Introduction

Individuals and households that suffer uninsured or underinsured losses under a major disaster declaration typically apply for Individual Assistance (IA), administered by the Federal Emergency Management Agency (FEMA), and may also apply for disaster loans, administered by the Small Business Administration (SBA).1 This report opens with an overview of the two programs and a discussion about how declarations are used to put them into effect. The report also discusses their respective application processes and eligibility criteria used by FEMA and SBA to make grant and loan determinations, respectively. The report then describes the appeals process before concluding with policy observations and considerations.

FEMA IA and the SBA Disaster Loan Program are interlaced to a certain degree. Functionally, SBA and FEMA have a computer matching agreement (CMA) to share real-time data on assistance provided to applicants. SBA and FEMA use the interface between their systems to identify potential duplication of benefits (DOB) and determine loan and grant eligibility. From an administrative perspective, eligibility and assistance from one source can impact eligibility and assistance from the other source.

While the overlap between the two programs may have some benefits, it arguably also causes some confusion. Moreover, as some observers have pointed out, there are elements of the application process that are not entirely known or understood. For instance, Members have asked for clarification concerning the criteria used to determine eligibility for grants and/or loans, as well as how decisions are made with respect to whether an applicant is provided a grant, loan, or both. Others have questioned whether determinations are made on a case-by-case basis, or if the determination criteria are applied uniformly to all applicants seeking disaster assistance.

Overview of Programs

The following sections provide descriptions of the SBA and FEMA programs that provide assistance to individuals and households. In many cases, disaster survivors find that they need assistance from both of these programs in addition to other sources of assistance including private insurance, state and local government assistance, and assistance from private voluntary organizations in order to fully recover.

SBA Home Disaster Loans

In addition to small business disaster loans, homeowners, renters, and personal property owners located in a declared disaster area are also eligible to apply for an SBA home disaster loan. SBA home disaster loans can be conceptualized as two categories of loans according to how the proceeds are put to use: Personal Property Loans and Real Property Loans.

Personal Property Loans

A Personal Property Loan provides a creditworthy homeowner or renter located in a declared disaster area with up to $40,000 to repair or replace personal property owned by the victim.2 Eligible items include furniture, appliances, clothing, and automobiles damaged or lost in a disaster. These loans cover only uninsured or underinsured property and primary residences in a declared disaster area. Eligibility of luxury items with functional use, such as antiques and rare artwork, is limited to the cost of an ordinary item meeting the same functional purpose. Interest rates for Personal Property Loans cannot exceed 8% per annum, or 4% per annum if the applicant is found by SBA to be unable to obtain credit elsewhere. Generally, borrowers pay equal monthly installments of principal and interest, beginning five months from the date of the loan. Loan maturities may be up to 30 years.

Real Property Loans

Real Property Loans provide creditworthy homeowners with uninsured or underinsured loss located in a declared disaster area with up to $200,000 to repair or replace the homeowner's primary residence to its pre-disaster condition.3 The loans may not be used to upgrade a home or build additions to the home, unless the upgrade or addition is required by city or county building codes such as a code-required elevation. Repair or replacement of landscaping and/or recreational facilities cannot exceed $5,000. A homeowner may borrow funds to cover the cost of improvements to protect their property against future damage (e.g., elevation, retaining walls, sump pumps, etc.). Mitigation funds may not exceed 20% of the disaster damage, as verified by SBA, to a maximum of $200,000 for home loans.4 As previously mentioned, interest rates cannot exceed 8% per annum, or 4% per annum if the applicant is unable to obtain credit elsewhere. Generally, borrowers pay equal monthly installments of principal and interest, beginning five months from the date of the loan. Loan maturities may be up to 30 years.

