Unemployment and Inflation: Implications for Policymaking

The unemployment rate is a vital measure of economic performance. A falling unemployment rate generally occurs alongside rising gross domestic product (GDP), higher wages, and higher industrial production. The government can generally achieve a lower unemployment rate using expansionary fiscal or monetary policy, so it might be assumed that policymakers would consistently target a lower unemployment rate using these policies. Part of the reason policymakers do not revolves around the relationship between the unemployment rate and the inflation rate.

In general, economists have found that when the unemployment rate drops below a certain level, referred to as the natural rate, the inflation rate will tend to increase and continue to rise until the unemployment rate returns to its natural rate. Alternatively, when the unemployment rate rises above the natural rate, the inflation rate will tend to decelerate. The natural rate of unemployment is the level of unemployment consistent with sustainable economic growth. An unemployment rate below the natural rate suggests that the economy is growing faster than its maximum sustainable rate, which places upward pressure on wages and prices in general leading to increased inflation. The opposite is true if the unemployment rate rises above the natural rate, downward pressure is placed on wages and prices in general leading to decreased inflation. Wages make up a significant portion of the costs of goods and services, therefore upward or downward pressure on wages pushes average prices in the same direction.

Two other sources of variation in the rate of inflation are inflation expectations and unexpected changes in the supply of goods and services. Inflation expectations play a significant role in the actual level of inflation, because individuals incorporate their inflation expectations when making price-setting decisions or when bargaining for wages. A change in the availability of goods and services used as inputs in the production process (e.g., oil) generally impacts the final price of goods and services in the economy, and therefore changing the rate of inflation.

The natural rate of unemployment is not immutable and fluctuates alongside changes within the economy. For example, the natural rate of unemployment is affected by

changes in the demographics, educational attainment, and work experience of the labor force;

institutions (e.g., apprenticeship programs) and public policies (e.g., unemployment insurance);

changes in productivity growth; and

contemporaneous and previous level of long-term unemployment.

Following the 2007-2009 recession, the actual unemployment rate remained significantly elevated compared with estimates of the natural rate of unemployment for multiple years. However, the average inflation rate decreased by less than one percentage point during this period despite predictions of negative inflation rates based on the natural rate model. Likewise, inflation has recently shown no sign of accelerating as unemployment has approached the natural rate. Some economists have used this as evidence to abandon the concept of a natural rate of unemployment in favor of other alternative indicators to explain fluctuations in inflation.

Some researchers have largely upheld the natural rate model while looking at broader changes in the economy and the specific consequences of the 2007-2009 recession to explain the modest decrease in inflation after the recession. One potential explanation involves the limited supply of financing available to businesses after the breakdown of the financial sector. Another explanation cites changes in how inflation expectations are formed following changes in how the Federal Reserve responds to economic shocks and the establishment of an unofficial inflation target. Others researchers have cited the unprecedented increase in long-term unemployment that followed the recession, which significantly decreased bargaining power among workers.

Unemployment and Inflation: Implications for Policymaking

Jump to Main Text of Report

Contents

- The Phillips Curve

- Rebuttal to the Phillips Curve

- The Natural Rate Model and Inflation

- How the Output Gap Impacts the Rate of Inflation

- Time Varying Natural Rate of Unemployment

- How Has the Natural Rate Shifted Over Time?

- Other Factors Impacting Inflation

- Missing Deflation Post 2007-2009 Recession

- Globalization and the Global Output Gap

- Financial Frictions in the Wake of Crisis

- Increased Inflation Anchoring

- Long-Term Versus Short-Term Unemployment and Inflation

- Alternative Measures of Economic Slack

- Concluding Thoughts on Missing Deflation

- Policy Implications of the Natural Rate Model

- Limitations to Fiscal and Monetary Policies

- Inflation's Impact on Economic Growth

- A Weakened Relationship Between Inflation and Unemployment?

- Changing the Natural Rate of Unemployment

Figures

Summary

The unemployment rate is a vital measure of economic performance. A falling unemployment rate generally occurs alongside rising gross domestic product (GDP), higher wages, and higher industrial production. The government can generally achieve a lower unemployment rate using expansionary fiscal or monetary policy, so it might be assumed that policymakers would consistently target a lower unemployment rate using these policies. Part of the reason policymakers do not revolves around the relationship between the unemployment rate and the inflation rate.

In general, economists have found that when the unemployment rate drops below a certain level, referred to as the natural rate, the inflation rate will tend to increase and continue to rise until the unemployment rate returns to its natural rate. Alternatively, when the unemployment rate rises above the natural rate, the inflation rate will tend to decelerate. The natural rate of unemployment is the level of unemployment consistent with sustainable economic growth. An unemployment rate below the natural rate suggests that the economy is growing faster than its maximum sustainable rate, which places upward pressure on wages and prices in general leading to increased inflation. The opposite is true if the unemployment rate rises above the natural rate, downward pressure is placed on wages and prices in general leading to decreased inflation. Wages make up a significant portion of the costs of goods and services, therefore upward or downward pressure on wages pushes average prices in the same direction.

Two other sources of variation in the rate of inflation are inflation expectations and unexpected changes in the supply of goods and services. Inflation expectations play a significant role in the actual level of inflation, because individuals incorporate their inflation expectations when making price-setting decisions or when bargaining for wages. A change in the availability of goods and services used as inputs in the production process (e.g., oil) generally impacts the final price of goods and services in the economy, and therefore changing the rate of inflation.

The natural rate of unemployment is not immutable and fluctuates alongside changes within the economy. For example, the natural rate of unemployment is affected by

- changes in the demographics, educational attainment, and work experience of the labor force;

- institutions (e.g., apprenticeship programs) and public policies (e.g., unemployment insurance);

- changes in productivity growth; and

- contemporaneous and previous level of long-term unemployment.

Following the 2007-2009 recession, the actual unemployment rate remained significantly elevated compared with estimates of the natural rate of unemployment for multiple years. However, the average inflation rate decreased by less than one percentage point during this period despite predictions of negative inflation rates based on the natural rate model. Likewise, inflation has recently shown no sign of accelerating as unemployment has approached the natural rate. Some economists have used this as evidence to abandon the concept of a natural rate of unemployment in favor of other alternative indicators to explain fluctuations in inflation.

Some researchers have largely upheld the natural rate model while looking at broader changes in the economy and the specific consequences of the 2007-2009 recession to explain the modest decrease in inflation after the recession. One potential explanation involves the limited supply of financing available to businesses after the breakdown of the financial sector. Another explanation cites changes in how inflation expectations are formed following changes in how the Federal Reserve responds to economic shocks and the establishment of an unofficial inflation target. Others researchers have cited the unprecedented increase in long-term unemployment that followed the recession, which significantly decreased bargaining power among workers.

