Housing Issues in the 114th Congress

Housing and residential mortgage markets in the United States are continuing to recover from several years of turmoil that began in 2007-2008, though the recovery has been uneven across the country. Nationally, home prices have been consistently increasing since 2012. Negative equity and mortgage foreclosure rates have been steadily decreasing, though both remain elevated. Home sales have begun to increase, with sales of existing homes approaching levels that were common in the early 2000s, though sales of new homes and housing starts remain relatively low.

Mortgage originations have also remained relatively low despite ongoing low interest rates, leading many to argue that it is too difficult for prospective homebuyers to qualify for a mortgage. Some believe that this is because mortgage regulations put in place in recent years are restricting access to mortgages for creditworthy homebuyers, while others hold that these rules provide important consumer protections and suggest that other factors are limiting mortgage access. About two-thirds of new mortgages continue to be backed by Fannie Mae or Freddie Mac or insured by a government agency such as the Federal Housing Administration (FHA) or the Department of Veterans Affairs (VA), with the remaining mortgages mostly being held on bank balance sheets.

In the rental housing market, vacancy rates have continued to decline and rents have continued to increase as more households become renters. Although the supply of rental housing has also increased, it has generally not kept pace with the increasing demand. Rising rents have contributed to housing affordability problems, which are especially pronounced for low-income renters.

The 114th Congress considered a number of housing-related issues against this backdrop. Some of these issues were related to housing for low-income individuals and families, including appropriations for housing programs in a limited funding environment, proposed reforms to certain rental assistance programs administered by the Department of Housing and Urban Development (HUD), debate over funding for two affordable housing funds (the Housing Trust Fund and the Capital Magnet Fund), and the possible reauthorization of the main program that provides housing assistance to Native Americans. Congress also took the occasion of HUD’s 50th anniversary to reflect on the department’s role through hearings and other actions.

Congress also deliberated on certain housing finance-related issues, including possible targeted changes to Fannie Mae and Freddie Mac, oversight of mortgage-related rulemakings, and issues related to the future and financial health of FHA.

Two fair housing issues were also active in the 114th Congress. HUD recently released a new rule updating certain HUD grantees’ responsibilities to “affirmatively further” fair housing. Separately, the Supreme Court issued a decision affirming that disparate impact claims are allowable under the Fair Housing Act. Congress expressed interest in both of these developments.

As in recent years, the 114th Congress considered several housing-related tax provisions as part of a broader tax extenders bill. These housing-related provisions included extensions of the exclusion for canceled mortgage debt, the deduction for mortgage insurance premiums, and provisions related to the low-income housing tax credit.

Housing Issues in the 114th Congress

Jump to Main Text of Report

Contents

- Introduction

- Overview of Housing and Mortgage Market Conditions

- Owner-Occupied Housing Markets

- The Home Mortgage Market

- Rental Housing Markets

- Assisted Housing Issues

- HUD's 50th Anniversary

- Appropriations for Housing Assistance Programs

- Assisted Housing Reform

- Native American Housing Assistance and Self-Determination Act Reauthorization

- Funding for the Housing Trust Fund and Capital Magnet Fund

- Homeownership and Mortgage Finance Issues

- Fannie Mae and Freddie Mac

- Oversight of Mortgage-Related Rulemakings

- The Federal Housing Administration

- FHA and GSE Distressed Loan Sales

- Fair Housing Issues

- Supreme Court Decision on Disparate Impact Claims Under the Fair Housing Act

- HUD's Affirmatively Furthering Fair Housing (AFFH) Rule

- Housing-Related Tax Extenders

- Tax Exclusion for Canceled Mortgage Debt

- Mortgage Insurance Premium Deductibility

- Low-Income Housing Tax Credit: The 9% Floor

- Low-Income Housing Tax Credit: Treatment of Military Housing Allowance

- Other Issues

- Lead Hazards

Figures

- Figure 1. Year-over-Year House Price Changes

- Figure 2. Mortgaged Homes with Negative Equity

- Figure 3. Foreclosure Inventory Rates

- Figure 4. Existing Home Sales

- Figure 5. New Home Sales

- Figure 6. Housing Starts

- Figure 7. Home Purchase Mortgage Originations

- Figure 8. Mortgage Interest Rates

- Figure 9. Share of Mortgage Originations by Type

- Figure 10. Rental and Homeownership Rates

- Figure 11. Rental Vacancy Rates

- Figure 12. Cost-Burdened Renter Households

Summary

Housing and residential mortgage markets in the United States are continuing to recover from several years of turmoil that began in 2007-2008, though the recovery has been uneven across the country. Nationally, home prices have been consistently increasing since 2012. Negative equity and mortgage foreclosure rates have been steadily decreasing, though both remain elevated. Home sales have begun to increase, with sales of existing homes approaching levels that were common in the early 2000s, though sales of new homes and housing starts remain relatively low.

Mortgage originations have also remained relatively low despite ongoing low interest rates, leading many to argue that it is too difficult for prospective homebuyers to qualify for a mortgage. Some believe that this is because mortgage regulations put in place in recent years are restricting access to mortgages for creditworthy homebuyers, while others hold that these rules provide important consumer protections and suggest that other factors are limiting mortgage access. About two-thirds of new mortgages continue to be backed by Fannie Mae or Freddie Mac or insured by a government agency such as the Federal Housing Administration (FHA) or the Department of Veterans Affairs (VA), with the remaining mortgages mostly being held on bank balance sheets.

In the rental housing market, vacancy rates have continued to decline and rents have continued to increase as more households become renters. Although the supply of rental housing has also increased, it has generally not kept pace with the increasing demand. Rising rents have contributed to housing affordability problems, which are especially pronounced for low-income renters.

The 114th Congress considered a number of housing-related issues against this backdrop. Some of these issues were related to housing for low-income individuals and families, including appropriations for housing programs in a limited funding environment, proposed reforms to certain rental assistance programs administered by the Department of Housing and Urban Development (HUD), debate over funding for two affordable housing funds (the Housing Trust Fund and the Capital Magnet Fund), and the possible reauthorization of the main program that provides housing assistance to Native Americans. Congress also took the occasion of HUD's 50th anniversary to reflect on the department's role through hearings and other actions.

Congress also deliberated on certain housing finance-related issues, including possible targeted changes to Fannie Mae and Freddie Mac, oversight of mortgage-related rulemakings, and issues related to the future and financial health of FHA.

Two fair housing issues were also active in the 114th Congress. HUD recently released a new rule updating certain HUD grantees' responsibilities to "affirmatively further" fair housing. Separately, the Supreme Court issued a decision affirming that disparate impact claims are allowable under the Fair Housing Act. Congress expressed interest in both of these developments.

As in recent years, the 114th Congress considered several housing-related tax provisions as part of a broader tax extenders bill. These housing-related provisions included extensions of the exclusion for canceled mortgage debt, the deduction for mortgage insurance premiums, and provisions related to the low-income housing tax credit.

Introduction

Housing and residential mortgage markets in the United States are continuing to recover from several years of turmoil that began with the bursting of a housing "bubble" that peaked in the mid-2000s and burst in 2007-2008. The bubble featured rapidly rising home prices in many areas of the country as well as looser credit standards for obtaining mortgages. The years of housing market turmoil that followed featured sharp declines in house prices, increased mortgage foreclosures, tighter mortgage credit standards, and lower levels of home sales and homebuilding.

Since about 2012, many national housing market indicators have been improving from their performance during the years of housing market turmoil. For example, house prices have been rising and negative equity and foreclosure rates have been falling. However, foreclosure rates and negative equity continue to be higher than is generally considered to be normal, and home sales and mortgage originations have been relatively low. In addition, housing affordability continues to be an issue for many households in general, and for low-income renter households in particular. Rising home prices impact the affordability of housing for prospective homebuyers, while increasing numbers of renter households and the corresponding effects on vacancy rates and rents have implications for the affordability and availability of rental housing.

The 114th Congress considered a number of housing-related issues against this backdrop. Some of these issues reflected larger questions about policies that could accelerate recovery in the housing and mortgage markets or factors that could be hampering recovery. For example, Congress considered legislation to modify certain mortgage-related laws and regulations that were put in place during the aftermath of the housing downturn, in response to concern that these new rules may be impeding access to mortgage credit. However, some feel that changes to the rules could weaken consumer protections. Congress also considered certain changes related to two government-sponsored enterprises (GSEs), Fannie Mae and Freddie Mac, as well as other housing finance-related issues.

