Addressing the Long-Run Deficit: A Comparison of Approaches

Changes from May 14, 2019 to June 7, 2022

This page shows textual changes in the document between the two versions indicated in the dates above. Textual matter removed in the later version is indicated with red strikethrough and textual matter added in the later version is indicated with blue.

Addressing the Long-Run Deficit: A Comparison of Approaches

Contents

- Introduction

- The Long-Run Budget: An Overview

- Long-Run Budget Issues: Overview

- Federal Spending: Patterns over Time

- Addressing the Long-Run Deficit:

June 7, 2022

A Comparison of Approaches

Jane G. Gravelle

The growth of the national debt, which is considered unsustainable under current policies,

Senior Specialist in

continues to be one of the central issues of domestic federal policymaking.

Economic Policy

Addressing a federal budget deficit that is unsustainable over the long run involves choices.

Donald J. Marples

Fundamentally, the issues require deciding what government goods, services, and transfers are

Specialist in Public Finance

worth paying taxes for. Most people would agree that the country benefits from a wide range of

government services—air traffic controllers, border security, courts and corrections, and so forth—provided by the federal government. Yet federal government provision of goods and

services comprises only a modest portion of the federal budget. Transfers, including interest payments, account for around 75% of the federal budget.

Central findings of this analysis include the following:

A comparatively small share of federal spending is for the direct provision of domestic government goods

and services.

Transfers and payments to persons and to state and local governments constitute most of federal spending,

about 75% of all federal spending.

Defense spending, accounting for about 15% of federal spending, has declined as a share of output over the

past 35 years, but it also tends to vary depending, in part, on the presence and magnitude of international conflicts.

The problem with the debt lies not in the past but in the future, as growth in spending for health and Social

Security is projected to continue faster than the economy as a whole. The increase in deficits and debt, in turn, leads to a significant increase in interest payments.

Because much of the pressure on future spending arises from imbalances in Social Security and Medicare

Part A (Hospital Insurance) trust funds, keeping these funds and their sources of financing intact is a concern that could constrain choices.

Preserving entitlements would likely require significant increases in taxes, such as raising rates, reducing

tax expenditures, increasing other taxes, or introducing new revenue sources.

Reductions in discretionary spending are insufficient to reduce the deficit to a sustainable level, so limiting

taxes as a percentage of output or constraining the overall size of the government to current levels would likely require significant cuts in mandatory spending, including entitlement programs such as Social Security, Medicare, and Medicaid.

Because the federal government provides about one-fifth of the revenue for state and local governments,

cutbacks in transfers to these governments may, in part, shift the burden of providing services from the national to subnational governments rather than altering the overall size of government services.

Congressional Research Service

link to page 5 link to page 5 link to page 6 link to page 8 link to page 9 link to page 9 link to page 11 link to page 14 link to page 15 link to page 15 link to page 17 link to page 17 link to page 19 link to page 21 link to page 22 link to page 24 link to page 24 link to page 24 link to page 26 link to page 27 link to page 27 link to page 28 link to page 28 link to page 29 link to page 30 link to page 33 link to page 5 link to page 9 link to page 9 link to page 12 link to page 12 link to page 14 link to page 14 link to page 16 link to page 21 link to page 22 link to page 23 link to page 23 Addressing the Long-Run Deficit: A Comparison of Approaches

Contents

Introduction ..................................................................................................................................... 1 The Long-Run Budget: An Overview ............................................................................................. 1 Long-Run Budget Issues: Overview ............................................................................................... 2 Federal Spending: Patterns over Time ............................................................................................. 4

Distribution of Spending by Fundamental Economic Form: Government Goods and

Distribution of Spending by Fundamental Economic Form: Government Goods and Services Versus Transfers - Distribution of Federal Spending by Mandatory and Discretionary Categories

- Distribution of Spending by Function

- Federal Taxes: Patterns over Time

- Tax Revenues

- Tax Structure

- Tax Expenditures

- Earmarked Revenues and Trust Funds

- Growth in the Debt

- Deficit Challenges Going Forward

- Addressing the Long-Run Deficit

- The Timing of Deficit Reductions

- Deficits Under Alternative Baselines

- Deficit Reduction Strategies

- Challenges to Reducing Budget Deficits

- How Much Can Discretionary Spending Cuts Reduce the Budget Deficit?

- Are Social Security and Medicare Hospital Insurance Trust Funds to Be Preserved?

- Services Versus Transfers ....................................................................................................... 5

Distribution of Federal Spending by Mandatory and Discretionary Categories ....................... 7 Distribution of Spending by Function ..................................................................................... 10

Federal Taxes: Patterns over Time .................................................................................................. 11

Tax Revenues ........................................................................................................................... 11 Tax Structure ........................................................................................................................... 13 Tax Expenditures ..................................................................................................................... 13 Earmarked Revenues and Trust Funds .................................................................................... 15

Growth in the Debt ........................................................................................................................ 17 Deficit Challenges Going Forward ................................................................................................ 18 Addressing the Long-Run Deficit ................................................................................................. 20

The Timing of Deficit Reductions ........................................................................................... 20 Deficits Under Alternative Baselines ...................................................................................... 20 Deficit Reduction Strategies ................................................................................................... 22 Challenges to Reducing Budget Deficits ................................................................................ 23

How Much Can Discretionary Spending Cuts Reduce the Budget Deficit? ..................... 23 Are Social Security and Medicare Hospital Insurance Trust Funds to Be

Preserved? ...................................................................................................................... 24

Can Long-Run Budget Issues Be Addressed by Keeping Tax Levels Constant? ............. 25

Can Long-Run Budget Issues Be Addressed by Keeping Tax Levels Constant? - What Would Be Required to Protect Entitlements? A Review of Tax Options

- Effects on State and Local Governments

Figures

- ................. 26 Effects on State and Local Governments .......................................................................... 29

Figures Figure 1. Federal Revenue and Spending,

FY1969-FY2018 as a %FY1970-FY2021, as a Percentage of GDP................... 1of GDP - Figure 2. Federal Spending by Economic Form,

CY1968-CY2018 as a % of GDP - CY1970-CY2021, as a Percentage of

GDP .............................................................................................................................................. 5

Figure 3. Federal Spending by Budget Category,

FY1969-FY2018 as a % of GDP - FY1970-FY2021, as a Percentage of

GDP .............................................................................................................................................. 8

Figure 4. Federal Spending by Functional Form,

FY1969-FY2018 as a % of GDP - Figure 5. Federal Revenues, FY1969-FY2018 as a % of GDP

- Figure 6. Federal Debt, FY1969-FY2023 as a % of GDP

- Figure 7. Federal Revenues and Spending, FY1968-FY2048 as a % of GDP

- Figure 8. Federal Spending, Selected Years FY1968-FY2048 as a % of GDP

- Figure 9. Federal Revenues, Selected Years FY1968-FY2048 as a % of GDP

Tables

- Table 1. Fiscal Situation, FY2018 as a % of GDP

- Table 2. Federal Spending by Fundamental Form, CY1980, CY2007, and CY2018 as a % of GDP

- FY1970-FY2021, as a Percentage of

GDP ............................................................................................................................................ 10

Figure 5. Federal Revenues, FY1970-FY2021, as a Percentage of GDP ...................................... 12 Figure 6. Federal Debt, FY1970-FY2027, as a Percentage of GDP.............................................. 17 Figure 7. Federal Revenues and Spending, FY1970-FY2051, as a Percentage of GDP ............... 18 Figure 8. Federal Revenue and Spending, Selected Years FY2006-FY2051, as a

Percentage of GDP ..................................................................................................................... 19

Congressional Research Service

link to page 6 link to page 11 link to page 11 link to page 13 link to page 13 link to page 14 link to page 14 link to page 18 link to page 18 link to page 20 link to page 20 link to page 20 link to page 20 link to page 25 link to page 25 link to page 26 link to page 26 link to page 34 Addressing the Long-Run Deficit: A Comparison of Approaches

Tables Table 1. Fiscal Situation, FY2020, as a Percentage of GDP ........................................................... 2 Table 2. Federal Spending by Fundamental Form, CY1980, CY2007, CY2019, and

CY2021, as a Percentage of GDP ................................................................................................ 7

Table 3. Federal Spending by Mandatory and Discretionary Categories, FY1980,

FY2007, and FY2019, as a Percentage

Table 3. Federal Spending by Mandatory and Discretionary Categories, FY1980, FY2007, and FY2018 as a % of GDP Tableof GDP ........................................................................... 9 Table 4. Federal Spending by Functional Form, FY1980, FY2007, andFY2018 as a %FY2019, as a Percentage of GDP .............................................................................................................. 10of GDP- Table 5. Federal Spending and Tax Expenditures by Function,

FY2018 as a % of GDP - FY2019, as a Percentage

of GDP ....................................................................................................................................... 14

Table 6. Financing and Benefits in the Social Security and Medicare Hospital Insurance

Trust Funds, FY1973, FY2007, and

FY2018FY2019, as a%Percentage of GDP ..................................... 16of GDP - Table 7. Supplementary Medical Insurance Trust Fund Income and Outflow, FY1973,

FY2007, and

FY2018FY2019, as a%Percentage of GDP ......................................................................... 16of GDP - Table 8. Long-Run Federal Budget Projections Under Extended and Alternative Extended

Baselines, FY2018, FY2028, and FY2038, as a

%Percentage of GDP ......................................... 21 Table 9. Projected Budgetary Effects of Alternative Budget Plans in FY2040 as a Percentage of GDP .............................................................................................................. 22 Contacts Author Information ........................................................................................................................ 30 Congressional Research Service link to page 5 Addressing the Long-Run Deficit: A Comparison of Approaches Introductionof GDP - Table 9. Projected Budgetary Effects of Alternative Budget Plans in FY2040 as a % of GDP

Summary

The growth of the national debt, which is considered unsustainable under current policies, continues to be one of the central issues of domestic federal policymaking.

