The Disaster Relief Fund: Overview and Issues

Changes from April 16, 2020 to November 13, 2020

This page shows textual changes in the document between the two versions indicated in the dates above. Textual matter removed in the later version is indicated with red strikethrough and textual matter added in the later version is indicated with blue.

Contents

- Introduction

- What is the Disaster Relief Fund and how is it used?

- What determines whether an incident qualifies as an emergency or disaster?

- Does all federally funded disaster relief come from the DRF?

- What federal government activities are funded under the DRF?

- Under what statute is the Disaster Relief Fund authorized?

- Where are appropriations for the Disaster Relief Fund provided?

- Are specific Disaster Relief Fund appropriations for specific disasters?

- How is the DRF being spent?

- Historical Context for Federal Disaster Relief Funding

- 1789-1947: Case by Case, After the Fact

- 1947-1950: General Disaster Relief Funding from the Federal Government Begins

- 1950-1966: The Disaster Relief Act of 1950—General Relief and Specific Relief

- 1966-1974: The Disaster Relief Act of 1966—General Relief Broadens

- 1974-Present: The Era of Federally Coordinated Emergency Management

- Appropriations for General Disaster Relief

- Types of Appropriations for Disaster Relief

- Supplemental Appropriations for Disaster Relief

- Annual Appropriations

- Continuing Appropriations

- DRF Funding History: FY1964-FY2019

- Factors in Changing Appropriations Levels

- Incident Frequency and Severity

- Programmatic Changes in Disaster Relief

- Changes in the Budget Process

- Budgeting Practices for Disaster Relief

- Management of Disaster Relief Funds

- 1978: The Creation of the Federal Emergency Management Agency

- Calculation of the Annual Appropriations Request

- Emergency Contingency Funding and Reserve Funds

- Rescissions and the DRF

- Issues for Congress

- Should the purpose of the DRF be rescoped?

- How much is enough to have on hand?

- What accommodations should be made in the federal budget for disaster relief?

Figures

- Figure 1. Nominal Dollar Disaster Relief Appropriations, FY1964-FY2019

- Figure 2. FY2019 Dollar Disaster Relief Appropriations, FY1964-FY2019

- Figure 3. Catastrophic Disasters, DRF Appropriations and Obligations, FY2014-FY2019

- Figure 4. DRF Annual and Supplemental Appropriations Within and Beyond Discretionary Spending Limits, FY2004-FY2019

Tables

Summary

The Disaster Relief Fund: Overview and Issues

November 13, 2020

The Disaster Relief Fund (DRF) is one of the most-tracked single accounts funded by Congress each year. Managed by the Federal Emergency Management Agency (FEMA),

William L. Painter

it is the primary source of funding for the federal government'’s domestic general

Specialist in Homeland

disaster relief programs. These programs, authorized under the Robert T. Stafford

Security and

Disaster Relief and Emergency Assistance Act, as amended (42 U.S.C. 5121 et seq.),

Appropriations

outline the federal role in supporting state, local, tribal, and territorial governments as

they respond to and recover from a variety of incidents. They take effect in the event

that nonfederal levels of government find their own capacity to deal with an incident is overwhelmed.

The appropriation which feeds the DRF predates current disaster relief programs and FEMA itself. It dates back to a half-million dollar deficiency appropriation to the President in 1948 that was drafted to allowallowed him to use these resources to provide temporary emergency assistance to communities in the wake of unspecified potential natural disasters. Although the appropriation was provided with one particular Upper Midwest flooding incident in mind, the legislative language allowed the funding to be used more broadly, if the President wished to do so. This policy of providing general disaster relief was a shift from previous policy, which largely left emergency management, disaster relief, and disaster recovery in the hands ofto other levels of government and private relief organizations. Prior to the development of the general relief program, when the federal government got involvedinvolved itself in disaster response and recovery, it was on an ad hoc, case-by-case basis. In the early 21st21st century, emergency management has its own federal agency.

The evolving federal role in disaster relief is partially illuminated by the robust funding stream provided for it through the DRF. At the end of FY2019, the DRF carried over a balance of more than $29 billion, and Congress was considering the largest annual appropriation for disaster relief for the third year in a row. However, what is a fixture of federal policy today was not a given a century ago. Examining the history of the program and its funding through the DRFDRF and the programs it supports may help Congress consider future approaches to disaster relief.

This report introduces the DRF and provides a brief history of federal disaster relief programs. It goes on to discuss the appropriations that fund the DRF, and provides a funding history from FY1964 to the present day, discussing factors that contributed to those changing appropriations levels. It concludes with discussion of how the budget request for the DRF has been developed and structured, given the unpredictability of the annual budgetary impact of disasters, and raises some potential issues for congressional consideration.

This report is updated on an annual basis.

Introduction

Congressional Research Service

link to page 5 link to page 5 link to page 5 link to page 6 link to page 6 link to page 7 link to page 8 link to page 8 link to page 8 link to page 8 link to page 9 link to page 10 link to page 12 link to page 13 link to page 14 link to page 14 link to page 16 link to page 17 link to page 17 link to page 17 link to page 18 link to page 19 link to page 20 link to page 23 link to page 23 link to page 26 link to page 27 link to page 30 link to page 30 link to page 30 link to page 30 link to page 33 link to page 34 link to page 35 link to page 36 link to page 37 link to page 37 link to page 21 link to page 22 link to page 26 The Disaster Relief Fund: Overview and Issues

Contents

Introduction ..................................................................................................................................... 1

What is the Disaster Relief Fund and how is it used? ............................................................... 1

What determines whether an incident qualifies as an emergency or disaster? ................... 1

Does all federally funded disaster relief come from the DRF? ................................................. 2

What federal government activities are funded under the DRF? ........................................ 2

Under what statute is the Disaster Relief Fund authorized? ..................................................... 3 Where are appropriations for the Disaster Relief Fund provided? ............................................ 4

Are specific Disaster Relief Fund appropriations for specific disasters? ........................... 4 How is the DRF being spent today? ................................................................................... 4 How is the DRF being used to respond to COVID-19? ...................................................... 4

Historical Context for Federal Disaster Relief Funding .................................................................. 5

1789-1947: Case by Case, After the Fact .................................................................................. 6 1947-1950: General Disaster Relief Funding from the Federal Government Begins ............... 8 1950-1966: The Disaster Relief Act of 1950—General Relief and Specific Relief .................. 9 1966-1974: The Disaster Relief Act of 1966—General Relief Broadens ............................... 10 1974-Present: The Era of Federally Coordinated Emergency Management ........................... 10

Pandemic COVID-19 and the Stafford Act ....................................................................... 12

Appropriations for General Disaster Relief ................................................................................... 13

Types of Appropriations for Disaster Relief............................................................................ 13

Supplemental Appropriations for Disaster Relief ............................................................. 13 Annual Appropriations ...................................................................................................... 14 Continuing Appropriations ................................................................................................ 15

DRF Funding History: FY1964-FY2020 ................................................................................ 16 Factors in Changing Appropriations Levels ............................................................................ 19

Incident Frequency and Severity ...................................................................................... 19 Programmatic Changes in Disaster Relief ........................................................................ 22 Changes in the Budget Process ......................................................................................... 23

Budgeting Practices for Disaster Relief ........................................................................................ 26

Management of Disaster Relief Funds .................................................................................... 26

1978: The Creation of the Federal Emergency Management Agency .............................. 26 Calculation of the Annual Appropriations Request ........................................................... 26 Emergency Contingency Funding and Reserve Funds ..................................................... 29 Rescissions and the DRF .................................................................................................. 30

Issues for Congress ........................................................................................................................ 31

Should the purpose of the DRF be rescoped? ......................................................................... 32 How much is enough to have on hand? ................................................................................... 33 What accommodations should be made in the federal budget for disaster relief? .................. 33

Figures Figure 1. Nominal Dollar Disaster Relief Appropriations, FY1964-FY2020 ............................... 17 Figure 2. FY2020 Dollar Disaster Relief Appropriations, FY1964-FY2020 ................................ 18 Figure 3. Catastrophic Disaster Costs, DRF Appropriations and Obligations .............................. 22

Congressional Research Service

link to page 29 link to page 29 link to page 24 link to page 24 link to page 38 link to page 40 link to page 38 link to page 42 The Disaster Relief Fund: Overview and Issues

