Department of Education Funding: Key Concepts and FAQ

Like most federal agencies, the Department of Education (ED) receives funds in support of its mission through various federal budget and appropriations processes. While not unique, the mechanisms by which ED receives, obligates, and expends funds can be complex. For example, ED receives both mandatory and discretionary appropriations; ED is annually provided forward funds and advance appropriations for some—but not all—discretionary programs; ED awards both formula and competitive grants; and a portion of ED’s budget subsidizes student loan costs (direct loans and loan guarantees). As such, analyzing ED’s budget requires an understanding of a broad range of federal budget and appropriations concepts. This report provides an introduction to these concepts as they are used specifically in the context of the congressional appropriations process for ED.

The first section of this report provides an introduction to key terms and concepts in the federal budget and appropriations process for ED. In addition to those mentioned above, the report includes explanations of terms and concepts such as authorizations versus appropriations; budgetary allocations, discretionary spending caps, and sequestration; transfers and reprogramming; and matching requirements.

The second section answers frequently asked questions about federal funding for ED or education in general. These are as follows:

How much funding does ED receive annually?

How much does the federal government spend on education?

Where can information be found about the President’s budget request and congressional appropriations for ED?

How much ED funding is in the congressional budget resolution?

What is the difference between the amounts in appropriations bills and report language?

What happens to education funding if annual appropriations are not enacted before the start of the federal fiscal year?

What happens if an ED program authorization “expires”?

The third section includes a brief description of, and links to, reports and documents that provide more information about budget and appropriations concepts.

Department of Education Funding: Key Concepts and FAQ

Jump to Main Text of Report

Contents

- Introduction

- Key Concepts and Terms

- Budget Authority, Obligation, Outlay, and Rescission

- Authorizations and Appropriations

- "Authorization of Appropriations"

- Discretionary and Mandatory Spending (Including Appropriated Mandatory Spending)

- 302(a) and 302(b) Allocations

- Fiscal Year, Award Year, and Other Units of Time

- "Carry Forward," Advance Appropriations, and Forward Funding

- Budget Caps and Sequestration

- Discretionary Spending Limits

- Mandatory Spending Sequestration

- The BCA and ED Funding

- Transfer and Reprogramming

- Formula and Competitive Grants

- Block and Categorical Grants

- Matching Funds or Requirements

- Frequently Asked Questions

- How much funding does the Department of Education receive annually?

- How much does the federal government spend on education?

- Where can information be found about the President's budget request and congressional appropriations for the Department of Education?

- How much ED funding is in the congressional budget resolution?

- What is the difference between the amounts in appropriations bills and report language?

- What happens to education funding if annual appropriations are not enacted before the start of the federal fiscal year?

- What happens if an ED program authorization "expires"?

- For More Information

Summary

Like most federal agencies, the Department of Education (ED) receives funds in support of its mission through various federal budget and appropriations processes. While not unique, the mechanisms by which ED receives, obligates, and expends funds can be complex. For example, ED receives both mandatory and discretionary appropriations; ED is annually provided forward funds and advance appropriations for some—but not all—discretionary programs; ED awards both formula and competitive grants; and a portion of ED's budget subsidizes student loan costs (direct loans and loan guarantees). As such, analyzing ED's budget requires an understanding of a broad range of federal budget and appropriations concepts. This report provides an introduction to these concepts as they are used specifically in the context of the congressional appropriations process for ED.

The first section of this report provides an introduction to key terms and concepts in the federal budget and appropriations process for ED. In addition to those mentioned above, the report includes explanations of terms and concepts such as authorizations versus appropriations; budgetary allocations, discretionary spending caps, and sequestration; transfers and reprogramming; and matching requirements.

The second section answers frequently asked questions about federal funding for ED or education in general. These are as follows:

- How much funding does ED receive annually?

- How much does the federal government spend on education?

- Where can information be found about the President's budget request and congressional appropriations for ED?

- How much ED funding is in the congressional budget resolution?

- What is the difference between the amounts in appropriations bills and report language?

- What happens to education funding if annual appropriations are not enacted before the start of the federal fiscal year?

- What happens if an ED program authorization "expires"?

The third section includes a brief description of, and links to, reports and documents that provide more information about budget and appropriations concepts.