FEMA Individual Assistance

IA can include several programs, depending on whether the governor of the affected state or the tribal leader requests that specific type of FEMA assistance. FEMA's IA includes (1) Mass Care and Emergency Assistance, (2) the Crisis Counseling Assistance and Training Program, (3) Disaster Unemployment Assistance, (4) Disaster Legal Services, (5) Disaster Case Management, and (6) the Individuals and Households Program.5

Mass Care and Emergency Assistance

Mass Care includes directly supporting sheltering, feeding, emergency supply distribution, and family reunification. Emergency Assistance includes a variety of services and functions, including coordination of volunteer organizations and unsolicited donations, managing unaffiliated volunteers and community relief services, supporting transitional sheltering, and supporting mass evacuations.

Crisis Counseling Assistance and Training Program

The Crisis Counseling Assistance and Training Program assists individuals and communities recovering from the effects of a disaster through community-based outreach and psycho-educational services.6 The program supports short-term counseling of disaster survivors. The program also provides information on coping strategies and emotional support by linking the survivor with other individuals and agencies that help survivors in the recovery process.

Disaster Unemployment Assistance

Disaster Unemployment Assistance provides information and resources to individuals who were employed or self-employed, or were scheduled to begin employment during a disaster. It may also be provided to those who can no longer work or perform their job duties due to damage to their place of employment, who do not qualify for regular unemployment benefits from a state, or who cannot perform work or self-employment due to an injury as direct result of a disaster.7

Disaster Legal Services

Disaster Legal Services provides legal assistance to low-income individuals who are unable to secure adequate legal services that meet their disaster-related needs.

Disaster Case Management

Disaster Case Management provides a partnership between a case manager and the disaster survivor to assist them in carrying out a disaster recovery plan. The recovery plan includes resources, service, decision-making priorities, progress reports, and the goals needed to close their case.

Individuals and Households Program (IHP)

The Individuals and Households Program (IHP) is comprised of two categories of assistance: Housing Assistance, and Other Needs Assistance. Housing Assistance may include financial assistance to:

- Reimburse for hotels, motels, or other short-term lodging.

- Rent alternate housing accommodations while the applicant is displaced from their primary residence.

- Make repairs to primary residence.

- Assist in replacing owner-occupied residences when the residence is destroyed.

- Enter into lease agreements with owners of multifamily rental properties located in the disaster area.

Housing Assistance may also include home repair and construction services provided in insular areas outside the continental United States and other locations where no alternative housing resources are available and where types of FEMA housing assistance that are normally provided (such as rental assistance) are unavailable, infeasible, or not cost-effective. In addition, FEMA may provide manufactured housing units as a form of temporary housing through its Transitional Sheltering Assistance program.

The Robert T. Stafford Disaster Relief and Emergency Assistance Act (P.L. 93-288, as amended, hereinafter the Stafford Act) originally capped IA financial assistance at "no greater than $25,000 under this section with respect to a single major disaster."8 The Stafford Act was later amended to adjust the cap annually to reflect changes in the Consumer Price Index published by the Department of Labor.9 The current IA cap is $33,300 and the approximate per household or individual award amount is $8,500.10 Households that have damages exceeding $33,300 may also need an SBA disaster loan to rebuild and repair their home.

Other Needs Assistance (ONA) provides financial assistance for other disaster-related expenses and needs. ONA is divided into two categories: (1) SBA dependent, and (2) non-SBA dependent.

SBA Dependent ONA

Only individuals or households who do not qualify for a loan from the SBA may be eligible for the following types of assistance:

- Personal Property Assistance: to repair or replace essential household items such as furnishings and appliances, accessibility items (as defined by the Americans with Disabilities Act), and specialized tools and protective clothing required by an employer.

- Transportation Assistance: to repair or replace a vehicle damaged by a disaster and other transportation-related costs.

- Moving and Storage Assistance: to relocate and store personal property from the damaged primary residence to prevent further disaster damage, such as ongoing repairs, and returning the property to the primary residence.

Non-SBA Dependent ONA

Non-SBA dependent types of ONA may be awarded regardless of the individual's or household's SBA disaster loan status and may include:

- Funeral Assistance: to assist with funeral expenses incurred as a direct result of a declared major disaster such as reallocation or reburial of unearthed remains and replacement of burial vessel and markers.

