Economic Impact of Infrastructure Investment

Infrastructure investment has received renewed interest as of late, with both President Trump and some Members of Congress discussing the benefits of such spending. Infrastructure can be defined in a number of ways depending on the policy discussion; in general, however, the term refers to longer-lived, capital-intensive systems and facilities, such as roads, bridges, and water treatment facilities.

Over the past several decades, government investment in infrastructure as a percentage of gross domestic product (GDP) has declined. Annual infrastructure investment by federal, state, and local governments peaked in the late 1930s, at about 4.2% of GDP, and since has fallen to about 1.5% of GDP in 2016. State and local governments consistently spend more on infrastructure directly than the federal government. In 2016, direct federal spending on nondefense infrastructure was less than 0.1% of GDP, whereas state and local spending was about 1.4% of GDP. However, the federal government transfers some funds each year to state and local governments for capital projects, which includes infrastructure projects, equaling about 0.4% of GDP in 2016. The United States also lags many other developed countries with respect to annual infrastructure spending. Spending on infrastructure, as a percentage of GDP, is higher in all G7 countries, except for Italy and Germany, than in the United States.

Infrastructure is understood to be a critical factor in the health and wealth of a country, enabling private businesses and individuals to produce goods and services more efficiently. With respect to overall economic output, increased infrastructure spending by the government is generally expected to result in higher economic output in the short term by stimulating demand and in the long term by increasing overall productivity. The short-term impact on economic output largely depends on the type of financing (whether deficit financed or deficit neutral) and the state of the economy (whether in a recession or expansion). The long-term impact on economic output is also affected by the method of financing, due to the potential for “crowding out” of private investment when investments are deficit financed. The type of infrastructure is also expected to affect the impact on economic output. Investments in core infrastructure, defined as roads, railways, airports, and utilities, are expected to produce larger gains in economic output than investments in some broader types of infrastructure, such as hospitals, schools, and other public buildings.

Changes in economic output are expected to have subsequent effects on employment; as such, infrastructure investments are likely to impact employment as well. Recent research suggests modest reductions in the unemployment rate in response to increased infrastructure investment. Again, it is expected that the method of financing and state of the economy will alter these impacts. Recent research has suggested that deficit-neutral investments are less likely to affect employment, whereas deficit-financed investments are expected to reduce unemployment in the short term. Additionally, recent economic research suggests that during an economic expansion, with a relatively strong labor market, infrastructure investments are unlikely to have any sustained impact on the unemployment rate. However, during a recession, the same investment is likely to reduce the unemployment rate to some degree, research suggests.

Economic Impact of Infrastructure Investment

Jump to Main Text of Report

Contents

- What Is Infrastructure?

- Infrastructure Investment Trends

- Infrastructure Investment in the United States

- International Comparisons

- The Economy and Infrastructure Investment

- Effects on Economic Output

- Financing

- Business Cycle Timing

- Type of Infrastructure

- Employment Effects

- Financing

- Business Cycle Timing

- Concluding Thoughts

Figures

- Figure 1. Annual Government Nondefense Investment in Public Capital, 1929-2016

- Figure 2. Annual Federal Nondefense Investment, 1929-2016

- Figure 3. Federal Nondefense Investment by Budget Function, 2012

- Figure 4. Annual State and Local Investment, 1947-2016

- Figure 5. Cumulative Stock of Nondefense Federal Capital, 1929-2016

- Figure 6. Cumulative Stock of State and Local Capital, 1929-2016

- Figure 7. Transportation Infrastructure Investment in G7 Countries, 2014

Summary

Infrastructure investment has received renewed interest as of late, with both President Trump and some Members of Congress discussing the benefits of such spending. Infrastructure can be defined in a number of ways depending on the policy discussion; in general, however, the term refers to longer-lived, capital-intensive systems and facilities, such as roads, bridges, and water treatment facilities.

Over the past several decades, government investment in infrastructure as a percentage of gross domestic product (GDP) has declined. Annual infrastructure investment by federal, state, and local governments peaked in the late 1930s, at about 4.2% of GDP, and since has fallen to about 1.5% of GDP in 2016. State and local governments consistently spend more on infrastructure directly than the federal government. In 2016, direct federal spending on nondefense infrastructure was less than 0.1% of GDP, whereas state and local spending was about 1.4% of GDP. However, the federal government transfers some funds each year to state and local governments for capital projects, which includes infrastructure projects, equaling about 0.4% of GDP in 2016. The United States also lags many other developed countries with respect to annual infrastructure spending. Spending on infrastructure, as a percentage of GDP, is higher in all G7 countries, except for Italy and Germany, than in the United States.

Infrastructure is understood to be a critical factor in the health and wealth of a country, enabling private businesses and individuals to produce goods and services more efficiently. With respect to overall economic output, increased infrastructure spending by the government is generally expected to result in higher economic output in the short term by stimulating demand and in the long term by increasing overall productivity. The short-term impact on economic output largely depends on the type of financing (whether deficit financed or deficit neutral) and the state of the economy (whether in a recession or expansion). The long-term impact on economic output is also affected by the method of financing, due to the potential for "crowding out" of private investment when investments are deficit financed. The type of infrastructure is also expected to affect the impact on economic output. Investments in core infrastructure, defined as roads, railways, airports, and utilities, are expected to produce larger gains in economic output than investments in some broader types of infrastructure, such as hospitals, schools, and other public buildings.

