Monetary Policy and the Federal Reserve: Current Policy and Conditions

Changes from February 22, 2019 to September 4, 2019

This page shows textual changes in the document between the two versions indicated in the dates above. Textual matter removed in the later version is indicated with red strikethrough and textual matter added in the later version is indicated with blue.

Contents

- Introduction

- Recent Monetary Policy Developments

- How Does the Federal Reserve Execute Monetary Policy?

- Policy Tools

- Targeting Interest Rates

Versusversus Targeting the Money Supply - Real

Versusversus Nominal Interest Rates - Economic Effects of Monetary Policy in the Short Run and Long Run

- Low Interest Rates and the Neutral Rate

Monetary versusMonetary VersusFiscal Policy- Unconventional Monetary Policy

During and Afterduring and after the Financial Crisis - The Early Stages of the Crisis and the Zero Lower Bound

- Direct Assistance

During and Afterduring and after the Financial Crisis - Quantitative Easing and the Growth in the Fed's Balance Sheet and Bank Reserves

- The "Exit Strategy": Normalization of Monetary Policy

Afterafter QE- The Federal Reserve's Review of Monetary Policy Strategy, Tools, and Communications

QE

Appendixes

Summary

Congress has delegated responsibility for monetary policy to the Federal Reserve (the Fed), the nation's central bank, but retains oversight responsibilities for ensuring that the Fed is adhering to its statutory mandate of "maximum employment, stable prices, and moderate long-term interest rates." To meet its price stability mandate, the Fed has set a longer-run goal of 2% inflation.

The Fed's control over monetary policy stems from its exclusive ability to alter the money supply and credit conditions more broadly. Normally, the Fed conducts monetary policy by setting a target for the federal funds rate, the rate at which banks borrow and lend reserves on an overnight basis. It meets its target through open market operations, financial transactions traditionally involving U.S. Treasury securities. Beginning in 2007, the federal funds target was reduced from 5.25% to a range of 0% to 0.25% in December 2008, which economists call the zero lower bound. By historical standards, rates were kept unusually low for an unusually long time to mitigate the effects of the financial crisis and its aftermath. Starting in December 2015, the Fed has been raising interest rates and expects to gradually raise rates further. The Fed raised rates once in 2016, three times in 2017, and four times in 2018, by 0.25 percentage points each time. In light of increased economic uncertainty and financial volatility, the Fed announced in January 2019 that it would be "patient" before raising rates againbegan raising interest rates. In total, the Fed raised rates nine times between 2015 and 2018, by 0.25 percentage points each time. In light of increased economic uncertainty, the Fed then reduced interest rates by 0.25 percentage points in July 2019.

The Fed influences interest rates to affect interest-sensitive spending, such as business capital spending on plant and equipment, household spending on consumer durables, and residential investment. In addition, when interest rates diverge between countries, it causes capital flows that affect the exchange rate between foreign currencies and the dollar, which in turn affects spending on exports and imports. Through these channels, monetary policy can be used to stimulate or slow aggregate spending in the short run. In the long run, monetary policy mainly affects inflation. A low and stable rate of inflation promotes price transparency and, thereby, sounder economic decisions.

The Fed's relative independence from Congress and the Administration has been justified by many economists on the grounds that it reduces political pressure to make monetary policy decisions that are inconsistent with a long-term focus on stable inflation. But independence reduces accountability to Congress and the Administration, and recent legislation and criticism of the Fed by the President has raised the question about the proper balance between the two.

While the federal funds target was at the zero lower bound, the Fed attempted to provide additional stimulus through unsterilized purchases of Treasury and mortgage-backed securities (MBS), a practice popularly referred to as quantitative easing (QE). Between 2009 and 2014, the Fed undertook three rounds of QE. The third round was completed in October 2014, at which point the Fed's balance sheet was $4.5 trillion—five times its precrisis size. After QE ended, the Fed maintained the balance sheet at the same level until September 2017, when it began to very gradually reduce it to a more normal size. The Fed has raised interest rates in the presence of a large balance sheet through the use of two new tools—by paying banks interest on reserves held at the Fed and by engaging in reverse repurchase agreements (reverse repos) through a new overnight facility. In January 2019, the Fed announced that it would continue using these tools to set interest rates permanently, in which case the balance sheet may not get much smaller than. In August 2019, it stopped reducing the balance sheet from its current size of $4 trillion.

With regard to its mandate, the Fed believes that unemployment is currently lower than the rate that it considers consistent with maximum employment, and inflation is close to the Fed's 2% goal by the Fed's preferred measure. Even after recent rate increases, monetary policy is still considered expansionary. This monetary policy stance is unusually stimulative compared with policy in this stage of previous expansions, and is being coupled with a stimulative fiscal policy (larger structural budget deficit). Debate is currently focused on how quickly the Fed should raise rates. Some contend the greater risk is that raising rates too slowly at full employment will cause inflation to become too high or cause financial instability, whereas others contend that raising rates too quickly will cause inflation to remain too low and choke off the expansionThe decision to cut rates in July was controversial. The Fed justified the cut on the grounds that risks of a growth slowdown have intensified and inflation is still below 2%. But it also argued that the economy was still strong, and some of the risks to the economy, such as higher tariffs, had not yet materialized at the time of the decision. Overly stimulative monetary policy in a strong expansion risks economic overheating, high inflation, or asset bubbles.

Introduction

The Federal Reserve's (the Fed's) responsibilities as the nation's central bank fall into four main categories: monetary policy, provision of emergency liquidity through the lender of last resort function, supervision of certain types of banks and other financial firms for safety and soundness, and provision of payment system services to financial firms and the government.1

Congress has delegated responsibility for monetary policy to the Fed, but retains oversight responsibilities to ensure that the Fed is adhering to its statutory mandate of "maximum employment, stable prices, and moderate long-term interest rates."2 The Fed has defined stable prices as a longer-run goal of 2% inflation—the change in overall prices, as measured by the Personal Consumption Expenditures (PCE) price index. By contrast, the Fed states that "it would not be appropriate to specify a fixed goal for employment; rather, the Committee's policy decisions must be informed by assessments of the maximum level of employment, recognizing that such assessments are necessarily uncertain and subject to revision."3 Monetary policy can be used to stabilize business cycle fluctuations (alternating periods of economic expansions and recessions) in the short run, while it mainly affects inflation in the long run. The Fed's conventional tool for monetary policy is to target the federal funds rate—the overnight, interbank lending rate.4

This report provides an overview of how monetary policy works and recent developments, a summary of the Fed's actions following the financial crisis, and ends with a brief overview of the Fed's regulatory responsibilities.

Recent Monetary Policy Developments

In 1957-2019 Date of Peak Rate Peak Rate (Nominal) Peak Rate (Inflation-Adjusted) Cumulative Subsequent Reduction in Nominal Rate (Percentage Points) October 1957 3.5% 0.6% 2.9 February 1960 4.0% 2.6% 2.8 September 1969 9.2% 3.5% 5.5 July 1974 12.9% 1.4% 7.7 April 1980 17.6% 3.0% 4.8 June 1981 19.1% 9.4% 10.4 May 1989 9.8% 4.5% 5.3 November 2000 6.5% 3.1% 4.8 July 2007 5.3% 2.9% 5.1 As of: July 2019 2.4% 0.6% potential max of 2.4 Source: CRS calculations based on Fed data; David Reifschneider, "Gauging the Ability of the FOMC to Respond to Future Recessions," Federal Reserve, Finance and Economics Discussion Series 2016-068, August 2016. Notes: Federal funds rate adjusted for inflation using the consumption price index. In early expansions in the table, the federal funds rate was not the explicit target of monetary policy. The table presents the average effective federal funds rate.December 2008, in the midst ofresponse to the financial crisis and the "Great Recession," the Fed lowered the federal funds ratefederal funds target was reduced from 5.25% in 2007 to a range of 0% to 0.25% in December 2008. This was the first time rates were ever lowered to what is referred to as the zero lower bound. The recession ended in 2009, but as the economic recovery consistently proved weaker than expected in the years that followed, the Fed repeatedly pushed back its time frame for raising interest rates. As a result, the economic expansion was in its seventh year and the unemployment rate was already near the Fed's estimate of full employment when it began raising rates on December 16, 2015. This was a departure from past practice—in the previous two economic expansions, the Fed began raising rates within three years of the preceding recession ending. Since then, the Fed has continued to raiseThe Fed then raised rates in a series of steps to incrementally tighten monetary policy. The Fed raised rates —by 0.25 percentage points each time—once in 2016, three times in 2017, and four times in 2018.