- Medical and Dental Assistance: to assist with medical or dental expenses caused by a major disaster, which may include injury, illness, loss of prescribed medication and equipment, or insurance copayments.

- Child Care Assistance: a one-time payment that covers up to eight cumulative weeks of child care expenses, for a household's increased financial burden to care for children aged 13 and under, or children aged 14 to 18 with a disability as defined by federal law.

- Miscellaneous or Other Items Assistance: reimbursement for eligible items purchased or rented after a major disaster incident for an individual or household's recovery, such as gaining access to the property or assisting with cleaning efforts.11

Stafford Act, SBA Disaster Declarations, and Designations

Two declaration authorities put FEMA IA and the SBA Disaster Loan Program into effect: (1) the Stafford Act, and (2) the Small Business Act (P.L. 85-536, as amended).

Stafford Act Declarations

The Stafford Act authorizes the President to issue major disaster declarations that provide states, tribes, and localities with a range of federal assistance in response to natural and human-caused incidents.12 Each presidential major disaster declaration includes a "designation" listing the counties eligible for assistance as well as the types of assistance FEMA is to provide under the declaration. Potential types of assistance include (1) Public Assistance (PA) for infrastructure repair;13 (2) Hazard Mitigation Grant Program (HMGP) grants to lessen the effects of future disaster incidents; and (3) Individual Assistance (IA) for aid to individuals and households. Under FEMA regulations:

The Assistant Administrator for the Disaster Assistance Directorate has been delegated authority to determine and designate the types of assistance to be made available. The initial designations will usually be announced in the declaration. Determinations by the Assistant Administrator for the Disaster Assistance Directorate of the types and extent of FEMA disaster assistance to be provided are based upon findings whether the damage involved and its effects are of such severity and magnitude as to be beyond the response capabilities of the state, the affected local governments, and other potential recipients of supplementary federal assistance. The Assistant Administrator for the Disaster Assistance Directorate may authorize all, or only particular types of, supplementary federal assistance requested by the governor.14

Not all major disaster declarations provide IA. Often major declarations only provide PA and HMGP (these are sometimes referred to as "PA-only" major disaster declarations).

Stafford Act disaster declarations also trigger the SBA Disaster Loan Program. The assistance designation, however, determines what loan types become available. In particular, the IA designation is important because it determines whether disaster loans will be made available to individuals and households. For example, if the President declares a major disaster and designates IA for a county, then all SBA disaster loan types become available to that county.15 On the other hand, if the President issues a PA-only major declaration, SBA disaster loans are generally only available to private nonprofit organizations. In many cases a major disaster is declared for an incident that designates IA for some counties, and designates PA for others. Only the IA-designated counties in that major disaster will be eligible for SBA home disaster loans.

SBA Disaster Declarations

A major disaster declaration, however, is not the only triggering mechanism for the SBA Disaster Loan Program. The Small Business Act authorizes the SBA Administrator to issue an "Agency" or "SBA declaration" that makes disaster loans available for homeowners, renters, businesses, and nonprofit organizations.16 The SBA declaration does not, however, trigger FEMA IA.17

Applications for Assistance

Applying for FEMA Individual Assistance

After a major disaster declaration has been issued and IA has been designated for the incident, applicants in a declared disaster area may register for FEMA and SBA assistance. Individuals and households can register for assistance online or by telephone.18 Individuals and households generally have 60 days from the date of a declaration to apply for IA.19 The registration process typically takes 20 minutes to complete and requires the following information:

- The applicant's social security number (or the social security number of a minor child in the household who is a U.S. Citizen, Non-Citizen National, or Qualified Alien if the parent or legal guardian is not a legal citizen).

- Financial information (gross household income at the time of the disaster).

- Contract information, insurance information.

- Electronic funds transfer or direct deposit information (to receive eligible assistance).

