Introduction

U.S. insurers and Congress face new policy issues and questions related to the opportunities and risks presented by the growth in the international insurance market and trade in insurance products.

Insurance is often seen as a localized product and U.S. insurance regulation has addressed this through a state-centric regulatory system. The McCarran-Ferguson Act,1 passed by Congress in 1945, gives primacy to the individual states, and every state has its own insurance regulator and state laws governing insurance. Although the risks of loss and the regulation may be local, the business of insurance, as with many financial services, has an increasingly substantial international component as companies look to grow and diversify.

The international aspects of insurance have spurred the creation of a variety of entities and measures, both domestic and foreign, to facilitate the trade and regulation of insurance services. Financial services have been addressed in a number of U.S. trade agreements going back to the North American Free Trade Agreement (NAFTA) in 1994. The International Association of Insurance Supervisors (IAIS) was created more than 20 years ago, largely under the impetus of the U.S. National Association of Insurance Commissioners (NAIC), to promote cooperation and exchange of information among insurance supervisors, including development of regulatory standards. The 2007-2009 financial crisis sparked further international developments, with heads of state of the G-20 nations creating the Financial Stability Board (FSB).

The postcrisis 2010 Dodd-Frank Wall Street Reform and Consumer Protection Act (Dodd-Frank)2 altered the U.S. insurance regulatory system, particularly as it relates to international issues. With the states continuing as the primary insurance regulators, following Dodd-Frank, the Federal Reserve exercised holding company oversight over insurers who owned a bank subsidiary or who were designated for enhanced supervision (popularly known as systemically important financial institutions or SIFIs) by the new Financial Stability Oversight Council (FSOC). The FSOC includes a presidentially appointed, independent voting member with insurance expertise as well as a state regulator as a nonvoting member. The Federal Reserve, already a major actor in efforts at the FSB and the Basel Committee on Banking Supervision,3 thus became a significant insurance supervisor and joined the IAIS shortly thereafter. Dodd-Frank also created a new Federal Insurance Office (FIO). The FIO is not a federal insurance regulator, but is tasked with representing the United States in international fora and, along with the United States Trade Representative (USTR), can negotiate international covered agreements relating to insurance prudential measures. The FIO also became a member of the IAIS and is participating significantly in IAIS efforts to create insurance capital standards.4

The new federal involvement in insurance issues, both domestic and international, has created frictions both among the federal entities and between the states and the federal entities, and has been a subject of both congressional hearings and proposed legislation.

This report discusses trade in insurance services and summarizes the various international entities and agreements affecting the regulation of and trade in insurance. It then addresses particular issues and controversies in greater depth, including the concluded U.S.-EU covered agreement, pending U.S.-UK covered agreement, and issues relating to international insurance standards. It includes an Appendix addressing legislation in the 115th Congress.

International Insurance Trade

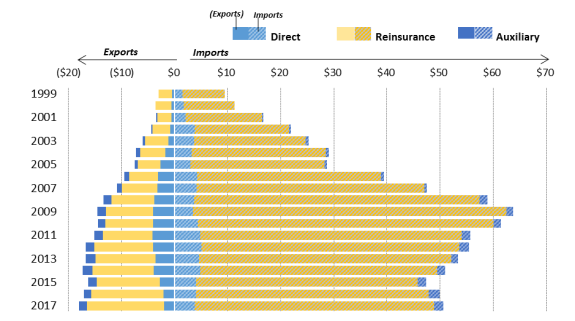

In 2017, total U.S. services accounted for $798 billion of U.S. exports and $542 billion of U.S. imports, creating a surplus of $255 billion. In financial services generally, the United States runs a substantial trade surplus, exporting $110 billion and importing $29 billion. In contrast, the United States imported nearly $51 billion in insurance services and exported $18 billion in 2017, mostly due to firms' reliance on foreign reinsurance.5 This deficit has dropped from its peak in 2009, but U.S. insurance services trade has been consistently in deficit for many years (see Figure 1).

Global performance by insurance brokers and agencies is concentrated, with Europe, North America, and North Asia accounting for 88.6% of total written premiums.6 Overall, the North American and European domestic insurance markets are highly competitive and there are fewer suppliers and less competition in the Asia-Pacific region.7

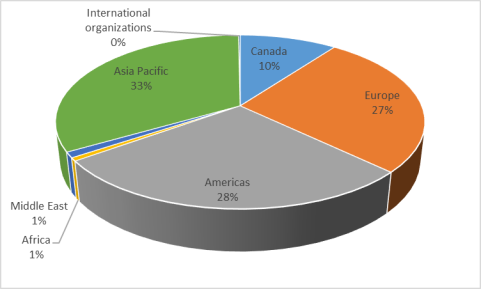

A third of U.S. insurance services exports are with Asia-Pacific, with Japan accounting for 14% of total U.S. insurance exports in 2017 (see Figure 2). Bermuda and the United Kingdom each account for another 15% of U.S. international insurance exports. Industry analysts note that although the current level of trade is relatively low for industry segments such as property, casualty, and direct insurance, it is rising as companies seek new markets for growth and risk diversification. The property casualty market declined from 2013 to 2018, in part due to intensifying natural disasters; however, moving forward, that market is expected to grow due to demand in emerging markets.8

|

|

Source: Bureau of Economic Analysis interactive data tool, October 30, 2018. |

Insurance in U.S. Free Trade Agreements

Services, including financial and insurance services, are traded internationally in accordance with trade agreements negotiated by the USTR on behalf of the United States, similar to trade in goods. As a member of the World Trade Organization (WTO), the United States helped lead the conclusion of negotiations on the General Agreement on Trade in Services (GATS) in 1994, thus creating the first and only multilateral framework of principles and rules for government policies and regulations affecting trade in services among the 164 WTO countries.9 The GATS provides the foundational floor on which rules in other agreements on services, including U.S. free trade agreements (FTAs), are based. Core GATS principles include most-favored nation (MFN), transparency, and national treatment.10 As part of the GATS negotiations, WTO members also agreed to binding market access commitments on a positive list basis in which each member specified the sectors covered by its commitments. For insurance services, the United States submitted its schedule of market access and national treatment commitments, as well as exceptions, under GATS to allow foreign companies to compete in the United States in accordance with the U.S. state-based system.11