Introduction

Federal policymakers statutorily established the U.S. Department of Education (ED) as a Cabinet-level agency in 1980.1 Its mission is to "promote student achievement and preparation for global competitiveness by fostering educational excellence and ensuring equal access."2

Like most federal agencies, ED receives funds in support of its mission through various federal budget and appropriations processes. These processes are complex. For example, ED receives both mandatory and discretionary appropriations; ED is annually provided forward funds and advance appropriations for some—but not all—discretionary programs; ED awards both formula and competitive grants; and a portion of ED's budget subsidizes student loan costs (through both direct loans and loan guarantees).

Because of this complexity, analyzing ED's budget requires an understanding of a broad range of federal budget and appropriations concepts. This report provides an introduction to these concepts as they are used specifically in the context of the congressional appropriations process for ED. It was designed for readers who are new or returning to the topic of ED budget and appropriations. The first section of this report provides an introduction to key terms and concepts in the federal budget and appropriations process with special relevance for ED. The second section answers frequently asked questions (FAQs) about federal funding for the department, as well as closely related questions about education funding in general. The third section includes a brief description of, and links to, reports and documents that provide more information about budget and appropriations concepts.

The scope of this report is generally (but not exclusively) limited to concepts associated with funding provided to ED through the annual appropriations process. It does not address all possible sources of federal funding for education, training, or related activities. For example, it does not seek to address education tax credits, student loans, or education and training programs at agencies other than ED.3 Where this report does address such topics, it does so in order to provide broad context for questions and key terms related to the appropriations process for ED. This report also addresses some frequently asked questions about education funding in general.

Key Concepts and Terms

The following section provides an introduction to selected key terms and concepts used in the congressional debate about federal funding for ED.

Budget Authority, Obligation, Outlay, and Rescission

In the federal budget process, the concept of spending is broken down into three related but distinct phases—budget authority, obligation, and outlay. Budget authority is the authority provided by federal law to enter into financial obligations that will result in immediate or future expenditures (or outlays) involving federal government funds. For reasons that are explained below, the amounts of budget authority, obligations, and outlays in a fiscal year are rarely the same for a budget account (or activity in that account). For example, ED's Education for the Disadvantaged account4 in FY2017 had $16.805 billion in total budget authority.5 That is, ED had legal authority to spend up to $16.805 billion in federal funds for the purposes associated with this account (which consists primarily of grants allocated to local educational agencies).6 During that same fiscal year, ED newly obligated (i.e., committed to spend) $16.789 billion of that available budget authority. Total outlays during FY2017 in the Education for the Disadvantaged account were $16.237 billion.7

Budget authority can only be provided through the enactment of law, and generally its amount, purpose, and the time period in which it may be used is specified. Budget authority may be for a broad set of purposes (e.g., improving the academic achievement of disadvantaged children) or for a particular purpose (e.g., obtaining annually updated local educational agency-level census poverty data from the Bureau of the Census). The amount of the budget authority is usually defined in specific terms (e.g., $10 billion) but sometimes is indefinite (e.g., "such sums as may be necessary"). The time element of budget authority provides a deadline as to when the funds must be obligated—one fiscal year, multiple fiscal years, or without fiscal year restriction (referred to as "no year" budget authority).

Once an agency receives its budget authority, it may take actions to obligate it legally, for example, by signing contracts or grant agreements. Over the course of a fiscal year, an agency may obligate budget authority that was first provided during that year or was provided in a prior fiscal year with a multiyear or no-year period of availability. Generally, all obligations must occur prior to the deadline associated with the budget authority. It is not until those obligations are due to be paid (i.e., become outlays) that federal funds from the Treasury are used to make the payments.

In addition to the amount of budget authority that is available to be obligated, the primary factor that affects the total amount of obligations in a fiscal year is when they are due. For example, outlays to pay salaries usually occur over the course of the year that the budget authority is made available because those payments must occur regularly (e.g., every two weeks). In contrast, outlays for a construction project may be structured to occur over several years as various stages of the project are completed. Outlays are reported in the fiscal year in which they occur, even those outlays that result from budget authority that first became available in previous fiscal years.

Budget authority that reaches the end of its period of availability is considered to have "expired." At this point, no new obligations may be incurred, although outlays to liquidate existing obligations are generally allowable, usually up to five fiscal years after the budget authority expired. Once that liquidation period has ended, it is generally the case that no further outlays may occur and the agency is to take administrative steps to cancel any remaining budget authority.8

Rescissions are generally provisions of law that repeal unobligated budget authority prior to its expiration. Such provisions may be used to eliminate budget authority for purposes that are considered to be outdated or no longer desirable. Rescissions also may be used to offset increases in budget authority for higher-priority activities.

