Introduction

Congress over the years has passed several domestic content laws that aim to protect American manufacturing and manufacturing jobs. In 1978, Congress placed domestic content restrictions on federally funded transportation projects that are carried out by nonfederal government agencies such as state and local governments.1 These restrictions are commonly referred to as the Buy America Act, or more simply, Buy America; they differ from requirements under the Buy American Act of 1933, which applies to direct purchases by the federal government.2 Statements and actions by the Trump Administration about reinvigorating domestic manufacturing and reinvesting in infrastructure have stimulated renewed interest in Buy America.3

Today, Buy America refers to several similar statutes and regulations that apply to federal funds used to support projects in highways, public transportation, aviation, and intercity passenger rail, including Amtrak.4 Buy America also applies to certain federally funded water infrastructure projects. Unless a nationwide or project-specific waiver is granted, Buy America requires the use of U.S.-made iron and steel and the domestic production and assembly of other manufactured goods, such as rolling stock used in public transportation.5

To evaluate the implications of Buy America on domestic manufacturing, this report analyzes the effects of Buy America on steel and rolling stock manufacturing in the context of industry trends. It also briefly discusses the effects of Buy America on the transportation system. The report begins by explaining Buy America restrictions in more detail; how Buy America comports with international trade agreements that generally forbid procurement restrictions favoring domestic products; and how a relatively new provision enacted by Congress may require imports of materials on federally funded transportation projects to be carried on U.S.-flag ships. The report identifies policy options Congress might consider in light of recent legislative proposals.

Buy America Requirements

Buy America requirements differ in law and regulation according to the specific funding program and administering agency (see Table A-1). These agencies are the Federal Transit Administration (FTA), the Federal Highway Administration (FHWA), the Federal Railroad Administration (FRA), and the Federal Aviation Administration (FAA). Buy America also applies to purchases by Amtrak.6 In certain situations, the statutes permit a regulating agency to waive the Buy America provisions. If a state or local government does not use federal funds on a project, the project is not subject to Buy America (although states may have laws imposing similar requirements on state-funded purchases).7

Buy America provisions applicable to funds administered by FHWA, for example, are found at 23 U.S.C. §313 and 23 C.F.R. §635.410, and apply to iron and steel permanently incorporated into a highway project. This requirement can be waived if the Secretary of Transportation determines that it would be inconsistent with the public interest, that the materials are not produced in the United States in sufficient quantities or of a satisfactory quality, or that the inclusion of domestic materials will raise the cost of the overall project by more than 25%. FHWA determined in a 1983 rulemaking that Buy America would not apply to raw materials, such as iron ore, limestone, and waste products, all of which "may be imported."8 Waste products that may be used under this waiver include scrap steel. FHWA also waived the application of Buy America requirements to products other than those manufactured predominantly of iron and steel.9 In 2012, FHWA clarified that a manufactured product must consist of at least 90% iron and steel for it to be considered manufactured predominantly of iron and steel and, thus, subject to Buy America requirements.10 In 1995, FHWA determined that due to inadequate national supply, a national waiver would be granted for certain iron products used in the manufacture of steel or iron, including pig iron and iron ore that is reduced, processed, or pelletized.11

Even though FHWA waives Buy America requirements for manufactured products, except those made predominantly of iron and steel, this is not the case with other U.S. Department of Transportation (DOT) agencies and Amtrak. For example, for the purchase of rolling stock using FTA funds, the Buy America requirement is waived only if (1) the cost of the components produced in the United States in FY2017 is more than 60% of the cost of all components of the rolling stock (65% for FY2018 and FY2019, and 70% for FY2020 onward); and (2) final assembly of the rolling stock occurs in the United States (49 U.S.C. §5323(j) and 49 C.F.R. §661). Moreover, for a rolling stock component to be considered produced in the United States or of domestic origin, "more than 60% of the subcomponents of that component, by cost, must be of domestic origin, and the manufacture of the component must take place in the United States" (49 C.F.R. §661.11(g)).12 For nonrolling stock manufactured goods purchased using FTA funds, 100% of the components, including steel and iron, must be made in the United States and assembly must be done in the United States. According to 49 C.F.R. §661.5, "a component is considered of U.S. origin if it is manufactured in the United States, regardless of the origin of its subcomponents."