The official unemployment rate has been in decline over the past several years, peaking at 10% shortly after the 2007-2009 recession before falling to 5% in January 2016. A falling unemployment rate is generally a cause for celebration as more individuals are able to find jobs; however, the current low unemployment rate has been increasingly cited as a reason to begin rolling back expansionary monetary and fiscal policy. After citing "considerable improvement in labor market conditions," in December 2015 for the first time in seven years, the Federal Reserve increased its federal funds target rate, reducing the expansionary power of its monetary policy.1

Labor market conditions have certainly improved since the depths of the financial crisis and 2007-2009 recession, but an unemployment rate of around 5% means that nearly 8 million people are still searching for jobs and are unable to find them. So why is the Federal Reserve reducing the amount of stimulus entering the economy when so many people are still looking for work? The answer involves the relationship between the two parts of the Federal Reserve's dual mandate—maximum employment and stable prices.

In general, economists have observed an inverse relationship between the unemployment rate and the inflation rate, i.e., the rate at which prices rise. This trade-off between unemployment and inflation become particularly pronounced (i.e., small changes in unemployment result in relatively large price swings) when the unemployment rate drops below a certain level, referred to by economists as the "natural unemployment rate." Alternatively, when the unemployment rate rises above the natural rate, inflation will tend to decelerate. In response to the financial crisis and subsequent recession, the Federal Reserve began employing expansionary monetary policy to spur economic growth and improve labor market conditions. Recently, the unemployment rate has fallen to a level consistent with many estimates of the natural rate of unemployment, between 4.6% and 5.0%.2 If the unemployment rate were to continue falling, it would likely fall below the natural rate of unemployment and cause accelerating inflation, violating the Federal Reserve's mandate of stable prices.

This report discusses the relationship between unemployment and inflation, the general economic theory surrounding this topic, the relationship since the financial crisis, and its use in policymaking.

The Phillips Curve

A relationship between the unemployment rate and prices was first prominently established in the late 1950s. This early research focused on the relationship between the unemployment rate and the rate of wage inflation.3 Economist A. W. Phillips found that between 1861 and 1957, there was a negative relationship between the unemployment rate and the rate of change in wages in the United Kingdom, showing wages tended to grow faster when the unemployment rate was lower, and vice versa. 4 His work was then replicated using U.S. data between 1934 and 1958, discovering a similar negative relationship between unemployment and wage growth.5

Economists reasoned that this relationship existed due to simple supply and demand within the labor market. As the unemployment rate decreases, the supply of unemployed workers decreases, thus employers must offer higher wages to attract additional employees from other firms. This body of research was expanded, shifting the focus from wage growth to changes in the price level more generally.6 The negative relationship between unemployment and inflation was dubbed the Phillips curve, due to Phillips's seminal work on the issue.

|

What is Inflation? Inflation is a general increase in the price of goods and services across the economy, or a general decrease in the value of money. Conversely, deflation is a general decrease in the price of goods and services across the economy, or a general increase in the value of money. The inflation rate is determined by observing the price of a consistent set of goods and services over time. In general, the two alternative measures of inflation are headline inflation and core inflation. Headline inflation measures the change in prices across a very broad set of goods and services, and core inflation excludes food and energy from the set of goods and services measured. Core inflation is often used in place of headline inflation due to the volatile nature of the price of food and energy, which are particularly susceptible to supply shocks. |

Many interpreted the early research around the Phillips curve to mean that a stable relationship existed between unemployment and inflation. This suggested that policymakers could choose among a schedule of unemployment and inflation rates; in other words, policymakers could achieve and maintain a lower unemployment rate if they were willing to accept a higher inflation rate and vice versa. This rationale was prominent in the 1960s, and both the Kennedy and Johnson Administrations considered this framework when designing economic policy.7

Rebuttal to the Phillips Curve

During the 1960s, economists began challenging the Phillips curve concept, suggesting that the model was too simplistic and the relationship would break down in the presence of persistent positive inflation. These critics claimed that the static relationship between the unemployment rate and inflation could only persist if individuals never adjusted their expectations around inflation, which would be at odds with the fundamental economic principle that individuals act rationally. But, if individuals adjusted their expectations around inflation, any effort to maintain an unemployment rate below the natural rate of unemployment would result in continually rising inflation, rather than a one-time increase in the inflation rate. This rebuttal to the original Phillips curve model is now commonly known as the natural rate model. 8

The natural rate model suggests that there is a certain level of unemployment that is consistent with a stable inflation rate, known as the natural rate of unemployment. The natural rate of unemployment is often referred to as the non-accelerating inflation rate of unemployment (NAIRU). When the unemployment rate falls below the natural rate of unemployment, referred to as a negative unemployment gap, the inflation rate is expected to accelerate. When the unemployment rate exceeds the natural rate of unemployment, referred to as a positive unemployment gap, inflation is expected to decelerate. The natural rate model gained support as 1970s' events showed that the stable tradeoff between unemployment and inflation as suggested by the Phillips curve appeared to break down. A series of negative oil supply shocks in the 1970s resulted in high unemployment and high inflation, known as stagflation, with core inflation and the unemployment rate both rising above 9% in 1975.

|

Unemployment Rate Versus NAIRU The official unemployment rate is released by the Bureau of Labor Statistics (BLS) based on a survey of individuals in the United States. For more information on how the unemployment rate is calculated, refer to CRS In Focus IF10443, Introduction to U.S. Economy: Unemployment, by Jeffrey M. Stupak. The NAIRU, however, is an estimated figure produced by various groups; henceforth, this report uses the estimated NAIRU from the Congressional Budget Office (CBO). The CBO estimates the NAIRU based on the characteristics of jobs and workers in the economy, and the efficiency of the labor market's matching process.9 |

The Natural Rate Model and Inflation

The economy's ability to produce goods and services, or potential output, is dependent on three main factors in the long run: (1) the amount of capital (machines, factories, etc.), (2) the number and quality of workers, and (3) the level of technology.10 Although these factors largely govern the economy's potential output, the economy's actual output is largely governed by demand for goods and services, which can rise above or below potential output. The economy is most stable when actual output equals potential output; the economy is said to be in equilibrium because the demand for goods and services is matched by the economy's ability to supply those goods and services. In other words, certain characteristics and features of the economy (capital, labor, and technology) determine how much the economy can sustainably produce at a given time, but demand for goods and services is what actually determines how much is produced in the economy.