Authorizations and Appropriations

|

Authorizations and Appropriations Authorization provisions generally come in two types: (1) Provisions that define the authority of the government to act, by establishing, altering, or terminating authorities, are referred to as "enabling" or "organic" authorizations; (2) "Authorizations of appropriations" essentially recommend a funding level for a program or agency in a given fiscal year but do not themselves provide that funding. Appropriations provisions provide funding for federal agencies to carry out certain purposes that are usually specified in authorization acts. |

The congressional budget process generally distinguishes between two types of measures—authorizations, which create or modify federal government programs or activities, and appropriations, which fund those activities. The provisions within authorization measures may be further distinguished as either enabling or organic provisions (e.g., statutory language or acts that authorize certain programs, policies, or activities) or express authorizations of appropriations provisions (e.g., statutory language or acts that recommend a future funding level for authorized programs, policies, or activities). These distinctions between authorizations and appropriations, and between the types of authorization provisions, are important for understanding why programs with "expired" authorizations can continue to function. This section focuses on the distinction between appropriations and enabling or organic authorizations; the section titled "Authorization of Appropriations" addresses the authorization of funding levels.9

Enabling or organic authorizations may be generally described as statutory provisions that define the authority of the government to act. These acts establish, alter, or terminate federal agencies, programs, policies, and activities. For example, the Economic Opportunity Act of 1964 (P.L. 88-452) contained statutory provisions that established the Federal Work-Study (FWS) program. The Higher Education Opportunity Act of 2008 (HEOA, P.L. 110-315) contained statutory provisions that altered and continued (e.g., "reauthorized") FWS. Authorization measures may also address organizational and administrative matters, such as the number or composition of offices within a department. Authorization measures are under the jurisdiction of legislative committees, such as the House Committee on Education and Labor and the Senate Committee on Health, Education, Labor and Pensions.

Authorizations may be permanent or limited-term. Permanent authorizations remain in place until Congress and the President enact a law or laws to amend or repeal the authorization. Most ED authorizations are permanent. For example, Title I-A of the Elementary and Secondary Education Act of 1965, as amended and reauthorized by the Every Student Succeeds Act (ESSA, P.L. 114-95), gives ED the authority to provide aid to local educational agencies (LEAs) for the education of disadvantaged children. In general, unless Congress and the President enacted legislation to repeal provisions of Title I-A, ED may distribute any budget authority it receives for such aid in accordance with the program parameters defined in such statutory language.

Limited-term authorizations end after a specified period of time, typically without requiring further legislative action. (These are sometimes called sunset provisions.) For example, the statute authorizing the Advisory Committee for Student Financial Assistance (ACSFA, 20 U.S.C. 1098(k)) specifies that ACSFA was authorized from the date of enactment until October 1, 2015. At that point, ACSFA was disbanded. The authorizations for some programs are intended to receive legislative action on a regular basis, as the authorities for those programs expire, while others are expected to receive legislative action as needed and not on a regular schedule.

Appropriations measures, on the other hand, are typically enacted annually and provide new budget authority for agencies, programs, policies, and activities that are already authorized and are under the jurisdiction of the House Appropriations Committee and the Senate Appropriations Committee.10 That is, appropriations give federal agencies the authority to use a certain amount of federal funds for program purposes that are usually specified in authorization acts. For example, the Department of Defense and Labor, Health and Human Services, and Education Appropriations Act, 2019 and Continuing Appropriations Act, 2019 (P.L. 115-245) appropriated $71.4 billion in discretionary budget authority to ED, of which $22.5 billion was specifically for the Pell Grant program.11

Budget authority that is provided in appropriations measures may be available for a single fiscal year, multiple fiscal years (or portions thereof), or an indefinite period of time. For example, P.L. 115-245 provided budget authority that was available for one year for ED's Indian Education account, a year-and-a-quarter for Special Education, and two years for Impact Aid.

In general, during a calendar year Congress may consider the following:

- 12 regular appropriations bills for the fiscal year that begins on October 1 (often referred to as the budget year) to provide the annual funding for the agencies, projects, and activities funded therein;12

- one or more continuing resolutions for that same fiscal year, to provide temporary funding if all 12 regular appropriations bills are not enacted by the start of the fiscal year; and

- one or more supplemental appropriations measures for the current fiscal year, to provide additional funding for selected activities over and above the amount provided through annual or continuing appropriations.13

Congress typically includes most regular annual ED appropriations in the Departments of Labor, Health and Human Services, and Education, and Related Agencies appropriations bill.

