Reauthorization of the Federal Aviation Administration (FAA) in the 115th Congress

Funding authorization for the Federal Aviation Administration (FAA), included in the FAA Extension, Safety, and Security Act of 2016 (P.L. 114-190), expired at the end of FY2017. A subsequent six-month extension (P.L. 115-63) is set to expire at the end of March 2018. Long-term FAA reauthorization measures (H.R. 2997 and S. 1405) are currently under consideration. In addition to setting spending levels, FAA authorization acts typically set policy on a wide range of issues related to civil aviation. This report considers prominent topics in the 115th Congress reauthorization debate.

Most FAA programs are financed through the Airport and Airway Trust Fund (AATF), which is funded by a variety of taxes and fees on air transportation. The financial health of the AATF is generally good. However, airlines’ unbundling of ancillary fees from airfares is adversely affecting AATF revenue, as only base airfares are subject to the ticket tax that is the largest source of revenue for the trust fund. Reductions in AATF revenue would leave FAA more reliant on appropriations from the general fund. Other major issues likely to arise during the reauthorization debate include the following:

Air traffic control privatization. Many commissions over the years have recommended moving responsibility for air traffic control from FAA, a government agency, to either an independent government-owned corporation or a private entity controlled by aviation stakeholders. Delays in implementing the satellite-based NextGen air traffic control system have renewed interest in this possibility, although Congress chose not to enact such proposals in 2016.

Unmanned aerial vehicles. Large numbers of drones have come into use, and the numerous reports of near-collisions between drones and manned aircraft raise safety concerns. Additionally, Congress has not addressed privacy concerns related to government-operated, commercial, and recreational drones.

Essential Airline Service (EAS). Congress has repeatedly attempted to limit the number of localities eligible to participate in this program to subsidize flights to communities that would otherwise lose all commercial airline service, as well as to limit the amount of subsidies per passenger. Few communities have been dropped from the program, and costs continue to rise.

Foreign airlines. Some U.S. airlines and airline labor unions seek reconsideration of the recent U.S. approval of a foreign carrier permit for Norwegian Air International, an Ireland-based discount air carrier, to fly across the Atlantic. Some U.S. carriers also have called for renegotiation of U.S. air service agreements with Persian Gulf states amid claims that three fast-growing airlines based in that region are posing unfair competition to U.S. air carriers.

Certification reform. FAA relies heavily on aircraft and aircraft parts manufacturers to provide technical expertise in the certification process. FAA oversight has been found to be inconsistent, raising questions regarding safety and efficiency. Equipment manufacturers have raised concerns that FAA’s certification process makes it difficult to bring new products to market in a timely fashion and threatens their international competitiveness.

This report does not attempt to be comprehensive. Many issues debated prior to passage of the FAA Extension, Safety, and Security Act of 2016 are not discussed unless further congressional consideration appears probable. Additional issues, not discussed in this report, may arise as Congress moves forward with reauthorization.

Reauthorization of the Federal Aviation Administration (FAA) in the 115th Congress

Jump to Main Text of Report

Contents

- Introduction

- Aviation Funding

- FAA Funding Accounts

- Airport Financing

- Evaluating Capital Needs

- Airport Improvement Program (AIP)

- AIP Funding

- Funding Distribution

- Entitlements (Formula Funds)

- Discretionary Funds

- State Block Grant Program

- The Federal Share of AIP Matching Funds

- Distribution of AIP Grants by Airport Size

- Grant Assurances

- Passenger Facility Charges

- Airport Privatization

- Types of Airport Privatization

- The Interests at Stake

- The Airport Privatization Pilot Program (APPP)

- Participation in APPP

- Why Has the APPP Not Stimulated Privatization?

- APPP Application Process

- Regulatory Conditions and Obligations

- Adequate Access to Funding

- Policy Issues Related to Privatization

- Aircraft Noise Issues

- The Next Generation Air Transportation System (NextGen)

- NextGen Evolution

- Elements and Funding

- Current Status

- Aircraft Equipage

- Anticipated Benefits

- Policy Concerns

- FAA Organizational Issues

- Facility Consolidation

- The Federal Contract Tower (FCT) Program

- Technological Developments Affecting Potential Safety Impacts of Possible Future Tower Closures or Facility Consolidations

- Facility Security and Continuity of Operations

- Air Traffic Control Privatization

- Controller Selection and Hiring

- Aviation Safety Issues

- Airline Safety

- Pilot and Airline Crew Fatigue

- Airline Pilot Qualifications and Pilot Supply

- Commercial Aircraft Tracking and Flight Data Recorders

- Satellite Tracking

- Deployable Recorders

- Oversight of Maintenance and Repair Stations

- Safety and Reliability Issues

- Regulatory Oversight

- The Role of Foreign Regulatory Agencies

- English Language Concerns

- Drug and Alcohol Testing and Substance Abuse Programs

- Airport Surface Movement Safety

- Integration of Unmanned Aircraft Operations

- Enforcement Authority

- Oversight of Commercial Space Activities

- Aircraft and Parts Certification

- Research and Development

- Airline Issues

- Essential Air Service (EAS)

- EAS Funding

- Subsidies

- Small Community Air Service Development Program

- Metropolitan Washington Airports Authority (MWAA)

- Airline Consumer Issues

- Passenger Rights Provisions in 2016 Reauthorization

- Training Regarding Assistance for Persons with Disabilities

- Air Travel Accessibility

- Refunds for Delayed Baggage

- Tarmac Delays

- Family Seating

- Advisory Committee for Aviation Consumer Protection

- International Aviation Issues

Figures

Tables

- Table 1. Aviation Taxes and Fees

- Table 2. Funding Levels for FAA Accounts

- Table 3. Annual AIP Authorizations and Amounts Made Available for Grants, FY2000-FY2017

- Table 4. Distribution of PFC Approvals and AIP Grants by Project Type, FY2016

- Table 5. Full Airport Privatization Under the APPP vs. Outside the APPP

- Table 6. Participation in the APPP

- Table 7. Funding for NextGen Programs

- Table 8. Regulatory Differences Between Domestic and Foreign Repair Stations

Summary

Funding authorization for the Federal Aviation Administration (FAA), included in the FAA Extension, Safety, and Security Act of 2016 (P.L. 114-190), expired at the end of FY2017. A subsequent six-month extension (P.L. 115-63) is set to expire at the end of March 2018. Long-term FAA reauthorization measures (H.R. 2997 and S. 1405) are currently under consideration. In addition to setting spending levels, FAA authorization acts typically set policy on a wide range of issues related to civil aviation. This report considers prominent topics in the 115th Congress reauthorization debate.

Most FAA programs are financed through the Airport and Airway Trust Fund (AATF), which is funded by a variety of taxes and fees on air transportation. The financial health of the AATF is generally good. However, airlines' unbundling of ancillary fees from airfares is adversely affecting AATF revenue, as only base airfares are subject to the ticket tax that is the largest source of revenue for the trust fund. Reductions in AATF revenue would leave FAA more reliant on appropriations from the general fund. Other major issues likely to arise during the reauthorization debate include the following:

- Air traffic control privatization. Many commissions over the years have recommended moving responsibility for air traffic control from FAA, a government agency, to either an independent government-owned corporation or a private entity controlled by aviation stakeholders. Delays in implementing the satellite-based NextGen air traffic control system have renewed interest in this possibility, although Congress chose not to enact such proposals in 2016.

- Unmanned aerial vehicles. Large numbers of drones have come into use, and the numerous reports of near-collisions between drones and manned aircraft raise safety concerns. Additionally, Congress has not addressed privacy concerns related to government-operated, commercial, and recreational drones.

- Essential Airline Service (EAS). Congress has repeatedly attempted to limit the number of localities eligible to participate in this program to subsidize flights to communities that would otherwise lose all commercial airline service, as well as to limit the amount of subsidies per passenger. Few communities have been dropped from the program, and costs continue to rise.