Buy America provisions restrict Amtrak's spending when the cost of articles, materials, or supplies bought is at least $1 million. The law requires Amtrak to purchase goods that are manufactured in the United States "substantially from articles, material, and supplies mined, produced, or manufactured in the United States."13 FRA has interpreted "substantially" to mean that the manufactured goods must have domestic component content greater than 50%, by cost.14

Trade Agreements and Domestic Preferences

The U.S. government builds few transportation projects directly. Instead, it generally funds highways, airports, and public transportation projects by making grants or loans to state or local governments. This funding structure has made it possible to avoid claims that Buy America violates international trade agreements.

The United States is a signatory to international agreements that restrict discrimination against trading partners in government procurement. Currently, 47 World Trade Organization (WTO) members, including the United States, have made binding commitments under the WTO Agreement on Government Procurement (GPA), whereby each provides the others access to its national procurement markets.15 Most U.S. bilateral and regional free trade agreements also include public procurement provisions. These agreements are generally based on "national treatment" and require the United States to treat goods, services, and suppliers of other signatories no less favorably than U.S. goods, services, and suppliers. As a consequence, firms based in countries covered by such agreements can bid on covered U.S. government procurement contracts over a certain dollar threshold. The thresholds are adjusted every two years.16 National treatment also means U.S. firms can bid on contracts in foreign procurement markets, giving American suppliers treatment no less favorable than domestic suppliers.

Although the United States is a WTO GPA signatory, state and local governments are excluded from coverage, even if federal funds are involved, unless they voluntarily agree to comply.17 Thus, where the federal government provides grants or loans to state and local authorities for transportation projects, it may attach domestic sourcing restrictions to these funds without violating international obligations.18

The exclusion of subnational procurement has caused considerable tension with major U.S. trading partners such as Canada and the European Union. In 2010, for example, the United States agreed to allow Canadian firms to bid on certain subnational economic stimulus contracts, including those involving construction of highways, bridges, and rail lines, in return for Canada's agreement to cover its provinces and territories under the WTO GPA.19

Cargo Preference

Cargo preference is another restriction applicable to federally supported activities, in this case requiring that a portion of "government-impelled" cargoes be carried on U.S.-flag vessels (46 U.S.C. §55305, 46 C.F.R. Part 381). Although cargo preference is not a Buy America requirement, a relatively new cargo preference provision may complicate transportation projects that are subject to Buy America. In 2008, Congress incorporated a provision in the FY2009 Duncan Hunter National Defense Authorization Act (NDAA; P.L. 110-417, §3511) specifying that cargo preference requirements also apply to cargo that is imported by an organization or person if the federal government "provides financing in any way with federal financial funds for the account of any persons unless otherwise exempted." At least 50% of such cargo must be shipped in U.S.-flag vessels. The law directs DOT to issue regulations and guidance to govern the administration of cargo preference by other federal agencies.20

The Maritime Administration (MARAD) within DOT has yet to clarify how the cargo preference requirements of the FY2009 NDAA will be implemented. The agency submitted a draft notice of proposed rulemaking for Office of Management and Budget approval in December 2011, but subsequently terminated the process after interagency coordination efforts failed. MARAD anticipates restarting the regulatory development process, but does not know when.21 FHWA has interpreted the law to apply cargo preference requirements to federally supported highway projects carried out by state departments of transportation and other agencies.22 MARAD has applied cargo preference requirements to vessel components imported for ships constructed with federal loan guarantees.23

Changes to Buy America in MAP-21 and FAST Act

There have been several changes to Buy America in the two most recent surface transportation reauthorization acts, the Moving Ahead for Progress in the 21st Century Act (MAP-21; P.L. 112-141), enacted in July 2012, and the Fixing America's Surface Transportation (FAST) Act (P.L. 114-94), enacted in December 2015. As part of MAP-21, Congress sought to prevent sponsors of highway projects from segmenting a project into smaller parts, some federally funded and some not, so as to free some segments of the project from Buy America requirements. To accomplish this, MAP-21 specified that FHWA Buy America requirements apply to all contracts eligible for assistance within the scope of a project's National Environmental Policy Act of 1969 (NEPA) document if at least one contract for the project is federally funded.

This provision addressed issues that arose during reconstruction of the San Francisco-Oakland Bay Bridge by the California Department of Transportation (CalTrans). After a major earthquake in 1989, California decided to reconstruct the Bay Bridge by refurbishing the western span and replacing the eastern span. CalTrans determined that it could obtain imported steel for the project more cheaply than domestic steel. To avoid Buy America requirements, it decided the eastern span would be built without federal funds. Subsequently, and controversially, the eastern span was built using steel made in China.24

Another effect of the provision prohibiting the segmenting of projects is that utility relocation work done as part of a federally funded highway project must now be Buy America-compliant even if the contract to do the utility work does not use federal funds.25 This change initially caused concern among state departments of transportation and industry associations that projects would be delayed as utilities sought to obtain Buy America-compliant products. In response, FHWA delayed implementation of the new requirements until January 1, 2014. The effects of compliance since then on highway projects, utilities, and manufacturers of products used by the utility industry are unknown.

