What Causes a Recession?

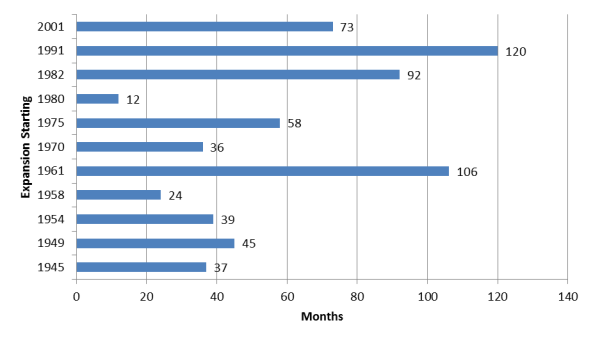

At 120 months in June, the current economic expansion is now tied with the longest in U.S. history. As can be seen in Figure 1, previous expansions vary greatly in length but have recently been longer. Dating back to the 1850s, only five have lasted over five years, including the last three.

This expansion, like all previous ones, will eventually end and be followed by a recession. Few economists are forecasting a recession in 2019, but recessions are notoriously hard to predict even a few months beforehand. For background, see CRS In Focus IF10411, Introduction to U.S. Economy: The Business Cycle and Growth, by Jeffrey M. Stupak.

|

Figure 1. Length of Previous Expansions Since World War II |

|

|

Source: The National Bureau of Economic Research (NBER). |

What will bring this economic expansion to an end? In the words of Janet Yellen, "it's a myth that expansions die of old age." Instead, the historical record points to a few culprits that have killed off expansions—an overheating economy that results in accelerating price inflation, a financial bubble, or an external "shock" to the economy, such as an oil price spike. The longer an expansion lasts, the more likely it will fall victim to one of these killers.

Overheating

Recessions can be caused by an overheated economy, in which demand outstrips supply, expanding past full employment and the maximum capacity of the nation's resources. Overheating can be sustained temporarily, but eventually spending will fall in order for supply to catch up to demand.

A classic overheating economy has two key characteristics—rising inflation and unemployment below its "natural" rate.

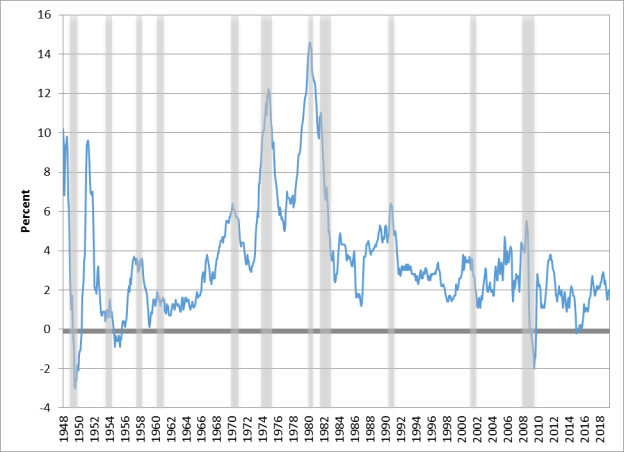

As shown in Figure 2, each recession since World War II has featured a run-up in inflation before the recession began, except for the 1953-1954 recession. Some of these increases were larger than others, however. The last three recessions were preceded by increases in the inflation rate of under 3 percentage points, while five of the eight before then featured an increase in inflation of at least 3 percentage points. (The largest increase was the 8 percentage point increase before the 1980 recession.)