In addition, the 114th Congress considered a number of issues related to affordable rental housing and assisted housing programs administered by the Department of Housing and Urban Development (HUD). These issues included appropriations for housing programs in a limited funding environment, certain reforms to some HUD-assisted housing programs, the reauthorization of the main program of housing assistance for Native American tribes, and debate about GSE contributions to two affordable housing funds that were created in 2008 but received GSE funding for the first time beginning in 2016.

Additional issues of active interest to Congress included oversight of HUD on the occasion of the department's 50th anniversary, issues related to enforcement of the Fair Housing Act, and the status of certain housing-related tax provisions.

This report begins with an overview of housing and mortgage market conditions to provide context for the housing issues that the 114th Congress considered, and then discusses major housing issues that were active during the Congress. This report is meant to provide a broad overview of the issues and is not intended to provide detailed information or analysis. However, it includes references to other, more in-depth CRS reports on the issues where possible.

Overview of Housing and Mortgage Market Conditions

Owner-Occupied Housing Markets

On a national basis, many owner-occupied housing market indicators have been improving in recent years, with mortgage foreclosure rates falling and household equity increasing. However, these and other indicators, such as home sales and housing starts, have not returned to the levels that were seen prior to the housing bubble. In the case of some indicators, such as house price growth or home sales, it may be unrealistic or undesirable to expect conditions to fully return to those levels.

Housing market conditions vary greatly across local housing markets. While some areas of the country have fully recovered from the housing market turmoil, other areas continue to struggle. In particular, many low-income and minority neighborhoods appear to be recovering less quickly than most other areas, if at all.1

Home Prices

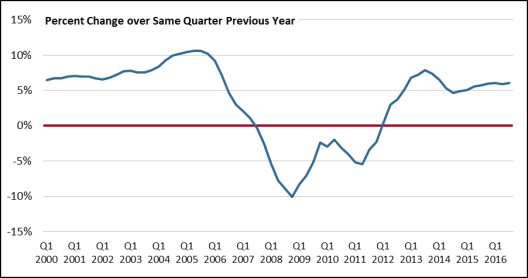

The housing market turmoil that began around 2007 was characterized by, among other things, falling house prices that left many households with little or no equity in their homes. As shown in Figure 1, on a year-over-year basis house prices increased from 2000 to mid-2007 then declined for several years through the end of 2011. House prices began to rise again nationally in 2012. They continued to rise throughout 2015 and 2016, with the rate of increase remaining relatively consistent since the beginning of 2015. While rising house prices are beneficial for current homeowners, and especially for households whose home values fell to levels below the amount they owed on their mortgages, they can also make it less affordable for prospective homebuyers to purchase homes.

Negative Equity

During the housing market turmoil, falling house prices left many households in a negative equity position, meaning that they owed more on their mortgages than their homes were currently worth. Negative equity can contribute to foreclosures because it prevents households from selling their homes for enough to pay off their mortgages if they are having difficulty staying current on mortgage payments. Furthermore, negative equity can affect the housing market by making households less likely to put their homes up for sale, as many homeowners may be reluctant to sell their homes if the sales prices will not be enough to pay off their mortgage balances.

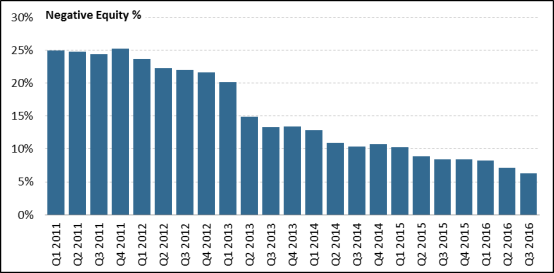

With home prices increasing on a national basis, the number of households estimated to have negative equity has been falling. As shown in Figure 2, in the third quarter of 2016 just over 6% of all mortgaged properties were estimated to have negative equity. In comparison, in the second quarter of 2011 the negative equity share was estimated at about 25%.

|

Figure 2. Mortgaged Homes with Negative Equity Q1 2011-Q3 2016 |

|

|

Source: Figure created by CRS based on data in CoreLogic's Equity Report, Third Quarter 2016. |

Although rising home prices have helped many households regain equity, it is estimated that over 3 million homes with a mortgage remain in negative equity across the country.2 Furthermore, although the overall rate of negative equity is improving, negative equity is not evenly distributed across the country. In particular, negative equity remains persistently high in many low-income and minority neighborhoods. Lower-priced homes also continue to experience negative equity at higher rates than higher-priced homes.3 This suggests that many areas are not experiencing housing market recovery at the same pace as other areas.

Home Foreclosures

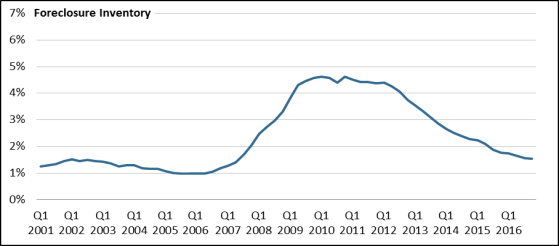

Partly because of rising house prices and decreasing negative equity, mortgage foreclosure rates have also been consistently declining. As shown in Figure 3, the share of mortgages in the foreclosure process decreased to about 1.5% in the fourth quarter of 2016. This is notably lower than the peak of over 4.5% in 2010 and the lowest rate of mortgages in the foreclosure process since the second quarter of 2007. In comparison, in the early 2000s foreclosure rates generally ranged between 1% and 1.5%.

Home Sales

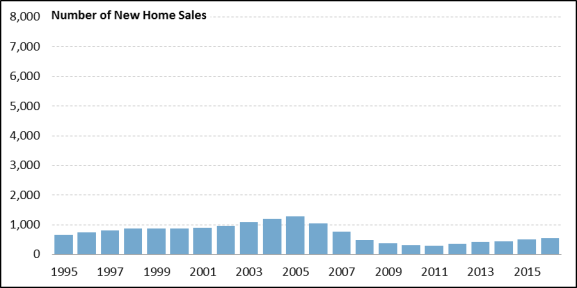

Home sales include both sales of existing homes and sales of newly built homes. Existing home sales generally number in the millions each year, while new home sales are usually in the hundreds of thousands. During the housing market turmoil, both existing home sales and new home sales fell. Both have been increasing somewhat in recent years, though new home sales in particular remain relatively low.

Figure 4 shows the annual number of existing home sales for each year from 1995 through 2016. Existing home sales during that period peaked in 2005 at over 7 million before falling to a low of about 4.1 million in 2008. In 2016, there were nearly 5.5 million existing homes sold, the highest number of existing home sales since 2006 and similar to the numbers seen in the late 1990s and early 2000s.

|

in thousands |

|

|

Source: Figure created by CRS using data from HUD's U.S. Housing Market Conditions report for the second quarter of 2016, available at https://www.huduser.gov/portal/ushmc/hd_home_sales.html, and the National Association of Realtors Existing Home Sales Overview Chart for Printing at https://www.nar.realtor/topics/existing-home-sales. |

Figure 5 shows the annual number of new home sales for each year from 1995 through 2016. Though the number of new home sales has begun to increase somewhat, reaching over 560,000 in 2016, new home sales remain well below the levels seen in the late 1990s and early 2000s, when they tended to be between 800,000 and 1 million per year.

|

in thousands |

|

|

Source: Figure created by CRS based on data from the U.S. Census Bureau, New Residential Sales Historical Data, Houses Sold (Annual), https://www.census.gov/construction/nrs/historical_data/index.html. |

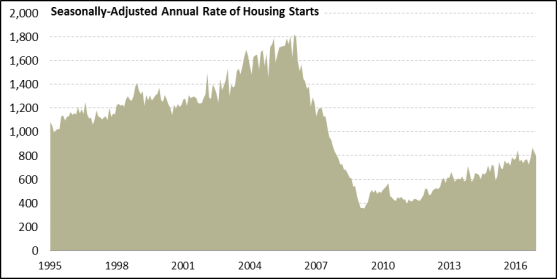

Housing Starts

Housing starts are the number of new homes on which construction is started in a given period. The number of housing starts is consistently higher than the number of new home sales. This is primarily because housing starts include homes that are not intended to be put on the for-sale market, such as homes built by the owner of the land or homes built for rental.4

Housing starts for single-family homes also fell during the housing market turmoil, reflecting decreased home purchase demand. Nevertheless, as housing markets have started to stabilize, there have been signs that housing starts are also beginning to increase. As shown in Figure 6, which shows the seasonally adjusted annual rate of housing starts for each month from January 1995 through December 2016, the seasonally adjusted annual rate of housing starts in one-unit residential buildings was generally between 1.2 million and 1.8 million each month from 2000 through 2007. Since that time, however, the seasonally adjusted annual rate of housing starts fell to a rate of between 400,000 and 600,000 for each month until about 2013. More recently, housing starts have been trending upward, and were close to or exceeded a seasonally adjusted annual rate of over 700,000 for much of 2015 and 2016. However, they remained well below the levels seen throughout the 1990s and early 2000s.

|

Seasonally adjusted annual rate by month; in thousands |

|

|

Source: Figure created by CRS using data from the U.S. Census Bureau, New Residential Construction Historical Data, http://www.census.gov/construction/nrc/historical_data/. Data are through December 2016. Notes: Figure reflects starts in one-unit structures only. The seasonally adjusted annual rate is the number of housing starts that would be expected if the number of homes started in that month (on a seasonally adjusted basis) were extrapolated over an entire year. |

The Home Mortgage Market

Most homeowners take out a mortgage to purchase a home. Therefore, owner-occupied housing markets are closely linked to the mortgage market (though they are not the same). The ability of prospective homebuyers to obtain mortgages impacts the demand for homes.