The GATS Financial Services Annex applies to "all insurance and insurance-related services, and all banking and other financial services (excluding insurance)." The Annex defines insurance services as follows:

(i.) Direct insurance (including co-insurance):

(A.) life

(B.) non-life

(ii.) Reinsurance and retrocession;

(iii.) Insurance intermediation, such as brokerage and agency;

(iv.) Services auxiliary to insurance, such as consultancy, actuarial, risk assessment and claim settlement services.12

The annex excludes "services supplied in the exercise of governmental authority," such as central banks, Social Security, or public pension plans.13 In the U.S. Schedule of Specific Commitments, the United States lists market access and national treatment limitations that constrain foreign companies' access in line with state laws. These include clarifying which states have no mechanism for licensing initial entry of non-U.S. insurance companies except under certain circumstances and which states require U.S. citizenship for boards of directors.14

Furthermore, the GATS and U.S. FTAs explicitly protect prudential financial regulation. The prudential exception within the GATS allows members to take "measures for prudential reasons, including for the protection of investors, depositors, policy holders or persons to whom a fiduciary duty is owed by a financial service supplier, or to ensure the integrity and stability of the financial system," even if those measures do not comply with the agreement.15

Most U.S. FTAs contain a chapter on financial services that builds on the commitments under GATS ("WTO-plus"). Like GATS, these chapters exclude government-provided public services. In addition to market access, national treatment, and MFN obligations, FTAs include WTO-plus obligations, such as increased transparency by providing interested persons from one party the opportunity to comment on proposed regulations of another party; allowing foreign providers to supply new financial services if domestic companies are permitted to do so; and providing access to public payment and clearing systems. Each FTA chapter defines the specific financial and insurance services covered and incorporates relevant provisions in other FTA chapters, such as Investment and Cross-Border Services.

|

U.S. Insurance Opportunities in China Some U.S. companies have expressed concerns about limited market access to China's growing insurance market due to trade barriers, such as foreign equity caps for establishing Chinese-U.S. joint ventures. Although China announced it would ease some of these restrictions in November 2017, it was a year later, in November 2018, that China acted on its pledge and raised the foreign ownership cap from 50% to 51%. China stated that it would begin to accept applications from foreign insurers for majority control of local joint ventures in early 2019, after guidelines are published. China also agreed to remove all equity caps completely by the end of 2020. |

The Proposed U.S.-Mexico-Canada Agreement

On November 30, 2018, President Trump and the leaders of Canada and Mexico signed the United States-Mexico-Canada Trade Agreement (USMCA) to update and revise the North American Free Trade Agreement (NAFTA).16 Still subject to congressional approval, the proposed USMCA contains several differences from NAFTA and is seen as representing the Trump Administration's approach to trade agreements. The proposed agreement has some similarities and differences from the proposed Trans-Pacific Partnership (TPP), which was negotiated under the Obama Administration and from which the United States withdrew in 2017. Given that the TPP also included both Mexico and Canada, many observers saw it as a template for the NAFTA renegotiations on certain issues.17

Like the TPP, the financial services chapter in the proposed USMCA reflects the growing trade in insurance and is an example of extensive and enforceable "WTO-plus" commitments.18 Compared with NAFTA, the proposed agreement clarifies the coverage of insurance services and contains a specific new provision on expedited availability of insurance services and transparency requirements designed to ensure the use of good regulatory practices to better enable U.S. firms to do business in those markets. In contrast to NAFTA, the proposed USMCA would apply both national treatment and market access obligations to cross-border supply of insurance services.

The USMCA provisions on cross-border data flows are stronger than similar provisions in recent U.S. FTAs. They would, for example, prohibit the use of data or computing localization requirements for financial services.19 Canada would have one year to comply with the ban, and it would need to remove existing localization requirements that have been a trade barrier for U.S. firms seeking to do business in Canada. Many provisions in the USMCA Digital Trade chapter are relevant to the insurance industry, such as permitting electronic signatures, protecting source code and algorithms, promoting cybersecurity, and allowing cross-border data flows.

By contrast, some changes in the investor-state dispute settlement system (ISDS) provide a narrower scope than in TPP or NAFTA, and ISDS would apply only to certain U.S. or Mexican covered investments, excluding Canada completely. Changes in the state-to-state dispute settlement system also may limit its effectiveness for the insurance sector in certain situations. These changes have raised concerns among insurance companies.

Similar to other trade agreements, the proposed USMCA would establish a Committee on Financial Services and provide for consultations between the parties on ongoing implementation and other issues of interest.