In 2019, the expansion became the longest in U.S. history. In July 2019, the Fed reduced the federal funds target by 0.25 percentage points. Usually, when the Fed begins cutting interest rates, it subsequently makes several reductions over a series of months in response to the onset of a recession, although sometimes the rate cuts are more modest and short-lived "mid-cycle corrections."5 If the range of 2.25%-2.5% turns out to be the highest that the federal funds target reached in the current expansion, then it will have been much lower than at the peak of previous expansions in either nominal or inflation-adjusted terms, as shown in Table 1.

Table 1. The Federal Funds Rate at the Peak of Expansions

once in 2016, three times in 2017, and four times in 2018, by 0.25 percentage points each time. The Fed has stated that "some further gradual increases in ... the federal funds rate" are necessary to fulfill its mandate. The Fed describes its plans as "data dependent," meaning they would be altered if actual employment or inflation deviate from its forecast.

Although monetary policy is now less stimulative than it had been at the zero lower bound, the Fed is still adding stimulus to the economy as long as the federal funds rate is below what economists call the "neutral rate" (or the long-run equilibrium rate). To illustrate, the federal funds rate is currently similar to the inflation rate, meaning that the real (i.e., inflation-adjusted) federal funds rate is around zero. However, there is uncertainty as to what constitutes a neutral rate today. By historical standards, a zero real interest rate would be well below the neutral rate, but the neutral rate appears to have fallen following the financial crisis, so that current rates may be close to the neutral rate today.5

Typically, the Fed keeps interest rates below the neutral rate when the economy is operating below full employment, at neutral levels when the economy is near full employment, and above the neutral rate when the economy is at risk of overheating. Indeed, the Fed identifies this as one of its "three key principles of good monetary policy."6 Because of lags between changes in interest rates and their economic effects, in the past, the Fed has often preemptively changed its monetary policy stance before the economy reaches the state that the Fed is anticipating.

Based on the maximum employment mandate, tight labor market conditions did not support the rate cut considering monetary policy was still slightly stimulative—adjusted for inflation, rates were close to zero. Based on the price stability mandate, lower rates could be justified to avoid a potentially long-lasting decline in inflation (which would be unexpected, given labor market tightness). Arguably, the experiences of Japan and the euro area demonstrate that persistently lower-than-desirable inflation has become a harder problem for central banks to solve than high inflation since the financial crisis. Monetary policy works with a lag, and if economic conditions were to deteriorate in the near future, it would be helpful to cut rates ahead of time. Financial volatility has increased, and the Fed has argued that there are heightened risks to the economic outlook coming from the slowdown in growth abroad and the potential for economic disruptions from "trade policy uncertainty."7 The inversion of parts of the yield curve (i.e., long-term Treasury yields are lower than short-term Treasury yields) is seen by some as a warning signal that rates are too high.8In this business cycle, the Fed has maintained a (progressively less) stimulative monetary policy throughout the expansion, boosting economic activity. In one sense, this policy could be viewed as having successfully delivered on the Fed's mandated goals of full employment and stable prices. The unemployment rate has been below 5% since 2015 and is now lower than the rate believed to be consistent with full employment. Other labor market measures are also consistent with full employment, with the possible exception of the still-low labor force participation rate. Economic theory posits that lower unemployment will lead to higher inflation in the short run, but inflation has not proven responsive to lower unemployment in recent years.76 After remaining persistently below the Fed's 2% target from mid-2012 to early 2018 as measured by core PCE, inflation has remainedhovered around 2% in 2018 as measured by headline or core PCE. Economic growth has also picked up beginning in the second quarter of 2017,was also higher from the third quarter of 2017 to the first quarter of 2019 after being persistently low by historical standards throughout the expansion. Since the first quarter of 2019, employment and economic growth appear to have slowed from an elevated pace back toward trend, where projections expect it to stay in the coming quarters. Meanwhile, inflation has dipped slightly below 2% again.

after being persistently low by historical standards throughout the expansion.

Contributing to the 2018 growth acceleration, a more expansionary fiscal policy (larger structural budget deficit) added more stimulus to the economy in the short run. Two notable policy changes contributing to fiscal stimulus in 2018 were the 2017 tax cuts (P.L. 115-97) and the boost to discretionary spending in FY2018 and FY2019 agreed to in P.L. 115-123. The Fed did little to offset this fiscal stimulus, as the pace of monetary tightening in 2018 was only slightly faster than in 2017.

Despite strong economic data (which is only available with a lag), the Fed announced in January 2019 that it would be "patient" before raising rates again in light of increased economic uncertainty and financial volatility.8 The Fed's intended policy path poses risks. If the Fed waits too long to raise rates again, the economy could overheat, resulting in high inflation and posing risk to financial stability. As an example of how overly stimulative monetary policy can lead to the latter, critics contend that the Fed contributed to the precrisis housing bubble by keeping interest rates too low for too long during the economic recovery starting in 2001. Critics see these risks as outweighing any marginal benefit associated with monetary stimulus when the economy is already so close to full employment.9 Raising rates more quickly would also provide more "headroom" for the Fed to lower rates more aggressively during the next economic downturn. The potential percentage point reduction in rates before hitting the zero bound is currently smaller than the rate cuts that the Fed has undertaken in past recessions.10

Alternatively, there is uncertainty about whether strong growth, low unemployment, inflation around 2%, and the generally benign economic environment will continue. Economic expansions do not "die of old age"; nevertheless, the current expansion is already the second longest on record and cannot last forever. The flattening of the yield curve (i.e., long-term Treasury yields are similar to short-term Treasury yields) is seen by some as a warning signal that rates are too high. Although there is a risk of stimulative monetary policy causing the economy to overheat, there is also a risk that tightening too quickly could be harmful if the economy slows. Some critics would prefer clear evidence that inflation is above the Fed's target or financial conditions are unstable before the Fed raises rates again.

How Does the Federal Reserve Execute Monetary Policy?

Monetary policy refers to the actions the Fed undertakes to influence the availability and cost of money and credit to promote the goals mandated by Congress, a stable price level and maximum sustainable employment. Because the expectations of households as consumers and businesses as purchasers of capital goods exert an important influence on the major portion of spending in the United States, and because these expectations are influenced in important ways by the Fed's actions, a broader definition of monetary policy would include the directives, policies, statements, economic forecasts, and other Fed actions, especially those made by or associated with the chairman of its Board of Governors, who is the nation's central banker.

The Fed's Federal Open Market Committee (FOMC) meets every six weeks to choose a federal funds target and sometimes meets on an ad hoc basis if it wants to change the target between regularly scheduled meetings. The FOMC is composed of the 7 Fed governors, the President of the Federal Reserve Bank of New York, and 4 of the other 11 regional Federal Reserve Bank presidents serving on a rotating basis.11

The Fed generally tries to avoid surprises, and FOMC members regularly communicate their views on the future direction of monetary policy to the public. The Fed describes its monetary policy plans as "data dependent," meaning they would be altered if actual employment or inflation deviate from its forecast.

