Medicare Part B: Enrollment and Premiums

Changes from May 6, 2020 to June 15, 2021

This page shows textual changes in the document between the two versions indicated in the dates above. Textual matter removed in the later version is indicated with red strikethrough and textual matter added in the later version is indicated with blue.

Contents

- Introduction

- Medicare Part B Eligibility and Enrollment

- Initial Enrollment Periods

- General Enrollment Period

- Special Enrollment Periods

- Late-Enrollment Premium Penalty and Exemptions

- Calculation of Penalty

- Penalty Exemptions

- Current Workers

- International Volunteers

- Equitable Relief

- Collection of the Part B Premium

- Deduction of Part B Premiums from Social Security Checks

- Part B Enrollees Who Do Not Receive Social Security Benefits

- Determining the Part B Premium

- Premium Calculation for 2020

- Contingency Margin

- Income-Related Premiums

- Determination of Income

- Income Categories and Premium Adjustments

- Income Thresholds

- Premium Assistance for Low-Income Beneficiaries

- Qualified Medicare Beneficiaries

- Specified Low-Income Medicare Beneficiaries

- Qualifying Individuals

- Protection of Social Security Benefits from Increases in Medicare Part B Premiums

- Some Beneficiaries Are Not Protected by the Hold-Harmless Provision

- Application of the Hold-Harmless Rule in Years Prior to 2016

- Application of the Hold-Harmless Rule in 2016

- Application of the Hold-Harmless Rule in 2017

- Application of the Hold-Harmless Rule in 2018

- Application of the Hold-Harmless Rule in 2019 and 2020

- Potential Application of the Hold-Harmless Rule in 2021

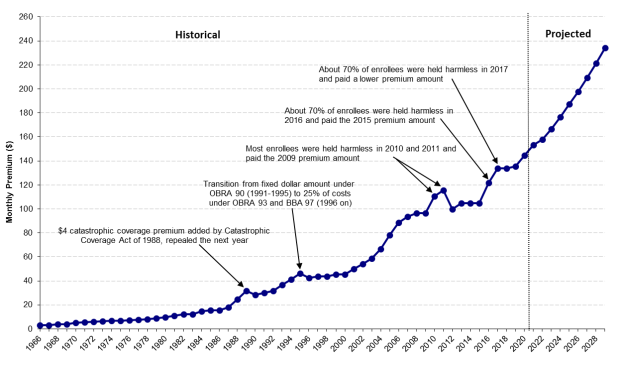

- Part B Premiums over Time

- Current Issues

- Premium Amount and Annual Increases

- Impact of the Hold-Harmless Provision on Those Not Held Harmless

- Proposals to Modify the Late-Enrollment Penalty

- Deficit Reduction Proposals

- Increasing Medicare Premiums

- Impose a Part B Premium Surcharge for Beneficiaries in Medigap Plans with Near First-Dollar Coverage

- Limit Federal Subsidies

- Considerations

Tables

- Table 1. Initial Enrollment Period

- Table 2. Monthly Medicare Part B Premiums for 2020

- Table 3. Part B Premium Adjustment for Married Beneficiaries Filing Separately for 2020

- Table 4. Medicare High-Income Premium Thresholds: 2017 to 2020

- Table 5. 2020 Medicare Savings Program Eligibility Standards

- Table A-1. Monthly Part B Premiums, 1966-2020

- Table B-1. Income Levels for Determining Part B Premium Adjustment and Per Person Premium Amounts, 2007-2020

- Table B-2. Income Levels for Determining Part B Premium Adjustment for Married Beneficiaries Filing Separately and Associated Premiums, 2007-2020

- Table C-1. Projected Part B Premiums

Appendixes

- Appendix A. History of the Part B Premium Statutory Policy and Legislative Authority

- Appendix B. Standard and High-Income Part B Premiums and Income Thresholds: 2007-2020

- Appendix C. Estimated Future Part B Premiums

- Appendix D. Bipartisan Budget Act of 2015 Changes to 2016 Part B Premiums

- Appendix E. Part A Premiums

Summary

Medicare Part B: Enrollment and Premiums

June 15, 2021

Medicare is a federal insurance program that pays for covered health care services of most individuals aged 65 and older and certain disabled persons. In calendar year 2020, 2021,

Patricia A. Davis

the program is expected to cover about 63 million persons (54 million aged and 9 million disabled) at a total cost of $862 billion. 64 mil ion persons at a total cost of $922 bil ion.

Specialist in Health Care

Most individuals (or their spouses) aged 65 and older who have worked in covered

Financing

employment and paid Medicare payroll taxes for 40 quarters receive premium-free

Medicare Part A (Hospital Insurance). Those entitled to Medicare Part A (regardless of

whether they are eligible for premium-free Part A) have the option of enrolling in Part B, which covers such things as physician and outpatient services and medical equipment.

Beneficiaries have a seven-month initial enrollment period, and those who enroll in Part B after this initial

enrollment period and/or reenroll after a termination of coverage may be subject to a late--enrollment penalty. This penalty is equal to a 10% surcharge for each 12 months of delay in enrollment and/or reenrollment. Under certain c ertain conditions, some beneficiaries are exempt from the late-enrollment penalty; these exempt beneficiaries include working individuals (and their spouses) with group coverage through their current employment, some international volunteers, and those granted "“equitable relief."

”

Whereas Part A is financed primarily by payroll taxes paid by current workers, Part B is financed through a combination of beneficiary premiums and federal general revenues. The standard Part B premiums are set to cover 25% of projected average per capita Part B program costs for the aged, with federal general revenues accounting for the remaining amount. In general, if projected Part B costs increase or decrease, the premium rises or fal sor falls proportionately. However, some Part B enrolleesenrol ees are protected by a provision in the Social Security Act

(the hold-harmless provision) that prevents their Medicare Part B premiums from increasing more than the annual increase in their Social Security benefit payments. This protection does not apply to four main groups of beneficiaries: low-income beneficiaries whose Part B premiums are paid by the Medicaid program; high-income beneficiaries who are subject to income-related Part B premiums; those whose Medicare premiums are not deducted from Social Security benefits; and new Medicare and Social Security enrollees.

Most Part B participants must pay monthly premiums, which do not vary with a beneficiary'’s age, health status, or place of residence. However, since 2007, higher-income enrollees pay higher premiums to cover a higher percentage of Part B costs ("“income-related monthly adjustment amounts"” (IRMAA)). AdditionallyAdditional y, certain low-income beneficiaries may qualify for Medicare cost-sharing and/or premium assistance from Medicaid through a Medicare Savings Program. The premiums of those receiving benefits through Social Security are deducted from their monthly payments.

Each year, the Centers for Medicare & Medicaid Services (CMS) determines the Medicare Part B premiums for the following year. The standard monthly Part B premium for 2020 is $144.602021 is $148.50. However, in 20202021, the hold-harmless provision applies to someabout 2% of Part B enrollees, and these individuals pay lower premiums. (The premiums of those held harmless vary depending on the dollar amount of the increase in their Social Security benefits.) Higher-income beneficiaries, currently defined as individuals with incomes over $8788,000 per year or

couples with incomes over $174176,000 per year, pay $202.40, $289.20, $376.00, $462.70, or $491.60207.90, $297.00, $386.10, $475.20, or $504.90 per month, depending on their income levels.

Current issues related to the Part B premium that may come before Congress include the amount of the premium and its rate of increase (and the potential net impact on Social Security benefits), the impact of the hold-harmless provision on those not held harmless, modifications to the late-enrollment penalty, and possible increases in Medicare premiums as a means to reduce federal spending and deficits.