Figure 4. DRF Annual and Supplemental Appropriations Within and Beyond

Discretionary Spending Limits, FY2004-FY2020 ..................................................................... 25

Tables Table 1. Disaster Declaration Activities and Projected Costs of Catastrophic Disaster

Declarations, FY2004-FY2019 .................................................................................................. 20

Table A-1. Nominal Dollar Disaster Relief Appropriations, FY1964-FY2020 ............................. 34 Table A-2. FY2020 Dollar Disaster Relief Appropriations, FY1964-FY2020 .............................. 36

Appendixes Appendix. General Disaster Relief Appropriations, FY1964-FY2020 ......................................... 34

Contacts Author Information ........................................................................................................................ 38

Congressional Research Service

The Disaster Relief Fund: Overview and Issues

Introduction The Disaster Relief Fund (DRF) is one of the most-tracked single accounts funded by Congress each year. Managed by the Federal Emergency Management Agency (FEMA), it is the primary source of funding for the federal government'’s domestic general disaster relief programs. These programs, authorized under the Robert T. Stafford Disaster Relief and Emergency Assistance Act, as amended (42 U.S.C. 5121 et seq.), outline the federal role in supporting state, local, tribal, and territorial governments as they respond to and recover from a variety of incidents. They take effect in the event that nonfederal levels of government find their own capacitycapacities to deal with an incident overwhelmed.

Although theincident is overwhelmed.

The current environment for emergency management policy assumes this federal role in domestic disaster relief as the default position and the availability of resources through the DRF a necessary requirement. However, this was not always the case. The concept of general disaster relief provided by the federal government predates both FEMA and the Stafford Act, but federal involvement in relief after natural and man-made disasters was very rare before the Civil War, and was at times considered unconstitutional. Domestic disaster relief efforts became more common after the Civil War, but were not seen as a necessary obligation of the federal government. Standing federal domestic disaster relief programs and a pool of resources to fund them only emerged after the Second World War. Prior to the development of these programs, domestic disaster relief and recovery was a matter for private nongovernmental organizations and state and local governments.

Once established, the federal role in domestic disaster response and recovery grew, proving politically popular and resilient despite periodic concerns about management, execution, and budgetary impacts. The DRF is the source of funding for most general disaster relief programs, so it is an indicator of the scope of those programs and the volume of taxpayer-funded aid they provide. Understanding the trends in the growth of the federal government'’s role in general disaster relief and recovery, and the associated costs of that role, may be useful as Congress considers changes in both emergency management and budgetary policies.

This report introduces the DRF and provides a brief history of federal disaster relief programs. It goes on to discuss the appropriations that fund the DRF, and provides a funding history from FY1964 to the present day, discussing factors that contributed to those changing appropriations levels. It concludes with discussion of how the budget request for the DRF has been developed and structured, given the unpredictability of the annual budgetary impact of disasters, and raises some potential issues for congressional consideration.

What is the Disaster Relief Fund and how is it used?

The DRF is the primary source of funding for the federal government'’s general disaster relief program—response and recovery effortsactivities pursuant to a range of domestic emergencies and disasters in existingdefined in law—as opposed to specific relief and recovery initiatives that may be enacted for individual incidents.

What determines whether an incident qualifies as an emergency or disaster?

Under the Robert T. Stafford Disaster Relief and Emergency Assistance Act (P.L. 93-288, as amended; hereinafter "“the Stafford Act"”), the President can declare that an emergency exists or a major disaster is occurring.11 These declarations make state, tribal, territorial, and local governments2

1 Or has occurred—declarations are specific by time and place.

Congressional Research Service

1

The Disaster Relief Fund: Overview and Issues

governments2 eligible for a variety of assistance programs, many of which are funded from the DRF.33 Declarations usually are made at the request of a state, tribal, or territorial government.

Does all federally funded disaster relief come from the DRF?

While the DRF funds Stafford Act disaster relief and recovery programs, several other federal departments and agencies have significant roles in disaster preparedness, relief, recovery, and mitigation. These include the Department of Housing and Urban Development, the Small Business Administration, U.S. Department of Agriculture, U.S. Army Corps of Engineers, and the Department of Health and Human Services. While FEMA may fund some of their activities out of the DRF through mission assignments,4 their broader disaster-related programs are funded through separate appropriations.4

5

What federal government activities are funded under the DRF?

Currently, the Federal Emergency Management Agency (FEMA) coordinates federal disaster response and recovery efforts. As such, it, and manages the DRF, which funds activities in five categories:

1.1. Activity pursuant to a major disaster declaration—This activity represents the vast majority of spending from the DRF. FEMA'’s primary"“Direct DisasterPrograms"Programs” are the Individual Assistance (IA),56 Public Assistance (PA),67 and the Hazard Mitigation Grant Program (HMGP) programs.78 Federal assistance provided by other federal agencies at FEMA'’s direction through"“missionassignments"assignments” is also paid for from the DRF.82. Predeclaration9 2. Predeclaration surge activities—These are activities undertaken prior to an emergency or major disaster declaration to prepare for response and recovery, such as deploying response teams or prepositioning equipment.3. Activity2 As well as certain private nonprofit organizations as stipulated in the Stafford Act. 3 For more information, see CRS Report R43784, FEMA’s Disaster Declaration Process: A Primer, by Bruce R. Lindsay. 4 Mission assignments are directives from FEMA to other federal agencies to perform specific work in response to a Stafford Act emergency or disaster declaration. The federal agency can seek reimbursement from FEMA for the costs incurred. For information on how FEMA manages these activities, see https://www.fema.gov/federal-agencies/mission-assignments. 5 For information on the breadth of federal disaster relief, see CRS Report R41981, Congressional Primer on Responding to and Recovering from Major Disasters and Emergencies, by Bruce R. Lindsay and Elizabeth M. Webster; and U.S. Government Accountability Office, Federal Disaster Assistance: Federal Departments and Agencies Obligated at Least $277.6 Billion during Fiscal Years 2005 through 2014, GAO-16-797, September 22, 2016, https://www.gao.gov/products/GAO-16-797. 6 For more information, see CRS Report R45085, FEMA Individual Assistance Programs: In Brief, by Shawn Reese. 7 For more information, see CRS Report R43990, FEMA’s Public Assistance Grant Program: Background and Considerations for Congress, by Jared T. Brown and Daniel J. Richardson. 8 For more information, see CRS Report R40471, FEMA’s Hazard Mitigation Grant Program: Overview and Issues, by Natalie Keegan. 9 Department of Homeland Security, Disaster Relief Fund, Fiscal Year 2019 Congressional Budget Justification, Federal Emergency Management Agency, Washington, DC, February 2018, p. FEMA-DRF-23, https://www.dhs.gov/sites/default/files/publications/Federal%20Emergency%20Management%20Agency.pdf. Congressional Research Service 2 The Disaster Relief Fund: Overview and Issues 3. Activity pursuant to an emergency declaration—This is federal assistance topursuant to an emergency declaration—This is federal assistance tosupplement state and local efforts in providing emergency services in any part of the United States.4.4. Fire Management Assistance Grants (FMAGs) for large wildfires—This is assistance for the mitigation, management, and control of any fires on public or private lands that could, if unchecked, worsen and result in a major disaster declaration.95.10 5. Disaster Readiness and Support (DRS) activities—These are ongoing, non- incident specific activities that allow FEMA to provide timely disaster response, operate its programs responsively and effectively, and provide oversight of its emergency and disaster programs.

The role of the federal government has evolved over the years, as described in the sections below, but emergency response and disaster relief has historically been a federalized "“bottom-up" ” operation, starting from the local or tribal governments affected, backed up by the state or territorial government,1011 and then turning to the federal government if their capacity is overwhelmed. The broadening of the federal role has been a factor in which activities are funded under the DRF.

under the DRF.

DRF Activities and Statutory Budget Controls

Implementation of budget controls in 2011 led to changes in the way DRF appropriations were structured to support Stafford Act activities. Since FY2012, the first fiscal year of statutory limits on discretionary spending under the Budget Control Act (BCA), a distinction has been made between budget authority for the activities pursuant to a specific major disaster declaration—the first of the activities listed above—and budget authority for other activities. The former now often carries a special There is no direct limit in the plain language of the appropriation that would restrict In the supplemental appropriation for the DRF in P.L. 116-136, Division B, a new approach was taken. Of the $45 billion funds in emergency-designated supplemental funds, $25 billion was specified as being for the cost of major disasters, and $15 million was specified as being for any Stafford Act activities—including those activities in the base as well as major disasters—allowing those funds to be used more flexibly in the face of the COVID-19 epidemic, without requiring a reprogramming or transfer. The statutory discretionary budget limits laid out in the BCA and the disaster relief adjustment mechanisms will expire after FY2021 under current law. |

Under what statute is the Disaster Relief Fund authorized?