Addressing a federal budget deficit that is unsustainable over the long run involves choices. Fundamentally, the issues require deciding what government goods, services, and transfers are worth paying taxes for. Most people would agree that the country benefits from a wide range of government services—air traffic controllers, border security, courts and corrections, and so forth—provided by the federal government. Yet federal government provision of goods and services comprises only a modest portion of the federal budget. Transfers, including interest payments, accounted for around 75% of the federal budget.

Central findings of this analysis include the following:

- A comparatively small share of federal spending is for the direct provision of domestic government goods and services.

- Transfers and payments to persons and to state and local governments constitute most of federal spending, about 75% of all federal spending.

- Defense spending, accounting for about 15% of federal spending, has declined as a share of output over the past 35 years, but it also tends to vary depending, in part, on the presence and magnitude of international conflicts.

- The problem with the debt lies not in the past but in the future, as growth in spending for health and Social Security is projected to continue faster than the economy as a whole. The increase in deficits and debt, in turn, leads to a significant increase in interest payments.

- Because much of the pressure on future spending arises from imbalances in Social Security and Medicare Part A (Hospital Insurance) trust funds, keeping these funds and their sources of financing intact is a concern that could constrain choices.

- Preserving entitlements would likely require significant increases in taxes, such as raising rates, reducing tax expenditures, increasing other taxes, or introducing new revenue sources.

- Reductions in discretionary spending are insufficient to reduce the deficit to a sustainable level, so limiting taxes as a percentage of output or constraining the overall size of the government to current levels would likely require significant cuts in mandatory spending, including entitlement programs such as Social Security, Medicare, and Medicaid.

- Because the federal government provides about one-fifth of the revenue for state and local governments, cutbacks in transfers to these governments may, in part, shift the burden of providing services from the national to subnational governments rather than altering the overall size of government services.

Introduction

The growth of the national debt, which is considered unsustainable under current policies, continues to be one of the central issues of domestic federal policymaking.

This report examines alternative approaches to reducing annual budget deficits and decisions about how to bring the national debt under control over the long term. To do this, the report first examines historical trends in federal spending and revenue policy to illustrate both the challenges and trade-offs inherent to making choices between (1) limiting the provision of defense and domestic public goods, (2) reducing transfers to persons including entitlements for the elderly and those with low income, (3) reducing support for state and local governments, and (4) raising taxes. Using projections of the debt and deficit, the report then addresses how limiting reliance on one source of deficit reduction creates pressure on other sources.

The Long-Run Budget: An Overview

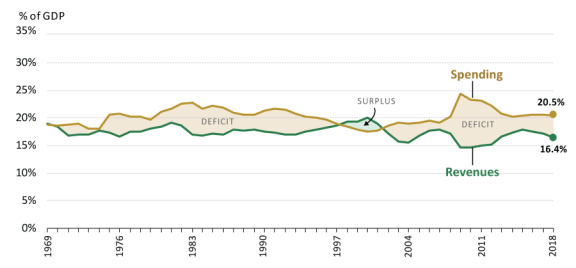

The federal government incurs a budget deficit when total spending exceeds revenues over the course of a fiscal year.11 Over the past 50 years, the federal government has, on average, run budget deficits of 2.9% of gross domestic product (GDP), though as seen inin Figure 1, thethe amount has fluctuated from a surplus of 2.3% of GDP in 2000 to a deficit of 9.814.9% of GDP in 2020.

% of GDP in 2009.

May 2022. A portion of the budget outcomes is a function of general economic conditions, and the remainder is a function of policy choices. For example, deficits tend to rise during recessions (through a combination of decreased revenues and increased spending on programs like unemployment), whereas the opposite is generally true during economic expansions. Policy choices, such as the decline in defense spending after the dissolution of the Soviet Union in 1991, may change the budget situation due to changes in national priorities.

Spending rose significantly during the

1 See CRS Report R45202, The Federal Budget: Overview and Issues for FY2019 and Beyond, by Grant A. Driessen, for detailed information on the federal budget.

Congressional Research Service

1

link to page 6 Addressing the Long-Run Deficit: A Comparison of Approaches

COVID-19 pandemic in 2020 to support individuals and businesses adversely affected by measures taken to limit the spread of the virus by governments, businesses, and individuals.

The accumulation of net deficits over time results in the federal debt. As shown inin Table 1, the the cumulative federal debt in 2018FY2020 was 78100% of GDP.

% of GDP.

Table 1. Fiscal Situation, FY2018FY2020, as a %Percentage of GDP

FY2020

Spending

31.2%

Revenue

16.3%

Deficit

14.9%

Debt

100.1%

Source: CBO Historical Budget Data, February 2021.

of GDP

|

FY2018 |

|

|

Spending |

20.3 |

|

Revenue |

16.4 |

|

Deficit |

3.9 |

|

Debt |

77.8 |

Source: CBO Historical Budget Data, January 2019.

Of concern is that the federal budget deficit has resulted in the growth of the federal debt that has regularly exceeded the growth rate of the economy. The debt can grow without increasing the ratio of debt to GDP as long as it rises at a rate less than or equal to GDP growth. For example, if the debt is 80% of GDP, as was the case prior to the pandemic, and the economy is growing at 1.6%, a deficit of 1.28% of GDP (1.6% of 80%) will maintain the debt-to-GDP ratio. The FY2018 FY2019 deficit is 4was 4.6% of GDP—a situation viewed by most economists as unsustainable.2

2 The response to the COVID-19 pandemic, while transitory, accelerated the growth in the debt-to-GDP ratio to 100%, which means a smaller deficit would be needed to return the ratio to 80%.

Long-Run Budget Issues: Overview Long-Run Budget Issues: Overview

Addressing a federal budget deficit that is unsustainable over the long run involves strategic choices.33 Fundamentally, the issues require deciding what government goods, services, and transfers are worth paying taxes for. Most people would agree that the country benefits from a wide range of government services—air traffic controllers, border security, courts and corrections, and so forth—provided by the federal government. Yet, as shown below, in 2007, the federal government provision of goods and services, outside of defense, constituted 10% of federal spending and 2% of GDP. Transfers, including interest payments, accounted for around 70% of the federal budget. Finding budget savings by reducing nondefense federal government services alone would fall short of what is needed to address the deficit.

In 2018

2 Some economists have argued that the growing level of debt will not only interfere with economic growth, but lead to a fiscal crisis where the United States loses access to credit markets. Others have suggested that too much attention is currently placed on the long-run outlook for the debt, particularly given low interest rates, and concerns about the long-run debt have limited worthwhile investments in education, infrastructure, and health and that these low interest rates mean that these fiscal constraints can be ignored. See Jason Furman and Lawrence H. Summers, “Who’s Afraid of Budget Deficits?” Foreign Affairs, March/April 2019, at https://www.foreignaffairs.com/articles/2019-01-27/whos-afraid-budget-deficits, for a discussion of these issues. They point out that there is no evidence that the United States will face a fiscal crisis but acknowledge that the debt cannot be allowed to grow forever. They suggest a middle road of ensuring that new spending and tax cuts do not add to the deficit in nonrecession years and that existing public services over time will require more revenues.

3 For further discussion of the unsustainability of the federal budget trajectory, see Congressional Budget Office (CBO), The 2021 Long-Term Budget Outlook, March 4, 2021, https://www.cbo.gov/publication/56977.