Covered Agreements

In comparison to trade agreements, a covered agreement is a relatively new form of an international agreement, established along with the FIO in Title V of the Dodd-Frank Act. The statute defines a covered agreement as a type of international insurance or reinsurance agreement for recognition of prudential measures that the FIO and the USTR negotiate on a bilateral or multilateral basis.20 FIO has no regulatory authority over the insurance industry, which is generally regulated by the individual states. This is a significant contrast to, for example, federal financial regulators, such as the Federal Reserve or the Securities and Exchange Commission (SEC), that might enter into international regulatory agreements at the Basel Committee on Banking Supervision or the International Organization of Securities Commissions, respectively. After such agreements are reached, the Federal Reserve or SEC would generally then implement the agreements under its regulatory authority using the federal rulemaking process.21

Although the FIO lacks regulatory authority, some state laws may be preempted if the FIO director determines that a state measure (1) is inconsistent with a covered agreement and (2) results in less favorable treatment for foreign insurers. The statute limits the preemption with the following provision:

(j) Savings Provisions.—Nothing in this section shall—

(A) any State insurance measure that governs any insurer's rates, premiums, underwriting, or sales practices;

(B) any State coverage requirements for insurance;

(C) the application of the antitrust laws of any State to the business of insurance; or

(D) any State insurance measure governing the capital or solvency of an insurer, except to the extent that such State insurance measure results in less favorable treatment of a non-United State insurer than a United States insurer.22

Further strictures are placed on the FIO determination, including notice to the states involved and to congressional committees; public notice and comment in the Federal Register; and the specific application of the Administrative Procedure Act, including de novo determination by courts in a judicial review.23 Although there is no legal precedent interpreting the covered agreement statute, it appears that these provisions would narrow the breadth of any covered agreement, particularly compared with other international agreements reached by federal financial regulators.24 International agreements have been undertaken without direct congressional direction under agencies' existing regulatory authorities. These authorities are then implemented through the regulatory rulemaking process, which may, in some cases, preempt state laws and regulations. Although the FIO and the USTR must consult with Congress on covered agreement negotiations, the statute does not require specific authorization or approval from Congress for a covered agreement. It does, however, require a 90-day layover period.

Covered Agreements and Trade Agreements: Key Differences

|

Key Differences Between Trade and Covered Agreements

|

Although the goals of a covered agreement and aspects of trade agreements may be similar—market access and regulatory compatibility—the role of Congress is different in each instance. Congress has direct constitutional authority over foreign commerce, while Congress has given itself a consultative role in insurance negotiations through the Dodd-Frank Act.

The U.S. Constitution assigns express authority over foreign trade to Congress. Article I, Section 8, of the Constitution gives Congress the power to "regulate commerce with foreign nations" and to "lay and collect taxes, duties, imposts, and excises." U.S. trade agreements such as the North American Free Trade Agreement (NAFTA), WTO agreements, and bilateral FTAs have been approved by majority vote of each house rather than by two-thirds vote of the Senate—that is, they have been treated as congressional-executive agreements rather than as treaties. This practice contrasts with the covered agreements, defined by Dodd-Frank (see above), which require congressional notification and a 90-day layover. The layover time could give Congress time to act on the agreement if Congress chooses, but congressional action is not required for a covered agreement to take effect. In further contrast, as mentioned previously, international agreements entered into by federal financial regulators, such as the Basel Capital accords in banking, have no specific congressional notification requirements, but must be implemented through the rulemaking process.

Trade Promotion Authority

U.S. bilateral, regional, and free trade agreements are conducted under the auspices of Trade Promotion Authority (TPA).25 TPA is the time-limited authority that Congress uses to set U.S. trade negotiating objectives, establish notification and consultation requirements, and allow implementing bills for certain reciprocal trade agreements to be considered under expedited procedures, provided certain statutory requirements are met.26

As noted above, the Dodd-Frank Act requires that the FIO or the Treasury Secretary and the USTR notify and consult with Congress before and during negotiations on a covered agreement. In addition, it requires the submission of the agreement and a layover period of 90 days, but does not require congressional approval.

By contrast, legislation implementing FTAs must be approved by Congress. Under TPA, the President must fulfill notification and consultative requirements in order to begin negotiations and during negotiations. Once the negotiations are concluded, the President must notify Congress 90 days prior to signing the agreement. After the agreement is signed, there are additional reporting requirements to disclose texts and release the U.S. International Trade Commission's economic assessment of the agreement. The introduction of implementing legislation sets off a 90-legislative-day maximum period of time for congressional consideration, and the legislation is accompanied by additional reports. If these notification and consultation procedures are not met to the satisfaction of Congress, procedures are available to remove expedited treatment from the implementing legislation.

State Role

As discussed above, the FIO and the USTR jointly negotiate covered agreements, with the states having a consultative role set in the statute. In international trade agreements the USTR is the lead U.S. negotiator, with representatives from executive branch agencies participating to provide expertise. In addition to consultations within the executive branch under an interagency process, USTR formally consults with state governments and regulators through the Intergovernmental Policy Advisory Committee on Trade (IGPAC) as part of the USTR advisory committee system for trade negotiations. USTR's Office of Intergovernmental Affairs and Public Engagement (IAPE) manages the advisory committees and provides outreach to official state points of contact, governors, legislatures, and associations on all trade issues of interest to states.27

The USTR cannot make commitments on behalf of U.S. states in trade negotiations. This can be a source of frustration for negotiating partners who seek market openings at the state level. As part of trade negotiations, USTR may try to persuade individual states to make regulatory changes, but USTR is limited to what state regulators voluntarily consent to do. In general, state laws and state insurance regulations are explicitly exempted from trade negotiations. For example, in the proposed USMCA agreement, the United States listed measures for which the FTA obligations would not apply, including "All existing non-conforming measures of all states of the United States, the District of Columbia, and Puerto Rico."28 In contrast, as explained above, in the context of a covered agreement, FIO and USTR may make limited commitments that result in preempting some state laws and regulations.

Enforcing Trade Agreements and Covered Agreements

In general, international trade agreements are binding agreements. If a party to a trade agreement believes another party has adopted a law, regulation, or practice that violates the commitments under the trade agreement, the party may initiate dispute settlement proceedings under the agreement's dispute settlement provisions, which may differ for each agreement. Each party to a trade agreement has an obligation to comply with dispute resolution rulings or potentially face withdrawal of certain benefits under the agreement. Dodd-Frank does not specify how disagreements might be resolved in covered agreements, thus each covered agreement would need to clarify the dispute resolution process.