The DRF is not separately authorized as a distinct entity, but the activities it funds are authorized under the Stafford Act (42 U.S.C. 5121 et seq.).

Where are appropriations for the Disaster Relief Fund provided?

Where are appropriations for the Disaster Relief Fund provided? Since FY1980—FEMA'’s first annual appropriation—the DRF has been funded through its own appropriation within FEMA'’s budget, first under the heading "“Disaster Relief,"” and then "“Disaster Relief Fund"” starting in FY2012. FEMA'’s annual appropriations were first provided through the VA, HUD, and Independent Agencies Appropriations Act, but have been included in the Department of Homeland Security Appropriations act since FY2004. Since the first "“Disaster Relief"Relief” appropriation for FY1948, most of the DRF'’s appropriations have been provided through supplemental appropriations. See Figure 1 and Figure 2 for details.

Are specific Disaster Relief Fund appropriations for specific disasters?

DRF appropriations have historically been provided for general disaster relief, rather than specific presidentially declared disasters or emergencies.

The most recent iterations of the appropriations bill text indicate the funds are provided for the "“necessary expenses in carrying out the Robert T. Stafford Disaster Relief and Emergency Assistance Act,"” thus covering all past and future disaster and emergency declarations.1112 Previous versions of the appropriations language going back to 1950 also referenced the legislation authorizing general disaster relief rather than targeting specific disasters. On a number of occasions, specific disasters have been mentioned in the appropriation, but funding was not specifically directed to one disaster over others.

While many disaster supplemental appropriations bills are associated with a specific incident or incidents—such as P.L. 113-2, ", “the Sandy Supplemental"”—the language in that act does not limit the use of the disaster relief appropriation to that specific incident.12

13

How is the DRF being spent?

today?

Since the enactment of P.L. 112-74, Congress has received regular reporting on spending from the DRF. Monthly reports on such spending since March 2013 are available on FEMA'’s website.13 14 Currently, the reports include information on DRF balances, actual and projected obligations from the DRF for large-scale disasters broken down by disaster declaration, and obligations and expenditures aggregated by incident. These reports also include estimates of the DRF balance through the end of the current fiscal year.

Historical Context for Federal Disaster Relief Funding

How is the DRF being used to respond to COVID-19?

With the COVID-19 response, major disaster assistance programs under the Stafford Act authorities are being used for the first time to respond to an infectious disease outbreak.15

On March 13, 2020, President Donald J. Trump made a series of emergency declarations under Section 501(b) of the Stafford Act in response to the nationwide spread of a novel coronavirus

12 P.L. 115-141, Div. F. 13 See, for this specific example, 127 Stat. 28. 14 These monthly reports are available at https://www.fema.gov/media-library/assets/documents/31789. 15 Two emergency declarations under the Stafford Act were made in the fall of 2000 for West Nile virus control. However, the difference in scale is significant: for example, New Jersey received $2.36 million for West Nile from the DRF in 2000 (according to the Emergency Management Section of the New Jersey State Police), and $1,978 million under the COVID-19 disaster declaration from the DRF as of the end of FY2020 (according to FEMA’s October 2020 monthly report on the DRF).

Congressional Research Service

4

The Disaster Relief Fund: Overview and Issues

disease (COVID-19).16 The declarations authorized assistance to all U.S. states, territories, tribes, and the District of Columbia. At the time he announced the declarations, he invited the recipients of those declarations to request major disaster declarations.17 FEMA notes that 50 states, five territories, and the District of Columbia have all requested and received major disaster declarations for COVID-19 response.18

Later that month, a supplemental appropriation for the DRF was provided in the CARES Act, P.L. 116-136, Division B, providing $45 billion in emergency-designated supplemental appropriations. As with other DRF appropriations, this funding was not directed specifically to COVID-19 efforts, but for Stafford Act activities generally, including those related to COVID-19.

On August 8, 2020, the Administration announced a “lost wages assistance” program, which would expand and extend unemployment benefits for several weeks. This initiative would use the Other Needs Assistance program under the Individual Assistance programs under the Stafford Act.19 More than $41 billion was obligated for this program in the closing months of FY2020—more than three-quarters of the DRF obligations related to COVID-19.20

As of the end of FY2020, FEMA associated $52.681 billion in DRF spending with the COVID-19 response.21 Of this amount, $42.143 billion was provided through the Individual Assistance program, the vast majority of which was for the lost wages initiative. $6.058 billion was provided for Public Assistance programs, which reimburses eligible public and nonprofit entities for the costs of major disaster response and recovery, and another $4.319 billion supported operational costs, including mission assignments.

Historical Context for Federal Disaster Relief Funding Disaster relief has not always been a part of the mission of the federal government. For nearly 80 years, federal domestic disaster relief was minimal, extremely narrow in scope, and largely did not address humanitarian needs, leaving thosenot address the humanitarian side of the relief equation, leaving that to private organizations and local levels of government. Even as the country emerged from the Civil War with more of a national identity and a sense that the federal government could act to provide relief in some circumstances, disaster aid remained limited, responding only after the fact on a case-by-case basis. Only after World War II did the concept emerge of a federal role in responding to disasters . This new role was more broadly defined, led by the President and funded in advance, as opposed to case-by-case responses to needs in the wake of the most severe events led by ad hoc congressional action. Over the ensuing years, the general disaster relief program and its funding grew, adoptingexpanding concepts of assistance that once had beenassistance once reserved for catastrophic events to respond toaddress more common natural disasters. In the

16 While the president made a single announcement, the declarations themselves apply to each individual state, territory, or tribe.

17 https://www.whitehouse.gov/briefings-statements/letter-president-donald-j-trump-emergency-determination-stafford-act/

18 https://www.fema.gov/disasters/coronavirus/disaster-declarations, as retrieved October 15, 2020. FEMA also notes that 32 tribes are working with FEMA under the emergency declarations.

19 For more information on the Lost Wages Assistance program, see CRS Insight IN11492, COVID-19: Supplementing Unemployment Insurance Benefits (Federal Pandemic Unemployment Compensation vs. Lost Wages Assistance), by Katelin P. Isaacs and Julie M. Whittaker.

20 Federal Emergency Management Agency, Disaster Relief Fund: Monthly Report, October 9, 2020, pp. 13, 25, https://www.fema.gov/about/reports-and-data/disaster-relief-fund-monthly-reports.

21 Ibid., p. 13.

Congressional Research Service

5

The Disaster Relief Fund: Overview and Issues

more common natural disasters. In the 1970s, the Federal Emergency Management Agency (FEMA) was established, institutionalizing the federal role in disaster response, recovery, mitigation, and preparedness—the role we recognize today. At the heart of that role is the set of relief programs that have evolved since the 1940s, known collectively as the Stafford Act, which are funded by the Disaster Relief Fund appropriation.

1789-1947: Case by Case, After the Fact

The Constitution provides little specific direction on the question of how the United States should confront disasters. While allusions to the intent of the Constitution speak to promoting domestic tranquility and promoting the general welfare, limitations on the federal role in state affairs combined with practical politics of the day to limitthe balance of national priorities and federal resources constrained federal involvement in disaster relief and recovery in the early years of the country.

The federal government did provide disaster relief on some occasions. Some observers note at least 128 instances from 1803 to 1947 when natural disasters prompted the federal government to provide some type of ad hoc relief on a case-by-case basis for specific incidents after they occurred.1422 Prior to the Civil War, these measures largely consisted of refunds of duties paid on goods destroyed in customs house fires, allowanceallowances for delayed payments of bonds, and land grants for resettlement.15

23

Proponents of disaster relief argued that the "“general welfare"” clause of the Constitution warranted the federal role in disaster relief.1624 Opponents did not find this justification convincing, as it was nonspecific,1725 and argued that certain natural disasters (such as flooding of the Mississippi River) were foreseeable, and therefore state and local governments had an obligation to be prepared.1826 They also contended that it was improper for the government to provide relief for specific places with money it collected for the common good;1927 and that the federal government could not afford to provide universal relief.

