged (i.e., elderly, or 65 years old and older) member who have at least one child. Families with no children or an aged member are as described. Families

Congressional Research Service

12

link to page 17 link to page 19 The Impact of the Federal Income Tax Code on Poverty

with aged adults are families with aged adults and no children. Children are under 18 years old. A family with workers is a family that includes at least one worker. Workers are individuals 18 years old and older who work at least one week during the year. For estimates of the number of families in poverty before the income tax by family type, see Table B-2. C-2. Items may not sum to totals due to rounding.

a.

a. Less than $100 mil ion.

Comparison to the Pre-TCJA Income Tax

Changes to the aggregate poverty gap between the current-law income tax and the prior-law (pre-TCJA) income tax measure the degree to which the federal income tax reduced financial hardship among poor families.

The prior-law income tax reduced the aggregate poverty gap to $145.1 billion. Hence, CRS estimates that the changes made by the TCJA reduced the aggregate poverty gap by an additional $1.5 billion compared to the pre-TCJA income tax. Table 2 breaks down this $1.5 billion reduction by family type and indicates that the majority of the additional reduction in the poverty gap—approximately $1.0 billion of the $1.5 billion—occurred among families with children. Almost all of that $1.0 billion went to families with children and workers.

Impact of the Income Tax on Poverty Compared to Selected Low-Income Assistance Programs Less than $100 million.

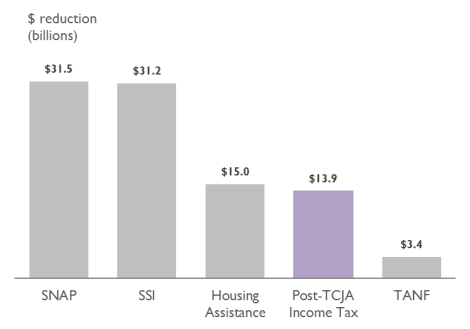

A Comparison of the Impact of the Post-TCJA Income Tax and Selected Low-Income Assistance Programs on Poverty Rates and the Poverty Gap

A comparison of estimated antipoverty effects of the post-TCJA income tax and other low-income assistance programs indicates that whilealthough the income tax substantially reduced the poverty rate, it had more limited effects on the aggregate poverty gap.22 17

Poverty Rate

Figure 7 shows the estimated percentage-point reduction in the poverty rate attributable to the post-TCJA income tax and several low-income assistance programs: the Supplemental Nutrition Assistance Program (SNAP); Supplemental Security Income (SSI); assisted housing programs (Section 8 vouchers and public housing); and Temporary Assistance for Needy Families (TANF) block grant cash assistance.2318 Only SNAP resulted in a comparable reduction in the overall poverty rate compared to the post-TCJA income tax.

17 For the purposes of this analysis, the estimated percentage-point reduction in poverty rates is calculated for each benefit program in isolation, assuming all other benefit programs are in effect.

18 For more information on these programs, see CRS Report R42505, Supplemental Nutrition Assistance Program (SNAP): A Primer on Eligibility and Benefits; CRS Report R44948, Social Security Disability Insurance (SSDI) and Supplemental Security Income (SSI): Eligibility, Benefits, and Financing; CRS Report RL34591, Overview of Federal Housing Assistance Programs and Policy; and CRS Report RL32748, The Temporary Assistance for Needy Families (TANF) Block Grant: A Primer on TANF Financing and Federal Requirements.

Congressional Research Service

13

link to page 32 link to page 20

The Impact of the Federal Income Tax Code on Poverty

Figure 7. Estimated Percentage-Point Reduction in the Poverty Rate from

the |

|

2017

Source: CRS estimates using TRIM3 and the ASEC B. Notes: Poverty status is determined using the SPM. Estimates under the |

Poverty Gap

Estimates of the reduction in the aggregate poverty gap from the post-TCJA income tax compared to selected low-income assistance programs highlight some of the limitations of the income tax in helping the poorest families. As illustrated in Figure 8, threetwo of the four low-income assistance programs reduced the poverty gap by greater amounts than the income tax.2419 This may occur for several reasons. First, these nontax programs tend to aid the very poor, and even though their benefits are not large enough to lift a family above the poverty threshold, they do provide significant financial assistance. Second, the majority of the income tax'’s antipoverty provisions—including the EITC and the ACTC—are available only to families with earned income. Poor families who receive the EITC and the ACTC tend to be "“less poor"” than other families who receive SNAP, SSI, housing assistance, and TANF.20

19 For the purposes of this analysis, the estimated reduction in the aggregate poverty gap is calculated for each benefit program in isolation, assuming all other benefit programs are in effect.