Fiscal Policy: Economic Effects

Changes from May 16, 2019 to January 21, 2021

This page shows textual changes in the document between the two versions indicated in the dates above. Textual matter removed in the later version is indicated with red strikethrough and textual matter added in the later version is indicated with blue.

Contents

- What is Fiscal Policy?

- Expansionary Fiscal Policy

- Potential Offsetting Effects to Expansionary Fiscal Policy

- Investment and Interest Rates

- Exchange Rates and the Trade Balance

- Inflation

- Fiscal Expansion Multipliers

- Long-Term Considerations Regarding Fiscal Stimulus

- Unsustainable Public Debt

- Decreased Business Investment

- Crowding Out Government Spending

- Withdrawing Fiscal Stimulus

- Potential Offsetting Effects to Withdrawing Fiscal Stimulus

- Investment and Interest Rates

- Exchange Rates and the Trade Balance

- Inflation

- Fiscal Contraction Multipliers

- Fiscal Policy Stance

Summary

Fiscal policy is the means by which the government adjusts its spending and revenue to influence the broader Fiscal Policy: Economic Effects

January 21, 2021

Fiscal policy describes changes to government spending and revenue behavior in an effort to influence the economy. By adjusting its level of spending and tax revenue, the government can affect the economy by either increasing or decreasing economic activity in the short term. For example,

Lida R. Weinstock

affect economic outcomes by either increasing or decreasing economic activity. For example,

Analyst in Macroeconomic

when the government runs a budget deficit, it is said to be engaging in fiscal stimulus, spurring —spurring

Policy

economic activity, —and when the government runs a budget surplus, it is said to be engaging in a a

fiscal contraction, —slowing economic activity.

The government can use fiscal stimulus to spur economic activity by increasing government spending, decreasing tax revenue, or a combination of the two. Increasing government spending tends to encourage economic activity either directly through purchasingthe purchase of additional goods and services from the private sector or indirectly by transferringthe transfer of funds to individuals who may then spend that money. Decreasing tax revenue tends to encourage economic activity indirectly by increasing individuals'’ disposable income, which tends tocan lead to those individuals consuming more goods and services. This sort of expansionary fiscal policy can be beneficial when the economy is in recession, as it lessens the negative impacts of a recession, such as elevated unemployment and stagnant wages. However, expansionary fiscal policy can result in rising interest rates, growing trade deficits, and accelerating inflation, particularly if applied during healthy economic expansions. These side effects from expansionary fiscal policy tend to partly offset its stimulative effects.

The government can use contractionary fiscal policy to slow economic activity by decreasing government spending, increasing tax revenue, or a combination of the two. Decreasing government spending tends to slow economic activity as the government purchases fewer goods and services from the private sector. Increasing tax revenue tends to slow economic activity by decreasing individuals'’ disposable income, likely causing them to decrease spending on goods and services. As the economy exits a recession and begins to grow at a healthy pace, policymakers may choose to reduce fiscal stimulus to avoid some of the negative consequences of expansionary fiscal policy, —such as rising interest rates, growing trade deficits, and accelerating inflation, —or to manage the level of public debt.

In recent history, the federal government has generally followed a pattern of increasing fiscal stimulus during a recession, then decreasing fiscal stimulus during the economic recovery.

Prior to the "“Great Recession"” of 2007-2009, the federal budget deficit was about 1% of gross domestic product (GDP) in 2007. During the recession, the budget deficit grew to nearly 10% of GDP in part due to additional fiscal stimulus applied to the economy. The budget deficit began shrinking in 2010, falling to about 2% of GDP by 2015. In contrast to the typical pattern of fiscal policy, the budget deficit began growing again in 2016, rising to nearly 45% of GDP in 20182019 despite relatively strong economic conditions. This change in fiscal policy is notable, as expanding fiscal stimulus when the economy is not depressed can result in rising interest rates, a growing trade deficit, and accelerating inflation. As of publication of this report, interest rates have not risen discernibly and are still near historic lows, and inflation rates show no sign of acceleration. The trade deficit has been growing in recent years; however, it is not clear that this growth in the trade deficit is a result of increased fiscal stimulus.

The federal government has two major tools for affecting the macroeconomy

The Coronavirus Disease 2019 (COVID-19) pandemic has caused a historically severe recession. Several relief bills were enacted in response, including the Coronavirus Preparedness and Response Supplemental Appropriations Act, 2020 (P.L. 116-123); the Families First Coronavirus Response Act (P.L. 116-127); the Coronavirus Aid, Relief, and Economic Security (CARES) Act (P.L. 116-136); and the Paycheck Protection Program and Health Care Enhancement Act (P.L. 116-139). These measures significantly increased the deficit, which totaled $3.1 trillion in FY2020 and amounted to 14.9% of GDP, the largest share since the end of World War II. Additional coronavirus relief was included in the Consolidated Appropriations Act, 2021 (P.L. 116-260).

Congressional Research Service

link to page 4 link to page 4 link to page 5 link to page 5 link to page 6 link to page 6 link to page 7 link to page 8 link to page 9 link to page 9 link to page 10 link to page 10 link to page 11 link to page 11 link to page 11 link to page 11 link to page 11 link to page 12 link to page 13 link to page 8 link to page 14 Fiscal Policy: Economic Effects

Contents

What Is Fiscal Policy? ..................................................................................................... 1 Expansionary Fiscal Policy ............................................................................................... 1

Potential Offsetting Effects to Expansionary Fiscal Policy ............................................... 2

Investment and Interest Rates ................................................................................. 2 Exchange Rates and the Trade Balance .................................................................... 3 Inflation .............................................................................................................. 3

Fiscal Expansion Multipliers ....................................................................................... 4

Considerations Regarding Persistent Fiscal Stimulus....................................................... 5

Unsustainable Public Debt ..................................................................................... 6 Decreased Business Investment .............................................................................. 6 Crowding Out Government Spending ...................................................................... 7

Withdrawing Fiscal Stimulus ............................................................................................ 7

Potential Offsetting Effects to Withdrawing Fiscal Stimulus ............................................. 8