MAP-21 also made changes aimed at making the FTA waiver determination process more transparent. MAP-21 requires FTA to publish each waiver request and a detailed explanation of the waiver determination in the Federal Register, and to make them easily accessible on its website. In addition, MAP-21 requires that FTA provide a report on waivers granted in the previous year to the Senate Banking Committee and the House Transportation and Infrastructure Committee.

The FAST Act increased the threshold for public transportation rolling stock to 65% for FY2018 and FY2019 and to 70% for FY2020 onward. However, it eliminated Buy America requirements for public transportation projects costing less than $150,000, up from the previous threshold of $100,000. In the event of a waiver denial, the FAST Act also requires FTA to provide a certification that the items can be purchased in the United States in sufficient quantity and quality, along with a list of manufacturers. This information must be published on the DOT website.26

Presidential Statements and Actions

The Trump Administration has announced that it will pursue efforts to protect domestic industries as part of its "Buy American and Hire American" initiative. To date, this includes two actions with respect to Buy America. First, an executive memorandum requires the Secretary of Commerce to develop a plan to have all new pipelines in the United States "use materials and equipment produced in the United States, to the maximum extent possible and to the extent permitted by law."27 According to the memorandum, steel made in the United States from imported scrap or imported slabs is not to be considered produced in the United States. Second, a separate executive order directs that "every agency shall scrupulously monitor, enforce, and comply with Buy American Laws, to the extent they apply, and minimize the use of waivers, consistent with applicable law."28 The term "Buy American Laws" is defined in the executive order to include Buy America.

Buy America and U.S. Steel Manufacturing

Unless the requirements are waived by the federal agency concerned, Buy America provisions require the use of U.S.-made steel in a wide variety of applications.

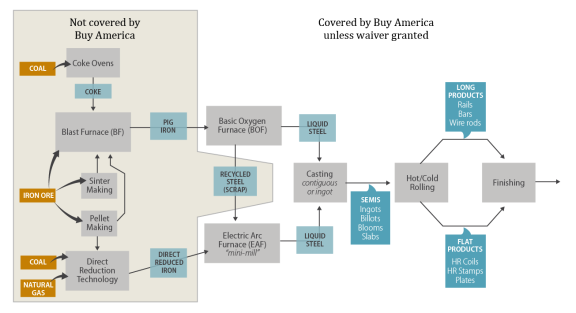

U.S. mills produce steel in three distinct ways. Approximately 62% of domestic production comes from plants known as minimills, which use electric arc furnaces to melt scrap steel and in some cases iron pellets. Another 37% is made in traditional integrated steel mills, which use ovens to turn coal into coke and then combine the coke with iron ore to produce pig iron in blast furnaces. The pig iron is then melted in a basic oxygen furnace to produce steel. A very small portion of U.S. production, approximately 1%, involves direct reduction technology, now used in a single U.S. mill.29

The raw materials used to produce steel in the United States largely come from domestic sources. Around 90% of the scrap used by minimills is obtained domestically, although the products from which scrap is commonly derived, such as vehicle bodies and beams used in construction, may originally have been imported. Integrated steel mills mostly use iron ore from Minnesota's Mesabi Iron Range and Michigan's Iron Range, which account for more than 90% of America's iron ore supply. U.S.-mined iron ore takes the form of taconite, a relatively low-grade source of iron-bearing rock typically containing 15% to 30% magnetic iron particles. To be useful in steelmaking, the taconite is formed into pellets before delivery to a steel mill.30

Figure 1 provides a graphic depiction of the iron and steel manufacturing process. Originally, Buy America covered raw materials used in steel manufacturing. A lack of adequate domestic supply resulted in a 1995 nationwide waiver for raw materials (iron ore and limestone), scrap (recycled steel scrap), pig iron, and processed, pelletized, and reduced iron ore.31 Because of the waiver, U.S. steel mills may use imported inputs to make Buy America-compliant steel products. Therefore, the part of steel production shown in the shaded section of Figure 1 is currently not subject to Buy America requirements. It is not clear how these requirements might be altered through the regulatory process, if at all, in response to President Trump's "Buy American and Hire American" executive order.