Congressional Research Service

2

Addressing the Long-Run Deficit: A Comparison of Approaches

In 2019, the latest year before the pandemic, transfers, including interest payments, accounted for 76% of the federal budget, up from 70% in 2007. Outside of the 9% provision for domestic goods, defense spending for goods and services constitutes about 15% of federal spending.4 In this area as well, there are limits to the savings that might be found without compromising national security. Therefore, to address the budget shortfalls facing the country over the long run, it is likely that (1) transfer payments, such as Social Security, Medicare, and Medicaid, to or on behalf of individuals (which already account for half of federal spending and are growing) must be reduced; (2) transfers to state and local governments must be reduced (which would shift the budget decisions to a different level of government); (3) taxes must be raised; or some combination of the three.

The next section of this report examines the government'’s spending allocation, the method of its financing, and how these shares and sources have changed over time. It demonstrates that the surge in the debt is a recent phenomenon that has occurred with the recession and is inherently transitory. Going forward, however, as shown in the subsequent section, the growth in transfers to the elderly and spending for health care—a trend that has been under way for some time but was offset by a decline in spending for other purposes, relative to GDP—will increasingly contribute to unsustainable deficits. The following section addresses philosophies for approaching deficit reduction, as embodied in a number of proposals. It discusses how different approaches to and constraints imposed on deficit reduction will have consequences for the menus of other available choices. For example, if deficit reduction begins with a constraint that taxes will not rise, policy would almost certainly require significant cutbacks in Social Security and Medicare. If the benefits of these programs are to be maintained, an increase in taxes would likely be required.

Central findings of this analysis include the following:

-

A comparatively small share of federal spending is for the direct provision of

domestic government goods and services.

- Transfers and payments to persons and to state and local governments constitute most of federal spending, about 75% of all federal spending.

- Defense spending, accounting for about 15% of federal spending, has declined as a share of output over the past 35 years, but it also tends to vary depending, in part, on the presence and magnitude of international conflicts.

- The problem with the debt lies not in the past but in the future, as spending growth for health and Social Security is projected to continue faster than the economy as a whole. The increase in debt, in turn, leads to a significant increase in interest payments.

-

Because much of the pressure on future spending arises from imbalances in

Social Security and Medicare Part A (Hospital Insurance) trust funds, keeping these funds and their sources of financing intact is a concern that could constrain choices.

- Preserving entitlements would likely require significant increases in taxes, such as raising rates, reducing tax expenditures, increasing other taxes, or introducing new revenue sources.

- Reductions in discretionary spending are insufficient to reduce the deficit to a sustainable level; thus, limiting taxes as a percentage of output or constraining the overall size of the government to current levels would likely require 4 Transfers rose during the pandemic, constituting 83% of spending in 2021, but this increase is temporary. Congressional Research Service 3 Addressing the Long-Run Deficit: A Comparison of Approaches significant cuts in mandatory spending, including entitlement programs such as Social Security, Medicare, and Medicaid.

- Because the federal government provides about one-fifth of the revenue for state and local governments, cutbacks in transfers to these governments may, in part, shift the burden of providing services from the national to subnational governments rather than altering the overall size of government services.

Federal Spending: Patterns over Time

The objectives of government spending and taxes are generally viewed as providing for public and quasi-public goods,45 such as defense, law enforcement, infrastructure, and education; correcting market failures,56 including externalities (both negative, such as pollution, and positive, such as research and development); achieving distributive justice; and managing business cycles. Measured by the amount of spending, defense is the most important pure public good the federal government provides. Many public and quasi-public goods, as well as income-support programs, are provided by state and local governments, and some federal spending is through grants to state and local governments for these programs. For example, in FY2016FY2019, state governments received 29.126.7% of total revenues from federal transfers, and local governments received 3.8%.64%.7 States also provide transfers to local governments, and local governments provide transfers among themselves as well. These intergovernmental transfers are important in evaluating budget proposals, because a reduction in transfers to state and local governments may in large part shift the burden to these governments rather than reduce the overall government role.

Spending in the U.S. budget can be divided in various ways that are relevant to considering deficit reduction. In the discussion that follows, government spending is divided by whether the spending is to provide public goods or transfers, whether it is discretionary or mandatory (and the major categories within those divisions), and by function. The first approach to presenting spending distinguishes between the provision of goods and services (defense and nondefense) and transfers to persons or to state and local governments. This approach is not a typical way of presenting budget data. It is important to divide spending in this way, however, to address concerns about potential inefficiency in federal government operations, especially outside of defense, as it indicates the scope for cutbacks relative to the deficit. The second approach divides spending into discretionary (provided in annual appropriations acts) and mandatory (controlled by permanent laws, and including entitlements to benefits). It is associated with the procedures needed to alter spending. The third, a common way of presenting budget data, divides spending by function (defense, education, energy, health, etc.). Later, this section also discusses trends in

5 A pure public good is one for which there is no marginal cost to an additional consumer and is non-excludible. The classic example is a lighthouse, but the most important one in terms of federal spending is national defense. Quasi-public goods do not necessarily have these pure characteristics, but they experience large spillover effects. For example, it is possible to charge subscriptions for fire protection, but subscribers benefit from putting out fires in adjacent properties. Allowing a nonsubscriber’s property to burn is not only generally viewed as unacceptable (especially if lives are at risk) but also endangers other properties and their inhabitants.

6 A market failure is not the lack of a market but the failure of a market to achieve the optimal outcome in which marginal costs equal marginal benefits. Market failures are ubiquitous, and many such failures may be too small or too difficult to correct to justify government intervention. Market failures arise from many sources, including externalities, monopoly power, imperfect information, and incomplete markets (in which contracts cannot be made, such as those between generations). Some kinds of insurance, in particular, tend to suffer from many market failures. A large part of federal government spending relates to insurance against various contingencies, such as spending on Social Security, unemployment, and health.

7 See U.S. Census Bureau, 2019 State and Local Government Finances, October 8, 2021, https://www.census.gov/data/datasets/2019/econ/local/public-use-datasets.html.

Congressional Research Service

4

link to page 9

Addressing the Long-Run Deficit: A Comparison of Approaches

by function (defense, education, energy, health, etc.). Later, this section also discusses trends in federal taxes by source, tax structure, tax expenditures, and receipts and payments in the major trust funds.

Distribution of Spending by Fundamental Economic Form: Government Goods and Services Versus Transfers

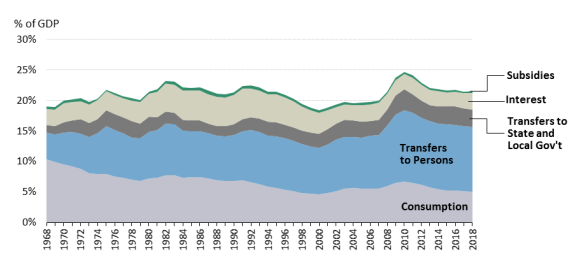

One way to look at spending is to examine the extent to which spending involves actual government consumption or production (that is, spending on the direct provision of goods and services) as compared with transfers, subsidies, and interest. The discussion in this section indicates that although total spending as a percentage of GDP fluctuated around 20% of GDP between 1973 and 2007, government involvement in the economy—narrowly defined as using resources to provide public goods directly—had fallen by a third and outside of defense had remained roughly constant and small (at around 2% of GDP). At the same time, transfers to persons increased by more than 40%, and transfers to state and local governments increased by less than 5%. Spending rose nearly 2% of GDP by 20182019, primarily due to transfers to persons, whereas consumption continued to decline. The increase in transfers and subsidies in 2020 and 2021 is expected to be temporary and was largely a response to the pandemic. Figure 2 shows how the economic form of federal spending has shifted since 1968.

Figure 2. Federal Spending by Economic Form, |

|

CY1970-CY2021, as a Percentage of GDP Source: National Income and Product Accounts (NIPA), Tables 1.1.5 and 3.2. |

In calendar year 2007, 28% of government spending was categorized as consumption and involved the direct provision of goods and services. Of the remaining amount, 44% were transfers to persons, 13% transfers to state and local governments, 14% interest payments, and 2% subsidies.7 8 Although federal government spending amounted to 19.9% of output in 2007, federal government spending on the provision of public and quasi-public goods was 5.5% of output.8 9

8 Data in this section are from the Bureau of Economic Analysis (BEA), “National Income and Product Accounts,” Tables 1.1.5 and 3.3, https://apps.bea.gov/iTable/index_nipa.cfm. Note that some numbers may not add up due to rounding.

9 These goods include goods such as national defense, infrastructure provided by the corps of engineers, the federal courts and prisons, the national forestry service and national parks, embassies and consulates in other countries, and similar goods.