Investment and Interest Rates ................................................................................. 8 Exchange Rates and the Trade Balance .................................................................... 8

Inflation .............................................................................................................. 8

Fiscal Contraction Multipliers ..................................................................................... 8

Fiscal Policy Stance ........................................................................................................ 9

Figures Figure 1. Federal Budget Deficit/Surplus .......................................................................... 10

Tables

Table 1. Average First-Year Fiscal Multipliers for Stimulus in Selected Models ........................ 5

Contacts Author Information ....................................................................................................... 11

Congressional Research Service

Fiscal Policy: Economic Effects

he federal government has two major tools for affecting the macroeconomy (in this case, the whole, or aggregate, U.S. economy): fiscal policy and monetary policy. These policy

T : fiscal policy and monetary policy. These policy interventions are generallygeneraly used to either increase or decrease economic activity to counter

the business cycle'’s impact on unemployment, income, and inflation. This report focuses on fiscal policy; forpolicy. For more information related to monetary policy, refer to CRS Report RL30354, Monetary

Policy and the Federal Reserve: Current Policy and Conditions, by Marc Labonte.

What isIs Fiscal Policy?

Fiscal policy is the means by which the government adjusts its budget balance through spending and revenue changes to influence broader economic conditions. According to mainstream economics, the Fiscal policy describes changes to government spending and revenue behavior in an effort to influence economic outcomes. The government can impact the level of economic activity, generally (often measured by gross domestic product (GDP),[GDP]) in the short term by changing its level of spending and tax revenue.1 Expansionary fiscal policy—an increase in government spending, a decrease in

tax revenue, or a combination of the two—is expected to spur economic activity, whereas contractionary fiscal policy—a decrease in government spending, an increase in tax revenue, or a combination of the two—is expected to slow economic activity. When the government'’s budget is running a deficit (when spending exceeds revenues), fiscal policy is said to be expansionary: when. When it is running a surplus (when revenues exceed spending), fiscal policy is said to be contractionary.

contractionary.

From a policymaker'’s perspective, expansionary fiscal policy is generallygeneral y used to boost GDP growth and the economic indicators that tend to move with GDP, such as employment and individual

individual incomes. However, expansionary fiscal policy also tends to affect interest rates and investment, exchange rates and the trade balance, and the inflation rate in undesirable ways, limiting limiting the long-term effectiveness of persistent fiscal stimulus. Contractionary fiscal policy can be used to slow economic activity if policymakers are concerned that the economy may be overheating, which can cause a recession. The magnitude of fiscal policy'’s effect on GDP will wil also differ based on where the economy is within the business cycle—whether it is in a recession

or an expansion.2

1 Expansionary Fiscal Policy

During a recession, aggregate demand (overall overal spending) in the economy fallsfal s, which generally general y results in slower wage growth, decreased employment, lower business revenue, and lower business investment. As seen during the current recession caused by the Coronavirus Disease

2019 (COVID-19) pandemic, recessions often lead tobusiness investment. Recessions occur for a number of reasons, but as seen during the most recent recession from 2007 to 2009, they can result in serious negative consequences for both individuals individuals and businesses.3 However, the2 The government can replace some of the lost aggregate demand and limit the negative impacts of a recession on individuals and businesses with the use of fiscal stimulus by increasing government spending, decreasing tax revenue, or a combination of the two. Government spending takes the form of both purchases of goods and services by the government, which directly

increase economic activity, and transfers to individuals, which indirectly increase economic activity as individuals spend those funds. Decreased tax revenue via tax cuts indirectly increases aggregate demand in the economy. For example, an individual income tax cut increases the

1 T he economy shifts from periods of increasing economic activity, known as economic expansions, to periods of decreasing economic activity, known as recession s. For more information, see CRS In Focus IF10411, Introduction to U.S. Econom y: The Business Cycle and Growth , by Lida R. Weinstock.

2 For more information on the causes of recessions, see CRS Insight IN10853, What Causes a Recession?, by Marc Labonte.

Congressional Research Service

1

Fiscal Policy: Economic Effects

amount of disposable income available amount of disposable income available to individuals, enabling them to purchase more goods and services. Standard economic theory suggests that in the short term, fiscal stimulus can lessen the negative impacts of a recession or hasten a recovery.43 However, the ability of fiscal stimulus to boost aggregate demand may be limited due to its interaction with other economic processes, including interest rates and investment, exchange rates and the trade balance, and the rate of inflation.

inflation. Potential Offsetting Effects to Expansionary Fiscal Policy

Investment and Interest Rates

To engage in fiscal stimulus by either increasing spending or decreasing tax revenue, the government must increase the size of its deficit and borrow money to finance that stimulus. This

can lead to an increase in interest rates and subsequent decreases in investment and some consumer spending.54 This rise in interest rates may therefore offset some portion of the increase

in economic activity spurred by fiscal stimulus.

At any given time, there is a limited supply of loanable funds available for the government and private parties to borrow from—a global pool of savings. If the government begins to borrow a larger portion of this pool of savings, it increases the demand for these funds. As demand for loanable funds increases, without any corresponding increase in the supply of these funds, the price to borrow these funds, (also known as interest rates,) increases. Rising interest rates generally general y

depress economic activity, as they make it more expensive for businesses to borrow money and invest in their firms. Similarly, individuals tend to decrease so-calledcal ed interest-sensitive spending—spending on goods and services that require a loan, such as cars, homes, and large appliances—when interest rates are relatively higher.65 The process through which rising interest rates diminish private- sector spending is often referred to as crowding out.76 However, the degree

to which crowding out occurs is partiallypartial y dependent on where the economy is within the business cycle,

cycle: either in a recession or in a healthy expansion.