Regulatory Cooperation

As discussed, U.S. FTAs include market access commitments and rules and disciplines governing financial services measures, such as nondiscrimination and transparency obligations. Although FTAs customarily establish a Financial Services Committee composed of each party's regulators to oversee implementation of the agreement and provide a forum for communication, U.S. FTAs to date exclude regulatory cooperation commitments for the financial services sector, though this is subject to change in future trade agreements.

On October 16, 2018, the Trump Administration notified Congress, under Trade Promotion Authority (TPA), of its intent to enter trade agreement negotiations with the European Union (EU), its largest overall trade and investment partner. The negotiating objectives published by USTR include to "expand competitive market opportunities for U.S. financial service suppliers to obtain fairer and more open conditions of financial services trade" and "improve transparency and predictability in the EU's financial services regulatory procedures, and ensure that the EU's financial regulatory measures are administered in an equitable manner."29 The EU member states are currently discussing the scope of the EU negotiating mandate, and U.S.-EU preparatory talks have been ongoing. In prior trade agreement negotiations between the two sides, the EU sought to include regulatory cooperation issues that could have addressed some of the same matters as the recent U.S.-EU covered agreement (see below). Some Members of Congress supported this position, whereas U.S. financial regulators opposed the inclusion at that time.

During the prior negotiations, the United States and the EU agreed to establish the Joint U.S.-EU Financial Regulatory Forum, which has met regularly. U.S. participants include representatives of the Treasury Department, Federal Reserve, Commodity Futures Trading Commission (CFTC), Federal Deposit Insurance Corporation (FDIC), SEC, and Office of the Comptroller of the Currency (OCC). The forum meetings include discussions of financial regulatory reforms, agency priorities, assessments of the cross-border impact of regulation, and cooperation efforts on specific financial issues.30

U.S.-EU Covered Agreement

On September 22, 2017, the United States and European Union signed the first bilateral insurance covered agreement.31 The covered agreement had been submitted to the House Committees on Financial Services and Ways and Means and the Senate Committees on Banking, Housing, and Urban Affairs and Finance on January 13, 2017. As noted above, a 90-day layover period is mandated in statute to allow Congress to review the agreement. The House Financial Services Committee Subcommittee on Housing and Insurance and the Senate Committee on Banking, Housing, and Urban Affairs each held a hearing on the agreement,32 but no legislative action affecting the agreement occurred.

To address concerns among U.S. insurance firms that their market access to the EU would become limited due to changes in EU regulatory policy, in November 2015, the Obama Administration notified Congress regarding plans to begin negotiations with the EU on a covered agreement. Expressed goals for the negotiations included (1) achieving recognition of the U.S. regulatory system by the EU, particularly through an "equivalency" determination by the EU that would allow U.S. insurers and reinsurers to operate throughout the EU without increased regulatory burdens, and (2) obtaining uniform treatment of EU-based reinsurers operating in the United States, particularly with respect to collateral requirements. The issue of equivalency for U.S. regulation is a relatively new one, as Solvency II only came into effect at the beginning of 2016 (see "The European Union, Solvency II, and Equivalency" below), whereas the question of reinsurance collateral has been a concern of the EU for many years (see "Reinsurance Collateral" below). The covered agreement negotiations also sought to facilitate the exchange of confidential information among supervisors across borders.

According to the USTR and Treasury, the bilateral agreement

- allows U.S. and EU insurers to rely on their home country regulators for worldwide prudential insurance group supervision when operating in either market;

- eliminates collateral and local presence requirements for reinsurers meeting certain solvency and market conduct conditions; and

- encourages information sharing between insurance supervisors.

The proposal sets time lines for each side to make the necessary changes and allows either side to not apply the agreement if the other side falls short on full implementation. Unlike the goals expressed to Congress when negotiations began, the agreement does not explicitly call for equivalency recognition of the U.S. insurance regulatory system by the EU. However, the agreement's provisions on group supervision would seem to meet the same goal of reducing the regulatory burden on U.S. insurers operating inside the EU. The proposal goes beyond a previous state-level proposal on reinsurance collateral requirements put forth by the NAIC and adopted by many states, and allows for the possibility of federal preemption if states are not in compliance.

Several U.S. industry groups welcomed the agreement, including the American Insurance Association (AIA), the Reinsurance Association of America, and the American Council of Life Insurers (ACLI). The AIA's senior vice president and general counsel noted that, "when negotiations began, U.S. insurance and reinsurance groups were facing growing obstacles to their ability to do business in Europe, but this agreement removes those barriers—affirming not only each other's regulatory systems, but also their commitments to non-discriminatory treatment and open, reciprocal, competitive insurance markets."33

State regulators and state lawmakers, respectively represented by the NAIC and National Council of Insurance Legislators (NCOIL), expressed concern with the agreement due to the limited state involvement in the negotiation process and the potential federal preemption of state laws and regulations. NCOIL expressed disappointment with the final signing, stating "this agreement is an intrusion by both the federal government and international regulatory authorities into the U.S. state based regulation of insurance regulation."34 Some insurers also question the utility of the agreement, with the president of the National Association of Mutual Insurance Companies (NAMIC) seeing ambiguity that "will result in confusion and potentially endless negotiations with Europe on insurance regulation."35 As mentioned, the agreement includes a review after an initial implementation period, at which time either the United States or EU may pull out of the agreement.

