Effects of Buy America on Transportation Infrastructure and U.S. Manufacturing

In 1978, Congress began placing domestic content restrictions on federally funded transportation projects that are carried out by nonfederal government agencies such as state and local governments. These restrictions, which have changed over the years, are commonly referred to as the Buy America Act, or more simply, Buy America. Although there has been ongoing congressional interest in domestic preference policy over the years, statements and actions by the Trump Administration about reinvigorating domestic manufacturing and investing in infrastructure have stimulated renewed interest in Buy America.

Buy America refers to several similar statutes and regulations that apply when federal funds are used to support projects involving highways, public transportation, aviation, and intercity passenger rail, including Amtrak. Unless a nationwide or project-specific waiver is granted, Buy America requires the use of U.S.-made iron and steel and the domestic production and assembly of other manufactured goods, particularly the production of rolling stock (railcars and buses) used in federally funded public transportation and Amtrak’s intercity passenger rail service. A separate law requires that at least half the value of products imported by sea for federally supported transportation projects be transported in U.S.-flag ships. This report examines the effects of Buy America on iron and steel manufacturing, rolling stock manufacturing, and transportation.

Although the Buy America provisions have been in place in some form for more than 40 years in transportation, it is difficult to know how they have affected steel and rolling stock manufacturing in the United States, whether measured by jobs, output, or any other indicator. Empirical evidence on the economic benefits or costs of domestic content laws is scarce, partly because the effects are small compared with macroeconomic forces such as global economic growth and the related growth in demand for steel. Buy America may have protected some domestic iron and steel manufacturing, and a relatively small number of jobs. Jobs in the domestic steel industry have declined sharply since 1990, largely attributable to factors such as higher industry productivity.

Buy America has likely bolstered the production of railcars and buses in the United States. These industries are comparatively small and employ relatively few workers. Railcar manufacturing, including freight rail, accounted for 0.2% of total factory employment in 2018. Demand for passenger railcars and buses is related strongly to the combined level of federal, state, and local government funding.

Transit rolling stock manufacturing in the United States by firms based in China appears to be Buy America compliant. Still, concerns have been raised by some Members of Congress about the economic and national security implications of this manufacturing production. Pending legislation seeks to prohibit transit agencies from buying buses and transit railcars from Chinese government-owned, -controlled or -subsidized companies.

For state and local providers of transportation infrastructure and services, Buy America could increase the cost of at least some projects, such as building highway bridges and procuring transit railcars and buses, and may result in fewer projects being undertaken. The price of steel produced in the United States tends to be higher than that of comparable steel produced in other countries. Buy America may also raise the cost of rolling stock procurements. The U.S. market is relatively small compared with those in other countries and regions, consequently domestic producers do not benefit from economies of scale. In addition, Buy America requirements have been blamed for project delays, which can arise from domestic supply problems, the difficulty of compliance, and the waiver application process.

Much of the congressional activity related to Buy America seeks to strengthen its requirements. The Fixing America’s Surface Transportation (FAST) Act (P.L. 114-94), enacted in December 2015, increased the share of public transit rolling stock components and subcomponents that must be produced in the United States to 65% in FY2019, and to 70% for FY2020 onward. Other bills have proposed increasing the share to 100%. Legislative proposals have also called for expanding Buy America to other parts of the transportation system, such as pipelines and school buses, and to other sectors, such as federally funded school projects.

Effects of Buy America on Transportation Infrastructure and U.S. Manufacturing

Jump to Main Text of Report

Contents

- Introduction

- Buy America Requirements

- Trade Agreements and Domestic Preferences

- Cargo Preference

- Changes to Buy America in MAP-21 and FAST Act

- Presidential Statements and Actions

- Effects of Buy America on U.S. Steel Manufacturing

- Effects of Buy America on U.S. Rolling Stock Manufacturing

- Passenger Railcars

- Buses

- Battery Electric Buses and Buy America

- Effects of Buy America on Transportation

- Proposed Legislation in the 116th Congress

- Strengthening Buy America Restrictions

- Broadening Buy America Requirements

Figures

Tables

Appendixes

Summary

In 1978, Congress began placing domestic content restrictions on federally funded transportation projects that are carried out by nonfederal government agencies such as state and local governments. These restrictions, which have changed over the years, are commonly referred to as the Buy America Act, or more simply, Buy America. Although there has been ongoing congressional interest in domestic preference policy over the years, statements and actions by the Trump Administration about reinvigorating domestic manufacturing and investing in infrastructure have stimulated renewed interest in Buy America.

Buy America refers to several similar statutes and regulations that apply when federal funds are used to support projects involving highways, public transportation, aviation, and intercity passenger rail, including Amtrak. Unless a nationwide or project-specific waiver is granted, Buy America requires the use of U.S.-made iron and steel and the domestic production and assembly of other manufactured goods, particularly the production of rolling stock (railcars and buses) used in federally funded public transportation and Amtrak's intercity passenger rail service. A separate law requires that at least half the value of products imported by sea for federally supported transportation projects be transported in U.S.-flag ships. This report examines the effects of Buy America on iron and steel manufacturing, rolling stock manufacturing, and transportation.

Although the Buy America provisions have been in place in some form for more than 40 years in transportation, it is difficult to know how they have affected steel and rolling stock manufacturing in the United States, whether measured by jobs, output, or any other indicator. Empirical evidence on the economic benefits or costs of domestic content laws is scarce, partly because the effects are small compared with macroeconomic forces such as global economic growth and the related growth in demand for steel. Buy America may have protected some domestic iron and steel manufacturing, and a relatively small number of jobs. Jobs in the domestic steel industry have declined sharply since 1990, largely attributable to factors such as higher industry productivity.

Buy America has likely bolstered the production of railcars and buses in the United States. These industries are comparatively small and employ relatively few workers. Railcar manufacturing, including freight rail, accounted for 0.2% of total factory employment in 2018. Demand for passenger railcars and buses is related strongly to the combined level of federal, state, and local government funding.

Transit rolling stock manufacturing in the United States by firms based in China appears to be Buy America compliant. Still, concerns have been raised by some Members of Congress about the economic and national security implications of this manufacturing production. Pending legislation seeks to prohibit transit agencies from buying buses and transit railcars from Chinese government-owned, -controlled or -subsidized companies.

For state and local providers of transportation infrastructure and services, Buy America could increase the cost of at least some projects, such as building highway bridges and procuring transit railcars and buses, and may result in fewer projects being undertaken. The price of steel produced in the United States tends to be higher than that of comparable steel produced in other countries. Buy America may also raise the cost of rolling stock procurements. The U.S. market is relatively small compared with those in other countries and regions, consequently domestic producers do not benefit from economies of scale. In addition, Buy America requirements have been blamed for project delays, which can arise from domestic supply problems, the difficulty of compliance, and the waiver application process.

Much of the congressional activity related to Buy America seeks to strengthen its requirements. The Fixing America's Surface Transportation (FAST) Act (P.L. 114-94), enacted in December 2015, increased the share of public transit rolling stock components and subcomponents that must be produced in the United States to 65% in FY2019, and to 70% for FY2020 onward. Other bills have proposed increasing the share to 100%. Legislative proposals have also called for expanding Buy America to other parts of the transportation system, such as pipelines and school buses, and to other sectors, such as federally funded school projects.

Introduction

Congress over the years has passed several domestic content laws that aim to protect American manufacturing and manufacturing jobs. In 1978, Congress began placing domestic content restrictions on federally funded transportation projects that are carried out by nonfederal government agencies such as state and local governments.1 These restrictions are commonly referred to as the Buy America Act, or more simply, Buy America; they differ from requirements under the Buy American Act of 1933, which governs purchases made directly by the federal government.2 Although there has been ongoing congressional interest in domestic preference policy over the years, statements and actions by the Trump Administration concerning the need to bolster domestic manufacturing and investment in infrastructure have reinvigorated the issue.3

Today, Buy America refers to several similar statutes and regulations that apply to federal funds used to support projects in highways, public transportation, aviation, and intercity passenger rail, including Amtrak.4 Unless a nationwide or project-specific waiver is granted, Buy America requires the use of U.S.-made iron and steel and the domestic production and assembly of other manufactured goods, such as rolling stock used in public transportation.5

To evaluate the implications of Buy America on the domestic economy, the report examines industry trends in the two most directly affected industries: iron and steel manufacturing and railcar and bus manufacturing. It also discusses the effects of Buy America on the transportation system. In addition, the report reviews legislative proposals introduced in recent Congresses that consider strengthening Buy America in transportation or broadening it to other infrastructure sectors.