Policy Tools

The Fed targets the federal funds rate to carry out monetary policy. The federal funds rate is determined in the private market for overnight reserves of depository institutions (called the federal funds market). At the end of a given period, usually a day, depository institutions must calculate how many dollars of reserves they want or need to hold against their reservable liabilities (deposits).1214 Some institutions may discover a reserve shortage (too few reservable assets relative to those they want to hold), whereas others may have reservable assets in excess of their wants. These reserves can be borrowed and lent on an overnight basis in a private market called the federal funds market. The interest rate in this market is called the federal funds rate. If it wishes to expand money and credit, the Fed will lower the target, which encourages more lending activity and, thus, greater demand in the economy. Conversely, if it wishes to tighten money and credit, the Fed will raise the target.

The federal funds rate is linked to the interest rates that banks and other financial institutions charge for loans. Thus, whereas the Fed may directly influence only a very short-term interest rate, this rate influences other longer-term rates. However, this relationship is far from being on a one-to-one basis because longer-term market rates are influenced not only by what the Fed is doing today, but also by what it is expected to do in the future and by what inflation is expected to be in the future. This fact highlights the importance of expectations in explaining market interest rates. For that reason, a growing body of literature urges the Fed to be very transparent in explaining what its policy is, will be, and in making a commitment to adhere to that policy.1315 The Fed has responded to this literature and is increasingly transparent in explaining its policy measures and what these measures are expected to accomplish.

The Federal Reserve uses two methods to maintain its target for the federal funds rate:

- Traditionally, the Fed primarily relied on open market operations, which involves the Fed buying existing U.S. Treasury securities in the secondary market (i.e., those that have already been issued and sold to private investors).

1416 Should the Fed buy securities, it does so with the equivalent of newly issued currency (Federal Reserve notes), which expands the reserve base and increases the ability of depository institutions to make loans and expand money and credit. The reverse is true if the Fed decides to sell securities from its portfolio. The Fed must stand ready to buy or sell as many securities as necessary to maintain its federal funds target. Outright purchases of securities were used for QE from 2009 to 2014, but normal open market operations are typically conducted through repos instead, described in the text box. When the Fed wishes to add liquidity to the banking system, it enters into repos. When it wishes to remove liquidity, the Fed enters into reverse repos.1517 Because of the large increase in bank reserves caused by QE, open market operations alone can no longer effectively maintain the federal funds target. - The Fed can also change the two interest rates it administers directly by fiat, and these interest rates influence market rates—the rate it charges to borrowers and the rate it pays to depositors.

- The Fed permits depository institutions to borrow from it directly on a temporary basis at the discount window.

1618 That is, these institutions can discount at the Fed some of their own assets to provide a temporary means for obtaining reserves. Discounts are usually on an overnight basis. For this privilege banks are charged an interest rate called the discount rate, which is set by the Fed at a small markup over the federal funds rate.1719 The Fed is referred to as the "lender of last resort" because direct lending, from the discount window and other recently created lending facilities, is negligible under normal financial conditions such as the present but was an important source of liquidity during the financial crisis. - In October 2008, the Federal Reserve began to pay interest on reserves that banks deposit at the Fed. (It pays interest on both required and excess reserves.) Since 2008, this has been the primary tool for maintaining the federal funds target. Reducing the opportunity cost for banks of holding that money as reserves at the Fed as opposed to lending it out influences the rates at which banks are willing to lend reserves to each other, such as the federal funds rate.

|

What Are Repos? Repurchase agreements (repos) are agreements between two parties to purchase and then repurchase securities at a fixed price and future date, often overnight. Although legally structured as a pair of security sales, they are economically equivalent to a collateralized loan. The difference in price between the first and second transaction determines the interest rate on the loan. The repo market is one of the largest short-term lending markets, where banks and other financial institutions are active borrowers and lenders. For the seller of the security, who receives the cash, the transaction is called a repo. For the purchaser of the security, who lends the cash, it is called a reverse repo. (When describing transactions, the Fed uses the terminology from the perspective of its counterparty.) Collateral protects the lender against potential default. In principle, any type of security can be used as collateral, but the most common collateral—and the types used by the Fed—are Treasury securities, agency MBS, and agency debt. Note: For background on the repo market, see Tobias Adrian et al., "Repo and Securities Lending," Federal Reserve Bank of New York, Staff Report no. 529, December 2011, available at http://www.newyorkfed.org/research/staff_reports/sr529.pdf. |

The Fed can also change the federal funds rate by changing reserve requirements, which specify what portion of customer deposits (primarily checking accounts) banks must hold as vault cash or on deposit at the Fed. Thus, reserve requirements affect the liquidity available within the federal funds market. Statute sets the numerical levels of reserve requirements, although the Fed has some discretion to adjust them. Currently, banks are required to hold 0% to 10% of customer deposits that qualify as net transaction accounts in reserves, depending on the size of the bank's deposits.1820 This tool is used rarely—the percentage was last changed in 1992.19

Each of these tools works by altering the overall liquidity available for use by the banking system, which influences the amount of assets these institutions can acquire. These assets are often called credit because they represent loans the institutions have made to businesses and households, among others.

Targeting Interest Rates Versusversus Targeting the Money Supply

The Fed's control over monetary policy stems from its exclusive ability to alter the money supply and credit conditions more broadly. The Fed directly controls the monetary base, which is made up of currency (Federal Reserve notes) and bank reserves. The size of the monetary base, in turn, influences broader measures of the money supply, which include close substitutes to currency, such as demand deposits (e.g., checking accounts) held at banks.

The Fed's definition of monetary policy as the actions it undertakes to influence the availability and cost of money and credit suggests two ways to measure the stance of monetary policy. One is to look at the cost of money and credit as measured by the rate of interest relative to inflation (or inflation projections), and the other is to look at the growth of money and credit itself. Thus, it is possible to look at either interest rates or the growth in the supply of money and credit in coming to a conclusion about the current stance of monetary policy—that is, whether it is expansionary (adding stimulus to the economy), contractionary (slowing economic activity), or neutral.

During the high inflation experience of the 1970s the Fed placed greater emphasis on money supply growth, but since then, most central banks including the Fed have preferred to formulate monetary policy in terms of the cost of money and credit rather than in terms of their supply. The Fed conducts monetary policy by focusing on the cost of money and credit as proxied by the federal funds rate.

Real Versusversus Nominal Interest Rates

A simple comparison of market interest rates over time as an indicator of changes in the stance of monetary policy is potentially misleading, however. Economists call the interest rate that is essential to decisions made by households and businesses to buy capital goods the real interest rate. It is often proxied by subtracting from the market interest rate the actual or expected rate of inflation. If inflation rises and market interest rates remain the same, then real interest rates have fallen, with a similar economic effect as if market rates (called nominal rates) had fallen by the same amount with a constant inflation rate.

The federal funds rate is only one of the many interest rates in the financial system that determines economic activity. For these other rates, the real rate is largely independent of the amount of money and credit over the longer run because it is determined by the interaction of saving and investment (or the demand for capital goods). The internationalization of capital markets means that for most developed countries the relevant interaction between saving and investment that determines the real interest rate is on a global basis. Thus, real rates in the United States depend not only on U.S. national saving and investment but also on the saving and investment of other countries. For that reason, national interest rates are influenced by international credit conditions and business cycles.

Economic Effects of Monetary Policy in the Short Run and Long Run

How do changes in short-term interest rates affect the overall economy? In the short run, an expansionary monetary policy that reduces interest rates increases interest-sensitive spending, all else equal. Interest-sensitive spending includes physical investment (i.e., plant and equipment) by firms, residential investment (housing construction), and consumer-durable spending (e.g., automobiles and appliances) by households. As discussed in the next section, it also encourages exchange rate depreciation that causes exports to rise and imports to fall, all else equal. To reduce spending in the economy, the Fed raises interest rates and the process works in reverse.