Reinsurance Collateral

The covered agreement aims to address EU concerns regarding U.S. state regulatory requirements that reinsurance issued by non-U.S. or alien36 reinsurers must be backed by collateral deposited in the United States. In the past, this requirement was generally for a 100% collateral deposit. Non-U.S. reinsurers long resisted this requirement, pointing out, among other arguments, that U.S. reinsurers do not have any collateral requirements in many foreign countries and that the current regulations do not recognize when an alien reinsurer cedes some of the risk back to a U.S. reinsurer. Formerly, the NAIC and the individual states declined to reduce collateral requirements, citing fears of unpaid claims from non-U.S. reinsurers and an inability to collect judgments in courts overseas. This stance, however, has changed in recent years.

In 2010, an NAIC Task Force approved recommendations to reduce required collateral based on the financial strength of the reinsurer involved and recognition of the insurer's domiciliary regulator as a qualified jurisdiction. The NAIC, in November 2011, adopted this proposal as a model law and accompanying model regulation.37 To take effect, however, these changes must be made to state law and regulation by the individual state legislatures and insurance regulators. The reinsurance models are part of the NAIC accreditation standards, and all states are expected to adopt them by 2019.

According to information provided to CRS by the NAIC, as of December 2018, 49 states have adopted the model law and 42 have adopted the accompanying regulation. To date, 29 reinsurers have been approved by the states as certified reinsurers for reduction in collateral requirements. To receive the reduced collateral requirements, the reinsurer's home jurisdiction must also be reviewed and listed on the NAIC List of Qualified Jurisdictions. As of January 2019, seven jurisdictions have been approved.38

The state actions addressing reinsurance collateral requirements, however, have not fully met concerns of foreign insurers regarding the issue. Non-U.S. reinsurers reportedly would like a single standard across the United States that would eliminate, not just reduce, collateral requirements.39 This desire was a significant part of the EU's expressed motivation to enter into covered agreement negotiations. A Council of the EU representative indicated that "an agreement with the U.S. will greatly facilitate trade in reinsurance and related activities" and would "enable us, for instance, to recognize each other's prudential rules and help supervisors exchange information."40

The European Union, Solvency II, and Equivalency

The covered agreement also aims to assist U.S. insurers concerned with potential regulatory burdens in relation to EU market requirements that went into effect in 2016. The European Union's Solvency II is part of a project aimed at transforming the EU into a single market for financial services, including insurance. In some ways, Solvency II is purely an internal EU project designed to more closely harmonize laws among the EU countries. However, as part of the Solvency II project, new equivalency determinations of foreign jurisdictions are to be made by the EU.41 An equivalency determination would allow insurers from a foreign jurisdiction to operate throughout the EU as do EU insurers. If the U.S. system of state-centered supervision of insurers were not judged to be "equivalent" to the EU insurance supervision, U.S. insurers could face more difficulty in operating in EU markets. Past suggestions have been made that an EU regulatory change might serve as "a useful tool in international trade negotiations as it could help improve access for European reinsurers to foreign markets," such as the United States.42 A June 6, 2014, letter from the European Commission to FIO and the NAIC drew an explicit connection between an equivalency designation applying to the United States and the U.S. removal of reinsurance capital requirements that the states place on non-U.S. reinsurers.43

Solvency II came into effect in the EU at the beginning of 2016. The EU has granted provisional equivalence to the United States along with five other countries and equivalence to three countries. The grant of provisional U.S. equivalence, however, applies only to capital requirements of EU insurers with U.S. operations,44 and U.S. insurers had reported experiencing difficulties with their operation in EU countries prior to the signing of the covered agreement.45

The U.S.-UK Covered Agreement

Following the 2016 referendum on the United Kingdom remaining in the European Union (popularly known as Brexit), the UK is scheduled to leave the EU by March 29, 2019. The future status and terms of the UK withdrawal from the EU is highly uncertain.46 Withdrawal from the EU may leave the UK outside the scope of any existing EU international agreements, including the U.S.-EU covered agreement. Thus, insurance trade between the United States and the UK could be negatively affected. As noted, the UK is an important market for U.S. firms, accounting for more than half of U.S. insurance exports in 2017.47

The United States and UK negotiated a separate covered agreement to address the potential disruption to insurance trade under Brexit. Announced on December 11, 2018,48 the substantive provisions of the U.S.-UK agreement mirror those in the U.S.-EU covered agreement—reinsurance capital and local presence requirements are to be eliminated and home country regulation is to be recognized for worldwide group supervision. According to the USTR and Treasury Department, the bilateral agreement aims to provide "regulatory certainty and market continuity" for U.S. and UK firms operating in the two markets. The Administration submitted the final text to Congress on December 11, 2018,49 starting the 90-day layover period for Congress to review the agreement prior to signature. The agreement implicitly recognizes the uncertainty regarding Brexit and will not come into effect until both parties provide notification that their internal procedures have been completed with the UK specifically taking account "of its obligations arising in respect of any agreement between the EU and the UK pursuant to Article 50 of the Treaty on European Union."50

The U.S.-UK covered agreement has been welcomed by most insurance stakeholders for addressing the uncertainty surrounding Brexit. For example, although the NAIC continues to have "concerns with the covered agreement mechanism, [the NAIC does] not object to its use in this instance to replicate consistent treatment for the UK."51

In addition to the covered agreement, on October 16, 2018, the Administration formally notified Congress of its intent to enter into negotiations of a bilateral U.S.-UK free trade agreement. Whether an agreement would include financial services regulatory cooperation is unclear, and the United States and the UK would not be able to start formal trade negotiations until the UK officially leaves the EU.

Future Covered Agreements

The U.S.-EU and U.S.-UK covered agreements as negotiated apply only to the jurisdictions that are party to the respective agreements. The United States, however, engages in a significant amount of trade in insurance services with other countries. Depending on what changes might be made to state insurance laws, reinsurers from other countries such as Bermuda or Japan could continue to face collateral requirements when offering products in the United States while competing with EU reinsurers free from such requirements.