During a recession, crowding out tends to be smallersmal er than during a healthy economic expansion

due to already depressed demand for investment and interest-sensitive spending. Because demand for loanable funds is already depressed during a recession, the additional demand created by government borrowing does not increase interest rates as much, and therefore does not crowd out

as much private spending as it would during an economic expansion.8

7

In addition to fiscal policy, the government can influence the business cycle through the use of monetary policy, which is . Federal monetary policy is largely implemented by the Federal Reserve. The Federal Reserve is, an independent government agency charged with maintaining stable prices and maximum

employment through its monetary policy. The Federal Reserve can influence interest rates throughout the economy by adjusting the federal funds rate, a very short-term interest rate faced 3 Chad Stone, “Fiscal Stimulus Needed to Fight Recessions,” Center on Budget and Policy Priorities, April 16, 2020, https://www.cbpp.org/research/economy/fiscal-stimulus-needed-to-fight-recessions.

4 Laurence Ball and Gregory Mankiw, “ What Do Budget Deficits Do?,” National Bureau of Economic Research (NBER), Working Paper no. 5263, September 1995. 5 Ball and Mankiw, “ What Do Budget Deficits Do?” 6 Benjamin M. Friedman, Crowding Out or Crowding In? Economic Consequences of Financing Government Deficits, Brookings Institution, https://www.brookings.edu/wp-content/uploads/2016/11/1978c_bpea_friedman.pdf.

7 Alan J. Auerbach and Yuriy Gorodnichenko, “Measuring the Output Responses to Fiscal Policy,” American Econom ic Journal: Economic Policy, vol. 4, no. 2 (May 2012).

Congressional Research Service

2

Fiscal Policy: Economic Effects

by banks. Decreasing interest rates reduces the cost to businesses and individuals of borrowing funds to make new investments and purchases. Conversely, increasing interest rates raises the cost to businesses and individuals of borrowing funds to make new investments and purchases. The Federal Reserve can conduct monetary policy in a complementary nature to fiscal policy, offsetting the rise in interest rates by decreasing the federal funds rate. Alternatively, the Federal Reserve can pursue a policy that offsets stimulus, pushing interest rates up by increasing the

federal funds rate.9

8

Exchange Rates and the Trade Balance

As discussed above, fiscal stimulus can cause interest rates to rise. As domestic rates rise relative to foreign rates, investors tend to seek out U.S. investments because the relatively highExchange Rates and the Trade Balance

Another potential consequence of government fiscal stimulus is an increase in the value of the U.S. dollar and a subsequent increase in the trade deficit, which mitigates some portion of the rise in economic activity resulting from the fiscal stimulus. As discussed above, fiscal stimulus can cause interest rates mean relatively high returns on investment. However, as foreign capital flows into the

United States, this can push rates back down as the supply of loanable funds increases, potential y

offsetting the initial rise in rates caused by the stimulus.

Nonetheless, increased demand for U.S. investment from foreign investors also means that the demand for the dollar would increase as foreign investors exchanged various foreign currencies for dollars that they could then invest. This increased demand for dollars increases the value of the dollar, referred to as appreciation. When the dollar appreciates it becomes more expensive relative to other currencies—it takes more foreign currency to “purchase” one dollar—and, therefore, U.S. goods and services become more expensive relative to foreign goods and services,

causing exports to decrease and imports to increase. The end result is general yrates to rise. In a global context where interest rates are rising in the United States relative to the rest of the world, demand for investment inside the United States is likely to increase among investors around the world as they seek out higher rates of return.10 The greater demand for investment in the United States is likely to temper the increase in interest rates resulting from fiscal stimulus. However, foreign investors must first exchange their own currency for U.S. dollars to invest in the United States. The increased demand for U.S. dollars increases the value of a U.S. dollar relative to other foreign currencies. As the U.S. dollar appreciates in value, domestic demand for imported goods increases because a U.S. dollar can now buy more goods and services abroad, but foreign demand for U.S. goods and services decreases because they are now relatively more expensive for foreigners. The end result is generally an increase in the U.S. trade deficit, as exports decrease and imports from abroad increase in the United States.119 An increasing trade deficit, all al else equal, means that consumption and production of domestic goods and services are fallingfal ing, partly offsetting the increase in aggregate demand caused by the stimulus.

stimulus.

As discussed above, however, during a recession interest rates are less likely to rise, or are likely to increase to a lesser degree, due to an already depressed demand for investment and spending within the economy.1210 Without rising interest rates, or if they increase to a lesser degree, the

associated increase in the trade deficit is also likely to be smallersmal er. In addition, if the Federal Reserve engages in similarly stimulative monetary policy, it may be able to mitigate some of the

anticipated increase in the trade deficit by further preventing an increase in interest rates.13

11

Inflation

TheInflation

As discussed above, the goal of fiscal stimulus is to increase aggregate demand within the economy. However, if fiscal stimulus is applied too aggressively, or is implemented when the economy is already operating near full capacity, it can result in an unsustainably large demand for goods and services that the economy is unable to supply. When the demand for goods and services is greater than the available available supply, prices tend to rise, a scenario known as inflation. A rising inflation rate can introduce distortions into the economy and impose unnecessary costs on individuals and

businesses, although economists generallygeneral y view low and stable inflation as a sign of a well-managed economy.14wel - 8 For further information regarding monetary policy, see CRS Report RL30354, Monetary Policy and the Federal Reserve: Current Policy and Conditions, by Marc Labonte. 9 Olivier Blanchard, Macroeconomics, 5th ed. (Upper Saddle River NJ: Pearson Education, 2009), pp. 450 -451. 10 Auerbach and Gorodnichenko, “Measuring the Output Responses to Fiscal Policy.” 11 For further information regarding monetary policy, see CRS Report RL30354, Monetary Policy and the Federal Reserve: Current Policy and Conditions, by Marc Labonte.

Congressional Research Service

3

Fiscal Policy: Economic Effects

managed economy.12 As such, rising inflation rates can hinder the effectiveness of fiscal stimulus on economic activity by imposing additional costs on individuals and interfering with the efficient allocation

efficient al ocation of resources in the economy.

The Federal Reserve has some ability to limit inflation by implementing contractionary monetary policy. If the Federal Reserve observes accelerating inflation as a result of additional fiscal stimulus, it can counteract this by increasing interest rates. The rise in interest rates results in a slowing of economic activity, neutralizing the fiscal stimulus, and may help to slow inflation as well.

wel .