Congressional Research Service

link to page 5 link to page 7 link to page 8 link to page 9 link to page 10 link to page 12 link to page 13 link to page 14 link to page 14 link to page 15 link to page 15 link to page 17 link to page 17 link to page 18 link to page 19 link to page 20 link to page 21 link to page 21 link to page 22 link to page 23 link to page 25 link to page 27 link to page 27 link to page 28 link to page 28 link to page 29 link to page 30 link to page 32 link to page 32 link to page 32 link to page 34 link to page 34 link to page 35 link to page 36 link to page 38 link to page 38 link to page 38 link to page 38 link to page 39 link to page 39 Medicare Part B: Enrollment and Premiums

Contents

Introduction ................................................................................................................... 1 Medicare Part B Eligibility and Enrollment ......................................................................... 3

Initial Enrollment Periods ........................................................................................... 4 General Enrollment Period .......................................................................................... 5 Special Enrollment Periods ......................................................................................... 6

Late-Enrollment Premium Penalty and Exemptions .............................................................. 8

Calculation of Penalty ................................................................................................ 9 Penalty Exemptions ................................................................................................. 10

Current Workers ................................................................................................. 10 International Volunteers....................................................................................... 11

Equitable Relief ................................................................................................. 11

Collection of the Part B Premium .................................................................................... 13

Deduction of Part B Premiums from Social Security Checks .......................................... 13

Part B Enrollees Who Do Not Receive Social Security Benefits ...................................... 14

Determining the Part B Premium ..................................................................................... 15

Premium Calculation for 2021 ................................................................................... 16 Contingency Margin ................................................................................................ 17

Income-Related Premiums.............................................................................................. 17

Determination of Income .......................................................................................... 18 Income Categories and Premium Adjustments.............................................................. 19

Legislative Changes to Income Thresholds .................................................................. 21

Premium Assistance for Low-Income Beneficiaries ............................................................ 23

Qualified Medicare Beneficiaries ............................................................................... 23

Specified Low-Income Medicare Beneficiaries ............................................................ 24 Qualifying Individuals.............................................................................................. 24

Protection of Social Security Benefits from Increases in Medicare Part B Premiums................ 25

Some Beneficiaries Are Not Protected by the Hold-Harmless Provision ........................... 26

Application of the Hold-Harmless Rule in 2021 ........................................................... 28 Potential Application of the Hold-Harmless Rule in 2022 .............................................. 28

Part B Premiums over Time ............................................................................................ 28 Current Issues............................................................................................................... 30

Premium Amount and Annual Increases ...................................................................... 30 Impact of the Hold-Harmless Provision on Those Not Held Harmless .............................. 31 Proposals to Modify the Late-Enrollment Penalty ......................................................... 32

Deficit Reduction Proposals ...................................................................................... 34

Increasing Medicare Premiums............................................................................. 34 Impose a Part B Premium Surcharge for Beneficiaries in Medigap Plans with

Near First-Dollar Coverage ............................................................................... 34

Limit Federal Subsidies ....................................................................................... 35

Considerations ................................................................................................... 35

Congressional Research Service

link to page 34 link to page 9 link to page 24 link to page 25 link to page 25 link to page 26 link to page 29 link to page 42 link to page 45 link to page 45 link to page 47 link to page 47 link to page 48 link to page 40 link to page 45 link to page 45 link to page 48 link to page 49 link to page 51 link to page 55 link to page 56 Medicare Part B: Enrollment and Premiums

Figures Figure 1. Monthly Medicare Part B Premiums ................................................................... 30

Tables

Table 1. Initial Enrollment Period ...................................................................................... 5 Table 2. Monthly Medicare Part B Premiums for 2021 ........................................................ 20 Table 3. Part B Premium Adjustment for Married Beneficiaries Filing Separately

for 2021 .................................................................................................................... 21

Table 4. Changes to the Medicare High-Income Premium Thresholds: 2017 to 2020................ 22 Table 5. 2021 Medicare Savings Program Eligibility Standards ............................................ 25

Table A-1. Monthly Part B Premiums, 1966-2020 .............................................................. 38 Table B-1. Income Levels for Determining Part B Premium Adjustment and Per Person

Premium Amounts, 2007-2021 ..................................................................................... 41

Table B-2. Income Levels for Determining Part B Premium Adjustment for Married

Beneficiaries Filing Separately and Associated Premiums, 2007-2021 ................................ 43

Table C-1. Projected Part B Premiums.............................................................................. 44

Appendixes Appendix A. History of the Part B Premium Statutory Policy and Legislative Authority ........... 36 Appendix B. Standard and High-Income Part B Premiums and Income Thresholds: 2007-

2021......................................................................................................................... 41

Appendix C. Estimated Future Part B Premiums ................................................................ 44 Appendix D. Bipartisan Budget Act of 2015 Changes to 2016 Part B Premiums ..................... 45 Appendix E. Application of the Hold-Harmless Provision in Years Prior to 2021 .................... 47 Appendix F. Part A Premiums ......................................................................................... 51

Contacts Author Information ....................................................................................................... 52

Congressional Research Service

Medicare Part B: Enrollment and Premiums

Introduction Medicare is a federal insurance program that pays for covered health care services of most individuals depending on their income levels.

Starting in 2018, the Medicare Access and CHIP Reauthorization Act of 2015 (MACRA; P.L. 114-10) reduced the income thresholds in the highest two income tiers so that more enrollees will pay higher premiums. The Bipartisan Budget Act of 2018 (BBA 18; P.L. 115-123) added an additional income tier beginning in 2019 for individuals with annual incomes of $500,000 or more or couples filing jointly with incomes of $750,000 or more.

Current issues related to the Part B premium that may come before Congress include the amount of the premium and its rate of increase (and the potential net impact on Social Security benefits), the impact of the hold-harmless provision on those not held harmless, modifications to the late-enrollment penalty, and possible increases in Medicare premiums as a means to reduce federal spending and deficits.

Introduction

Medicare is a federal insurance program that pays for covered health care services of most individuals aged 65 and older and certain disabled persons. Medicare serves approximately one in six Americans and virtually all virtual y al of the population aged 65 and over. In calendar year (CY) 2020, 2021, the program is expected to cover about 63 million persons (54 million aged and 9 million disabled)64 mil ion persons at a total cost of about $862 billion, 922 bil ion, accounting for approximately 3.94% of gross domestic product.11 The Medicare program is

administered by the Centers for Medicare & Medicaid Services (CMS) within the Department of Health and Human Services (HHS), and individuals enroll in Medicare through the Social

Security Administration (SSA).

Medicare consists of four parts—Parts A through D. Part A covers hospital services, skilled skil ed nursing facility services, home health visits, and hospice services. Part B covers a broad range of medical services and supplies, including physician services, laboratory services, durable medical equipment, and outpatient hospital services. Enrollment in Part B is voluntary; however, most Medicare beneficiaries (about 91%) are enrolled in Part B. Part C (Medicare Advantage) provides

private plan options, such as managed care, for beneficiaries who are enrolled in both Part A and

Part B. Part D provides optional outpatient prescription drug coverage.2

2

Each part of Medicare is funded differently.33 Part A is financed primarily through payroll taxes

imposed on current workers (2.9% of earnings, shared equallyequal y between employers and workers), which are credited to the Hospital Insurance (HI) Trust Fund. Beginning in 2013, workers with annual wages over $200,000 for single tax filers or $250,000 for joint filers pay an additional 0.9%.4 Beneficiaries general y0.9%.4 Beneficiaries generally do not pay premiums for Part A. In 20202021, total Part A expenditures are expected to reach about $351 billion372 bil ion, representing about 4140% of program costs.5 5 Parts B and

D, the voluntary portions, are funded through the Supplementary Medical Insurance (SMI) Trust Fund, which is financed primarily by general revenues (transfers from the U.S. Treasury) and premiums paid by enrollees. In 20202021, about $2.8 billionbil ion in fees on manufacturers and importers of brand-name prescription drugs also will wil be used to supplement the SMI Trust Fund.66 In 20202021, Part B expenditures are expected to reach about $404 billion434 bil ion, and Part D expenditures are expected to

reach about $107 billion116 bil ion, representing about 47% and 1213% of program costs, respectively. (Part C is financed proportionately through the HI and SMI Trust Funds; expenditures for Parts A and B

services provided under Part C are included in the above expenditure figures.)

Part B beneficiary premiums are normally

1 Expenditure estimates from Boards of T rustees, Federal Hospital Insurance and Federal Supplementary Medical Insurance T rust Funds, 2020 Annual Report of the Boards of Trustees of the Federal Hospital Insurance and Federal Supplem entary Medical Insurance Trust Funds, April 22, 2020, at https://www.cms.gov/Research-Statistics-Data-and-Systems/Statistics-T rends-and-Reports/ReportsTrustFunds/index.html. (Hereinafter, 2020 Medicare T rustees Report.) T hese projections do not take into account the potential effects of the Coronavirus Disease 2019 (COVID-19) public health emergency.