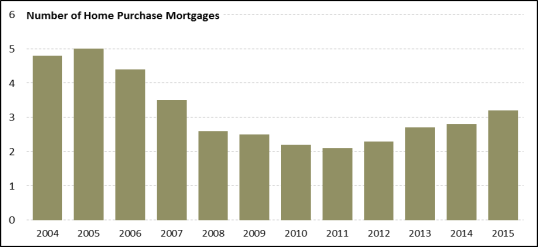

Home Purchase Mortgage Originations

As shown in Figure 7, in the years following 2007 the number of mortgages originated for home purchases (as opposed to mortgages to refinance a home) was relatively low, though it has been increasing somewhat in recent years. While close to 5 million home purchase mortgages were originated in 2004, that number fell to 2.5 million in 2008 and 2.1 million in 2011. In 2015, there were about 3.2 million home purchase mortgage originations, up from about 2.8 million in 2014 and 2.7 million in 2013.5

There are several possible reasons why home purchase mortgage originations, and home sales in general, may not be increasing more quickly. Economic pressures could be affecting both the supply of homes on the market and demand for those homes. For example, some current homeowners may be unwilling to sell their homes due to negative equity or other reasons, leading to lower numbers of homes for sale in many markets.6 Stagnant or declining incomes and factors such as rising student loan debt may be depressing the demand for home purchases, particularly among younger households who would traditionally be first-time homebuyers.7

Demographic trends may also be playing a role. As the baby boomer generation ages, fewer households may be seeking to move since older households tend to move less frequently than younger households.8 At the same time, younger households, who traditionally make up a large share of first-time homebuyers, appear to be waiting longer to purchase homes. While this could be partly due to economic pressures, younger households are also more likely to delay major life events, such as marriage, compared to previous generations. This could also contribute to some households waiting longer to purchase a home.9

Additionally, many observers argue that mortgage credit is unusually tight—that is, it is too difficult for many households that would like to buy homes to get a mortgage to finance the purchase. This is discussed further in the next subsection.

Mortgage Credit Access

Some prospective homebuyers may find themselves unable to obtain mortgages due to their credit histories, the cost of obtaining a mortgage (such as down payments and closing costs), or other factors. In general, it is beneficial to the housing market when creditworthy homebuyers are able to obtain mortgages to purchase homes. However, access to mortgages must be balanced against the risk of offering mortgages to people who will not be willing or able to repay the money they borrowed. Striking the right balance of credit access and risk management, and the question of who is considered to be "creditworthy," continue to be subjects of ongoing debate.

A variety of organizations attempt to measure the availability of mortgage credit. While their methods vary, many experts agree that mortgage credit is tighter than it was in the years prior to the housing bubble and subsequent housing market turmoil. In particular, researchers note that a higher proportion of loans are made to the highest credit quality borrowers and that the mortgage market is taking on less default risk than it did in the years that preceded the looser credit standards of the housing bubble.10 However, some also argue that mortgage credit is not too tight and note that the Federal Housing Administration, in particular, continues to serve lower credit quality borrowers.11

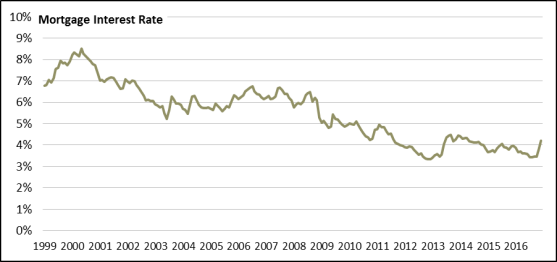

Interest Rates

Relatively low numbers of mortgage originations have persisted despite continued low mortgage interest rates. As shown in Figure 8, the average interest rate on a 30-year fixed-rate mortgage has been under 5% since May 2010 and was under 4% for most of 2012 and the first half of 2013.12 Interest rates started to rise slowly in the second half of 2013 but generally remained below 4.5%. Since then, interest rates again declined and were below 4% for much of 2015 and 2016.

|

Figure 8. Mortgage Interest Rates January 1999-December 2016 |

|

|

Source: Figure created by CRS based on data from Freddie Mac's Primary Mortgage Market Survey, 30-Year Fixed Rate Historic Tables, available at http://www.freddiemac.com/pmms/. |

To the extent that interest rates eventually begin to rise in a more sustained way, it may have implications for mortgage affordability, particularly when combined with rising house prices and, in some cases, higher mortgage insurance fees. Rising interest rates could also deter some existing homeowners from selling their homes, because any new mortgages these homeowners obtained would likely have higher interest rates than what they are currently paying.

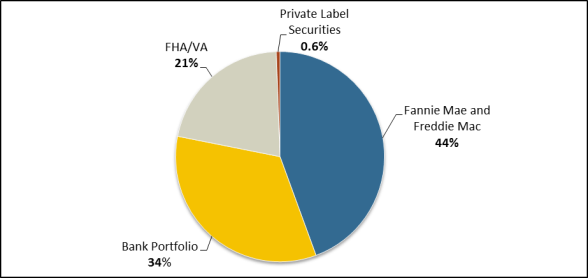

Mortgage Market Composition

When a lender originates a mortgage, it can choose to hold that mortgage in its own portfolio, sell it to a private company, or sell it to Fannie Mae or Freddie Mac, two congressionally chartered government-sponsored enterprises (GSEs). Furthermore, a mortgage might be insured by a federal government agency, such as the Federal Housing Administration (FHA) or the Department of Veterans Affairs (VA). In the years after the housing bubble burst, there was an increase in the share of mortgages with some federal backing (either mortgage insurance from a government agency or a guarantee from Fannie Mae or Freddie Mac), leading some to worry about increased government exposure to risk and a lack of private capital for mortgages.

As shown in Figure 9, nearly two-thirds of the total dollar volume of mortgages originated in the first three quarters of 2016 were either guaranteed by a federal agency such as FHA or VA (21%) or backed by Fannie Mae or Freddie Mac (44%). Over one-third of the dollar volume of mortgages originated was held in bank portfolios (34%), while less than 1% was securitized in the private market. The share of new mortgage originations, by dollar volume, insured by a federal agency or guaranteed by Fannie Mae or Freddie Mac has fallen from a high of nearly 90% in 2009. Nevertheless, the share of mortgage originations with federal mortgage insurance or a Fannie or Freddie guarantee remains elevated compared to the 2002-2007 period, when FHA and VA mortgages constituted a very small share of the mortgage market and the GSE share ranged from about 30% to 50%.13

Rental Housing Markets

In the years since the housing market turmoil began, the homeownership rate has decreased while the percentage of households who rent their homes has correspondingly increased. Although the supply of rental housing has also increased, both through new construction and as some formerly owner-occupied homes are converted to rentals, in many markets the rise in the number of renters has increased competition for rental housing and pushed up rents. This, in turn, has resulted in more renter households being cost-burdened, defined as paying more than 30% of income toward housing costs.