Changes in economic output are expected to have subsequent effects on employment; as such, infrastructure investments are likely to impact employment as well. Recent research suggests modest reductions in the unemployment rate in response to increased infrastructure investment. Again, it is expected that the method of financing and state of the economy will alter these impacts. Recent research has suggested that deficit-neutral investments are less likely to affect employment, whereas deficit-financed investments are expected to reduce unemployment in the short term. Additionally, recent economic research suggests that during an economic expansion, with a relatively strong labor market, infrastructure investments are unlikely to have any sustained impact on the unemployment rate. However, during a recession, the same investment is likely to reduce the unemployment rate to some degree, research suggests.

Infrastructure investment has received renewed interest as of late, with both President Trump and some Members of Congress discussing the benefits of such spending. The condition and performance of infrastructure is thought to affect the economic well-being of countries in a number of ways. This report provides an overview of the trends surrounding infrastructure investment in the United States and examines the potential impact of additional infrastructure investments on economic output and employment.

What Is Infrastructure?1

Although infrastructure spending has garnered increased attention recently, there is no generally agreed-upon definition of infrastructure. In general, the term refers to longer-lived, capital-intensive systems and facilities. Some restrict the definition to include systems and facilities that have traditionally been provided by the public sector, such as highways and water treatment facilities. However, others include predominantly privately owned systems and facilities, such as those involved in electricity production and distribution. The definition of infrastructure can be extended even further to include research and development expenditures, as they add to the stock of technology and information available for use by private individuals.

Infrastructure is beneficial for both businesses and households and for the economy broadly. For businesses, infrastructure can help to lower fixed costs of production, especially transportation costs, which are often a central determinant of where businesses are located.2 For households, a wide variety of final goods and services are provided through infrastructure services, such as water, energy, and telecommunications.3 Infrastructure benefits the economy overall, as it allows more goods and services to be produced with the same level of inputs, fostering long-term economic growth.

Federal, state, and local governments share the cost of infrastructure investments, with the majority of direct spending coming from state and local governments. The federal government contributes to infrastructure investments in the form of direct spending, grants to state and local governments, loan guarantees, and preferential tax treatment.

Infrastructure Investment Trends

Due to the ambiguous definition of infrastructure, tracking government spending on infrastructure investments can often be difficult. One of the more comprehensive sources of data on government investment in infrastructure is the Bureau of Economic Analysis (BEA), which tracks government spending and investment in various areas.4 Government spending is divided into consumption expenditures and investments.5 Consumption expenditures consist of spending by the government to produce and provide goods and services to the public, such as paying Census workers to survey households. By contrast, investment spending consists of government spending on fixed assets, or capital, used to benefit the public for more than one year, such as roads, bridges, computers, and government buildings. Investment is then further divided into three categories: (1) structures, which include many of the classic examples of infrastructure (water systems, highways, bridges, etc.); (2) equipment (computers, military hardware, etc.); and (3) intellectual property (software, research and development, etc.). This report largely focuses on structures, as this most closely aligns with the types of infrastructure cited by policymakers.

Investment is generally recorded in two alternative ways, which can present different perspectives on overall investment. First, BEA reports the annual flow of funds spent by the government on investment projects. However, because the results of these investments tend to produce value for many years at a time, BEA also tracks the total value of all investments that are still productive, which is often referred to as the "total stock of investments." BEA tracks the total value of all government investments by estimating the stock of productive capital and increasing the capital stock when new funds are invested and decreasing the capital stock over time as projects deteriorate, or depreciate. The overall capital stock will either increase or decrease over time depending on the size of the flow of investment funds relative to the depreciation of the capital stock. If the flow of funds each year is larger than the loss of value due to depreciation, then the stock of capital will grow over time; if the flow of new funds is less than the loss of value due to depreciation, then the stock of capital will decrease over time.

The following sections will examine the annual flow of U.S. government spending into public investments, describe the overall stock of public capital over time, and then compare infrastructure investment in the United States to that in other industrialized economies.

Infrastructure Investment in the United States

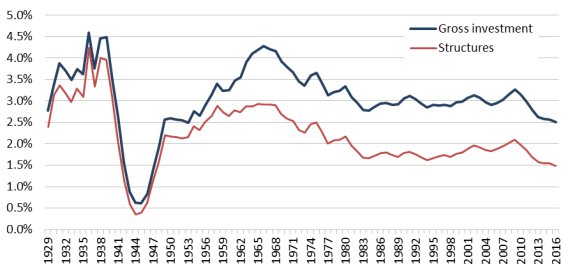

Nondefense gross government investment (federal, state, and local) in the United States has largely been in decline since the 1960s, falling from above 4% of GDP to about 2.5% in 2016, as shown in Figure 1. Overall, nondefense gross investment, as a percentage of GDP, was even higher for a number of years in the 1930s, before decreasing significantly during and shortly after the end of World War II, as gross government investment shifted to defense-related spending and GDP grew quickly. Nondefense gross investment in the 1960s then rose to similar levels seen before World War II, and then began slowly declining over time.

It is common to limit analysis of infrastructure investments to nondefense investments; national defense investments generally do not fit the definition of infrastructure because they are not available to the public to assist in the production of goods and services. In 2016, about 54% of federal investment was directed to national defense purposes, whereas about 46% was directed to nondefense purposes.6

A similar pattern emerges for general government (federal, state, and local) nondefense investment in structures over this period. Government investment in structures peaked in the 1930s at about 4.2% of GDP, before dipping dramatically during the World War II period, as shown in Figure 1. General government investment in structures then rebounded to about 2.9% of GDP by the 1960s, and has since generally been in decline, falling to about 1.5% of GDP in 2016.