2 For additional information on the Medicare program, see CRS Report R40425, Medicare Primer. 3 See CRS Report R43122, Medicare Financial Status: In Brief. 4 See Internal Revenue Service, Questions and Answers for the Additional Medicare Tax, at http://www.irs.gov/Businesses/Small-Businesses-&-Self-Employed/Questions-and-Answers-for-the-Additional-Medicare-T ax.

5 All expenditure data are from the 2020 Medicare T rustees Report. T he estimates do not reflect the potential impact of the COVID-19 pandemic on Medicare spending or the impact of related legislation enacted since the time of that report.

6 Centers for Medicare & Medicaid Services (CMS), “Medicare Program: Medicare Part B Monthly Actuarial Rates, Premium Rate, and Annual Deductible Beginning January 1, 2021,” 85 Federal Register 71904, November 12, 2020.

Congressional Research Service

1

link to page 51 link to page 21 link to page 27 link to page 29 link to page 29 Medicare Part B: Enrollment and Premiums

Part B beneficiary premiums are normal y set at a rate each year equal to 25% of average expected per capita Part B program costs for the aged for the year.77 Higher-income enrollees pay higher premiums set to cover a greater percentage of Part B costs,88 while those with low incomes may qualify for premium assistance through one of several Medicare Savings Programs administered by Medicaid.99 Individuals who receive Social Security or Railroad Retirement Board (RRB) retirement or disability benefits have their Part B premiums automaticallyautomatical y deducted

from their benefit checks. Part B premiums are generallygeneral y announced in the fall fal prior to the year that they are in effect (e.g., the 20202021 Part B premiums were announced in November 2019).10

In 20202020).10 In 2021, the standard monthly Part B premium is $144.60.11148.50.11 However, in 20202021, about 32% of Part B enrollees are protected by a hold-harmless provision in the Social Security Act that prevents their Medicare Part B premiums from increasing more than the annual dollar amount of the increase in

their Social Security benefit payments. These individuals pay premiums of less than $144.60.12

2020 Medicare Part B Premiums

Source: Centers for Medicare & Medicaid Services (CMS), Fact Sheet, "2020 Medicare Parts A & B Premiums and Deductibles," November 8, 2019. |

with

Joint Tax Return with

Monthly

Income:

Income:

Premium

Less than or equal to $88,000

Less than or equal to $176,000

$148.50

Greater than $88,000 and less than or

Greater than $176,000 and less

equal to $111,000

than or equal to $222,000

207.90

Greater than $111,000 and less than

Greater than $222,000 and less

or equal to $138,000

than or equal to $276,000

297.00

Greater than $138,000 and less than

Greater than $276,000 and less

or equal to $165,000

than or equal to $330,000

386.10

Greater than $165,000 and less than

Greater than $330,000 and less

$500,000

than $750,000

475.20

Greater than or equal to

Greater than or equal to $500,000

$750,000

504.90

Source: Centers for Medicare & Medicaid Services (CMS), Fact Sheet, “2021 Medicare Parts A & B Premiums and Deductibles,” November 6, 2020.

In addition to premiums, Part B beneficiaries may pay other out-of-pocket costs when they use services. The annual deductible for Part B services is $198203.00 in 2020.132021.13 After the annual 7 In 2021, beneficiary premiums are expected to cover about 15.0% of the costs of “traditional” Medicare (Parts A and B combined), 14.5% from Part B premiums, and 0.6% from voluntary Part A premiums. See Appe ndix E for information on Part A premiums. 8 Depending on their income, beneficiaries subject to income-related monthly adjustments pay a total monthly premium of 35%, 50%, 65%, 80%, or 85% of expected per capita Part B costs for the aged. See “ Income-Related Premium.”

9 See “Premium Assistance for Low-Income Beneficiaries.” 10 CMS, Fact Sheet, “2021 Medicare Parts A & B Premiums and Deductibles,” November 6, 2020, at https://www.cms.gov/newsroom/fact-sheets/2021-medicare-parts-b-premiums-and-deductibles. 11 CMS, “Medicare Program: Medicare Part B Monthly Actuarial Rates, Premium Rate, and Annual Deductible Beginning January 1, 2021,” 85 Federal Register 71904, November 12, 2020, at https://www.federalregister.gov/documents/2020/11/12/2020-25029/medicare-program-medicare-part-b-monthly-actuarial-rates-premium-rates-and-annual-deductible.

12 Data provided by CMS, May 2021. T he premiums of those held harmless vary depending on the dollar amount of the increase in their Social Security benefits. See “ Protection of Social Security Benefits from Increases in Medicare Part B Premiums.” 13 Annual increases in the deductibles are not protected by the hold-harmless provision.

Congressional Research Service

2

link to page 51 Medicare Part B: Enrollment and Premiums

After the annual deductible is met, beneficiaries are responsible for coinsurance costs, which are generallygeneral y 20% of

Medicare-approved Part B expenses.

This report provides an overview of Medicare Part B premiums, including information on Part B eligibility

eligibility and enrollment, late-enrollment penalties, collection of premiums, determination of annual premium amounts, premiums for high-income enrolleesenrol ees, premium assistance for low-income enrollees, protections for Social Security recipients from rising Part B premiums, and historical Medicare Part B premium trends. This report also provides a summary of various premium-related issues that may be of interest to Congress. Specific Medicare and Social

Security publications and other resources for beneficiaries, and those who provide assistance to

them, are cited where appropriate.

Medicare Part B Eligibility and Enrollment

An individual (or the spouse of an individual) who has worked in covered employment and paid Medicare payroll taxes for 40 quarters is entitled to receive premium-free Medicare Part A benefits upon reaching the age of 65.14 Those who have paid in for fewer than 40 quarters may

enroll in Medicare Part A by paying a premium.14 All 15 Al persons entitled to Part A (regardless of whether they are eligible for premium-free Part A) are also entitled to enroll in Part B. An aged person not entitled to Part A may enroll in Part B if he or she is aged 65 or over and either a U.S. citizen or an alien lawfully admitted for permanent residence who has resided in the United States

continuously for the immediately preceding five years.

Those who are receiving Social Security or RRB benefits are automaticallyautomatical y enrolled in Medicare, and coverage begins the first day of the month they turn 65.1516 These individuals will wil receive a Medicare card and a "“Welcome to Medicare"” package about three months before their 65th birthday.1665th

birthday.17 Those who are automaticallyautomatical y enrolled in Medicare Part A also are automatically automatical y enrolled in Part B.1718 However, because beneficiaries must pay a premium for Part B coverage, they have the option of turning it down.1819 Disabled persons who have received cash payments for 14 See CMS, “ Original Medicare (Part A and B) Eligibility and Enrollment ,” at https://www.cms.gov/Medicare/Eligibility-and-Enrollment/OrigMedicarePartABEligEnrol.

15 For additional information on Part A premiums, see Appendix E. 16 For additional information on enrolling in Medicare Parts A and B, see Medicare publication “Enrolling in Medicare Part A & Part B,” at https://www.medicare.gov/Pubs/pdf/11036-Enrolling-Medicare-Part-A-Part-B.pdf. 17 See “‘Welcome to Medicare’ package (automatically enrolled),” at https://www.medicare.gov/forms-help-resources/mail-you-get-about-medicare/welcome-to-medicare-package-automatically-enrolled. When first becoming eligible for Medicare, beneficiaries need to make a number of choices regarding the benefits they wish to sign up for and how they wish to receive them. For example, new enrollees need to decide whether they wish to remain in traditional Medicare (Parts A and B, the default option) or if they would like to receive their A and B benefits through a private Medicare Advantage Plan (Part C). Additionally, beneficiaries need to decide whether they would like to sign up for an outpatient prescription drug plan (Part D). T hese opt ions are described in the “ Welcome to Medicare” package. For free personalized health insurance counseling, beneficiaries may contact their local State Health Insurance Assistance Programs (SHIPs); contact information may be found at http://www.medicare.gov/contacts/ and https://acl.gov/programs/connecting-people-services/state-health-insurance-assistance-program-ship.