As the U.S. economy became more robust, federal revenues grew, weakening the position of those in Congress who opposed a federal role in disaster assistance on the basis of the lack of such resources.

Congressional willingness to provide assistance was not always sufficient to ensure its provision, however. In 1887, President Grover Cleveland vetoed a bill that would have provided $10,000 to pay for seeds for farmers in Texas after a drought, arguing as follows:

I can find no warrant for such an appropriation in the Constitution; and I do not believe that the power and duty of the General Government ought to be extended to the relief of individual suffering which is in no manner properly related to the public service or benefit. A prevalent tendency to disregard the limited mission of this power and duty should, I A prevalent tendency to disregard the limited mission of this power and duty should, I

22 Moss, David A., “Courting Disaster: The Transformation of Federal Disaster Policy Since 1803.” In The Financing of Catastrophe Risk, edited by Kenneth A. Froot, Chicago: University of Chicago Press, 1999, p. 312.

23 A survey of customs duty relief and delayed payments on bonds can be found in the remarks of Rep. C. Johnson, “New York Fire,” Congressional Globe 24, p. 136 (February 17, 1836). 24 Rep. Carleton Hunt, “Relief of Sufferers by Flood,” House debate, Congressional Record, vol. 15, part 3 (March 26, 1884), p. 2295.

25 Rep. Charles Napoleon Brumm, “Relief of Sufferers by Flood,” House debate, Congressional Record, vol. 15, part 3 (March 26, 1884), p. 2296.

26 Rep. William Whitney Rice, “Relief of Sufferers by Flood,” House debate, Congressional Record, vol. 15, part 3 (March 26, 1884), p. 2293.

27 Rep. Lewis Beach, “Relief of Sufferers by Flood,” House debate, Congressional Record, vol. 15, part 3 (March 26, 1884), p. 2295.

Congressional Research Service

6

The Disaster Relief Fund: Overview and Issues

think, be steadfastly resisted, to the end that the lesson should be constantly enforced that though the people support the Government, the Government should not support the people.

The friendliness and charity of our countrymen can always be relied upon to relieve their fellow-citizens in misfortune. This has been repeatedly and quite lately demonstrated. Federal aid in such cases encourages the expectation of paternal care on the part of the Government and weakens the sturdiness of our national character, while it prevents the fellow-citizens in misfortune. This has been repeatedly and quite lately demonstrated. Federal aid in such cases encourages the expectation of paternal care on the part of the Government and weakens the sturdiness of our national character, while it prevents the indulgence among our people of that kindly sentiment and conduct which strengthens the bonds of a common brotherhood.20

28

Much of the disaster relief provided in this period was nongovernmental in nature. In 1881, Clara Barton founded the American National Red Cross (ANRC),2129 which provided disaster aid from funds it raised from private sources. One year before a catastrophic earthquake struck San Francisco in 1906, the incorporating legislation for the ANRC was revised to task the organization with "“mitigating the sufferings caused by pestilence, famine, fire, floods, and other great national calamities, and to devise and carry on measures for preventing the same."22”30 In the days after the earthquake, President Theodore Roosevelt issued an appeal for assistance from the public for the ANRC'’s relief efforts:

In the face of so horrible and appalling a national calamity as that which has befallen San Francisco, the outpouring of the nation'’s aid should, as far as possible, be entrusted to the American Red Cross, the national organization best fitted to undertake such relief work.... In order that this work may be well systematized and in order that the contributions, which I am sure will flow in with lavish generosity, may be wisely administered, I appeal to the people of the United States, to all cities, chambers of commerce, boards of trade, people of the United States, to all cities, chambers of commerce, boards of trade, relief committees and individuals to express their sympathy and render their aid by contributions to the American Red Cross.23

31

While the federal government provided assistance inad hoc response and recovery in theassistance to San Francisco case on an ad hoc basis, , the majority of the assistanceaid was provided was through private means. Congress appropriated $2.5 million in the days after the quake forto the Secretary of War to provide "“subsistence and quartermaster's ’s supplies ... to such destitute persons as have been rendered homeless or are in needy circumstances as a result of the earthquake and commissary stores to such injured and destitute persons as may require assistance,"24”32 but nonfederal cash contributions to the ANRC and the local relief organizations exceeded $9 million in the two years following the disaster.25

33

The ANRC served as the major institutional source of relief for disaster victims in the United States, serving communities and individuals in cooperation with state and local governments with relatively little direct contributionscontribution from the federal government for many years. The Red Cross continued to play a leading role in nongovernmental disaster relief as the federal government's ’s role in disaster aid evolved and expanded through the 20th century and into the 21st.

20th century and into the 21st. 28 House bill 10203, 50th Congress. Richardson, James D. (compiler), Compilation of the Messages and Papers of the Presidents (1897), Volume 11, page 5142. 29 This is the formal legal name of the organization commonly referred to as the American Red Cross. 30 P.L. 58-4, 23 Stat. 600. 31 Red Cross Flyer, Library of Congress Manuscript Division, made available through the Theodore Roosevelt Digital Library (www.theordorerooseveltcenter.org) at http://www.theodoreroosevelt.org/Research/Digital-Library/Record?libID=o529079. 32 Public Resolution No. 16, April 19, 1906, 34 Stat. 827. 33 O’Connor, Charles James, “San Francisco Relief Survey: The organization and methods of relief used after the earthquake and fire of April 18, 1906,” The Russell Sage Foundation, 1913, p. 33. Congressional Research Service 7 The Disaster Relief Fund: Overview and Issues 1947-1950: General Disaster Relief Funding from the Federal Government Begins

After the Second World War, the federal government started becoming more involved in disaster relief beyond specific incident-by-incident relief efforts. In 1947, P.L. 80-233 authorized the federal government to provide surplus property to state and local governments for disaster relief under the Disaster Surplus Property Program. Less than eight months later, the Administrator of the Federal Works Agency noted in a letter to President Harry S. Truman that the program would not provide adequate relief to communities over the longer term.

34

The next year, Congress made its first appropriation for general disaster relief. The Second Deficiency Appropriation Act, 1948,2635 which was enacted on June 25, 1948, provided funding directly to the President as follows:

DISASTER RELIEF

Disaster Relief: To enable the President, through such agency or agencies as he may

DISASTER RELIEF

Disaster Relief: To enable the President, through such agency or agencies as he may designate, and in such manner as he shall determine, to supplement the efforts and available resources of State and local governments or other agencies, whenever he finds that any local governments or other agencies, whenever he finds that any flood, fire, hurricane, earthquake, or other catastrophe in any part of the United States is of sufficient severity and magnitude to warrant emergency assistance by the sufficient severity and magnitude to warrant emergency assistance by the Federal Government in alleviating hardship, or suffering caused thereby, and if the governor of any State in which such catastrophe shall occur shall certify that such assistance is required, $500,000, to remain available until June 30, 1949, and to be expended without regard to such provisions regulating the expenditure of Government funds or the employment of such provisions regulating the expenditure of Government funds or the employment of persons in the Government service as he shall specify: Provided, That no expenditures shall be be made with respect to any such catastrophe in any State until the governor of such State shall have entered into an agreement with such agency of the Government as the President may designate giving assurance of expenditure of a reasonable amount of the funds of the government of such State, local governments therein, or other agencies, for the same or similar purposes with respect to such catastrophe: Provided further, That no part of this appropriation shall be expended for departmental personal services: Provided further, That no part of this appropriation shall be expended for permanent construction: no part of this appropriation shall be expended for permanent construction: Provided further, That within any affected area Federal agencies are authorized to participate in any such emergency assistance.27

36

Although this legislation comes with broad latitude for the President in expending these funds, this appropriation contained several hallmarks that continue in today'’s disaster relief structure:

-

the President makes the determination that a disaster has occurred, and that

federal aid is required;

- the state has a role in certifying the need and committing state resources to be eligible for federal support;

aid is to "34 U.S. President (Truman), “Letter to the Administrator, Federal Works Agency, on the Disaster Surplus Property Program,” Public Papers of the Presidents of the United States: Harry S. Truman, 1948 (Washington: GPO, 1964), p. 46. 35 P.L. 80-785. 36 The term “Disaster Relief Fund” as a title for the Disaster Relief appropriation seemed to have evolved informally. The Disaster Relief appropriation was initially provided under a heading of “Funds Appropriated to the President” (this practice would continue until the mid-1980s) and was described in its early years frequently as “the President’s disaster relief fund.” See, for example, Rep. Angell, “Second Deficiency Appropriation Bill, 1948,” House debate, Congressional Record, vol. 94, part 7 (June 16, 1948), p. 8467. Congressional Research Service 8 The Disaster Relief Fund: Overview and Issues aid is to “supplement the efforts and available resources of State and localsupplement the efforts and available resources of State and localgovernments or other agencies,"” rather than to fund the entire relief effort; and- the President may direct federal agencies to participate in emergency assistance.

