The Yield Curve and Predicting Recessions

Economists and financial markets closely monitor interest rates in hopes of gleaning information about the path of the economy. One measure of particular interest is the "yield curve." Recently, the yield curve associated with U.S. Treasuries has been inverted. This Insight discusses possible explanations for the inversion, including whether the inversion is signaling that the economy will enter a recession.

What Is the Yield Curve?

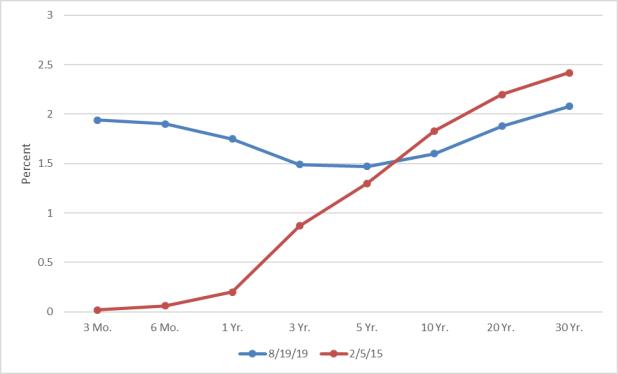

A yield curve plots the interest rates on various short-, medium-, and long-term bonds by the same issuer. Normally, short-term interest rates are lower than longer-term interest rates for a variety of reasons, producing an upward-sloping yield curve. For example, Figure 1 shows the Treasury bond yield curve on February 5, 2015. As the maturity date lengthens, the yield is higher at each point on the curve.

What Is a Yield Curve Inversion?

Occasionally, short-term interest rates are higher than longer-term rates, creating an inverted yield curve. Since March, the yield curve associated with U.S. Treasuries has shown signs of inversion. On August 19, 2019, the yields on 3-, 5-, and 10-year Treasuries were below the yields on Treasuries with a maturity of a year or less (see Figure 1). The yield on 20-year Treasuries were also lower than the yields on 3- or 6-month Treasuries. The yields on 30-year Treasuries was higher than the yield on 3-month Treasuries, but the spread between the two has been narrowing, suggesting that the portions of the yield that have not inverted have flattened. As the figure illustrates, the yield curve inversion has occurred because short-term rates have risen and long-term rates have declined.

|

|

Source: U.S. Treasury. |

Does a Yield Curve Inversion Predict a Recession?

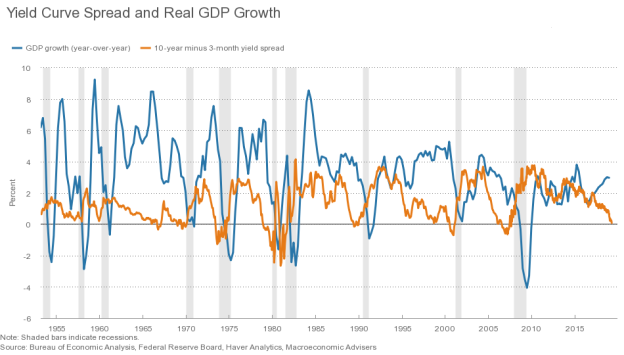

Historically, an inverted yield curve has tended to precede recessions, and therefore, investors believe that the current inverted Treasury yield curve could foreshadow the next recession. A common gauge of an inverted yield curve is when the difference between the yields on 10-year and 3-month Treasuries is negative. By this measure, the yield curve has inverted before each of the last seven recessions, which are marked by gray bars in Figure 2.

However, three other features of this data illustrate that the yield curve's predictive power should not be overstated. First, there can be a considerable lag between when the yield curve inverts and when the economy enters into a recession. Second, this time lag varies. And third, sometimes the yield curve has inverted without a subsequent recession. Together, these three observations imply that an inverted yield curve does not guarantee that a recession will occur or—if a recession is going to occur—that it is necessarily imminent. Studies have found that the yield curve inversion has some predictive power but is not as accurate as other measures at predicting recessions.

|

Figure 2. Yield Curve Spread and Real GDP Growth 1953-2019 |

|

An inverted yield curve can be a signal of an upcoming recession if it reflects investors' pessimism over the path of future interest rates and the economy. The Federal Reserve (Fed) controls the federal funds rates, giving it significant influence over short-term interest rates. The Fed typically raises the federal funds rates before a recession, when the expansion is peaking, and reduces the federal funds rates during a recession. When investors become nervous about the outlook of the economy, they begin to expect that the Fed will lower short-term rates in the future and thus will move into longer-term bonds, pushing down longer-term rates. (Yields fall when bond prices rise.) The flattening of the yield curve since November 2018 has been driven by the 1.5 percentage point decline in the 10-year yield over that period. The recent inversion could be capturing investors' belief that the Fed will continue to reduce short-term rates, which it cut for the first time in over a decade in July.

An inversion could also signal the effect future tightening credit conditions may have on economic activity. Banks earn profits by borrowing short-term funds at a low rate and making longer-term loans at a higher rate. When the yield curve inverts, or starts to flatten, it squeezes bank profits as banks' cost to borrow funds begins to rise, while the revenue they earn from loans begins to fall. This can lead banks to cut back on lending, causing consumers to curtail spending and businesses to reduce investment.

There are also a number of reasons why an inverted yield curve may not be indicative of an oncoming recession. Investors could be incorrect in their belief that future interest rates will fall. Many forecasters are predicting that the economy will slow, putting downward pressure on long-term rates, without the economy entering a recession. U.S. interest rates may currently be influenced by low global rates, reflecting foreign economic issues. The risks associated with holding long-term bonds may have fallen for reasons other than expectations that future short-term rates will fall. For example, investors may expect future inflation to be lower and more stable.

Additionally, if Treasury securities of different maturities are not perfect substitutes, an increase in demand for long-term Treasuries could flatten the yield curve independent of changes in the economic outlook. For example, a desire for safe, liquid assets among foreign governments and financial institutions that want to match the duration of their long-term liabilities could be driving the demand for long-term Treasuries. The Fed also recently stopped reducing the amount of Treasury securities it holds on its balance sheet, leaving its holdings at a permanently higher level than investors may have originally anticipated, thereby reducing the available supply on the market in the future—though large projected federal budget deficits ensure that the overall supply of Treasury securities will continue rising under current policy.