18 T hose who live in Puerto Rico are not automatically enrolled in Medicare Part B. T hey need to sign up for Part B during the initial enrollment period or possibly be subject to a penalty. See archived CRS Report R44275, Puerto Rico and Health Care Finance: Frequently Asked Questions, and Social Security Administration (SSA) Publication “Medicare in Puerto Rico,” at http://www.socialsecurity.gov/pubs/EN-05-10521.pdf. T he following bills, introduced in the 116th Congress, would have extended this automatic enrollment to residents of Puert o Rico: the Fairness in Medicare Part B Enrollment Act of 2019 (H.R. 2310), and the T erritories Health Equity Act of 2019 (H.R. 1354 and S. 1773). 19 Should a beneficiary decline Part B coverage, a new Medicare card will be issued that indicates that the beneficiary

Congressional Research Service

3

link to page 9 link to page 12 link to page 12 Medicare Part B: Enrollment and Premiums

Disabled persons who have received cash payments for 24 months under the Social Security or RRB disability programs also automaticallyautomatical y receive a Medicare card and are enrolled in Part B unless they specificallyspecifical y decline such coverage.1920 Those who choose to receive coverage through a Medicare Advantage plan (Part C) must enroll in Part B.

Part B.

Those who are not receiving Social Security or RRB benefits, for example because they are still working20stil working21 or have chosen to defer enrollment because they have not yet reached their full retirement benefit eligibility age,2122 must file an application with the SSA or RRB for Medicare benefits.2223 There are two kinds of enrollment periods, one that occurs when individuals are initially eligible

initial y eligible for Medicare and one annual general enrollment period for those who missed signing up during their initial enrollment period. A beneficiary may drop Part B enrollment and

reenroll an unlimited number of times; however, premium penalties may be incurred.

Initial Enrollment Periods

Those who are not automaticallyautomatical y enrolled in Medicare may sign up during a certain period when they first become eligible. The initial enrollment period is seven months long and begins three months before the month in which the individual first turns 65. (SeeSee Table 1.) Beneficiaries who

do not file an application for Medicare benefits during their initial enrollment period could be subject to the Part B late-enrollment penalty. (See "“Late-Enrollment Premium Penalty and Exemptions."Exemptions.”) If an individual accepts the automatic enrollment in Medicare Part B, or enrolls in Medicare Part B during the first three months of the initial enrollment period, coverage will wil start with the month in which an individual is first eligible, that is, the month of the individual's 65th ’s 65th birthday. Those who enroll during the last four months will wil have their coverage start date delayed

from one to three months after enrollment.2324 The initial enrollment period of those eligible for Medicare based on disability for

has Part A coverage only. (In the 117th Congress, H.R. 1826 would eliminate Part B late-enrollment penalties for Puerto Rico residents who enroll within five years of becoming entitled to Part A.)

20 Individuals with Amyotrophic Lateral Sclerosis are not subject to the 24 -month waiting period; for these individuals Medicare coverage begins the first day of the month during which disability benefits st art. Additionally, the Medicare coverage period for persons diagnosed with end-stage renal disease generally begins in the third month after the month when dialysis begins. 21 For additional information, see CMS, “Employer Community: Information about Medicare Enrollment,” at https://www.cms.gov/Outreach-and-Education/Find-Your-Provider-T ype/Employers-and-Unions/Employer-community.html.

22 In the past, individuals generally were eligible to receive both full Social Security retirement benefits and Medicare coverage starting at the age of 65. However, the age to receive full retirement benefits has changed for some people, depending on the year they were born. For example, those turning 65 in 2021 will not be eligible for full Social Security benefits until the age of 66 and 4 months. See https://www.ssa.gov/benefits/retirement/planner/agereduction.html. 23 T o apply, individuals can call or visit their local Social Security office or call Social Security at 1-800-772-1213. Some people also may apply online if they meet certain rules, at https://www.ssa.gov/benefits/medicare/. For Railroad Retirement Board (RRB) retirees, application information may be found at https://www.rrb.gov/Benefits/Medicare. See also SSA, “Apply Online For Medicare In Less T han 10 Minutes—Even If You Are Not Ready T o Retire,” at http://www.socialsecurity.gov/pubs/EN-05-10530.pdf, and SSA, “ How to Apply Online for Medicare Only,” at http://www.socialsecurity.gov/pubs/EN-05-10531.pdf.

24 An eligibility, enrollment date, and premium calculator may be found on the Medicare.gov website at https://www.medicare.gov/eligibilitypremiumcalc/. T he Consolidated Appropriations Act, 2021 (P.L. 116-260; Division CC, §102) eliminates these delays starting in 2023. For initial enrollment periods occurring in 2023 and subsequent years, coverage will begin the first day of the month after the month of enrollment for enrollments occurring during any of the seven months of the initial enrollment period.

Congressional Research Service

4

link to page 9 link to page 9 Medicare Part B: Enrollment and Premiums

Medicare based on disability or permanent kidney failure is linked to the date the disability or

or permanent kidney failure is linked to the date the disability or treatment began.24

|

3 Months Before the Month One Turns 65 |

The Month During Which One Turns 65 |

Up to 3 Months After the Month One Turns 65 |

||||

|

Effective Dates |

|

If one enrolls during one's birthday month, the start date will be the 1st day of the next month. |

The start date will be delayed if one enrolls during the last 3 months of the initial enrollment period.

| |||

|

Example for Someone Turning 65 During the Month of June (The seven-month initial enrollment period would run from March 1 through September 30.) |

If one enrolls in March, April, or May, coverage begins June 1. |

If one enrolls in June, coverage begins July 1. |

| |||

1.

Source: Table prepared by CRS based on Social Security Administration, " “Medicare,"” Publication No. 05-10043, at https://www.ssa.gov/pubs/EN-05-10043.pdf.

a. If one's birthday falls on the 1st of the month, then the enrollment period starts a month earlier and coverage may begin on the 1st day of the month prior to one's birthday month.

. a. Starting in 2023, per changes made by the Consolidated Appropriations Act, 2021 ( P.L. 116-260; Division

CC, §102), the coverage delays for enrol ment during the last three months of the initial enrol ment period wil be eliminated, and coverage wil be effective the first day of the month fol owing the month of enrol ment for enrol ments during any of the last four months of the initial enrol ment period.

b. If one’s birthday fal s on the 1st of the month, then the enrol ment period starts a month earlier and

coverage may begin on the 1st day of the month prior to one’s birthday month.

General Enrollment Period General Enrollment Period

An individual who does not sign up for Medicare during the initial enrollment period must wait

until the next general enrollment period. In addition, persons who decline Part B coverage when first eligible, or terminate Part B coverage, must also wait until the next general enrollment period

25 For additional information on Medicare eligibility for the disabled, see CRS Report RS22195, Social Security Disability Insurance (SSDI) and Medicare: The 24-Month Waiting Period for SSDI Beneficiaries Under Age 65 .

Congressional Research Service

5

link to page 12 Medicare Part B: Enrollment and Premiums

to enroll or reenroll. The general enrollment period lasts for three months from January 1 to March 31 of each year, with coverage beginning on July 1 of that year.26 A late-enrollment

penalty may apply.2527 (See "“Late-Enrollment Premium Penalty and Exemptions"” below.)

Special Enrollment Periods

Certain individuals may be eligible to enroll in Medicare Part B during specific timeframes outside of their initial enrollment period or the annual general enrollment period. For example, a working individual and/or the spouse of a working individual may be able to delay enrollment in

Medicare Part B and enroll during a special enrollment period (SEP) without being subject to the late-enrollment penalty. Delayed enrollment is permitted when an individual aged 65 or older has group health insurance coverage based on the individual'’s (or spouse'’s) current employment (with an employer with 20 or more employees). (In 2019, about 2.1 million of the 4.0 million 2020, about 2.2 mil ion of the 3.8 mil ion working aged population were enrolled in Part A only, with most of the rest enrolled in both Parts A and B.)2628 Delayed enrollment is also permitted for certain disabled persons who have group

health insurance coverage based on their own or a family member'’s current employment with a large group health plan. For the disabled, a large group health plan is defined as one that covers

100 or more employees.