|

|

Source: Figure adapted by CRS from Eurofer, Study on the Competitiveness of the European Steel Sector, August 2008, p. 10. |

After the steel is produced, it is cast into variety of shapes and left to cool. Ingots, which vary in size, are often rolled further to produce rectangular steel slabs. Companies known as slab converters have sought a nonavailability waiver for products manufactured in the United States from imported steel slabs.32 Slab converters claim there is insufficient supply of domestically made steel slabs available from U.S. integrated steel mills.33 In addition, they claim that the original Buy America requirements were issued before slab converters even existed, and the requirement unfairly prevents them from participating in federal-aid highway projects. To date, FHWA has denied a waiver to slab converters, a position supported by steel industry trade groups such as the Steel Manufacturers Association, which considers a waiver on steel slabs to be a weakening of Buy America rules.34 This waiver seems unlikely to be issued in light of President Trump's recent order directing agencies to minimize the use of waivers.35

Economic Effects

Assessing the economic effects of Buy America on the steel industry is difficult due to the lack of relevant data.36 It is unclear how much iron and steel are used in transportation projects that have federal funding; hence data are not available to calculate how much steel is produced and sold domestically as a direct result of Buy America. Nevertheless, the available data suggest that the steel produced for the Buy America market represents a small portion of total domestic demand for steel.

Industry sources estimate that net shipments of steel mill products in the United States totaled 86.5 million tons in 2015. Of these shipments, roughly 20 million tons, or about a quarter, were consumed in public and private construction projects.37 This quarter, however, includes steel used in a range of nontransportation projects, such as office buildings, shopping centers, and apartment towers, as well as in transportation projects that are not publicly funded, such as those in the freight rail industry. Steel used in rail transportation projects of all types, including those undertaken by freight railroads as well passenger cars and locomotives for Amtrak and commuter services, amounted to 1.7 million tons in 2015. This represented 1.6% of U.S. steel production last year.38

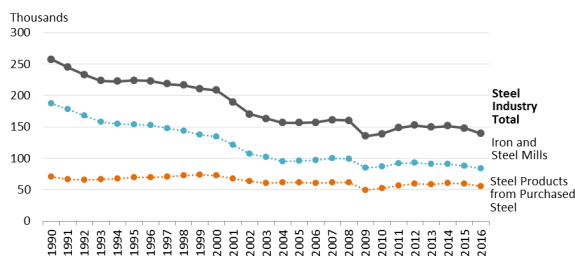

A key rationale for Buy America is its positive effect on steel industry employment. Direct employment in steel has declined from almost 260,000 jobs in 1990 to around 140,000 jobs in 2016 (Figure 2), due largely to higher productivity. According to the American Iron and Steel Institute, the number of labor hours needed to produce one finished ton of steel has fallen 81% since 1980, from 10.1 to 1.9.39 If broader Buy America requirements were to increase annual demand for U.S.-made steel by 1 million tons (about 1%), and if each ton were to require 1.9 hours of labor, steel-industry employment would be expected to rise by approximately 1,000 jobs (assuming a 1,900-hour work year). A similar estimate can be derived from data in a December 2013 report by the Steel Manufacturers Association, which represents North American minimills, indicating that an increase of 1 million tons of domestic steel production would create 792 new steel manufacturing jobs.40 Presumably, these jobs would pay well, as steel mill workers earned an average annual wage of $78,965 in 2015, significantly above the average of $64,305 for all manufacturing.41

|

|

Source: CRS analysis of Bureau of Labor Statistics, Current Employment Statistics, for iron and steel mills (NAICS 3311) and steel products from purchased steel (NAICS 3312). |

Buy America and U.S. Rolling Stock Manufacturing

Besides its restriction on the sourcing of iron and steel, Buy America also places limits on state and local governments and Amtrak when using federal funds to purchase manufactured goods. One of the main manufactured products this affects is rolling stock, which includes intercity passenger rail trains, public transportation rail cars and buses, and associated equipment.42 Under Buy America domestic sourcing requirements, as noted earlier, rolling stock final assembly must take place in the United States. Moreover, significant proportions of the systems and components used to assemble rail vehicles and buses must be manufactured in the United States, although this can differ depending on the agency source of the federal funds.