Applying for an SBA Disaster Loan

Applicants can apply for SBA disaster loans online, in-person at a disaster center, or by mail.20 Applicants must fill out SBA Form 5C and IRS Form 4506-T. The forms require certain information about the applicant including their social security number, income, insurance, assets, debt amounts, and tax information. The applicant may also be required to indicate whether their employment has changed in the last two years, as well as provide deed and proof of residency information. If the applicant is claiming damage to an automobile, they may be required to provide proof of ownership (a copy of the registration, title, bill of sale, etc.).21

Applicant Eligibility Criteria and Screening

Though integrated to a large extent, ultimately each agency is responsible for determining eligibility based on the applicant's losses and the forms of assistance they have received. In the case of SBA disaster loans, the SBA's Office of Disaster Assistance (ODA) determines eligibility based on the applicant's disaster-related losses, as verified by SBA.22 IA eligibility determinations are made by FEMA's Individual Assistance Division, under the Office of Response and Recovery.

The SBA Disaster Loan Program uses three main criteria for making credit decisions: (1) eligibility, which is based on the applicant's disaster-related losses; (2) satisfactory credit; and (3) repayment ability, including minimum income levels. SBA will not decline an application for not having collateral to secure a loan but, to the extent it is available, a borrower may be required to pledge collateral for loans over certain amounts (e.g., $25,000 for physical damage loans).23

According to FEMA's Individuals and Households Program Unified Guidance, FEMA is required to use four main criteria for determining FEMA IA eligibility: (1) the applicant is a U.S. citizen, non-citizen national, or qualified alien residing; (2) FEMA must be able to verify the applicant's identity; (3) the applicant's insurance, or other forms of disaster assistance received, cannot meet their disaster-caused needs; and (4) the applicant's necessary expenses and serious needs are directly caused by a declared disaster.24 As described below and discussed in more detail in "SBA Income Test," while FEMA claims that assistance is based on damage amounts rather than income, household income does appear to be a key criterion for making grant determinations.

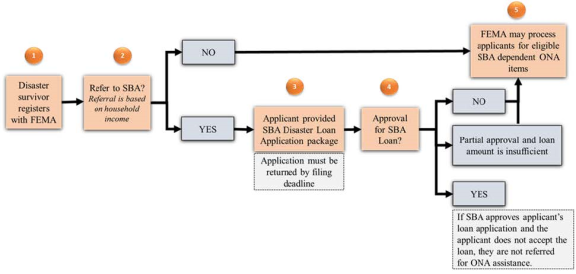

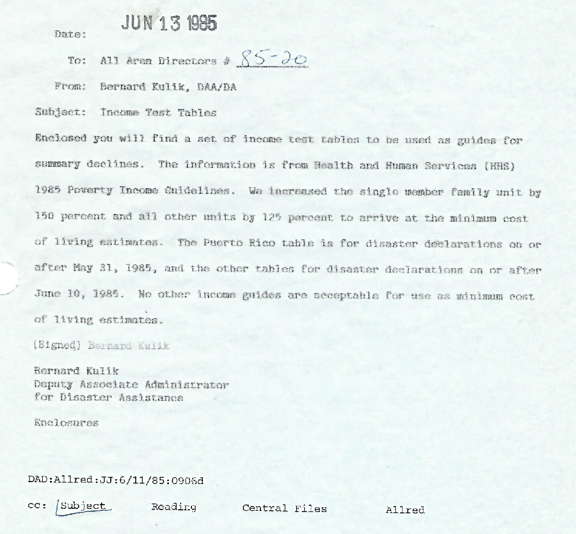

As demonstrated in Figure 1, applicants typically apply for FEMA IA assistance first. Based on income information provided as part of the FEMA registration process FEMA applies an income test developed by SBA for its initial applicant screening. Applicants above certain income thresholds are not eligible for FEMA IA assistance and are referred back to SBA for loan consideration. SBA developed the minimum income levels or "minimum cost of living estimates" by applying a formula to the U.S Department of Health and Human Services Federal Poverty Guidelines.25 As shown in Table 1, SBA establishes minimum income levels by multiplying the poverty level for a family of one by a factor of 1.5, and multiplying the poverty level for families of greater than one by a factor of 1.25.26 The income test formula is not specifically authorized in statute and is not published in SBA regulations. Rather, the formula was first introduced as agency policy in 1985 by SBA Memorandum 85-20 as a means to help determine the applicant's ability to repay the loan and is still in use today (see Appendix B).