Specifically

Specifical y, persons permitted to delay coverage without penalty are those persons whose Medicare benefits are determined under the Medicare Secondary Payer program.2729 Under Medicare Secondary Payer rules, an employer (with 20 or more employees) is required to offer workers aged 65 and over (and workers'’ spouses aged 65 and over) the same group health insurance coverage that is made available to other employees.2830 The worker has the option of

accepting or rejecting the employer'’s coverage. If he or she accepts the coverage, the employer plan is primary (i.e., pays benefits first) for the worker and/or spouse aged 65 or over, and Medicare becomes the secondary payer (i.e., fillsfil s in the gaps in the employer plan, up to the limits of Medicare'’s coverage). Similarly, a group health plan offered by an employer with 100 or more employees is the primary payer for its employees under 65 years of age, or their dependents, who

are entitled to Medicare because of disability.29

31

26 Starting with the 2023 general enrollment period, coverage will begin the first day of the month after the month of enrollment, per the Consolidated Appropriations Act, 2021 (P.L. 116-260; Division CC, §102). 27 T he Part B general enrollment period is different from the Medicare Advantage and Part D annual enrollment period which runs from October 15 to December 7 each year, with coverage effective the following January.

28 2019 Medicare Working-Aged Beneficiary Counts from CMS 100% Unloaded Enrollment Database. Data provided by CMS, May 2021.

29 Social Security Act §1837(i) and 42 C.F.R. §407.20. See Medicare Publication “Medicare and Other Health Benefits: Your Guide to Who Pays First,” https://www.medicare.gov/Pubs/pdf/02179-Medicare-Coordination-Benefits-Payer.pdf, and CMS, “ Medicare Secondary Payer,” at https://www.cms.gov/Medicare/Coordination-of-Benefits-and-Recovery/Coordination-of-Benefits-and-Recovery-Overview/Medicare-Secondary-Payer/Medicare-Secondary-Payer.html. Also see CRS Report RL33587, Medicare Secondary Payer: Coordination of Benefits. 30 T he requirement that large employers’ coverage pays primary for Medicare-eligible employees was created by the T ax Equity and Fiscal Responsibility Act of 1982 (P.L. 97-248) and amended by the Consolidated Omnibus Budget Reconciliation Act of 1985 (COBRA; P.L. 99-272).

31 For Medicare-eligible beneficiaries employed by organizations with fewer than 20 employees (or fewer than 100 employees for the disabled), Medicare generally pays primary and the employer group health plan generally pays secondary. However, those who are covered under group health plans from employers of any size, based on their own or their spouse’s current employment, will not be subject to the enrollment limitations or late-enrollment penalties for the period of time in which they have group health plan coverage. See SSA, Program Operations Manual System (POMS), HI 00805.751, “ SEP and Premium Surcharge Requirements for the Aged Effective 8/86 ,” at https://secure.ssa.gov/apps10/poms.nsf/lnx/0600805751. Organizations with fewer than 20 employees are not,

Congressional Research Service

6

link to page 12 link to page 12 Medicare Part B: Enrollment and Premiums

Such individuals may sign up for Medicare Part B (or Part A)32Such individuals may sign up for Medicare Part B (or Part A)30 anytime that they (or their spouse) are stil are still working, and they are covered by a group health plan through the employer or union based on that work.31 Additionally33 Additional y, those who qualify for Medicare based on age may sign up during the eight-month period after retirement or the ending of group health plan coverage, whichever happens first. (If an individual'’s group health plan coverage, or the employment on which it is based, ends during the initial enrollment period, that individual would not qualify for a

SEP.)3234 Disabled individuals whose group plan is involuntarily terminated have six months to

enroll without penalty.33

35

For those enrolling during an employment-related SEP, coverage generallygeneral y begins the first of the month following the month of enrollment, and late-enrollment penalties would not apply.3436 Those who qualify for a SEP based on coverage through current employment must provide proof of that

coverage and employment when applying.35

37

Certain international volunteers and individuals eligible for "“equitable relief"” may also qualify for a SEP and an exemption from the late-enrollment penalty. See "“Late-Enrollment Premium Penalty and Exemptions" ” below for additional detail on these circumstances.

Additional y, beginning in 2023, the Consolidated Appropriations Act, 2021 (P.L. 116-260; Division CC,

Section 102) provides the Secretary of HHS the authority to establish special enrollment periods

for beneficiaries who meet “exceptional conditions” that are to be defined by the Secretary.

however, required to offer the same group health insurance to their Medicare-eligible employees that they offer to their other employees. In such cases, small employers may choose to instead offer coverage that wraps around the Medicare benefit or not provide any coverage, and their Medicare-eligible employees may need to enroll in Medicare Part s A and B when first eligible to avoid potential late-enrollment penalties and/or gaps in coverage. Individuals who are turning 65 and still working should check with their employers’ benefit administrator to learn how their employer health coverage works with Medicare. 32 T hose who have a Health Savings Account (HSA) with a high -deductible health plan through one’s own or one’s spouse’s current employment may need to stop contributing to the HSA at least six months prior to applying for Part A in order to avoid a tax penalty. See CRS In Focus IF11425, Health Savings Accounts (HSAs) and Medicare.

33 See Social Security publication “How to Apply for Medicare Part B during Your Special Enrollment Period,” at https://www.ssa.gov/pubs/EN-05-10012.pdf. 34 See “Special Enrollment Period” section of Social Security web page. SSA, “ Retirement Planner: Applying for Medicare Only,” at https://www.ssa.gov/benefits/medicare/.

35 T he Balanced Budget Act of 1997 (BBA; P.L. 105-33) added this exception to the penalty. This exception is for disabled persons (a) who, at the time they first become eligible for Part B, are enrolled in a group health plan (regardless of size) by virtue of their current or former employment and (b) whose continuous enrollment under the plan is involuntarily terminated at a time when their enrollment in the plan is by virtue of their or their spouse’ s former (i.e., not current) employment. These individuals have a special six-month enrollment period beginning on the first day of the month in which the termination occurs. 36 For those who apply while still employed or during the first month of the SEP, coverage may begin the month of enrollment. See SSA publication “Medicare” at https://www.ssa.gov/pubs/EN-05-10043.pdf. 37 T o sign up for Part B while employed or during the 8 months after employment ends, one must complete an “Application for Enrollment in Part B” (CMS-40B) and a “Request for Employment Information” (CMS-L564). Form CMS-40B and instructions for submission may be accessed at https://www.cms.gov/Medicare/CMS-Forms/CMS-Forms/CMS-Forms-Items/CMS017339, and form CMS-L564 and instructions for submission may be found at https://www.cms.gov/Medicare/CMS-Forms/CMS-Forms/CM S-Forms-Items/CMS009718. Under certain circumstances where individuals are unable to obtain evidence from the employer or health plan, alternative documentation may be accepted. For example, see January 28, 2021, question at SSA.gov, Social Security and Coronavirus Disease (COVID-19), “ Can I enroll in Medicare?” at https://www.ssa.gov/coronavirus/.

Congressional Research Service

7

link to page 13 link to page 14 Medicare Part B: Enrollment and Premiums

Late-Enrollment Premium Penalty and Exemptions Late-Enrollment Premium Penalty and Exemptions

Beneficiaries who do not sign up for Part B when first eligible, or who drop it and then sign up again later, may have to pay a late-enrollment penalty for as long as they are enrolled in Part B.36 38 Monthly premiums for Part B may go up 10% for each full 12-month period that one could have had Part B but did not sign up for it. (See "“Calculation of Penalty.".”) Some may be exempt from paying a late-enrollment penalty if they meet certain conditions that allowal ow them to sign up for

Part B during a SEP. (See "“Penalty Exemptions.".”) In 20192020, about 1.4% of Part B enrollees (about 764,000776,200) paid this penalty.3739 On average, their total premiums (standard premium plus penalty)

were about 2827% higher than what they would have been had they not been subject to the penalty.

Those who receive premium assistance through a Medicare Savings Program do not pay the late-enrollment penalty.38 Additionally, 40 Additional y, for those disabled persons under the age of 65 subject to a premium penalty, once the individual reaches the age of 65, he or she qualifies for a new

enrollment period and no longer pays a penalty.

The penalty provision was included in the original Medicare legislation enacted in 1965 to help prevent adverse selection by creating a strong incentive for all eligible al eligible beneficiaries to enroll in Part B.3941 Adverse selection occurs when only those persons who think they need the benefits actuallyactual y enroll in the program. When this happens, per capita costs are driven up and premiums

go up, causing more enrollees (presumably the healthier and less costly ones) to drop out of the program.4042 With most eligible persons over the age of 65 enrolled in Part B, the costs are spread over the majority of this population and per capita costs are less than would be the case if adverse

selection had occurred.