Buy America Requirements

Laws and regulations governing Buy America requirements for transportation infrastructure differ according to the specific funding program and administering agency (see Table A-1). The agencies involved are the Federal Transit Administration (FTA), the Federal Highway Administration (FHWA), the Federal Railroad Administration (FRA), and the Federal Aviation Administration (FAA). Buy America also applies to purchases by Amtrak.6 In certain situations, the statutes permit a regulating agency to waive the Buy America provisions. If a state or local government does not use federal funds on a project, the project is not subject to Buy America (although states may have laws imposing similar requirements on state-funded purchases).7

Buy America provisions applicable to funds administered by FHWA, for example, are found at 23 U.S.C. §313 and 23 C.F.R. §635.410, and apply to iron and steel permanently incorporated into a highway project. This requirement can be waived if the Secretary of Transportation determines that it would be inconsistent with the public interest, that the materials are not produced in the United States in sufficient quantities or of a satisfactory quality, or that the inclusion of domestic materials will raise the cost of the overall project by more than 25%.8 FHWA determined in a 1983 rulemaking that Buy America would not apply to raw materials, such as iron ore, limestone, and waste products, all of which "may be imported."9 Waste products that may be used under this waiver include scrap steel. FHWA also waived the application of Buy America requirements to products other than those manufactured predominantly of iron and steel.10 In 2012, FHWA clarified that a manufactured product must consist of at least 90% iron and steel for it to be considered manufactured predominantly of iron and steel and, thus, subject to Buy America requirements.11 In 1995, FHWA determined that due to inadequate national supply, a national waiver would be granted for certain iron products used in the manufacture of steel or iron, including pig iron and iron ore that is reduced, processed, or pelletized.12

Even though FHWA waives Buy America requirements for manufactured products, except those made predominantly of iron and steel, this is not the case with other U.S. Department of Transportation (DOT) agencies and Amtrak.13 For example, for the purchase of rolling stock using FTA funds, the Buy America requirement is waived only if (1) the cost of the components produced in the United States in FY2019 is more than 65% of the cost of all components of the rolling stock, increasing to 70% for FY2020 onward; and (2) final assembly of the rolling stock occurs in the United States (49 U.S.C. §5323(j) and 49 C.F.R. §661). For a rolling stock component to be considered produced in the United States or of domestic origin, more than 65% in FY2019 and 70% in FY2020 onward "of the subcomponents of that component, by cost, must be of domestic origin, and the manufacture of the component must take place in the United States" (49 C.F.R. §661.11(g)).14 In FY2019, if more than 65% of the cost of a component's subcomponents is from domestic manufacturing, then 100% of the cost of the component is considered domestic when calculating the domestic content of rolling stock. The cost of a rolling stock subcomponent, in turn, is considered domestic if it is manufactured in the United States no matter what the origin of the elements that go into it—the sub-subcomponents (49 C.F.R. §661.11(h)). Buy America also permits rolling stock manufacturers to receive credit for U.S.-made steel or iron used in foreign-made car body shells, for which the average cost of the vehicle is more than $300,000.15

For manufactured goods other than rolling stock purchased using FTA funds, 100% of the components, including steel and iron, must be made in the United States and assembly must be done in the United States. According to 49 C.F.R. §661.5, "a component is considered of U.S. origin if it is manufactured in the United States, regardless of the origin of its subcomponents."

Trade Agreements and Domestic Preferences

The U.S. government builds few transportation projects directly. Instead, it generally funds highways, airports, and public transportation projects by making grants or loans to state or local governments. This funding structure has made it possible to avoid claims that Buy America violates international trade agreements.

The United States is a signatory to international agreements that restrict discrimination against trading partners in government procurement. Currently, 48 World Trade Organization (WTO) members, including the United States, have made binding commitments under the WTO Agreement on Government Procurement (GPA), whereby each provides the others access to its national procurement markets.16 Most U.S. bilateral and regional free-trade agreements also include public procurement provisions. These agreements are generally based on "national treatment," and they require the United States to treat goods, services, and suppliers of other signatories no less favorably than U.S. goods, services, and suppliers. As a consequence, firms based in countries covered by such agreements can bid on covered U.S. government procurement contracts over a certain dollar threshold. The thresholds are adjusted every two years.17 National treatment also means U.S. firms can bid on contracts in certain foreign procurement markets, where American suppliers are entitled to treatment no less favorable than domestic suppliers.

Although the United States is a WTO GPA signatory, state and local governments are excluded from coverage, unless they voluntarily agree to comply.18 Thus, state and local governments may require domestic sourcing restrictions when procuring with their own funds without violating international obligations. These international obligations, moreover, are not violated when state and local authorities have to comply with Buy America when using federal government grants or loans for transportation projects. Consequently, Buy America does not violate the WTO GPA.19

The exclusion of subnational procurement under the WTO GPA has caused considerable tension with major U.S. trading partners such as Canada. Unlike the United States and Canada, Mexico is not a member of the WTO GPA. For this reason subnational procurement with Mexico is governed instead by the North American Free Trade Agreement (NAFTA), which also permits the use of domestic preferences in state and local government contracts. The proposed United States-Mexico-Canada Agreement would not change this.20

Cargo Preference

Cargo preference is another restriction applicable to federally supported activities, in this case requiring that a portion of "government-impelled" cargoes be carried on U.S.-flag vessels.21 Although cargo preference is not a Buy America requirement, one cargo preference provision may affect transportation projects that are subject to Buy America. In 2008, Congress incorporated a provision in the FY2009 Duncan Hunter National Defense Authorization Act (NDAA) specifying that cargo preference requirements also apply to cargo that is imported by an organization or person if the federal government "provides financing in any way with federal funds for the account of any persons unless otherwise exempted."22 At least 50% of such cargo must be shipped in U.S.-flag vessels. The law directs DOT to issue regulations and guidance to govern the administration of cargo preference by other federal agencies.23

The Maritime Administration (MARAD) within DOT has not issued regulations to implement the cargo preference requirements of the FY2009 NDAA. The agency submitted a draft notice of proposed rulemaking for Office of Management and Budget approval in December 2011, but the process after interagency coordination efforts has not moved forward. MARAD has not indicated when it might restart the regulatory development process.24 FHWA has interpreted the law to apply cargo preference requirements to federally supported highway projects carried out by state departments of transportation and other agencies.25 MARAD has applied cargo preference requirements to vessel components imported for ships constructed with federal loan guarantees.26

Changes to Buy America in MAP-21 and FAST Act

Several changes to Buy America were included in the two most recent surface transportation reauthorization acts: the Moving Ahead for Progress in the 21st Century Act (MAP-21; P.L. 112-141), enacted in July 2012, and the Fixing America's Surface Transportation (FAST) Act (P.L. 114-94), enacted in December 2015. As part of MAP-21, Congress sought to prevent sponsors of highway projects from segmenting a project into smaller parts, some federally funded and some not, so as to free some segments of the project from Buy America requirements. To accomplish this, MAP-21 (Section 1518) specified that FHWA Buy America requirements apply to all contracts eligible for assistance within the scope of a project's National Environmental Policy Act (NEPA) document if at least one contract for the project is federally funded.27

This provision addressed issues that arose during reconstruction of the San Francisco-Oakland Bay Bridge by the California Department of Transportation (CalTrans). After a major earthquake in 1989, California decided to reconstruct the Bay Bridge by refurbishing the western span and replacing the eastern span. CalTrans determined that it could obtain imported steel from China for the project more cheaply than domestic steel. To avoid Buy America requirements, it decided the eastern span would be built without federal funds. Subsequently, and controversially, the eastern span was built using steel made in China.28

Another effect of the provision prohibiting the segmenting of projects is that utility relocation work done as part of a federally funded highway project must now be Buy America-compliant. Buy America applies even if the contract to do the utility work does not use federal funds.29 This change caused concern among state departments of transportation and industry associations that projects would be delayed as utilities sought to obtain Buy America-compliant products.30 In response, FHWA delayed implementation of the new requirements until January 1, 2014. The effects of compliance since then on highway projects, utilities, and manufacturers of products used by the utility industry are unknown.