Increasing Share of Renters

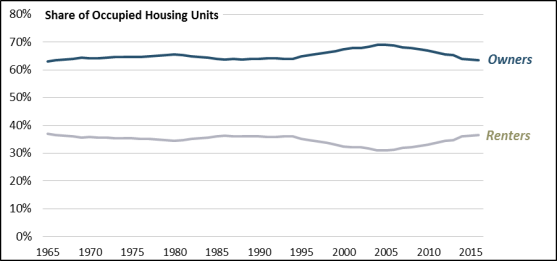

As shown in Figure 10, the share of renters has been increasing in recent years, reaching close to 37% of all occupied housing units in 2016. This was the highest share of renters since the early 1990s. The homeownership rate has correspondingly decreased, falling from a high of 69% in 2004 to just over 63% in 2016.14

In addition to an increase in the share of households who rent, the overall number of renter households has been increasing as well. In 2016, there were over 43 million occupied rental housing units, compared to 40 million in 2013 and fewer than 36 million in 2008.15

Vacancy Rates

In general, the increase in renters has led to a decrease in rental vacancy rates in many, though not all, areas of the country.16 This has been the case in many areas even though the supply of rental housing has been increasing through both new multifamily construction and the conversion of some previously owner-occupied single-family units to rental housing.17 In many cases, the increase in the rental housing supply has not kept up with the increase in rental housing demand.

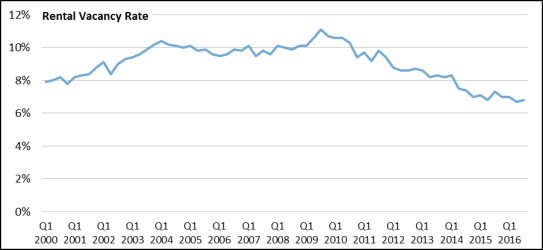

As shown in Figure 11, on a national basis the rental vacancy rate was over 10% in most quarters from 2008 through 2010. Since then, the rate has steadily declined, reaching about 8% at the end of 2013 and 7% at the end of both 2014 and 2015. At the end of 2016, the rental vacancy rate was 6.9%.18

|

Figure 11. Rental Vacancy Rates Q1 2000-Q4 2016 |

|

|

Source: Figure created by CRS based on data from U.S. Census Bureau, Housing Vacancies and Homeownership Historical Tables, Table 1, "Quarterly Rental Vacancy Rates: 1956 to Present," http://www.census.gov/housing/hvs/data/histtabs.html. |

Rental Housing Affordability

Decreasing vacancy rates tend to lead to an increase in rents. Harvard University's Joint Center for Housing Studies reports that rents have generally been increasing in recent years at a rate that outpaces inflation.19 Rising rents can contribute to housing affordability problems, particularly for households with lower incomes.

Under one common definition, housing is considered to be affordable if a household is paying no more than 30% of its income in housing costs. Under this definition, households that pay more than 30% are considered to be cost-burdened, and those that pay more than 50% are considered to be severely cost-burdened.

According to the Joint Center for Housing Studies, citing American Community Survey data, the overall number of cost-burdened households increased slightly in 2014 to 39.8 million, compared to 39.6 million in 2013. However, this represented a decrease from 40.9 million households in 2012.

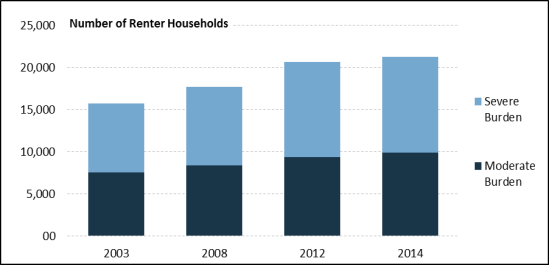

The number of cost-burdened renter households increased to 21.3 million, compared to 20.8 million in 2013 and 20.6 million in 2012. This represents close to half of all households who rent.20 Not surprisingly, cost burdens are more common among lower-income households. Minority households are more likely to be cost-burdened, and affordability problems are particularly prevalent in higher-cost housing markets.21 Figure 12 shows the number of renter households with moderate or severe cost burdens in 2014 and selected previous years.

|

Figure 12. Cost-Burdened Renter Households thousands of households |

|

|

Source: Figure created by CRS based on data in Joint Center for Housing Studies, State of the Nation's Housing reports, Appendix Tables, http://jchs.harvard.edu/research/state_nations_housing. |

Furthermore, according to HUD, 7.7 million renters were considered to have "worst-case housing needs" in 2013 (the most recent data available).22 Households with worst-case housing needs are defined as renters with incomes at or below 50% of area median income who do not receive federal housing assistance and who pay more than half of their incomes for rent, live in severely inadequate conditions, or both.23 The 7.7 million households with worst-case housing needs in 2013 was a decrease from 8.5 million in 2011, but it was 30% higher than the 6 million households with worst-case housing needs in 2007.24

Assisted Housing Issues

A number of the housing issues that the 114th Congress considered had to do with federally assisted housing programs that are intended to provide affordable housing for eligible lower-income households. Most federal housing programs are administered by HUD.

HUD's 50th Anniversary

HUD was created as a Cabinet-level agency by the Housing and Urban Development Act of 1965, which was signed into law by President Lyndon B. Johnson on September 9, 1965. HUD,25 stakeholders,26 researchers,27 the press,28 and Members of Congress29 took the opportunity of HUD's 50th anniversary to reflect on and assess the function of the department to-date and to consider its role in the future. In honor of the anniversary, the chairman of the House Financial Services Committee put out a call for "all interested advocates, organizations, and ordinary citizens to join the effort to modernize the delivery of federal housing assistance and submit their ideas on how to restructure and rebuild HUD for today's generation."30 Subsequently, the committee held a hearing entitled "The Future of Housing in America: 50 Years of HUD and its Impact on Federal Housing Policy."31

Appropriations for Housing Assistance Programs

Concern in Congress about federal budget deficits has led to increased interest in reducing the amount of discretionary funding provided each year through the annual appropriations process. The desire to limit discretionary spending has implications for HUD's budget, the largest source of funding for direct housing assistance, because it is made up almost entirely of discretionary appropriations.

More than three-quarters of HUD's appropriations are devoted to three programs: the Section 8 Housing Choice Voucher (HCV) program, Section 8 project-based rental assistance, and the public housing program. Funding for Section 8 vouchers makes up the largest share of HUD's budget, accounting for nearly half. The cost of the Section 8 voucher program has been growing in recent years. This is in part because Congress has created more vouchers each year over the past several years (largely to replace units lost to the affordable housing stock in other assisted housing programs or to provide targeted assistance for homeless veterans), and in part because the cost of renewing individual vouchers has been rising as gaps between low-income tenants' incomes and rents in the market have been growing.32

The cost of Section 8 project-based rental assistance has also been growing in recent years as more and more long-term rental assistance contracts on older properties expire and are renewed, requiring new appropriations.33 Public housing, the third-largest expense in HUD's budget, has, arguably, been underfunded (based on studies undertaken by HUD of what it should cost to operate and maintain public housing)34 for many years. As a result, there is regular pressure from low-income housing advocates and others to increase funding for public housing.

In a budget environment featuring limits on discretionary spending, the pressure to provide more funding for HUD's largest programs must be balanced against the pressure from states, localities, and advocates to maintain or increase funding for other HUD programs, such as the Community Development Block Grant (CDBG) program, grants for homelessness assistance, and funding for Native American housing.

Further, HUD's funding needs must be considered in the context of those for the Department of Transportation (DOT). Funding levels for both departments are determined by the Transportation, HUD, and Related Agencies (THUD) appropriations subcommittee, generally in a bill by the same name. While HUD's budget is generally smaller than DOT's, it makes up the largest share of the discretionary funding in the THUD appropriations bill each year because the majority of DOT's budget is made up of mandatory funding.

All of these considerations influenced the 114th Congress's consideration of HUD appropriations.

For more information about trends in HUD funding, see CRS Report R42542, Department of Housing and Urban Development (HUD): Funding Trends Since FY2002, by Maggie McCarty; for the current status of HUD appropriations and related CRS reports, see the CRS Appropriations Status Table.

Assisted Housing Reform

Over most of the past 10 years, Congress has considered reforms to the nation's largest direct housing assistance programs: the Section 8 Housing Choice Voucher, Section 8 project-based rental assistance, and public housing programs. These programs combined serve approximately 4.5 million families, including families headed by individuals who are elderly or have disabilities, as well as families with and without children. The majority of the proposed reforms are aimed at streamlining administration of the programs, although some have been farther reaching than others. Recent reform proposals, including those considered but not enacted in the 111th and 112th Congresses, have included a number of fairly noncontroversial administrative provisions, along with others that have proved more controversial.