As the Part B late-enrollment penalty is tied to Medicare eligibility and not to access to covered services, individuals who live in areas where Medicare benefits are generallygeneral y not provided, such as outside of the United States or in prison, could still stil be subject to the Part B late-enrollment penalty if they do not sign up for (or if they drop) Part B when eligible.41 To illustrate43 To il ustrate, if a retired Medicare-eligible individual stopped paying Part B premiums while living

38 For more information, see Medicare.gov “Part B Late Enrollment Penalty,” at https://www.medicare.gov/your-medicare-costs/part-b-costs/part-b-late-enrollment-penalty.

39 Figures provided by CMS, May 2021. 40 T he state pays the standard premium regardless of the date the beneficiary first became eligible for Medicare Part B. See SSA, Program Operations Manual System (POMS), Section HI 00815.001, “ State Buy-In Program General Description,” at https://secure.ssa.gov/apps10/poms.nsf/lnx/0600815001; and Ibid., Section HI 00815.039, “Effect of Buy-In on the Individual,” at https://secure.ssa.gov/apps10/poms.nsf/lnx/0600815039.

41 Social Security Act §1839(b). 42 Specifically, adverse selection occurs when beneficiaries, who generally have more information than insurers about their own health status and expected health care needs, make insurance purchasing decisions based on their expect ed use of the insurance benefit. T heir decision to purchase insurance is based on a comparison of the value of the insurance coverage, given their expected use, and the cost of the insurance. Should only (or disproportionately) persons who are high health care users enroll in the program, per capita costs would increase, thereby making the health insurance purchase decision less attractive for healthier, and presumably less costly, beneficiaries who then , in turn, might drop out of the program. Subsequent iterations of this cycle would drive premium costs higher and higher for a smaller and smaller subset of ever sicker and costlier beneficiaries.

43 By comparison, to be eligible for the outpatient prescription drug benefit under Part D, a Medicare beneficiary must reside in a geographic area where a Part D plan is available. Individuals who are incarcerated or who live outside the United States are therefore not eligible to enroll in (or continue enrollment in) Part D. Because the Part D penalty is based on periods when one is eligible but not enrolled, periods of incarceration or extended residence outside of the United States would not be included in that calculation. For example, an individual living outside of the country during his or her initial enrollment period would be given a special enrollment period (SEP) upon returning to the United States and would be able to sign up for Part D at that time without penalty. See SSA, Program Operations Manual

Congressional Research Service

8

Medicare Part B: Enrollment and Premiums

Medicare-eligible individual stopped paying Part B premiums while living overseas for a three-year period and reenrolled when returning to the United States, he or she would not be entitled to a SEP. This individual would instead need to enroll during the general enrollment period and

could also be subject to late-enrollment penalties based on that three-year lapse in coverage.

Additionally,

Additional y, Part B does not have a "creditable"“creditable” coverage exemption similar to that under the Part D outpatient prescription drug benefit.4244 Except for certain circumstances discussed below, having equivalent coverage does not entitle one to a SEP should one decide to enroll in Part B later. For example, an individual who has retiree coverage similar to Part B and therefore decides

not to enroll in Part B when first eligible could be subject to late-enrollment penalties if he or she

enrolls in Part B at a later time (for example, because the retiree coverage was discontinued).

Calculation of Penalty

The late-enrollment penalty is equal to a 10% premium surcharge for each full 12 months of delay in enrollment and/or reenrollment during which the beneficiary was eligible for Medicare.43 45 The period of the delay is equal to (1) the number of months that elapse between the end of the initial initial enrollment period and the end of the enrollment period in which the individual actually actual y

enrolls or (2) for a person who reenrolls, the months that elapse between the termination of

coverage and the close of the enrollment period in which the individual enrolls.

General yenrolls.

Generally, individuals who do not enroll in Part B within a year of the end of their initial

enrollment period would be subject to the premium penalty. For example, if an individual'’s initial enrollment period ended in September 20172018 and the individual subsequently enrolled during the 20182019 general enrollmentenrol ment period (January 1 through March 31), the delay would be less than 12 months and the individual would not be subject to a penalty. However, if that individual delayed enrolling until the 20202021 general enrollment period, the premium penalty would be 20% of that year'

year’s standard premium. (Although the elapsed time covers a total of 30 months of delayed enrollment, the episode includes only two full 12-month periods.) An individual who waits 10

years to enroll in Part B could pay twice the standard premium amount.

The late-enrollment surcharge is calculated as a percentage of the monthly standard premium amount (e.g., $144.60 in 2020),44148.50 in 2021),46 and that amount is added to the beneficiary'’s premium each month. The hold-harmless provision does not provide protection from increases in the penalty amounts. This means that although those who are held harmless in 2020 pay reduced

amounts.47

System (POMS), Section HI 03001.001, “ Description of the Medicare Part D Prescription Drug Program,” at https://secure.ssa.gov/poms.nsf/lnx/0603001001, and CMS Publication, “ Understanding Medicare Part C & D Enrollment Periods,” at https://www.medicare.gov/Pubs/pdf/11219-Understanding-Medicare-Part-C-D.pdf. 44 Under Part D, individuals who have maintained drug coverage equivalent to Medicare’s standard prescription drug coverage prior t o enrolling in Part D are not subject to a late-enrollment penalty. Examples of “ creditable” Part D drug coverage include drug coverage from a former employer or union, T RICARE, the Department of Veteran s Affairs (VA), the Federal Employees Health Benefits Program (FEHBP), or the Indian Health Service. As an illustration, if an individual did not sign up for Part D when first becoming eligible because he or she already had equivalent coverage through a former employer, the individual could sign up for Part D at any time wit hout penalty during the time he or she maintained creditable coverage. Should that coverage end, the individual would be entitled to a special enrollment period and could enroll in Part D without penalty . Beneficiaries who have a break in creditable prescription drug coverage usually have 63 consecutive days to enroll in Part D during a SEP.

45 Social Security Act §1839(b). 46 SSA, Program Operations Manual System (POMS), Section HI 01001.010, “Premium Increase for Late Enrollment,” at https://secure.ssa.gov/poms.nsf/lnx/0601001010. 47 Although those who are held harmless pay reduced premiums, any late-enrollment penalties are calculated as a percentage of the 2020 premium of $144.60 per month.

premium for that year (e.g., in 2021, a percentage of $148.50).

Congressional Research Service

9

link to page 21 Medicare Part B: Enrollment and Premiums

Using the example above in which an individual is subject to a 20% premium penalty, the total

monthly premium in 20202021 would be calculated as follows (see text box):

Calculation of Late-Enrollment Penalty

Example of a 20% penalty in 2020 for an individual who is

Premium Penalty = $144.60 × 20% = $28.92 Example of a 20% penalty in 2021:

Premium Penalty = $148.50 × 20% = $29.70

Penalty-Adjusted Premium

Premium Penalty = $144.60 × 20% = $28.92 Penalty-Adjusted Premium = $140.00** + $28.92 = $168.90* *Premium amounts are rounded to the nearest 10 cents. **Actual premiums of those held harmless in 2020 vary. This dollar figure is used as an example. |

= $148.50 + $29.70 = $178.20

*Premium amounts are rounded to the nearest 10 cents.

For those subject to the high-income premium (see "“Income-Related Premiums"”), the late-enrollment surcharge applies only to the standard monthly premium amount and not to the higher-income adjustment portion of their premiums. Using the example of a 20% penalty for a beneficiary with an income of between $8788,000 and $109111,000, the applicable income-related adjustment of $57.8059.40 would be added on to the penalty-adjusted premium of $173.50 ($144.60 + $28.90178.20 ($148.50 +

$29.70 penalty), for a total monthly premium of $231.30.45

237.60.48

There is no upper limit on the amount of the surcharge that may apply, and the penalty continues to apply for the entire time the individual is enrolled in Part B. Each year, the surcharge is calculated using the standard premium amount for that particular year. Therefore, if premiums

increase in a given year, the dollar value of the surcharge will wil increase as well.

wel . Penalty Exemptions

Under certain conditions, select beneficiaries may be exempt from the late-enrollment penalty. Beneficiaries who are exempt include working individuals (and their spouses) with group coverage, some international volunteers, and those who based their nonenrollment decision on incorrect information provided by a federal representative. Individuals who are permitted to delay enrollment have their own SEPs.