MAP-21 also made changes aimed at making the FTA waiver determination process more transparent. MAP-21 requires FTA to publish each waiver request and a detailed explanation of the waiver determination in the Federal Register, and to make them easily accessible on its website. In addition, MAP-21 requires that FTA provide a report on waivers granted in the previous year to the Senate Committee on Banking, Housing, and Urban Affairs and the House Committee on Transportation and Infrastructure.

The FAST Act of 2015 increased the domestic content threshold for public transportation rolling stock from more than 60% in FY2017 and prior years to more than 65% for FY2018 and FY2019 and to more than 70% for FY2020 onward. It eliminated Buy America requirements for public transportation projects costing less than $150,000, up from the previous threshold of $100,000.31 In the event of a waiver denial, the FAST Act also requires FTA to certify that the items can be purchased in the United States in sufficient quantity and quality, along with a list of manufacturers. This information must be published on the DOT website.32

Presidential Statements and Actions

The Trump Administration has announced that it will pursue efforts to protect domestic industries as part of its "Buy American and Hire American" initiative. To date, this includes three actions with respect to Buy America.

First, in January 2017, President Trump signed an executive memorandum which requires the Secretary of Commerce to develop a plan to have all new pipelines in the United States "use materials and equipment produced in the United States, to the maximum extent possible and to the extent permitted by law."33 Despite a deadline of late July 2017, the Commerce Department has yet to produce such a plan, and there have been no other public actions specific to the memorandum.34 According to the memorandum, steel made in the United States from imported scrap or imported slabs is not to be considered produced in the United States.35

Second, Executive Order (E.O.) 13788, signed by the President in April 2017, directs that "every agency shall scrupulously monitor, enforce, and comply with Buy American Laws, to the extent they apply, and minimize the use of waivers, consistent with applicable law."36 The term "Buy American Laws" is defined in the executive order to include Buy America. Although the executive order does not rescind any trade agreements or call for their renegotiation, it does require the Secretary of Commerce and the Office of the U.S. Trade Representative "to assess the impacts of all United States free trade agreements and the World Trade Organization Agreement on Government Procurement on the operation of Buy American laws."37

Third, E.O. 13858, signed by the President in January 2019, directs federal agencies to encourage recipients of federal funding to use more American-produced goods, materials, and products in procurement contracts.38 As well as reiterating policy established in April 2017, the E.O. requires each agency administering infrastructure programs involving federal financial assistance to identify in a report to the President opportunities to maximize the use of Buy American principles. These reports were due no later than May 31, 2019. To date, no announcements have been made about the submission of these reports or the information they contain. The E.O. also encourages agencies providing financial assistance for infrastructure projects to promote the use of American-made steel, iron, aluminum, concrete, and other building and manufactured materials to recipients. Infrastructure projects are defined to include a wide range of sectors in addition to transportation, such as energy production, distribution, and storage; drinking water and wastewater; broadband internet; and cybersecurity.

It is not clear how these actions might alter affect the implementation of Buy America, if at all. So far, the Trump Administration has not changed the existing Buy America rules, but it is reconsidering them. For example, in a Federal Register notice published in April 16, 2018, FHWA noted that in response to E.O. 13788 the agency is "evaluating how to revise its Buy America policies and procedures, including the process and manner in which it decides whether to grant waivers for vehicles and equipment. This evaluation may result in delays in decisions on whether to grant Buy America waivers in the future."39

Effects of Buy America on U.S. Steel Manufacturing

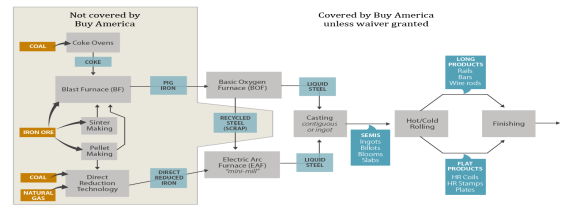

U.S. steel manufacturing is one industry directly affected by Buy America. Its provisions generally require the use of U.S.-made steel in a wide variety of applications. An overview of the domestic steel making process is necessary to understand Buy America's effects on the industry.

U.S. mills produce steel in three distinct ways. Approximately 68% of domestic production comes from plants known as minimills, which use electric arc furnaces to melt scrap steel and in some cases iron pellets. Another 31% is made in traditional integrated steel mills, which use ovens to turn coal into coke and then combine the coke with iron ore to produce pig iron in blast furnaces. The pig iron is then melted in a basic oxygen furnace to produce steel. A very small portion of U.S. production, approximately 1%, involves direct reduction technology, now used in a single U.S. mill.40

The raw materials used to produce steel in the United States largely come from domestic sources. Around 90% of the scrap used by minimills is obtained domestically, although the products from which scrap is commonly derived, such as vehicle bodies and beams used in construction, may originally have been imported. Integrated steel mills mostly use iron ore from Minnesota's Mesabi Iron Range and Michigan's Iron Range, which account for more than 90% of America's iron ore supply. U.S.-mined iron ore takes the form of taconite, a relatively low-grade source of iron-bearing rock typically containing 15% to 30% magnetic iron particles. To be useful in steelmaking, the taconite is formed into pellets before delivery to a steel mill.41

Figure 1 shows the iron and steel manufacturing process. Originally, Buy America covered raw materials used in steel manufacturing. A lack of adequate domestic supply resulted in a 1995 nationwide waiver for raw materials (iron ore and limestone); scrap (recycled steel scrap); pig iron; and processed, pelletized, and reduced iron ore.42 Because of the waiver, U.S. steel mills may use imported inputs to make Buy America-compliant steel products. Therefore, the part of steel production shown in the shaded section of Figure 1 is currently not subject to Buy America requirements.

|

|

Source: Figure adapted by CRS from Eurofer, Study on the Competitiveness of the European Steel Sector, August 2008, p. 10. |

After the steel is produced, it is cast into a variety of shapes and left to cool. Blocks of steel, known as ingots, which vary in size, are often rolled further to produce rectangular steel slabs. Companies known as slab converters have sought a nonavailability waiver for products manufactured in the United States from imported steel slabs.43 Slab converters claim there is insufficient supply of domestically made steel slabs available from U.S. integrated steel mills.44 In addition, they claim the original Buy America requirements were issued before slab converters even existed, and the requirement unfairly prevents them from participating in federal-aid highway projects. To date, FHWA has denied a waiver to slab converters, a position supported by steel industry trade groups such as the Steel Manufacturers Association, which considers a waiver on steel slabs to be a weakening of Buy America rules.45 This waiver seems unlikely to be issued in light of President Trump's executive order directing agencies to minimize the use of waivers, and the Trump Administration's more recent use of Section 232 tariffs.46 These tariffs limit imports of steel into the United States, including shipments of imported semi-finished steel slabs.47

Assessing the economic effects of Buy America on the steel industry is difficult due to the lack of relevant data.48 It is unclear how much iron and steel are used in transportation projects that receive federal funding; hence, data are not available to calculate how much steel is produced and sold domestically as a direct result of Buy America. Nevertheless, the available data suggest that the steel produced for the Buy America market represents a small portion of total domestic demand for steel.