The Section 8 Housing Choice Voucher program is HUD's largest direct housing assistance program for low-income families, both in terms of the number of families it serves (over 2 million) and the amount of money it costs (over $19 billion in FY2015, over 40% of HUD's appropriation). The program is administered at the local level, by public housing authorities (PHAs), and provides vouchers—portable rental subsidies—to very low-income families. They can use the vouchers to reduce their rents in the private market units of their choice (subject to certain cost limits). The program has been criticized for, among other issues, its administrative complexity—particularly income eligibility and rent policies—and growing cost.35

Project-based rental assistance involves contracts between HUD and private property owners for over 1 million units of affordable housing. Under the terms of those contracts, the property owners receive federal subsidies in exchange for agreeing to lease their units at affordable rents to eligible low-income tenants. Recent reform proposals have called for similar administrative streamlining (involving income eligibility and rent policies) as well as incentives to encourage owners to continue to participate in the program, and enhanced protections for tenants when owners exit the program.

The public housing program has existed longer than either Section 8 program but is now smaller in size, with approximately 1 million units of low-rent public housing available to eligible low-income tenants. Public housing is owned by the same local PHAs that administer the Section 8 voucher program and those PHAs receive annual operating and capital funding from Congress through HUD. Much of the public housing stock is old and in need of capital repairs. According to the most recent study conducted by HUD, addressing the outstanding physical needs of the public housing stock would cost nearly $26 billion.36 The amount Congress typically provides in annual appropriations for capital needs has not been sufficient to address that backlog. In response, PHAs have increasingly relied on other sources of financing, particularly private market loans, to meet the capital needs of their housing stock, including by converting their public housing properties to Section 8 assistance through the Rental Assistance Demonstration.37 Like the two Section 8 programs, the public housing program has been criticized for being overly complex and burdensome to administer, especially in light of recent funding reductions.

Recent reform proposals have included changes to the income eligibility and rent determination process for all three programs, designed to make it less complicated, and changes to the physical inspection process in the voucher program to give PHAs more options for reducing the frequency of inspections and increasing sanctions for failed inspections. Recent reform proposals have also sought to modify and expand the Moving to Work (MTW) demonstration. MTW permits a selected group of PHAs to seek waivers of most federal rules and regulations governing the Section 8 voucher program and the public housing program in pursuit of three statutory purposes: reduce program costs and achieve greater cost effectiveness; provide work incentives and supports for families with children; and increase housing choices for families. The future of MTW and whether it should be expanded has proven to be one of the more controversial elements of assisted housing reform.

No major reform legislation was considered in the 113th Congress. However, the President requested, in his annual budget submissions, that Congress enact several of the less controversial administrative reforms (e.g., those related to income calculation and verification) as part of the annual appropriations acts. The FY2014 Omnibus funding measure (P.L. 113-76) and the FY2015 HUD appropriations law (P.L. 113-235) included several of the requested administrative reforms.38 The FY2016 appropriations law (P.L. 114-113) contained a more controversial provision: an expansion of the MTW demonstration by 100 agencies.

Early in the 114th Congress, several relatively noncontroversial administrative reform bills were approved by the House, including the Tenant Income Verification Relief Act of 2015 (H.R. 233), to allow PHAs and owners of federally assisted housing to recertify fixed-income families' incomes only once every three years instead of annually; and the Preservation Enhancement and Savings Opportunity Act of 2015 (H.R. 2482), to allow the owners of certain Section 8 project-based rental assistance properties to access property reserves, subject to certain limitations. These bills, and others, were enacted into law as part of the Surface Transportation Reauthorization and Reform Act of 2015 (P.L. 114-94).39

Late in the first session of the 114th Congress, the chairman of the Housing and Insurance Subcommittee of the House Financial Services Committee introduced the Housing Opportunity through Modernization Act of 2015 (H.R. 3700), which was co-sponsored by the ranking member of the subcommittee. It included a number of reforms related to administrative streamlining—including changes to income definition and review policies for all three primary assisted housing programs, changes to Section 8 voucher inspection procedures, and increased flexibility in public housing funding—that were similar to consensus provisions from earlier reform bills, among other provisions. It did not include some of the more controversial provisions from prior reform bills, such as a further expansion of the MTW demonstration. It was approved unanimously by the House on February 2, 2016. The Senate approved the bill via unanimous consent on July 14, 2016, and President Obama signed it into law on July 29, 2016 (P.L. 114-201). For more information on H.R. 3700, see CRS Report R44358, Housing Opportunity Through Modernization Act (H.R. 3700), by Maggie McCarty, Libby Perl, and Katie Jones.

Native American Housing Assistance and Self-Determination Act Reauthorization

The Native American Housing Block Grant (NAHBG) is the main federal program that provides housing assistance to Native American tribes and Alaska Native villages. It provides formula funding to tribes to use for a range of affordable housing activities that benefit low-income Native Americans or Alaska Natives living in tribal areas. The NAHBG is authorized by the Native American Housing Assistance and Self-Determination Act of 1996 (NAHASDA), which reorganized the federal system of housing assistance for tribes while recognizing the rights of tribal self-governance and self-determination. The most recent authorization for most NAHASDA programs expired at the end of FY2013, although these programs have generally continued to be funded through annual appropriations laws.

Although the 113th Congress considered reauthorization legislation, none was enacted. In the 114th Congress, both the House and the Senate again considered NAHASDA reauthorization bills. The House passed a NAHASDA reauthorization bill (H.R. 360) in March 2015, while in the Senate a different bill (S. 710) was reported out of committee.

Among other things, both H.R. 360 and S. 710 would have reauthorized the NAHBG and the Native Hawaiian Housing Block Grant, which provides housing assistance to low-income Native Hawaiians, as well as two home loan guarantee programs that benefit Native Americans and Native Hawaiians, respectively. Both bills would have also made some changes to NAHBG program requirements, authorized a demonstration program intended to increase private financing for housing activities in tribal areas, and authorized a program to provide housing vouchers and supportive services for Native American veterans who are homeless or at risk of homelessness.40 In response to concerns about certain tribes not spending their NAHBG funds in a timely fashion, both bills also included a provision to reduce funding to tribes with annual allocations of $5 million or more who have large balances of unexpended NAHBG funds. (The vast majority of tribes receive annual allocations below $5 million.)

Although the House and Senate bills were similar in many ways and addressed many of the same issues, they were not identical. Each bill contained some provisions not included in the other, and in some cases the bills addressed the same issue in different ways. Furthermore, while tribes and Congress are generally supportive of NAHASDA, there has been some disagreement in Congress over specific provisions or policy proposals that have been included in reauthorization bills. Ultimately, no NAHASDA reauthorization legislation was enacted during the 114th Congress.

For more information on NAHASDA and the NAHBG in general, see CRS Report R43307, The Native American Housing Assistance and Self-Determination Act of 1996 (NAHASDA): Background and Funding, by Katie Jones. For more information on reauthorization efforts in the 114th Congress, see CRS Report R44261, The Native American Housing Assistance and Self-Determination Act (NAHASDA): Issues and Reauthorization Legislation in the 114th Congress, by Katie Jones.

Funding for the Housing Trust Fund and Capital Magnet Fund

In 2008, Congress established two new affordable housing funds in the Housing and Economic Recovery Act (HERA, P.L. 110-289):

- The Housing Trust Fund is a HUD program that is intended to provide dedicated federal funding for affordable housing activities, with a focus on the production of rental housing for very low- and extremely low-income households. The funding is provided to states via formula.

- The Capital Magnet Fund is a Treasury program, administered by the Community Development Financial Institutions (CDFI) Fund, that is intended to provide competitive funding for affordable housing activities to CDFIs and other eligible nonprofit organizations.41 The Capital Magnet Fund can be used for a broader range of affordable housing activities than the Housing Trust Fund.

Rather than being funded through the annual appropriations process, the Housing Trust Fund and the Capital Magnet Fund are funded through contributions from Fannie Mae and Freddie Mac. However, Fannie Mae and Freddie Mac were placed into conservatorship in 2008 shortly after P.L. 110-289 was enacted, and their regulator suspended the contributions to the funds before they ever started. For several years following 2008, the Housing Trust Fund was not funded. The Capital Magnet Fund was funded once, through a one-time discretionary appropriation in FY2010.