FEMA refers applicants to the SBA Disaster Loan Program if they meet or exceed certain income levels and therefore do not qualify for grant assistance. For example, it could be inferred that an individual who earns $18,210 or more per year would initially be denied FEMA grant assistance and referred to the SBA Disaster Loan Program to apply for an SBA disaster loan to repair and rebuild their home (see Stage 2 of Figure 1).

If the applicant is denied an SBA disaster loan, or the loan is insufficient for their recovery needs, the applicant is referred back to FEMA for eligible "SBA dependent ONA" assistance from FEMA (see stage 5 of Figure 1).

SBA disaster loan applicants with income below the minimum income level are classified as Failed Income Test (FIT). FIT applicants are notified that their SBA disaster loan application has been denied and advised that they will be notified if there are any changes to the decision. They are then referred back to FEMA to be considered for possible additional FEMA grant assistance.

|

|

Source: Federal Emergency Management Agency, Individuals and Households Program Unified Guidance, FP 104-009-03, September 2016, p. 89, available at https://www.fema.gov/media-library-data/1483567080828-1201b6eebf9fbbd7c8a070fddb308971/FEMAIHPUG_CoverEdit_December2016.pdf. Note: ONA= Other Needs Assistance. ONA provides financial assistance for other disaster-related expenses and needs. For more information on ONA see CRS Report R44619, FEMA Disaster Housing: The Individuals and Households Program—Implementation and Potential Issues for Congress, by [author name scrubbed]. |

|

Number of Persons |

HHS Poverty Guidelines for 2018 |

SBA Income Threshold |

|

1 |

$12,140 |

$18,210 |

|

2 |

$16,460 |

$20,575 |

|

3 |

$20,780 |

$25,975 |

|

4 |

$25,100 |

$31,375 |

|

5 |

$29,420 |

$36,775 |

|

6 |

$33,740 |

$42,175 |

|

7 |

$38,060 |

$47,575 |

|

8 |

$42,380 |

$52,975 |

Source: Based on CRS interpretation of U.S Department of Health and Human Services, U.S. Federal Poverty Guidelines Used to Determine Financial Eligibility for Certain Federal Programs, Washington, DC, at https://aspe.hhs.gov/poverty-guidelines; and formula applied in SBA Memorandum 85-20: Bernard Kulik, Deputy Associate Administrator for Disaster Assistance, U.S. Small Business Administration, Income Test Tables:, SBA Memorandum 85-20, June 13, 1985.

FEMA Appeals

Applicants may submit a written appeal if they disagree with any FEMA determination within 60 days of the date of their eligibility notification letter. Applicants may appeal initial eligibility determinations for housing assistance and ONA, and denials for continued rental assistance, and direct housing assistance. FEMA does not accept multiple appeals for the same reason, but may request additional information and conduct additional reviews as new information is received.

All appeals must be in writing and require an applicant signature—they cannot be accepted via email.27 The applicant must submit their appeal to the state, territorial, or tribal government if ONA is administered under the Joint or State Option.28

SBA Appeals

Applicants have six months to request a reconsideration of a decline decision for an SBA disaster loan application. Applicants have 30 days to appeal a subsequent decline decision of their SBA disaster loan application.29

Policy Observations and Considerations

CMA and Duplication of Benefits

Following a major disaster, homeowners and businesses may have access to a number of resources to assist in the response, recovery, and rebuilding process. The range of resources includes insurance payouts, state and local government assistance, charitable donations from private institutions and individuals, as well as certain forms of federal assistance. In addition to FEMA and SBA disaster assistance, individuals and households may be eligible for the Department of Housing and Urban Development's (HUD's) Community Development Block Grant Disaster Recovery (CDBG-DR) program.30 Compensation from multiple sources that exceed the total loss amount is generally considered a duplication of benefits. When duplication occurs, the recipient is liable to the United States to pay back the duplicated benefit.