The conditions laid out in this appropriation were echoed in the next two appropriations, provided in 1949, which totaled $1 million.28

37 1950-1966: The Disaster Relief Act of 1950—General Relief and Specific Relief

The Disaster Relief Act of 1950 formalized the structure outlined in the initial appropriations legislation, and indicated for the first time that

it is the intent of Congress to provide an orderly and continuing means of assistance by the Federal Government to States and local governments in carrying out their responsibilities to alleviate suffering and damage resulting from major disasters, to repair essential public facilities in major disasters, and to foster the development of such State and facilities in major disasters, and to foster the development of such State and local organizations and plans to cope with major disasters as may be necessary.29

38

Section 8 of the act limited the authorized disaster relief funding to $5 million in total.3039 This restriction did not effectively constrain funding, however. The first supplemental appropriation for general disaster relief authorized under the Disaster Relief Act for 1950 provided $25 million, and a waiver of the Section 8 limitation.3140 The first authorized annual appropriation for general disaster relief was for $800,000, enacted August 31, 1951, less than two months later.3241 Annual appropriations were "“to be available until expended,"” rather than expiring as previous general disaster relief appropriations had, and their use for administrative expenses was statutorily capped at 2% per year.33

42

Under the Kennedy and Johnson Administrations, the federal government'’s role in disaster relief expanded further.3443 Federal general disaster relief programs broadened in 1962, with the inclusion of several American territories, and provision of grants for repair of state facilities.35

44

However, Congress still passed specific legislation authorizing relief programs pursuant to other major disasters. In 1964 and 1965, post-disaster legislation provided specific relief for victims of an earthquake in Alaska,3645 flooding in western states,37 and victims of Hurricane Betsy in Florida, Louisiana, and Mississippi.3846 and Hurricane Betsy in Florida, Louisiana,

37 P.L. 81-3, P.L. 81-5; 63 Stat. 5. 38 P.L. 81-875; 64 Stat. 1109. 39 P.L. 81-875; 64 Stat. 1111. 40 P.L. 82-80; 65 Stat. 123. 41 P.L. 82-137; 65 Stat. 268. 42 This limitation would rise to three percent in an FY1956 supplemental appropriation (P.L. 84-406; 70 Stat. 12), and be carried in appropriations legislation through FY1979.

43 For a broader discussion of this evolution, see “The Evolution of U.S. Disaster Relief Policy,” by Bruce R. Lindsay and Francis X. McCarthy, in CRS Committee Print CP10000, The Evolving Congress: A Committee Print Prepared for the Senate Committee on Rules and Administration.

44 P.L. 87-592. 45 P.L. 88-451. 46 P.L. 89-41.

Congressional Research Service

9

The Disaster Relief Fund: Overview and Issues

and Mississippi.47 In a history of disaster relief legislation, one observer described the situation thus:

In 1962, 1964, and 1965, Congress had sought to preserve P.L. 81-875 [the Disaster Relief Act of 1950] and yet provide disaster assistance in the case of the very big disasters by special legislation only for the states named. Although no one at the time appeared aware that the new types of assistance would become precedents for general legislation, it was in the nature of the system that ultimately they would be reenacted for general use.39

48

1966-1974: The Disaster Relief Act of 1966—General Relief Broadens

Broadens The Disaster Relief Act of 196640196649 revised the general disaster assistance program by providing more assistance to public colleges and universities, as well as authorizing assistance to repair local public facilities.4150 The Disaster Relief Act of 196942196951 was enacted in response to Hurricane Camille, although the expansion of the federal role in disaster assistance it representedformalized had been included in legislation since 1965. It included broader public and individual assistance, including temporary housing, food assistance, unemployment assistance, andmatching funds to help states develop preparedness plans, and authorization for the federal government fundingto fund up to half the cost of repair and restoration of public facilities, and providing matching funds to help states develop preparedness plans.43.52 Not all of these costs would be borne by the funding provided to the President, and the programs were only authorized through calendar 1970, but they represented a significant broadening of federal government involvement.

The Disaster Relief Act of 197044197053 consolidated the previous disaster relief legislation into a single act, and made many of the Camille-driven programs permanent, including a permanent programprograms to provide temporary housing assistance, and programs for debris removal, and permanent repair and replacement of state and local public facilities.

1974-Present: The Era of Federally Coordinated Emergency Management

Management The Disaster Relief Act of 197445197454 provided for a more robust preparedness program, and introduced the concept of "emergency"“emergency” declarations to accommodate assistance in cases where an incident did not rise to the "“major disaster"” threshold.46

55

The Disaster Relief and Emergency Assistance Amendments of 1988 (P.L. 100-707, hereinafter DREAA) renamed the Disaster Relief Act of 1974 as the Robert T. Stafford Disaster Relief and

47 P.L. 89-339. 48 Frank P. Bourgin, A History of Federal Disaster Relief Legislation, 1950-1974, Federal Emergency Management Agency, Washington, DC, September 1983, p. 103.

49 P.L. 89-769. 50 Bourgin, p. 75. 51 P.L. 91-79. 52 Bourgin, p. 103. 53 P.L. 91-606. 54 P.L. 93-288. 55 Although it was expected to expire in December 1977, it was extended to the end of fiscal year 1980.

Congressional Research Service

10

The Disaster Relief Fund: Overview and Issues

Emergency Assistance Act (the aforementioned Stafford Act).56Emergency Assistance Act (the aforementioned Stafford Act).47 It made the following programmatic changes:

-

Authorized the President to declare an emergency under the Stafford Act in

"“any occasion or instance"” in which federal aid is needed—allowing for assistance without a major disaster declaration;48 - 57

Defined a

"“major disaster"” as"“any natural catastrophe ... or, regardless of cause, any fire, flood, or explosion, in any part of the United States, which in the determination of the President causes damage of sufficient severity and magnitude to warrant major disaster assistance...."49 - ”58 Established a 75% minimum level of assistance for the immediate response, debris removal, and repair of public facilities; and

-

Provided for a 50/50 cost share for hazard mitigation grants.

50

59 The Stafford Act and the DREAA are the pieces of legislation that structure the current relationship between the federal and state government in emergency management and disaster relief. These laws, which appear at 42 U.S.C. 5121 et seq., continue to be amended, with reform legislation frequently following on the heels of exceptionally large disasters, or complexes of disasters. This has happened three times since FEMA was incorporated into DHS in 2003:

1.1. The Post Katrina Emergency Reform Act of 2006 (PKEMRA)5160—Enacted as a sixth title to the FY2007 DHS Appropriations Act, PKREMRA reauthorized and restructured FEMA, and made amendments to the Stafford Act, including allowing federal assistance to be provided in the absence of a specific request, improved assistance for individuals with disabilities, and expanded availability of public assistance to non-governmental organizations.2.2. The Sandy Recovery Improvement Act (SRIA)5261—Enacted as a part of the FY2013 supplemental appropriations act, SRIA included alternative procedures for the Stafford Act Public Assistance program to allow disaster impacted area to get assistance on the basis of cost estimates rather than reimbursement of costs, among other reforms.3.3. The Disaster Recovery Reform Act of 2018 (DRRA)5362—Enacted through language that was attached to an FAA reauthorization measure in the wake of wildfires in California as well as Hurricanes Harvey, Irma, and Maria, DRRA has provisions to broaden federal investments from the DRF into mitigation effortstothat protect public infrastructure, as well as making improvements to the Public Assistance and Individual Assistance programs. For additional information on these reforms, see CRS Report R45819, The Disaster Recovery Reform Act of 2018 (DRRA): A Summary of Selected Statutory Provisions, coordinated by Elizabeth M. Webster and Bruce R. Lindsay.