Inflation has general y remained low despite relatively high deficit spending during the 11-year expansion between the Great Recession and the current COVID-19-induced recession. This indicates that in the near term, the size of this potential offsetting benefit could be relatively smal

and even prove counter to the Federal Reserve’s monetary policy strategy of targeting an average

of 2% inflation over time.13

Fiscal Expansion Multipliers Fiscal Expansion Multipliers

Economists attempt to evaluate the overall overal impact of fiscal stimulus on the economy by estimating fiscal multipliers, which measure the ratio of a change in economic output to the change in government spending or revenue that causes the change in output.1514 A fiscal multiplier greater than one suggests that for each dollar the government spends or each dollar taxes are cut

or transfers are increased, the economy grows by more than one dollar. A multiplier may be larger than one if the initial government stimulus results in further spending by private actors. For example, if the government increases spending on infrastructure projects as part of its stimulus, directly increasing aggregate demand, numerous contractors and construction workers will wil likely receive additional income as a consequence. If those workers then spend a portion of their new

income within the economy, it further increases aggregate demand. Alternatively, a fiscal multiplier multiplier of less than one suggests that for each dollar the government spends, the economy grows by less than one dollar, suggesting the expansionary power of the fiscal stimulus is being

partly offset by the contractionary pressures discussed above.

Estimates of fiscal multipliers vary depending on the form of the fiscal stimulus and on which economic model the economist uses to measure the multiplier.15 For example, a 2012 academic research article estimated fiscal multipliers for various forms of stimulus utilizingusing several different prominent economic models from the Federal Reserve Board, the European Central Bank, the

International Monetary Fund (IMF), the European Commission, the OrganisationOrganization for Economic Co-operation and Development (OECD), the Bank of Canada, and two models developed by academic economists. The authors found varying estimates (see, the Bank of Canada, and two models developed by academic

12 See, for example, Richard G. Anderson, “ Inflation’s Economic Cost: How Large? How Certain?,” Federal Reserve Bank of St. Louis, July 2006, https://www.stlouisfed.org/publications/regional-economist/july-2006/inflations-economic-cost -how-large-how-certain.

13 In August 2020, the Federal Reserve announced a change to its monetary policy strategy statement and that instead of targeting an inflation rate of 2%, it would target an average rate of 2%. For more information, see Board of Governors of the Federal Reserve System, “ Guide to Changes in the Statement on Longer-Run Goals and Monetary Policy Strategy,” https://www.federalreserve.gov/monetarypolicy/guide-to-changes-in-statement-on-longer-run-goals-monetary-policy-strategy.htm; and CRS Insight IN11499, The Federal Reserve’s Revised Monetary Policy Strategy Statem ent, by Marc Labonte.

14 Nicoletta Batini et al., Fiscal Multipliers: Size, Determinants, and Use in Macroeconomic Projections, International Monetary Fund, September 2014, https://www.imf.org/external/pubs/ft/tnm/2014/tnm1404.pdf.

15 For more information on different types of models used to estimate fiscal multipliers, see CRS Report R46460, Fiscal Policy and Recovery from the COVID-19 Recession, by Jane G. Gravelle and Donald J. Marples.

Congressional Research Service

4

link to page 8 Fiscal Policy: Economic Effects

economists. The authors found varying estimates (see Table 1) for different forms of fiscal stimulus ranging from 1.59 for cash transfers to low-income individuals to 0.23 for reduced labor income taxes.1616 Based on these estimates, increasing government spending on consumption by 1% of GDP would result in a 1.55% increase in GDP, and decreasing labor income taxes by 1%

of GDP would result in a 0.23% increase in GDP.

Table 1. Average First-Year Fiscal Multipliers for Stimulus in Selected Models

Fiscal Stimulus

Multiplier

Government Investment

1.59

Government Consumption

1.55

Targeted Transfers

1.30

Consumption Taxes

0.61

General Transfers

0.42

Corporate Income Taxes

0.24

Labor Income Taxes

0.23

Source: Gunter Coenen et al., “Effects of Fiscal Stimulus in Structural Models,” American Economic Journal: Macroeconomics, Table 1. Average First-Year Fiscal Multipliers for Stimulus in Selected Models

|

Fiscal Stimulus |

Multiplier |

|

Government Investment |

1.59 |

|

Government Consumption |

1.55 |

|

Targeted Transfers |

1.30 |

|

Consumption Taxes |

0.61 |

|

General Transfers |

0.42 |

|

Corporate Income Taxes |

0.24 |

|

Labor Income Taxes |

0.23 |

Source: Gunter Coenen, Christopher J. Erceg, Charles Freedman et al., "Effects of Fiscal Stimulus in Structural Models," American Economic Journal, Macroeconomics, vol. 4, no. 1 (January 2012), p. 46.

vol. 4, no. 1 (January 2012), p. 46. Note: Multipliers are averages across the seven models of the first-year effects on real GDP of fiscal stimulus lasting for two years, assuming no change in monetary policy for two years.

The magnitude of fiscal multipliers likely depends on where the economy is in the business cycle. As discussed above, during a recession fiscal stimulus is less likely to result in offsetting contractionary effects—such as rising interest rates, trade deficits, and inflation—resulting in a larger increase in economic activity from fiscal stimulus. Accordingly, another academic research article attempted to estimate fiscal multipliers depending on whether the economy was in an expansion or a recession, and found that the multiplier for government spending was between 0 and 0.5 during expansions and between 1.0 and 1.5 during recessions.17

Long-Term Considerations Regarding Therefore, multipliers are expected to be smal er during expansions when stimulus is more likely to result in the crowding out of private

consumption, investment, and net exports. Accordingly, many models estimate much larger

multipliers during recessions than expansions.17

Considerations Regarding Persistent Fiscal Stimulus Fiscal Stimulus

Persistently applying fiscal stimulus can negatively affect the economy in the long term through three main avenues. First, persistent, large budget deficits can result in a rising debt-to-GDP ratio and lead to an unsustainable level of debt.1818 Second, persistent fiscal stimulus—particularly during economic expansions—can limit long-term economic growth by crowding out private

investment. Third, rising public debt will wil require a growing portion of the federal budget to be directed toward interest payments on the debt, potentiallypotential y crowding out other, more worthwhile

sources of government spending.