Two primary policy approaches are being considered to address concerns regarding an uneven playing field between European and non-European reinsurers. It would be possible to negotiate additional covered agreements with non-European jurisdictions, as was done with the UK. In addition to the negotiation of new covered agreements, state laws enacted in response to the U.S.-EU covered agreement might themselves remove reinsurance collateral requirements for all or some non-EU jurisdictions. The NAIC is in the process of adopting an updated model law regarding reinsurance collateral, which would do this for a subset of "qualified jurisdictions" including Japan, Bermuda, and Switzerland.

International Insurance Entities

Outside of international trade negotiations and agreements, two separate but interrelated entities have the most significant impact on international insurance issues in the United States: the Financial Stability Board and the International Association of Insurance Supervisors.

The Financial Stability Board

The FSB was established in April 2009 by G-20 nations to help strengthen the global financial system following the 2008 financial crisis. The FSB's functions include assessing vulnerabilities to the global financial system; coordinating with financial authorities of member nations; and recommending measures to protect and strengthen the global financial system. The FSB's members comprise financial regulatory agencies of G-20 nations. U.S. FSB members are the Department of the Treasury, the Federal Reserve, and the SEC; no insurance-focused representative from the United States is included. The FSB's recommendations and decisions are not legally binding on any of its member nations. Rather, the FSB "operates by moral suasion and peer pressure, in order to set internationally agreed policies and minimum standards that its members commit to implementing at national level."52

The International Association of Insurance Supervisors

The IAIS, created in 1994, is the international standard-setting body, establishing a variety of guidance documents and conducting educational efforts for the insurance sector. Its mission is "to promote effective and globally consistent supervision of the insurance industry."53 The IAIS is primarily made up of insurance regulators worldwide with most jurisdictions having membership. U.S. members include all the individual states, the NAIC, the Federal Reserve, and the Federal Insurance Office. FIO and the Federal Reserve became IAIS members only after the passage of the Dodd-Frank Act. These U.S. members serve on many IAIS committees and working groups and have held various committee positions, past and present. An NAIC representative serves as chair of the IAIS Policy Development Committee, which plays a central role in drafting IAIS-proposed standards; the FIO director previously served as chair of this committee's prior incarnation, the IAIS Financial Stability and Technical Committee. The NAIC coordinates individual state participation in IAIS committees and working groups. According to the NAIC, three NAIC members serve on the IAIS Executive Committee, including one as vice chair; three serve on the Policy Development Committee; and three serve on the Macroprudential Committee. The NAIC's 56 members have 15 votes in the IAIS general meetings, with the NAIC designating which of its members may exercise their votes.54

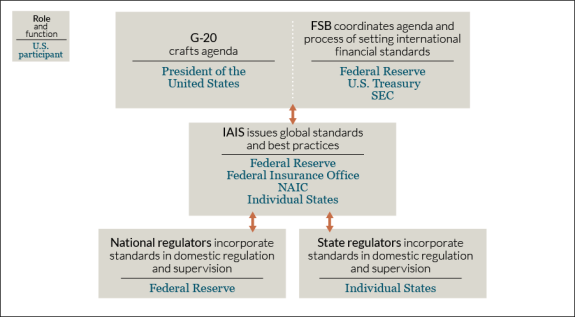

Figure 3 provides a graphical representation of the relationships between international entities and their U.S. members.

|

Figure 3. International Financial Architecture for Insurance |

|

|

Source: Congressional Research Service. Note: For a general overview of the international financial architecture, please see CRS In Focus IF10129, Introduction to Financial Services: International Supervision, by Martin A. Weiss. |

International Insurance Standards and Designations

As part of its monitoring of global financial stability, the FSB has designated a number of financial institutions as globally systemically important. An FSB designation is meant to indicate that the failure of an individual institution could have a negative impact on the global financial system. Initially, the designation focused on global systemically important banks (G-SIBs), but it also encompasses global systemically important insurers (G-SIIs), and nonbank noninsurer global systemically important financial institutions (NBNI G-SIFIs), such as large asset managers, broker-dealers, and hedge funds. Designated institutions are expected to meet higher qualitative and quantitative regulatory and capital standards to help ensure their stability during a crisis. Although the FSB designations may be similar in intent to the designations done under the FSOC in the United States, FSB designations are a separate process with somewhat different criteria.

In 2016, the FSB designated nine G-SIIs, including three U.S. insurers (AIG, MetLife, and Prudential Financial).55 The FSB also had requested that the IAIS develop capital standards and other regulatory measures to apply to G-SIIs as well as Internationally Active Insurance Groups (IAIGs), a wider set of insurers that fall short of the G-SII designation.56 In 2017, the FSB did not publish a new G-SII list, allowing the 2016 list to continue to be in effect.57 In 2018, the FSB decided not to identify G-SIIs, and it may suspend or discontinue the identification of G-SIIs depending on a new IAIS "holistic framework" to address systemic risk based on specific activities rather than individual firm designations.58

In addition to the standards addressing systemic risk, the IAIS is developing a general Common Framework for the Supervision of Internationally Active Insurance Groups (ComFrame). ComFrame encompasses a range of supervisory standards, particularly capital standards for IAIGs. The ComFrame process dates to 2010; currently, a public comment period has ended for a draft of the overall framework and a "2.0" version of specific insurance capital standards, with additional consultations continuing and formal adoption scheduled at the end of 2019.59