An examination of U.S. economic history will show that money- and credit-induced demand expansions can have a positive effect on U.S. GDP growth and total employment. The extent to which greater interest-sensitive spending results in an increase in overall spending in the economy in the short run will depend in part on how close the economy is to full employment. When the economy is near full employment, the increase in spending is likely to be dissipated through higher inflation more quickly. When the economy is far below full employment, inflationary pressures are more likely to be muted. This same history, however, also suggests that over the longer run, a more rapid rate of growth of money and credit is largely dissipated in a more rapid rate of inflation with little, if any, lasting effect on real GDP and employment.2022

Economists have two explanations for this paradoxical behavior. First, they note that, in the short run, many economies have an elaborate system of contracts (both implicit and explicit) that makes it difficult in a short period for significant adjustments to take place in wages and prices in response to a more rapid growth of money and credit. Second, they note that expectations for one reason or another are slow to adjust to the longer-run consequences of major changes in monetary policy. This slow adjustment also adds rigidities to wages and prices. Because of these rigidities, changes in the growth of money and credit that change aggregate demand can have a large initial effect on output and employment, albeit with a policy lag of six to eight quarters before the broader economy fully responds to monetary policy measures. Over the longer run, as contracts are renegotiated and expectations adjust, wages and prices rise in response to the change in demand and much of the change in output and employment is undone. Thus, monetary policy can matter in the short run but be fairly neutral for GDP growth and employment in the longer run.21

In societies in which high rates of inflation are endemic, price adjustments are very rapid. During the final stages of very rapid inflations, called hyperinflation, the ability of more rapid rates of growth of money and credit to alter GDP growth and employment is virtually nonexistent, if not negative.

|

Federal Reserve Independence The Fed is more independent from Congress and the Administration than most other agencies. Its independence is attributable to structural reasons, such as 14-year terms of office for its Economists have justified this independence on the grounds that the mismatch between short-term and long-term benefits of monetary policy decisions (discussed above) creates political pressure to pursue interest rate targets that are too low to be consistent with stable inflation. |

Monetary VersusLow Interest Rates and the Neutral Rate

Economists judge monetary policy to be contractionary or stimulative based on whether the actual federal funds rate is above or below, respectively, the neutral rate. For example, monetary policy was contractionary for most of the 1980s because the federal funds rate was above the estimated neutral rate. Since the crisis, monetary policy has been stimulative because the federal funds rate has been below the estimated neutral rate. (As the Fed has raised interest rates, it has remained stimulative but has been less stimulative than previously.)

The neutral interest rate (sometimes called r* or the natural rate of interest) is conceptual and not directly observed—it is the idea that at any given time there is some level for the federal funds rate that will neither stimulate nor hold back economic activity. Various statistical techniques can be used to infer the neutral rate.

Since the crisis, the federal funds rate (as well as long-term rates) has been very low by historical standards—it was nearly zero from 2008 to 2015. Before the crisis, many economists assumed that the real (inflation-adjusted) neutral rate was about 2% and fairly constant over time. At the prevailing inflation rate of 2%, that would translate to a neutral rate of about 4%. If the actual federal funds rate is consistently below the neutral rate—in other words, if monetary policy is persistently stimulative—at full employment, inflation would be expected to rise. Yet the actual federal funds rate has now been below 4% since 2008 without any noticeable sustained increase in inflation, even as the economy has returned to full employment. This outcome is consistent with a decline in the neutral rate. According to some estimates, the real neutral rate has fallen by more than a percentage point since 2008.29

A decline in the neutral rate has implications for monetary policy. It means that any given federal funds rate is less stimulative or more contractionary than it would have been before the neutral rate fell. As a result, a simple historical comparison of prevailing federal funds rates before and after the crisis would give the misleading impression that monetary policy since the crisis has been more stimulative than it actually was. (Also, inflation has been lower since the crisis than it was in earlier decades, so the difference in real rates over the decades is smaller than the difference in actual rates.)

Although the neutral rate is a useful concept for framing monetary policy decisions, uncertainty about its true value points to the difficulty of basing policy on a variable that cannot be directly observed. For example, Fed Chairman Jerome Powell stated in January that "our policy rate is now in the range of the [Fed's] estimates of neutral."30 Choosing to set interest rates equal to the neutral rate would be intended to neither slow down nor speed up economic activity. But if the Fed has incorrectly estimated that the neutral rate has fallen more than it has, then monetary policy is still stimulative, and the risk of inflation rising or economic overheating is greater.

In light of this uncertainty, the neutral rate could be de-emphasized in policymaking, but without it, policy decisions may become less forward-looking, as the difference between actual rates and the neutral rate helps project future employment and inflation. Thus, a de-emphasis could lead to worse outcomes because of lags between policy changes and economic outcomes.

A lower neutral rate also limits how much monetary stimulus is potentially available to fight the next economic downturn, as discussed in the section below entitled "The Federal Reserve's Review of Monetary Policy Strategy, Tools, and Communications."31

Monetary versus Fiscal Policy

Either fiscal policy (defined here as changes in the structural budget deficit, caused by policy changes to government spending or taxes) or monetary policy can be used to alter overall spending in the economy. However, there are several important differences to consider between the two.

First, economic conditions change rapidly, and in practice monetary policy can be more nimble than fiscal policy. The Fed meets every six weeks to consider changes in interest rates and can call an unscheduled meeting any time. Large changes to fiscal policy typically occur once a year at most. Once a decision to alter fiscal policy has been made, the proposal must travel through a long and arduous legislative process that can last months before it can become law, whereas monetary policy changes are made instantly.27

Both monetary and fiscal policy measures are thought to take more than a year to achieve their full impact on the economy due to pipeline effects. In the case of monetary policy, interest rates throughout the economy may change rapidly, but it takes longer for economic actors to change their spending patterns in response. For example, in response to a lower interest rate, a business must put together a loan proposal, apply for a loan, receive approval for the loan, and then put the funds to use. In the case of fiscal policy, once legislation has been enacted, it may take some time for authorized spending to be outlayed. An agency must approve projects and select and negotiate with contractors before funds can be released. In the case of transfers or tax cuts, recipients must receive the funds and then alter their private spending patterns before the economy-wide effects are felt. For both monetary and fiscal policy, further rounds of private and public decisionmaking must occur before multiplier or ripple effects are fully felt.

Second, monetary policy is determined based only on the Fed's mandate, whereas fiscal policy is determined based on competing political goals. Fiscal policy changes have macroeconomic implications regardless of whether that was policymakers' primary intent. Political constraints have prevented increases in budget deficits from being fully reversed during expansions. Over the course of the business cycle, aggregate spending in the economy can be expected to be too high as often as it is too low. This means that stabilization policy should be tightened as often as it is loosened, yet increasing the budget deficit has proven to be much more popular than implementing the spending cuts or tax increases necessary to reduce it. As a result, the budget has been in deficit in all but five years since 1961, which has led to an accumulation of federal debt that gives policymakers less leeway to potentially undertake a robust expansionary fiscal policy, if needed, in the future. By contrast, the Fed is more insulated from political pressures, as discussed in the previous section, and experience shows that it is willing to raise or lower interest rates.

Third, the long-run consequences of fiscal and monetary policy differ. Expansionary fiscal policy creates federal debt that must be serviced by future generations. Some of this debt will be "owed to ourselves," but some (presently, about half) will be owed to foreigners. To the extent that expansionary fiscal policy crowds out private investment, it leaves future national income lower than it otherwise would have been.2833 Monetary policy does not have this effect on generational equity, although different levels of interest rates will affect borrowers and lenders differently. Furthermore, the government faces a budget constraint that limits the scope of expansionary fiscal policy—it can only issue debt as long as investors believe the debt will be honored, even if economic conditions require larger deficits to restore equilibrium.