Congressional Research Service

5

link to page 11 Addressing the Long-Run Deficit: A Comparison of Approaches

Based on budget data reported subsequently, 3.8% was for defense, leaving 1.7% for nondefense. Because total nondefense discretionary spending was 3.4% of GDP, half of this amount was transfers.

By 2018

By 2019, before the pandemic, with the economy at or near full employment, federal government consumption spending had declined to 5.2% of output, whereas transfers had increased. Government spending on nondefense goods and services was 1.92.0% of GDP, and defense spending was 3.2% of GDP. Budget data for FY2017FY2019 indicate that discretionary spending was 6.3% of GDP, with defense spending at 3.12% of GDP and nondefense at 3.21% of GDP. Thus, roughly 60% 35% of nondefense spending, about 1.9% of GDP, was transfers at that time.

State and local government spending (netting out transfers between these remaining two levels of government spending) in 2007 was 14% of output, and total spending by all forms of government (after netting out federal transfers) was 31.533.2% of output. A larger share of state and local spending (which includes federal government transfers), 69%, was in government provision of goods and services (consumption), with 21% in transfers to persons, 9% in interest payments, and less than 1% in subsidies. In the third quarter of 20182019, state and local spending net of federal transfers was 14was 13.6%, for a total of 32.530.8% for all government spending. Provision of goods and services was 64%; transfers were 26%; and interest was 9%.

10%.

Combining all levels of government, in 2007, government production of goods and services was 15.2% of output, thus the federal government share (5.5%) was about one-third of the total provided by all levels of government. Subtracting 3.8% from the federal government share and the total share to eliminate national defense spending (shown subsequently), the federal share of nondefense provision of goods and services by all levels of government was 11%. In 20182019, the nondefense share had risen to 14was 10%, with the federal share (5.2% of output) remaining at 36%.

at 37.4%.

Similar results are found when examining employment levels. Total government civilian employment in 2007 was 16% of total nonagricultural employment, with the federal government accounting for 2%, the state government accounting for 3.7%, and local government accounting for the remaining 10.4%.9 By September 201810 By March 2022, the employment share remained atwas about 15%, and each level of government maintained approximately the same shares (with local government falling to 9.6%).

1.9%, 3.4%, and 9.3%).

The share of federal government spending that goes to the direct provision of public or quasi-public goods (consumption) has declined over time, as shown in Table 2, whichwhich compares 1980 with 2007, 2019, and 2021 and 2018. The decline from 7.2% of GDP in 1980 to 5.5% of GDP in 2007 is largely due to a reduction in defense spending.

The latest data available, 2021, are affected by pandemic spending, which is not expected to continue.

10 Data from Bureau of Labor Statistics (BLS), Establishment Data, Table B-13, https://www.bls.gov/news.release/empsit.t17.htm.

Congressional Research Service

6

link to page 12 Addressing the Long-Run Deficit: A Comparison of Approaches

Table 2. Federal Spending by Fundamental Form, CY1980, CY2007, and CY2018 as a %CY2019, and

CY2021, as a Percentage of GDP

Category

1980

2007

2019

2021

Consumption

7.2%

5.5%

5.1%

5.2%

Transfers to Persons

7.7%

8.7%

10.8%

15.8%

Transfers to State and Local Governments

2.4%

2.5%

2.8%

4.8%

Interest

3.8%

2.8%

2.7%

2.2%

Subsidies

0.3%

0.3%

0.3%

2.1%

Total

21.4%

19.9%

21.5%

30.1%

of GDP

|

Category |

1980 |

2007 |

2018 |

|

Consumption |

7.2 |

5.5 |

5.0 |

|

Transfers to Persons |

7.7 |

8.7 |

10.6 |

|

Transfers to State and Local Governments |

2.4 |

2.5 |

2.8 |

|

Interest |

3.8 |

2.8 |

2.7 |

|

Subsidies |

0.3 |

0.3 |

0.3 |

|

Total |

21.4 |

19.9 |

21.5 |

Source: Bureau of Economic Analysis (BEA), National Income and Product Accounts (NIPA), Tables 1.1.5 and 3.2.

and 3.2.

The discussion in this section indicates that although total spending as a percentage of GDP fluctuated around 20% of GDP between 1973 and 2007, federal government involvement in the economy—narrowly defined as using resources to provide public goods directly—had fallen by a third and outside of defense had remained roughly constant and small (at around 2%small (2% or less of output). At the same time, transfers to persons increased by more than 40% and transfers to state and local governments increased by less than 5%. Spending rose nearly 2% of GDP by 20182019, primarily due to transfers to persons, whereas consumption continued to decline.

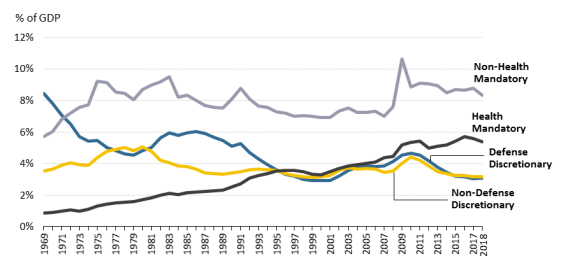

Distribution of Federal Spending by Mandatory and Discretionary Categories10

Discretionary Categories11 Budget accounts often classify spending in budget documents as mandatory or discretionary spending, along with subcategories of spending. Though technically classified as mandatory spending, interest payments tend to be listed separately because they are a consequence of past spending and tax policies. Discretionary spending is controlled by the annual appropriations process and is normally divided into defense and nondefense categories. Discretionary spending is where most of the public provision of goods and services occurs, but some discretionary spending is in the form of transfers. Mandatory spending is generally governed by a set of permanent statutory provisions, and some of these programs (such as Social Security and Medicare) are referred to as entitlements.

Since the late 1960s, as shown inin Figure 3, defensedefense spending has declined as a share of output, first as a result of the ending of the Vietnam War (by FY1981, defense spending was 5.2% of output). It rose in the 1980s and then fell, reaching 3.0% by 2001, before rising again with the Afghanistan and (second) Iraq wars. This pattern suggests that although defense spending may generally grow with the economy and be affected by other factors (such as moving to an all-volunteer force or the peacetime buildup in the 1980s), it also fluctuates depending on whether the United States is engaged in prolonged international conflicts.

FY1970-FY2021, as a Percentage of GDP Source: Created by CRS. Data from CBO Historical Budget Data, May 2022. Nondefense discretionary spending has fluctuated much less, although it rose in the late 1970s, then reverted to historical levels. Nondefense discretionary funding, although small as a share of the budget and of GDP, is largely the spending that many people think of when they think of the direct provision of goods and services by the federal government.

What Does Federal Nondefense Discretionary Spending Cover?

Nondefense discretionary spending covers a broad array of programs:

12

As noted in the discussion above, nontransfer domestic spending is 2% of GDP. In Thus, any one program area is modest as a share of output, which means that cuts in a particular area would also be small. For example, total spending on the entire federal domestic enforcement program, including immigration and the border patrol, federal courts and prosecutors, federal prisons, and the FBI, constitutes three-tenths of 1% of output, and even a significant cutback in this spending would be small compared with projected deficits of 4.3 percentage points of GDP by FY2024. |

12 Calculations are based on Office of Management and Budget, Historical Tables, Table 5.6, https://www.whitehouse.gov/omb/budget/historical-tables/. Data are for FY2019, since FY2020 and FY2021 are atypical years due to spending related to COVID-19.

Congressional Research Service

8

link to page 13 link to page 6 Addressing the Long-Run Deficit: A Comparison of Approaches

Mandatory spending, although it varies over time, has generally increased as a share of the economy since the 1960s.1213 The increase is most pronounced for health spending and has grown relative to GDP due to rising health care costs, certain other benefit changes, aging, and increased life spans.

Table 3 further disaggregates mandatory spending for selected years since the FY1980 (FY1980, FY2007, and FY2018FY2019). Overall discretionary spending over this time period declined from 9.9% of GDP to 6.23% of GDP, or a change of 36.93% (with declines of 35.433.3% for defense and 37.339.2% for nondefense discretionary spending), whereas total mandatory spending has increased by 35.9% 40.2% over the same time period.