- Foreign airlines. Some U.S. airlines and airline labor unions seek reconsideration of the recent U.S. approval of a foreign carrier permit for Norwegian Air International, an Ireland-based discount air carrier, to fly across the Atlantic. Some U.S. carriers also have called for renegotiation of U.S. air service agreements with Persian Gulf states amid claims that three fast-growing airlines based in that region are posing unfair competition to U.S. air carriers.

- Certification reform. FAA relies heavily on aircraft and aircraft parts manufacturers to provide technical expertise in the certification process. FAA oversight has been found to be inconsistent, raising questions regarding safety and efficiency. Equipment manufacturers have raised concerns that FAA's certification process makes it difficult to bring new products to market in a timely fashion and threatens their international competitiveness.

This report does not attempt to be comprehensive. Many issues debated prior to passage of the FAA Extension, Safety, and Security Act of 2016 are not discussed unless further congressional consideration appears probable. Additional issues, not discussed in this report, may arise as Congress moves forward with reauthorization.

Introduction

The funding authorization for the Federal Aviation Administration (FAA), included in the FAA Extension, Safety, and Security Act of 2016 (P.L. 114-190) and the subsequent Disaster Tax Relief and Airport and Airway Extension Act of 2017 (P.L. 115-63), is now set to expire on March 31, 2018.1 In addition to setting spending levels, FAA authorization acts typically set policy on a wide range of issues related to civil aviation. This report considers topics likely to arise as the 115th Congress continues to debate FAA reauthorization. It does not attempt to be comprehensive. Many issues debated prior to passage of the FAA Extension, Safety, and Security Act of 2016 are not discussed unless further congressional consideration appears probable. Additional issues, not discussed in this report, may arise as Congress moves forward.

Aviation Funding

Most FAA programs are financed through the Airport and Airway Trust Fund (AATF),2 sometimes referred to as the Aviation Trust Fund. The AATF was established in 1970 under the Airport and Airway Development Act of 1970 (P.L. 91-258) to provide for expansion of the nation's airports and air traffic system. Since FY2009, the AATF has provided between 66.6% and 93% of FAA's total annual funding, with the remainder coming from general fund appropriations.3 Revenue sources for the trust fund include passenger ticket taxes, segment fees, air cargo fees, and fuel taxes paid by both commercial and general aviation aircraft (see Table 1).

|

Tax or Fee |

Rate |

|

Passenger ticket tax (on domestic ticket purchases and frequent flyer awards) |

7.5% |

|

Flight segment tax (domestic, indexed annually to Consumer Price Index) |

$4.10 |

|

Cargo waybill tax |

6.25% |

|

Frequent flyer tax |

7.5% |

|

General aviation gasoline |

19.4 cents/gallon |

|

General aviation jet fuela (kerosene) |

21.9 cents/gallon |

|

Commercial jet fuela (kerosene) |

4.4 cents/gallon |

|

International departure/arrivals tax (indexed annually to Consumer Price Index) |

$18.00 |

|

Fractional ownership surtax on general aviation jet fuel |

14.1 cents/gallon |

In addition to excise taxes deposited into the trust fund, FAA imposes air traffic service fees on flights that transit U.S.-controlled airspace but do not take off from or land in the United States. These overflight fees partially fund the Essential Air Service (EAS) program.4

In 2016, the AATF had revenues of over $14.4 billion and maintained a cash balance of more than $14 billion. The uncommitted balance was estimated to be approximately $5.7 billion at the end of FY2016, reversing several years of decline following the onset of the global economic crisis in 2008.5 The trust fund balance is projected to grow in the near term, as AATF revenue continues to rise and airport capital needs are projected to decline over the next five years. In the longer term, however, the vitality of the AATF remains a concern, as reductions in general fund appropriations to FAA have increased the proportion of FAA funding that is derived from the trust fund.

Changes in airline business practices pose a risk to the AATF revenue structure. Trust fund revenue is largely dependent on airlines' ticket sales, and the spread of low-cost air carrier models has held down ticket prices and therefore AATF receipts. In addition, airlines increasingly impose fees for a variety of options and amenities, such as checked bags and onboard meals, rather than including them in the base ticket price. Generally, fees not included in the base ticket price are not subject to federal excise taxes. Air carriers generated over $4.17 billion in baggage fees alone in 2016, which would have brought about $313 million into the trust fund had they been subject to the 7.5% ticket tax.6

Airlines have long contended that general aviation operators, particularly corporate jets, should provide a larger share of the revenues supporting the trust fund. General aviation interests dispute this, arguing that the air traffic system mainly supports the airlines, and that nonairline users pay a reasonable share given the relatively small incremental costs arising from their flights. Proposals in 2012 to increase the general aviation jet fuel tax were not adopted. The Clinton, George W. Bush, and Obama Administrations all proposed per-flight user charges. In the 110th Congress, the Senate voted to impose a $25-per-flight fee on all commercial and general aviation flights (see S. 1300, 110th Congress) as an additional revenue source for the AATF.7 None of those proposals has been enacted into law.

FAA Funding Accounts

In recent years, FAA funding has totaled between $15 billion and $16 billion annually. FAA funding is divided among four main accounts. Operations and Maintenance (O&M) makes up the largest portion of the FAA budget, receiving slightly more than 60% of total FAA appropriations. It is the only FAA account that is funded, in part, by general fund contributions. The O&M account principally funds air traffic operations and aviation safety programs. The Airport Improvement Program (AIP) provides federal grants-in-aid for projects such as new runways and taxiways; runway lengthening, rehabilitation, and repair; and noise mitigation near airports. The Facilities and Equipment (F&E) account provides funding for the acquisition and maintenance of air traffic facilities and equipment, and for engineering, development, testing, and evaluation of technologies related to the federal air traffic system. The Research, Engineering, and Development account finances research on improving aviation safety and operational efficiency and on reducing environmental impacts of aviation operations. Authorizations and appropriations for these accounts are shown in Table 2.

|

Account |

FY2012 |

FY2013 |

FY2014 |

FY2015 |

FY2016 |

FY2017 |

|

Operations and Maintenance (O&M) |

||||||

|

Authorized levels |

9,653 |

9,539 |

9,596 |

9,653 |

9,910 |

9,910 |

|

Appropriated amounts |

9,653 |

9,148 |

9,651 |

9,741 |

9,909 |

10,026 |

|

Airport Improvement Program (AIP) |

||||||

|

Authorized levels |

3,350 |

3,350 |

3,350 |

3,350 |

3,350 |

3,350 |

|

Appropriated amounts |

3,350 |

3,343 |

3,480 |

3,350 |

3,350 |

3,350 |

|

Facilities and Equipment (F&E) |

||||||

|

Authorized levels |

2,731 |

2,715 |

2,730 |

2,730 |

2,855 |

2,855 |

|

Appropriated amounts |

2,731 |

2,588 |

2,600 |

2,600 |

2,855 |

2,855 |

|

Research, Engineering, and Development |

||||||

|

Authorized levels |

168 |

168 |

168 |

168 |

166 |

166 |

|

Appropriated amounts |

168 |

159 |

133 |

157 |

166 |

177 |

|

TOTALS |

||||||

|

Authorized levels |

15,902 |

15,772 |

15,814 |

15,901 |

16,281 |

16,281 |

|

Appropriated amounts |

15,902 |

15,238 |

15,864 |

15,848 |

16,281 |

16,407 |

Source: CRS analysis of P.L. 114-190, P.L. 112-55 (FY2012 Appropriations), P.L. 113-6 (FY2013 Appropriations), P.L. 113-76 (FY2014 Appropriations), P.L. 113-235 (FY2015 Appropriations), P.L. 114-113 (FY2016 Appropriations), P.L. 115-31 (FY2017 Appropriations).