Fourth, openness of an economy to highly mobile capital flows changes the relative effectiveness of fiscal and monetary policy. Expansionary fiscal policy would be expected to lead to higher interest rates, all else equal, which would attract foreign capital looking for a higher rate of return, causing the value of the dollar to rise.2934 Foreign capital can only enter the United States on net through a trade deficit. Thus, higher foreign capital inflows lead to higher imports, which reduce spending on domestically produced substitutes and lower spending on exports. The increase in the trade deficit would cancel out the expansionary effects of the increase in the budget deficit to some extent (in theory, entirely if capital is perfectly mobile). Expansionary monetary policy would have the opposite effect—lower interest rates would cause capital to flow abroad in search of higher rates of return elsewhere, causing the value of the dollar to fall. Foreign capital outflows would reduce the trade deficit through an increase in spending on exports and domestically produced import substitutes. Thus, foreign capital flows would (tend to) magnify the expansionary effects of monetary policy.3035

Fifth, fiscal policy can be targeted to specific recipients. In the case of normal open market operations, monetary policy cannot. This difference could be considered an advantage or a disadvantage. On the one hand, policymakers could target stimulus to aid the sectors of the economy most in need or most likely to respond positively to stimulus. On the other hand, stimulus could be allocated on the basis of political or other noneconomic factors that reduce the macroeconomic effectiveness of the stimulus. As a result, both fiscal and monetary policy have distributional implications, but the latter's are largely incidental whereas the former's can be explicitly chosen.

In cases in which economic activity is extremely depressed, monetary policy may lose some of its effectiveness. When interest rates become extremely low, interest-sensitive spending may no longer be very responsive to further rate cuts. Furthermore, interest rates cannot be lowered below zero so traditional monetary policy is limited by this "zero lower bound." In this scenario, fiscal policy may be more effective. As is discussed in the next section, some argue that the U.S. economy experienced this scenario following the recent financial crisis.

Of course, using monetary and fiscal policy to stabilize the economy are not mutually exclusive policy options. But because of the Fed's independence from Congress and the Administration, the two policy options are not always coordinated. If Congress and the Fed were to choose compatible fiscal and monetary policies, respectively, then the economic effects would be more powerful than if either policy were implemented in isolation. For example, if stimulative monetary and fiscal policies were implemented, the resulting economic stimulus would be larger than if one policy were stimulative and the other were neutral. Alternatively, if Congress and the Fed were to select incompatible policies, these policies could partially negate each other. For example, a stimulative fiscal policy and contractionary monetary policy may end up having little net effect on aggregate demand (although there may be considerable distributional effects). Thus, when fiscal and monetary policymakers disagree in the current system, they can potentially choose policies with the intent of offsetting each other's actions.3136 Whether this arrangement is better or worse for the economy depends on what policies are chosen. If one actor chooses inappropriate policies, then the lack of coordination allows the other actor to try to negate its effects.

Unconventional Monetary Policy During and Afterduring and after the Financial Crisis

When the United States experienced the worst financial crisis since the Great Depression from 2007 to 2009, the Fed undertook increasingly unprecedented steps in an attempt to restore financial stability. These steps included reducing the federal funds rate to the zero lower bound, providing direct financial assistance to financial firms, and "quantitative easing." These unconventional policy decisions continue to have consequences for monetary policy today, as the Fed embarks on monetary policy "normalization."

The Early Stages of the Crisis and the Zero Lower Bound

The bursting of the housing bubble led to the onset of a financial crisis that affected both depository institutions and other segments of the financial sector involved with housing finance. As the delinquency rates on home mortgages rose to record numbers, financial firms exposed to the mortgage market suffered capital losses and lost access to liquidity. The contagious nature of this development was soon obvious as other types of loans and credit became adversely affected. This, in turn, spilled over into the broader economy, as the lack of credit soon had a negative effect on both production and aggregate demand. In December 2007, the economy entered a recession.

As the housing slump's spillover effects to the financial system, as well as its international scope, became apparent, the Fed responded by reducing the federal funds target and the discount rate.3237 Beginning on September 18, 2007, and ending on December 16, 2008, the federal funds target was reduced from 5.25% to a range between 0% and 0.25%, where it remained until December 2015. Economists call this the zero lower bound to signify that once the federal funds rate is lowered to zero, conventional open market operations cannot be used to provide further stimulus. The Fed attempted to achieve additional monetary stimulus at the zero bound through a pledge to keep the federal funds rate low for an extended period of time, which has been called forward guidance or forward commitment.

The decision to maintain a target interest rate near zero was unprecedented. First, short-term interest rates have never before been reduced to zero in the history of the Federal Reserve.3338 Second, the Fed waited much longer than usual to begin tightening monetary policy in the current recovery. For example, in the previous two expansions, the Fed began raising rates less than three years after the preceding recession ended.

Direct Assistance During and Afterduring and after the Financial Crisis

With liquidity problems persisting as the federal funds rate was reduced, it appeared that the traditional transmission mechanism linking monetary policy to activity in the broader economy was not working. Monetary authorities became concerned that the liquidity provided to the banking system was not reaching other parts of the financial system. As noted above, using only traditional monetary policy tools, additional monetary stimulus cannot be provided once the federal funds rate has reached its zero bound. To circumvent this problem, the Fed decided to use nontraditional methods to provide additional monetary policy stimulus.

First, the Federal Reserve introduced a number of emergency credit facilities to provide increased liquidity directly to financial firms and markets. The first facility was introduced in December 2007, and several were added after the worsening of the crisis in September 2008. These facilities were designed to fill perceived gaps between open market operations and the discount window, and most of them were designed to provide short-term loans backed by collateral that exceeded the value of the loan.3439 A number of the recipients were nonbanks that are outside the regulatory umbrella of the Federal Reserve; this marked the first time that the Fed had lent to nonbanks since the Great Depression. The Fed authorized these actions under Section 13(3) of the Federal Reserve Act,3540 a seldom-used emergency provision that allowed it to extend credit to nonbank financial institutions and to nonfinancial firms as well.

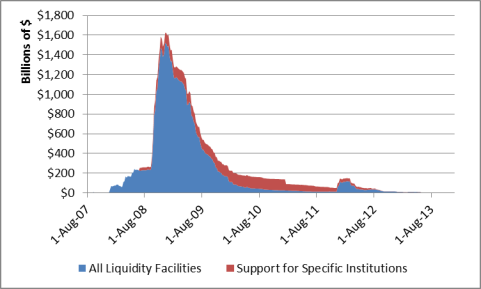

The Fed provided assistance through liquidity facilities, which included both the traditional discount window and the newly created emergency facilities mentioned above, and through direct support to prevent the failure of two specific institutions, American International Group (AIG) and Bear Stearns. The amount of assistance provided was an order of magnitude larger than normal Fed lending, as shown in Figure 1. Total assistance from the Federal Reserve at the beginning of August 2007 was approximately $234 million provided through liquidity facilities, with no direct support given. In mid-December 2008, this number reached a high of $1.6 trillion, with a near-high of $108 billion given in direct support. From that point on, it fell steadily. Assistance provided through liquidity facilities fell below $100 billion in February 2010, when many facilities were allowed to expire, and support to specific institutions fell below $100 billion in January 2011.3641 The last loan from the crisis was repaid on October 29, 2014.3742 Central bank liquidity swaps (temporary currency exchanges between the Fed and central foreign banks) are the only facility created during the crisis still active, but they have not been used on a large scale since 2012. All assistance through expired facilities has been fully repaid with interest. In 2010, the Dodd-Frank Wall Street Reform and Consumer Protection Act43 Act38 changed Section 13(3) to rule out direct support to specific institutions in the future.

|

Figure 1. Direct Fed Assistance to the Financial Sector (August 1, 2007-December 31, 2013) |

|

|

Source: Fed, Recent Balance Sheet Trends, https://www.federalreserve.gov/monetarypolicy/bst_recenttrends.htm. |

From the introduction of its first emergency lending facility in December 2007 to the worsening of the crisis in September 2008, the Fed sterilized the effects of lending on its balance sheet (i.e., prevented the balance sheet from growing) by selling an offsetting amount of Treasury securities. After September 2008, assistance exceeded remaining Treasury holdings, and the Fed allowed its balance sheet to grow. Between September 2008 and November 2008, the Fed's balance sheet more than doubled in size, increasing from less than $1 trillion to more than $2 trillion. The loans and other assistance provided by the Federal Reserve to banks and nonbank institutions are considered assets on this balance sheet because they represent money owed to the Fed.