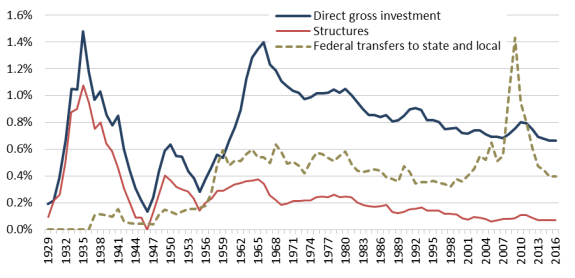

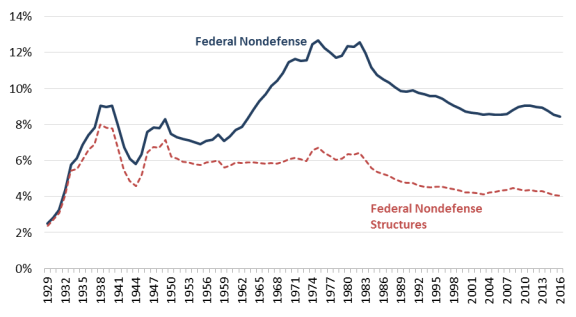

Direct federal investment, which refers to spending that occurs at the federal level rather than transfers to state and local governments, peaked in the 1930s as a percentage of GDP, and again in the 1960s before beginning to gradually decline over the next several decades, falling from about 1.4% of GDP in 1966 to about 0.7% of GDP in 2016, as shown in Figure 2.7 Direct federal investment in structures has been relatively flat recently, hovering around 0.1% of GDP since 2000. Direct federal investment in structures also peaked in the 1930s, reaching above 1.0% of GDP briefly, then again to a lesser extent in the late 1940s and 1960s, at around 0.4% of GDP.

Whereas direct investment by the federal government has largely been in decline over the previous several decades, transfers from the federal government to state and local government for capital investments have exceeded direct federal spending since the mid-1950s. As shown in Figure 2, transfers to state and local governments for capital investments began in the 1930s and increased through the 1960s to about 0.6% of GDP. These transfers then began to decline through the 1970s, 1980s, and 1990s, before rising rapidly in the 2000s, with much of the increase in 2009 attributable to the American Recovery and Reinvestment Act of 2009 (P.L. 111-5). Transfers, as a percentage of GDP, have now declined to levels similar to in the 1980s and 1990s, around 0.4% of GDP.

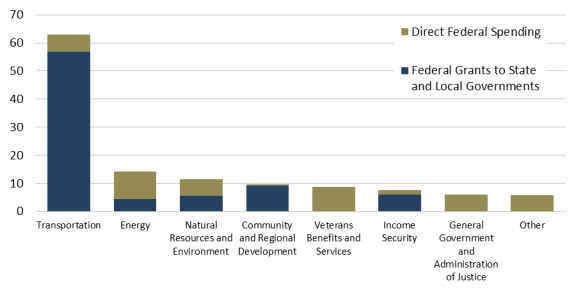

According to data from the Congressional Budget Office (CBO), as of 2012, the federal government spent about $126 billion on nondefense investments through direct spending and transfers to state and local governments. The largest share of this money, by budget function, was invested in transportation, accounting for about $63 billion, as shown in Figure 3. The next largest source of investment was energy, which accounted for about $14 billion in 2012. Depending on the budget function, the mix of investments through direct federal spending and grants to state and local governments varies considerably. Within transportation about 90% of federal investments are made through grants to state and local governments, whereas within energy almost 70% of federal investments are made through direct federal spending.

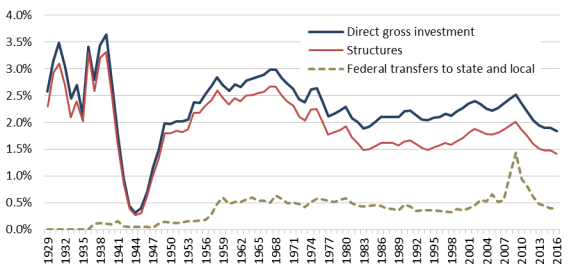

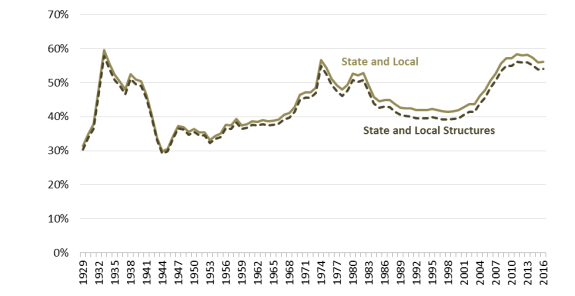

State and local investment has followed a similar pattern over time as investment at the federal level. State and local investment in structures peaked in 1939 at 3.3% of GDP, before shrinking dramatically during and shortly after World War II, then increasing back to about 2.7% of GDP in the late 1960s, as shown in Figure 4. Following the 1960s, investment in structures declined through the 1970s to about 1.5% of GDP, and then increased between 1994 and 2009 to a level of about 2.0% of GDP. Since the 2009 peak, state and local investment in structures has again declined back to about 1.4% of GDP. Although this level of state and local investment is relatively low by historical standards, the federal government transferred about 0.4% of GDP to state and local governments in 2016 in the form of grants for capital investments (see Figure 2).