.

56 P.L. 100-707. 57 102 Stat. 4689. 58 102 Stat. 4690. 59 These grants would be amended in 1993 to a 75/25 cost share. 60 P.L. 109-295, Title VI. 61 P.L. 113-2, Division B. 62 P.L. 115-254, Division D.

Congressional Research Service

11

The Disaster Relief Fund: Overview and Issues

Pandemic COVID-19 and the Stafford Act

With the COVID-19 response, major disaster assistance programs under the Stafford Act authorities are being used for the first time to respond to an infectious disease outbreak.63

Remarks from the passage of the Stafford Act seem to indicate that this may not have been what the architects of the measure envisioned. While not explicitly excluding the use of the major disaster declaration for infectious disease, Rep. Arlen Stangeland (R-MN), the Ranking Member of the Subcommittee on Water Resources of the House Public Works and Transportation Committee, noted in his comments on the final version of the bill that other authorities existed for public health matters:

Title I reorganizes the disaster relief program to clearly define Presidential authority to respond to major disasters and emergencies. Major disasters would include primarily natural catastrophes or, in certain instances, nonnatural catastrophes while emergencies would include any occasion or instance in which Federal assistance was necessary. However, we do not intend for emergency declarations to be available in responding to public health problems such as disease epidemics or environmental or nuclear catastrophes for which Federal assistance is already available...

On March 13, 2020, President Donald J. Trump made a series of emergency declarations under Section 501(b) of the Stafford Act in response to the nationwide spread of a novel coronavirus disease (COVID-19).64 The declarations authorized assistance to all U.S. states, territories, tribes, and the District of Columbia. At the time he announced the declarations, he invited the recipients of those declarations to request major disaster declarations.65 FEMA notes that 50 states, four territories, and the District of Columbia have all requested and received major disaster declarations for COVID-19 response.66

Later that month, a supplemental appropriation for the DRF was provided in the CARES Act, P.L. 116-136, Division B, providing $45 billion in emergency-designated supplemental appropriations. As with other DRF appropriations, this funding was not provided specifically for COVID-19 efforts, but for Stafford Act programs more broadly. From March 13, 2020, through July 31, 2020 (from the declarations through the end of the third quarter), FEMA spent $7.271 billion from the DRF on Stafford Act costs related to COVID-19 declarations: $3.700 billion on operating expenses, and $3.289 billion on Public Assistance programs, which reimburses eligible public and nonprofit entities for the costs of major disaster response and recovery. $179 million was provided through the Individual Assistance program.

On August 8, 2020, the Administration announced a new “lost wages assistance” program, which would expand and extend unemployment benefits for several weeks using up to $44 billion from the DRF. This initiative would be implemented through the Other Needs Assistance program under the Individual Assistance programs under the Stafford Act.67 Almost $43 billion was

63 Two emergency declarations under the Stafford Act were made in the fall of 2000 for West Nile virus control. 64 While the president made a single announcement, the declarations themselves apply to each individual state, territory, or tribe.

65 https://www.whitehouse.gov/briefings-statements/letter-president-donald-j-trump-emergency-determination-stafford-act/

66 https://www.fema.gov/disasters/coronavirus/disaster-declarations, as retrieved October 15, 2020. FEMA also notes that 32 tribes are working with FEMA under the emergency declarations.

67 For more information on the Lost Wages Assistance program, see CRS Insight IN11492, COVID-19: Supplementing Unemployment Insurance Benefits (Federal Pandemic Unemployment Compensation vs. Lost Wages Assistance), by Katelin P. Isaacs and Julie M. Whittaker.

Congressional Research Service

12

The Disaster Relief Fund: Overview and Issues

obligated for this program before it terminated68—more than three-quarters of the DRF obligations related to COVID-19 to that point,69 and more than six times the $6.8 billion obligated under the ONA program to that point since its inception in 2002.70

As of the end of FY2020, FEMA had associated $52.681 billion in DRF spending with the COVID-19 response. $42.143 billion was provided through the Individual Assistance program, the vast majority of which was for the lost wages initiative. $6.058 billion was provided for Public Assistance programs, and $4.319 billion was for FEMA’s operational costs.

It remains to be seen whether the Stafford Act COVID-19 response is a new model for dealing with public health issues. Congress may choose to refine this novel application, or reset the authorities of the Stafford Act along its earlier precedents.

Appropriations for General Disaster Relief

Appropriations for General Disaster Relief

Types of Appropriations for Disaster Relief

General disaster relief activities by the federal government under the Stafford Act are funded through the appropriations process. Three types of appropriations support these activities:

Supplemental Appropriations are requested by the Administration on an ad hoc basis, generally to address a need not sufficiently covered in the annual appropriations process. These move on a short timetable and generally do not go through the complete committee process. More than 82% of net appropriations for the DRF have been provided through supplemental appropriations.

Annual Appropriations: Requested by the Administration in February as a part of the annual budget process, these are expected to be passed by Congress and enacted into law prior to the start of the fiscal year in October. Annual appropriations measures fund the core activities of the government and are developed through the committee process.

Continuing Appropriations: Provided when annual appropriations work remains unresolved at the beginning of the new fiscal year, these appropriations are temporary budget authority provided at a rate for operations based on the prior fiscal year to allow the government to continue functioning. The measure that provides them is termed a "“continuing resolution,"” or "CR."“CR.” These continuing appropriations may expire (in the case of an interim CR), or extend to the end of the fiscal year (in the case of a "“long-term"” CR).

Supplemental Appropriations for Disaster Relief

The current Disaster Relief Fund concept can trace its birth back to an appropriations bill in the 1940s—the Second Deficiency Appropriations Act, 1948.5471 Deficiency appropriations bills, which provided funding to meet unanticipated needs during the fiscal year, were a forerunner of modern supplemental appropriations bills. The severity, frequency, and resultant costs to the federal government offrom the array of disasters that will strike the United States have always been strike the United States have always been

68 Federal Emergency Management Agency, “Lost Wages Assistance Totals,” October 26, 2020, email from FEMA Congressional Affairs.

69 October 2020 Disaster Relief Fund Report, pp. 13, 25, https://www.fema.gov/about/reports-and-data/disaster-relief-fund-monthly-reportscccccchfrtbcnttilrgfvrnecgthdnhvbfibvlclvrkd.

70 CRS analysis of ONA data from OpenFEMA databases downloaded October 27, 2020. 71 P.L. 80-785.

Congressional Research Service

13

link to page 20 link to page 20 The Disaster Relief Fund: Overview and Issues

unpredictable in an annual budgetary context. To respond to this uncertainty, disaster relief funding frequently has been provided through deficiency, and later supplemental, appropriations.

When Congress and the Administration began to express concerns about the budget deficit in the 1980s, efforts were made to restrain supplemental spending by limiting it to cases of "“dire emergency."” With the implementation of budget control in the 1990s, a special designation for emergency spending was created. If both Congress and the Administration agreed that certain spending was an emergency requirement, budget limits would be adjusted to accommodate that spending. Congress used the emergency designation on a disaster relief appropriation for the first time in an FY1992 supplemental appropriations act.5572 Congress continues to use emergency designations in supplemental appropriations legislation to provide budgetary flexibility.

At one point, Congress was statutorily required to use the designation for disaster relief appropriations. Under the terms of the aforementioned FY1992 supplemental appropriations act, beginning in FY1993, Congress required "“all amounts appropriated for disaster assistance payments [under the Stafford Act] that are in excess of either the historical annual average obligation of $320,000,000, or the amount submitted in the President'’s initial budget request, whichever is lower" to” be designated as emergency requirements under a specific provision of the Balanced Budget and Emergency Deficit Control Act of 1985.5673 This practice of emergency designation above a particular threshold was followed until FY2000, when a clause appeared in the appropriation noting that discretionary appropriations were being provided notwithstanding the restrictions of this section of the U.S. Code.57

74

With the passage of the Budget Control Act in 2011, which provided additional budgetary flexibility for the costs for major disasters, supplemental disaster relief appropriations declined in frequency, but remained a primary contributor to balances in the DRF. See the "“DRF Funding History: FY1964-FY2019"FY20” section below for details.

Annual Appropriations

As was noted above, the

The first general disaster relief funding was provided in an annual appropriations act in 1948, and carried its own authorizing provisions. Stand-alone authorization for general disaster relief first came in 1950.