With the federal funds rate at its zero bound and direct lending falling as financial conditions began to normalize in 2009, the Fed faced the decision of whether to try to provide additional monetary stimulus through unconventional measures. It did so through two unconventional tools—large-scale asset purchases (quantitative easing) and forward guidance.

Quantitative Easing and the Growth in the Fed's Balance Sheet and Bank Reserves

With short-term rates constrained by the zero bound, the Fed hoped to reduce long-term rates through large-scale asset purchases, which were popularly referred to as quantitative easing (QE). Between 2009 and 2014, the Fed undertook three rounds of QE, buying U.S. Treasury securities, agency debt, and agency mortgage-backed securities (MBS). These securities now comprise most of the assets on the Fed's balance sheet.

To understand the effect of quantitative easing on the economy, it is first necessary to describe its effect on the Fed's balance sheet. In 2009, the Fed's emergency lending declined rapidly as market conditions stabilized, which would have caused the balance sheet to decline if the Fed took no other action. Instead, asset purchases under the first round of QE (QE1) offset the decline in lending, and from November 2008 to November 2010, the overall size of the Fed's balance sheet did not vary by much. Its composition changed because of QE1, however—the amount of Fed loans outstanding fell to less than $50 billion at the end of 2010, whereas holdings of securities rose from less than $500 billion in November 2008 to more than $2 trillion in November 2010. The second round of QE, QE2, increased the Fed's balance sheet from $2.3 trillion in November 2010 to $2.9 trillion in mid-2011. It remained around that level until September 2012,3944 when it began rising for the duration of the third round, QE3. It was about $4.5 trillion (comprised of $2.5 trillion of Treasury securities, $1.7 trillion MBS, and $0.4 trillion of agency debt) when QE3 ended in October 2014, and has remained at that level sincewhere it remained until 2017.

Table 12 summarizes the Fed's QE purchases. In total, the Fed's balance sheet increased by more than $2.5 trillion over the course of the three rounds of QE, making it about five times larger than it was before the crisis.

Table 12. Quantitative Easing (QE):

Changes in Asset Holdings on the Fed's Balance Sheet

(billions of dollars)

|

Treasury Security Holdings |

Agency MBS Holdings |

Agency Debt Holdings |

Total Assets |

|

|

QE1 |

+$302 |

+$1,129 |

+$168 |

+$451 |

|

QE2 |

+$788 |

-$142 |

-$35 |

+$578 |

|

QE3 |

+$810 |

+874 |

-$48 |

+$1,663 |

|

Total |

+$1,987 |

+$1,718 |

+$40 |

+$2,587 |

Source: Congressional Research Service (CRS)CRS calculations based on Fed data.

Notes: The first round of QE, QE1, was announced in March 2009. The "QE1" and "total" rows include agency securities and mortgage-backed securities (MBS) that the Fed began purchasing in September 2008 and January 2009, respectively. The final column does not equal the sum of the first three columns because of changes in other items (not shown) on the Fed's balance sheet. The final row does not equal the sum of the first three rows because it includes changes in holdings between the three rounds of QE. Data on the table are based on actual data, not announced amounts at the onset of the program. The two can differ because of timing and the maturity of prior holdings, which decrease the amounts shown in the table.

This increase in the Fed's assets must be matched by a corresponding increase in the liabilities on its balance sheet.4045 The Fed's liabilities mostly take the form of currency, bank reserves, and cash deposited by the U.S. Treasury at the Fed. QE has mainly resulted in an increase in bank reserves, from about $46 billion in August 2008 to $820 billion at the end of 2008. Since October 2009, excess bank reserves have exceeded $1 trillion, and they have been between $2.5 trillion and $2.8 trillion since 2014.41peaking at $2.7 trillion in August 2014.46 The increase in bank reserves can be seen as the inevitable outcome of the increase in assets held by the Fed because the bank reserves, in effect, financed the Fed's asset purchases and loan programs. Reserves increase because when the Fed makes loans or purchases assets, it credits the proceeds to the recipients' reserve accounts at the Fed.

The intended purpose of QE was to put downward pressure on long-term interest rates. Purchasing long-term Treasury securities and MBS should directly reduce the rates on those securities, all else equal. The hope is that a reduction in those rates feeds through to private borrowing rates throughout the economy, stimulating spending on interest-sensitive consumer durables, housing, and business investment in plant and equipment. Indeed, Treasury and mortgage rates have been unusually low since the crisis compared with the past few decades, although the timing of declines in those rates does not match up closely to the timing of asset purchases. Determining whether QE reduced rates more broadly and stimulated interest-sensitive spending requires controlling for other factors, such as the weak economy, which tends to reduce both rates and interest-sensitive spending.42

The increase in the Fed's balance sheet has the potential to be inflationary because bank reserves are a component of the portion of the money supply controlled by the Fed (called the monetary base), which grew at an unprecedented pace during QE. In practice, overall measures of the money supply have not grown as quickly as the monetary base, and inflation has remained below the Fed's goal of 2% for most of the period since 2008. The growth in the monetary base has not translated into higher inflation because bank reserves have mostly remained deposited at the Fed and have not led to increased lending or asset purchases by banks.

Another concern is that by holding large amounts of MBS, the Fed is allocating credit to the housing sector, putting the rest of the economy at a disadvantage compared with that sector. Advocates of MBS purchases note that housing was the sector of the economy most in need of stabilization, given the nature of the crisis (this argument becomes less persuasive as the housing market continues to rebound); that MBS markets are more liquid than most alternatives, limiting the potential for the Fed's purchases to be disruptive; and that the Fed is legally permitted to purchase few other assets, besides Treasury securities.

The "Exit Strategy": Normalization of Monetary Policy Afterafter QE

On October 29, 2014, the Fed announced that it would stop making large-scale asset purchases at the end of the month.43 Now that QE is completed, attention has turned to the Fed's "exit strategy" from QE and zero interest rates. The Fed laid out its plans to normalize monetary policy in a statement in September 2014.44 It plans to continue implementing48 With QE ending, the Fed laid out its plans to normalize monetary policy in a statement in September 2014, also called the "exit strategy."49 In the 2014 announcement, the Fed announced it would continue to implement monetary policy by targeting the federal funds rate.4550 The basic challenge to doing so is that the Fed cannot effectively alter the federal funds rate by altering reserve levels (as it did before the crisis) because QE has flooded the market with excess bank reserves. In other words, in the presence of more than $21 trillion in bank reserves, the market-clearing federal funds rate is close to zero even if the Fed would like it to be higher.46

The most straightforward way51

One option to return to normal monetary policy would be to remove those excess reserves by shrinking the balance sheet through asset sales. The Fed does not intend to did not sell any securities during normalization, however.47 Instead, it is gradually reducing the balance sheet by ceasing to roll over securities as they mature, which began in September 2017—almost three years after QE ended. Initially, it allowed only $6 billion of Treasuries and $4 billion of MBS to run off each month, which was gradually increased to $30 billion of Treasuries and $20 billion of MBS per month, where it will remain until normalization is completed. The Fed believes that it would only cease shrinking the balance sheet or use QE again in the future if it its ability to stimulate the economy using reductions in the federal funds rate were insufficient.

The Fed intends to ultimately reduce the balance sheet until it holds "no more securities than necessary to implement monetary policy efficiently and effectively."4853 The Fed has stated that it foresees a balance sheet size that is consistent with this goal will be larger than it was before the crisis. In part, that is because other liabilities on the Fed's balance sheet are larger—there is more currency in circulation now than there was before the crisis, and the Treasury has kept larger balances on average in its account at the Fed. But the balance sheet willis also be significantly larger because the Fed decided in January 2019 to continue using its new method of targeting the federal funds rate even after normalization is completed.4954 Under the new method, the federal funds rate is not determined by supply and demand in the market for bank reserves, and the Fed would prefer to maintain abundant bank reserves so that it does not have to use open market operations to respond to changes in banks' demand for reserves. By contrast, if it wenthad gone back to the pre-crisis method of targeting the federal funds rate, only minimal excess reserve balances would be necessary (but perhaps more than before the crisis), so its balance sheet could be much smaller.