Implementation of International Standards

In general, actions undertaken by international bodies, such as the FSB's designations of G-SIIs or adoption of capital standards by the IAIS, have no immediate effect on the regulatory system within the United States. To be implemented, such standards must be adopted by regulators in the United States or enacted into law if regulators do not already have sufficient legal authority to adopt the standards. In many cases, it is expected that members of such international bodies will adopt the agreed-to standards. For example, the Basel Committee on Bank Supervision (BCBS) charter includes among the members' responsibilities that they commit to "implement and apply BCBS standards in their domestic jurisdictions within the pre-defined timeframe established by the Committee."60 In some situations, the translation from international standard to national implementation may be relatively straightforward because the agencies agreeing to the international standards are the same agencies that have the authority to implement the standards at home.61

The mix of federal and state authorities over insurance in the United States, however, has the potential to complicate the adoption of international standards, such as the IAIS's capital standards that are under development. In the case of insurance, the U.S. representation at the IAIS includes (1) the NAIC, which collectively represents the U.S. state regulators, but has no regulatory authority of its own; (2) the 56 different states and territories, which collectively regulate the entire U.S. insurance market, but individually oversee only individual states and territories; (3) the Federal Reserve, which has holding company oversight only over designated systemically significant insurers and insurers with depository subsidiaries;62 and (4) the FIO, which has authority to monitor and report but no specific regulatory authority. Thus, it is possible for a situation to develop where some part of the U.S. representation at the IAIS may agree to particular policies or standards without agreement by the entity having authority to actually implement the policies or standards that are being agreed to.

Moral Suasion and Market Pressures

Although international standards may not be self-executing, nations may still face pressures to implement these standards. For example, the International Monetary Fund performs a Financial Sector Assessment Program (FSAP) of many countries every five years. In the latest FSAPs from 2010 and 2015, the judgments and recommendations offered regarding the U.S. insurance regulatory system compared U.S. laws and regulations to core principles adopted by the IAIS. Although U.S. regulators generally accept the IAIS core principles, the FSAP does note that state regulators specifically "disagree with a few of the ratings ascribed to certain" core principles and the states "do not believe that each of the proposed regulatory reforms recommended in the Report is warranted, or would necessarily result in more effective supervision."63

Pressure may also derive from internationally active market participants, including both domestic and foreign firms. Companies operating in different jurisdictions incur costs adapting to different regulatory environments. To minimize these costs, companies may pressure jurisdictions to adopt similar rules. Even if one country's rules might be more favorable to the company seen in the abstract, it may still be more efficient for a company if all the countries adopt slightly less favorable, but substantially similar, rules. Thus, for example, a U.S. company operating in multiple countries might favor adoption of U.S. regulations similar to international standards to simplify business operations, even if it finds the U.S. regulations generally preferable.

Specific Policy Concerns with International Standards

Those concerned about potential international insurance standards often raise the possibility that these standards may be "bank-like" and thus inappropriate for application to insurers.64 A primary concern in this regard is the treatment of financial groups. In banking regulation, a group holding company is expected, if not legally required, to provide financial assistance to subsidiaries if necessary. In addition, safety and soundness regulations may be applied at a group-wide level. A somewhat similar focus on the group-wide level is also found in the EU's Solvency II and in possible future IAIS standards. Within U.S. insurance regulation, however, state regulators in the United States historically have focused on the individual legal entities and on ensuring that the specific subsidiaries have sufficient capital to fulfill the promises inherent in the contracts made with policyholders.65 Since the financial crisis, the U.S. regulators have increased oversight at the overall group level, but the possible movement of capital between subsidiaries remains an issue. The NAIC has indicated specifically that "it is critical that the free flow of capital (i.e., assets) across a group should not jeopardize the financial strength of any insurer in the group."66 A group-wide approach that facilitates capital movement among subsidiaries could potentially improve financial stability as a whole if it prevents a large financial firm from becoming insolvent in the short run. It also could provide protection for individual policyholders if it results in additional resources being made available to pay immediate claims. Potential movement of capital within groups, however, could also potentially reduce financial stability if it were to cause customers to doubt the payment of future claims and thus promote panic or contagion. Free movement of capital across subsidiaries could also harm policyholders in the future if it results in insufficient capital to pay such claims.

Congressional Outlook

The 116th Congress faces an immediate issue regarding the U.S.-UK covered agreement. This agreement is currently in its statutory 90-day layover period (which began December 11, 2018) before it can take effect. Congress could enact legislation directly affecting the agreement, conduct hearings or other oversight mechanisms, or allow the covered agreement to take effect without direct action.

The U.S.-UK covered agreement may not be the only international insurance issue before this Congress. With expected continued growth in the international insurance market and differences in regulatory approaches, the frictions between U.S. and foreign regulators as well as between state and federal regulators seem likely to continue. Congress may choose to address these issues in multiple ways including, for example,

- amending Dodd-Frank and the statutory role of FIO and the USTR in international insurance negotiations;

- legislating an increased role for states in U.S. representation to international insurance regulatory entities;

- endorsing international insurance standards and legislating their adoption by states;

- encouraging additional covered agreements to address the countries not covered by the current ones; or

- encouraging the inclusion of insurance services as part of negotiations of potential free trade agreements.

Appendix. Legislation in the 115th Congress

The following summarizes legislation addressing international insurance issues in the 115th Congress. Legislation is ordered according to the stage to which it advanced in the legislative process.

Economic Growth, Regulatory Relief, and Consumer Protection Act (P.L. 115-174/S. 2155)

S. 2155 was introduced by Senator Michael Crapo and 19 cosponsors on November 16, 2017. The bill, covering a broad range of financial services provisions largely dealing with noninsurance issues, was marked up and reported on a vote of 16-7 by the Senate Committee on Banking, Housing, and Urban Affairs in December 2017. A new section was added during the Senate committee markup with language similar to S. 1360 (discussed below).67 S. 2155 passed the Senate by a vote of 67-31 on March 14, 2018. The House passed S. 2155 without amendment on May 22, 2018, and the President signed the bill into P.L. 115-174 on May 24, 2018.