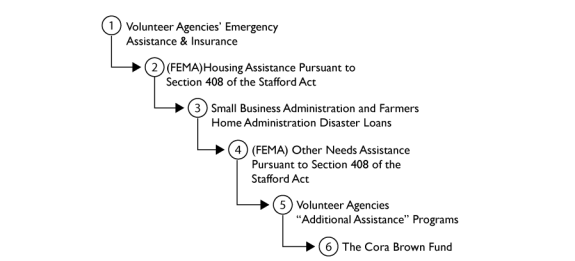

Section 312 of the Stafford Act requires federal agencies to ensure that individuals (and businesses) do not receive disaster assistance for losses for which they have already been compensated or may expect to be compensated.31 FEMA is the primary agency responsible for policy and procedural guidance on duplication of benefits. The uniformity requirement set forth in Section 312 of the Stafford Act is located in FEMA regulation 44 C.F.R. §206.191, which establishes a delivery sequence of disaster assistance provided by federal agencies and organizations (see Figure 2).

|

An organization's position within the sequence determines the order in which it should provide assistance and what other resources must be considered before that assistance is provided. Further, each organization is responsible for delivering assistance without regard to duplication later in the sequence.

According to FEMA regulations, the agency or organization that is lower in the delivery sequence should not provide assistance that duplicates assistance provided by an agency or organization higher in the sequence. When the delivery sequence has been disrupted, the disrupting agency is responsible for rectifying the duplication.

As mentioned previously in this report, SBA and FEMA have a computer matching agreement (CMA) to share real-time data on assistance provided to applicants. SBA also shares relevant data with states, territories, tribes, and local government jurisdictions and voluntary agencies. In cases where the data contains personally identifiable information (PII), a Memorandum of Understanding (MOU) must first be prepared and signed by both SBA and the authorized requesting party to help avoid duplication of benefits.32

SBA and FEMA entered into the CMA pursuant to section (o) of the Privacy Act of 1974 (5 U.S.C. §552a).33 As outlined in the September 25, 2015, Federal Register notice, "the financial and administrative responsibilities will be evenly distributed between SBA and DHS/FEMA unless otherwise set forth in this agreement."34 The Federal Register notice further stated that the CMA is "part of a government-wide initiative, Executive Order 13411—Improving Assistance for Disaster Victims (August 29, 2006) ... to ensure that benefits provided to disaster survivors by DHS/FEMA and SBA are not duplicated."35

Though the CMA is part of a government-wide initiative to prevent duplication of benefits, it is solely used by FEMA and SBA. Some may argue that the CMA should also be used by other federal agencies that offer disaster assistance (such as CDBG-DR). Others, however, might argue using the CMA with agencies other than FEMA and SBA is problematic or potentially ineffective. For example, HUD provides funds to state and local jurisdiction grantees. HUD does not have the individual award data to match up with SBA loan applicant data to determine instances of duplication.

If Congress is concerned about the use of the CMA, it could investigate how it could be used in conjunction with other disaster assistance programs. If CMA is not being universally used by federal agencies, Congress could investigate why it is not being used, evaluate challenges preventing its use, and mandate its use across the federal government. Additionally, Congress could use oversight to investigate how effective the CMA has been at preventing duplication since its implementation.

Similarly, Congress could also review how MOUs are being used by states, territories, tribes, local government jurisdictions, and voluntary agencies to determine their efficacy in reducing duplication. Congress could also consider making the MOUs a requirement for certain types of assistance or investigate other incentives that would induce the entities to sign MOUs.

SBA Income Test

As mentioned previously, both FEMA and SBA screen applicants according to minimum income levels (see Table 1). SBA creates the minimum income levels by applying a formula to the U.S Department of Health and Human Services Federal Poverty Guidelines. According to SBA Standard Operation Procedure (SOP), minimum income includes wages, alimony, child support payments, interest and dividend income from savings, retirement, pension, social security or disability payments.