The Fed has not yet announced when the wind-down will be completed or how large the balance sheet would be upon completion, but the January 2019 FOMC minutes noted the wind-down could be completed as soon as this year.50 In that case, the balance sheet would not be much smaller than its current size of $4 trillion when normalization is completed—more than four times larger than its pre-crisis sizehave been much smaller.

The Fed ended the balance sheet wind-down in August 2019. At that point, the size of the balance sheet was about $3.8 trillion, and bank reserves were about $1.5 trillion. Going forward, the Fed will continue to allow $20 billion in MBS run off the balance sheet each month but will now replace the maturing MBS with Treasury securities instead of allowing the balance sheet to shrink by that amount. Although the Fed has stated that it intends to eventually stop holding MBS, at this rate the Fed would still have sizable MBS holdings in 2025, according to projections from the New York Fed.51

In order to raise the federal funds rate in the presence of large reserves, the Fed has raised the two market interest rates that are close substitutes—it has directly raised the rate it pays banks on reserves held at the Fed and used large-scale reverse repurchase agreements (repos) to alter repo rates.52

In 2008, Congress granted the Fed the authority to pay interest on reserves.5357 Because banks can earn interest on excess reserves by lending them in the federal funds market or by depositing them at the Fed, raising the interest rate on bank reserves should also raise the federal funds rate.5458 In this way, the Fed can lock up excess liquidity to avoid any potentially inflationary effects because reserves kept at the Fed cannot be put to use by banks to finance activity in the broader economy.5559 In practice, the interest rate that the Fed has paid banks on reserves has been slightly higher than the federal funds rate, which some have criticized as a subsidy to banks.56

Reverse repos are another tool for draining liquidity from the system and influencing short-term market rates. They drain liquidity from the financial system because cash is transferred from market participants to the Fed. As a result, interest rates in the repo market, one of the largest short-term lending markets, rise. The Fed has long conducted open market operations through the repo market, but since 2013 it has engaged in a much larger volume of reverse repos with a broader range of nonbank counterparties, including the government-sponsored enterprises (such as Fannie Mae and Freddie Mac) and certain money market funds, through a new Overnight Reverse Repurchase Operations Facility. The Fed is currently not capping the amount of overnight reverse repos offered through this facility. There has been some concern about the potential ramifications of the Fed becoming a dominant participant in this market and expanding its counterparties. For example, will counterparties only be willing to transact with the Fed in a panic, and will the Fed be exposed to counterparty risk with nonbanks that it does not regulate?57

|

How Has QE Affected the Fed's Profits and the Federal Budget Deficit? The Fed earns interest on its securities holdings, and it uses this interest to fund its operations. (It receives no appropriations from Congress.) The Fed's income exceeds its expenses, and it remits most of its net income to the Treasury, which uses it to reduce the budget deficit. Although the increases in, first, direct lending and, later, holdings of mortgage-related securities increased the potential riskiness of the Fed's balance sheet, it had the ex post facto effect of more than doubling the Fed's net income and remittances to Treasury. Remittances from net income to Treasury rose from $35 billion in 2007 to more than $75 billion annually from 2010 to 2017. However, normalization is likely to continue reducing remittances because of the smaller portfolio holdings and rising costs associated with paying higher interest on bank reserves and reverse repos, with remittances from net income falling to $62 billion in 2018. Although some analysts have raised concerns that the Fed could have negative net income in the next few years as a result of normalization, the New York Fed is not currently projecting that will occur under various interest rate and balance sheet scenarios. Instead, it projects that remittances will decline from the higher levels that have prevailed since the crisis to In November 2018, the Fed announced a "broad review of the strategy, tools, and communication practices it uses to pursue the monetary policy goals established by the Congress: maximum employment and price stability."63 The mandate itself and the Fed's 2% inflation target are not part of the review. The Fed has been holding town halls with stakeholders and a research conference as part of the review. According to Chair Powell, one purpose of the review is to evaluate whether changes are needed in how monetary policy is carried out in response to the economic changes that have occurred since the Great Recession.64 For example, inflation is less responsive to changes in unemployment, and the peak federal funds rate is much lower than in the previous nine expansions for which data are available.65 Because the Fed is much closer to the zero lower bound than in previous expansions, it has much less scope to stimulate the economy (if necessary) using reductions in the federal funds rate. So long as the 2% inflation target is maintained and the neutral rate remains low, it will be difficult to avoid the zero lower bound during periods of economic weakness based on the size of previous rate reductions in downturns. As part of the review, the FOMC has discussed "makeup" strategies as a way to potentially deliver more stimulus given the zero lower bound problem.66 Given the tendency for inflation to undershoot the 2% target during downturns, the idea behind the makeup strategy is to explicitly pledge to deliver inflation above 2% at other times, so that inflation will average 2% over the business cycle.67 A challenge to the success of makeup strategies has been the Fed's inability to get inflation to even reach the 2% target in this expansion: If it cannot even deliver 2% inflation, how will it deliver inflation above 2%? Another challenge is that makeup strategies could be hard to communicate to the public and could risk undermining the stability of the public's inflation expectations. The review is also considering whether there are other tools to provide stimulus that the Fed should use at the zero lower bound besides forward guidance and QE. For example, Vice Chair Richard Clarida noted that some other countries have targeted government bond yields to provide additional stimulus.68 |

Appendix. Regulatory Responsibilities

The Fed has distinct roles as a central bank and a regulator. Its main regulatory responsibilities are as follows:

- Bank regulation. The Fed supervises bank holding companies (BHCs) and thrift holding companies (THCs), which include all large and thousands of small depositories, for safety and soundness.

5969 The Dodd-Frank Act requires the Fed to subject BHCs with more than $50 billion in consolidated assets to enhanced prudential regulation (i.e., stricter standards than are applied to similar firms) in an effort to mitigate the systemic risk they pose.6070 The Fed is also the prudential regulator of U.S. branches of foreign banks and state banks that have elected to become members of the Federal Reserve System. Often in concert with the other banking regulators,6171 it promulgates rules and supervisory guidelines that apply to banks in areas such as capital adequacy, and examines depository firms under its supervision to ensure that those rules are being followed and those firms are conducting business prudently. The Fed's supervisory authority includes consumer protection for banks under its jurisdiction that have $10 billion or less in assets.6272

- Prudential regulation of nonbank systemically important financial institutions. The Dodd-Frank Act allows the Financial Stability Oversight Council (FSOC)

6373 to designate nonbank financial firms as systemically important (SIFIs). Designated firms are supervised by the Fed for safety and soundness. Since enactment, the number of designated firms has ranged from four, initially, to none today.6474

- Regulation of the payment system. The Fed regulates the retail and wholesale payment system for safety and soundness. It also operates parts of the payment system, such as interbank settlements and check clearing. The Dodd-Frank Act subjects payment, clearing, and settlement systems designated as systemically important by the FSOC to enhanced supervision by the Fed (along with the Securities and Exchange Commission and the Commodity Futures Trading Commission, depending on the type of system).

- Margin requirements. The Fed sets margin requirements on the purchases of certain securities, such as stocks, in certain private transactions. The purpose of margin requirements is to mandate what proportion of the purchase can be made on credit.

The Fed attempts to mitigate systemic risk and prevent financial instability through these regulatory responsibilities, as well as through its lender of last resort activities and participation on the FSOC (whose mandate is to identify risks and respond to emerging threats to financial stability). The Fed has focused more on attempting to mitigate systemic risk through its regulations since the financial crisis, and has also restructured its internal operations to facilitate a macroprudential approach to supervision and regulation.65

Author Contact Information

Acknowledgments

This report was originally authored by Gail E. Makinen, formerly of the Congressional Research Service.