Note: The partial FY2018 funding provided by P.L. 115-63 extended funding at the annualized FY2017 level through March 31, 2018. For more information, see CRS Insight IN10795, Short-Term FAA Extension in Place, but Legislative Debate Continues, by [author name scrubbed] and [author name scrubbed].

Airport Financing8

The federal government supports the development of airport infrastructure in three different ways. First, the AIP provides federal grants to airports for planning and development, mainly of capital projects related to aircraft operations such as runways and taxiways. Second, Congress has authorized airports to assess a local passenger facility charge (PFC) on each boarding passenger, subject to specific federal approval. PFC revenues can be used for a broader range of projects than AIP funds, including "landside" projects such as passenger terminals and ground access improvements. Third, federal law grants investors preferential income tax treatment on interest income from bonds issued by state and local governments for airport improvements (subject to compliance with federal rules). Airports may also draw on state and local funds and on operating revenues such as lease payments and landing fees.

Different airports use different combinations of AIP funding, PFCs, tax-exempt bonds, state and local grants, and airport revenues to finance particular projects. Small airports are more likely to be dependent on AIP grants than large or medium-sized airports. Larger airports are much more likely to issue tax-exempt bonds or finance capital projects with the proceeds of PFCs. Each of these funding sources places various legislative, regulatory, or contractual constraints on airports that use it. The availability and conditions of one source of funding may also influence the availability and terms of other funding sources. In a 2007 study, GAO found that bonds financed 50% of airports' capital spending, AIP 29%, PFCs 17%, state and local contributions 4%, and airport revenue 4%.9

Evaluating Capital Needs

The assessment of airport capital needs is fundamental to determining the appropriate federal support needed to foster a safe and efficient national airport system.10 The federal government's interest goes beyond capacity issues to include implementation of federal safety and noise policies.

The U.S. passenger airline industry has seen a wave of bankruptcies and several major airline mergers since 2000, including the merger of American Airlines and U.S. Airways in 2013. Consolidation led to a reduction in the number of commercial flights between 2005 and 2009. Since that year, the number of commercial flights has been fairly steady, but at a level 15% to 18% lower than in 2005, as carriers have consolidated operations and eliminated some duplicative hubs and routes.11 Government data indicate that domestic airlines have shown considerable capacity discipline; instead of adding flights, they have been flying fuller planes, with an average load factor nearly 85% in 2017.12 The reduced number of flights may ease the pressure on airport and air traffic control facilities.

Both FAA and the Airports Council International-North America (ACI-NA) have issued projections of airports' long-term financial needs. FAA estimated in its report that the national system's capital needs for FY2017-FY2021 will total $32.5 billion (an annual average of $6.5 billion).13 The ACI-NA capital needs survey resulted in an estimate of $99.9 billion over the same years (an annual average of $20 billion).14 The main reason for the widely differing estimates was disparate views on what kinds of airport projects to include.15

The FAA estimate was based on information taken from airport master plans and state system plans, but FAA planners screened out planned projects not justified by aviation activity forecasts or not eligible for AIP grants. Only designated airports were included in the FAA study. Implicit in this methodology is that the planning has been carried through to the point where financing is identified. The ACI-NA study casts a substantially wider net. It includes projects funded by PFCs, bonds, or state or local funding; airport-funded air traffic control facilities; security projects funded by airports or the Transportation Security Administration (TSA); "necessary" AIP-ineligible projects such as parking facilities, hangars, revenue portions of terminals, and off-airport roads and transit facilities; and AIP-eligible projects for which AIP funding was not requested. These additions cause the ACI-NA estimate of capital needs to be far higher than the FAA estimate.

FAA has devoted particular attention to evaluating capital needs at the largest airports, which handle the vast majority of commercial passenger boardings. The agency has undertaken three studies to determine which improvements at major airports are most critical to increasing system capacity. The most recent such study, called FACT3, was released in January 2015.16 FACT3 concluded that the nationwide air traffic system has become more reliable and that congestion has been reduced, due to the combined effects of structural change in the airline industry as well as the addition of 18 new runways and 7 extended runways at the busiest hub airports since 2000. FACT3 indicated that while NextGen is helping to manage delays caused by airport congestion, new capacity and other solutions are still necessary to address traffic growth and reduce delays at some of the largest and busiest airports. The study found that while capacity constraints across the aviation system may not be as dire as in previous analyses, several of the busiest airports would continue to be capacity-constrained in the near term, including all the New York City-area airports, Philadelphia International Airport, and Hartsfield-Jackson Atlanta International Airport.17

Airport Improvement Program (AIP)

The AIP provides federal grants to airports for airport development and planning. Participants range from very large publicly owned commercial airports to small general aviation airports that may be privately owned but are available for public use.18 AIP funding is usually limited to construction of improvements related to aircraft operations, such as runways and taxiways. Commercial revenue-producing facilities are generally not eligible for AIP funding, nor are operating costs.19 The structure of AIP funds distribution reflects congressional priorities and the objectives of assuring airport safety and security, increasing airport capacity, reducing congestion, helping fund noise and environmental mitigation costs, and financing small state and community airports.

The main financial advantage of the AIP to airports is that as a grant program, it can provide funds for capital projects without the financial burden of debt financing, although airports are required to provide a relatively modest local match to the federal funds. Limitations on the use of AIP grants include the range of projects that the AIP can fund and the requirement that recipients adhere to all program regulations and grant assurances.

Federal law requires the Secretary of Transportation to publish a national plan for the development of public-use airports in the United States. This appears as a biannual FAA publication called the National Plan of Integrated Airport Systems (NPIAS).20 For an airport to receive AIP funds, it must be listed in the NPIAS.

AIP Funding

The AIP program structure and authorizations are set in FAA authorization acts. AIP spending authorized and the amounts made available for grants since FY2000 are illustrated in Table 3.

Table 3. Annual AIP Authorizations and Amounts Made

Available for Grants, FY2000-FY2017

(dollars in millions)

|

Fiscal Year |

Authorization |

Grant Amounts Available |

|

2000 |

$2,475 |

$1,851 |

|

2001 |

$3,200 |

$3,140 |

|

2002 |

$3,300 |

$3,223 |

|

2003 |

$3,400 |

$3,295 |

|

2004 |

$3,400 |

$3,294 |

|

2005 |

$3,500 |

$3,384 |

|

2006 |

$3,600 |

$3,424 |

|

2007 |

$3,700 |

$3,402 |

|

2008 |

$3,675 |

$3,471 |

|

2009 |

$3,900 |

$3,385 |

|

2010 |

$3,515 |

$3,378 |

|

2011 |

$3,515 |

$3,378 |

|

2012 |

$3,350 |

$3,199 |

|

2013 |

$3,350 |

$3,192 |

|

2014 |

$3,350 |

$3,194 |

|

2015 |

$3,350 |

$3,193 |

|

2016 |

$3,350 |

$3,192 |

|

2017 |

$3,350 |

Sources: FAA, AIP Annual Report of Accomplishments, 2009, and data from FAA Airports Branch. Amounts made available for grants do not include obligations used for administration expenses, the Small Community Air Service Program, and some research funding.