As actual output diverges from potential output, inflation will tend to become less stable. All else equal, when actual output exceeds the economy's potential output, a positive output gap is created, and inflation will tend to accelerate. When actual output is below potential output, a negative output gap is generated, and inflation will tend to decelerate. Within the natural rate model, the natural rate of unemployment is the level of unemployment consistent with actual output equaling potential output, and therefore stable inflation.

How the Output Gap Impacts the Rate of Inflation

During an economic expansion, total demand for goods and services within the economy can grow to exceed the economy's potential output, and a positive output gap is created. As demand grows, firms rush to increase their output to meet this new demand. In the short term though, firms have limited options to increase their output. It often takes too long to build a new factory, or order and install additional machinery, so instead firms hire additional employees. As the number of available workers decreases, workers can bargain for higher wages, and firms are willing to pay higher wages to capitalize on the increased demand for their goods and services. However, as wages increase, upward pressure is placed on the price of all goods and services because labor costs make up a large portion of the total cost of goods and services. Over time, the average price of goods and services rises to reflect the increased cost of wages.

The opposite tends to occur when actual output within the economy is lower than the economy's potential output, and a negative output gap is created. During an economic downturn, total demand within the economy shrinks. In response to decreased demand, firms reduce hiring, or lay off employees, and the unemployment rate rises. As the unemployment rate rises, workers have less bargaining power when seeking higher wages because they become easier to replace. Firms can hold off on increasing prices as the cost of one of their major inputs—wages—becomes less expensive. This results in a decrease in the rate of inflation.

Time Varying Natural Rate of Unemployment

The natural rate of unemployment is not constant. As discussed earlier, the natural rate of unemployment is the rate that is consistent with sustainable economic growth, or when actual output is equal to potential output. It is therefore expected that changes within the economy can change the natural unemployment rate.11

Four main features of the economy affect the natural unemployment rate:

- 1. Labor market composition,

- 2. Labor market institutions and public policy,

- 3. Productivity growth, and

- 4. Long-term—that is, longer than 26 weeks—unemployment rates.12

As the characteristics of the labor force change—for example, with respect to age, educational attainment, and work experience—and alter the productive capacity of the economy, the natural rate is also expected to shift. Individual worker's characteristics affect the likelihood that a worker will become unemployed and the speed (or ease) at which he or she can find work. For example, younger workers tend to have less experience and therefore have higher levels of unemployment on average. Consequently, if young workers form a significant portion of the labor force, the natural rate of unemployment will be higher. Alternatively, individuals with higher levels of educational attainment generally find it easier to find work; therefore, as the average level of educational attainment of workers rises, the natural rate of unemployment will tend to decrease.13

Labor market institutions and public policies in place within an economy can also impact the natural rate of unemployment by improving individuals' ability to find and obtain work. For example, apprenticeship programs provide individuals additional work experience and help them find work faster, which can decrease the natural rate of unemployment. Alternatively, ample unemployment insurance benefits may increase the natural rate of unemployment, as unemployed individuals will spend longer periods looking for work.14

The rate of productivity growth also impacts the natural unemployment rate. According to economic theory, employee compensation can grow at the same speed as productivity without increasing inflation. Individuals become accustomed to compensation growth at this speed and come to expect similar increases in their compensation year over year based on the previous growth in productivity. A decrease in the rate of productivity growth would eventually result in a decrease in the growth of compensation; however, workers are likely to resist this decrease in the pace of wage growth and bargain for compensation growth above the growth rate of productivity. This above average compensation growth will erode firms' profits and they will begin to lay off employees to cut down on costs, leading to a higher natural rate of unemployment. The opposite occurs with an increase in productivity growth, businesses are able to increase their profits and hire additional workers simultaneously, resulting in a lower natural rate of unemployment.15

Lastly, the contemporaneous and previous level of long-term unemployment in an economy can shift the natural rate of unemployment. Individuals who are unemployed for longer periods of time tend to forget certain skills and become less productive, and are therefore less attractive to employers. In addition, some employers may interpret long breaks from employment as a signal of low labor market commitment or worker quality, further reducing job offers to this group. As the proportion of long-term unemployed individuals increases, the natural rate of unemployment will also increase.16

How Has the Natural Rate Shifted Over Time?

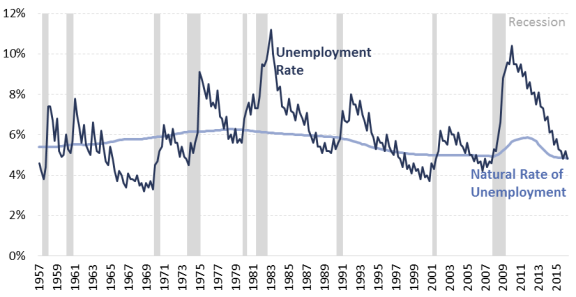

Understanding the relationship between the current unemployment rate and the natural rate is important when designing economic policy, and the fact that the natural rate can shift over time further complicates the design of economic policy. As shown in Figure 1, the estimated natural rate of unemployment has been relatively stable over time, shifting from a high of 6.3% in the late 1970s to about 4.8% in 2016, a spread of only 1.5 percentage points.17 The major inflection points seen in the natural rate over time are largely the result of changes in the makeup of the labor force and changes in productivity growth over time.

As shown in Figure 1, the estimated natural rate slowly increased in the late 1950s, 1960s and the early 1970s. Several economists have suggested that much of this increase in the natural rate, from about 5.4% to close to 6.3%, was due to the large number of inexperienced workers entering the labor force as members of the baby-boomer generation began looking for their first jobs.18

The natural rate began to decrease in the 1980s, with a period of relatively rapid decline in the early 1990s (see Figure 1). A portion of this decrease in the 1980s is likely due to baby boomers becoming more experienced and productive workers. The sharp decrease in the 1990s has been largely explained by an increase in the rate of productivity growth in the economy. Productivity growth, total output per hour of labor, was about 1.5% between 1975 and 1989, but rose to about 2.2% between 1990 and 2000 largely due to the rise of computers and the Internet.19

Beginning in 2008, the natural rate began to increase sharply, as shown in Figure 1. The rapid increase in the natural rate after 2007 can largely be explained by changes in the makeup of the labor force and changes in government policy.20 As shown in Figure 4, the number of individuals who were unemployed for more than 26 weeks increased dramatically after the 2007-2009 recession. Individuals who are unemployed for longer durations tend to have more difficulty finding new jobs, and after the recession, the long-term unemployed made up a significant portion of the labor force, which increased the natural rate of unemployment. In addition, some research has suggested the extension of unemployment benefits may also increase the natural rate of unemployment.21 Additionally, some portion of the increase in the natural unemployment rate may be due to the decrease in productivity, as productivity growth fell to 0.7% between the third quarter of 2009 and the second quarter of 2016.22