Some economic research has suggested that relatively high public debt negatively impacts economic growth. For example, one academic research paper suggested that for developed

16 Gunter Coenen et al., “Effects of Fiscal Stimulus in Structural Models,” American Economic Journal: Macroeconom ics, vol. 4, no. 1 (January 2012), pp. 22-68.

17 Auerbach and Gorodnichenko, “Measuring the Output Responses to Fiscal Policy.” 18 Assuming annual budget deficits exceed the annual increase in GDP, the debt -to-GDP ratio will rise over time.

Congressional Research Service

5

Fiscal Policy: Economic Effects

countries, a 10 percentage countries, a 10-percentage-point increase in the debt-to-GDP ratio is associated with a 0.15- to 0.20-percentage-

percentage point decrease in per capita real GDP growth.19

19 Unsustainable Public Debt

As noted, persistent fiscal stimulus can result in a rising debt-to-GDP ratio and lead to an unsustainable level of public debt.2020 A rising debt-to-GDP ratio can be problematic if the

perceived or real risk of the government defaulting on that debt begins to rise. As the perceived risk of default begins to increase, investors will wil demand higher interest rates to compensate themselves.

themselves.

The tipping point at which public debt becomes unsustainable is difficult to predict. A continually continual y rising debt-to-GDP ratio is likely to lead to an unsustainable level of debt over time. The threshold at which a nation'’s debt becomes unsustainable depends on a number of factors, such as the denomination of the debt, political circumstances, and, potentiallypotential y most importantly, underlying economic conditions. A change in these circumstances may shift a nation'’s debt to be

unsustainable without the underlying amount of debt changing at allal . To date, it does not appear that the United States has an immediate concern with respect to unsustainability; however, the U.S. debt-to-GDP ratio is projected to continually rise under current policy.21

given that interest rates are historical y low,21 although the unpredictability of interest rates has led to some cal s for caution.22 The debt-to-GDP ratio in FY2020 was the highest since World War II and is

projected to remain high, at least in the short-term, given the ongoing pandemic and recession.23

Decreased Business Investment

Decreased Business Investment

Persistent fiscal stimulus, and the associated budget deficits, can decrease the size of the economy in the long term as a result of decreased investment in physical capital.2224 As discussed previously, the government'’s deficit spending can result in higher interest rates, which generallygeneral y lead to lower levels of business investment. Business investment—spending on physical capital such as factories, computers, software, and machines—is an important determinant of the long-term size

of the economy. Physical capital investment allowsal ows businesses to produce more goods and services with the same amount of labor and raw materials. As such, government deficits that lead to lower levels of business investment can result in lower quantities of physical capital, and

therefore may reduce the productive capacity of the economy in the long term.23

25

As discussed earlier, some of the increase in interest rates and decline in domestic investment resulting from fiscal stimulus will likelycould be offset by additional investment incapital flowing into the United States 19 Manmohan S. Kumar and Jaejoon Woo, Public Debt and Growth, International Monetary Fund, Working Paper, vol. 10, no. 174 (July 2010).

20 Public debt is the money that the government owes to its creditors, which include private citizens, institutions, foreign governments, and other parts of the federal government. For more information on the public debt, see CRS Report R44383, Deficits, Debt, and the Econom y: An Introduction , by Grant A. Driessen. 21 Olivier Blanchard, Reexamining the Economic Costs of Debt, Peterson Institute for International Economics, November 20, 2019, https://www.piie.com/commentary/testimonies/reexamining-economic-costs-debt.

22 John Cochrane, “Debt Denial,” The Grumpy Economist, December 9, 2020, https://johnhcochrane.blogspot.com/2020/12/debt-denial.html. 23 U.S. Congressional Budget Office (CBO), Monthly Budget Review: Summary for Fiscal Year 2020, November 9, 2020, p. 1.

24 Depending on the size of the capital stock and the debt -to-GDP level, particularly when both are initially relatively low, deficit -financed government investment, such as infrastructure projects, may lead to a higher capital stock overall and therefore increase the productive capacity of the economy.

25 Ball and Mankiw, “ What Do Budget Deficits Do?”

Congressional Research Service

6

Fiscal Policy: Economic Effects

the United States from abroad. The inflow of capital from abroad is beneficial, as it allowscan be beneficial if it al ows for additional investment in the United StatesU.S. economy. However, in exchange for these investmentcapital flows, the United States is nowwould be sending a portion of its national income to foreigners in the form of interest payments. With a larger portion of investment flows coming from abroad, rather than from within the United Statesthe capital stock owned by foreigners, rather than Americans, a larger

, a larger portion of the U.S. national income willwould be sent abroad.

Crowding Out Government Spending

Rising public debt may also be of concern due to its associated interest payments. All Al else equal, an increase in the level of public debt will wil result in an increase in interest payments that the government must make each year. Rising interest payments may displace government spending on more worthwhile programs. In 2019, interest payments on the debt are projected to be about 1.8% of GDP, or about $382 billion. By 2029 interest payments on the debt are expected to increase significantly, rising to about 3.0% of GDP or about $921 billion.24

were $375 bil ion. Despite a roughly 25% increase in the amount of debt held by the public in FY2020,26 interest payments

are down 8.5% from 2019, at $337 bil ion, due in large part to lower interest rates.27

Withdrawing Fiscal Stimulus Withdrawing Fiscal Stimulus

As the economy shifts from a recession and into an expansion, broader economic conditions will generallywil general y improve, whereby unemployment fallsfal s and wages and private spending increaseincreases. With improving economic conditions, policymakers may choose to begin withdrawing fiscal stimulus

by decreasing the size of the deficit or potentially potential y by applying contractionary fiscal policy and running a budget surplus. As discussed in the previous section, policymakers may choose to withdraw fiscal stimulus for a number of reasons. First, persistent fiscal stimulus when the economy is near full capacity can exacerbate the negative consequences of fiscal stimulus, such as decreasing investment, rising trade deficits, and accelerating inflation. Second, decreasing the

size of the budget deficit slows the accumulationgrowth of public debt.