"Authorization of Appropriations"

|

GEPA and Appropriations Authorizations at ED The General Education Provisions Act (GEPA), as amended, contains a broad array of statutory provisions that are applicable to the majority of federal education programs administered by ED. One such provision, Section 422, effectively adds one additional fiscal year to most ED appropriations authorizations. For example, if Congress does not enact legislation extending the appropriations authorization of the Title I-A program by FY2020 (the last fiscal year for which the Elementary and Secondary Education Act (ESEA) provides an appropriations authorization for this program), then Section 422 of GEPA will authorize appropriations for the Title I-A program for one additional fiscal year (FY2021). The authorized Title I-A funding level under the GEPA extension in FY2021 will be the same level as the final year authorized under ESEA. |

In addition to enabling or organic authorizations that establish the authority for federal government activities and appropriations that provide the authority to actually expend federal funds on those activities, laws may include provisions that provide an explicit authorization of appropriations.

An authorization of appropriations (or, alternatively, appropriations authorization) is a provision of law that essentially recommends a funding level for a program or agency in a given fiscal year. Appropriations authorizations may include a range of fiscal years and a specific funding level for each fiscal year within that range (e.g., $10 million in FY2007, $12 million in FY2008, etc.); may be indefinite (e.g., "such sums as may be necessary"); or may not be provided at all. For example, Section 1002 of the Elementary and Secondary Education Act of 1965, as amended and reauthorized by the Every Student Succeeds Act (ESSA, P.L. 114-95), includes an authorization of appropriations provision effectively recommending a specific funding level ($15.9 billion) for the Title I-A program in a certain fiscal year (FY2019).

Contrary to common misconception, an authorization of appropriations does not convey actual budget authority. Further, a lapse or gap in the fiscal years covered by an authorization of appropriations (its "expiration") does not usually affect the underlying organic authorization, which provides authority to the federal government to engage in the programs or activities to which the authorization of appropriations relates.14 If appropriations are provided for programs with an expired authorization of appropriations, federal agencies generally would have sufficient legal authority to implement and operate these programs. This is because an authorization of appropriations is "basically a directive to Congress itself, which Congress is free to follow or alter (up or down) in the subsequent appropriation act."15

Authorizations of appropriations, however, are significant for the purposes of congressional rules. House and Senate rules require that a purpose must have been "authorized" prior to when discretionary appropriations are provided.16 While simply establishing an entity, program, or activity in law generally satisfies that authorization requirement, sometimes provisions are enacted that explicitly authorize future appropriations ("authorizations of appropriations"). If the period of time for which an authorization of appropriations has been provided lapses and is not renewed—for example, at the start of FY2010, if the authorization of appropriations ended in FY2009—then subsequent appropriations for those purposes are sometimes described as being "unauthorized" from the perspective of House and Senate rules and could be subject to a point of order during floor consideration.17 However, such points of order are frequently waived.

Discretionary and Mandatory Spending (Including Appropriated Mandatory Spending)

There are two broad categories of budget authority in the federal budget and appropriations process: discretionary spending and mandatory spending. ED receives both kinds of spending, but there are important distinctions between them that are relevant to understanding both how ED receives federal funding and how much it receives.

Discretionary spending is budget authority that is provided and controlled by appropriations acts. This spending is for programs and activities that are authorized by law, but the amount of budget authority for those programs and activities is determined through the annual appropriations process. Even if a discretionary spending program has been authorized previously, Congress is not required to provide appropriations for it or to provide appropriations at authorized levels. For example, Section 399 of the Higher Education Act, as amended (HEA), authorized discretionary appropriations of $75 million in FY2010 for the Predominantly Black Institutions (PBIs) program authorized under HEA, Section 318. However, actual discretionary appropriations for the Section 318 PBI program in FY2010 were $10.8 million.

Mandatory spending is budget authority that is controlled by authorizing acts. Such spending includes "entitlements," which are programs that require payments to persons, state or local governments, or other entities if those entities meet specific eligibility criteria established in the authorizing law.18 This budget authority may be provided through a one-step process in which the authorizing act sets the program parameters (usually eligibility criteria and a payment formula) and provides the budget authority for that program. Such funding remains available automatically each year for which it is provided, without the need for further legislative action by Congress. For example, HEA, Section 420R provides mandatory appropriations for Iraq and Afghanistan Service Grants (IASG).