According to one industry estimate, the U.S. domestic market for railroad rolling stock totaled $19 billion in 2016.43 Federal data indicate that manufacturers of all types of railroad rolling stock directly employed 30,100 workers in 2015, accounting for 0.2% of total factory employment. These data, however, cover the production of equipment that is not publicly funded and thus not subject to Buy America, such as freight locomotives and freight rail cars.44 According to one industry estimate, the size of the U.S. market for new street, subway, and transit cars, which would represent only a portion of the Buy America public transportation market, was at least $2.6 billion in 2017.45

Although a few domestic firms have tried to carve out niches in the transit market, foreign-based manufacturers build essentially all intercity passenger rail cars and rail transit vehicles produced in the United States. Buy America has required them to establish assembly plants in the United States rather than import finished vehicles. Often, the plant location is selected in conjunction with negotiations to supply vehicles to a local transit agency. In September 2015, for example, the China Railway Rolling Stock Corporation (CRRC), a unit of the Chinese state railways, began building a $95 million assembly plant in Springfield, MA, shortly after receiving a contract to provide 284 subway cars for the Massachusetts Bay Transportation Authority.46 CRRC intends to hire at least 150 factory workers for the plant, and full production is slated to begin sometime in 2018.47

Such plants typically lack private customers. Their dependence on demand for passenger rail and transit vehicles acquired with the help of federal grants means that they are comparatively small, and may lack economies of scale that could help reduce unit costs. Their cost structures and the varying requirements for transit and passenger rail vehicles in other countries may make it difficult for U.S. plants to export. By one estimate, 89% of global demand for passenger rail rolling stock in the 2017-2019 period will be outside North America.48

Assemblers of transit vehicles depend on an extensive global supply chain that includes steel and aluminum producers and component suppliers that make thousands of parts and accessories such as transmissions, axles, steering systems, and engines. An estimate by First Research, a private research firm, says purchased steel and components represent 50% of rolling stock manufacturing costs.49 In 2010, the Duke University Center on Globalization, Governance & Competitiveness identified about 150 subcontractor firms in the United States that sold components to passenger and transit rail vehicle manufacturers.50

Some argue more public-sector investment in public transportation systems is needed to significantly bolster the passenger rail car manufacturing industry in the United States.51 Over the last decade, annual domestic demand for new passenger rail cars has fluctuated from a low of 497 units in 2011 to a high of 1,141 in 2009 (see Table 1).52 Since 2006, domestic manufacturers have shipped 8,970 new passenger cars to Amtrak and transit agency purchasers. This figure includes regional, intercity, rapid transit, and light rail cars as well as streetcar units. There were reports of a backlog of more than 3,700 vehicles at the end of 2016, including 59 intercity cars for Amtrak to be manufactured by CAF USA, 765 commuter cars to be manufactured by Bombardier for the Bay Area Rapid Transit (BART) system in California, and 590 rapid transit cars to be built by Kawasaki for the Washington Metropolitan Area Transit Authority (WMATA).53 It is unclear how much of this manufacturing would occur in the United States in the absence of Buy America.

In the context of current Buy America restrictions, and based on one recent estimate, the outlook through 2022 is for more than 5,000 new passenger rail cars, including intercity, commuter rail, and transit cars.54 An unknown for the entire industry is the level of future federal assistance to vehicle purchasers. If federal funding declines, many transit operators will, in all probability, reduce their demand for new vehicles and opt where possible to rebuild their current fleets for extended service. Alternatively, if federal funding increases, demand for new domestically produced passenger rail cars will likely grow.

|

Year |

Regional/Intercity |

Rapid Transit |

Light Rail/Street Car/ |

Total |

|

2006 |

358 |

250 |

130 |

738 |

|

2007 |

139 |

402 |

121 |

662 |

|

2008 |

227 |

272 |

97 |

596 |

|

2009 |

187 |

752 |

202 |

1,141 |

|

2010 |

199 |

782 |

148 |

1,129 |

|

2011 |

235 |

113 |

149 |

497 |

|

2012 |

343 |

243 |

59 |

645 |

|

2013 |

531 |

337 |

166 |

1,034 |

|

2014 |

251 |

484 |

116 |

851 |

|

2015 |

251 |

462 |

258 |

971 |

|

2016 |

94 |

424 |

188 |

706 |

|

Total |

2,815 |

4,521 |

1,634 |

8,970 |

Source: 2016 Passenger Rail Car Market, Railway Age, pp. 46-47, January 2017.