Industry sources estimate that net shipments of steel mill products in the United States totaled 90.9 million tons in 2017. Of these shipments, roughly 23 million tons, or about a quarter, were consumed in public and private construction projects.49 This quarter, however, includes steel used in a range of nontransportation projects, such as office buildings, shopping centers, and apartment towers, as well as in transportation projects that are not publicly funded, such as those in the freight rail industry. Steel used in rail transportation projects of all types, including those undertaken by freight railroads as well passenger railcars and locomotives for Amtrak and commuter services, amounted to 1.2 million tons in 2017. This represented 1.9% of U.S. steel production in 2017.50

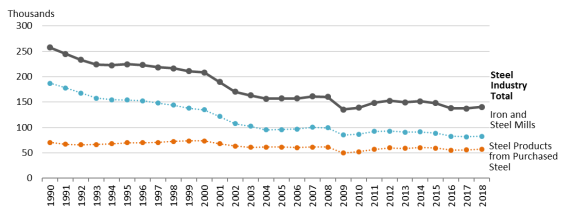

A key rationale for Buy America is its positive effect on steel industry employment. Direct employment in steel has declined from almost 260,000 jobs in 1990 to around 140,100 jobs in 2018 (Figure 2), due largely to higher productivity. While steel industry employment rose 2% from 2017 to 2018, it remained below the level prior to the recession that began in December 2007. According to the American Iron and Steel Institute (AISI), the number of labor hours needed to produce one finished ton of steel has fallen 81% since 1980, from 10.1 to 1.9 in 2017.51 If broader Buy America requirements were to increase annual demand for U.S.-made steel by 1 million tons (about 1%), and if each ton were to require 1.9 hours of labor, steel-industry, employment would be expected to rise by approximately 1,000 jobs (assuming a 1,900-hour work year). A similar estimate can be derived from data in a December 2013 report by the Steel Manufacturers Association, which represents North American minimills, indicating that an increase of 1 million tons of domestic steel production would create 792 new steel manufacturing jobs.52 Presumably, these jobs would pay well, as steel mill workers earned an average annual wage of $91,927 in 2018, significantly above the average of $68,528 for all manufacturing.53

|

|

Source: CRS analysis of Bureau of Labor Statistics, Current Employment Statistics, for iron and steel mills (NAICS 3311) and steel products from purchased steel (NAICS 3312). |

Using a macroeconomic model, researchers funded by the Canadian government concluded that eliminating Buy America requirements would result in 57,000 fewer U.S. manufacturing jobs, including about 1,600 fewer jobs in the United States in iron and steel production. However, they estimated that the U.S. economy overall would gain more than 300,000 jobs if Buy America were terminated.54 This is equal to approximately 0.2% of payroll employment in the United States.

The price of raw materials and components used to build transportation infrastructure and rolling stock depends, in part, on broader market conditions for such goods and, in part, on U.S. government policies. In 2018, for example, the U.S. government imposed tariffs on steel and aluminum products imported into the United States.55 This has increased not only the prices of imported products, but also of domestically produced products that compete with affected imports or use them as inputs. Consequently, the cost of some products needed to meet Buy America requirements has increased.

Effects of Buy America on U.S. Rolling Stock Manufacturing

Besides its restriction on the sourcing of iron and steel, Buy America also places limits on state and local governments and Amtrak when using federal funds to purchase manufactured goods. One of the main manufactured products this affects is rolling stock, which includes intercity passenger rail trains, public transportation railcars and buses, and associated equipment. Under Buy America domestic sourcing requirements, as noted earlier, rolling stock final assembly must take place in the United States. Moreover, significant proportions of the systems and components used to assemble railcars and buses must be manufactured in the United States, although the specific statutory and regulatory requirements can differ depending on the agency source of the federal funds.

According to one industry estimate, the U.S. domestic market for railroad rolling stock totaled more than $22 billion in 2019.56 Federal data indicate that manufacturers of all types of railroad rolling stock directly employed approximately 22,900 workers in 2018, up 2.5% from a decade earlier. The industry accounted for 0.2% of total factory employment in 2018.57 These data, however, cover the production of equipment that is not publicly funded and thus not subject to Buy America, such as freight locomotives and freight railcars. According to one industry estimate, the size of the U.S. market for all types of railcars—passenger and freight—was $6.9 billion in 2019, but only some is affected by the Buy America requirements and that portion is unknown.58

Passenger Railcars

Buy America supports production of railcar manufacturing in the United States. Foreign-based manufacturers supply most of the U.S. market for passenger railcars, including subway and light rail vehicles. Major passenger railcar assembly plants currently operating in the United States include Hornell, NY (Alstom); Plattsburgh, NY (Bombardier); Lincoln, NE (Kawasaki); Yonkers, NY (Kawasaki); Sacramento, CA (Siemens); Salt Lake City, UT (Stadler); and Springfield, MA (China Railway Rolling Stock Corporation, CRRC). In June 2019, Bombardier announced plans to open a new assembly plant in Pittsburg, CA, to make cars for the San Francisco Bay Area Rapid Transit District (BART). In 2018, two domestic passenger railcar assembly plants closed. One was operated by the South Korean company Hyundai Rotem in Philadelphia, and the other was operated by the Japanese company Nippon Sharyo in Rochelle, IL.59

CRRC, a company owned by the Chinese government, is a relatively new entrant into the passenger railcar market in the United States. The company is subject to Buy America in the same way as any other railcar manufacturer. It won its first contract to build railcars for the Massachusetts Bay Transportation Authority (MBTA) in 2014. This contract did not involve federal funds so Buy America does not apply. CRRC has also won federally supported contracts for public transportation railcars subject to Buy America from the Chicago Transit Authority (CTA), the Los Angeles Metro, and the Southeastern Pennsylvania Transportation Authority (SEPTA) in Philadelphia.60 CRRC opened an assembly plant in Springfield, MA, in 2018 to assemble subway cars for the MBTA.61 CRRC is also constructing a second $100 million railcar assembly plant in Chicago, which may be fully operational later in 2019.62

Although not directly a Buy America issue, some Members of Congress have expressed particular interest in CRRC because of allegations that, as a state owned enterprise (SOE), it can underbid the competition to win U.S. transit contracts. The allegation has not been proven, and CRRC has not won every U.S. contract on which it has bid.63 A 2019 congressional hearing heard concerns about the security implications of Chinese-SOE made railcars operating domestically.64 CRRC is reportedly interested in bidding for a contract with the Washington Metropolitan Area Transit Authority (WMATA).65 Legislation introduced in the 116th Congress seeks to prevent transit agencies in general, and WMATA specifically, from receiving certain federal funds if they buy railcars from CRRC. Depending on how these provisions are written and interpreted, transit agencies also may be prohibited from purchasing rolling stock from other Chinese companies, such as BYD, a bus manufacturer.66

Factories that assemble passenger railcars and transit vehicles typically lack private customers. Their dependence on contracts partially funded by federal grants means that they are comparatively small and may lack economies of scale that could help reduce unit costs. Their cost structures and the varying requirements for transit and passenger rail vehicles in other countries may make it difficult for U.S. plants to export. North America is a relatively small market for transit rolling stock and is likely to remain so.67

Over the last decade, annual domestic deliveries of new passenger railcars have fluctuated from a low of 208 units in 2017 to a high of 1,141 in 2009 (see Table 1). Since 2009, domestic manufacturers have shipped almost 7,900 new passenger railcars to Amtrak and transit agency purchasers. This figure includes regional, intercity, rapid transit, and light railcars as well as streetcar units. In addition, there were reports of a backlog of more than 1,000 vehicles at the end of 2018, including orders for 10 intercity railcars for Amtrak to be manufactured by CAF USA and 168 high-speed intercity railcars to be made by Alstom, 160 rapid transit railcars to be manufactured by Bombardier for the New York City Transit (NYC Transit) system in New York, and 64 light rail railcars to be built by CRRC for the Los Angeles subway system.68 It is unclear how much of this manufacturing would occur in the United States in the absence of Buy America.

|

Year |

Regional/Intercity |

Rapid Transit |

Light Rail/Street Car/Automated People Mover |

Total |

|

2009 |

187 |

752 |

202 |

1,141 |

|

2010 |

199 |

782 |

148 |

1,129 |

|

2011 |

235 |

113 |

149 |

497 |

|

2012 |

343 |

243 |

59 |

645 |

|

2013 |

531 |

337 |

166 |

1,034 |

|

2014 |

251 |

484 |

116 |

851 |

|

2015 |

251 |

462 |

258 |

971 |

|

2016 |

94 |

424 |

188 |

706 |

|

2017 |

34 |

34 |

140 |

208 |

|

2018 |

373 |

220 |

98 |

691 |

|

Total |

2,498 |

3,851 |

1,524 |

7,873 |

Source: 2018 Passenger Rail Car Market, Railway Age, pp. 46-47, January 2019.