In December 2014, Fannie Mae's and Freddie Mac's regulator directed them to begin setting aside funds for the Housing Trust Fund and Capital Magnet Fund for the first time during calendar year 2015.42 The first contributions were transferred to the funds in early 2016. HUD announced the first Housing Trust Fund allocations to states in May 2016,43 and the CDFI Fund announced competitive grant awards through the Capital Magnet Fund in September 2016.44

These affordable housing funds, particularly the Housing Trust Fund, have been controversial. Supporters argue that these funds are necessary to address a pressing need for an increased supply of affordable rental housing for the poorest households.45 Supporters also argue that a benefit of these programs is that they are funded outside of the annual appropriations process, meaning that they are less likely to compete with other housing programs for funding.46 Critics raise a number of concerns, including arguing that these funds are duplicative of other housing programs and that providing funding outside of the appropriations process limits Congress's role in overseeing them.47 Further, opponents argue that Fannie Mae and Freddie Mac should not be diverting funds to the Housing Trust Fund or Capital Magnet Fund while they remain in conservatorship, and that the programs could become "slush funds" for favored political groups despite limitations on the uses of funds.48

Given these concerns, some Members of Congress have sought to stop Fannie Mae and Freddie Mac from funding the Housing Trust Fund and/or the Capital Magnet Fund. For example, in the 114th Congress, the Pay Back the Taxpayers Act (H.R. 574) would have prohibited Fannie Mae and Freddie Mac from contributing to either fund while Fannie and Freddie remain in conservatorship. The bill was not enacted. Additionally, the FY2016 HUD appropriations bill that passed the House (H.R. 2577) would have diverted any funds intended for the Housing Trust Fund (but not the Capital Magnet Fund) in FY2016 to HUD's HOME program instead.49 That provision was not included in the final FY2016 HUD appropriations law.

For more information on the Housing Trust Fund, see CRS Report R40781, The Housing Trust Fund: Background and Issues, by Katie Jones.

Homeownership and Mortgage Finance Issues

Other issues that the 114th Congress considered were related to the housing finance system and the ability of households to obtain mortgages.

Fannie Mae and Freddie Mac

Fannie Mae and Freddie Mac are two government-sponsored enterprises (GSEs) that were created by Congress to support homeownership. By law, Fannie Mae and Freddie Mac cannot make mortgages; rather, they are restricted to purchasing mortgages that meet certain requirements from lenders.50 Once the GSEs purchase a mortgage, they either package it with others into a mortgage-backed security (MBS), which they guarantee and sell to institutional investors, or retain it as a portfolio investment.

In 2008, during the housing and mortgage market turmoil, Fannie Mae and Freddie Mac entered voluntary conservatorship overseen by their regulator, the Federal Housing Finance Agency (FHFA). As part of the legal arrangements of this conservatorship, the Treasury Department contracted to purchase up to $200 billion of new senior preferred stock from each of the GSEs. To date, Treasury has purchased a total of nearly $188 billion of senior preferred stock from the two GSEs and has received a total of $251 billion in dividends.51 These funds become general revenues. Since June 2012, neither GSE has needed additional support from Treasury.

Many policymakers agree on the need for comprehensive housing finance reform legislation that would transform or eliminate the GSEs' role in the housing finance system. While there is broad agreement on certain principles of housing finance reform—such as increasing the private sector's role in the mortgage market and maintaining access to affordable mortgages—there is much disagreement over the details. The 113th Congress considered, but did not enact, housing finance reform legislation.

There was less movement toward comprehensive housing finance reform in the 114th Congress. However, the 114th Congress considered legislation that would make certain specific, more-targeted reforms to the GSEs. Some of these proposed reforms focused on the terms of the GSEs' conservatorship, while others attempted to advance some of the larger goals of housing finance reform, such as increasing the role of private capital in the housing finance system. Specifically, legislation was introduced in the 114th Congress to restrict the use of the GSEs' dividends paid to Treasury to offset other spending, prevent Treasury from disposing of the senior preferred stock without enabling legislation, and limit executive compensation at the GSEs. Legislation was also proposed to mandate that the GSEs share mortgage risks with the private sector, and to encourage improvements to the secondary mortgage market through a common platform for mortgage securitization. Each of these issues is discussed in turn.

GSE Profits

When the GSEs purchase a mortgage, they charge the seller a fee for guaranteeing timely payment of principal and interest to the ultimate investor. Unless offset by reduced mortgage purchases or increased losses due to foreclosure, increasing guarantee fees increases GSE profits.52 Under the terms of Treasury's support agreements, all of the GSEs' profits from whatever sources53—including those arising from increased guarantee fees—are paid as dividends to Treasury.

In recent years, Congress has sometimes used, or proposed to use, a portion of the increases to these fees as offsets for other types of government spending. In particular, the Temporary Payroll Tax Cut Continuation Act of 2011 (P.L. 112-78) directed FHFA to increase the GSEs' guarantee fees through 2021 and use the increase to offset the cost of extending the payroll tax cut. More recently, other bills have proposed extending the guarantee fee increase as a "pay for" to offset spending, though legislation that would do so has not been enacted.54 Some have opposed the use of GSE fees to fund other activities, arguing that raising fees unnecessarily increases costs for mortgage borrowers. Others have raised concerns that the ability to use GSE fees as offsets for other spending could reduce enthusiasm for broader housing finance reform.

The Financial Regulatory Improvement Act of 2015 (S. 1484)55 would have prohibited the use of the GSEs' guarantee fees in scoring appropriations under the Congressional Budget Act of 1974 (P.L. 93-344).56 The bill contained two exceptions. First, the fees could have been scored if they resulted from the disposition of the senior preferred stock. Second, the fees could have been scored if the proceeds were used to finance reforms of the secondary mortgage market.57

Fannie Mae's and Freddie Mac's support agreements with Treasury require the GSEs to reduce their capital buffer each year until it is eliminated on January 1, 2018. Both FHFA Director Melvin L. Watt58 and Fannie Mae President and CEO Timothy J. Mayopoulos59 have said that after January 1, 2018, any losses would require the GSEs to draw down support agreement funds at Treasury. Fannie Mae has $117.6 billion60 and Freddie Mac has $140.5 billion61 available to draw from Treasury under the support agreement.

Treasury to Hold Senior Preferred Stock Indefinitely

The Consolidated Appropriations Act, 2016 (P.L. 114-113) included provisions that restrict the Secretary of the Treasury from disposing of the senior preferred stock unless future legislation authorizing such action is signed into law.62 This could give Congress input into the future of the GSEs.

Technically, the GSEs' conservatorship and the senior preferred stock are separate issues. The conservatorship could be ended and control returned to the common stockholders without disposing of the senior preferred stock. As a practical matter, it is hard to find any significant value to a company that must pay all its profits to the government. Moreover, the agreements with Treasury that require all profits to be paid to Treasury as dividends prevent the GSEs from accumulating reserves to offset losses greater than quarterly earnings. Under conservatorship, the Treasury's support agreements are substitutes for such reserves. These agreements are unlikely to continue in effect if the GSEs are not in conservatorship.

In addition, any change to the status of the GSEs would have to consider the warrants (a type of option) that Treasury can use to purchase control of each of the GSEs at nominal cost. On other occasions when the federal government has provided significant financial support to companies, such as Chrysler and General Motors, Treasury has auctioned off similar warrants at a profit.

Executive Compensation

In July 2015, FHFA approved Fannie Mae's and Freddie Mac's requests to raise the annual target compensation of their chief executive officers to $4 million from $600,000. The Equity in Government Compensation Act of 2015 (P.L. 114-93), enacted in November 2015, reduced the maximum executive compensation to $600,000.

Risk Sharing

In 2012, FHFA directed Fannie Mae and Freddie Mac to develop programs to share mortgage credit risk with the private sector, which would reduce the risk they impose on the federal government. Both of the GSEs have developed programs under which they, in effect, purchase insurance from the private sector.63 S. 148464 would have encouraged these programs by codifying them.

Common Securitization Platform

Fannie Mae and Freddie Mac each issue their own MBS, which differ from each other. FHFA has determined that both GSEs' computer systems supporting the MBSs must be modernized and that it would improve the efficiency of the secondary mortgage market if the GSEs adopted a common MBS. This MBS system modernization is being developed by a jointly owned subsidiary known as Common Securitization Solutions (CSS). Freddie Mac issued MBS implementing the common securitization platform (CSP) release 1 in December 2016.65 Both GSEs are expected to issue MBS implementing CSP release 2 in 2018.66

S. 1484 would have directed FHFA to expand access to CSS to other private MBS issuers besides the GSEs.67 It would have required reports to Congress, revised the composition of the CSS board of directors, established a timetable for issuing the new type of MBS, and restricted the risks that CSS can take.