Other Factors Impacting Inflation

The rate of inflation is not determined exclusively by the unemployment gap. Two prominent factors that also impact the rate of inflation are (1) expected inflation and (2) supply shocks.23 Individuals and businesses form expectations about the expected rate of inflation in the future, and make economic choices based on these expectations. For example, if individuals expect 2% inflation over the next year, they will seek a 2% increase in their nominal salary to preserve their real purchasing power. Firms will also incorporate inflation expectations when setting prices to keep the real price of their goods constant. An increase in the expected rate of inflation will be translated into an actual increase in the rate of inflation as wages and prices are set by individuals within the economy.24

Economic events that impact the supply of goods or services within the economy, known as supply shocks, can also impact the rate of inflation. The classic example of a supply shock is a reduction in the supply of available oil. As the supply of oil decreases, the price of oil, and any good that uses oil in its production process, increases. This leads to a spike in the overall price level in the economy, namely, inflation. Policymakers generally focus on negative supply shocks, which reduce the supply of a good or service, but positive supply shocks, which increase the supply of a good or service, can also occur. Positive supply shocks generally reduce inflation.

Missing Deflation Post 2007-2009 Recession

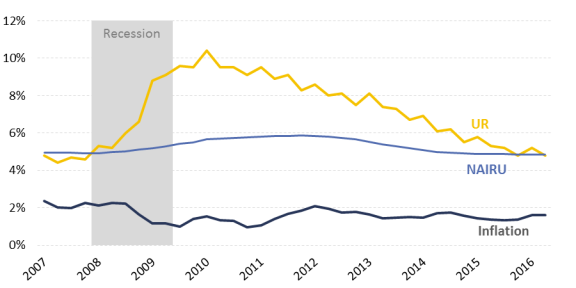

Events following the 2007-2009 recession have again called into question how well economists understand the relationship between the unemployment gap and inflation. As a result of the global financial crisis and the U.S. 2007-2009 recession, the unemployment rate rose above 10% and remained significantly elevated compared with estimates of the natural rate of unemployment for multiple years, as shown in Figure 1. The natural rate model suggests that this significant and prolonged unemployment gap should have resulted in decelerating inflation during that period. Actual inflation did decline modestly during that period, decreasing from an average rate of about 2% between 2003 and 2007 to about 1.4% on average between 2008 and mid-2015.25 However, based on previous experience with unemployment gaps of this size and inflation forecasts based on the natural rate model, many economists anticipated a more drastic decrease in the inflation rate, with some predicting negative inflation (or deflation) rates reaching 4% during that period.26 The movements of the unemployment rate and inflation rate after the financial crisis are displayed in Figure 2.

|

|

Source: BLS, CBO. Note: Inflation as measured by core PCE. Unemployment rate is not seasonally adjusted. |

Numerous competing hypotheses exist for why a significant decrease in the inflation rate failed to materialize. The following sections describe the prominent hypotheses and discuss the available evidence for these hypotheses.

Globalization and the Global Output Gap

Over the previous several decades, the U.S. economy has become more integrated with the global economy as trade has become a larger portion of economic activity. Economists have suggested that as economies increase their openness to the global economy, global economic forces will begin to play a larger role in domestic inflation dynamics. This suggests that inflation may be determined by labor market slack and the output gap (the difference between actual output and potential output) on a global level rather than a domestic level. Since the 1980s, trade (as measured by the sum of imports and exports) has expanded significantly in the United States, increasing from less than 20% of GDP to more than 30% of GDP between 2011 and 2013.

According to the International Monetary Fund, the average output gap following the 2007-2009 recession among all advanced economies was smaller than the output gap in the United States, as shown in Table 1. In 2009, the actual output among all advanced economies was about 4% below potential output, whereas the actual output in the United States was about 5% below potential output. If increased trade openness has subdued the impact of the domestic output gap on inflation in favor of the global output gap, the smaller output gap among other advanced economies may help to explain the unexpectedly modest decrease in inflation after the 2007-2009 recession.

Table 1. U.S. Output Gap and Average Output Gap Among Advanced Economies

(output gap, percentage of potential GDP)

|

2007 |

2008 |

2009 |

2010 |

2011 |

2012 |

2013 |

2014 |

2015 |

|

|

Advanced Economies (Average) |

2.494 |

0.798 |

-3.992 |

-2.313 |

-1.854 |

-1.983 |

-2.17 |

-1.844 |

-1.507 |

|

United States |

2.189 |

-0.339 |

-4.963 |

-3.733 |

-3.413 |

-2.74 |

-2.883 |

-2.224 |

-1.623 |

Source: International Monetary Fund, World Economic Outlook Database, April 2016.

The empirical evidence surrounding the growing impact of the global output gap on domestic inflation, which focused on the time period before the 2007-2009, is mixed. A number of researchers have found that the global output gap has some impact on domestic inflation dynamics;27 however, others have found no relationship between the global output gap and domestic inflation.28

Researchers who contend that the global output gap is influential with respect to domestic inflation have then attempted to determine if the strength of this influence has grown alongside increases in trade openness. When the global output gap influences domestic inflation, however, the strength of this impact seems to be unrelated to changes in trade openness.29 Based on this evidence, it appears unlikely that changes in trade openness over recent decades and the smaller output gap abroad resulted in the unexpectedly modest decrease in inflation after the 2007-2009 recession.

Financial Frictions in the Wake of Crisis

Alternative explanations for the lack of deflation after the 2007-2009 recession cite the global financial crisis and decreased access to external financing for businesses. Typically, during a recession, as demand for goods and services decreases, the price of those goods and services also tends to decrease. However, some economists have argued that the financial crisis decreased the supply of external financing (i.e., equity issues, bank loans) available for businesses, which increased borrowing costs. In the face of increased borrowing costs, some businesses, especially liquidity constrained businesses with so-called sticky customer bases,30 would have opted to raise prices to remain solvent until the costs of borrowing decreased as the financial sector recovered. Limited empirical work has found evidence of this behavior by businesses during the 2007-2009 recession, and therefore may help to explain the unexpectedly modest decrease in inflation following the recession.31

Increased Inflation Anchoring

Changes in how individuals form inflation expectations, as a result of broad changes in how the Federal Reserve conducts monetary policy, may also help to explain the unexpectedly moderate decrease in the rate of inflation after the 2007-2009 recession.