State and local governments directly invest significantly more in general, and into structures, than the federal government (as seen by comparing Figure 2 and Figure 4); however, some of the direct investments made by state and local governments are the result of transfers from the federal government. As shown in Figure 4, in 2016, state and local governments directly invested funds equivalent to about 1.8% of GDP, but the federal government also transferred funds equivalent to 0.4% of GDP to state and local governments for capital investments in that year. If all of the funds transferred from the federal government were invested into structures, it would still mean state and local governments spent about 1.1% of GDP on structure investments, whereas the federal government contributed about 0.5% of GDP to investment in structures, including direct investments and transfers to state and local governments.

Overall, the stock of public capital at the federal, state, and local level—that is, the total value of all productive investments—as a percentage of GDP trended upward during the post-World War II period. However, the stocks of structures installed by different levels of government have diverged over recent decades. During the post-World War II period, the stock of nondefense federal structures has been in decline, falling from around 7% of GDP in the late 1940s to about 4% of GDP in 2016, as shown in Figure 5. In contrast, the stock of structures installed at the state and local levels has been trending upward during the post-World War II period, increasing from about 36% of GDP in the late 1940s to about 54% of GDP in 2016, as shown in Figure 6. This shift in capital stock from the federal government to state and local governments is partially understood to be because of the federal government's shift away from direct investments and toward grants to state and local governments in recent decades.

|

Figure 5. Cumulative Stock of Nondefense Federal Capital, 1929-2016 (as a share of GDP) |

|

|

Source: CRS calculations based on data from the Bureau of Economic Analysis. |

|

Figure 6. Cumulative Stock of State and Local Capital, 1929-2016 (as a share of GDP) |

|

|

Source: CRS calculations based on data from the Bureau of Economic Analysis. |

International Comparisons

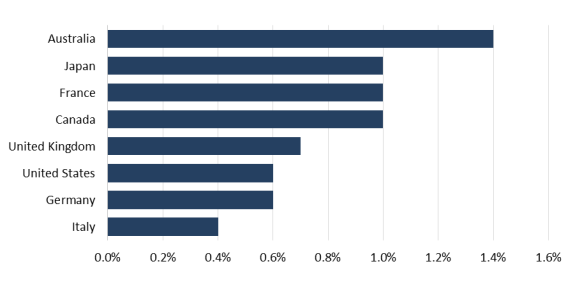

Data reflecting overall infrastructure investment across countries are relatively sparse; however, the Organization for Economic Co-operation and Development (OECD) tracks government investment specifically in transportation infrastructure. The United States lags behind many other advanced economies with respect to transportation infrastructure investment as a percentage of GDP. According to OECD data, which include spending on roads, rails, inland waterways, maritime ports, and airports, the United States spends less on transportation infrastructure as a percentage of GDP than most OECD countries.8 As shown in Figure 7, in 2014, the United States lagged all other G7 countries, except Italy and Germany, spending about 0.6% of GDP on transportation infrastructure, compared with a G7 average of about 0.8%. Although many OECD countries have higher infrastructure investment rates than the United States, the United States may have a higher stock of infrastructure than some of these other countries due to differing rates of past investment. However, the OECD does not produce data on the stock of infrastructure across countries.

|

Figure 7. Transportation Infrastructure Investment in G7 Countries, 2014 (as a share of GDP) |

|

|

Source: OECD, Infrastructure Investment, https://data.oecd.org/transport/infrastructure-investment.htm. Notes: Infrastructure is defined as road, rail, inland waterways, maritime ports, and airports. Includes spending by all levels of government. |

The Economy and Infrastructure Investment

Infrastructure is generally understood to be a critical factor in the economic well-being of a country, enabling private businesses and individuals to produce goods and services in a more efficient manner, although there is debate about the optimal amount of infrastructure investment. The remainder of this report focuses on the ways in which additional infrastructure investments affect economic output and employment. As the following sections explain, all infrastructure investments are not the same. The impact of these investments is likely to differ with respect to a few key considerations, including the way in which the investments are financed, the timing of the investments with respect to the business cycle, and the type of infrastructure being created. The following sections touch on the potential impact of additional infrastructure investment and examine how these factors are likely to amplify or subdue its economic impact.

Effects on Economic Output

Over the long term, economists expect a larger stock of public capital to result in higher levels of economic output. An increase in the public capital stock, such as new or improved roads, raises output directly in the near term (government spending is included in GDP) and also allows individuals and businesses to be more productive in the long term, freeing up time and resources that can be put toward generating additional economic output or used to enjoy more leisure time. For example, a new bridge may greatly shorten commute times and distances for truck drivers, allowing them to deliver goods to consumers more quickly and at lower cost to themselves, and allowing businesses to produce and deliver more goods to consumers. These changes result in productivity growth for the economy as a whole, which is the most important determinant of long-term economic growth.

Ample research has attempted to estimate the impact of public infrastructure investments on economic output. A recent review of the literature utilized meta-regression analysis to take advantage of the nearly 30 years of international research on the subject.9 The authors found that on average for the United States, a 1% increase in the public capital stock (about $138 billion in 2016) would result in a higher level of private-sector economic output by 0.083% in the short term (about $12.8 billion), compared with a baseline.10 The same 1% increase would increase the long-term level of private-sector economic output by 0.122% (about $18.7 billion in 2016), compared to a baseline.11 By contrast, CBO currently estimates that a 1% increase in public capital would increase the long-term level of private-sector output by 0.06% (about $9.2 billion in 2016).12 It is important to underscore that the estimated impact is exclusively for private-sector economic output, rather than total economic output, as the impact would likely be larger, particularly in the short term, if total economic output were being evaluated.