After trending upward from FY1982 to FY1992, grant funding approved in annual appropriations declined through the mid-1990s as part of federal deficit reduction efforts, leaving large gaps between authorized AIP spending levels and the amounts the program was actually allowed to expend. The Wendell H. Ford Aviation Investment and Reform Act for the 21st Century (AIR-21; P.L. 106-181), enacted in 2000, provided major increases in the AIP's authorization, starting in FY2001. The amount available for grants peaked at $3.47 billion in FY2008. The FAA Modernization and Reform Act of 2012 authorized funding through FY2015 at an annual level of $3.35 billion. The FAA Extension, Safety, and Security Act of 2016 authorized funding through FY2017 at an annual level of $3.35 billion. A six-month extension, included in the Disaster Tax Relief and Airport and Airway Extension Act of 2017 (P.L. 115-63), continued federal funding through March 2018.

|

Current AIP Funding Guarantees Historically, FAA authorization acts have included provisions designed to compel appropriators to both fully expend annual trust fund revenues and fully fund FAA's capital programs: the AIP and Facilities and Equipment (F&E).21 The current guarantee requires that total budget resources made available from the trust fund in any year (including appropriations and obligation limitations) for the AIP, F&E, research and development, and the trust fund share of FAA operations must be equal to the sum of 90% of the revenues for the year plus the amount calculated by subtracting the amount made available from the trust fund from the actual revenues received, based on the data from the fiscal year two years prior to the current fiscal year. This guarantee is enforced by making it out of order in both the House and the Senate to consider any provision that does not adhere to the guarantees. Point-of-order enforcement provisions have had limited success in the past. This is largely because points of order may be waived by the Rules Committee in the House, and points of order are rarely raised against conference reports in the Senate. |

Funding Distribution

The distribution system for AIP grants is complex. It is based on a combination of formula grants (also referred to as apportionments or entitlements) and discretionary funds.22 Each year, the entitlements are first apportioned by formula to specific airports or types of airports. Once the entitlements are satisfied, the remaining funds are defined as discretionary funds. Airports apply for discretionary funds for projects in their airport master plans. Formula grants and discretionary funds are not mutually exclusive, in the sense that airports receiving formula funds may also apply for and receive discretionary funds. Grants are generally awarded directly to airports.

Entitlements (Formula Funds)

Entitlements are funds that are apportioned by formula to airports, and may generally be used for any eligible airport improvement or planning project. These funds are divided into four categories: primary airports, cargo service airports, general aviation airports, and Alaska supplemental funds. Each category distributes AIP funds by a different formula.

Most airports have up to three years to use their apportionments. Non-hub commercial service airports have up to four years. The formula distributions are contingent on an annual AIP obligation limitation of $3.2 billion or more. If this threshold is not met in a particular fiscal year, most formulas revert to prior authorized funding formulas.

Primary Airports. The apportionment for airports that board more than 10,000 passengers each year is based on the number of boardings (also referred to as enplanements) during the prior calendar year.23 The amount apportioned for each fiscal year is equal to double the amount that would be received according to the following formulas:

- $7.80 for each of the first 50,000 passenger boardings;

- $5.20 for each of the next 50,000 passenger boardings;

- $2.60 for each of the next 400,000 passenger boardings;

- $0.65 for each of the next 500,000 passenger boardings; and

- $0.50 for each passenger boarding in excess of 1 million.

The minimum allocation to any primary airport is $1 million. The maximum is $26 million.24

Cargo service airports. Some 3.5% of AIP funds subject to apportionment are apportioned to airports served by all-cargo aircraft with a total annual landed weight of more than 100 million pounds. The allocation formula is the proportion of the individual airport's landed weight to the total landed weight at all cargo service airports.25

General aviation airports. General aviation, reliever, and nonprimary commercial service airports are apportioned 20% of AIP funds subject to apportionment. From this share, all airports, excluding all nonreliever primary airports, receive the lesser of the following:

- $150,000 or

- one-fifth of the estimated five-year costs for airport development for each of these airports as listed in the most recent NPIAS.

Any remaining funds are distributed according to a state-based population and area formula. FAA makes the project decisions on the use of these funds in consultation with the states. Although FAA has ultimate control, some states view these funds as an opportunity to address general aviation needs from a statewide, rather than a local or national, perspective.26

Alaska supplemental funds. Funds are apportioned to airports in Alaska to assure that Alaskan airports receive at least twice as much funding as they did under the Airport Development Aid Program in 1980.27

Forgone apportionments. Large and medium hub airports that collect a passenger facility charge of $3 or less have their AIP formula entitlements reduced by an amount equal to 50% of their projected PFC revenue for the fiscal year until they forgo or give back 50% of their AIP formula grants. In the case of PFC above the $3 level, the percentage forgone is 75%. A special small airport fund, which provides grants on a discretionary basis to airports smaller than medium hub, gets 87.5% of these forgone funds. The discretionary fund gets the remaining 12.5%.

Discretionary Funds

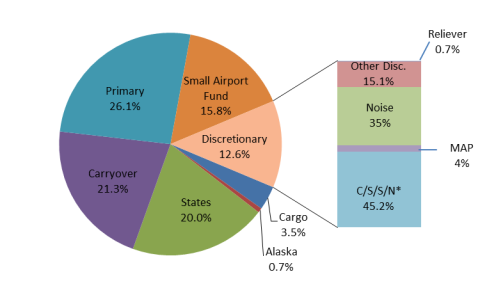

The discretionary fund includes the money not distributed under the apportioned entitlements, as well as the forgone PFC revenues that were not deposited into the small airport fund. AIP discretionary funding for FY2016 was about 13% of total AIP funding. Discretionary grants are approved by FAA based on project priority and other selection criteria. Figure 1 illustrates the composition of both apportioned and discretionary grants, based on FY2016 data.

Despite its name, the discretionary fund is not allocated solely at FAA's discretion. Allocations are subject to the following three set-asides and certain other spending criteria:

- Airport noise set-asides. At least 35% of discretionary funds are set aside for noise compatibility planning and for carrying out noise abatement and compatibility programs.

- Military Airport Program. At least 4% of discretionary funds are set aside for conversion and dual use of up to 15 current and former military airports. The program allows funding of some projects not normally eligible under the AIP.

- Grants for reliever airports. Two-thirds of 1% of discretionary funds are set aside for reliever airports in metropolitan areas suffering from flight delays.28

The Secretary of Transportation is also directed to see that 75% of the grants made from the discretionary fund are used to preserve and enhance capacity, safety, and security at primary and reliever airports, and also to carry out airport noise compatibility planning and programs at these airports. From the remaining 25%, FAA is required to set aside $5 million for the testing and evaluation of innovative aviation security systems.

Subject to these limitations and the three set-asides, the Secretary of Transportation, through FAA, has discretion in distribution of grants from the remainder of the discretionary fund.29

State Block Grant Program30

Under this program, FAA provides funds directly to participating states for projects at airports classified as other than primary airports. Each participating state receives a block grant made up of the state's apportionment (formula) funds and available discretionary funds. A block grant program state is responsible for selecting and funding AIP projects at the small airports in the state. In making the selections, the participating states are required to comply with federal priorities. Each block grant state is responsible for project administration as well as most of the inspection and oversight roles normally assumed by FAA. The states that currently participate in the state block grant program are Georgia, Illinois, Michigan, Missouri, New Hampshire, North Carolina, Pennsylvania, Tennessee, Texas, and Wisconsin.

The Federal Share of AIP Matching Funds

For AIP projects, the federal government share differs depending on the type of airport.31 The federal share, whether funded by formula or discretionary grants, is as follows:

- 75% for large and medium hub airports (80% for noise compatibility projects);

- 90% for other airports;

- "not more than" 90% for airport projects in states participating in the state block grant program;

- 70% for projects funded from the discretionary fund at airports receiving exemptions under 49 U.S.C. Section 47134, the pilot program for private ownership of airports;

- airports reclassified as medium hubs due to increased passenger volumes may retain eligibility for up to a 90% federal share for a two-year transition period;

- certain economically distressed communities receiving subsidized air service may be eligible for up to a 95% federal share of project costs.