Once the initial separate authorization was put in place for general disaster relief, appropriations were provided for FY1952, FY1956-FY1958, and FY1962. With the broadening of the relief program to cover more types of damages and the authorization of aid on general terms that had only been made on a case-by-case basis before the mid-1960s, appropriations for general disaster relief became more common—and larger. Annual appropriations for general disaster relief have been provided each year since FY1964, with only two exceptions.58

As noted above, with the development, codification, and expansion of the federal role in emergency management, appropriations for general disaster relief became more common—and larger. Annual appropriations for general disaster relief have been provided each year since FY1964, with only two exceptions.75

72 P.L. 102-229, the “Dire Emergency Supplemental Appropriations and Transfers for Relief from the Effects of Natural Disasters, for Other Urgent Needs, and for Incremental Cost of ‘Operation Desert Shield/Desert Storm’ Act of 1992.” 73 P.L. 102-229, 105 Stat. 1711. The reference remains in law as 42 U.S.C §5203, but P.L. 105-33, the Balanced Budget Act of 1997 (at 111 Stat. 699) changed the underlying law on which the requirement depended.

74 P.L. 106-74, at 115 Stat. 687. The same clause appeared in FY2003, but has not been a part of enacted DRF appropriations since then.

75 In FY1984 and FY1991, no appropriation was requested or made for disaster relief, as unobligated balances were deemed sufficient to fund anticipated disasters. See Federal Emergency Management Agency, Justification of Estimates, Fiscal Year 1984, Part 2, Washington, DC, January 1983, p. DR-3, and Federal Emergency Management Agency, Justification of Estimates, Fiscal Year 1992, Washington, DC, February 1991, p. DR-3.

Congressional Research Service

14

link to page 27 The Disaster Relief Fund: Overview and Issues

Disaster Relief Designation Disaster Relief Designation

The adoption of a special designation for the costs of major disasters under the Stafford Act as a part of the Budget Control Act of 2011 (P.L. 112-25) made it easier to provide budget authority to the DRF in the annual appropriations process.5976 In the first seven appropriations cycles since the implementation of this designation in FY2012, more budget authority was provided for the DRF in annual appropriations measures than in the 63 prior cycles combined, accounting for inflation. The gross appropriation for the DRF of $12.558 billion in FY2019 was the largest annual appropriation ever for the DRF, breaking the record set by the FY2018 annual appropriation. That record appears likely to be broken again, as the Trump Administration requested $14.550 billion for the DRF in FY2020, and both House and Senate committee-reported annual DHS appropriations bills meet or exceed that funding level.

Since the FY2013 budget request, FEMA has bifurcated its annual appropriations request between the costs of major disasters—the "“Disaster Relief Category"”—and everything else funded by the DRF—"“Base Disaster Relief,"” which includes funding for emergency designations, fire management assistance, pre-disaster declaration surge activities, and Disaster Readiness and Support Programs. The former category is eligible for the designation as "“disaster relief,"” a designation that triggers an upward adjustment of statutory discretionary spending limits to accommodate it without triggering sequestration. The latter category is not, and scores as discretionary spending.

With the supplemental appropriation provided in the CARES Act, a new approach was taken. Of the $45 billion funds in emergency-designated supplemental funds, $25 billion was specified as being for the cost of major disasters, and $15 million was specified as being for any Stafford Act activities—including those activities in the base as well as major disasters—allowing those funds to be used more flexibly in the face of the COVID-19 epidemic, without requiring a reprogramming or transfer.77

Continuing Appropriations

Continuing Appropriations

Even though the DRF is a "“no-year"” fund, and its appropriations are available until expended, it does get temporary replenishment from continuing resolutions (CRs) at times, until its annual appropriations are finalized.

In FY1982, for the first time, interim general disaster relief funding was provided in a CR through an "“anomaly,"” a provision providing funds at an operating rate different from that base rate of operations provided in the resolution.60

These "anomaly"78

These “anomaly” provisions may also provide flexibility that can help avoid some of the complications that can arise under the constraints of operating under continuing appropriations. For example, CRs generally provide funding at a constant rate of operations, with certain restrictions. This can complicate disaster response and recovery, when calls for funding vary in scale and timing from year to year. When FEMA responds to major disasters of significant size while operating under a CR, eitherThe DRF could, in some circumstances, risk being depleted

76 See “Changes in the Budget Process” and CRS In Focus IF10720, Calculation and Use of the Disaster Relief Allowable Adjustment.

77 FEMA did not choose to publicly track those funds separately, but instead first included them in its totals for the DRF base in its monthly reporting on DRF balances. Once it became clear that the largest draw on resources for COVID-19 efforts would be based on the major disaster declarations, FEMA accounted for these funds in the major disaster designated portion starting in May 2020.

78 P.L. 97-92; 95 Stat. 1187.

Congressional Research Service

15

link to page 38 The Disaster Relief Fund: Overview and Issues

by response and recovery needs while operating under a CR. This risk can be addressed in one of two ways: responsively, when FEMA requests special flexibility from the Office of Management and Budget (OMB)—which apportions CR funding to agencies—or CRs direct flexibility to; or proactively, when a special provision is included in the CR that directs such flexibility be provided to ensure adequate resources are available for disaster response and recovery. Such language can be found in the initial CRs for FY2018 through FY2020FY2021, which all provide that the funds provided "“may be apportioned up to the rate for operations necessary to carry out response and recovery activities"” under the Stafford Act.61

79 Lapses in Annual Appropriations and the DRF

Most annual appropriations expire at the end of the fiscal year. On several occasions in recent history, neither annual nor continuing appropriations were enacted prior to the beginning of the fiscal year, leading to a The Disaster Relief appropriation can fund disaster relief operations, as its appropriations do not expire at the end of the fiscal year, but lapses in annual appropriations have an impact on agency efficiency. Some disaster-related functions have been subject to emergency furlough in the past. |

DRF Funding History: FY1964-FY2019

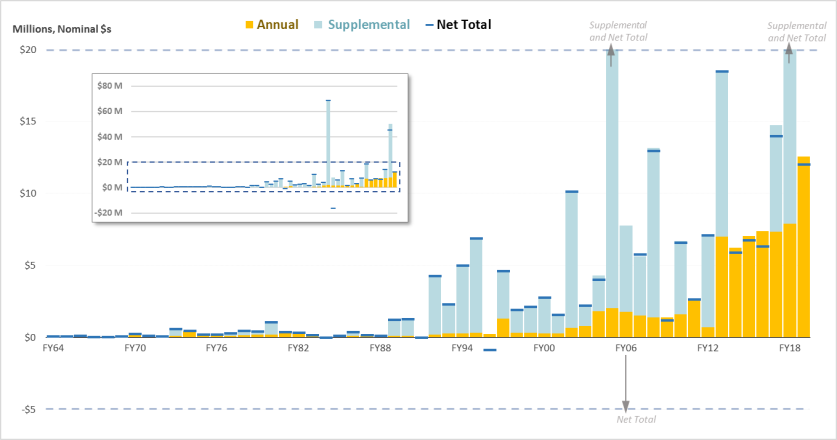

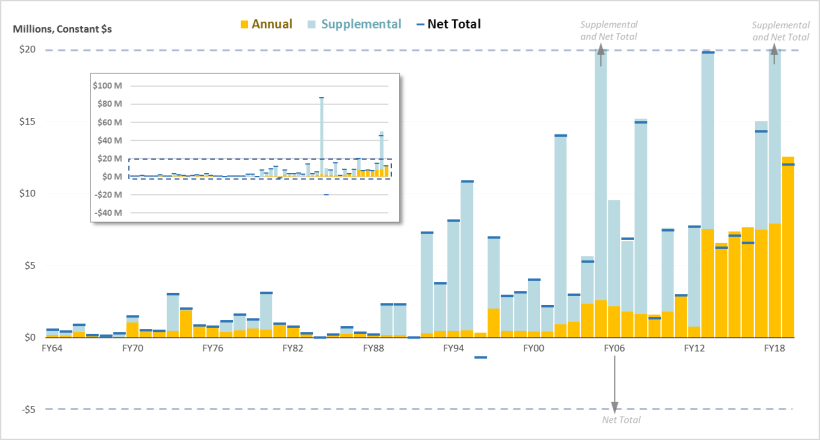

FY2020 The following figures show appropriations for the DRF from FY1964 through FY2019.