In the context of current Buy America restrictions, and based on one recent estimate, the outlook for orders through 2024 is for more than 6,500 new passenger railcars, including intercity, commuter rail, and transit railcars.69 An unknown for the entire industry is the level of future federal assistance to vehicle purchasers. If federal funding declines, many transit operators will, in all probability, reduce their demand for new vehicles and opt where possible to rebuild their current fleets for extended service. Alternatively, if federal funding increases, demand for new domestically produced passenger rail cars will likely grow.

Meeting Buy America requirements can be challenging because assemblers of transit vehicles depend on an extensive global supply chain that includes steel and aluminum producers and component suppliers that make thousands of parts and accessories such as transmissions, axles, steering systems, and engines. An estimate by First Research, a private research firm, says purchased steel and specialty components represent 50% or more of rolling stock manufacturing costs.70 In 2010, the Duke University Center on Globalization, Governance & Competitiveness identified about 150 subcontractor firms in the United States that sold components to passenger and transit rail vehicle manufacturers.71

Buses

Manufacturing of transit buses in the United States has been a small and concentrated manufacturing sector over the past few decades, despite Buy America.72 In 2018, the market research group First Research estimated domestic bus manufacturing revenue at around $5 billion, including school buses and intercity buses along with public transit buses.73 According to the American Public Transportation Association (APTA), each year transit agencies purchase somewhere between 4,000 to 6,000 buses.74 Like other vehicles, transit buses are mostly made of steel.75

In 2017, New Flyer, Gillig, and Nova were the three largest manufacturers of heavy-duty transit buses in the United States, representing more than 80% of total production. New Flyer makes around 1,000 transit buses annually in Minnesota, Alabama, and Indiana.76 Gillig, a privately owned U.S.-headquartered manufacturer, makes fewer than 1,000 transit buses a year in California, with the capacity to make 1,800 buses annually, and it is working on its first battery electric bus.77 Nova, a subsidiary of the Swedish firm Volvo Group, holds most of the remaining share of the North American market. Nova's bus plant in Plattsburgh, NY, manufactures 40-foot buses and 62-foot articulated buses.78 Orion, part of Daimler Buses North America, stopped assembling buses in the United States in 2013, citing "low public sector investments by municipal government agencies" as a reason.79

The federal government does not provide labor market statistics for bus manufacturing, but publicly available data indicate that the number of workers employed in bus manufacturing is relatively small. For instance, New Flyer employed around 6,000 workers in 2018, and Gillig had about 960 workers in 2017.80 In addition, there are likely several thousand more jobs in the broader bus manufacturing supply chain.

Battery Electric Buses and Buy America

Battery electric buses represent a tiny fraction of the total number of transit buses operating in the United States, but their future development and production may cause significant changes to the bus market. According to reports, there were fewer than 300 battery electric transit buses operating in the United States at the end of 2017, less than 1% of all transit system buses.81 One reason for the smaller number of battery electric buses is that they are costly to purchase, although operating costs are typically lower than for other types of buses. For example, a 40-foot diesel bus costs roughly $525,000, compared to a comparable battery electric bus at nearly $775,000.82 The costs of natural gas and hybrid buses fall somewhere in between these amounts. Other reasons for limited use have been battery capacity, with an electrical charge often limiting bus operating range to about 150 miles, and the need for new types of supporting infrastructure.83

Three companies currently assemble battery electric buses in the United States. One is BYD (Build Your Dreams), a Chinese company. Its workforce, numbering nearly 900 U.S. employees, assembles electric transit buses in California. BYD has the capacity to produce 1,500 electric buses per year in the United States, using its own battery-cell technology.84 Another manufacturer is New Flyer; all of its factories in the United States are capable of producing electric buses. New Flyer delivered its first two battery electric buses to the Chicago Transit Authority in 2014.85 A third is Proterra, a privately owned U.S. company. It has factories in California and South Carolina, where it assembles 35- and 40-foot battery electric transit buses for customers such as Foothill Transit, serving Los Angeles's San Gabriel Valley.86 Other manufacturers are developing electric buses, including Gillig, which expects to manufacture its first battery electric bus in 2020.87

Unlike conventionally powered buses, battery electric buses do not have engines or transmissions to power them. Instead, large batteries and an electric motor are used for propulsion. The batteries are manufactured with thousands of small lithium ion cells that are combined into increasingly larger groups—in some cases called cassettes, blocks, and modules—through welding and other techniques. Sensing, cooling, and battery management system technology is added before modules are wired into a large pack. By one estimate, a battery pack accounts for about 26% of the cost of making an electric bus. The majority of lithium-ion battery manufacturing capacity is currently located in China.88 BYD, one of the world's leading battery manufacturers, has three lithium-ion battery factories in China.89 According to a press report, BYD may build additional battery factories in Europe and the United States.90 LG Chem, a South Korean manufacturer, is another leading producer of batteries used in vehicles sold in the United States.91

In most cases, bus manufacturers import lithium ion cells that are assembled into batteries in the United States. Importing lithium ion cells does not appear to violate Buy America, possibly because they are considered sub-subcomponents that are substantially transformed into subcomponent packs with modules, coolants, and sensors in U.S. manufacturing plants. As noted earlier, a rolling stock subcomponent is considered domestic if it is manufactured in the United States no matter what the origin of the elements that go into it. FTA has been reviewing its assessment of components, subcomponents, and manufacturing processes in the production of battery electric buses. To date, the agency has not proposed a revision to Buy America regulations that might take account of newer technologies such as those used in battery electric buses.

Effects of Buy America on Transportation

Buy America is primarily an industrial policy intended to protect U.S. manufacturing and manufacturing employment from foreign competition. For example, international manufacturers supply most transit railcars to domestic transit agencies, but to comply with Buy America these employers have set up assembly plants located in the United States. For state and local providers of transportation infrastructure and services, however, Buy America could increase the cost and completion time of at least some projects, such as building highway bridges and procuring transit railcars and buses, and this may result in fewer projects being undertaken. Quantifying the effects of Buy America on project costs and time is difficult because Buy America is only one of many economic and regulatory factors that determines them.92

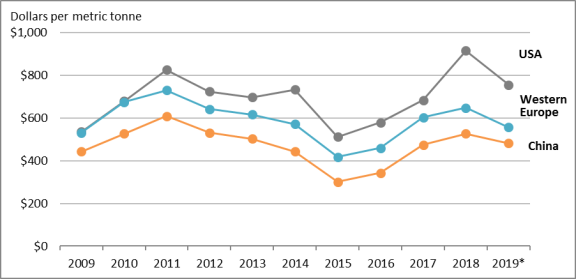

Buy America rules prohibit agencies from buying less-expensive steel from overseas suppliers for use in public works projects. However, a project sponsor can apply for a waiver if inclusion of domestically produced iron, steel, or manufactured goods would increase the overall cost of the project by more than 25%. The price of steel produced in the United States tends to be higher than that of comparable steel produced in other countries.93 For example, the benchmark average U.S. hot-rolled band price in recent years has consistently been higher than the Chinese price and, in most years, has been higher than the Western European price (Figure 3). However, higher transportation costs for imported steel may reduce or eliminate its cost advantage at a particular project site.