However, these are only average estimates, and the economic impact depends on how the investment is financed, broader economic conditions when the investment is made, and the type of infrastructure invested in.

Financing

There are numerous ways to finance additional government investments in infrastructure. In general, the literature focuses on instances where either the national or regional governments spend on infrastructure directly, as this is the more common approach historically. However, there are other options, such as offering tax incentives, providing loan guarantees, and creating private-public partnerships. Given the current uncertainty regarding alternative financing mechanisms that may be included in future legislation, this report focuses on the economic impact of spending undertaken directly by the government.13

Government investment is financed in two distinct ways: either through deficit financing or deficit-neutral financing. The short-term impact of infrastructure investment can differ significantly depending on the type of financing used. Investments are considered deficit financed if there is no decrease in government spending or increase in tax revenue to offset the new spending. Investments are considered deficit neutral if there is a decrease in government spending or an increase in tax revenue to offset the new spending.

The total economic impact of deficit financing for infrastructure investments is unclear, as it creates two opposing forces with respect to economic output. Additional public investments are likely to boost (or "stimulate") economic output in the short term both directly and indirectly. As the government spends additional funds on infrastructure projects, this directly increases economic output as the government purchases goods and services from contractors.14 Moreover, deficit-financed investments may indirectly increase economic output even further via the multiplier effect.15 The multiplier effect suggests that $1 of government spending may increase economic output by more than $1, particularly during economic downturns. For example, as the government hires contractors to complete new infrastructure projects, the employees and suppliers utilized by the contractors now have additional money as well, and will likely spend at least some of it on goods and services provided by other businesses. The successive flow of funds, first from the government to contractors, then to employees and suppliers, may result in a larger GDP increase than the original spending by the government. However, government spending affects aggregate demand only once the funds are actually distributed. For many infrastructure projects it may take an extended period of time for funds to actually be spent, as projects must first be selected, competing bids reviewed, etc. Thus, the short-term impact of infrastructure investment may take longer to materialize than the impacts of other types of government spending that can be implemented faster, such as cash transfers to individuals.

Although deficit-financed investments may increase short-term economic output, the long-term impact may be reduced due to the "crowding out" of private investment. As the government borrows funds for infrastructure investments, it generally results in higher interest rates. As a result of the increased interest rates, private investment and interest-sensitive consumer spending is expected to decrease. The CBO estimates that a $1 increase in the federal deficit decreases private investment by about 33 cents.16 The replacement of private investment with public investment is often of concern to economists because, on average, private investment is thought to be more productive than public investment.17 So although deficit-financed investments are more likely to produce short-term gains in economic output, they may impose long-term costs to economic output as they replace some amount of private investment.

Alternatively, deficit-neutral infrastructure investments are unlikely to affect economic output in the short term. When investments are deficit neutral, they have no immediate impact on aggregate demand because government spending remains level. Moreover, because the government is not borrowing additional money, interest rates are unlikely to change in the short term. However, depending on what types of spending are cut or taxes are raised, offsets could have positive or negative effects on long-term output that would need to be weighed against the long-term benefits of additional infrastructure spending. Although deficit-neutral public investments are not expected to have any significant impacts on short-term economic output, they are less likely to result in crowding out of private investment. As such, additional deficit-neutral investments are expected to have a larger positive impact on long-term economic output than deficit-financed investments, all else equal.

In an attempt to account for how different financing mechanisms may affect public investment's impact on output, International Monetary Fund (IMF) researchers estimated these impacts separately for deficit-financed and deficit-neutral investments. The authors found that an increase in deficit-financed public investment of 1 percentage point of GDP tends to increase overall GDP by 0.9% within the first year and by 2.9% after four years, but the authors found no significant change in GDP when investments were deficit neutral.18 However, recent analysis by the CBO suggested that, depending on the structure (a onetime expenditure versus a series of annual expenditures) and size of deficit-financed federal investment spending, the long-term impact may either increase or decrease the level of GDP compared with a baseline. CBO found that a deficit-financed increase in public investment of $100 billion would increase GDP by about $20 billion in the short term, and result in the level of GDP being about $1 billion higher after 10 years compared with a baseline. When deficit neutral, the same investment would not increase GDP in the short term, but would result in the level of GDP being about $4 billion higher after 10 years compared with a baseline.19 Much of the difference between the results produced by the CBO and IMF researchers is due to differing estimates in how public capital impacts productivity and the degree to which public investment crowds out private investment. CBO assumes public capital is less effective at increasing productivity and more likely to crowd out private investment than the IMF researchers.

An additional possible downside of deficit-financed investments is the potential increase in the debt-to-GDP ratio. Economists are generally concerned with the debt-to-GDP ratio rather than absolute levels of debt, as a country's GDP is indicative of its ability to pay off the debt. Elevated debt-to-GDP ratios may impede economic growth if they lead to macroeconomic instability, such as rising interest rates on government debt.20 The U.S. debt-to-GDP ratio increased significantly during and after the recent recession, rising from about 35% in 2006 to over 76% in 2016.21 Nevertheless, interest rates on this debt have remained at historic lows, suggesting investors are confident in the United States' ability to continue meeting its debt obligations. The already elevated ratio of debt to GDP may give pause to some when considering deficit-financed infrastructure investments. However, deficit-financed investments may not necessarily increase the debt-to-GDP ratio; the increase in economic output may be greater than the increase in debt.22 Some research has suggested that deficit-financed investments have no impact on the debt-to-GDP ratio and can even decrease it,23 whereas other research has suggested such investments will likely increase the ratio.24 As discussed in the following section, the magnitude of the increase in economic output will additionally depend in part on the business cycle.