The government can withdraw fiscal stimulus by increasing taxes, decreasing spending, or a combination of the two. When the government raises individual income taxes, for example, individuals

individuals have less disposable income and decrease their spending on goods and services in response. The decrease in spending reduces aggregate demand for goods and services, slowing economic growth temporarily. Alternatively, when the government reduces spending, it reduces aggregate demand in the economy, which again temporarily slows economic growth. As such, when the government reduces the deficit, regardless of the mix of fiscal policy choices used to do

so, aggregate demand is expected to decrease in the near term. However, withdrawing fiscal stimulus is expected to result in lower interest rates and more investment;, a depreciation of the U.S. dollar and a shrinking trade deficit;, and a slowing inflation rate. 2528 These effects tend to spur additional economic activity, partly offsetting the decline resulting from withdrawing fiscal stimulus. Whether the decrease in aggregate demand is problematic for overall economic overal economic

performance depends on the overal state of the overall economy at that time.

26 U.S. Department of the T reasury, Debt Position and Activity Report for September 2019 and September 2020, https://www.treasurydirect.gov/govt/reports/pd/pd_debtposactrpt.htm.

27 CBO, Monthly Budget Review: Summary for Fiscal Year 2020, November 9, 2020, p. 5. 28 Blanchard, Macroeconomics, pp. 450-451.

Congressional Research Service

7

link to page 7 link to page 7 link to page 8 Fiscal Policy: Economic Effects

Potential Offsetting Effects to Withdrawing Fiscal Stimulus

Potential Offsetting Effects to Withdrawing Fiscal Stimulus

Investment and Interest Rates

Withdrawing fiscal stimulus is likely to put downward pressure on domestic interest rates, which encourages additional spending and investment, increasing economic activity. When the

government decreases its budget deficit, the demand for loanable funds decreases because the government reduces the amount of those funds it is borrowing. The decrease in demand for loanable funds decreases the price to borrow those funds (i.e., interest rates decline). Declining interest rates encourage increased business investment into new capital projects and consumer

spending into durable goods by reducing the cost of borrowing.26

29 Exchange Rates and the Trade Balance

Withdrawing fiscal stimulus iswould also be expected to result in a depreciation of the U.S. dollar and an improved trade balance with the rest of the world. Assuming the shrinking deficit causes a decline in U.S. interest rates relative to interest rates abroad, individuals in the United States and abroad would rather make financial investments outside of the United States to benefit from those higher interest rates. Individuals shifting their investments outside the United States must first

exchange their U.S. dollars for foreign currency, which decreases the value of the U.S. dollar relative to foreign currencies. As the U.S. dollar depreciates, foreign goods and services become relatively more expensive for U.S. residents, and U.S. goods and services become relatively less expensive for foreign individuals.27 This generally30 This general y results in an improved trade balance as foreign demand for U.S. goods and services (exports) increases and domestic demand for foreign goods

and services (imports) decreases.

Inflation

An increase in net exports additional y directly increases the size of the U.S. economy, at least partial y negating the decrease in aggregate demand caused by

the withdrawal of stimulus.

Inflation

When fiscal stimulus is withdrawn, aggregate demand for goods and services in the economy also

tends to shrink, which is expected to slow inflation. Economists generallygeneral y view relatively low and stable inflation as beneficial for economic growth, because businesses and consumers are relatively certain about the future price of goods and can make efficient decisions with respect to

investment and consumption over time.28

31 Fiscal Contraction Multipliers

The ultimate impact on the economy of withdrawing fiscal stimulus depends on the relative magnitude of its effects on aggregate demand, interest rates and investment, exchange rates and

the trade deficit, and inflation. The same fiscal multipliers discussed earlier in the "“Fiscal Expansion Multiplier" ” section can be used to estimate the impact of withdrawing fiscal stimulus by simply reversing the sign for each multiplier. As shown inin Table 1, decreasing government spending on consumption by 1% of GDP is expected to reduce real GDP by 1.55% after the first

29 Ball and Mankiw, “ What Do Budget Deficits Do?” 30 Ball and Mankiw, “ What Do Budget Deficits Do?” 31 See, for example, Anderson, “ Inflation’s Economic Cost: How Large? How Certain?”

Congressional Research Service

8

link to page 13 Fiscal Policy: Economic Effects

yearyear, compared to no change in fiscal policy. Alternatively, increasing labor income taxes by 1%

of GDP is expected to reduce real GDP by 0.23% after the first year.29

32

Again, monetary policy can be used alongside fiscal policy to affect the overall overal impact on the

economy. For example, the Federal Reserve could lower interest rates to spur aggregate demand as the federal government withdraws fiscal stimulus in an effort to offset the decline in aggregate demand resulting from the shrinking deficit. This could allowal ow the government to withdraw fiscal

stimulus without decreasing aggregate demand or economic activity.

Fiscal Policy Stance

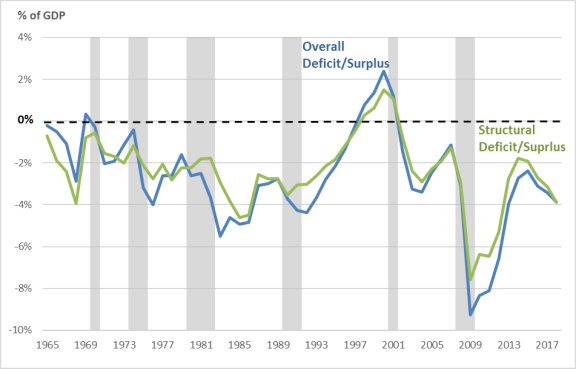

As shown inin Figure 1, the federal government has generallygeneral y been running a budget deficit for

much of the past 3060 years—save for two short periods in the 1960s and 1990s. This suggests that the federal government has been applying some level of fiscal stimulus to the economy for much of the past three decadesover half a century, although the level of stimulus has increased and decreased over time. However, simply examining the overall overal budget deficit to judge the level of fiscal stimulus can be misleading, as the levels of federal spending and revenue differ over time automaticallyautomatical y due to