In 2018, for example, the average price of domestic hot-rolled band was $916 per metric ton, which was about $400 per metric ton higher than the price of the same product made in China. Industry estimates suggest that freight, insurance, and handling from Asia to ports on the Pacific and Gulf coasts would have added about $60 per metric ton to the import price, leaving a Chinese cost advantage of $330 per ton at dockside.94 The differential with respect to a particular project would also depend on the costs of moving steel from a domestic mill or a port to the job site. Both steel costs and freight transportation costs can vary significantly over time due to global steel demand, energy prices, exchange rates, and other factors. In the United States, hot-rolled band prices increased sharply during the first half of 2018, with the price registering a 10-year high of more than $1,000 per metric ton at the beginning of July 2018. U.S. steel prices have been dropping since then to $671 per metric ton in June 2019. One factor that contributed to higher steel prices in the first half of 2018 was the 25% tariff the Trump Administration imposed on imported steel in March 2018.

|

Figure 3. Steel Prices Excluding Transportation and Other Importation Costs Hot-Rolled Band Price, 2009-2019 (Current Dollars) |

|

|

Source: World Steel Dynamics, Steelbenchmarker: Price History, Tables and Charts, June 10, 2019, http://steelbenchmarker.com/files/history.pdf. Notes: *Average price through June. For other years, prices are annual averages. The hot-rolled band price is the price of the first product off the hot strip mill. Price data does not include freight, insurance, handling, import tariffs, and other associated costs. |

An assessment of the costs of using domestically produced steel in federally funded highway projects between 2009 and 2011 estimated that Buy America requirements increased the cost of construction by $652 million annually, or about $2 billion over the three-year period.95

Buy America may also raise the cost of rolling stock procurements. One reason is that the U.S. market is relatively small compared with those in other countries and regions; consequently, domestic producers do not benefit from economies of scale. According to one estimate, in 2015, the transit bus fleet in North America was about half the size of that in Europe and about one-eighth the size of the fleet in China.96 Similarly, the number of metro railcars in service in North America is about half that of Europe and a quarter the number in the Asia-Pacific region (including China, India, South Korea, and Japan).97

An analysis of bus procurement in public transportation notes that buses in the United States are about twice the price of those in Japan and South Korea. This study also makes the case that bus purchasers are limited in their choice of buses, and that the domestic industry is less innovative. The authors conclude that if public transit agencies could import buses, "they would have access to a greater menu of differentiated products at lower prices. This would lead to a higher quality of service provision (e.g., better service frequency and coverage) which could induce urbanites to substitute from private vehicles to buses."98

An analysis of transit railcar procurements in 5 U.S. cities and 14 cities in other economically advanced countries found that costs were 34% higher in the United States. However, the authors note that the "cost-differential between U.S. metro cars and foreign metro cars is likely explained by more than just Buy America regulations."99

Other direct costs associated with Buy America are mainly related to administering and enforcing its requirements, costs that are mostly absorbed by state and local government project sponsors. These costs include the effort required by contractors to document the national origin of iron, steel, and manufactured products and agency administration of the certification process. Extra work may also be required of contractors to put together two bids for a given project, one incorporating domestic products and one with foreign products. Waiver requests, another cost, may be prepared by the state or local government project sponsor alone or in cooperation with the contractor.100

Buy America may make it more time-consuming to complete transportation projects, ultimately causing higher project costs. Delays can arise from domestic supply problems and the waiver application process. Extending Buy America requirements to utility relocations, for example, led to concerns about project delivery among state departments of transportation.101 The private developer of a proposed high-speed rail line from the outskirts of Los Angeles (Victorville) to Las Vegas, XpressWest, blamed Buy America compliance for blocking its plans. The company sought low-cost financing through the federal Railroad Rehabilitation and Improvement Financing (RRIF) program, subjecting it to Buy America. Although there were other issues with the project, the Secretary of Transportation suspended consideration of the loan request because the sponsors were having difficulties satisfying the Buy America requirements.102

More generally, in a survey of people in the public transportation industry in the mid-1990s, Buy America was mentioned by respondents as the cause of project delay more often than any other reason.103 One possible reason is that compliance with Buy America requirements is often not straightforward. Sometimes there are disagreements about whether a good should be treated as an end product, a component, or a subcomponent, and a project may be delayed while the federal agency concerned considers the circumstances of a particular procurement.104

An example of this is the installation of a water mist fire suppression system by New York's Metropolitan Transportation Authority (MTA) in two new stations as part of the federally funded Second Avenue subway project. Originally, MTA entered into contracts to buy a fire suppression system from a company that manufactured many of the parts in Finland. After studying the situation in 2011, the MTA found that the fire suppression system would be Buy America compliant because it was a component of the end product, the transit station. Thus, the parts of the fire suppression system, the subcomponents, could be made in a foreign country. A second company challenged this interpretation in 2013, and FTA began a formal investigation in 2014. In 2015, FTA determined that the fire suppression system was the end product not the transit station, thus the pieces of the system were components and would have to be made in the United States to be Buy America compliant. Consequently, MTA was required to start over with the procurement of a fire suppression system.105

Cargo preference requirements for imported materials purchased by state and local governments and private organizations with federal financial assistance have the potential to raise costs of transportation projects and contribute further to delays. Shipping rates for cargo aboard U.S.-flag vessels tend to be higher than those for similar cargo on foreign-flag vessels, and services are less frequent, as the number of U.S.-flag commercial vessels providing international service is much smaller than the number of foreign-flag vessels serving the United States.106 For such reasons, imported materials purchased under Buy America waivers generally may be less attractive to project sponsors if the imported products are subject to cargo preference.

Although Buy America may increase the cost and completion time of transportation projects, its effects may be less important overall than other federal requirements. In its 2008 study of highway projects, GAO found that Buy America was mentioned much less often by state department of transportation officials than environmental requirements when asked about decisions to undertake projects without federal funds. Of 39 states that indicated they had decided not to use federal funds to avoid federal requirements in the last 10 years, 33 mentioned environmental requirements and 5 mentioned Buy America.107

To avoid federal requirements that attach to federal funding, including Buy America, several states have enacted legislation that encourages state and local governments to concentrate federal highway funding, where possible, on a lesser number of state department of transportation-controlled projects. In Nebraska, for instance, the Federal Funds Purchase Program, which has been in effect since 2013, allows local public agencies to exchange the use of federal funds for a reduced amount of state funds, currently 90%.108 This reduces the number of projects to which Buy America applies. Federal law requires that states expend a proportion of their federal highway funding in certain geographic areas, but otherwise does not restrict how state departments of transportation distribute their grants among jurisdictions within the state.

Proposed Legislation in the 116th Congress

As Congress discusses a possible infrastructure program and prepares for reauthorization of surface transportation programs in 2020, many legislative proposals related to domestic content have emerged. While most would strengthen transportation-related Buy America restrictions, some would expand the coverage of Buy America beyond the realm of transportation. This section discusses measures proposed in the 116th Congress.

Strengthening Buy America Restrictions

The FAST Act, enacted in December 2015, made Buy America more restrictive by increasing the share of public transit rolling stock components and subcomponents that must be produced in the United States. Legislation such as the Buy America 2.0 Act (H.R. 2755), introduced by Representative Boyle, would increase the share of public transit rolling stock components and subcomponents that must be produced in the United States by five percentage points annually beginning in FY2021, reaching 100% by FY2026. The bill would also mandate that 100% of components and subcomponents in FAA's facilities and equipment purchases be U.S.-made by FY2026.

The BuyAmerican.gov Act (S. 1324/H.R. 2472), introduced by Senator Portman and Representative Lipinski, would require the General Services Administration to establish a centralized, publicly available website to collect and display information about each requested waiver of Buy America laws and regulations. The Keep Buying American Act (S. 405), introduced by Senator Stabenow, would mandate that annual reports required under E.O. 13788 and E.O. 13858 be submitted to Congress and published publicly.

In response to increased investment in the United States by Chinese railcar and bus manufacturers, Senator Cornyn and Representative Rouda introduced the Transit Infrastructure Vehicle Security Act (S. 846/H.R. 2739).109 The bills would prevent federal funds from being used by transit agencies to purchase railcars or buses manufactured by an entity that

is owned or controlled by, is a subsidiary of, or is otherwise related legally or financially to a corporation based in a country that—(i) is identified as a nonmarket economy country (as defined in section 771(18) of the Tariff Act of 1930 (19 U.S.C. 1677(18))) as of the date of enactment of this subsection; (ii) was identified by the United States Trade Representative in the most recent report required by section 182 of the Trade Act of 1974 (19 U.S.C. 2242) as a priority foreign country under subsection (a)(2) of that section; and (iii) is subject to monitoring by the Trade Representative under section 306 of the Trade Act of 1974 (19 U.S.C. 2416).