Section 211 of P.L. 115-174 finds that the Treasury, Federal Reserve, and FIO director shall support transparency in international insurance fora and shall "achieve consensus positions with State insurance regulators through the [NAIC]" when taking positions in international fora. It creates an "Insurance Policy Advisory Committee on International Capital Standards and Other Insurance Issues" at the Federal Reserve made up of 21 members with expertise on various aspects of insurance. The Federal Reserve and the Department of the Treasury are to complete an annual report and to provide testimony on the ongoing discussions at the IAIS through 2022, and the Federal Reserve and FIO are to complete a study and report, along with the opportunity for public comment and review by the Government Accountability Office (GAO), on the impact of international capital standards or other proposals prior to agreeing to such standards. Unlike S. 1360, however, the enacted law does not have specific requirements on the final text of any international capital standard. After signing S. 2155, the President released a statement indicating that the congressional directions in the findings contravene the President's "exclusive constitutional authority to determine the time, scope, and objectives of international negotiations" but that the President will "give careful and respectful consideration to the preferences expressed by the Congress in section 211(a) and will consult with State officials as appropriate."68

International Insurance Standards Act (H.R. 4537/S. 488, Title XIV)

Representative Sean Duffy, along with seven cosponsors, introduced H.R. 4537 on December 4, 2017. (A substantially similar bill, H.R. 3762, was previously introduced and addressed in an October 24, 2017, hearing by the House Financial Services' Subcommittee on Housing and Insurance.) H.R. 4537 was marked up and ordered reported on a vote of 56-4 by the House Committee on Financial Services on December 12-13, 2017. It was reported (H.Rept. 115-804) on July 3, 2018. The House considered a further amended version on July 10, 2018, and passed it under suspension of the rule by a voice vote. H.R. 4537 was not taken up by the Senate in the 115th Congress.

S. 488 originally was introduced by Senator Pat Toomey as the Encouraging Employee Ownership Act, increasing the threshold for disclosure relating to compensatory benefit plans. After Senate passage on September 11, 2017, it was taken up in the House and amended with a number of different provisions, mostly focusing on securities regulation.69 Title XIV of the amended version of S. 488, however, was nearly identical to H.R. 4537 as it passed the House. The House-passed version of S. 488 was not taken up by the Senate in the 115th Congress.

H.R. 4537 as passed by the House and S. 488 as passed by the House would have instituted a number of requirements relating to international insurance standards and insurance covered agreements. U.S. federal representatives in international fora would have been directed not to agree to any proposal that does not recognize the U.S. system as satisfying that proposal. Such representatives would have been required to consult and coordinate with the state insurance regulators and with Congress prior to and during negotiations and to submit a report to Congress prior to entering into an agreement.

With regard to future covered agreements, the bill would have required U.S. negotiators to provide congressional access to negotiating texts and to "closely consult and coordinate with State insurance commissioners." Future covered agreements were to be submitted to Congress for possible disapproval under "fast track" legislative provisions.70 The Congressional Budget Office's cost estimate on H.R. 4537 as reported from committee found that,

Any budgetary effects of enacting H.R. 4537 would depend, in part, on how often the United States negotiates international insurance agreements and how frequently the negotiators must consult and coordinate with state insurance commissioners. CBO has no basis for predicting that frequency but expects that the cost of such consultations would be less than $500,000 per year.71

International Insurance Capital Standards Accountability Act of 2017 (S. 1360)

S. 1360 was introduced by Senator Dean Heller with cosponsor Senator Jon Tester on June 14, 2017, and referred to the Senate Committee on Banking, Housing, and Urban Affairs. Similar language to S. 1360 was added to P.L. 115-174/S. 2155 as discussed above.

S. 1360 would have created an "Insurance Policy Advisory Committee on International Capital Standards and Other Insurance Issues" at the Federal Reserve made up of 11 members with expertise on various aspects of insurance. It would have required both an annual report and testimony from the Federal Reserve and the Department of the Treasury on the ongoing discussions at the IAIS through 2020. The Federal Reserve and FIO would have been required to complete a study and report, along with the opportunity for public comment and review by GAO, on the impact of international capital standards or other proposals prior to agreeing to such standards. Any final text of an international capital standard would have been required to be published in the Federal Register for comment and could not have been inconsistent with either state or Federal Reserve capital standards for insurers.

International Insurance Standards Act of 2017 (H.R. 3762)

H.R. 3762 was introduced by Representative Sean Duffy with cosponsor Representative Denny Heck on September 13, 2017. It was addressed in an October 24, 2017, hearing by the House Financial Services' Subcommittee on Housing and Insurance, but it was not the subject of further committee action. The sponsor introduced an identically titled and substantially similar bill, H.R. 4537, which was ordered reported by the House Committee on Financial Services on December 13, 2017. See the above section on H.R. 4537 for more information on the bill.

Federal Insurance Office Reform Act of 2017 (H.R. 3861)

H.R. 3861 was introduced by Representative Sean Duffy with cosponsor Representative Denny Heck on September 28, 2017. It was addressed in an October 24, 2017, hearing by the House Financial Services' Subcommittee on Housing and Insurance, but it was not the subject of further action.

H.R. 3861 would have amended the Dodd-Frank Act provisions creating the Federal Insurance Office, generally limiting the focus and size of FIO. It would have placed FIO specifically within the Office of International Affairs and narrowed its function in international issues to representing the Treasury rather than all of the United States. It also would have required FIO to reach a consensus with the states on international matters. The bill would have removed FIO's authority to collect and analyze information from insurers, including its subpoena power, and to issue reports with this information. Under the bill, the authority to preempt state laws pursuant to covered agreements would have rested with the Secretary of the Treasury, and FIO would have been limited to five employees.