Current Workers

As described above (see "“Special Enrollment Periods"”), some individuals (or their spouse) who are stil are still working and receiving employer-provided health insurance through that employment may qualify for a SEP and not be subject to late-enrollment penalties. Those who fail to enroll during this special enrollment period are considered to have delayed enrollment and thus could be

subject to the penalty.4649 For example, even though an individual may have continued health 48 T hose who pay the high-income premiums are not protected by the hold-harmless provision. For additional information, see SSA, Program s Operation Manual, Section HI 01101.031, “How IRMAA is Calculated and How IRMAA Affects the T otal Medicare Premium,” at https://secure.ssa.gov/apps10/poms.nsf/lnx/0601101031. 49 T hose who are covered under group health plans from employers of any size, based on their own or their spouse’s current employment, will not be subject to the enrollment limitations or late-enrollment penalties for the period of time

Congressional Research Service

10

Medicare Part B: Enrollment and Premiums

may have continued health coverage through the former employer after retirement or have COBRA coverage,4750 he or she must sign up for Part B within eight months of retiring to avoid paying a Part B penalty if he or she eventual yshe eventually enrolls. Individuals who return to work and receive health care coverage through that employment may be able to drop Part B coverage, qualify for a new special enrollment period upon leaving that employment, and reenroll in Part B without penalty as long as

enrollment is completed within the specified time frame.

International Volunteers

Some international volunteers may also be exempt from the Part B late-enrollment penalty. The Deficit Reduction Act of 2005 (P.L. 109-171) permits certain individuals to delay enrollment in Part B without a late-enrollment penalty if they volunteered outside of the United States for at least 12 months through a program sponsored by a tax-exempt organization defined under Section

501(c)(3) of the Internal Revenue Code.4851 These individuals must demonstrate that they had health insurance coverage while serving in the international program.4952 Individuals permitted to delay enrollment have a six-month SEP, which begins on the first day of the first month they no

longer qualify under this provision.

Equitable Relief

Under certain circumstances, a SEP may be created and/or late-enrollment penalties may be waived if a Medicare beneficiary can establish that an error, misrepresentation, or inaction of a federal worker or an agent of the federal government (such as an employee of the Social Security Administration, CMS, or a Medicare administrative contractor) resulted in late Part B enrollment.5053 To qualify for an exception under these conditions, the beneficiary must provide

documentary evidence of the error, which "“can be in the form of statements from employees, agents, or persons in authority that the allegedal eged misinformation, misadvice, misrepresentation,

inaction, or erroneous action actually occurred."51

actual y occurred.”54

Time-limited equitable relief also may be granted for certain categories of individuals. For example, CMS may provide a special enrollment period to those affected by a weather-related emergency or a major disaster.5255 As described below, during the Coronavirus Disease 2019 (COVID-19)COVID-19 public health emergency, certain individuals who were not able to enroll in Part B in a timely manner are being allowedwere al owed additional time to enroll under equitable relief (through June 17, 2020. Additionally,

2020). Additional y, CMS determined that it did not provide adequate information regarding Part

in which they have group health plan coverage. See SSA, Program Operations Manual System (POMS), HI 00805.751, “SEP and Premium Surcharge Requirements for the Aged Effective 8/86,” at https://secure.ssa.gov/apps10/poms.nsf/lnx/0600805751.

50 For a description of COBRA, see CRS Report R40142, Health Insurance Continuation Coverage Under COBRA. 51 Social Security Act §1837(k) and 42 C.F.R. §407.21. 52 See SSA, Program Operations Manual System (POMS), Section HI 00805.355, “Evidentiary Requirements for the SEP or Premium-Surcharge Rollback for International Volunteers,” at https://secure.ssa.gov/apps10/poms.nsf/lnx/0600805355. 53 Social Security Act §1837(h) and 42 C.F.R. §407.32. 54 For additional information, see SSA, Program Operations Manual System (POMS), Section HI 00805.170, “Conditions for Providing Equitable Relief,” at https://secure.ssa.gov/poms.nsf/lnx/0600805170, and Ibid, Section HI 00805.175, “Evidence of Government Error or Delay ,” at https://secure.ssa.gov/poms.nsf/lnx/0600805175.

55 See SSA, Program Operations Manual System (POMS), Section HI 00805.324, “Equitable Relief for Enrollment Request Affected by Major Disasters,” at https://secure.ssa.gov/apps10/poms.nsf/lnx/0600805324.

Congressional Research Service

11

Medicare Part B: Enrollment and Premiums

CMS determined that it did not provide adequate information regarding Part B enrollment to certain individuals with exchange coverage who enrolled in Medicare Part A and is allowing

al owed equitable relief to these individuals (through June 2020.

).

Limited Time Medicare Enrollment Equitable Relief Equitable Relief During the COVID-19 Pandemic-Related National Emergency

National Emergency Beneficiaries who were not able to enroll in Part B in a timely manner as a result of local Social Security field office closures during the COVID-19 public health emergency may bewere granted certain enrollment flexibilities under equitable relief.53 Specifically, CMS is granting56 Specifical y, CMS granted equitable relief in the form of additional time to enroll during one'’s initial enrollment period, during the annual general

enrollment period, or during a special enrollment period (SEP), such as the 8-month period when a beneficiary'’s employer coverage based on current employment ends. Beneficiaries arewere eligible for this equitable relief only if they had an initial enrollment period, general enrollment period, or SEP during the period from March 17, 2020 through June 17, 2020, and the beneficiary did not apply for Part B during that enrollment period. Eligible beneficiaries who wishwanted to use this

equitable relief to enroll in Part B mustneeded to file their enrollment request by June 17, 2020.54 Coverage will be Coverage was effective the month that would have been applicable had the application been filed

at the time of the individual'’s original (but missed) initial, general, or special enrollment period.

Limited Time Equitable Relief Relief for Individuals with Medicare Part A and Exchange Coverage

CMS generally

CMS general y encourages those who have coverage through an individual exchange (also known as marketplace) plan, and subsequently become eligible for Medicare, to drop the exchange

coverage and enroll in Medicare during their initial enrollment period. After an individual has become eligible for Medicare Part A, any tax credits and cost-sharing reductions that that individual individual receives through an exchange plan ends.5557 CMS recognized that "“these individuals did not receive the information necessary at the time of their Medicare [initial enrollment period], Part B SEP for the working aged or disabled, or initial enrollment in the Exchange to make an

informed decision regarding their Part B enrollment."56”58 This may have resulted in these individuals individuals not enrolling in Part B, or enrolling in Part B late and being subject to a late

enrollment penalty.

CMS is thus offering

CMS thus offered time-limited equitable relief through June 30, 2020, for certain individuals enrolled in both premium-free Medicare Part A and in a plan provided through the health insurance exchanges.57 Specifically, those who are currently, or had previously been,59 Specifical y, those who had been enrolled in an exchange plan and in premium-free Medicare Part A, and had a Part A entitlement date that began on or after July 1, 2013 (or a Part B SEP that ended on or after October 1, 2013) may enroll in Part B without penalty through June 30, 2020. Additionally, the Part B late enrollment penalties of those who had both Part A and exchange coverage and signed up for Part B outside of their initial enrollment period may be reduced or eliminated. To request this equitable relief, qualifying individuals must contact the Social Security Administration and provide appropriate documentation indicating that they were enrolled in an exchange plan and eligible for Medicare during the specified period.58

could enroll in Part B without

56 See CMS, “Enrollment Issues for COVID-19 Pandemic-Related National Emergency, Questions and Answers for Medicare Beneficiaries,” at https://www.cms.gov/files/document/enrollment-issues-covid-ab-faqs.pdf. 57 CMS indicates that in this instance, the individual should contact the marketplace at least 15 days before the date one wants the coverage to end. 58 CMS Factsheet, “Assistance for Individuals with Medicare Part A and Exchange Coverage Infor mation for SHIPs and Exchange Assisters,” October 2019, https://www.cms.gov/Medicare/Eligibility-and-Enrollment/Medicare-and-the-Marketplace/Downloads/SHIP-Navigator-Fact-Sheet -2019.pdf.

59 Individuals who paid a premium for Medicare Part A were not eligible for this equitable relief, as they are required to enroll in Part B in order to enroll in Part A. T hose enrolled in a Marketplace Small Business Health Options Program (SHOP) plan were also not eligible for this equitable relief, as such plans are considered employer sponsored plans and, as described earlier, these individuals already qualify for a special enrollment period once that coverage ends.