According to SBA Memorandum 85-20 (see Appendix B), the income test table is used as a guide "for summary declines." It is unclear from SBA SOPs if income levels are a hard limit to screen out applicants, or if there is some discretion in the process. Additionally, some might be confused about income standards based on publicly available information provided to disaster survivors. For example, in a news release published in the wake of the 2011 Missouri River flooding, FEMA stated "federal and state disaster assistance programs are available to all who suffered damages. Aid is damage-based, not income-based. The kinds of help provided depend on an applicant's circumstances and unmet needs"36 In another news release issued May 9, 2014, FEMA stated that "income is not a consideration for FEMA disaster assistance."37

On the one hand, it could be argued that the income test is being used by FEMA as a "pre-decisional" screening tool, and that ultimately, income is not a factor for FEMA grant assistance. Others may disagree and question why FEMA reviews household income if it has no bearing on grant assistance. If Congress does not want grant determinations to be based on income, it could prohibit FEMA from collecting income information and using it as a screening tool. If, however, Congress determines that grant determinations should be based, at least in part, on certain income levels, it could require FEMA to publish policy documents that specify how income is used to award grant assistance.

Congress may also consider whether SBA should continue to use established thresholds and formulas based on SBA Memorandum 85-20 to determine eligibility, or provide SBA with some measure of discretion in the process. Some might argue that uniformity is needed to ensure equitable determinations. Others might argue that a one size-fits-all approach does not address special or mitigating circumstances. In general, eligibility for an SBA disaster loan is assigned to the person (or entity in the case of businesses) that legally owns or is responsible for the repair or replacement of the disaster-damaged property based on that person's ability to repay the loan. It could be argued, however, that the ability to pay a loan is not solely determined by income and that a range of factors and circumstances should be also be considered. For example, a retired person may not meet a certain minimum income level, but own assets that could be liquidated for repayment purposes. Another example is the parent(s) of a university student who are willing to co-sign for their child's disaster loan. In both these examples, strict adherence to an income test might prevent people from obtaining loans who may be able to repay them through nontraditional methods. Congress may also consider whether the income test is an ineffective screening tool for identifying applicants that meet the income test but cannot repay their disaster loan; for example, a person who earns more than the minimum income level, but has debt that impedes their ability to repay the disaster loan.

Finally, it is not clear if FEMA has access to the same income information as SBA. As mentioned earlier, minimum income includes wages, alimony, child support payments, interest and dividend income from savings, retirement, pension, social security, and disability payments. This information is gathered on SBA Form 5C and IRS Form 4506-T. Applicants, however, can fill these forms out after initially registering with FEMA. This could result in the reporting of different income levels. For example, the income reported to FEMA could be less than what is reported to SBA.

If Congress is concerned about how determinations are made, it could consider requiring SBA and FEMA to publish specific determination criteria in their respective regulations and policy guidance documents. Congress may also consider putting the determination formula into statute. Finally, Congress may decide whether it is best to have uniformity in the determination process, or whether to provide the agencies certain parameters that allow for some discretion when making grant and loan decisions.

Appendix A. Relevant Statutory Authorities and Regulations

The following is a listing of selected authorities and regulations pertaining to the duplication of disaster assistance benefits. This list should be considered representative, not exhaustive.

Stafford Act (42 U.S.C. §5155)

The Stafford Act is the primary statute governing the provision of federal disaster assistance, particularly FEMA assistance. Section 312 of the Stafford Act requires federal agencies that provide financial disaster assistance to ensure that individuals, businesses, or other entities suffering losses as a result of a major disaster or emergency do not receive assistance for losses for which they have already been compensated. Section 312 also requires the President to establish procedures that ensure uniformity in preventing duplication of benefits. Under Section 312, any person, business, or other entity that has received or is entitled to receive federal disaster assistance is liable to the United States for the repayment of such assistance to the extent that such assistance duplicates benefits available for the same purpose from another source, including insurance and other federal programs.