The substantial, but presumably temporary, increase in federal spending in FY2020 (see Table 1) was primarily in income security and other (mandatory), with smaller increases in nondefense discretionary, Social Security, Medicare, and Medicaid.14

Table 3. Federal Spending by Mandatory and Discretionary Categories, FY1980,

FY2007, and FY2018FY2019, as a %Percentage of GDP

Percentage

Change

Category

FY1980

FY2007

FY2019

FY1980-FY2019

Discretionary

9.9%

7.2%

6.3%

-36.3%

Defense

4.8%

3.8%

3.2%

-33.3%

Nondefense

5.1%

3.4%

3.1%

-39.2%

Mandatory

9.2%

10.2%

12.9%

+40.2%

Social Security

4.2%

4.1%

4.9%

+16.7%

Medicare

1.2%

2.3%

3.7%

+208.1%

Medicaid

0.5%

1.2%

1.9%

+280.0%

Income Security

1.6%

1.4%

1.4%

-12.5%

Other Retirement and

1.7%

1.1%

1.4%

-17.6%

Disability

Other

1.2%

0.4%

0.9%

-25.0%

Offsetting Receipts

-1.2%

-0.8%

-1.3%

33.3%

Interest

1.9%

1.7%

1.8%

-5.2%

Total

21.0%

19.1%

21.0%

-0.0%

Source of GDP

|

|

|

|

| ||||||

|

Discretionary |

9.9 |

7.2 |

6.2 |

-36.9 |

||||||

|

Defense |

4.8 |

3.8 |

3.1 |

-35.4 |

||||||

|

Nondefense |

5.1 |

3.4 |

3.2 |

-37.3 |

||||||

|

Mandatory |

9.2 |

10.2 |

12.5 |

+35.9 |

||||||

|

|

Social Security |

4.2 |

4.1 |

4.9 |

+16.7 |

|||||

|

|

Medicare |

1.2 |

2.3 |

3.6 |

+191.7 |

|||||

|

|

Medicaid |

0.5 |

1.2 |

1.9 |

+290.0 |

|||||

|

|

Income Security |

1.6 |

1.4 |

1.4 |

-12.5 |

|||||

|

|

Other Retirement and Disability |

1.7 |

1.1 |

1.3 |

-23.5 |

|||||

|

|

Other |

1.2 |

0.4 |

0.8 |

-33.3 |

|||||

|

|

Offsetting Receipts |

-1.2 |

-0.8 |

-1.3 |

33.3 |

|||||

|

Interest |

1.9 |

1.7 |

1.6 |

-15.7 |

||||||

|

Total |

21.0 |

19.1 |

20.3 |

-3.3 |

||||||

Source: CBO Historical Tables, February 2021, https://www.cbo.gov/data/budget-economic-data#2.

https://www.cbo.gov/system/files/2018-06/51134-2018-04-historicalbudgetdata.xlsx.

Within mandatory spending, health spending (Medicare and Medicaid)—which has increased 223.5229.4% since FY1980—primarily drives the overall increase in mandatory spending. This increase is attributed to changes in demographics from an aging population and medical cost growth primarily, although benefit changes also contribute to the increase. Spending for Social Security also rose 16.7% over this period—primarily due to the number of Social Security beneficiaries and increased life expectancies. Other mandatory programs that provide benefits for low-income individuals, the unemployed, retirement programs for federal workers, and other

13 See CRS Report R44641, Trends in Mandatory Spending: In Brief, by D. Andrew Austin; and CRS Report R44763, Present Trends and the Evolution of Mandatory Spending, by D. Andrew Austin.

14 Overall spending increased to 31.2%, with an increase to 5% in income security and 5% in other mandatory and to 4.4% in nondefense discretionary. These increases reflected programs such as the increased unemployment compensation (both due to job loss and enhanced benefits) and the paycheck protection program.

Congressional Research Service

9

link to page 14 link to page 14 link to page 14

Addressing the Long-Run Deficit: A Comparison of Approaches

purposes (such as agricultural support payments) have remained relatively constant or declined since FY1980.

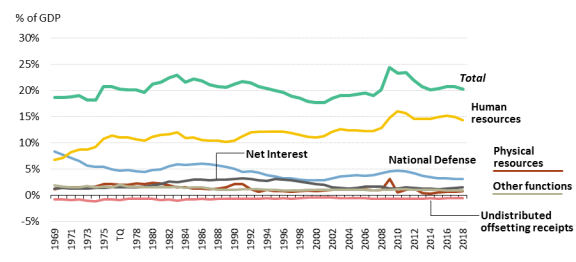

Distribution of Spending by Function

Another traditional way of viewing the budget is by budget function relating to the purpose of spending (education, health, etc.).1315 Figure 4 shows federal spending by budget function since 1969.

1970.

Figure 4. Federal Spending by Functional Form, |

|

|

These comparisons, shown inFY1970-FY2021, as a Percentage

of GDP

Graphic is interactive in the web version of the report.

Source: Created by CRS. Data from FY2023 President’s Budget, Historical Table 3.1.

These comparisons, shown in Table 4, provide a similar picture to the previous allocation: although total spending as a share of output has fluctuated somewhat from FY1980 to FY2018, FY2021, the federal government has an increasing share of output in health and programs for the elderly, with declining shares for almost every other functional category. In FY2007, 64% of spending was for human resources, with 20% for defense, 9% for interest, and 5% for all other functions. In FY2019In FY2018, the share devoted to human resources had further risen, whereas the share spent on national defense had declineddeclined. Table 4 presents these categories as a percentage of GDP and illustrates that the subcategories for many types of spending, which are those that represent direct provision of government goods and services, are small as a percentage of GDP.

The presumably temporary increase in FY2020 for total government spending to 31.3% of GDP was primarily due to increased spending on human resources (which rose to 20.7%) and to a lesser extent for physical resources (which rose to 4.1%).

Table 4. Federal Spending by Functional Form, FY1980, FY2007, and FY2018 as a %FY2019,

as a Percentage of GDP

Budget Function

FY1980

FY2007

FY2019

National Defense

4.8%

3.9%

3.2%

15 See CRS Report R41726, Discretionary Budget Authority by Subfunction: An Overview, by D. Andrew Austin, for additional detail.

Congressional Research Service

10

Addressing the Long-Run Deficit: A Comparison of Approaches

Budget Function

FY1980

FY2007

FY2019

Human Resources

11.2%

12.3%

14.8%

Education

1.1%

0.6%

0.7%

Health

0.8%

1.9%

2.8%

Medicare

1.1%

2.6%

3.1%

Income Security

3.1%

2.6%

2.4%

Social Security

4.2%

4.1%

0.9%

Veterans’ Benefits

0.8%

0.5%

1.0%

Physical Resources

2.4%

0.9%

0.7%

Energy

0.4%

0.0%

0.0%

Natural Resources and the

0.5%

0.2%

0.2%

Environment

Commerce and Housing Credit

0.3%

0.0%

-0.1%

Transportation

0.8%

0.5%

0.5%

Community and Regional

0.4%

0.2%

0.1%

Development

Net Interest

1.9%

1.7%

1.8%

Other

1.6%

0.9%

1.1%

International Activities

0.5%

0.2%

0.3%

General Science and Space

0.2%

0.2%

0.2%

Agriculture

0.3%

0.1%

0.2%

Administration of Justice

0.2%

0.3%

0.3%

General Government

0.5%

0.1%

0.1%

Offsetting Receipts

-0.7%

-0.6%

-0.5%

Total

21.2%

19.1%

21.1%,

Source of GDP

|

Budget Function |

FY1980 |

FY2007 |

FY2018 |

|

|

National Defense |

4.8 |

3.9 |

3.1 |

|

|

Human Resources |

11.2 |

12.3 |

14.3 |

|

|

Education |

1.1 |

0.6 |

0.5 |

|

|

Health |

0.8 |

1.9 |

2.7 |

|

|

Medicare |

1.1 |

2.6 |

2.9 |

|

|

Income Security |

3.1 |

2.6 |

2.4 |

|

|

Social Security |

4.2 |

4.1 |

4.9 |

|

|

Veterans' Benefits |

0.8 |

0.5 |

0.9 |

|

|

Physical Resources |

2.4 |

0.9 |

0.8 |

|

|

Energy |

0.4 |

0.0 |

0.0 |

|

|

Natural Resources and the Environment |

0.5 |

0.2 |

0.2 |

|

|

Commerce and Housing Credit |

0.3 |

0.0 |

0.0 |

|

|

Transportation |

0.8 |

0.5 |

0.5 |

|

|

Community and Regional Development |

0.4 |

0.2 |

0.2 |

|

|

Net Interest |

1.9 |

1.7 |

1.6 |

|

|

Other |

1.6 |

0.9 |

0.9 |

|

|

International Activities |

0.5 |

0.2 |

0.2 |

|

|

General Science and Space |

0.2 |

0.2 |

0.2 |

|

|

Agriculture |

0.3 |

0.1 |

0.1 |

|

|

Administration of Justice |

0.2 |

0.3 |

0.3 |

|

|

General Government |

0.5 |

0.1 |

0.1 |

|

|

Offsetting Receipts |

-0.7 |

-0.6 |

-0.5 |

|

|

Total |

21.2 |

19.1 |

20.3 |

|

Source: Office of Management and Budget, Budget of the U.S. Government Historical Tables FY2020, https://www.whitehouse.gov/wp-content/uploads/2019/03/hist03z1-fy2020.xlsx.