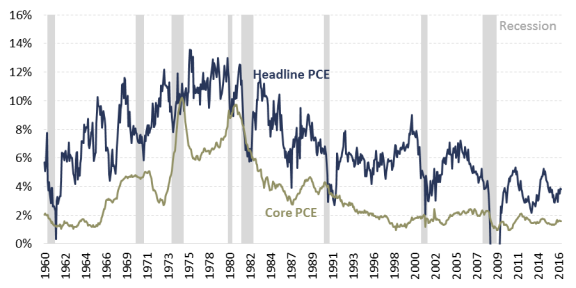

After the high inflation of the late 1970s and 1980s, the Federal Reserve became more concerned with maintaining a stable rate of inflation in the face of economic shocks.32 Previously, the Federal Reserve accommodated changes in inflation that resulted from economic shocks. Under the previous policy regime, an economic shock that raised inflation would also increase inflation expectations, which would further increase inflation. As seen in Figure 3, before the 1980s, the fluctuations in inflation were more volatile, with a spread of multiple percentage points from year to year. However, under the new policy regime, economic actors were less likely to shift inflation expectations as a result of an economic shock because they believed the Federal Reserve would stabilize any changes in inflation due to economic shocks.33 This change in how economic actors formed inflation expectations is thought to have reduced the volatility of changes in the rate of inflation during economic shocks. The decreased volatility can be seen in Figure 3 as the spread seen in core inflation decreases significantly after the early 1980s.

|

|

Source: Bureau of Economic Analysis (BEA). Notes: A 12-month percentage change as measured by Personal Consumption Expenditures (PEC) Index. Core inflation excludes energy and food prices from the measure of inflation. |

Beginning in the 1990s, the Federal Reserve appeared to make another change in how it was conducting monetary policy. Not only was the Federal Reserve working to stabilize changes in inflation that resulted from economic shocks, but it appeared to be targeting a specific inflation rate of 2.5% core inflation per year.34 Economists suggested that if the Federal Reserve maintained a consistent inflation target over time then economic actors' inflation expectations would become anchored at the Federal Reserve's target inflation rate. A number of researchers have found that inflation expectations have indeed become anchored around the Federal Reserve's inflation target, and that the strength of this anchoring effect has increased since the 1990s.35 The increase inflation anchoring can be seen in Figure 3, as core inflation begins hovering around 2% beginning shortly after the early 1990s. As discussed earlier, actual inflation is heavily influenced by inflation expectations. As inflation expectations become anchored at a specific rate, these expectations place pressure on actual inflation to remain at that specific rate, acting as a positive feedback loop, which pushes actual inflation back to the inflation anchor after any shock pushes actual inflation away from the anchored rate. The increased level of inflation anchoring helps to explain the lack of deflationary pressure after the 2007-2009 recession.36

An increase in the degree to which inflation becomes anchored may have important implications for future policymaking. As expected inflation becomes more anchored, policymakers may be able to use monetary and fiscal policy more generously without impacting the actual inflation rate. However, if individuals begin to lose confidence in the Federal Reserve's ability to maintain their target inflation rate because the Federal Reserve pursues policies incompatible with price stability, inflation expectations can become unanchored resulting in a more volatile inflation rate as a result of shifting inflation expectations.

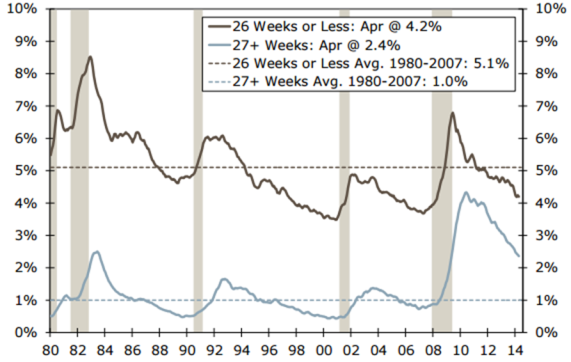

Long-Term Versus Short-Term Unemployment and Inflation

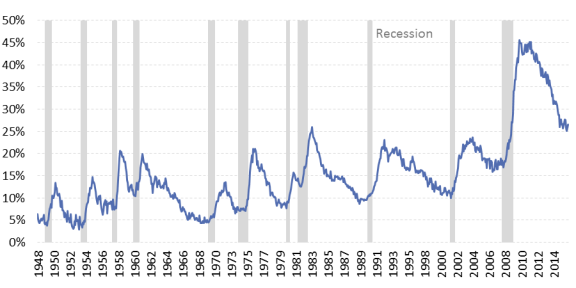

The global financial crisis and subsequent recession in the United States was unique in many ways, including the outsized increase in the proportion of individuals who were unemployed for longer than 26 weeks. As shown in Figure 4, the percentage of unemployed individuals who had been jobless for more than 26 weeks rose to over 45% after the 2007-2008 recession, significantly higher than during any other period in the post-WWII era. The sharp rise of the long-term unemployed has been offered as another potential explanation for the missing deflation after the 2007-2009 recession.

|

|

Source: BLS. Note: Individuals with unemployment duration longer than 26 weeks are considered long-term unemployed. Long-term unemployment rate is the number of long-term unemployed as a percentage of total unemployed. |

Some economists argue that inflation dynamics are driven specifically by the short-term unemployment rate, rather than the total unemployment rate (which includes short-term and long-term unemployment). 37 Employers tend to favor the short-term unemployed so strongly over the long-term unemployed that the long-term unemployed are essentially removed from contention for employment opportunities. Employers tend to avoid hiring the long-term unemployed for a number of reasons, as discussed in the "Time Varying Natural Rate of Unemployment" section. Because the long-term unemployed are essentially removed from the labor pool, from the perspective of employers, the numbers of long-term unemployed individuals have very little impact on wage-setting decisions compared with the short-term unemployed. As a result, the long-term unemployed impact inflation to a lesser degree than the short-term unemployed.

|

Figure 5. Unemployment Rate by Duration 3-Month Moving Average |

|

|

Source: John E. Silvia and Sarah Watt House, Short- and Long-Term Unemployment: A Labor Market Divided, Wells Fargo Securities, May 6, 2014, at http://www.realclearmarkets.com/docs/2014/05/ShortLongTermUnemployment_05062014.pdf. |

The total unemployment rate remained elevated above estimates of the NAIRU for about seven and a half years following the 2007-2009 recession, but this was largely due to the unprecedented increase in the level of long-term unemployed. The short-term unemployment rate spiked, but fell to pre-recession levels relatively quickly after the end of the recession compared with long-term unemployment, as shown in Figure 5. Compared with the persistent unemployment gap for total unemployment after the 2007-2009 recession, the unemployment gap for the short-term unemployed dissipated much faster and therefore would have resulted in a more moderate decrease in the inflation rate. Using the short-term unemployment gap rather than the total unemployment gap to forecast inflation following the 2007-2009 recession, recent research has produced significantly more accurate inflation forecasts and has accounted for much of the missing deflation forecasted by others.38

Results of this research suggest that when considering the effects of monetary or fiscal policy on inflation, policymakers would benefit from using a measure of the unemployment gap that weights the unemployment rate for the short-term unemployed more heavily than the long-term unemployed.