FY2020.

Each fiscal year shows a gross total of annual appropriations and discretionary appropriations (represented by a two-part bar) and a net total (represented by a black mark on each bar), which takes into account rescissions and transfers from the DRF. An inset graphic provides the scale to include funding levels for several outlier years,6381 while showing the detail of appropriations for the more typical years. The first figure shows data in nominal dollars, and the second shows constant FY2019FY2020 dollars.

The figures show an increase in appropriations for the DRF starting in the 1990s, largely due to increases in supplemental appropriations. Annual appropriations rose significantly in the early 2000s and again starting in FY2013. Even with the surge in appropriations for the 2017 catastrophic series of disasters, which included Hurricane Harvey, Hurricane Maria, and the California wildfires, and the large supplemental appropriation for the DRF for COVID-19 in FY2020, FY2005 remains the single highest year for appropriations for the DRF, when a series of hurricanes, including Katrina, Rita, and Wilma hit the southeastern United States.64

82

A table showing the underlying data for each figure appears in the Appendix.

79 P.L. 115-56, Division D, §129; P.L. 115-245, Division C, §124; and P.L. 116-59, §133. 80 For details, see CRS Report R43252, FY2014 Appropriations Lapse and the Department of Homeland Security: Impact and Legislation, by William L. Painter.

81 FY2005, FY2006, and FY2017. 82 The following year, a significant amount of what had been provided was rescinded and re-appropriated to other agencies to provide disaster assistance and repair storm and flood damage.

Congressional Research Service

16

Figure 1. Nominal Dollar Disaster Relief Appropriations, FY1964-FY2020

Source Appendix.

|

|

Source: CRS analysis of appropriations laws. : CRS analysis of appropriations laws. Notes: Totals for FY2005, FY2006, |

CRS-17

Figure 2. |

|

FY2020 Source: CRS analysis of appropriations laws. Notes: Totals for FY2005, FY2006, |

CRS-18

link to page 22 The Disaster Relief Fund: Overview and Issues

Factors in Changing Appropriations Levels

FEMA' For years, FEMA’s budget justifications have noted for years, in one form or another, that "“[t]he primary cost driver associated with Major Disasters is disaster activity."65 Although”83 While year-to-year disaster relief appropriations are largely driven by disaster activity and ongoing recovery needs, when analyzing historical data over an extended time frame, other factors such as programmatic changes in general disaster relief and certain changes in the budget process may also warrant consideration.

Incident Frequency and Severity

The two largest factors affecting year-to-year disaster relief appropriations are disaster activity, which varies in frequency and severity, and the ongoing recovery costs from previous disasters. Federal involvement in disaster response and recovery occurs when lower levels of government find their capabilities are overwhelmed and turn to the federal government for help. Reduced (or increased) numbers of calls for relief mean reduced (or increased) need for disaster relief appropriations.

The incidents that lead to expenditures from the DRF vary in scale. Equally powerful storms may strike a community with a glancing blow or a direct hit. An earthquake may hitstrike a rural area, or a major city with complex infrastructure. Stricken communities, states, territories, and tribes have varying levels of preparedness for particular types of disaster. Spending to help large, complex communities rebuild disaster-damaged facilities and infrastructure and mitigate against future disasters is a significant multiyear cost largely paid for from the Disaster Relief Fund.

, and different amounts of public infrastructure to repair and replace.

Some observers have noted that as the U.S. population grows and develops property in disaster-prone areas, and as patterns of severe weather shift, the costs of disasters are likely to continue to rise.6684 According to the National Centers for Environmental Information of the National Oceanic and Atmospheric Administration, from 1980 through October 20192020, the United States has averaged between six and sevenaveraged slightly more than six weather-related disaster events that each cost $1 billion or more each year.85 From 1980 through 2007, more than seven billion-dollar events occurred in only one year (1998). Since 2007, these events have become more frequent: only one year since 2007only one year has seen fewer than seven such events, and ten or more such events have occurred each year from 2015 to 2019.67

Using Figure 2, one can contrast thissince 2015. The United States was struck by an annual record-tying 16 such events in just the first nine months of 2020.86

The contrast between the period of high-frequency, high-impact events ofin the 2010s toand the relatively calm period of the 1980s is illustrated in Figure 2. . Without the driver of large disasters, DRF appropriations remained modest. OverDuring the period from FY1981 to FY1991, abnormally low levels of disaster activity led to no supplemental appropriations for 7 of those 11 fiscal years, and no annual appropriations in either FY1984 or FY1991—the only two fiscal years for which this has occurred since FY1964. By contrast, over the last six years, the DRF has required sustained high levels of appropriations, including three of its six highest total appropriations ever

83 Department of Homeland Security, Disaster Relief Fund, Fiscal Year 2019 Congressional Budget Justification, Federal Emergency Management Agency, Washington, DC, February 2018, p. FEMA-DRF-30, https://www.dhs.gov/sites/default/files/publications/Federal%20Emergency%20Management%20Agency.pdf.

84 For information on forecasts for hurricane-specific disaster costs, see Congressional Budget Office, Potential Increases in Hurricane Damage in the United States: Implications for the Federal Budget, Washington, DC, June 2016, https://www.cbo.gov/publication/51518.

85 These cost figures are based on CPI-adjusted data. 86 NOAA, National Centers for Environmental Information (NCEI), U.S. Billion-Dollar Weather and Climate Disasters (2018), https://www.ncdc.noaa.gov/billions/.

Congressional Research Service

19

link to page 24 The Disaster Relief Fund: Overview and Issues

by fiscal year, even adjusting for inflation, and back-to-back largest annual appropriations in FY2018 and FY2019.

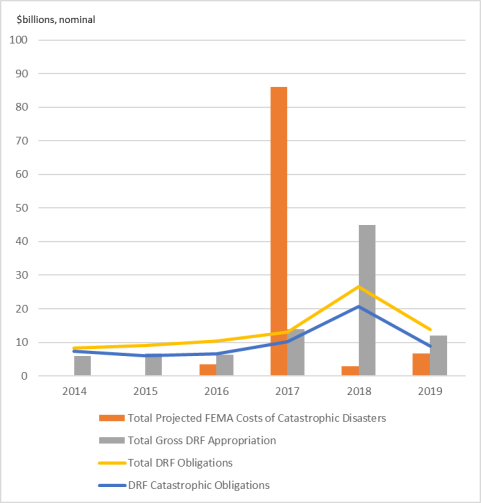

Further analysis of recent years shows the association between spending fromappropriations for the DRF and the frequency of high-cost events is closer than the association with the number of major disaster declarations. Table 1 shows data from FEMA regarding the number of major disasters declared from FY2004 through FY2019. It also shows FEMA'’s accounting for the number of major disasters incurring more than $500 million in projected costs to FEMA in terms of the federal share of Stafford Act programs, and the totals of those costs by fiscal year of the incident. The last column shows the total gross appropriations for the DRF for each fiscal year.

Table 1. Disaster Declaration Activities and Projected Costs of Catastrophic

Disaster Declarations, FY2004-FY2019

Total

Projected

FEMA Costs of

Total Gross

Number of

Number of

Catastrophic

DRF

Major

Catastrophic

Disasters

Appropriation

Disaster

Disaster

($millions,

($millions,

Fiscal Year

Declarations

Declarations

nominal)

nominal)

2004

65

5

6,906

4,023

2005

45

5

47,919

68,427

2006

53

1

2,606

-16,391

2007

67

0

—

5,743

2008

68

3

8,048

12,935

2009

63

0

—

1,178

2010

79

1

573

6,573

2011

98

2

1,344

2,650

2012

46

1

706

7,076

2013

65

3

22,767

18,469

2014

48

0

—

5,897

2015

44

0

—

6,729

2016

41

2

3,407

6,329

2017

60

8

85,991

13,996

2018

54

2

2,914

45,011

2019

53

4

6,628

12,005

Total

949

37

189,809

200,650

Annual

59.3

2.3

11,863

12,541

Average

Source: Email from FEMA Office of Congressional Affairs to CRS, September 24, 2019, and data from FEMA’s Disaster Declarations, FY2004-FY2019

|

Fiscal Year |

Number of Major Disaster Declarations |

Number of Catastrophic Disaster Declarations |

Total Projected FEMA Costs of Catastrophic Disasters ($millions, nominal) |