omb/budget/historical-tables/. Federal Taxes: Patterns over Time

This section discusses four issues related to taxes: (1) the sources of tax revenue and their growth over time; (2) the differences in structure and distribution of revenue sources; (3) the size and distribution of tax expenditures (special income tax provisions such as exclusions, deductions, and credits); and (4) taxes that are specified as the revenue source for certain spending.14

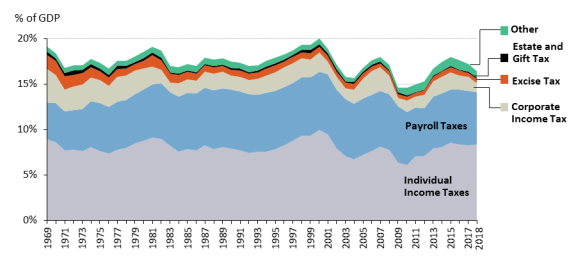

16 Tax Revenues

The federal income tax system has several components. The largest component, in terms of revenue generated, is the individual income tax. For FY2018, an estimated $1.7 trillion, or 50% of the federal government'’s revenue, came from the individual income tax. The corporate income 16 See CRS Report R45145, Overview of the Federal Tax System in 2020, by Molly F. Sherlock and Donald J. Marples, for additional detail on the sources of revenues, their growth over time, and tax structure.

Congressional Research Service

11

link to page 16

Addressing the Long-Run Deficit: A Comparison of Approaches

The corporate income tax was estimated to generate another $218 billion in revenue in FY2018, or just under 7% of total revenue. Social insurance or payroll taxes generated an estimated $1.2 trillion, or 35% of revenue in FY2018. Estimates indicate that the remainder of federal revenue collected in FY2018 came from excise taxes (3%) or other sources (6%).15

17

The relative importance of these components can change over time, as seen in Figure 5. The individual income tax, the largest single source of revenue as a percentage of GDP, has fluctuated considerably over time. Individual income tax revenues grew in the late 1970s due to bracket creep, reaching 9.4% in FY1981.1618 The tax cuts induring the Reagan Administration are the major reason revenues declined, falling to 7.9% in FY1990. Revenues increased slightly with the 1993 Clinton Administration tax increase (tax increase during the Clinton Administration (P.L. 103-66), but the more significant growth occurred with the strong economic performance in the late 1990s, leading to a ratio of 9.9% in FY2000. They declined during the first decade of the 21st21st century following the tax cuts during the George W. Bush Administration tax cuts ((P.L. 107-16) and JGTRRA (P.L. 108-27). Along with the individual income tax, total taxes have also fluctuated. Prior to the Bush tax cutstax cuts during the Bush Administration, total taxes dropped as low as 17.1% in FY1977 and rose as high as 20.6% in FY2001. During the 2007-2009 recession, taxes fell to less than 15% of GDP.

Corporate taxes have fluctuated as well, although largely due to economic conditions, whereas payroll taxes rose to around their current levels as a percentage of GDP by the mid-1980s, reached a peak of 6.8% in 2001, and have since declined slightly. Excise taxes have declined by two-thirds, and other revenue sources have remained about the same. Part of the decline in excise taxes is because these taxes are imposed on a per-unit basis and not indexed for inflation and, with the exception of tobacco taxes, have generally not been increased.

17 Other sources include estate and gift taxes, customs duties and fees, and deposits of earnings by the Federal Reserve System.

18 Bracket creep refers to the increase in the effective tax rate as nominal income grows because exemptions and rate brackets were not indexed for inflation at that time. There is also some amount of real bracket creep that causes effective tax rates to rise over time as real income grows.

Congressional Research Service

12

Addressing the Long-Run Deficit: A Comparison of Approaches

Tax Structure Tax Structure

These revenue sources differ in some important ways. Individual income taxes are progressive, have graduated rates, and can be revised in a variety of ways, including changing rates, deductions, exclusions, and credits. Income taxes are the main source of revenue for most federal spending outside of Social Security and Medicare Hospital Insurance (HI, whose benefits are less than half of Medicare spending).1719 Corporate income taxes are levied at a flat rate after allowing for various deductions and credits. Estate taxes are also progressive, but they are a small share of government revenues and have been declining in magnitude over the past 20 years.

Payroll taxes tend to fall more heavily on middle- and lower-income individuals.20 Payroll taxes, the next-largest source of revenue after individual income taxes, have flat rates (except for the Additional Medicare Tax) with an earnings cap for Social Security (but not Medicare). These taxes tend to be proportional, with a reduced burden on high-income taxpayers. Because of their simple structure, the main options for increasing revenues from this source are increasing rates and raising or eliminating the earnings cap.

Social Security payroll taxes are the basic source of finance for the Social Security program, and they are linked to benefits so that larger taxes lead eventually to larger benefits, although there are progressive elements in the benefit formula. Medicare payroll taxes qualify individuals for Medicare HI coverage, but the Medicare benefits are the same for all recipients.

Excise taxes, which largely apply to alcohol, tobacco, and transportation fuels, tend to be regressive and fall more heavily on middle- and lower-income individuals, but are also a smaller revenue source.21 Transportation fuel taxes are a major source of finance for highways, airports, and other transportation needs.

Tax Expenditures

Tax expenditures are revenue losses attributable to federal income tax laws that allow a special exclusion, exemption, deduction, credit, preferential tax rate, or deferred tax liability. The special tax credits and deductions in the income tax can also be viewed as a form of spending through the tax code. That is, one can view revenues as receipts without the special benefits and the special benefits from tax expenditures as spending. According to an FY1974-FY2004a Government Accountability Office (GAO) study, tax expenditures averaged 7.5% of GDP during that period.18FY1974-FY2004.22 In FY2007, tax expenditures were 7.2% of GDP and about 36% of total government direct spending.19 In FY201823 In FY2019, tax expenditures were 7.21% of GDP and about 3534% of government spending.20

24

19 The Medicare Payment Advisory Commission (MedPAC), REPORT TO THE CONGRESS: Medicare Payment Policy, March 2019, http://medpac.gov/docs/default-source/reports/mar19_medpac_entirereport_sec.pdf?sfvrsn=0.

20 For more information on payroll taxes, see CRS Report R47062, Payroll Taxes: An Overview of Taxes Imposed and Past Payroll Tax Relief, by Anthony A. Cilluffo and Molly F. Sherlock.

21 For more information on excise taxes, see CRS Report R46938, Federal Excise Taxes: Background and General Analysis, by Anthony A. Cilluffo.

22 GAO, Tax Expenditures Represent a Substantial Federal Commitment and Need to be Reviewed, GAO-05-690, September 2005, http://www.gao.gov/new.items/d05690.pdf.

23 Joint Committee on Taxation (JCT), Estimates of Federal Tax Expenditures for Fiscal Years 2007-2011, September 24, 2007, JCS-3-07, https://www.jct.gov/publications.html?func=startdown&id=1198.

24 Joint Committee on Taxation (JCT), Estimates of Federal Tax Expenditures for Fiscal Years 2019-2023, October 4, 2018, JCX-55-19, https://www.jct.gov/publications/2019/jcx-55-19/, and CBO, 10-Year Economic Projections, August 2019, https://www.cbo.gov/about/products/budget-economic-data#4.