Alternative Measures of Economic Slack

Still others have suggested that the failure of natural rate model to accurately estimate inflation following the financial crisis is evidence that the natural rate model may be incorrect or inadequate for forecasting inflation.39 In response to the perceived failure of the model, some researchers are searching for other potential indicators that can better explain and predict changes in inflation.

The unemployment gap is used as a measure of overall economic slack to help explain changes in inflation; however, it may not be the best measure currently. One recent article has suggested that an alternative measure of economic slack based on recent minimum unemployment rates may offer an improved measure for forecasting inflation. The new measure consists of the difference between the current unemployment rate and the minimum unemployment rate seen over the current and previous 11 quarters. As the current unemployment rate rises above the minimum unemployment seen in previous quarters, inflation tends to decrease, and vice versa. This relationship appears to be relatively stable over time and, more importantly, improves on some other inflation forecasts for periods during and shortly after the 2007-2009 recession.40

Concluding Thoughts on Missing Deflation

After the 2007-2009 recession, actual unemployment rose above CBO's estimated natural rate of unemployment for 31 consecutive quarters. Average core inflation declined, as predicted, but only modestly, from about 2.0% per year between 2003 and 2007 to about 1.4% per year between 2008 and mid-2015.41 This modest decrease in the rate of inflation called into question the validity of the natural rate model. In response, researchers began investigating potential reasons for the unexpectedly mild decrease in inflation. A number of explanations have been offered to explain the missing deflation, ranging from increased financing costs due to crippled financial markets following the global financial crisis, to changes in the formation of inflation expectations since the 1990s, to the unprecedented level of long-term unemployment that resulted from the recession. Researchers have found a degree of empirical evidence to support all of these claims, suggesting it may have been a confluence of factors that resulted in the unexpectedly modest inflation after the recession.

Policy Implications of the Natural Rate Model

The natural rate model has implications for the design and implementation of economic policy, specifically limitations to fiscal and monetary policies and alternative policies to affect economic growth without potentially accelerating inflation.

Limitations to Fiscal and Monetary Policies

The natural rate model suggests that government's ability to spur higher employment through fiscal and monetary policies is limited in important ways. Expansionary fiscal and monetary policies can be used to boost gross domestic product (GDP) growth and reduce unemployment, by increasing demand for goods and services, but doing so comes at a cost.

According to the natural rate model, if government attempts to maintain an unemployment rate below the natural rate of unemployment, inflation will increase and continuously rise until unemployment returns to its natural rate. As a result, growth will be more volatile than if policymakers had attempted to maintain the unemployment rate at the natural rate of unemployment. As higher levels of inflation tend to hurt economic growth, expansionary economic policy can actually end up limiting economic growth in the long run by causing accelerating inflation. The impact of inflation on economic growth is discussed in the "Inflation's Impact on Economic Growth" section below.

As discussed earlier, the relationship of unemployment to the natural rate of unemployment is used as a benchmark to determine when there is either a positive or negative output gap (i.e., actual output differs from potential output). Alternative measures could be used to indicate an output gap, however, the literature surrounding this topic has largely found using the unemployment gap to be a reliable measure of the overall output gap.42

Inflation's Impact on Economic Growth

In general, policymakers avoid pursuing an unemployment target below the natural rate of unemployment because accelerating inflation imposes costs on businesses, individuals, and the economy as a whole. Inflation tends to interfere with pricing mechanisms in the economy, resulting in individuals and businesses making less than optimal spending, saving, and investment decisions. 43 Additionally, economic actors (e.g., workers, firms, and investors) often take action to protect themselves from the negative impacts of inflation, but in doing so divert resources from other more productive activities. 44 For example, to guard against inflation firms will shy from long-term investments, favoring short-term investments even if they offer a lower rate of return. Inflation's impact on economic growth is especially pronounced at higher levels of inflation than the United States has experienced in recent decades.45

Ultimately these inefficient decisions reduce incomes, economic growth, and living standards. For these reasons, it is generally accepted that inflation should be kept low to minimize these distortions in the economy. Some would argue that an inflation rate of zero is optimal; however, a target of zero inflation makes a period of accidental deflation more likely, and deflation is thought to be even more costly than inflation. Deflation is thought to be especially damaging as decreasing prices provide a strong incentive for consumers to abstain from purchasing goods and services, as their dollars will be worth more in the future, decreasing aggregate demand. In an effort to balance these two risks, policymakers, including the Federal Reserve, often target a positive, but low, inflation rate, generally around 2%, which reduces inefficiencies within the economy while protecting against deflation.46

A Weakened Relationship Between Inflation and Unemployment?

The unexpectedly mild decrease in the rate of inflation following the sustained unemployment gap after the 2007-2009 recession suggested a weakening of the relationship between the unemployment gap and inflation, and evidence of a weakened relationship persists several years into the current economic expansion. Expansionary monetary and fiscal policies have been in place for the better part of a decade. The unemployment rate is approximating estimates of the natural rate of unemployment, and yet the inflation rate has yet to rise to the Federal Reserve's long-term target of 2% per year. The current state of the economy suggests that either the subdued relationship seen between the unemployment gap and inflation during the depths of the economic downturn appears to be persisting even as economic conditions improve, or the unemployment gap may no longer act as an accurate measure of the output gap.

If the relationship between inflation and the unemployment rate has indeed weakened, it would have important implications for economic policy. On the one hand, it may allow policymakers to employ fiscal and monetary policies more aggressively without accelerating inflation at the same rate as would have been previously expected.47 On the other hand, however, a weakened relationship would also suggest that if inflation were to begin accelerating, a larger and more sustained period of elevated unemployment may be necessary to stabilize inflation than otherwise anticipated.48 Further research and time is necessary to determine if the weakened relationship seen after the recession is a temporary phenomenon specific to the financial crisis and subsequent events, or if it is a more enduring shift in the strength of the dynamic between unemployment and inflation.

Alternatively, the Federal Reserve's inability to meet their inflation target despite the unemployment rate falling to levels consistent with the natural rate of unemployment, may suggest that the unemployment gap is no longer an accurate proxy for the output gap. In the second quarter of 2016, the unemployment rate was about 4.9%, consistent with estimates of the natural rate of unemployment (4.6%-5.0%),49 but the CBO still estimated an output gap of about 2% during the same period. 50 The difference between the unemployment gap and output gap may be due to persistent slack in the labor market as a result of the 2007-2009 recession, which is not captured by the official unemployment rate. Alternative measures of labor market underutilization show that some of the weakness in labor markets that resulted from the recession still persists.51 For example, following the recession, the labor force participation rate52 decreased from about 66% to less than 63%. Some of this decrease is due to an aging population but some is due to individuals giving up on finding work due to poor economic conditions.53 The unemployment rate does not account for individuals who stopped looking for work, and therefore may understate the actual amount of slack left in the economy. This could help explain why the CBO estimates a current output gap, while the unemployment gap seems to have disappeared. Following the significant damage to the labor market as a result of the 2007-2009 recession, it is likely beneficial to use multiple measures of labor market underutilization in addition to the official unemployment rate to judge the potential size of the unemployment and output gap.