|

(Consumer Price Index) |

|

|

Source: Bureau of Labor Statistics (BLS). Note: Recessions are shaded. |

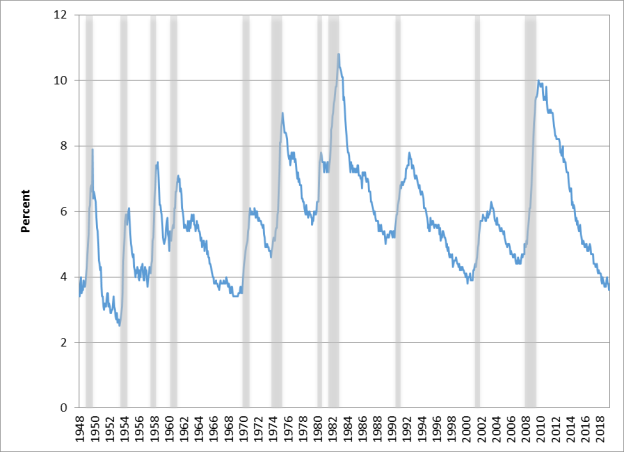

As shown in Figure 3, unemployment fell to 5% or lower before all but two recessions since World War II, and fell below 4% in four of five recessions before the 1970s, but only one since (before the 2001 recession). No specific threshold unemployment rate has consistently triggered a recession, in part because the natural rate of unemployment has not been constant over time; for example, CBO estimates that it has varied from 4.6% to 6.3% since 1949. In each recession since World War II except for 1981-1982, unemployment was lower than CBO's estimate of the natural rate before the recession began.

|

|

Note: Recessions are shaded. |

The recessions beginning in 1957, 1969, and 1973 fit the classic overheating story well. The rest featured too high of an unemployment rate or too small of a run-up in inflation before the recession. For example, unemployment was above 7% when the 1981-1982 recession started.

Does today's economy show signs of classic overheating? This expansion has been unprecedentedly long in part because the "Great Recession" that preceded it left the economy in a depressed state for several years, reducing the risk of overheating. Now, the unemployment rate is very low—below CBO's estimate of the natural rate—but so is inflation. The unemployment rate has not been as low as the current rate (3.6%) since 1969. In that expansion, unemployment stayed below 4% for about four years, during which time inflation steadily accelerated, before the economy entered a recession. Thus, low unemployment does not necessarily trigger a recession immediately.

Asset Bubbles

The last two recessions were arguably caused by overheating of a different type. While neither featured a large increase in price inflation, both featured the rapid growth and subsequent bursting of asset bubbles. The 2001 recession was preceded by the "dot-com" stock bubble, and the 2007-2009 recession was preceded by the housing bubble.

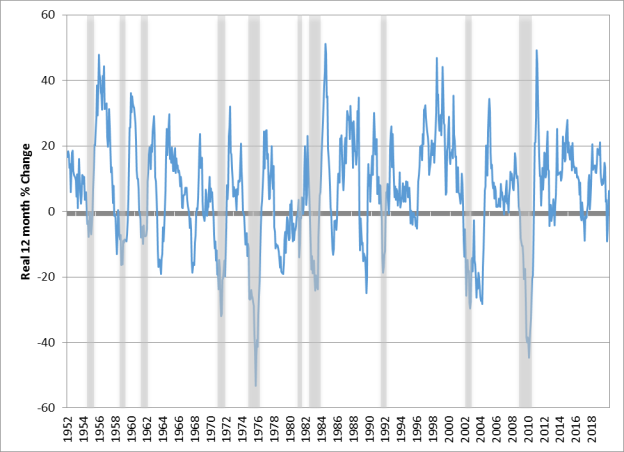

Stock market volatility since 2018 and stock market valuation metrics that are still high by historical standards have led to questions about whether there is currently a bubble. Unfortunately, it is difficult to accurately identify bubbles and to predict when they will cause problems for the broader economy. Because stock prices are volatile, large increases and declines over, say, 12-month periods are not uncommon, and the latter do not always coincide with recessions, as shown in Figure 4.

|

|

Source: Congressional Research Service based on NBER, BLS, Yahoo! Finance data. Note: Recessions are shaded. |

All recessions feature stock market downturns, but not all downturns are caused by bubbles; instead, deteriorating economic conditions reduce corporations' future profitability, which lowers stock prices. Bubbles cause broader macroeconomic damage when they result in a substantial reallocation of physical capital and sectoral employment that must then be reversed when the bubble bursts—the liquidation of failed dot-com firms or the decline in new housing starts and construction employment during the foreclosure crisis, for example.

Economic Shocks

Recessions are not always caused by overheating. They can also be triggered by negative, unexpected, external events, which economists refer to as "shocks" to the economy that disrupt the expansion. Shocks can potentially happen at any point in the expansion, but a longer expansion provides more opportunities for shocks.

A classic example of a shock is the oil shocks of the 1970s and 1980s. They help explain why those recessions featured high inflation despite unemployment being relatively high. Shocks could also stem from the spillover effects of an economic crisis abroad, although these are typically not large enough relative to the U.S. economy to cause a recession.

The U.S. economy has benefited from the absence of large external shocks in the past couple of years, which has been supportive of growth and low inflation. Unlike overheating, there is little advanced warning as to when a shock may occur.