These provisions would likely apply to Chinese government-owned, -controlled or -subsidized companies, including CRRC and BYD. If enacted, these provisions would prevent transit agencies from purchasing rolling stock from such companies even when they are Buy America compliant. Other provisions in the bill would prevent transit agencies from sidestepping this prohibition by using only state and local funds when procuring rail rolling stock. The measure includes a grandfather clause for rail rolling stock purchase contracts entered into before the enactment of the legislation. It also would require any agency that operates rail transit service to develop and execute a plan for identifying and reducing cybersecurity risks.110

Broadening Buy America Requirements

Buy America-type requirements are no longer restricted to the transportation sector. Requirements for domestically made iron and steel products are included in both the clean water state revolving fund (CWSRF) and drinking water state revolving fund (DWSRF) programs.111 Bills have been proposed to expand Buy America to other parts of the transportation system, to further infrastructure sectors, and to infrastructure materials other than iron and steel.

The Made in America Act (S. 1955/H.R. 3459), introduced by Senator Baldwin and Representative Garamendi, would apply Buy America-type requirements to several federal infrastructure-related programs where there are currently no such requirements. It would also broaden these requirements beyond iron, steel, and manufactured products to cover purchases of other construction materials such as nonferrous metals, plastic products, concrete, glass, lumber, and drywall.

The Clean School Bus Act of 2019 (S. 1750), introduced by Senator Harris, would create a new program in the Department of Energy to provide grants to school districts to buy electric school buses. Grant recipients would be required to adhere to Buy America requirements similar to those for transit agencies using federal transit funding.

The Strengthening Buy America for Small Shipyard Grants Act (S. 1287), introduced by Senator Baldwin, would add a Buy America requirement to the Small Shipyard Grants program administered by the Maritime Administration.

S. 266/H.R. 865 the Rebuild America's Schools Act, introduced by Senator Jack Reed and Representative Robert Scott, would extend Buy America requirements to school infrastructure projects supported by a federal grant or certain types of tax-preferred bond. It would require that these infrastructure projects use American-made iron, steel, and manufactured products.

Appendix. DOT Buy America Requirements

|

Agency |

Domestic Content |

Price Threshold |

Potentially Affected Industries |

Basis for Waivers |

|

Federal Transit Administration (FTA): |

100% U.S.-made requirement for iron, steel, and manufactured goods. Buy America does not apply to rolling stock if in FY2019 more than 65% of components, by value, are produced domestically and final assembly is in the United States. Threshold rises to more than 70% from FY2020 |

Above $150,000 (FTA's statute at 49 U.S.C. 5323(J)(13) is no longer tied to the U.S. government's simplified acquisition threshold) |

Iron and steel producers; |

1. Inconsistent with the public interest, which can include a wide range of impacts on domestic markets or firms, or on project outcomes |

|

Federal Highway Administration (FHWA): |

100% U.S.-made requirement for iron, steel, and manufactured goods made predominantly of steel and iron |

Above $2,500 or 0.1% of the contract price, whichever is greater |

Iron and steel producers; |

1. Inconsistent with the public interest |

|

Federal Railroad Administration (FRA): |

100% U.S.-made requirement for iron, steel, and manufactured goods |

Above $100,000 |

Iron and steel producers; |

1. Inconsistent with the public interest |

|

Federal Aviation Administration (FAA): |

All steel and manufactured goods must be produced in the United States. Preference does not apply if more than 60%, by value, of all components and subcomponents of the facility or equipment are produced domestically and final assembly is in the United States |

Unspecified; |

Iron and steel producers; manufacturers of products for airport construction and operation |

1. Inconsistent with the public interest |

|

Amtrak (National Railroad Passenger Corporation): |

All manufactured and unmanufactured goods must be substantially domestic; |

$1 million and above |

Iron and steel producers; |

1. Inconsistent with the public interest |

Source: CRS, adapted from U.S. Department of Transportation, Buy America Provisions—Side-by-Side, http://www.transportation.gov/buy-america-provisions-side-side-comparison.

Author Contact Information

Acknowledgments

Amber Wilhelm, Graphics Specialist, provided assistance with the figures in this report.

Footnotes

| 1. |

Buy America requirements date to the passage of the Surface Transportation Assistance Act of 1978 (STAA; P.L. 95-599). |

| 2. |

CRS Report R43354, Domestic Content Restrictions: The Buy American Act and Complementary Provisions of Federal Law, by David H. Carpenter and Erika K. Lunder. |

| 3. |

Executive Order 13788, "Buy American and Hire American," 82 Federal Register 18837, April 21, 2017; Executive Order 13858, "Strengthening Buy-American Preferences for Infrastructure Projects," 84 Federal Register 2039, February 5, 2019. |

| 4. |

Congress has also established Buy America-type requirements applicable to certain water infrastructure projects funded by the Environmental Protection Agency. |

| 5. |

Rolling stock is a broad term, which Buy America (49 C.F.R. Part 661.3) defines as "transit vehicles such as buses, vans, cars, railcars, locomotives, trolley cars and buses, and ferry boats, as well as vehicles used for support services." |

| 6. |

A side-by-side comparison of the Buy America provisions applying to various U.S. Department of Transportation (DOT) agencies can be found at http://www.transportation.gov/highlights/buyamerica. Programs administered by the Maritime Administration are not subject to Buy America requirements, but they are subject to other domestic preference restrictions that derive from earlier statutes such as the Jones Act, which refers to Section 27 of the Merchant Marine Act of 1920, P.L. 66-261, as amended. |

| 7. |

For example, in 1978 Pennsylvania enacted the Steel Products Procurement Act, which requires suppliers contracting with a public agency to use U.S.-made steel unless the head of a public agency determines that the required steel products are not produced domestically in sufficient quantities. 73 Pa. S. §§1881 et seq. Several other states have enacted some form of domestic steel preference legislation, including Maryland, Texas, and West Virginia. See Government Accountability Office (GAO), Federal-Aid Highways: Federal Requirements for Highways May Influence Funding Decisions and Create Challenges, but Benefits and Costs Are Not Tracked, GAO-09-36, p. 28, December 2008. |

| 8. |

23 U.S.C. §313(b). |

| 9. |

48 Federal Register 1946 (Interim Final Rule, January 17, 1983); 48 Federal Register 53099, 53103 (Final Rule, November 25, 1983). |

| 10. |

Ibid, 53099. |

| 11. |

Federal Highway Administration, "Clarification of Manufactured Products under Buy America," memorandum from John R. Baxter, Associate Administrator for Infrastructure to FHWA Division Administrators, December 21, 2012, https://www.fhwa.dot.gov/construction/contracts/121221.cfm. |

| 12. |

FHWA, 60 Federal Register 15478-15479, March 24, 1995, http://www.gpo.gov/fdsys/pkg/FR-1995-03-24/pdf/95-7362.pdf. |

| 13. |

The law (49 U.S.C. §24305(f)(2)(B)) requires Amtrak to purchase goods that are manufactured in the United States "substantially from articles, material, and supplies mined, produced, or manufactured in the United States." FRA has interpreted "substantially" to mean that the manufactured goods must have domestic component content greater than 50%, by cost. See letter from Joseph Szabo, Administrator, Federal Railroad Administration (FRA), to Jeff Martin, Chief Logistics Officer, Amtrak, "Re: Request for a Buy American Exemption for Acela Power Car Central Block Assemblies," March 7, 2012, available at https://www.fra.dot.gov/eLib/Details/L04370. FRA has been delegated authority by the Secretary of Transportation to evaluate requests from Amtrak for exemptions from these requirements. FRA, "Buy America Frequently Asked Questions," https://www.fra.dot.gov/eLib/Details/L02740, p. 11. |