Sometimes, however, the authorizing statute for an entitlement does not include language providing authority to make the payment to fulfill the legal obligation that it creates. Under this approach to mandatory spending, the budget authority is provided in appropriations measures. Such spending is referred to as appropriated mandatory spending or an "appropriated entitlement" and occurs through a two-step process. First, authorizing legislation becomes law that sets program parameters (through eligibility requirements and benefit levels, for example), then the appropriations process is used to provide the budget authority needed to finance the commitment.

|

Pell Grants A Quasi-entitlement? The Pell Grant program is sometimes referred to as a "quasi-entitlement," because the way that it functions in practice is similar to appropriated mandatory spending. That is to say, the Pell Grant program is "appropriated," but the funds it receives through the annual appropriations process are considered to be discretionary spending because there is no legal obligation to provide them. However, Congress and the President have not frequently exercised the option to reduce award levels or cap the number of recipients—which are variables that factor into the calculation of how much funding the program requires each year—and have generally provided the amount of budget authority (through the annual appropriations process or other means) necessary to fund the formula in the authorizing statute.19 |

As with mandatory spending, congressional appropriations committees have limited control over the amount of budget authority provided for appropriated mandatory spending because the amount needed is the result of previously enacted commitments in law. In other words, the authorizing statute for appropriated mandatory spending establishes a legal obligation to make payments (such as an entitlement) and the funding in annual appropriations acts is provided to fulfill that legal financial obligation. Because the cost of appropriated mandatory programs may vary from year to year, the funding that is provided through the annual appropriations process is based on a projection of costs for the relevant fiscal year.

Most ED line items included in regular annual appropriations acts are discretionary. One exception to this is the Vocational Rehabilitation State Grants program, which is appropriated mandatory spending.20

302(a) and 302(b) Allocations

The concepts in this section relate to how Congress decides the amount of discretionary and mandatory funding to appropriate each fiscal year, which ultimately impacts how much funding ED is provided. Generally speaking, Congress does not start by estimating the cost of every ED program and adding those amounts to reach a total. What happens instead (typically) is that the House and the Senate agree on a total for all federal spending through a budget resolution.21 That amount is then divided between appropriations and authorizing committees. The appropriations committees then divide their portions among each of their subcommittees. Each subcommittee then determines funding levels for the agencies within its jurisdiction. This is called the 302(a) and 302(b) allocation process.

More specifically, the Congressional Budget and Impoundment Control Act of 1974 (CBA)22 requires that Congress adopt a concurrent resolution on the budget each fiscal year. This budget resolution constitutes a procedural agreement between the House and the Senate that establishes overall budgetary and fiscal policy to be carried out through subsequent legislation. The spending elements of the agreement establish total new budget authority and outlay levels for each fiscal year covered by the resolution. The agreement also allocates federal spending among 20 functional categories (such as national defense; transportation; and education, training, employment, and social services), setting budget authority and outlay levels for each function.

Within each chamber, the total new budget authority and outlays for each fiscal year are also allocated among committees with jurisdiction over spending, thereby setting spending ceilings for each committee. These ceilings are referred to as the 302(a) allocations.23 The 302(a) allocation to each of the authorizing committees (such as the Senate Health, Education, Labor and Pensions Committee) establishes spending ceilings on the mandatory spending under each committee's jurisdiction. The 302(a) allocations to the House and the Senate appropriations committees include discretionary spending and also appropriated mandatory spending.

Once the appropriations committees receive their spending ceilings, they separately subdivide the amount among their respective subcommittees, providing spending ceilings for each subcommittee. These spending ceilings are referred to as 302(b) suballocations.24 For example, for FY2019 the amount of the initial 302(a) allocation to the House Appropriations Committee was $1.2 trillion for discretionary budget authority and $955 billion for appropriated mandatory budget authority. The appropriations subcommittee that is responsible for funding ED is the Labor, Health and Human Services, Education, and Related Agencies (LHHS) subcommittee. When the committee apportioned that allocation among its 12 subcommittees, the initial suballocation for the LHHS subcommittee was $177 billion for discretionary budget authority and $783 billion for appropriated mandatory budget authority.25

The congressional allocations are of budget authority for the upcoming fiscal year. Budget authority enacted in previous fiscal years that first becomes available for obligation in the upcoming fiscal year counts against the congressional allocations for the upcoming fiscal year. (This type of budget authority is referred to as "advance appropriations" and is discussed further in the section ""Carry Forward," Advance Appropriations, and Forward Funding.")