Business Cycle Timing

The business cycle timing of additional public investments is also likely to alter the impact of public investments on short-term economic output. Current economic theory suggests that in the short term, if public investments are made during a recession, the impact on economic output will be larger than if the same investments were made during an economic expansion.25 When the economy is in recession, the short-term economic boost from additional public spending is expected to be larger because various economic inputs are being underutilized and can be called up for production relatively quickly. For example, during a recession large numbers of unemployed workers are generally available, and factories are running below capacity, allowing production to ramp up quickly when the government begins offering new contracts to companies. Alternatively, when the economy is expanding healthily, the boost to short-term economic activity may be smaller because there is less excess capacity in the economy. Additionally, if undertaken at full employment, additional spending may result in higher rates of inflation, or the Federal Reserve might raise rates to counter rising inflation, which would decrease the impact on short-term output.

Recent empirical research has largely confirmed this assumption, suggesting significantly larger output responses to public investment in times of recession versus expansion. A recent article estimated the impact could be about 1.5 times larger during a recession than during an expansion, suggesting a 1% increase in public investment would boost economic output by 3.4% during a recession and about 2.3% during an expansion.26 A recent article published by the IMF suggested an even smaller impact during an expansion. The authors found that during a recession, an increase in investment spending of 1 percentage point of GDP would potentially increase economic output by 1.5% in the first year and by 3% after four years, whereas there was no significant change in short-term output when public investments were made during an expansion.27

The U.S. economy has been in an expansion since June 2009, and although growth has been slower than average, economic indicators suggest the economy is near full employment. Under normal circumstances, the economy being at full employment would be an argument against additional infrastructure spending, as it could potentially lead to higher inflation or require the Federal Reserve to increase interest rates to offset the stimulative nature of the spending. However, a number of economists believe the U.S. economy is suffering from some type of ailment that is preventing the economy from growing faster. If this is the case, expansionary fiscal policy, such as increased infrastructure spending, could help to push the economy out of its current slow-growth path.28

Type of Infrastructure

Infrastructure investment's overall impact on economic output largely depends on how effective the investments are in increasing productivity—in other words, how helpful they are in the production of goods and services. Some types of infrastructure, such as roads, are more closely associated with the production of goods and services, whereas others, such as schools or government office buildings, have some societal benefit but do not have the same close relationship to economic output. Researchers have thus attempted to distinguish between so-called "core" infrastructure and other infrastructure. Core infrastructure includes roads, railways, airports, and utilities. This definition excludes some broader types of infrastructure, such as hospitals, schools, and other public buildings.

As part of the same large-scale review of research discussed earlier, the authors reviewed a subset of articles that distinguished between core and all types of infrastructure.29 The authors found that core infrastructure tended to have a larger impact on private-sector economic output than all types of infrastructure taken together. With respect to all types of infrastructure, a 1% increase in the public capital stock is expected to increase private-sector economic output by 0.083% in the short term and 0.122% in the long term. When looking only at core infrastructure, the same 1% investment is expected to increase private-sector economic output by 0.131% in the short term and 0.170% in the long term.30

Employment Effects

Changes in economic output tend to occur alongside changes in employment; as the economy produces more goods and services, it generally requires more people to produce those goods and services. A long-standing economic rule of thumb, often referred to as Okun's Law, suggests that increased economic growth generally leads to increased employment, and vice versa.31 This relationship is most obvious during economic downturns, when a decrease in economic growth generally occurs alongside a decrease in employment and a rising unemployment rate. The same is generally true during times of economic growth, with rising employment and a decreasing unemployment rate. Assuming that increased public investment spurs additional economic output, there will likely be some change in employment as well. In addition, faster productivity growth is expected to reduce the long-term unemployment rate in the economy, allowing the economy to sustainably operate at lower levels of unemployment without increasing the rate of inflation.32

Another way to look at the relationship between economic output and employment involves a basic understanding of how economic output is accounted for. The most prominent measure of economic output is GDP, which sums the cost of all goods and services produced during a specific time period. An alternative way to measure total economic output is as the total income received within all sectors of the economy in a given period. These two measures theoretically will produce the same amount, as any money paid for goods and services is eventually paid to other individuals in the form of salaries, wages, dividends, rental payments, etc. Therefore, any increase in GDP is also an increase in aggregate incomes. These increased incomes may be paid out in the form of new jobs, or increased pay for existing jobs; it is thus not clear how much an increase in GDP may actually boost overall employment.

Current research surrounding the employment impact of additional public investment is difficult to summarize, as researchers generally use different measures of employment, including overall labor demand, employment levels, and the unemployment rate. However, estimates of the impact of public investment on employment range from a positive impact to no impact. A recent article by IMF researchers suggests that among OECD countries, an increase in public investment of 1 percentage point of GDP generally decreases the unemployment rate by 0.11% in the short term and 0.35% in the medium term.33 Alternatively, researchers estimated the impact of increased public capital on labor demand, finding that in the United States a 1% increase in public capital would increase labor demand by 1.13% in the short term, 1.07% in the medium term, and 0.08% in the long term.34 As defined by the authors, an increase in labor demand constitutes an increase in wages, employment, or both; therefore, it is difficult to draw concrete examples of how public capital may affect employment levels.