Despite Buy America rules that require more than 60% of the value of the subcomponents of transit vehicles and equipment to be produced in the United States and the final assembly to occur in the United States, domestic transit bus manufacturing has remained over many decades a small and concentrated manufacturing sector. In 2016, bus manufacturing revenue was estimated at $5.1 billion, including school buses and intercity buses along with public transit buses.55 According to the American Public Transportation Association (APTA), bus manufacturers in a typical year produce somewhere between 4,000 to 6,000 buses for the public transit market.56 Transit bus manufacturers directly employ around 5,000 workers, although there are likely several thousand more jobs in the broader bus manufacturing supply chain.57 Like other vehicles, transit buses are mostly made of steel.58

New Flyer, a Canadian company, and Gillig, a U.S.-headquartered manufacturer, account for 75% of the North America heavy-duty transit bus market.59 New Flyer makes fewer than 1,000 transit buses annually in Minnesota and Alabama.60 Gillig makes between 1,100 and 1,600 transit buses a year in California.61 Nova, a subsidiary of the Swedish firm Volvo Group, holds most of the remaining share of the North America market. Nova's bus plant in Plattsburgh, NY, manufactures 40-foot buses and 62-foot articulated buses.62 Orion, part of Daimler Buses North America, stopped assembling buses in the United States in 2013, citing "low public sector investments by municipal government agencies" as a reason,63 and New Flyer acquired North American Bus Industries (NABI) the same year.64 BYD, a Chinese company, is an example of a new entrant into the U.S. transit bus market. It currently manufactures around 200 electric buses at its factory in California, but plans to ramp up its U.S. production to 1,000 each year.65

Effects of Buy America on Transportation

Buy America is primarily an industrial policy designed to protect U.S. manufacturing and manufacturing employment. However, Buy America could increase the cost and completion time of at least some transportation projects, and may result in fewer projects being undertaken. Evidence of these effects, however, is largely anecdotal. In a review of the costs and benefits of various federal requirements on highway projects, the Government Accountability Office (GAO) found that several studies discussed regulatory costs and benefits, but "none of the studies we reviewed separately estimated the costs of the Buy America program's requirements."66 Highway projects most affected by Buy America are bridges because of the amount of iron and steel required. Transit projects most affected by Buy America are rail rolling stock and bus procurement.

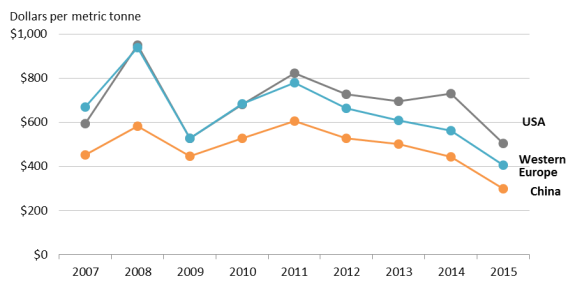

Buy America rules prohibit customers from buying less expensive steel from overseas suppliers for use in public works projects. A project sponsor, however, can apply for a waiver if inclusion of domestically produced iron, steel, or manufactured goods would increase the overall cost of the project by more than 25%. The price of steel produced in the United States tends to be higher than that of comparable steel produced in other countries.67 For example, the benchmark average U.S. hot-rolled band price in recent years has consistently been higher than the Chinese price and, in most years, has been higher than the Western European price (Figure 3). However, higher transportation costs for imported steel may reduce or eliminate its cost advantage at a particular project site.

In 2015, for example, the average price of domestic hot-rolled band was about $200 per metric ton higher than the price of the same product made in China. Industry estimates suggest that freight, insurance, and handling from Asia to ports on the Pacific and Gulf coasts would have added about $60 per metric ton to the import price, leaving a Chinese cost advantage of $140 per ton at dockside.68 The differential with respect to a particular project would also depend on the costs of moving steel from a domestic mill or a port to the job site. Both steel costs and freight transportation costs can vary significantly over time due to global steel demand, energy prices, exchange rates, and other factors.

Buy America may also raise the cost of rolling stock procurements. One analysis of bus procurement in public transportation notes that buses in the United States are about twice the price of those in Japan and South Korea. This study also makes the case that bus purchasers are limited in their choice of buses, and that the protected industry is less innovative. They conclude that if public transit agencies could import buses, "they would have access to a greater menu of differentiated products at lower prices. This would lead to a higher quality of service provision (e.g., better service frequency and coverage) which could induce urbanites to substitute from private vehicles to buses."69 Other direct costs associated with Buy America are mainly related to administering and enforcing its requirements, costs that are mostly absorbed by state and local government project sponsors. These costs include the effort required by contractors to document the national origin of iron, steel, and manufactured products and agency administration of the certification process. Extra work may also be required of contractors to put together two bids for a given project, one incorporating domestic products and one with foreign products. Waiver requests, another cost, may be prepared by the state or local government project sponsor alone or in cooperation with the contractor.70