Fiscal Year, Award Year, and Other Units of Time

Department of Education budget, appropriations, and program-related data may be reported using a variety of different "years" or units of time. These units of time include the fiscal year, calendar year, academic or school year, and the award year. Readers are cautioned to remain alert to the unit of time when considering and comparing various funding levels reported for ED activities. To be strictly comparable, the units of time must be the same.

When the federal government accounts for the funds it has budgeted, appropriated, or spent, the unit of time it uses is the fiscal year (FY). The federal fiscal year is generally the 12-month period between October 1 and the following September 30. The current year is the fiscal year that is in progress; the prior year is the fiscal year immediately preceding the current year. Outyears are any future fiscal years beyond the current year. The fiscal year is the standard unit of time used in the congressional appropriations process; most funding levels in appropriations bills and committee documents are reported by fiscal year.26

The federal fiscal year differs from the calendar year (January 1 to December 31), the typical academic or school year (fall to spring),27 and the federal student aid award year (July 1 through the following June 30). Annual funding levels reported in ED budget and program-related documents may use one or more of these different units of time. For example, ED's FY2019 congressional budget justification includes both fiscal year and award year funding levels for the Pell Grant program. These funding levels are not strictly comparable.

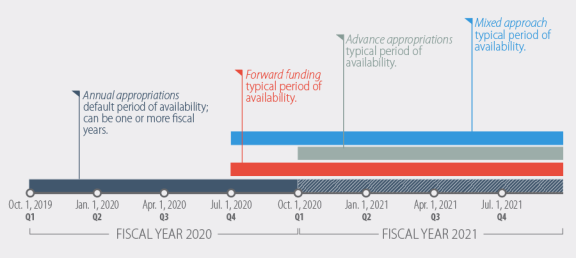

"Carry Forward," Advance Appropriations, and Forward Funding

Funding for federal programs that is provided in regular appropriations acts is usually available for obligation at the start of the fiscal year and may only be obligated during that fiscal year unless otherwise specified. Budget authority also may be provided for more than one fiscal year ("multiyear") or without fiscal year limitation ("no-year"). (See section on "Authorizations and Appropriations.") In other words, in some cases, budget authority may be obligated over multiple fiscal years or may be available to be obligated indefinitely (until it is exhausted).

The concept of carry forward (or carry over) applies to budget authority that was enacted and became available in a previous fiscal year and is still available for obligation in the next fiscal year. (If a federal agency has not entirely obligated its multi- or no-year budget authority by the end of the fiscal year, any unexpired multiyear budget authority and all remaining no-year budget authority may continue to be available for obligation in the next fiscal year.) Such carry forward budget authority is typically notated as "unobligated balances brought forward" in the OMB Appendix to the annual budget. For example, the FY2019 OMB Appendix reports that budgetary resources available to the Education for the Disadvantaged account in FY2017 included $660 million in unobligated balances brought forward (of $16.805 billion, total).

The concepts of advance appropriations and forward funding relate to when such funding first becomes available to be obligated relative to the timing of its enactment and thus differ significantly from carry forward. With advance appropriations and forward funding, the budget authority becomes available for obligation at a point in time that is delayed beyond the start of the fiscal year.

- Advance appropriations become available for obligation starting at least one fiscal year after the budget year.

- Forward funding becomes available beginning late in the budget year and is carried into at least one following fiscal year.

Federal accounts and programs may receive annual appropriations, advance appropriations, forward funding, or a mixed approach. The most common mixed approach used in ED appropriations combines advance appropriations and forward funding.

Figure 1 illustrates the period of availability for annual appropriations, forward funding, and advance appropriations. It also includes an illustration of the default (or typical) period of availability for annual appropriations.28

The period of availability for budget authority in ED's accounts does not usually follow a single rule. In a typical appropriations act, some ED accounts and programs will receive annual appropriations (e.g., Indian Education), while others will receive appropriations under a mixed approach including advance appropriations and forward funding (e.g., ESEA Title I). In general, the advance appropriations-forward funding combination is used for accounts that provide funds to recipients (such as elementary and secondary schools) who might experience service disruptions if they received funds aligned with the federal fiscal year and not the academic or school year. One advantage of this approach is that it allows schools to obligate funds prior to the start of the school year. It also gives schools time to plan for, and adjust to, changes in federal funding levels.