Financing

In the short term, the method of financing additional public investment is likely to alter its impact on employment. If additional public spending is deficit neutral, economists estimate the impact on overall demand is likely to be minimal in the short term, as discussed in the "Effects on Economic Output" section. Therefore, they conclude that investment will likely not generate new jobs, but rather shift jobs to construction and other areas connected to infrastructure projects. However, economists estimate that a deficit-financed increase in public investment is expected to affect short-term demand and therefore increase employment as demand for labor rises. Researchers with the IMF looked at the impact of increased public investment on the unemployment rate depending on the mode of financing, finding a significantly larger impact on short-term unemployment when the spending was deficit financed rather than deficit neutral. The researchers found that an increase in public investment of 1 percentage point of GDP would potentially decrease the unemployment rate by nearly 2% over four years when deficit financed, but found no impact on the unemployment rate when it was deficit neutral.35

The method of financing is also likely to alter the impact of public investments on long-term employment outcomes due to differing impacts on productivity growth. Deficit-neutral investments are likely to decrease the long-term unemployment rate to a larger degree than deficit-financed investments, because they are unlikely to crowd out private investments, resulting in faster productivity growth, all else equal. Deficit-financed investments would be expected to reduce the long-term unemployment rate, but to a lesser degree, as some amount of crowding out of private investment is likely to occur, resulting in a smaller increase in productivity growth and therefore a smaller decrease in the long-term unemployment rate. Estimates of the impact of public investment on the long-term unemployment rate would likely be quite imprecise, as it is only estimated based on the movement of other economic processes, rather than observed directly, and it shifts over time in response to changes in productivity growth but also labor force composition, public policy and institutions, and the level of long-term unemployment.36

Business Cycle Timing

The ability of public infrastructure investments to generate additional employment is likely to differ based on whether the economy is in recession or expansion, with a larger boost to employment occurring during a recession. In the midst of a recession, the economy is generally operating below its potential, with numerous unemployed workers and businesses producing fewer goods and services than is possible. In this scenario, increased infrastructure investment is likely to have a larger impact on employment because there are so many idle workers available to begin work immediately. Conversely, during an economic expansion, there are fewer unemployed individuals struggling to find work. As such, additional infrastructure investments are less likely to generate new jobs, and rather would shift jobs toward occupations related to infrastructure, such as construction and architecture.

Researchers at the IMF estimated the impact of additional public investment on employment depending on the state of the economy. The authors found that during an expansion, there was no significant impact on employment. However, during a recession, an increase in public investment of 1 percentage point of GDP decreased the unemployment rate by 0.5% after one year and 0.75% after four years.37 The U.S. unemployment rate as of May 2017 was 4.3%, which is below most estimates of the long-term unemployment rate (i.e., full employment).38 However, some economic indicators suggest there is still room for employment growth, as a number of prime age adults dropped out of the labor force during the recession and may return as economic conditions continue to improve.

Concluding Thoughts

Public infrastructure is a valuable resource to both consumers and businesses alike, improving their ability to produce and consume goods and services more efficiently. The ability for businesses to produce goods and services more efficiently is a crucial determinant of economic growth, and increased infrastructure investment—if well targeted and depending on the degree of crowding out—likely contributes to increased productivity over time, leading to higher GDP over the long term. In the near term, public infrastructure investments can also have a varying impact on GDP by stimulating aggregate demand. The anticipated impact on near-term GDP will generally depend on the financing mechanism, overall economic conditions, and the type of infrastructure. The largest short-term gains in GDP would likely be achieved if the investments were deficit financed, the funds were spent during a recession, and the investments focused on core infrastructure (i.e., roads, bridges, and railways). But because of crowding out, long-term gains (outside of a recession) would generally be greater if infrastructure investment were deficit neutral.

In addition, public infrastructure investments may affect employment in the near and medium term. As the government selects contractors to complete new infrastructure projects, contractors hire additional workers, such as architects and construction workers. Economic research suggests the largest impact on short- and medium-term employment would be achieved by deficit-financed investments that take place during a recession.39 In the long term, infrastructure investment is less likely to have a significant impact on employment outcomes.

Author Contact Information

Footnotes

| 1. |

This section has been adapted from CRS In Focus IF10592, Infrastructure Investment and the Federal Government, by William J. Mallett. |

| 2. |

Ward Romp and Jakob de Haan, "Public Capital and Economic Growth: A Critical Survey," Perspektiven der Wirtschaftspolitik, vol. 8, no. 51 (April 2007), pp. 6-52. |

| 3. |

Stephane Straub, "Infrastructure and Development: A Critical Appraisal of the Macro-Level Literature," Journal of Developmental Studies, vol. 47, no. 5 (May 2011), pp. 683-708. |

| 4. |

Data on infrastructure investment at the federal level are also available from the Historical Tables produced by the Office of Management and Budget; however, these sources do not include data on state and local infrastructure spending. |

| 5. |

Because BEA measures the output of goods and services, it does not include government transfers or subsidies in the standard measure of government spending, unlike the federal budget definition of spending. |

| 6. |

CRS calculations based on data from the Bureau of Economic Analysis. |

| 7. |

Direct federal investments are limited to funds spent directly by the federal government on investment projects; funds that are transferred to state and local governments for investment by the federal government are recorded as state and local investment since they are the entity which directly spends the funds on investment projects. |

| 8. |

Organization for Economic Co-operation and Development (OECD), "Infrastructure Investment," available at https://data.oecd.org/transport/infrastructure-investment.htm. |

| 9. |

Meta-regression analysis is a quantitative method for conducting literature reviews. |

| 10. |

Pedro Bom and Jenny Ligthart, "What Have We Learned From Three Decades of Research on the Productivity of Public Capital?" Journal of Economic Surveys, vol. 28, no. 5 (December 2015), pp. 902-905. |