Footnotes

| 1. |

For background on the makeup of the Federal Reserve, see CRS In Focus IF10054, Introduction to Financial Services: The Federal Reserve, by Marc Labonte. |

||||||||||||||

| 2. |

Section 2A of the Federal Reserve Act, 12 U.S.C. §225a. |

||||||||||||||

| 3. |

Federal Reserve, Statement on Longer-Run Goals and Monetary Policy Strategy, January 24, 2012, http://www.federalreserve.gov/monetarypolicy/files/FOMC_LongerRunGoals.pdf. |

||||||||||||||

| 4. |

Current and past monetary policy announcements can be accessed at http://www.federalreserve.gov/monetarypolicy/fomccalendars.htm. For more information on the business cycle, see CRS In Focus IF10411, Introduction to U.S. Economy: The Business Cycle and Growth, by Jeffrey M. Stupak. |

||||||||||||||

| 5. |

| ||||||||||||||

| 6. |

Federal Reserve, Principles for the Conduct of Monetary Policy, webpage, March 2018, https://www.federalreserve.gov/monetarypolicy/principles-for-the-conduct-of-monetary-policy.htm. The other two principles are that monetary policy should be well understood and systematic and that interest rates should respond with a more than one-for-one change to a change in inflation. |

||||||||||||||

| 7. |

For more information, see CRS Report R44663, Unemployment and Inflation: Implications for Policymaking, by Jeffrey M. Stupak. |

||||||||||||||

| 8. |

Federal Reserve, press release, January 30, 2019, https://www.federalreserve.gov/monetarypolicy/files/monetary20190130a1.pdf. |

||||||||||||||

| 9. |

See, for example, John Taylor, "A Monetary Policy for the Future," speech at the International Monetary Fund, April 15, 2015, http://web.stanford.edu/~johntayl/2015_pdfs/A_Monetary_Policy_For_the_Future-4-15-15.pdf. |

||||||||||||||

| 10. |

Janet Yellen, "The Federal Reserve's Monetary Policy Toolkit," speech at Jackson Hole, Wyoming, August 26, 2016, at https://www.federalreserve.gov/newsevents/speech/yellen20160826a.htm. |

||||||||||||||

| 6.

|

|

For more information, see CRS Report R44663, Unemployment and Inflation: Implications for Policymaking, by Jeffrey M. Stupak. 7.

|

|

See CRS Insight IN10971, Escalating U.S. Tariffs: Affected Trade, coordinated by Brock R. Williams. 8.

|

|

See CRS Insight IN11098, The Yield Curve and Predicting Recessions, by Mark P. Keightley and Marc Labonte. 9.

|

|

Federal Reserve, "Transcript of Chairman Powell's Press Conference," July 31, 2019, https://www.federalreserve.gov/mediacenter/files/FOMCpresconf20190731.pdf. 10.

|

|

Janet Yellen, "The Federal Reserve's Monetary Policy Toolkit," speech at Jackson Hole, WY, August 26, 2016, https://www.federalreserve.gov/newsevents/speech/yellen20160826a.htm. 11.

|

|

Nick Timiraos, "Powell Says Fed Won't Bend to Political Pressure," Wall Street Journal, June 25, 2019, https://www.wsj.com/articles/feds-powell-trade-uncertainty-global-growth-worries-could-prompt-rate-cuts-11561481986. 12.

|

|

See, for example, John Taylor, "A Monetary Policy for the Future," speech at the International Monetary Fund, April 15, 2015, http://web.stanford.edu/~johntayl/2015_pdfs/A_Monetary_Policy_For_the_Future-4-15-15.pdf. |

Of the monetary policy tools described below, the board is generally responsible for setting reserve requirements and interest rates paid by the Fed, whereas the federal funds target is set by the FOMC. The discount rate is set by the 12 Federal Reserve banks, subject to the board's approval. In practice, the board and FOMC coordinate the use of these tools to implement a consistent monetary policy stance. The New York Fed determines what open market operations are necessary on an ongoing basis to maintain the federal funds target. |

|

Depository institutions are obligated by law to hold some fraction of their deposit liabilities as reserves. They are also likely to hold additional or excess reserves based on certain risk assessments they make about their portfolios and liabilities. |

|||||||||||||||

|

See, for example, Anthony M. Santomero, "Great Expectations: The Role of Beliefs in Economics and Monetary Policy," Business Review, Federal Reserve Bank of Philadelphia, Second Quarter 2004, pp. 1-6, and Gordon H. Sellon, Jr., "Expectations and the Monetary Policy Transmission Mechanism," Economic Review, Federal Reserve Bank of Kansas City, Fourth Quarter 2004, pp. 4-42. |

|||||||||||||||

|

The Fed is legally forbidden from buying securities directly from the Department of the Treasury. Instead, it buys them on secondary markets from primary dealers. For a technical explanation of how open market operations are conducted, see Cheryl L. Edwards, "Open Market Operations in the 1990s," Federal Reserve Bulletin, November 1997, pp. 859-872; Benjamin Friedman and Kenneth Kuttner, "Implementation of Monetary Policy: How Do Central Banks Set Interest Rates?," National Bureau of Economic Research, Working Paper no. 16165, March 2011. |

|||||||||||||||

|

In addition to open market operations, the Fed has entered into reverse repos since 2013 through a newly created facility, the Overnight Reverse Repurchase Operations Facility. See the section below entitled "The "Exit Strategy": Normalization of Monetary Policy |

|||||||||||||||

|

All depository institutions, as defined by 12 U.S.C. §461, may borrow from the discount window and are subject to reserve requirements regardless of whether they are members of the Federal Reserve. |

|||||||||||||||

|

Until 2003, the discount rate was set slightly below the federal funds target, and the Fed used moral suasion to discourage healthy banks from profiting from this low rate. To reduce the need for moral suasion, lending rules were altered in early 2003. Since that time, the discount rate has been set at a penalty rate above the federal funds rate target. However, during the financial crisis, the Fed encouraged banks to use the discount window. |

|||||||||||||||

|

Checking accounts are subject to reserve requirements, but savings accounts are not. As a result, the Fed defines by regulation the different characteristics that checking and savings accounts may have. For example, savings accounts are subject to a limit on monthly withdrawals. |

|||||||||||||||

|

The deposit threshold is regularly adjusted for inflation. For current reserve requirements, see http://www.federalreserve.gov/monetarypolicy/reservereq.htm. |

|||||||||||||||

|

During the financial crisis, the historical relationship between money growth and inflation did not hold, as will be discussed below in the section entitled "Quantitative Easing and the Growth in the Fed's Balance Sheet and Bank Reserves." |

|||||||||||||||

|

Two interesting papers bearing on what monetary policy can accomplish by two former officials of the Federal Reserve are Anthony M. Santomero, "What Monetary Policy Can and Cannot Do," Business Review, Federal Reserve Bank of Philadelphia, First Quarter 2002, pp. 1-4, and Frederic S. Mishkin, "What Should Central Banks Do?," Review, Federal Reserve Bank of St. Louis, November/December 2000, pp. 1-14. |

|||||||||||||||

|

The Fed earns interest on its securities holdings, and it uses this interest to fund its operations. It sets its own budget and is not subject to the appropriations process. |

|||||||||||||||

|

For more information, see CRS Report R43391, Independence of Federal Financial Regulators: Structure, Funding, and Other Issues, by Henry B. Hogue, Marc Labonte, and Baird Webel. |

|||||||||||||||

|

Christopher Condon, "A Timeline of Trump's Quotes on Powell and the Fed," Bloomberg, December 17, 2018. |

|||||||||||||||

|

Note that this prediction has not always held over time—at times, some Members of Congress have criticized the Fed for keeping interest rates too low. |

|||||||||||||||

|

See CRS Report RL31056, Economics of Federal Reserve Independence, by Marc Labonte. |

|||||||||||||||

|

|