Budget Caps and Sequestration

The Budget Control Act of 2011 (BCA, P.L. 112-25) sought to reduce the federal budget deficit through a variety of budgetary mechanisms, including the establishment of limits (or caps) on discretionary spending and automatic spending reductions (known as sequestration) for both discretionary and mandatory spending. The BCA only places limits on discretionary spending, and the purpose and triggers for budgetary reductions through sequestration differ significantly between discretionary and mandatory spending. In addition to describing how the BCA operates in light of these key distinctions, the following sections discuss the implications of the BCA for ED.29

|

BCA-Related Budget Control Mechanisms The BCA imposed statutory limits on discretionary spending for specified fiscal years. (The BCA established no statutory limits on mandatory spending.) The BCA also established procedures to lower the discretionary limits to achieve additional savings. The BCA requires that sequestration—a largely across-the-board reduction of funding for nonexempt programs and activities—occur under certain circumstances. These circumstances differ for discretionary and mandatory spending.

|

Discretionary Spending Limits

The BCA imposes separate limits on "defense" and "nondefense" discretionary spending each fiscal year from FY2012 to FY2021. The defense category includes all discretionary spending under budget function 050 (defense).30 The nondefense category includes discretionary spending in all the other budget functions. In general, discretionary budget authority for ED is subject to the nondefense limit.

If discretionary spending is enacted in excess of the statutory limits, enforcement primarily occurs through sequestration, which is the automatic cancelation of budget authority through largely across-the-board reductions of nonexempt programs and activities.31 The purpose of sequestration is to reduce the level of spending subject to the discretionary spending limit so that it no longer exceeds that limit. Any across-the-board reductions through sequestration affect only nonexempt spending subject to the breached limit, and they are in the amount necessary to reduce spending so that it complies with the limit.

Pursuant to procedures under the BCA, the discretionary spending limits initially established by that act are to be further lowered each fiscal year to achieve certain additional budgetary savings.32 The amount of the revised limits for the upcoming fiscal year is calculated by OMB and reported with the President's budget submission each year.33 The timing of this calculation, which occurs many months prior to the beginning of the fiscal year, is intended to allow time for congressional consideration of appropriations measures that comply with the revised limits. Since the enactment of the BCA, however, a series of laws have been enacted that supersede the spending limit level that otherwise would have been established by the OMB calculation. The effect of these laws in most cases has been to increase the limits above what they otherwise would have been. The most recent such law, which increased the spending limits for FY2018 and FY2019, was the Bipartisan Budget Act of 2018 (BBA 2018, P.L. 115-123).34

Mandatory Spending Sequestration

In addition to the lowered discretionary spending limits, the BCA provides for reductions to mandatory spending each fiscal year, which are also achieved through sequestration. (Some mandatory spending is exempt from these automatic reductions.) However, mandatory spending sequestration differs from discretionary spending sequestration in that it occurs automatically each fiscal year, and is not triggered by spending levels or other budgetary factors. In other words, mandatory spending sequestration in the BCA context is used as a means to automatically reduce that type of spending each fiscal year on a largely across-the-board basis.

The amount of the reduction to defense and nondefense mandatory spending is calculated by OMB and announced at the same time as the reductions to the statutory discretionary spending limits each fiscal year (with the President's budget submission). Nonexempt mandatory budget authority at ED is subject to the nondefense reduction.

The BCA and ED Funding

The BCA affects funding levels at ED in several ways. In establishing caps on total federal discretionary budget authority—caps which are the basis for the allocations of both total federal spending and the division of that amount to each of the appropriations subcommittees through the 302(a) and 302(b) processes (discussed above)—the BCA can impact total discretionary funding at ED. Further, if those caps are exceeded, ED's discretionary budget authority may be subject to sequestration. Since the BCA has been in effect, a discretionary spending sequestration has only occurred once—in FY2013.35

For ED programs that receive nonexempt mandatory funding, the BCA requires an annual sequester in an amount calculated by OMB. The dollar amount of the reduction for a particular ED account is based on the percentage by which nonexempt mandatory spending in the nondefense category needs to be cut to achieve the total required savings. For example, in FY2018 mandatory funds in the Rehabilitation Services and Disability Research, Higher Education, TEACH Grant Program, IASG, and Student Financial Assistance Debt Collection accounts were subject to the nondefense mandatory sequestration that was calculated based on a reduction of 6.6%.36 For FY2019, this reduction is 6.2%.37