Congressional Research Service

12

link to page 27 link to page 27 Medicare Part B: Enrollment and Premiums

penalty through June 30, 2020. Additional y, the Part B late enrollment penalties of those who had both Part A and exchange coverage and signed up for Part B outside of their initial enrollment

period could have been reduced or eliminated.

Collection of the Part B Premium Collection of the Part B Premium

Part B premiums may be paid in a variety of ways.5960 If an enrollee is receiving Social Security or Railroad Retirement benefits,6061 the Part B premiums must, by law, be deducted from these

benefits. Additionally, Additional y, Part B premiums are deducted from the benefits of those receiving a Federal Civil Service Retirement annuity.6162 The purpose of collecting premiums by deducting them from benefits is to keep premium collection costs at minimum. This withholding does not apply to those beneficiaries receiving state public assistance through a Medicare Savings Program because their premiums are paid by their state Medicaid program. (See "“Premium Assistance for

Low-Income Beneficiaries.")

.”)

Part B enrollees who do not receive monthly Social Security, Railroad Retirement, or Civil Service Retirement benefits, or assistance through a Medicare Savings Program, pay premiums

directly to CMS.62

63 Deduction of Part B Premiums from Social Security Checks

By law, a Social Security beneficiary who is enrolled in Medicare Part B must have the Part B premium automaticallyautomatical y deducted from his or her Social Security benefits.6364 Automatic deduction from the Social Security benefit check also applies to Medicare Advantage participants who are enrolled in private health care plans in lieu of traditional Medicare.6465 In instances in which a beneficiary'beneficiary’s monthly Social Security benefit is not sufficient to cover the entire Part B premium

amount, Medicare may bill bil the beneficiary for the balance.65 In 201966 In 2020, about 68% of Medicare Part B enrollees (41.7 millionmil ion) had their Part B premiums deducted from their Social Security benefit checks.66

checks.67

Social Security beneficiaries who do not pay Medicare Part B premiums include those who are under the age of 65 and do not yet qualify for Medicare (e.g., began receiving Social Security

60 SSA, Program Operations Manual System (POMS), Section HI 01001.020, “ Collection of Premiums,” at https://secure.ssa.gov/poms.nsf/lnx/0601001020.

61 Social Security Act §1840(a)(1) and §1840(b)(1). See CRS Report R42035, Social Security Primer, and CRS Report RS22350, Railroad Retirem ent Board: Retirem ent, Survivor, Disability, Unem ploym ent, and Sickness Benefits.

62 See CRS Report 98-810, Federal Employees’ Retirement System: Benefits and Financing . 63 42 C.F.R. §408.60. 64 Social Security Act §1840(a)(1). 65 Beneficiaries who receive their Parts A and B benefits through Medicare Advantage (MA, Part C), must still pay the monthly Part B premium, but may pay different amounts. For example, some MA plans may offer an additional benefit by reducing t he amount one pays for the Part B premium. Alternatively, some MA plans may be more expensive than traditional Medicare, for example because they provide benefits beyond what is provided under traditional Medicare, and may charge a premium in addition to t he Part B premium. T he Social Security Administration has in place a “safety net” to prevent the deduction of more than $300 of Part C and Part D plan premiums from a single Social Security check. For amounts over $300, the enrollee may be billed directly.

66 SSA, Program Operations Manual System (POMS), Section HI 01001.041, “Collection from Beneficiaries When the Amount of the Benefit Payment is Less than the Amount of the Premium ,” at https://secure.ssa.gov/apps10/poms.nsf/lnx/0601001041.

67 Figures provided by CMS, May 2021.

Congressional Research Service

13

link to page 29 link to page 29 Medicare Part B: Enrollment and Premiums

under the age of 65 and do not yet qualify for Medicare (e.g., began receiving Social Security benefits at the age of 62); receive low-income assistance from Medicaid to pay the Part B premium; have started to receive Social Security disability insurance (SSDI) but are not eligible for Medicare Part B because they have not received SSDI for 24 months; or chose not to enroll in

Medicare Part B.

The amount of an individual'’s Social Security benefits cannot go down from one year to the next as a result of the annual Part B premium increase, except in the case of higher-income individuals subject to income-related premiums. (See "“Protection of Social Security Benefits from Increases in Medicare Part B Premiums.".”) For those beneficiaries "“held harmless,"” the dollar amount of

their Part B premium increases would be held below or equal to the amount of the increase in

their monthly Social Security benefits.

Part B Enrollees Who Do Not Receive Social Security Benefits

A small A smal percentage of Medicare Part B enrollees do not receive Social Security benefits. For example, some individuals aged 65 and older may have deferred signing up for Social Security for various reasons, for instance if they have not yet reached their full Social Security retirement age67age68 or are still stil working. Additionally, Additional y, certain persons who spent their careers in employment

that was not covered by Social Security—including certain federal, state, or local government workers and certain other categories of workers—do not receive Social Security benefits but may still stil qualify for Medicare. For those who receive benefit payments from the RRB68RRB69 or the Civil Service Retirement System (CSRS),6970 Part B premiums are deducted from the enrollees'’ monthly benefit payments. While RRB retirement benefit amounts are protected by the hold-harmless

provision, CSRS benefits are not held harmless from annual increases in the Part B premium.

For those who do not receive these types of benefit payments, Medicare will generally bill wil general y bil directly for their premiums every three months.7071 The enrollee who is being billed bil ed does not

necessarily have to pay his or her own premiums; premiums may be paid by the enrollee, a relative, friend, organization, or anyone else.71 72 In cases where an organization wants to be billed bil ed for the Part B premiums of a number of Medicare beneficiaries, it may enter into a formal group-billing bil ing arrangement with CMS.7273 Those approved as group billersbil ers include such entities as city and

county governments, state teacher retirement systems, and certain religious orders.

68 See CRS Report R44670, The Social Security Retirement Age. 69 Social Security Act §1840(b)(1). 70 Generally, employees of the federal government hired before 1984 are covered by the Civil Service Retirement System (CSRS) and are not covered by Social Security. Most federal workers first hired into federal service on or after January 1984 participate in the Federal Employees’ Retirement System (FERS), which includes Social Security coverage. However, the T ax Equity and Fiscal Responsibility Act (P.L. 97-248) enabled federal workers to be eligible for Medicare based on their federal employment . See CRS Report R42741, Laws Affecting the Federal Em ployees Health Benefits (FEHB) Program . 71 Payment may be made by check, money order, or credit card; alternatively, one may schedule a payment to be automatically deducted from one’s bank account. Premium billing form and information may be found at https://www.medicare.gov/forms-help-resources/mail-you-get-about -medicare/medicare-premium-bill-cms-500.

72 SSA, Program Operations Manual System (POMS), Section HI 01001.225, “When Premium Notices May Be Sent to an Individual Other T han an Enrollee,” at https://secure.ssa.gov/apps10/poms.nsf/lnx/0601001225.

73 SSA, Program Operations Manual System (POMS), Section HI 01001.230, “Group Collection-General,” at https://secure.ssa.gov/poms.nsf/lnx/0601001230.

Congressional Research Service

14

link to page 21 link to page 12 link to page 12 link to page 21 link to page 29 link to page 29 link to page 40 Medicare Part B: Enrollment and Premiums

Nonpayment of premiums results in termination of enrollment in the Part B program, although a grace period (through the last day of the third month following the month of the due date) is allowed

al owed for beneficiaries who are billedbil ed and pay directly.73

74 Determining the Part B Premium

Each year, the CMS actuaries estimate total per capita Part B costs for beneficiaries aged 65 and older over for the following year and set the Part B premium to cover 25% of expected Part B expenditures.74

expenditures.75 However, because prospective estimates may differ from the actual spending for the year, contingency margin adjustments are made to ensure sufficient income to accommodate potential variation in actual expenditures during the year. (See "“Contingency Margin.".”) The Part B premium is a single national amount that does not vary with a beneficiary'’s age, health status, or place of residence. Premiums may be adjusted upward for late enrollment (see "Late-“Late-

Enrollment Premium Penalty and Exemptions”") and for beneficiaries with high incomes (see "“Income-Related Premiums”"), or they may be adjusted downward for those protected by the hold-harmless provision (see "“Protection of Social Security Benefits from Increases in Medicare Part B Premiums").

Premiums”).