This cost-share structure means that smaller airports pay a lower share of AIP-funded project costs than larger airports. The airports themselves must raise the remaining share from other sources.32

Distribution of AIP Grants by Airport Size

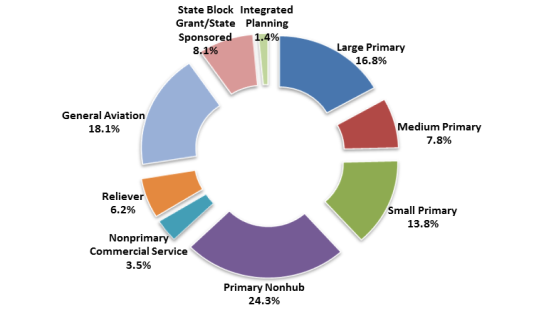

Although smaller airports' individual grants are of much smaller dollar amounts than the grants going to large and medium hub airports, the smaller airports are much more dependent on the AIP to meet their capital needs. This is particularly the case for noncommercial airports, which received over 27% of AIP grants distributed in FY2016. Figure 2 shows the share of AIP grants awarded in FY2016, by value, broken out by airport type.

|

|

Source: Data from FAA Airports Branch. |

Grant Assurances

Airports' grant applications are conditioned on assurances regarding future airport operations. Examples of such assurances include making the airport available for public use on reasonable conditions and without unjust economic discrimination (against all types, kinds, and classes of aeronautical activities); charging air carriers making similar use of the airport substantially comparable amounts; maintaining a current airport layout plan; making financial reports to FAA; and expending airport revenue only on capital or operating costs at the airport.33 Within the AIP context, assurances are a means of guaranteeing the implementation of federal policy.

Obligations derived from airports' assurances extend beyond the formal closure of AIP grant-supported projects. Obligations related to the use, operation, and maintenance of an airport remain in effect for the expected life of the improvement, up to 20 years. In the case of the purchase of land with AIP funds, the federal obligations do not expire.34 Airports may request that FAA release them from their AIP contractual obligations. Typically, as a condition of the release, the airport sponsor must either reimburse the federal government for the AIP grants (in the case of land grants, the federal share of the fair market value of the land) or reinvest the amount in an approved AIP project.35

Decisions about which airport expansion projects are most justified have implications for the reauthorization of the AIP. Large runway projects can require long lead times—10 or more years from concept to initial construction is not unusual. At large and medium hub airports, runway projects are usually paid for, in part, by AIP funds. Therefore, some projects needed by 2025 may require AIP funding in earlier years. Because large and medium airports must forgo either 50% or 75% of their AIP formula entitlement funds if they levy passenger facility charges (see below), most federal funding for their runway projects will probably need to take the form of AIP discretionary funds. If the AIP budget is constrained in the future, either under a reauthorization bill or during the annual appropriations process, and the entitlement formulas remain as they are, the discretionary portion of the AIP budget may be squeezed, limiting large airports' ability to draw on AIP funds for major capacity expansion projects.

There are several ways Congress might shift AIP funds if it seeks to give priority to enhancing capacity at large and medium hub airports. One would be to eliminate the requirement that large and medium hub airports that impose the maximum PFCs forgo 75% of their entitlement. This change would give larger airports a greater share of entitlement funding, but at the cost of depleting the discretionary small airport fund and reducing AIP grants to small airports. Alternatively, changes in the statutory set-asides of discretionary funds could give FAA more flexibility to use that money for capacity enhancement, but might reduce funding for noise mitigation and other purposes.

The current AIP structure and funding mechanism generally tend to benefit airports smaller than medium hub size. In particular, the increased amount of apportioned funds has limited the availability of funds for discretionary grants, such as those for operational evolution plan projects at major airports. Policy changes giving airports increased flexibility in the use of their entitlements might benefit smaller airports not served by commercial aviation, in line with the national goal of having an "extensive" national airport system,36 but this use of funds might conflict with the goal of reducing congestion at major commercial airports.

One way to reduce the amount of trust fund revenue needed for the AIP would be to allow large and medium hub airports to opt out of the AIP and rely exclusively on PFCs to finance capital projects. This would require raising or eliminating the federal cap on PFCs. These "defederalized" airports could then be released from some or all of the AIP grant assurances under which they now operate, such as land use requirements and airport revenue use restrictions.37 If airports exit the program, AIP spending could be reduced or redirected to other airports.

Passenger Facility Charges

In 1990, concerns that existing sources of funds for airport development would be insufficient to meet national needs led to authorization of a new user charge, the passenger facility charge (PFC). The PFC was seen as a complementary funding source to the AIP. The Aviation Safety and Capacity Expansion Act of 199038 allowed the Secretary of Transportation to authorize public agencies that control commercial airports to impose a fee on each paying passenger boarding an aircraft at their airports. Initially, there was a $3 cap on each airport's PFC and a $12 limit on the total PFCs that a passenger could be charged per round trip.

The PFC is a state, local, or port authority fee, not a federally imposed tax deposited into the Treasury.39 Because of the complementary relationship between the AIP and PFCs, PFC provisions are generally folded into the sections of FAA reauthorization legislation dealing with the AIP. The money raised from PFCs must be used to finance eligible airport-related projects. Unlike AIP funds, PFC funds may be used to service debt incurred to carry out projects.40

Legislation in 2000 raised the PFC ceiling to $4.50, with an $18 limit on the total PFCs that a passenger can be charged per round trip. To impose a PFC above $3, an airport has to show that the funded projects will make significant improvements in air safety, increase competition, or reduce congestion or noise impacts on communities, and that these projects could not be fully funded by using the airport's AIP formula funds or AIP discretionary grants. Large and medium hub airports imposing PFCs above the $3 level forgo 75% of their AIP formula funds. PFCs at large and medium hub airports may not be approved unless the airport has submitted a written competition plan to FAA, which includes information about the availability of gates, leasing arrangements, gate-use requirements, controls over airside and ground-side capacity, and intentions to build gates that could be used as common facilities.

The FAA Modernization and Reform Act of 2012 included minor changes to the PFC program. The act made permanent the pilot program that authorized non-hub small airports to impose PFCs. The act also required GAO to study alternative means of collecting PFCs without including the PFC in the ticket price.41 The FAA Extension, Safety, and Security Act of 2016 did not include significant changes to the PFC program.

Unlike AIP grants, of which over 70% in FY2016 went to airside projects (runways, taxiways, aprons, and safety-related projects), PFC revenues are heavily used for landside projects such as terminals and transit systems on airport property, and for interest payments. Table 4 shows the AIP grant awards and PFC approvals by project type in FY2014. Annual system-wide PFC collections grew from $85.4 million in 1992 to over $3 billion in 2016.42

|

Type of Project |

PFC |

AIP |

|

Airside |

15.7% |

71.1% |

|

Landside |

60.2% |

12.3% |

|

Noise |

0.0% |

4.4% |

|

Roads/Access |

2.6% |

0.6% |

|

Interest on Bonds |

21.4% |

— |

|

Unclassified, State Block Grants, Misc. |

— |

11.7% |

|

Total |

100.0% |

100.0% |

Source: FAA, Airports Branch.

The PFC statutory language lends itself to a broader interpretation of "capacity enhancing" projects, and the implementing regulations are less constraining than those for AIP funds. Air carriers, which historically have preferred funding to be dedicated to airside projects, must be notified and provided with an opportunity for consultation about airports' proposals to fund projects with PFC revenues. They are generally less involved in the PFC project planning and decision-making process than is the case with AIP projects. The difference in the pattern of project types may also be influenced by the fact that larger airports, which collect most of the PFC revenue, tend to have substantial landside infrastructure, whereas smaller airports that are much more dependent on AIP funding have comparatively limited landside facilities.

The central legislative issue related to PFCs is whether to raise or eliminate the $4.50 per enplaned passenger ceiling.43 In general, airports argue for increasing or eliminating the ceiling, whereas most air carriers and some passenger advocates oppose higher limits on PFCs. A GAO study released in January 2015 modeled several scenarios of higher PFCs, and found that raising the cap would significantly increase PFC collections available to airports. However, the GAO report suggests that higher PFCs could also marginally slow passenger growth, and therefore the growth in revenues to the Airport and Airway Trust Fund.44

The permissible uses of revenues are an ongoing point of contention. Airport operators, in particular, would like more freedom to use PFC funds for off-airport projects, such as transportation access projects, and want the process of obtaining FAA approval to be streamlined. Carriers, on the other hand, often complain that airports use PFC funds to finance proposals of dubious value, especially outside airport boundaries, instead of high-priority projects that offer meaningful safety or capacity enhancements. The major air carriers are also unhappy with their limited influence over project decisions, as airports are required only to consult with resident air carriers instead of having to get their agreement on PFC-funded projects.