Changing the Natural Rate of Unemployment

In addition to fiscal and monetary policies, alternative economic policies could be used to target higher economic output without the risk of accelerating inflation by lowering the natural rate of unemployment. As discussed in the "Time Varying Natural Rate of Unemployment" section, four main factors determine the natural rate of unemployment, (1) the makeup of the labor force, (2) labor market institutions and public policy, (3) growth in productivity, and (4) contemporaneous and previous levels of long-term unemployment. Policies to improve the labor force, by either making employees more desirable to employers or improving the efficiency of the matching process between employees and employers, would drive down the natural rate of unemployment. In addition, changes to labor market institutions and public policy that ease the process of finding and hiring qualified employees, such as increased job training or apprenticeship programs, could also help lower the natural unemployment rate. A wide range of policies have been suggested that may increase the growth rate of productivity and therefore decrease the natural rate of unemployment, such as increasing government investment in infrastructure, reducing government regulation of industry, and increasing incentives for research and development. In addition, more aggressive policy interventions to help individuals find work during economic downturns may help to prevent spikes in long-term unemployment and avoid increases in the natural rate of unemployment.

Author Contact Information

Acknowledgments

The report was originally authored by Jeffrey Stupak, former CRS Analyst in Macroeconomic Policy.

Footnotes

| 1. |

Board of Governors of the Federal Reserve System, "2015 Monetary Policy Decisions," press release, December 16, 2015, at https://www.federalreserve.gov/newsevents/press/monetary/20151216a.htm. |

| 2. |

Board of Governors of the Federal Reserve System, "Federal Reserve Board and Federal Open Market Committee Release Economic Projections from the June 14-15 FOMC meeting," press release, June 15, 2016, at https://www.federalreserve.gov/newsevents/press/monetary/20160615b.htm, and Congressional Budget Office (CBO), Potential GDP and Underlying Inputs, January 2016, at https://www.cbo.gov/about/products/budget_economic_data#6. |

| 3. |

For further information on unemployment, refer to CRS In Focus IF10443, Introduction to U.S. Economy: Unemployment, by Jeffrey M. Stupak, and for information on inflation refer to CRS In Focus IF10477, Introduction to U.S. Economy: Inflation, by Jeffrey M. Stupak. |

| 4. |

A. W. Phillips, "The Relation Between Unemployment and the Rate of Change of Money Wage Rates in the United Kingdom, 1861-1957," Economica, vol. 25 (1958), pp. 283-299. |

| 5. |

Paul A. Samuelson and Robert M. Solow, "Analytical Aspects of Anti-Inflation Policy," The American Economic Review, vol. 50, no. 2 (May 1960), pp. 177-194. |

| 6. |

Wages generally make up a large portion of the price of goods, and therefore an increase in wages will generally lead to increasing prices. |

| 7. |

Robert J. Gordon, "The History of the Phillips Curve: Consensus and Bifurcation," Economica, vol. 78 (2011), pp. 10-50. |

| 8. |

See Milton Friedman, "The Role of Monetary Policy," The American Economic Review, vol. 57, no. 1 (March 1968), pp. 1-12, and Edmund Phelps, "Phillips Curve, Expectations of Inflation and Optimal Employment Over Time," Economica, vol. 34, no. 135 (August 1967), pp. 254-281. |

| 9. |

U.S. Congressional Budget Office (CBO), The Natural Rate of Unemployment, April 2007. |

| 10. |

Potential output is an estimate of the level gross domestic product (GDP) consistent with a high-rate of resource use, however potential output is not a ceiling on output. For a description of how CBO estimates potential output, refer to Robert Arnold, CBO's Method for Estimating Potential Output: An Update, CBO, August 2001, at https://www.cbo.gov/sites/default/files/107th-congress-2001-2002/reports/potentialoutput.pdf. |

| 11. |

Robert J. Gordon, "The Time-Varying NAIRU and its Implications for Economic Policy," Journal of Economic Perspectives, vol. 11, no. 1 (Winter 1997), p. 12. |

| 12. |

J. Bradford Delong and Martha L. Olney, Macroeconomics, 2nd ed. (New York: McGraw-Hill Irwin, 2006), pp. 358-361. |

| 13. |

Ibid. |

| 14. |

Ibid. |

| 15. |

Laurence Ball and Gregory Mankiw, "The NAIRU in Theory and Practice," Journal of Economic Perspective, vol. 16, no. 4 (Fall 2002), pp. 115-136. |

| 16. |

Elena Rusticelli, "Rescuing the Phillips Curve: Making Use of Long-term Unemployment in the Measurement of the NAIRU," OECD Journal: Economic Studies, vol. 2014/1, 2015. |

| 17. |

These figures are estimated; therefore, the natural rate of unemployment may have shifted more or less during this period. |

| 18. |

Robert J. Gordon, "Foundations of the Goldilocks Economy," Brookings Institution, Brookings Papers on Economic Activity no. 2, 1998, pp. 297-333. |

| 19. |

Laurence Ball and Gregory Mankiw, "The NAIRU in Theory and Practice," The Journal of Economic Perspectives, vol. 16, no. 4 (Autumn 2002), pp. 115-136. |

| 20. |

Mary C. Daly, Bart Hobijn, and Robert Valletta, et al., "A Search and Matching Approach to Labor Markets: Did the Natural Rate of Unemployment Rise," Journal of Economic Perspectives, vol. 26, no. 3 (Summer 2012), pp. 3-26. |

| 21. |

Ibid. |

| 22. |

The Congressional Research Service (CRS) calculations using data from the BLS. |

| 23. |

A supply shock is an unexpected event that impacts the supply of a good or service within the economy. |

| 24. |

Laurence Ball and Gregory Mankiw, "The NAIRU in Theory and Practice," Journal of Economic Perspectives, vol. 16, no. 4 (Fall 2002), pp. 115-136. |

| 25. |

CRS calculations based on data from the Bureau of Economic Analysis (BEA). |

| 26. |

Robert J. Gordon, The Phillips Curve is Alive and Well: Inflation and the NAIRU During the Slow Recovery, NBER, Working Paper no. 19390, August 2013. |