Buy America may make it more time-consuming to complete transportation projects, ultimately causing higher project costs. Delays can arise from domestic supply problems and the waiver application process. Extending Buy America requirements to utility relocations, for example, led to concerns about project delivery among state departments of transportation, although this effect may wane as utilities become accustomed to working with the Buy America requirements.71 The private developer of a proposed high-speed rail line from the outskirts of Los Angeles (Victorville) to Las Vegas, XpressWest, blamed Buy America compliance for blocking its plans. The company sought low-cost financing through the federal Railroad Rehabilitation and Improvement Financing (RRIF) program, subjecting it to Buy America. Although there have been other issues with the project, the Secretary of Transportation suspended consideration of the loan request because the sponsors were having difficulties satisfying the Buy America requirements.72 More generally, in a survey of people in the public transportation industry in the mid-1990s, Buy America was mentioned by respondents as the cause of project delay more often than any other reason.73

The FY2009 Duncan Hunter National Defense Authorization Act (NDAA; P.L. 110-417, §3511) established cargo preference requirements for imported materials purchased by state and local governments and private organizations with federal financial assistance. The requirements have the potential to raise costs of transportation projects and contribute further to delays. Shipping rates for cargo aboard U.S.-flag vessels tend to be higher than those for similar cargo on foreign-flag vessels, and services are less frequent, as the number of U.S.-flag commercial vessels providing international service is much smaller than the number of foreign-flag vessels serving the United States.74 On balance, imported materials purchased under Buy America waivers will generally be less attractive to project sponsors if the imported products are subject to cargo preference.

Although Buy America may increase the cost and completion time of transportation projects, its effects may be less important overall than other federal requirements. In its 2008 study of highway projects, GAO found that Buy America was mentioned much less often by state department of transportation officials than environmental requirements when asked about decisions to undertake projects without federal funds. Of 39 states that indicated they had decided not to use federal funds to avoid federal requirements in the last 10 years, 33 mentioned environmental requirements and 5 mentioned Buy America.75

Policy Options for Congress

One option for Congress is to leave the Buy America requirements unchanged. Supporters of the status quo could argue Buy America requirements do an effective job of supporting some domestic manufacturing employment and encouraging some foreign manufacturers to establish factories in the United States. It could also be argued that the content requirements are adequate, and that the administrative waivers process provides enough flexibility to accommodate changing technologies and market conditions. Changes to the law, moreover, might introduce uncertainty and delay in project delivery.76

Policy options for changing Buy America broadly conceived are

- tightening Buy America restrictions,

- loosening Buy America restrictions,

- standardizing Buy America restrictions, and

- broadening Buy America restrictions to other parts of the transportation system or to nontransportation sectors.

Tightening Buy America Restrictions

Congress could modify Buy America by making it more restrictive.

The FAST Act, enacted in December 2015, did this by increasing the share of public transit rolling stock components and subcomponents that must be produced in the United States. Other bills, such as the Invest in American Jobs Act of 2015 (S. 1043, 114th Congress), introduced by Senators Merkley and Baldwin, have proposed increasing the share to 100%.

More technical changes to tighten Buy America are contained in the Buy American Improvement Act of 2017 (H.R. 904), introduced by Representative Lipinski. This bill proposes to subject rolling stock purchased using highway funds administered by FHWA to the same Buy America requirements as those purchased with funds administered by FTA. It would also require FHWA to reevaluate its regulations for manufactured products other than those made of iron and steel. Moreover, it would require FTA to develop audit requirements and best practices for documenting compliance with Buy America, and includes initiating a new rule for standards by which to measure the percentage value of a component relative to the entire procurement. The bill would require Amtrak to contract with the National Institute of Standards and Technology (NIST) to search for domestic suppliers of products before seeking a waiver.77 FAA would be required to do a similar search for domestic suppliers. The bill also would apply Buy America requirements to projects financed with local passenger facility charges, federally authorized fees collected from airline passengers by certain airport operators.