Congressional Research Service

13

link to page 11 link to page 13 link to page 14 link to page 18 Addressing the Long-Run Deficit: A Comparison of Approaches

From the perspective of dividing government activity between transfers and direct provision of public goods, as in Table 2, tax expenditures are transfers and subsidies that go to persons, as is the case with the bulk of federal spending. From the perspective of discretionary versus mandatory spending, as inin Table 3, theythey are similar to a mandatory form of spending. Finally, from the perspective of budget function, as inin Table 4 and as shown inin Table 5, whichwhich compares spending and tax expenditures by budget function for FY2018FY2019, the pattern of tax expenditures is quite different from that of spending. A much larger share of tax expenditures is for physical resources. For specific subcategories, the largest share of tax expenditures is for commerce and housing, a category that attracts a small share of spending. The size of this category reflects special benefits for earnings from capital income. It also reflects benefits for housing in the form of mortgage interest and property tax deductions and, to a lesser extent, exemption from capital gains taxtaxes on owner-occupied housing and the low-income housing credit. The relatively large share for general government reflects tax-exempt bonds and itemized deductions for state and local income and sales taxes. (These amounts could also be distributed across the functional categories of state spending and thus would be more broadly distributed.) Much of the benefit for tax-exempt bonds goes to education and highways, where funds are borrowed for capital improvements.) Tax expenditures also provide significant benefits for health through the exemption of employer-provided health insurance and for income security, largely through benefits for pensions and other retirement savings.

|

Budget Function |

Spending |

Tax Expenditures |

|

|

National Defense |

3.14 |

0.03 |

|

|

Human Resources |

14.39 |

4.34 |

|

|

Education, Training, Employment, Social Services |

0.48 |

1.23 |

|

|

Health |

2.90 |

1.14 |

|

|

2.87 |

— |

||

|

Income Security |

2.43 |

1.74 |

|

|

Social Security |

4.84 |

0.18 |

|

|

Veterans' Benefits |

0.86 |

0.05 |

|

|

Physical Resources |

0.97 |

1.87 |

|

|

Energy |

0.02 |

0.06 |

|

|

Natural Resources and the Environment |

0.20 |

0.00 |

|

|

Commerce and Housing |

0.02 |

1.76 |

|

|

Transportation |

0.46 |

0.03 |

|

|

Community and Regional Development |

0.26 |

0.02 |

|

|

Net Interest |

1.51 |

0.01 |

|

|

Other |

0.98 |

0.90 |

|

|

International Activities |

0.23 |

0.47 |

|

|

General Science and Space |

0.15 |

0.06 |

|

|

Agriculture |

0.13 |

0.00 |

|

|

Administration of Justice |

0.34 |

— |

|

|

General Government |

0.13 |

0.38 |

|

|

Offsetting Receipts |

-0.50 |

— |

|

|

Total |

20.49 |

7.16 |

|

Source: Budget of the U.S. Government Historical Tables FY2019, https://www.govinfo.gov/content/pkg/BUDGET-2019-TAB/pdf/BUDGET-2019-TAB.pdf and JCX-81-18.

FY2019, as a

Percentage of GDP

Budget Function

Spending

Tax Expenditures

National Defense

3.25%

0.03%

Human Resources

14.82%

4.02%

Education, Training, Employment, Social

0.65%

1.00%

Services

Health

2.77%

1.13%

Medicare

3.08%

—

Income Security

2.44%

1.67%

Social Security

4.94%

0.17%

Veterans’ Benefits

0.95%

0.05%

Physical Resources

0.66%

2.06%

Energy

0.02%

0.11%

Natural Resources and the Environment

0.18%

0.00%

Commerce and Housing

-0.12%

1.89%

Transportation

0.45%

0.03%

Community and Regional Development

0.13%

0.03%

Net Interest

1.78%

0.00%

Other

1.01%

1.01%

International Activities

0.25%

0.46%

General Science and Space

0.15%

0.07%

Agriculture

0.18%

0.00%

Congressional Research Service

14

link to page 20 Addressing the Long-Run Deficit: A Comparison of Approaches

Budget Function

Spending

Tax Expenditures

Administration of Justice

0.31%

—

General Government

0.11%

0.47%

Offsetting Receipts

-0.47%

—

Total

21.05%

7.12%

Source: Budget of the U.S. Government Historical Tables, https://www.whitehouse.gov/omb/budget/historical-tables/; JCT, Estimates of Federal Tax Expenditures For Fiscal Years 2019-2023, JCX-55-19; and CBO, 10-Year Economic Projections, August 2019, https://www.cbo.gov/about/products/budget-economic-data#4.

Earmarked Revenues and Trust Funds Earmarked Revenues and Trust Funds

As noted above, dedicated revenues finance spending on certain categories of services, some of which are termed trust funds and some special federal funds. There are about 200 trust funds, but only a few of them are important in terms of magnitude or for considering budgetary reform.21

25

In some cases, the trust funds lead to questions about addressing the deficit. Although some of these funds rely on contributions from general revenues, the Social Security and the Medicare HI trust funds primarily rely on payroll taxes.2226 The largest trust funds relate to Social Security, which is divided into Old Age and Survivors Insurance (OASI) and Disability Insurance (DI), and Medicare, which is divided into Hospital Insurance Part A and Supplementary Medical Insurance (SMI) Parts B and D.23

27

Payroll taxes are the primary source of finance for Social Security and Medicare HI (also known as Medicare Part A). The funding of these programs is organized through trust funds that can also hold assets and earn interest. Medicare SMI, which pays for physician services and outpatient drugs, is financed primarily by a combination of premiums and general revenues.

Table 6 shows the inflow of revenues and the payment of benefits in the three trust funds financed by payroll taxes. (This table does not include earnings from interest on government securities held by the funds and transfers of income taxes collected on Social Security benefits; it also does not reflect administrative costs.) As indicated in the table, OASI payroll tax revenue (as a percentage of GDP) has declined over the past 11 yearsperiod of FY2007-FY2019, while payments have increased substantially. In contrast, DI and HI payroll tax revenues have been flat or increasing (as a percentage of GDP) over the same time period, while payments have been flat or increasing more modestly than OASI. By FY2018, payments for Social Security and Medicare benefits exceeded payroll tax collections. Because initial Social Security benefits are indexed to wages (and subsequently to prices), they tend to be a relatively constant share of output. Benefits have grown because of increasing longevity and an aging population. Revenues also tend to be a relatively constant share of output but were increased in the mid-1980s.

25 The 12 largest trust funds are Social Security (including Old-Age and Survivors Insurance and Disability Insurance), Medicare (including Supplementary Medical Insurance and Hospital Insurance), Civil Service Retirement and Disability, Military Retirement, Unemployment Insurance, Highway, Federal Employees Health Benefits, Foreign Military Sales, Airport and Airway, and Railroad Retirement.

26 Transfers are made to the Social Security and Medicare HI trust funds in the amount of income taxes collected on Social Security benefits. A temporary transfer was also made for the temporary two-percentage-point reduction in the employee share of Social Security taxes for 2011 and 2012.

27 See CRS Report RL33028, Social Security: The Trust Funds, by Barry F. Huston; and CRS Report R40425, Medicare Primer, coordinated by Patricia A. Davis, for further details on the history of these programs.

Congressional Research Service

15

link to page 20 Addressing the Long-Run Deficit: A Comparison of Approaches

Table 6. Financing and Benefits in the Social Security and Medicare Hospital

Table 6. Financing and Benefits in the Social Security and Medicare Hospital Insurance Trust Funds, FY1973, FY2007, and FY2018FY2019, as a %Percentage of GDP

Payroll Taxes

Benefits Payments

Program

FY1973

FY2007

FY2019

FY1973

FY2007

FY2019

of GDP

|

Program |

Payroll Taxes |

Benefits Payments |

||||

|

FY1973 |

FY2007 |

FY2018 |

FY1973 |

FY2007 |

FY2018 |

|

Social Security Old Age and Survivors Insurance (OASI)

3.0%

3.8%

3.6%

3.1%

3.4%

4.2%

|

3.0 |

3.8 |

3.4 |

3.1 |

3.4 |

4.1 |

Social Security Disability Insurance (DI)

0.4%

0.6%

0.7%

0.4%

0.7%

0.7%

|

0.4 |

0.6 |

0.8 |

0.4 |

0.7 |

0.7 |

Medicare Hospital Insurance (HI)

0.6%

1.3%

1.3%

0.5%

1.4%

1.5%

|

0.6 |

1.3 |

1.3 |

0.5 |

1.4 |

1.5 |

Source: Budget of the U.S. Government Historical Tables FY2020, , https://www.whitehouse.gov/wp-content/uploads/2019/03/hist13z1-fy2020.xlsx.

omb/budget/historical-tables/. Note: This table does not show the period beginning in the mid-1980s when sizable surplus revenues were collectedcol ected for Social Security.

Table 7 provides information on the income and outflow for the SMI trust fund. In FY1971, this fund was nearly equally financed by premiums paid by beneficiaries and federal contributions from general revenues. Although premiums have increased as a percentage of output, the vast majority of financing is now from general revenues. The premium share for Medicare Part B (physicians) fluctuated over time, but it is now set by law at 25% of the cost of funding Medicare Part B; the premiums share for Medicare Part D (drug) program is set at 25.5% of the estimated cost of the standard benefit.24

28

Table 7. Supplementary Medical Insurance Trust Fund Income and Outflow, FY1973,

FY2007, and FY2018FY2019, as a %Percentage of GDP

Income or Outflow

FY1973

FY2007

FY2019

Premiums

0.1%

0.4%

0.5%

Federal Contributions

0.1%

1.3%

1.6%

Benefits

0.2%

1.6%

2.1%

Source: White House, Budget of the U.S. Government Historical Tables, of GDP

|

Income or Outflow |

FY1973 |

FY2007 |

FY2018 |

|

Premiums |

0.1 |

0.4 |

0.5 |

|

Federal Contributions |

0.1 |

1.3 |

1.6 |

|

Benefits |

0.2 |

1.6 |

2.0 |

Source: White House, Budget of the U.S. Government Historical Tables FY2020, https://www.whitehouse.gov/wp-content/uploads/2019/03/hist13z1-fy2020.xlsx.

https://www.whitehouse.gov/omb/budget/historical-tables/. As these tables indicate, the size of these programs, particularly Medicare, has grown over time. SMI has grown faster than HI, and general revenue contributions have grown at a similar pace. SMI currently accounts for more than half the cost of Medicare.