changes in the state of the economy, rather than deliberate choices made each year by Congress. During economic expansions, tax revenue tends to increase and spending tends to decrease automaticallyautomatical y, as rising incomes and employment result in higher average incomes and therefore greater individual and corporate income tax revenues. Federal spending on income support programs, such as food stamps and unemployment insurance, tends to fall fal as fewer people need

financial assistance and unemployment claims fall fal during economic expansions. The combination of rising tax revenue and fallingfal ing federal spending tends to improve the government'’s budget deficit. The opposite is true during recessions, when federal spending rises and revenue shrinks. These cyclical fluctuations in revenue and spending are often referred to as automatic stabilizers.30stabilizers.33 Therefore, when examining fiscal policy, it is often beneficial to estimate the budget deficit excluding these automatic stabilizers, referred to as the structural deficit, to get a sense of

the affirmative fiscal policy decisions made each year by Congress.

|

|

Note: Grey bars denote recessions as determined by the National Bureau of Economic Research. |

As shown in

32 Coenen et al., “Effects of Fiscal Stimulus in Structural Models,” p. 46. 33 CBO, How CBO Estimates Automatic Stabilizers, November 2015.

Congressional Research Service

9

link to page 13

Fiscal Policy: Economic Effects

Figure 1. Federal Budget Deficit/Surplus

Source: U.S. Congressional Budget Office, https://www.cbo.gov/publication/56095. Note: Grey bars denote recessions as determined by the National Bureau of Economic Research. The FY2020 overal deficit as a percent of potential GDP was calculated by dividing the actual FY2020 deficit by CBO’s July 2020 estimate for potential GDP, which can be found at https://www.cbo.gov/system/files/2020-07/51135-2020-07-economicprojections.xlsx.

As shown in Figure 1, budget deficits tend to increase during and shortly after recessions (denoted by grey bars) as policymakers attempt to buoy the economy by applying fiscal stimulus. This can be seen explicitly by viewing the structural deficit/surplus, as this only shows affirmative changes in fiscal policy made by Congress. The budget deficit then tends to shrink as the economy enters into recovery and fiscal stimulus is less necessary to support economic growth. However, in recent years, the federal budget has bucked this trend. After the structural deficit peaked in 2009 at roughly 7.5% of GDP, it began to

decline through 2014, fallingfal ing to about 2.0% of GDP. Beginning in 2016, in spite ofdespite relatively strong

economic conditions, the structural deficit has started to rise again, nearing 45.0% of GDP in 2019.

COVID-19 has caused a deep recession in the U.S. economy,34 and several relief bil s were

enacted in response, including the Coronavirus Preparedness and Response Supplemental Appropriations Act, 2020 (P.L. 116-123); the Families First Coronavirus Response Act (P.L. 116-127); the Coronavirus Aid, Relief, and Economic Security (CARES) Act (P.L. 116-136); and the Paycheck Protection Program and Health Care Enhancement Act (P.L. 116-139). Most recently, additional coronavirus relief was included in the Consolidated Appropriations Act, 2021 (P.L.

116-260). Relief included direct cash transfers to consumers, forgivable loans to smal businesses, and increased unemployment benefits, among others. The deficit totaled $3.1 tril ion in FY2020, equal to 14.9% of nominal GDP—the highest share of GDP since the end of World War II.35 The

relief measures enacted in FY2020—which does not include P.L. 116-260—is projected to

34 For more information on the economic effects of the COVID-19 pandemic, see CRS Report R46606, COVID-19 and the U.S. Econom y, by Lida R. Weinstock. 35 CBO, Monthly Budget Review: Summary for Fiscal Year 2020, November 9, 2020, p. 1.

Congressional Research Service

10

Fiscal Policy: Economic Effects

increase FY2020-FY2030 deficits by $2.6 tril ion, so its effect on the deficit is relatively short-

lived.36

Author Information

Lida R. Weinstock

Analyst in Macroeconomic Policy

Acknowledgments

This report was originally authored by Jeffrey Stupak, former CRS Analyst in Macroeconomic Policy.

Disclaimer

This document was prepared by the Congressional Research Service (CRS). CRS serves as nonpartisan shared staff to congressional committees and Members of Congress. It operates solely at the behest of and under the direction of Congress. Information in a CRS Report should n ot be relied upon for purposes other than public understanding of information that has been provided by CRS to Members of Congress in connection with CRS’s institutional role. CRS Reports, as a work of the United States Government, are not subject to copyright protection in the United States. Any CRS Report may be reproduced and distributed in its entirety without permission from CRS. However, as a CRS Report may include copyrighted images or material from a third party, you may need to obtain the permission of the copyright holder if you wish to copy or otherwise use copyrighted material.

36 CBO, An Update to the Budget Outlook: 2020 to 2030, September 2020, p. 33.

Congressional Research Service

R45723 · VERSION 10 · UPDATED

11 .0% of GDP in 2018.

Given that the economy is arguably at or exceeding full employment currently, the increase in fiscal stimulus since 2016 is notable.31 As discussed earlier, expanding fiscal stimulus when the economy is not depressed can result in rising interest rates, a growing trade deficit, and higher inflation. As of publication of this report, interest rates and inflation do not appear to have been affected by the additional fiscal stimulus; interest rates are at historic lows and inflation shows no signs of acceleration.32 The trade deficit has been growing in recent years; however, it is not clear that this growth in the trade deficit is a result of increased fiscal stimulus.33