Airport Privatization45

Almost all commercial service airports in the United States are owned by local and state governments, or by public entities such as airport authorities or multipurpose port authorities.46 In 1996, Congress established the Airport Privatization Pilot Program (APPP)47 to explore the prospect of privatizing publicly owned airports and using private capital to improve and develop them. In addition to reducing demand for government funds, privatization has been promoted as a way to make airports more efficient and financially viable.

Participation in the APPP has been limited. Two airports have completed the privatization process, and one of them later reverted to public ownership. Owners of other airports considered privatization, but eventually chose not to proceed. The lack of interest in privatization among U.S. airports could be the result of (1) readily available financing sources for publicly owned airports; (2) barriers or lack of incentives to privatize; (3) the potential implications for major stakeholders; and (4) satisfaction with the status quo.

Privatization refers to the shifting of governmental functions, responsibilities, and sometimes ownership, in whole or in part, to the private sector. With respect to airports, "privatization" can take many forms up to and including the transfer of an entire airport to private operation and/or ownership. In the United States, most cases of airport privatization fall into the category of "partial privatization;" full privatization, either under or outside the APPP, has been rare.

Types of Airport Privatization

Airport privatization has taken four generic forms:

- Service contracts. Many U.S. airports outsource some noncore operations to private firms that specialize in those functions. Examples of operations that are frequently outsourced are cleaning and janitorial services, airport landscaping, shuttle bus operations, and concessions in airport terminals. Outsourcing of service contracts is probably the most common type of privatization among U.S. airports.

- Management contracts. Some airports engage the management expertise of the private sector by contracting out specific facilities or responsibilities such as parking, terminal concessions, terminal operations, airfield signage, fuel farms, and aircraft refueling. In a few cases, a private management company has been awarded a contract to manage an entire airport for a specified term.

- Developer financing/operation. A wide range of contracts has been used to involve the private sector in providing financing, development, operation, and maintenance services. This is also known as the Design-Build-Finance-Operate-Maintain (DBFOM) model. Airport DBFOM examples include passenger terminals (notably Terminal 5 at Chicago O'Hare International Airport and Terminal 4 at New York John F. Kennedy International Airport), parking garages, and rental car facilities.48

- Long-term lease or sale. Full privatization involves the sale or long-term lease of an airport to a private owner or operator. Under a long-term lease or concession agreement, the airport owner grants full management and development control to the private operator in exchange for capital improvements and other obligations such as an up-front payment and/or profit-sharing arrangements. Under a full sale, ownership and full responsibility for operation, capital improvements, and maintenance would be transferred to a private buyer. Several airports in Europe have been privatized in this way, but there have been no sales of commercial service airports in the United States.

The Interests at Stake

Airport privatization, especially in the case of long-term lease or sale, involves four major stakeholders: airport owners, which in the United States are mostly local or regional governments or public entities; air carriers; private investors; and the federal government. These stakeholders ultimately decide whether a privatization deal goes forward, but they tend to have different objectives and, in many cases, divergent interests. Airline passengers may experience the effect of privatization via, for example, airport concession offerings, operational efficiency, and changes in prices and fees, but passenger interests are usually not represented formally in discussions of privatization.

Airport owners, who are usually local governments, might embrace privatization as a source of revenue, but federal regulations generally require that lease or sale revenue from airport privatization be used only for airport purposes (unless the majority of airlines agrees otherwise, under the APPP). On the other hand, privatization involves surrendering control of an economically important facility. Reducing or eliminating responsibilities of the public agency or authority that owns the airport may lead to the loss of public-sector jobs. Hence a public-sector owner may see few benefits from selling or leasing an airport to a private operator unless the facility is losing money—and in that case, private investors might not find the airport an attractive investment. The APPP encourages privatization by granting certain exemptions to public-sector owners with regard to revenue diversion and other obligations.

Air carriers, including both scheduled passenger airlines and cargo airlines, would like to keep their costs low. They also want to have some control over how airport revenues are used, especially to ensure that the fees paid by themselves and their customers are used for airport-related purposes. Their interest in low landing fees and low rents for ticket counters and other facilities may be contrary to the interest of potential private operators in increasing revenue. At the same time, however, air carriers have an interest in ensuring that the airports they use are well maintained and carefully managed. They might have reason to support a proposed privatization if they thought it would result in lower charges, better airport services, or increased efforts to promote the airport.

Private investors and operators expect a financial return on their investments. They generally will be looking above all at growth potential such as opportunities to bring additional flights to the airport, to earn additional lease revenue by improving amenity offerings such as shopping and dining for passengers, or to draw more freight traffic by offering lower fees or improved facilities. If they attempt to increase profitability by raising landing fees or rents, that may bring them into conflict with air carriers using the airport.

The federal government, represented by FAA, has been directed by Congress to engage private capital in aviation infrastructure development and reduce reliance on federal grants and subsidies. However, FAA also has statutory mandates to maintain the safety and integrity of the national air transportation system and to enforce compliance with commitments, known as "grant assurances," that airports have made to obtain grants under the AIP. Thus FAA is likely to carefully examine privatization proposals that might risk closures of runways or airports or otherwise reduce aviation system capacity, or that appear to favor certain airport users over others.

The divergent interests of stakeholders are a significant issue in privatization. Striking a balance among these interests while facilitating privatization is one of the purposes of the APPP.

The Airport Privatization Pilot Program (APPP)

Section 149 of the Federal Aviation Reauthorization Act of 1996 (49 U.S.C. §47134; P.L. 104-264) authorizes the FAA Administrator to exempt participating airports from all or part of the requirements to use airport revenue for airport-related purposes, to repay federal grants, or to return airport property acquired with federal assistance upon the lease or sale of the airport deeded by the federal government.49 The law originally limited participation in the APPP to no more than five airports. The FAA Modernization and Reform Act of 2012 (P.L. 112-95) increased the number of airports that may participate from 5 to 10. Only one large hub commercial airport may participate in the program, and that airport may only be leased, not sold. Only general aviation airports can be sold under the APPP.

Table 5 provides a comparison of the requirements and regulations governing airport privatization under and outside the APPP.

|

Full Privatization Under APPP |

Full Privatization Outside APPP |

|

|

Eligible Airports |

A maximum of 10 airports may participate, among which only one may be a large hub airport. One slot is reserved for a general aviation airport. Commercial airports may only be leased; general aviation airports may be sold. |

No restrictions on number or type of airports. |

|

Use of Sale/Lease Proceeds |

Airports can request U.S. Department of Transportation (DOT) approval to use sale/lease proceeds for nonairport purposes. For commercial service airports, this also requires consent of 65% of airlines. For general aviation airports, this requires consultation with owners of aircraft based at the airport. |

Sale/lease proceeds are considered airport revenue, and must be used for airport purposes. |

|

Grant Repayment |

DOT may grant exemptions from existing repayment obligations. Airports must abide by other grant assurance obligations. |

DOT cannot grant exemptions from grant assurance obligations or existing repayment obligations. |

|

AIP Formula Grants |

Private operator is eligible for grants from AIP formula funds, but at a lower federal share. |

Private operator may be eligible for grants from AIP formula funds under certain conditions such as when a privately owned airport is used for public purpose as a reliever or provides at least 2,500 passenger boardings a year. |

|

Rates or Charges on Airlines |

Rates on airlines may not rise faster than the inflation rate without consent of 65% of airlines. Rate increases for general aviation aircraft owners may not exceed percentage rate increase for airlines. |

Rates and charges must be reasonable and not unjustly discriminatory, pursuant to grant assurances. |

|

Charges on Passengers |

Private operator is authorized to impose, collect, and use revenue from passenger facility charges (PFCs). |

Private operator is authorized to impose charges on passengers (subject to reasonableness and nondiscrimination requirements of the grant assurances), but not to impose, collect, or use PFCs. |

Source: Federal Aviation Administration.