Loosening Buy America Restrictions

There are no legislative proposals in the 115th Congress to loosen Buy America requirements substantially. Two provisions in the 114th Congress proposed to make Buy America somewhat less restrictive. The FAST Act included one of these provisions, raising the threshold for purchases in public transportation subject to Buy America requirements from $100,000 to $150,000. However, it did not include another proposal to raise the threshold for Amtrak purchases subject to Buy America from $1 million to $5 million.78

Standardizing Buy America Restrictions

Standardizing the Buy America requirements with respect to rolling stock purchases and possibly having a single office within DOT to enforce them might simplify enforcement, particularly with respect to rolling stock purchases by public transportation providers and Amtrak. There has been no recent legislation on this issue.79

Broadening Buy America Restrictions

There are proposals to expand Buy America to other parts of the transportation system and to other sectors such as clean energy manufacturing. The American Pipeline Jobs and Safety Act of 2017 (H.R. 683), for example, introduced by Representative Nolan, proposes to extend Buy America requirements to gas and hazardous liquid pipelines regulated by DOT's Pipeline and Hazardous Materials Safety Administration. Currently, Buy America does not apply to these pipelines because they are privately built and operated. H.R. 683 would require, as a new safety standard, that the construction or replacement of regulated pipelines use only steel produced in the United States from iron ore and taconite mined and processed in the United States. Steel made from scrap in the United States would comply with the provision if "the recycled materials are combined with iron ore and taconite mined and processed in the United States."80

Another proposal to broaden Buy America was the Make It in America: Create Clean Energy Manufacturing Jobs in America Act (H.R. 1524, 113th Congress). This bill proposed requiring clean-energy goods and equipment purchased by states with federal funding, such as wind turbines and solar panels, to meet an 85% American-made content threshold. H.R. 1524 would also have required 85% U.S. content of purchases for which private companies claim the Renewable Energy Investment Tax Credit and the Renewable Energy Production Tax Credit.

The Water Resources Reform and Development Act of 2014 (P.L. 113-121) amended the Clean Water Act to add Buy America requirements to projects receiving assistance from state revolving funds (33 U.S.C. §1381 et seq.). Buy America requirements were included in the Water Infrastructure Improvements for the Nation Act (WIIN; P.L. 114-322) for funds made available in FY2017 from a state revolving fund under the Safe Drinking Water Act (42 U.S.C. §§300f-300j). Several bills have been introduced in the 115th Congress to make this Buy America provision permanent (e.g., H.R. 939, H.R. 1068, H.R. 1071). Buy America provisions have also been included in annual appropriations acts for grants to capitalize state revolving funds under the Clean Water Act and the Safe Drinking Water Act. The American Recovery and Reinvestment Act of 2009 (P.L. 111-5) generally imposed Buy American requirements on federally funded projects, and the Consolidated Appropriations Act, 2014 (P.L. 113-76) included specific Buy America requirements for clean water and drinking water projects funded by the act.81

Another bill in the 115th Congress, S. 181, introduced by Senator Brown, would seek to apply Buy America to federal infrastructure-related programs where there are currently no such requirements. It would also broaden Buy America requirements to include other construction materials such as nonferrous metals, plastic pipes, concrete, glass, lumber, and insulation.

Appendix. DOT Buy America Requirements

|

Agency |

Domestic Content |

Price Threshold |

Potentially Affected Industries |

Waivers |

|

Federal Transit Administration (FTA): |

100% U.S.-made requirement for iron, steel, and manufactured goods. Buy America does not apply to rolling stock if more than 60% of components, by value, are produced domestically and final assembly is in the United States. Threshold rises to 65% for FY2018 and FY2019 and 70% for FY2020 onward. |

Above $150,000 |

Iron and steel producers; |

1. Inconsistent with the public interest, which can include a wide range of impacts on domestic markets or firms, or on project outcomes |

|

Federal Highway Administration (FHWA): |

100% U.S.-made requirement for iron, steel, and manufactured goods made predominantly of steel and iron |

Above $2,500 or 0.1% of the contract price, whichever is greater |

Steel manufacturers; |

1. Inconsistent with the public interest |

|

Federal Railroad Administration (FRA): |

100% U.S.-made requirement for iron, steel, and manufactured goods |

Above $100,000 |

Steel manufacturers; |

1. Inconsistent with the public interest |

|

Amtrak (National Railroad Passenger Corporation): |

All manufactured and unmanufactured goods must be substantially domestic; |

$1 million and above |

Steel manufacturers; |

1. Inconsistent with the public interest |

|

Federal Aviation Administration (FAA): |

All steel and manufactured goods must be produced in the United States. Preference does not apply if more than 60%, by value, of all components and subcomponents of the facility or equipment are produced domestically and final assembly is in the United States. |

Unspecified; |

Companies offering products or materials for airport construction |

1. Inconsistent with the public interest |

Source: CRS, adapted from U.S. Department of Transportation, Buy America Provisions—Side-by-Side, http://www.transportation.gov/buy-america-provisions-side-side-comparison.