One open question surrounding the formulation of a long-run budget policy is whether to continue financing Social Security and Medicare HI from payroll taxes. In this case, both programs'programs’ future benefits are expected to outstrip future receipts and eventually draw down all the assets. The Social Security (OASI) trust fund is projected to run out of accumulated assets in 2034,2529 and the HI trust fund is predicted to run out in 2026.26

30

28 See CRS Report R43122, Medicare Financial Status: In Brief, by Patricia A. Davis. 29 See CRS Report RL33028, Social Security: The Trust Funds, by Barry F. Huston, for additional discussion. 30 See CRS Report RS20946, Medicare: Insolvency Projections, by Patricia A. Davis; and CRS Report R43122, Medicare Financial Status: In Brief, by Patricia A. Davis, for additional discussion.

Congressional Research Service

16

link to page 21

Addressing the Long-Run Deficit: A Comparison of Approaches

Since its implementation in 1935, Social Security has been treated as a separate program, similar to a retirement plan, in which contributions (e.g., payroll taxes) during the working years create an entitlement to benefits in old age. A similar approach has been used for the more recently established Medicare HI. If these programs are to be kept separate, then they must be brought into balance separately and, to maintain the historic source of financing, any shortfall not addressed through benefit cuts or delayed eligibility must be addressed through increases in a specific tax—the payroll tax.27

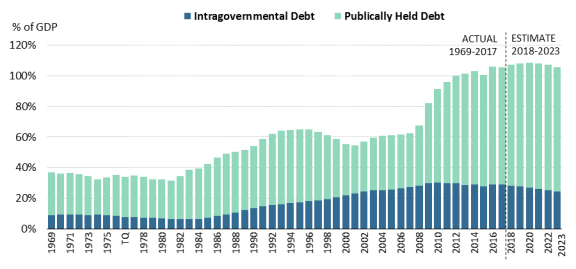

31 Growth in the Debt

Federal debt may be divided into two major categories: (1) debt held by the public, which is the sum of accrued net deficits and outstanding money from federal credit programs; and (2) intragovernmental debt, which is the amount of federal debt held by other federal agencies. As of February 28, 2019April 30, 2022, the amount of federal debt outstanding was $22.11630.4 trillion, with 7378.5% of that debt held by the public and 2621.5% held as intragovernmental debt.2832 Figure 6 shows the federal debt as a share of the economy from FY1969FY1970 projected through FY2023.

Individuals, firms, the Federal Reserve, state and local governments, and foreign governments are eligible to purchase publicly held debt. Such debt may be acquired directly through the auction process from which most publicly held debt is initially sold or on the secondary market if the debt is deemed "“marketable,"” or eligible for resale. As of February 28, 2019April 30, 2022, the total amount of publicly held debt outstanding was $16.25123.4 trillion. Publicly held debt is the measure of concern for the sustainability of the debt since it measures debt owned outside of the government. This debt grew rapidly as a percent of GDP during the 2007-2009 recession and afterward and has continued to grow (while intergovernmental debt relative to GDP has declined).

31 Money can be moved from the general fund to the trust funds, as in the case of income taxes on Social Security benefits, but such actions may weaken the relationship between benefits and payments in the underlying programs.

32 The Bureau of the Fiscal Service, Monthly Statement of the Public Debt of the United States, April 30, 2022, https://www.treasurydirect.gov/govt/reports/pd/mspd/2022/opds042022.pdf.

Congressional Research Service

17

link to page 22

Addressing the Long-Run Deficit: A Comparison of Approaches

The majority of publicly held debt is marketable, and it includes all Treasury notes, bonds, bills, Treasury Inflation Protected Securities (TIPS), and Treasury-issued Floating Rate Notes (FRNs). Nonmarketable debt held by the public is composed of U.S. savings bonds, State and Local Government Securities (SLGS), and other, smaller issues.2933 As of February 28, 2019, 96.6April 30, 2022, 97.4% of publicly held issues, or $15.74123.2 trillion, was marketable.

Unlike publicly held debt, intragovernmental debt issuances are almost exclusively nonmarketable. As of February 28, 2019April 30, 2022, of the $5.8656.5 trillion in total intragovernmental debt, $0.029 02 trillion (0.53%) was marketable debt. Intragovernmental debt is held by components of the federal government, with the majority of nonmarketable debt held by trust funds devoted to Social Security and military and federal worker retirements and marketable debt held by the Federal Financing Bank (a government corporation created to reduce the cost of federal borrowing). Intragovernmental debt has declined in recent years as major trust funds have begun to finance benefits from assets.

Because intragovernmental debt is held only in federal government accounts, such debt cannot be accessed by the outside institutions. Conversely, the bonds that finance publicly held debt activity may compete for assets in private and financial markets. Public debt issues may be a particularly attractive collateral option on the secondary market if the federal government is perceived as a safe credit risk.

Deficit Challenges Going Forward

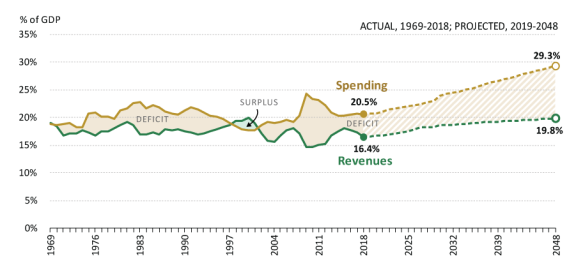

The CBO budget baseline projects that over the next 10 years, the deficit will average roughly 4.4% of GDP. This is 1.5% of GDP more than the average deficit (i.e., 2.9% of GDP) over the preceding 50 yearsyears. Figure 7 shows the federal budget deficit (surplus) from FY1968FY1970 through projected deficits in FY2048.

Most economists agree that deficits are sustainable as long as the deficits as a share of the economy are less than the growth rate of the economy. The CBO budget baseline assumes that economic growth will be just under 1.8% over the next 10 years. This growth rate is less than both the average deficit over the preceding 50 years (2.9% of GDP) and the projected federal deficits over the next 10 years (4.4% of GDP).

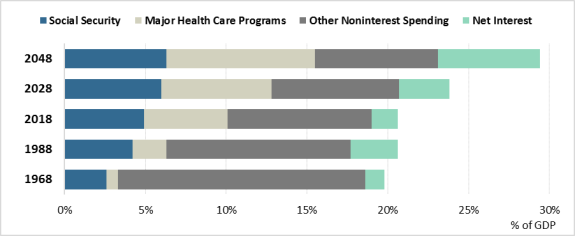

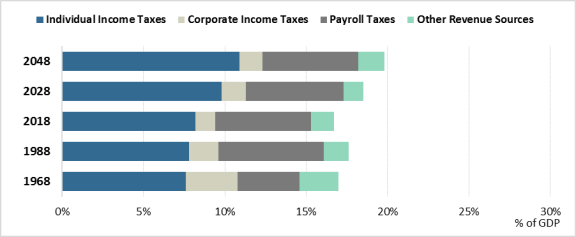

Although the budget situation over the next 10 years is challenging, the long-term outlook is even more daunting—with the budget deficit estimated to be an average of 8.411.5% of GDP from FY2039 to FY2048FY2041 to FY2051. As deficits are a result of the combination of spending and tax decisions, examining them separately may offer some insightsinsights. Figure 8 shows CBO'’s analysis of federal revenue and spending projected for selected years from FY2006 through FY2051.

Revenue trends in the long-run projections show continued growth in the share of federal revenue from the individual income tax. The share of federal revenue from the individual income tax is projected to increase from 49.6% in FY2019 to 53.7% in FY2031 and 55.7% in FY2051. During the same time period, the share of federal revenue from payroll taxes is projected to decrease from 35.9% in FY2019 to 33.2% in FY2031 and 30.5% in FY2051. The shares of federal revenue from the corporate income tax and other sources are roughly flat over the same time period.

Figure 8. Federal Revenue and Spending, Selected Years FY2006-FY2051, as a

Percentage of GDP

Source: Created by CRS. Data from CBO, The 2021 Long-Run Budget Outlook, March 2021.