Oversight of Mortgage-Related Rulemakings

Financial regulators are continuing to implement mortgage-related rulemakings that are part of the financial reforms implemented in response to the bursting of the housing bubble and the ensuing housing and mortgage market turmoil. The Consumer Financial Protection Bureau (CFPB) has issued rules related to, among other things, the ability to repay and qualified mortgage (QM) standards, homeownership counseling, escrow requirements, mortgage servicing, loan originator compensation, and mortgage disclosure forms.68 Federal bank regulators have issued rules that affect banks' holdings of mortgage-related assets. In addition, six federal agencies issued a final rule for credit risk retention and qualified residential mortgages (QRM).69 Regulators have issued additional mortgage-market rules besides those mentioned above.

While each of the rules is different, the 114th Congress focused on several policy issues that are common among them. First, some are concerned about the regulatory burden lenders face in satisfying the new rules, especially small lenders.70 Others argue, however, that the benefits associated with the new regulations, such as enhanced protections for consumers and promoting stability in the housing finance system, justify the higher costs on lenders. Second, some in Congress question how the rules will affect credit availability for creditworthy borrowers. As discussed earlier in the "Overview of Housing and Mortgage Market Conditions" section, mortgage originations and home sales are at relatively low levels and mortgage credit is relatively tight compared to the early 2000s, and some argue that the new regulations have contributed to the slow recovery. Others contend, however, that the regulations are intended to prevent those unable to repay their loans from receiving credit and have been appropriately tailored to ensure that those who can repay are able to receive credit.

The 114th Congress considered these and other policy concerns in its oversight of the financial regulators through many different hearings and by acting on legislation. In the Senate, the Senate Banking Committee reported the Financial Regulatory Improvement Act of 2015 (S. 1484).71 S. 1484 encompassed a broad package of reforms to the financial regulatory system, including several sections that would have modified mortgage-related rulemakings. S. 1484 included provisions related to, among other things, the QM rule, appraisals, manufactured housing, and the Federal Home Loan Banks.72

In the House, the Financial Services Committee reported numerous pieces of legislation that would have also modified some of the mortgage-market rulemakings. The bills covered, among other things, manufactured housing, the QM rule, escrow accounts, mortgage servicing, and mortgage disclosures. Several of these bills passed the House, such as the Preserving Access to Manufactured Housing Act of 2015 (H.R. 650) and the Mortgage Choice Act of 2015 (H.R. 685). Many of the proposals to modify mortgage-related rulemakings that received floor or committee action were also included in the Financial CHOICE Act (H.R. 5983), a wide-ranging package of proposals that would have reformed many aspects of the financial system.73 The Financial CHOICE Act was reported by the Financial Services Committee on September 13, 2016.

For more information on some of the legislative proposals to modify mortgage-related rulemakings in the 114th Congress, see CRS Report R44035, "Regulatory Relief" for Banking: Selected Legislation in the 114th Congress, coordinated by Sean M. Hoskins.

The Federal Housing Administration

The Federal Housing Administration (FHA), part of HUD, insures certain mortgages made by private lenders against the possibility that the borrower will not repay the mortgage as promised. The insurance protects the lender, rather than the borrower, in the case of borrower default. FHA insurance can make mortgages more easily available to some households that might otherwise have difficulty qualifying for an affordable mortgage, such as those with small down payments.

FHA is intended to be self-supporting: fees paid by borrowers are meant to cover the costs of defaults. However, for the last several years there have been concerns about FHA's finances. By law, FHA is required to maintain a capital ratio of 2%. The capital ratio fell below 2% in FY2009 and remained below that level until it again reached the 2% threshold at the end of FY2015.74 Concerns about FHA's finances culminated when FHA received a mandatory appropriation from Treasury at the end of FY2013 to ensure that it had sufficient funds to cover all of its anticipated future costs. Since that time, FHA's finances have improved (as evidenced by the capital ratio again reaching the 2% threshold), although concerns remain.

There is often a tension between FHA's mission of expanding access to affordable mortgage credit and its need to protect its finances. This tension was highlighted in January 2015, when FHA announced that it was reducing the fees that it charges to borrowers for mortgage insurance.75 Many industry and consumer groups had urged such a decision, noting that lowering the fees would make mortgages more affordable for many prospective homebuyers, and that the decrease could protect FHA's insurance fund by making FHA insurance more attractive for higher-quality borrowers.76 However, critics argued that lowering the fees could impede FHA's ability to rebuild its finances by reducing its revenue or underpricing its risk.77

FHA has also been taking steps intended to provide more clarity to lenders about FHA's requirements and under what circumstances FHA would take administrative or legal actions against lenders for not meeting those requirements. In recent years, many have argued that FHA's requirements have not been clear enough, and that lenders fear FHA will pursue significant enforcement actions against them for what they consider to be minor violations of requirements.78 This, in turn, can make lenders less willing to offer FHA-insured mortgages, or to only offer such mortgages to a narrow subset of borrowers who are the least likely to default on their mortgages.

To address these concerns, FHA has been in the process of consolidating its loan requirements in a new handbook, making changes to certifications that lenders must submit to FHA to participate in FHA insurance programs, and updating metrics that measure lenders' performance. Though these changes collectively are intended to provide more clarity to lenders, and in turn expand access to FHA-insured mortgages, some industry groups and others have argued that some of these changes have not gone far enough in providing lenders with additional certainty.79 On the other hand, some in Congress have raised concerns that certain changes, such as the changes to the lender certifications, could make it more difficult for FHA to hold lenders accountable.80

For more information on FHA-insured mortgages in general, see CRS Report RS20530, FHA-Insured Home Loans: An Overview, by Katie Jones. For more information on FHA's financial status, see CRS Report R42875, FHA Single-Family Mortgage Insurance: Financial Status of the Mutual Mortgage Insurance Fund (MMI Fund), by Katie Jones.

FHA and GSE Distressed Loan Sales

Over the past few years, Fannie Mae and Freddie Mac (the GSEs) and FHA have implemented initiatives to sell pools of distressed mortgages to outside investors prior to the foreclosure process being completed.81 This is in contrast to the traditional process of a mortgage servicer foreclosing on a mortgage and then conveying the foreclosed property to the GSEs or FHA, respectively, to market and sell. Loan sales are intended to reduce the losses to FHA and the GSEs by sparing those entities some of the costs of maintaining and marketing a foreclosed property. These sales may also benefit some borrowers, because the investors who purchase the mortgages may be able to offer certain foreclosure prevention options that would not have been allowed under FHA or GSE requirements.

Some policy organizations and advocacy groups, as well as some Members of Congress, have opposed these loan sales entirely or argued that FHA and the GSEs should do more to ensure that sales are structured in a way to benefit more homeowners and contribute to neighborhood stabilization. In particular, some worry that the investors who purchase distressed mortgages do not do enough to attempt to keep borrowers in their homes or to make sure that vacant foreclosed properties do not become blights on communities.82 Among other things, critics of these loan sales have argued that more loans should be sold to nonprofit organizations that may be more committed to keeping borrowers in their homes and that other steps should be taken to protect borrowers.

Both FHA and the GSEs have made some changes to their loan sales programs, including adopting some measures called for by advocates.83 While some argue that these changes have not gone far enough, others have expressed concerns that some of the changes could decrease the prices that investors are willing to pay for the loans and therefore limit the extent to which the loan sales result in lower losses for FHA or the GSEs. In light of these concerns, the House Financial Services Committee held a hearing to examine recent changes to FHA's loan sale program in July 2016.84

Fair Housing Issues

Two issues related to fair housing have also prompted congressional interest and were active during the 114th Congress.

Supreme Court Decision on Disparate Impact Claims Under the Fair Housing Act

The Fair Housing Act (FHA) was enacted "to provide, within constitutional limitations, for fair housing throughout the United States."85 It prohibits discrimination on the basis of race, color, religion, national origin, sex, physical and mental handicap, and familial status. Subject to certain exemptions, the FHA applies to all sorts of housing, public and private, including single family homes, apartments, condominiums, and mobile homes. It also applies to "residential real estate-related transactions," which include both the "making [and] purchasing of loans ... secured by residential real estate [and] the selling, brokering, or appraising of residential real property."86

In June 2015, the Supreme Court, in Texas Department of Housing and Community Affairs v. Inclusive Communities Project,87 confirmed the long-held interpretation that, in addition to outlawing intentional discrimination, the FHA also prohibits certain housing-related decisions that have a discriminatory effect88 on a protected class.89 The Supreme Court's holding in Inclusive Communities that "disparate-impact claims are cognizable under the [FHA]" mirrors previous interpretations of the Department of Housing and Urban Development90 (HUD) and all 11 federal courts of appeals91 that had ruled on the issue.