Stafford Act (42 U.S.C. §5174)

Section 408(a)(1) states that the President may provide assistance to individuals and households who, as a result of a major disaster, "have necessary expenses and serious needs in cases in which the individuals and households are unable to meet such expenses or needs through other means."

FEMA Regulation

44 C.F.R. 206.191, which establishes the policies implementing Section 312 of the Stafford Act, states that it is FEMA policy to prevent the duplication of benefits between its own programs, other assistance programs, and insurance benefits. The regulation requires individuals to repay all duplicated assistance to the agency providing the assistance. Under 44 C.F.R. 206.191, a federal agency providing disaster assistance is responsible for preventing or rectifying duplication of benefits when they occur. 44 C.F.R. 206.191 also includes a "delivery sequence" hierarchy intended to prevent waste, fraud, and abuse of program assistance, including the duplication of benefits (see Figure 2).

44 C.F.R. 206.111 defines financial ability of the applicant of pay housing costs. According to 44 C.F.R. 206.111 if the "household income has not changed subsequent to or as a result of the disaster then the determination is based upon the amount paid for housing before the disaster. If the household income is reduced as a result of the disaster then the applicant will be deemed capable of paying 30 percent of gross post disaster income for housing. When computing financial ability, extreme or unusual financial circumstances may be considered by the Regional Administrator."

Small Business Act (15 U.S.C. §636(b)(1)(A))

The first proviso in 15 U.S.C. §636(b)(1)(A) states that SBA is authorized to make disaster loans "provided that such damage or destruction is not compensated for by insurance or otherwise."

Small Business Act (15 U.S.C. §647)

Section 18(a) of the Small Business Act (P.L. 85-536, as amended) prohibits the SBA from providing benefits that duplicate the assistance provided by another department or agency of the federal government. Section 18(a) states that if loan applications are refused or denied by a department or agency due to administrative withholding or due to an administratively declared moratorium, then no duplication is deemed to have occurred.

SBA Regulation

13 C.F.R. 123.101(c) states that applicants for SBA Disaster Loan assistance are not eligible for a home disaster loan if their damaged property can be repaired or replaced with the proceeds of insurance, gifts, or other compensation. These amounts must either be deducted from the amount of the claimed losses or, if received after SBA has disbursed the loan, must be paid to SBA as principal payments on the loan.

Appendix B. SBA Memorandum 85-20

|

Appendix C. FEMA and SBA Constituent Resources

The following provides various FEMA and SBA resources and information that may be of use for constituents in declared disaster areas.

Application Websites

FEMA Assistance:

https://www.disasterassistance.gov/

SBA Assistance:

https://disasterloan.sba.gov/ela/

Contact Numbers

FEMA

1-800-621-FEMA (3362)

TTY: 1-800-462-7585

SBA

1-800-659-2955

TTY: 1-800-877-8339

Frequently Asked Questions About FEMA Individual Assistance

https://www.fema.gov/news-release/2015/06/04/frequently-asked-questions-about-individual-assistance

Frequently Asked Questions About the SBA Disaster Loan Program

https://www.sba.gov/sites/default/files/articles/sba-disaster-loans-faq.pdf

SBA Form 5C

https://disasterloan.sba.gov/ela/Documents/Disaster%20Home%20Loan%20Application%20(SBA%20Form%205c).aspx

SBA Form 5C in Spanish

https://disasterloan.sba.gov/ela/Documents/Loan%20Application%20Home%20Spanish%20(Form%205C).pdf

IRS Form 4506-T Instructions

https://disasterloan.sba.gov/ela/Documents/Request%20for%20Transcript%20of%20Tax%20Return%20(IRS%20Form%204506T).aspx?ff=false&sp=0

IRS Form 4506-T

https://disasterloan.sba.gov/ela/Documents/Request%20for%20Transcript%20of%20Tax%20Return%20(IRS%20Form%204506T).aspx?pt=Home&sp=1

IRS Form 4506-T Instructions in Spanish