| 14. |

Federal Transit Administration Buy America regulations define a component as "any article, material, or supply, whether manufactured or unmanufactured, that is directly incorporated into the end product at the final assembly location" (49 C.F.R. §661.3). Moreover, "a component is considered to be manufactured if there are sufficient activities taking place to advance the value or improve the condition of the subcomponents of that component; that is, if the subcomponents have been substantially transformed or merged into a new and functionally different article" (49 C.F.R. §661.11(e)). See also, FTA, Conducting Pre-Award and Post-Delivery Audits for Rolling Stock Procurements, FTA Report No. 0106, January 2017, p. 54. |

| 15. |

Section 3011 of the FAST Act (49 U.S.C. §5323(j)(5)). |

| 16. |

For a list of signatories, see https://www.wto.org/english/tratop_e/gproc_e/memobs_e.htm. |

| 17. |

The thresholds differ depending on the type of procurement and the level of government making the purchase. |

| 18. |

More than three dozen states have voluntarily waived most of their domestic preference provisions for state procurement. Several large manufacturing states, including Georgia, Indiana, New Jersey, Ohio, and Virginia, have not agreed to comply with the WTO GPA (see Annex 2 of the U.S. GPA Agreement). For more information on the United States' international procurement obligations, see https://ustr.gov/issue-areas/government-procurement/additional-information-on-US-Procurement. |

| 19. |

Revised WTO GPA Annex 2, note 5 ("For the state entities included in this Annex, this Agreement does not apply to restrictions attached to federal funds for mass transit and highway projects."). |

| 20. |

See United States-Mexico-Canada Agreement Text, https://ustr.gov/trade-agreements/free-trade-agreements/united-states-mexico-canada-agreement/agreement-between; CRS Report R44981, NAFTA Renegotiation and the Proposed United States-Mexico-Canada Agreement (USMCA), by M. Angeles Villarreal and Ian F. Fergusson. |

| 21. |

46 U.S.C. §55305, 46 C.F.R. Part 381. |

| 22. |

P.L. 110-417, §3511; 46 U.S.C. §55305(b). |

| 23. |

The application of the law to nonfederal entities is codified at 46 U.S.C. §55305; 46 C.F.R. §381.7. The law specifies that cargo preference includes cargoes generated by a federal grant, guaranty, loan, and/or advance of funds program. It also applies to the borrower, grantee, and any of their contractors or subcontractors. |

| 24. |

U.S. Congress, House Committee on Transportation and Infrastructure, Subcommittee on Coast Guard and Maritime Transportation, The State of the U.S.-Flag Maritime Industry, 115th Cong., 2nd sess., January 17, 2018, p. 10. |

| 25. |

FHWA, "Cargo Preference Act and Federal-aid Projects," Letter from Chief Counsel, December 8, 2015, https://www.fhwa.dot.gov/construction/cqit/cargo/151208.cfm. |

| 26. |

80 Federal Register 22611, April 22, 2015. Comments filed by U.S. shipbuilders and domestic ocean carriers in response to the proposed policy clarification asserted that the requirement would severely disrupt shipbuilding supply chains. For additional background, see CRS Report R44831, Revitalizing Coastal Shipping for Domestic Commerce, by John Frittelli. |

| 27. |

NEPA requires federal agencies to assess the potential environmental impacts of a proposed action before proceeding (P.L. 91-190; 42 U.S.C. §4321 et seq.). |

| 28. |

David Barboza, "Bridge Comes to San Francisco With a Made-in-China Label," New York Times, June 25, 2011. |

| 29. |

Gloria M. Shepherd, Application of Buy America to non FHWA-funded Utility Relocations, FHWA, July 11, 2013, http://www.fhwa.dot.gov/construction/contracts/130711.cfm. |

| 30. |

Letter from the American Association of State Highway and Transportation Officials, et al., to the Secretary of Transportation, "Application of Buy America Requirements to Utility Relocations," June 28, 2013, https://www.crowell.com/files/Application-of-Buy-America-Requirements-to-Utility-Relocations.pdf. |

| 31. |

FTA has issued policy guidance on the small purchase waiver, which states that FTA procurements are statutorily fixed at a small purchase threshold of $150,000 or less, regardless of the size of the project, 49 U.S.C. § 5323(j)(13). For additional information, see FTA's website at https://www.transit.dot.gov/buyamerica. |

| 32. |

FTA, "Fact Sheet: Buy America, 5323(j)," https://www.transit.dot.gov/funding/grants/buy-america-fact-sheet. |

| 33. |

Executive Memorandum, "Construction of American Pipelines," 82 Federal Register 8659, January 30, 2017, https://www.gpo.gov/fdsys/pkg/FR-2017-01-30/pdf/2017-02031.pdf. |

| 34. |

The presidential memorandum of January 24, 2017, instructed that "The Secretary shall submit the plan to the President within 180 days of the date of this memorandum." |

| 35. |

Some U.S. steel companies, such as slab converters California Steel Industries and NLMK USA, claim there is an acute domestic slab shortage, while other steel producers say there is plenty of slab readily available in the United States. The Department of Commerce's Bureau of Industry and Security, in response to an exclusion request by CSI from Section 232 tariffs, ruled in 2019 that slabs made in the United States are in a "sufficient and reasonably available amount and of a satisfactory quality." |

| 36. |

Executive Order 13788, "Buy American and Hire American," 82 Federal Register 18837, April 21, 2017. |

| 37. |

Ibid. |

| 38. |

Executive Order 13858, "Strengthening Buy-American Preferences for Infrastructure Projects," 84 Federal Register 2039, February 5, 2019. |

| 39. |

FHWA, "Buy America Waiver Notification," 83 Federal Register 16422, April 16, 2018. |

| 40. |

Direct reduction technology is used to produce iron ore in a thermal, natural gas-based process. The ore is turned into a pellet, lump, or briquetted form and transformed to steel in electric arc furnaces. CRS calculation based on American Iron and Steel Institute (AISI), 2017 Annual Statistical Report, June 28, 2018, p. 69; and Midrex, 2017 World Direct Reduction Statistics, May 24, 2018, p. 8. |

| 41. |

The United States depleted its high-quality red iron ore deposits in the 1950s. Thereafter, the mining industry developed new technologies that allowed for the processing of lower-quality ore into pellets. Pelletizing involves crushing iron ore, grinding it into a powder, rolling the powder into balls, and firing the balls in a furnace to produce marble-sized pellets that contain 60% to 70% iron. |

| 42. |

See U.S. Department of Transportation, "General Material Requirements: Buy America Requirements," 60 Federal Register 15478-15479, March 24, 1995, http://www.gpo.gov/fdsys/pkg/FR-1995-03-24/pdf/95-7362.pdf. |

| 43. |

In 2015, FHWA denied a waiver request from two major slab converters, California Steel Industries and NLMK. See letters from Walter C. Waidelich, Jr., Associate Administrator for Infrastructure, to Gary Lee Moore, Interim Executive Director, Port of Los Angeles, February 3, 2015, and to Robert Miller, President, NLMK USA, April 9, 2015. The letters are available to congressional clients from the report authors upon request. |

| 44. |

Steel slab converters include firms such as CSI, which produces a portion of its hot-rolled, cold-rolled, and galvanized sheet from domestic slab, but imports much more of its semi-finished feedstock from foreign suppliers. Because of this, a significant portion of CSI's California-finished steel is unusable in most federal projects. See CSI, California Steel Industries, Comments on Section 232 National Security Investigation of Imports of Steel Opposing Tariffs or Quotas on Slab Imports, May 31, 2017. |

| 45. |

Letter from Philip K. Bell, President, Steel Manufacturers Association, to Earl Comstock, Director, Office of Policy and Strategic Planning, U.S. Department of Commerce, April 7, 2017, http://steelnet.org/sma-comments-on-construction-of-pipelines-using-domestic-iron-and-steel/. |

| 46. |

P.L. 87-794; 19 U.S.C. §1862. |

| 47. |

Justin Ganderson, Frederic Levy, and Sandy Hoe et al., Key Takeaways From President Trump's "Buy American" Executive Order, Covington, Inside Government Contracts, April 2017, https://www.insidegovernmentcontracts.com/2017/04/key-takeaways-president-trumps-buy-american-executive-order/. |

| 48. |