Author Contact Information

Footnotes

| 1. |

Olivier Blanchard, Macroeconomics, 5th ed. (Upper Saddle River NJ: Pearson Education, 2009), pp. 450-451. |

| 2. |

The economy shifts from periods of increasing economic activity, known as economic expansions, to periods of decreasing economic activity, known as recessions. For more information, see CRS In Focus IF10411, Introduction to U.S. Economy: The Business Cycle and Growth, by Jeffrey M. Stupak. |

| 3. |

For more information on the causes of recessions, refer to CRS Insight IN10853, What Causes a Recession?, by Marc Labonte. |

| 4. |

Michael Greenstone and Adam Looney, The Role of Fiscal Stimulus in the Ongoing Recovery, Brookings Institution, July 6, 2012, https://www.brookings.edu/blog/jobs/2012/07/06/the-role-of-fiscal-stimulus-in-the-ongoing-recovery/. |

| 5. |

Laurence Ball and Gregory Mankiw, What Do Budget Deficits Do? National Bureau of Economic Research (NBER), Working Paper no. 5263, September 1995. |

| 6. |

Ibid. |

| 7. |

Benjamin M. Friedman, Crowding Out or Crowding In? Economic Consequences of Financing Government Deficits, Brookings Institution, Brookings Papers on Economic Activity, 3:1978, https://www.brookings.edu/wp-content/uploads/2016/11/1978c_bpea_friedman.pdf. |

| 8. |

Alan J. Auerbach and Yuriy Gorodnichenko, "Measuring the Output Responses to Fiscal Policy," American Economic Journal: Economic Policy, vol. 4, no. 2 (May 2012). |

| 9. |

For further information regarding monetary policy, refer to CRS Report RL30354, Monetary Policy and the Federal Reserve: Current Policy and Conditions, by Marc Labonte. |

| 10. |

Laurence Ball and Gregory Mankiw, What Do Budget Deficits Do? National Bureau of Economic Research (NBER), Working Paper no. 5263, September 1995. |

| 11. |

Olivier Blanchard, Macroeconomics, 5th ed. (Upper Saddle River NJ: Pearson Education, 2009), pp. 450-451. |

| 12. |

Alan J. Auerbach and Yuriy Gorodnichenko, "Measuring the Output Responses to Fiscal Policy," American Economic Journal: Economic Policy, vol. 4, no. 2 (May 2012). |

| 13. |

For further information regarding monetary policy, refer to CRS Report RL30354, Monetary Policy and the Federal Reserve: Current Policy and Conditions, by Marc Labonte. |

| 14. |

See, e.g., Richard G. Anderson, Inflation's Economic Cost: How Large? How Certain? Federal Reserve Bank of St. Louis, July 2006, at https://www.stlouisfed.org/publications/regional-economist/july-2006/inflations-economic-cost-how-large-how-certain. |

| 15. |

Nicoletta Batini, Luc Eyraud, Lorenzo Forni et al., Fiscal Multipliers: Size, Determinants, and Use in Macroeconomic Projections, International Monetary Fund, September 2014, https://www.imf.org/external/pubs/ft/tnm/2014/tnm1404.pdf. |

| 16. |

Gunter Coenen et al., "Effects of Fiscal Stimulus in Structural Models," American Economic Journal, Macroeconomics, vol. 4, no. 1 (January 2012), pp. 22-68. |

| 17. |

Alan J. Auerbach and Yuriy Gorodnichenko, "Measuring the Output Responses to Fiscal Policy," American Economic Journal: Economic Policy, vol. 4, no. 2 (May 2012). |

| 18. |

Assuming annual budget deficits exceed annual GDP growth, the debt-to-GDP ratio will rise over time. |

| 19. |

Manmohan S. Kumar and Jaejoon Woo, Public Debt and Growth, International Monetary Fund (IMF), Working Paper, vol. 10, no. 174 (July 2010). |

| 20. |

Public debt is the money that the government owes to its creditors, which include private citizens, institutions, foreign governments, and other parts of the federal government. For more information on the public debt, refer to CRS Report R44383, Deficits, Debt, and the Economy: An Introduction, by Grant A. Driessen. |

| 21. |

Moody's Analytics, Fiscal Space, An alternative, economic fundamentals-based measure of the risk of sovereign debt default, https://www.economy.com/dismal/tools/global-fiscal-space-tracker. |

| 22. |

Depending on the size of the capital stock and the debt-to-GDP level, particularly when both are initially relatively low, deficit-financed government investment, such as infrastructure projects, may lead to a higher capital stock overall and therefore increase the productive capacity of the economy. |

| 23. |

Laurence Ball and Gregory Mankiw, What Do Budget Deficits Do? National Bureau of Economic Research (NBER), Working Paper no. 5263, September 1995. |

| 24. |

U.S. Congressional Budget Office, Updated Budget Projections: 2019 to 2029, May 2019, p. 15. |

| 25. |

Olivier Blanchard, Macroeconomics, 5th ed. (Upper Saddle River NJ: Pearson Education, 2009), p. 450-451. |

| 26. |

Laurence Ball and Gregory Mankiw, What Do Budget Deficits Do? National Bureau of Economic Research (NBER), Working Paper no. 5263, September 1995. |

| 27. |

Laurence Ball and Gregory Mankiw, What Do Budget Deficits Do? National Bureau of Economic Research (NBER), Working Paper no. 5263, September 1995. |

| 28. |

See, e.g., Richard G. Anderson, Inflation's Economic Cost: How Large? How Certain? Federal Reserve Bank of St. Louis, July 2006, at https://www.stlouisfed.org/publications/regional-economist/july-2006/inflations-economic-cost-how-large-how-certain. |

| 29. |

Gunter Coenen et al., "Effects of Fiscal Stimulus in Structural Models," American Economic Association, vol. 4, no. 1 (January 2012), p. 46. |

| 30. |

U.S. Congressional Budget Office, How CBO Estimates Automatic Stabilizers, November 2015. |

| 31. |

Board of Governors of the Federal Reserve System, "Monetary Policy Outlook for 2019," speech, January 10, 2019, https://www.federalreserve.gov/newsevents/speech/clarida20190110a.htm. |

| 32. |

CRS Insight IN11044, Low Interest Rates, Part 1: Economic and Fiscal Implications, by Marc Labonte; and Federal Reserve Bank of St. Louis, Personal Consumption Expenditures Excluding Food and Energy, at https://fred.stlouisfed.org/series/PCEPILFE. |

| 33. |

Bureau of Economic Analysis, International Transactions, at https://www.bea.gov/data/intl-trade-investment/international-transactions. |