The Supreme Court stressed that lower courts and HUD should rigorously evaluate plaintiffs' disparate impact claims to ensure that evidence has been provided to support not only a statistical disparity but also causality (i.e., that a particular policy implemented by the defendant caused the disparate impact). The Court also emphasized that claims should be disposed of swiftly in the preliminary stages of litigation when plaintiffs have failed to provide sufficient evidence of causality. Although plaintiffs historically have faced fairly steep odds of getting their disparate impact claims past the preliminary stages of litigation, much less succeeding on the merits, the "cautionary standards" emphasized by the Supreme Court might result in even fewer successful disparate impact claims being raised in the courts and swifter disposal of claims that are raised. This could, in turn, discourage claims from being raised at all.

While some in Congress praised the Supreme Court's decision,92 others have opposed the use of disparate impact claims in Fair Housing Act cases. In the 114th Congress, the Protect Local Independence in Housing Act of 2015 (H.R. 3145) was introduced in response to the Inclusive Communities ruling. It would have amended the FHA to make clear that the act does not protect against disparate impact discrimination. Furthermore, a floor amendment to the Commerce, Justice, Science, and Related Agencies Appropriations Act, 2016 (H.Amdt. 337 to H.R. 2578), which passed the House, would have prohibited the Department of Justice from using funds appropriated by the bill from being used to enforce the FHA in a manner that relies on disparate impact discrimination. Similarly, a floor amendment to the Transportation, Housing and Urban Development, and Related Agencies Appropriations Act, 2016 (H.Amdt. 428 to H.R. 2577), which passed the House, would have prohibited HUD from using funds appropriated by the bill "to implement, administer, or enforce" its disparate impact regulations. These provisions were not included in the final FY2016 appropriations law.

For more information, see CRS Report R44203, Disparate Impact Claims Under the Fair Housing Act, by David H. Carpenter.

HUD's Affirmatively Furthering Fair Housing (AFFH) Rule

The Fair Housing Act also requires HUD to administer its programs in a way that affirmatively furthers fair housing.93 Statutes governing the Community Development Block Grant (CDBG) and public and assisted housing programs also require that funding recipients affirmatively further fair housing,94 and, through regulation, jurisdictions receiving formula funds through CDBG, Emergency Solutions Grants (ESG), the Home Investment Partnerships Program, and Housing Opportunities for Persons with AIDS (HOPWA) must affirmatively further fair housing as part of the consolidated planning process.95 These jurisdictions, together with Public Housing Authorities (PHAs), are collectively referred to by HUD as "program participants."

On July 16, 2015, HUD published a rule governing the obligation of program participants to affirmatively further fair housing.96 In general, the requirements of the rule apply to program participants based on the three- or five-year cycle when their Consolidated or PHA Plans are due. The year in which the first AFH is due varies, with entitlement communities receiving CDBG grants greater than $500,000 submitting an AFH as early as 2016, and other grantees and PHAs having later start dates.97 Until implementation of the AFFH rule, program participants have satisfied their obligation to affirmatively further fair housing by certifying to HUD that they conducted an "Analysis of Impediments" (AI) to fair housing and were taking appropriate actions to overcome impediments. A Government Accountability Office analysis of a sample of AIs in 2010 found that many were outdated or lacked content,98 serving in part to prompt HUD to develop its AFFH rule.99 The AFFH rule defines more specifically what it means to affirmatively further fair housing,100 and requires that program participants submit an Assessment of Fair Housing (AFH) to HUD at least every five years. The rule encourages program participants to collaborate and submit joint or regional AFHs both to save time and resources and to approach fair housing from a broader perspective.

Under the AFH, program participants are to assess their jurisdictions and regions for fair housing issues, specifically, areas of segregation or lack of integration, racially or ethnically concentrated areas of poverty, significant disparities in access to opportunity, and disproportionate housing needs. Program participants identify factors that contribute to these fair housing issues and set priorities and goals for overcoming the effects of the contributing factors. Program participants are to include strategies and actions to achieve their goals in their Consolidated and PHA Plans. HUD provides data for program participants to use in preparing their AFHs, and has developed tools that help program participants through the AFH process. In addition, the AFH requires public participation, and, unlike the AI, program participants must submit and have their AFHs approved by HUD.

When HUD released its proposed AFFH rule describing the new process on July 19, 2013, it received more than 1,000 comments. Some commenters expressed support for the rule as a way to increase housing opportunity and attain the goals of the Fair Housing Act.101 Opponents of the AFFH rule contended that it intrudes on local jurisdictions' authority and constitutes social engineering.102 Other concerns about the rule include the potential cost of preparing AFHs, especially for small jurisdictions and PHAs; whether investment in racially and ethnically concentrated areas of poverty could be prioritized; the fact that program participants may be unable to change the conditions affecting fair housing; and uncertainty about how HUD will enforce the rule.

In the 114th Congress, proposed legislation, including appropriations language, would have kept HUD from implementing the AFFH rule. For example, the Local Zoning Decisions Protection Act of 2015 (S. 1909) would have prohibited federal funds from being used to administer, implement, or enforce the AFFH rule, and from being used to maintain a database containing information on community racial disparities or disparities in access to housing. In addition, the House amended its version of the FY2016 Departments of Transportation and Housing and Urban Development appropriations act (H.Amdt. 399 to H.R. 2577) to prohibit funds appropriated by the bill from being used to carry out the AFFH rule. Such a provision was not included in the final FY2016 HUD appropriations law. Further, when the Senate considered the FY2017 HUD funding bill (also H.R. 2577), an amendment to withhold funding was proposed (S.Amdt. 3897), but ultimately tabled. Instead, an amendment was adopted that would have prevented HUD from using funds to direct grantees to make specific changes to their zoning laws as part of enforcing the AFFH rule (S.Amdt. 3970). As of the date of this report, FY2017 appropriations had not been finalized, and funding was provided pursuant to a continuing resolution.

For more information about the AFFH rule and HUD Fair Housing programs, see CRS Report R44557, The Fair Housing Act: HUD Oversight, Programs, and Activities, by Libby Perl.

Housing-Related Tax Extenders

In the past, Congress has regularly extended a number of temporary tax provisions addressing a variety of policy issues, including housing. This set of temporary provisions is commonly referred to as "tax extenders." Congress last passed tax extenders legislation on December 18, 2015, via Division Q of P.L. 114-113—the Protecting Americans from Tax Hikes Act (or "PATH" Act).

Tax Exclusion for Canceled Mortgage Debt

Historically, when all or part of a taxpayer's mortgage debt has been forgiven, the amount canceled has been included in the taxpayer's gross income.103 This income is typically referred to as canceled mortgage debt income. The borrower will realize ordinary income to the extent the canceled mortgage debt exceeds the value of any money or property given to the lender in exchange for cancelling the debt. For example, such exchanges are common in a "short sale" when the lender allows the borrower to sell the home for less than the remaining amount owed on the mortgage and may forgive the remaining debt. Lenders report canceled debt to the Internal Revenue Service (IRS) using Form 1099-C. A copy of the 1099-C is also sent to the borrower, who generally must include the amount listed as gross income in the year of discharge.

The Mortgage Forgiveness Debt Relief Act of 2007 (P.L. 110-142), signed into law on December 20, 2007, temporarily excluded qualified canceled mortgage debt income that is associated with a primary residence from taxation. Thus, the act allowed taxpayers who did not qualify for one of several existing exceptions to exclude canceled mortgage debt from gross income. The provision was originally effective for debt discharged before January 1, 2010, and was subsequently extended several times.104 Most recently, the PATH Act extended the exclusion through the end of 2016. The act also allows for debt discharged after 2016 to be excluded from income if the taxpayer entered into a binding written agreement before January 1, 2017.

The rationales for extending the exclusion are to minimize hardship for households in distress and lessen the risk that non-tax homeownership retention efforts are thwarted by tax policy. It may also be argued that extending the exclusion would continue to assist the recoveries of the housing market and overall economy. Opponents of the exclusion may argue that extending the provision would make debt forgiveness more attractive for homeowners, which could encourage homeowners to be less responsible about fulfilling debt obligations. The exclusion may also be viewed as unfair, as its benefits depend on whether or not a homeowner is able to negotiate a debt cancelation, the income tax bracket of the taxpayer, and whether or not the taxpayer retains ownership of the house following the debt cancellation.

The Joint Committee on Taxation (JCT) estimated the two-year extension included in the PATH Act would result in a 10-year revenue loss of $5.1 billion.105