Participation in APPP

The APPP has had limited success in increasing the number of privately run airports. Since its inception, 11 airports have applied to enter the APPP; two have completed the entire privatization process. One of these later reverted to public ownership. The most recent applicant is Westchester County Airport, NY, which applied to enter the program in December 2016. Table 6 lists the APPP applicants and their status.

|

Status |

Airport |

Location |

Application Results |

|

Inactive |

Brown Field Municipal Airport |

San Diego, CA |

Application withdrawn in 2001. |

|

Inactive |

Chicago Midway International Airport |

Chicago, IL |

Application withdrawn in 2013. |

|

Inactive |

Gwinnett County Briscoe Field Airport |

Lawrenceville, GA |

Application withdrawn in 2012. |

|

Active* |

Hendry County Airglades Airport |

Clewiston, FL |

In August 2014, FAA approved management contract between county and private operator, pending submission of final APPP application by the county. |

|

Inactive |

Louis Armstrong New Orleans International Airport |

New Orleans, LA |

Application withdrawn in 2010. |

|

Privatized* |

Luis Muñoz Marín International Airport |

San Juan, Puerto Rico |

Preliminary approved in December 2009; final application approved in February 2013. Privatized under long-term lease. |

|

Inactive |

New Orleans Lakefront Airport |

New Orleans, LA |

Application terminated in 2008. |

|

Inactive |

Niagara Falls International Airport |

Niagara Falls, NY |

Application withdrawn in 2001. |

|

Inactive |

Rafael Hernandez Airport |

Aguadilla, Puerto Rico |

Application withdrawn in 2001. |

|

Active* |

St. Louis Lambert International Airport |

St. Louis, MO |

Preliminary application accepted in April 2017. |

|

Inactive |

Stewart International Airport |

Newburgh, NY |

Airport privatized in 2000 after FAA approval; reverted to public operation in 2007. |

|

Active* |

Westchester County Airport |

White Plains, NY |

Preliminary application accepted on December 2, 2016. |

Source: Federal Aviation Administration; U.S. Government Accountability Office, Airport Privatization, GAO-15-42, November 2014.

Notes: The rows marked with an asterisk represent the four active participants as of October 2017. FAA terminated New Orleans Lakefront Airport's application when the airport missed the deadline to submit additional materials.

Why Has the APPP Not Stimulated Privatization?

The APPP has had limited success in stimulating wide interest in airport privatization. The program's relatively modest results appear to have several causes.

APPP Application Process

Applying to privatize an airport under the APPP, as reported by FAA, makes the transfer from public to private ownership too "time consuming" and presents risks that could cause a potential deal to fail.50 The application process begins with an airport filing a preliminary application for FAA approval. FAA has 30 days to review the preliminary application. The entire process, however, may take years to complete. In the case of Hendry County Airglades Airport, for example, a preliminary application was approved by FAA in 2010, but final FAA approval is still pending.

Once an airport receives preliminary approval, it then may select a private operator, negotiate an agreement, and submit a final application to FAA. There is no timeline as to how quickly FAA must complete its review of the final application. After FAA gives notice of its proposed approval of the final application and lease agreement in the Federal Register, there is a 60-day public review and comment period. After that, FAA completes its review and prepares its Findings and Record of Decision (ROD), in which it addresses the public comments and publishes the details of its decision.51

Regulatory Conditions and Obligations

Airport privatization under the APPP has a number of regulatory requirements. These requirements may have lessened airport owners' and/or investors' interest in privatization. They include the need for 65% of air carriers serving the airport52 to approve a lease or sale of the airport; restrictions on increases in airport rates and charges that exceed the rate of increase of the Consumer Price Index (CPI); and a requirement that a private operator comply with grant assurances made by the previous public-sector operator to obtain AIP grants.53 In addition, after privatization, the airport will be eligible for AIP formula grants to cover 70% of the cost of improvements, versus the normal 75%-90% federal share at publicly owned airports. This serves as a disincentive to privatize an airport because it will receive less federal money after privatization.

Adequate Access to Funding

In surface transportation, a key purpose of privatization is to attract private capital to supplement public spending that is insufficient to provide the desired level of construction and maintenance.54 In general, lack of resources has been a far less important issue for airport operators than for highway and public transportation agencies.

Publicly owned airports have access to five major sources of funding. The AIP provides federal grants to airports for planning and development, mainly of capital projects related to aircraft operations, such as runways and taxiways.55 Local passenger facility charges of up to $4.50 per boarding passenger, imposed pursuant to federal law, can generate revenue for a broad range of projects including "landside" projects on airport property such as passenger terminals and ground access improvements, and for interest payments. Tax-exempt bonds, often secured by airport revenue, offer less costly financing than is generally available to private entities. Tenant leases, landing fees, and other charges are important revenue sources at some airports. Many airports, especially smaller ones, also benefit from state and local grants.56

These financing arrangements have important implications for airport privatization.

- If a publicly owned airport were to be privatized outside the APPP, its private operator may not be eligible to receive AIP formula funds and may have to draw on its own resources to improve runways and taxiways. The operator would not be entitled to issue bonds with federal tax-exempt status, and would therefore have to pay higher interest rates on its bonds than a public-sector operator. On the other hand, the private operator would have relative freedom to impose passenger usage fees and to increase landing fees, rents, and other charges, so long as this was not done in a discriminatory fashion.

- An airport privatized under APPP would continue to have access to federal AIP grants, although the private operator would have to provide a 30% match, considerably more than the 10%-25% matches required of publicly owned airports. The operator would not be entitled to issue bonds with federal tax-exempt status, and would therefore have to pay higher interest rates on its bonds than a public-sector operator. It could continue to collect passenger facility charges, but could not impose charges higher than those authorized by federal law. Its ability to raise fees paid by air carriers would be constrained.

These limitations are largely the consequence of federal laws. They may explain why airport privatization has been less attractive in the United States than in Europe and Canada.

Two factors that have facilitated privatization in other countries do not exist in the United States. First, many of the major airports that have been privatized in Europe and Canada were previously owned by national governments, not by local or provincial governments, so the decision to privatize did not need to be taken at multiple levels of government. Second, the tax-favored status of debt issued by U.S. state and local governments has no analogue in most other countries, so the shift from public to private ownership did not necessarily entail higher borrowing costs, as it would in the United States.

Policy Issues Related to Privatization

Congress has been interested in airport privatization as a way to save money by making airports less dependent on federal assistance while also, in the long run, increasing the nation's aviation capacity to meet growing demand for air travel. However, under current federal law, privatization has struggled to achieve these goals.

Privatization outside the framework of the APPP is generally unattractive to both airport owners and potential investors. Streamlining the APPP application and review process might make privatization somewhat more attractive by reducing the risks arising from a long application period, such as changes in economic and capital market conditions. However, significantly increasing interest in airport privatization is likely to require structural change to the existing airport financing system. Options might include the following:

- Offering the same tax treatment to private and public airport infrastructure bonds. This could be done by eliminating the current federal income tax exemption of interest on bonds issued by public-sector airport owners or by extending tax-exempt or tax-preferential treatment to airport infrastructure bonds issued by private investors. Either change would eliminate a major disincentive to shift airports from public to private ownership. On the other hand, removing the tax exemption on public-sector airport bonds would raise airports' financing costs, while extending it to private-sector bonds could have consequences for federal revenues.