| 11. |

Ibid. |

| 12. |

U.S. Congressional Budget Office, The Macroeconomic and Budgetary Effects of Federal Investment, June 2016, pp. 24-25. |

| 13. |

For a discussion of some of the other infrastructure financing mechanisms, refer to CRS Report R43308, Infrastructure Finance and Debt to Support Surface Transportation Investment, by William J. Mallett and Grant A. Driessen. |

| 14. |

Economic output, as measured by GDP, necessarily increases as the government spends money because government expenditures are included as a component of GDP. |

| 15. |

Nicoletta Batini et al., Fiscal Multipliers: Size, Determinants, and Use in Macroeconomic Projections, International Monetary Fund, September 2014, https://www.imf.org/external/pubs/ft/tnm/2014/tnm1404.pdf. |

| 16. |

U.S. Congressional Budget Office, The Macroeconomic and Budgetary Effects of Federal Investment, June 2016, pp. 9. |

| 17. |

Ibid., p. 2. |

| 18. |

Abdul Abiad, Davide Furceri, and Petia Topalova, The Macroeconomic Effects of Public Investment: Evidence from Advanced Economies, IMF Working Paper, vol. WP/15/95, May 2015. |

| 19. |

U.S. Congressional Budget Office, The Macroeconomic and Budgetary Effects of Federal Investment, June 2016. |

| 20. |

Carmen Reinhart, Vincent Reinhart, and Kenneth Rogoff, Debt Overhangs: Past and Present, NBER Working Paper Series, Working Paper 18015, April 2012. |

| 21. |

Federal Reserve Bank of St. Louis and U.S. Office of Management and Budget, "Federal Debt Held by the Public as Percent of Gross Domestic Product," available at https://fred.stlouisfed.org/series/FYGFGDQ188S. |

| 22. |

For more discussion of this topic, refer to CRS Report R44383, Deficits and Debt: Economic Effects and Other Issues, by Grant A. Driessen. |

| 23. |

International Monetary Fund, Legacies, Clouds, Uncertainties, October 2014, Chapter 3, http://www.imf.org/external/pubs/ft/weo/2014/02/. |

| 24. |

U.S. Congressional Budget Office, The Macroeconomic and Budgetary Effects of Federal Investment, June 2016. |

| 25. |

Alan J. Auerbach and Yuriy Gorodnichenko, "Measuring the Output Responses to Fiscal Policy," American Economic Journal, vol. 4, no. 2 (May 2012), pp. 1-27. |

| 26. |

Ibid. |

| 27. |

Aseel Almansour, David Furceri, and Carlos M. Granados, et al., World Economic Outlook: Legacies, Clouds, Uncertanties, International Monetary Fund, October 2014, pp. 75-114, at http://www.imf.org/en/Publications/WEO/Issues/2016/12/31/Legacies-Clouds-Uncertainties. |

| 28. |

Lawrence Summers, "U.S. Economic Prospects: Secular Stagnation, Hysteresis, and the Zero Lower Bound," Business Economics, vol. 49, no. 2 (2014). For a more thorough discussion of the current economic expansion in the United States, refer to CRS Report R44543, Slow Growth in the Current U.S. Economic Expansion, by Mark P. Keightley, Marc Labonte, and Jeffrey M. Stupak. |

| 29. |

Pedro Bom and Jenny Ligthart, "What Have We Learned From Three Decades of Research on the Productivity of Public Capital?," Journal of Economic Surveys, vol. 28, no. 5 (December 2015), pp. 889-916. |

| 30. |

Ibid. |

| 31. |

Edward S. Knotek, "How Useful is Okun's Law?" Federal Reserve Bank of Kansas City Economic Review, vol. 92, no. 4 (Fourth Quarter 2007), pp. 73-103. |

| 32. |

Laurence Ball and Gregory Mankiw, "The NAIRU in Theory and Practice," Journal of Economic Perspective, vol. 16, no. 4 (Fall 2002), pp. 115-136. |

| 33. |

Abdul Abiad, Davide Furceri, and Petia Topalova, The Macroeconomic Effects of Public Investment: Evidence from Advanced Economies, IMF Working Paper, vol. WP/15/95, May 2015. |

| 34. |

Panicos O. Demetriades and Theofanis P. Mamuneas, "Intertemporal Output and Employment Effects of Public Infrastructure Capital: Evidence from 12 OECD Economies," The Economic Journal, vol. 110, no. 465 (July 2000), pp. 687-712. |

| 35. |

Abdul Abiad, Davide Furceri, and Petia Topalova, The Macroeconomic Effects of Public Investment: Evidence from Advanced Economies, IMF Working Paper, vol. WP/15/95, May 2015. |

| 36. |

For a more thorough discussion of the long-term unemployment rate, refer to CRS Report R44663, Unemployment and Inflation: Implications for Policymaking, by Jeffrey M. Stupak. |

| 37. |

Abdul Abiad, Davide Furceri, and Petia Topalova, The Macroeconomic Effects of Public Investment: Evidence from Advanced Economies, IMF Working Paper, vol. WP/15/95, May 2015. |

| 38. |

Bureau of Labor Statistics, at https://data.bls.gov/timeseries/LNS14000000. |

| 39. |

Abdul Abiad, Davide Furceri, and Petia Topalova, The Macroeconomic Effects of Public Investment: Evidence from Advanced Economies, IMF Working Paper, vol. WP/15/95, May 2015. |