| 27. |

Laudio Borio and Andrew Filardo, Globalisation and Inflation: New Cross-Country Evidence on the Global Determinants of Domestic inflation, Bank for International Settlements, Working Paper, no. 227, May 2007 and Laurence M. Ball, Has Globalization Changed Inflation?, NBER, Working Paper s no. 12687, November 2006. |

| 28. |

Nigel Pain, Isabell Koske, and Marte Sollie, Globalisation and Inflation in the OECD Countries, OECD Economics Department, Working Paper no. 524, November 2006; and Jane Ihrig; et al., Some Simple Tests of the Globalization and Inflation Hypotheses, Board of Governors of the Federal Reserve System, International Finance Discussion Paper no. 891, April 2007. |

| 29. |

Jane Ihrig et al., Some Simple Tests of the Globalization and Inflation Hypotheses, Board of Governors of the Federal Reserve System, International Finance Discussion Paper no. 891, April 2007; Francesco Bianchi and Andrea Civelli, "Globalization and Inflation: Evidence from a Time Varying VAR," Review of Economic Dynamics, vol. 18, no. 2 (April 2015), pp. 406-433; and Jean Boivin and Marc Giannoni, Global Forces and Monetary Policy Effectiveness, NBER, Working Paper no. 13736, January 2008. |

| 30. |

A product is said to have a sticky customer base if it is especially costly or time consuming for customers to switch producers or search for new ones. Simon Gilchrist et al., Inflation Dynamics During the Financial Crisis, Board of Governors of the Federal Reserve System, Finance and Economics Discussion Series no. 2015-012, March 2015. |

| 31. |

Ibid. |

| 32. |

Laurence M. Ball and Sandeep Mazumder, Inflation Dynamics and the Great Recession, NBER, Working Paper no. 17044, May 2011. |

| 33. |

Martin Sommer, Supply Shocks and the Persistence of Inflation, Econ WPA, Macroeconomics no. 408005, 2004; Mark A. Hooker, "Are Oil Shocks Inflationary?: Asymmetric and Nonlinear Specifications Versus Changes in Regime," Journal of Money, Credit, and Banking, vol. 34, no. 2 (May 2002), pp. 540-561; and Jeffrey C. Fuhrer, Giovanni Olivei, and Geoffrey M. B. Tootell, Empirical Estimates of Changing Inflation Dynamics, Federal Reserve Bank of Boston, Working Paper no. 09-4, May 2009. |

| 34. |

John Taylor, Discretion Versus Policy Rules in Practice, Carnegie-Rochester Conference Series on Public Policy, vol. 39 (1993), pp. 2-33. |

| 35. |

Frederic S. Mishkin, Inflation Dynamics, NBER, Working Paper no. 13147, June 2007 and Laurence M. Ball and Sandep Mazunder, Inflation Dynamics and the Great Recession, NBER, Working Paper no. 17044, May 2011. |

| 36. |

Laurence M. Ball and Sandep Mazunder, Inflation Dynamics and the Great Recession, NBER, Working Paper no. 17044, May 2011. |

| 37. |

Elena Rusticelli, "Rescuing the Phillips Curve: Making Use of Long-term Unemployment in the Measurement of the NAIRU," OECD Journal: Economic Studies, vol. 2014/1, 2015. |

| 38. |

Robert J. Gordon, The Phillips Curve is Alive and Well: Inflation and the NAIRU during the Slow Recovery, NBER, Working Paper, no. 19390, August 2013, and Elena Rusticelli, "Rescuing the Phillips Curve: Making Use of Long-term Unemployment in the Measurement of the NAIRU," OECD Journal: Economic Studies, vol. 2014/1, 2015 |

| 39. |

Robert E. Hall, "The Long Slump," The American Economic Review, vol. 101, no. 2 (April 2011), pp. 431-469. |

| 40. |

James H. Stock and Mark W. Watson, Modeling Inflation After the Crisis, NBER, Working Paper no. 16488, October 2010. |

| 41. |

CRS calculations based on data from the BEA. |

| 42. |

Christopher J. Erceg and Andrew T. Levin, "Labor Force Participation and Monetary Policy in the Wake of the Great Recession," Journal of Money, Credit, and Banking, vol. 46, no. S2 (October 2014), pp. 3-49. |

| 43. |

Clive Briault, "The Costs of Inflation," Bank of England Quarterly Bulletin, vol. 35, no. 1 (1995), pp. 33-45, at http://www.bankofengland.co.uk/archive/Documents/historicpubs/qb/1995/qb950102.pdf. |

| 44. |

Ibid. |

| 45. |

Robert J. Barro, Inflation and Economic Growth, National Bureau of Economic Research (NBER), Working Paper no. 5326, October 1995. |

| 46. |

Board of Governors of the Federal Reserve System, Why Does the Federal Reserve Aim for 2 Percent Inflation Over Time?, at https://www.federalreserve.gov/faqs/economy_14400.htm. |

| 47. |

Lael Brainard, The "New Normal" and What It Means for Monetary Policy, The Chicago Council on Global Affairs, Chicago, September 12, 2016, at https://www.federalreserve.gov/newsevents/speech/brainard20160912a.pdf. |

| 48. |

Olivier Blanchard, Eugenio Cerutti, and Lawrence Summers, Inflation and Activity—Two Explorations and Their Monetary Policy Implications, NBER, Working Paper no. 21726, November 2015. |

| 49. |

Board of Governors of the Federal Reserve System, "Federal Reserve Board and Federal Open Market Committee Release Economic Projections from the June 14-15 FOMC Meeting," press release, June 15, 2016, at https://www.federalreserve.gov/newsevents/press/monetary/20160615b.htm, and CBO, Potential GDP and Underlying Inputs, January 2016, at https://www.cbo.gov/about/products/budget_economic_data#6. |

| 50. |

CBO, Budget and Economic Data: Potential GDP and Underlying Inputs, August 2016, at https://www.cbo.gov/about/products/budget_economic_data#1. |

| 51. |

David G. Blanchflower and Andrew T. Levin, Labor Market Slack and Monetary Policy, NBER, Working Paper no. 21094, April 2015. |

| 52. |

The labor force participation rate is the percentage of the population that is either employed or unemployed (that is, either working or actively seeking work). |

| 53. |

Stephanie Aaronson, Tomaz Cajner, and Bruce Fallick, et al., Labor Force Participation: Recent Developments and Future Prospects, Brookings Institute, Brookings Papers on Economic Activity, 2014, pp. 197-275, https://www.brookings.edu/wp-content/uploads/2016/07/Fall2014BPEA_Aaronson_et_al.pdf. |