- Changing AIP requirements. Reducing the percentage match private operators must provide to obtain AIP grants to the level of comparable public operators would make privatization more attractive to private investors, but would increase their share of federal funding.

- Relaxing AIP grant assurances. If private investors were freed from some of the requirements agreed to by the public owner in order to obtain AIP funding, privatization might become more attractive to investors. However, some of the changes that might be most attractive to investors, such as allowing the sale of airport property, might interfere with the federal interest in maintaining aviation system capacity and safety.

- Liberalizing rules governing fees. Allowing privatized airports more flexibility to impose passenger facility charges and to raise rents and landing fees would make privatization more attractive to investors. However, this might increase airline opposition to privatization and could lead to higher costs for passengers and air cargo shippers.

- Easing limits on the use of privatization revenue. Reducing the obstacles for public-sector owners to use privatization revenue for nonairport purposes would stimulate local and state government interest in privatization. On the other hand, it could potentially lead to a lower level of investment in aviation infrastructure.

Aircraft Noise Issues

Noise from aircraft taking off and landing is an issue at many airports. Under the National Environmental Policy Act (NEPA), FAA and airport operators are required to assess environmental impacts, including noise impacts, associated with federally funded airport projects and airspace redesigns. Noise has been a contentious issue in the redesign of airspace in the New York City, New Jersey, and Philadelphia region. Similarly, noise concerns have been raised regarding a number of airport expansion projects, including the completion of a new runway at Chicago's O'Hare International Airport in 2013.

The number of residents in the United States exposed to significant amounts of aircraft noise has declined precipitously, from about 7 million in 1975 to an estimated 320,000 in 2012.57 Major reductions in aircraft noise levels have been achieved over the past 30 years. Louder Stage 2 airliners over 75,000 pounds were phased out in the 1990s, and a provision in the FAA Modernization and Reform Act of 2012 required that all jet airplanes, regardless of size, meet quieter Stage 3 or Stage 4 noise standards by the end of 2015. Newly introduced aircraft types must meet Stage 4 noise standards, and FAA plans to issue rules for even more stringent Stage 5 noise standards.58 Noise reductions have been achieved through quieter engine technologies, greater use of lightweight aircraft materials, and advances in aerodynamics. FAA, in cooperation with the National Aeronautics and Space Administration and industry, has invested in the research and development of quiet aircraft technologies.

While reducing aircraft noise emissions has been highly successful and new aircraft are significantly quieter than their predecessors, the volume of air traffic, particularly around major airports, has increased over the past 30 years. Historically, Congress has addressed airport noise concerns by setting aside 35% of discretionary funding under the AIP for noise mitigation and abatement. Generally, these funds may be used only within the Day Night Average Sound Level (DNL)59 65 decibel (dB) noise impact area around an airport. Proposals to grant FAA the flexibility to routinely fund noise mitigation projects in areas with lower DNL levels would enable it to support additional abatement projects, but could divert resources from capacity and safety projects. A related issue is whether to make the planning for noise-mitigating air traffic control procedures at individual airports eligible for AIP funding.

The Next Generation Air Transportation System (NextGen)

NextGen refers to the Next Generation Air Transportation System, a large-scale modernization of air traffic technologies and procedures intended to expand national airspace system capacity to meet future demand. NextGen is a multiyear initiative to modernize and improve the efficiency of the national airspace system, primarily by migrating to technologies and procedures using satellite-based navigation and aircraft tracking. Initiated in legislation in 2003 (see P.L. 108-176), the NextGen system targets full-scale implementation by 2025.

With regard to air traffic management, the goals of NextGen include

- reduced air traffic separation;

- flexible spacing and sequencing of aircraft, both in the air and on the ground;

- increased utilization of airspace, airports, and runways, particularly those that are currently underutilized;

- improved and tailored weather forecasts; and

- reductions in environmental impacts of noise and emissions.60

In 2003, Vision 100—Century of Aviation Reauthorization Act (P.L. 108-176) established an interagency Joint Planning and Development Office (JPDO) within FAA to develop and implement an integrated plan for the Next Generation Air Transportation System (NGATS, now known as NextGen) capable of meeting the needs associated with projected air traffic demands in 2025. The act also established a senior policy committee to consult with industry stakeholders and advise the Secretary of Transportation on goals and strategic objectives for transforming the national airspace system to meet future needs and provide policy guidance to the JPDO.

In 2004, the JPDO released its first iteration of the Integration National Plan for NextGen. The NextGen integrated plan, as envisioned, seeks to ensure that the NextGen system meets air transportation safety, security, mobility, efficiency, and capacity needs by 2025. It contends that if steps are not taken to alleviate air travel congestion through NextGen in concert with airport capacity expansion, the annual cost to consumers related to air traffic delays and flight cancellations could be as high as $20 billion by 2025.61

The FAA Modernization and Reform Act of 2012 refined and expanded several facets of NextGen implementation. It established the position of Chief NextGen Officer within FAA, and redesignated the JPDO director as Associate Administrator for NextGen Planning and Development and Interagency Coordination. The act required the NextGen Senior Policy Committee to submit annual progress reports to Congress. It also ordered a U.S. Department of Transportation Office of Inspector General (DOT OIG) review of the Automated Dependent Surveillance (ADS-B) ground system installation and deployment of ADS-B services, and a National Research Council review of the enterprise architecture for NextGen. The act directed FAA to accelerate the deployment of NextGen technologies and procedures and defined specific national airspace performance metrics that FAA must track. Other provisions required FAA to evaluate the role of airport surveillance technologies in the implementation of NextGen airport surface operations management; authorized the establishment of a NextGen research and development center of excellence; and authorized public-private partnerships to leverage and maximize private-sector capital for the purpose of equipping general aviation and commercial aircraft with NextGen avionics. FAA is to report to Congress on its initiatives to encourage NextGen equipage, including policies that give priority handling to ADS-B-equipped aircraft.

The Consolidated Appropriations Act of 2014 (P.L. 113-76) defunded the JPDO for FY2014 and directed FAA to absorb the JPDO's functions into its operations account under the NextGen and operations planning activity. In May 2014, FAA moved the JPDO functions into a newly created NextGen Interagency Planning Office.

NextGen Evolution

A report by the Ash Center for Democratic Governance and Innovation at Harvard University described NextGen as "one of the most significant efforts of cross-boundary transformation ever contemplated by the United States government and its industry partners."62 The report observed that the NextGen concept eliminates the historical delineation between air traffic control infrastructure and aircraft navigation and communications devices by integrating certain elements of the underlying infrastructure into cockpit instrumentation.63

The genesis of core NextGen technological concepts was the effort of the cargo airline industry to develop low-cost collision avoidance and aircraft tracking technologies. In the 1990s, cargo airlines were exempted from regulations requiring transport-category aircraft to be equipped with traffic collision avoidance systems (TCAS). The cargo airlines' initiatives to develop a low-cost alternative to TCAS that could also provide airline fleet tracking capabilities using Global Positioning System (GPS) technology led to the initial development of core NextGen cockpit technologies.

In 1999, express cargo carrier UPS received accolades for its role in developing ADS-B technology, now considered the backbone of the NextGen system. Its subsidiary, UPS Aviation Technologies, played a major part in developing ADS-B avionics that were flight-tested by UPS airplanes under FAA's Ohio River Valley demonstration project, a component of its Safe Flight 21 research-and-development program in the 1990s. UPS Aviation Technologies was subsequently acquired by Garmin Ltd. in 2003. Garmin has since positioned itself as a major supplier of GPS navigation devices, ADS-B equipment, and advanced avionics, primarily for small to midsized general aviation aircraft.

Also, in 1999, FAA initiated the Capstone Program in Alaska to explore the potential safety benefits of GPS, ADS-B, advanced avionics, and flight information service broadcasts for general aviation operations. The research program served as a test bed for technologies that came to form the core of the NextGen initiative.