For both mandatory and discretionary spending sequestration, the dollar amount that is canceled in each account differs depending on the amount of sequesterable budgetary resources in that account. For example, for the FY2013 sequester, OMB calculated that nondefense discretionary spending would need to be reduced by 5%. The English Language Learner account, which had total sequesterable budgetary resources of $737 million, would thus be reduced by $37 million (5% of $737 million). Likewise, Impact Aid had sequesterable budgetary resources of $1.299 billion and was reduced by $65 million (5% of $1.3 billion).

Some ED programs, such as the Pell Grant program, are exempt from sequestration or follow special rules. For example, during periods when a sequestration order is in effect for mandatory spending, the BCA directs that origination fees charged on federal student loans made under the William D. Ford Federal Direct Loan program must be increased by the nondefense, mandatory sequestration percentage.38 For more information, see CRS Report R42050, Budget "Sequestration" and Selected Program Exemptions and Special Rules.

Readers are cautioned, when comparing or analyzing funding levels for ED accounts and programs, to assess whether such funding levels reflect pre- or post-sequestration funding levels. Administration and congressional budget and appropriations materials may use pre- or post-sequestration amounts, or both.

Transfer and Reprogramming

Both authorization and appropriations measures may also provide transfer authority. Transfers shift budget authority from one account or fund to another or allow agencies to make such shifts. Agencies are prohibited from making transfers between accounts without statutory authority. For example, in FY2019 the appropriations act that funded ED provided that up to 1% of any discretionary budget authority appropriated to the department could be transferred between accounts, subject to certain restrictions.39

Agencies may, however, generally shift budget authority from one activity or program to another within an account without additional statutory authority. This is referred to as reprogramming. For example, in FY2016 ED shifted $158,336 from the Strengthening Native American-serving Nontribal Institutions program that would have otherwise lapsed to the Fund for the Improvement of Postsecondary Education/First in the World (FIPSE/FITW) program using reprogramming authority.40 The appropriations subcommittees have established notification and other oversight procedures for various agencies to follow regarding reprogramming actions. Generally, these procedures differ with each subcommittee. For instance, in FY2019 reprogramming requirements applicable to ED were carried in the appropriations act that funded the department. Those requirements included consultation with the House and the Senate appropriations committees, as well as written notification, ahead of reprogramming actions that met certain criteria.41

Formula and Competitive Grants

The Department of Education uses one of two processes to distribute the funds it receives for grant making. It may distribute such funds by mathematical formula—usually such formulas are predetermined and established in statute—or through merit-based competitions.

ED's Title I, Part A program, for example, is a formula grant program. It provides funding to local educational agencies (through state educational agencies) using various mathematical formulas that consider the number of school-age children in poverty, state average per-pupil expenditures, and similar variables.42 The Innovative Approaches to Literacy program, on the other hand, is a merit-based competitive grant program. Applicants must meet certain criteria (such as whether they promote science, technology, engineering, and math education) and are awarded points based on how well they meet those criteria. Applicants with the highest weighted scores receive grants.43

Block and Categorical Grants

Policy debates about education funding sometimes focus on whether funds ought to be provided through block grants or categorical grants.44 Block grants are general or multipurpose grants that, in the federal education context, are typically awarded to states through a formula-based process. Block grant funding may be used for a wide variety of purposes. Awardees (not federal officials) determine how to use such funds within a broad set of options. For example, the Elementary and Secondary Education Act, as amended by ESSA (P.L. 114-95), authorized a new block grant program at ED called "Student Support and Academic Enrichment Grants." Formula funding provided through this block grant could serve a variety of purposes. Such purposes include providing all students with access to a well-rounded education, improving school conditions for student learning, and improving the use of technology in order to improve the academic achievement and digital learning of all students.45

Categorical grants, on the other hand, are typically available for a more narrow and defined set of purposes or program activities. They may be distributed by formula or competition. ED's Carol M. White Physical Education program, which provides funds to schools and community-based organizations to initiate, expand, or enhance physical education programs, is an example of a competitively awarded categorical grant. (ESSA incorporated this program into the Student Support and Academic Enrichment block grant.)

Matching Funds or Requirements

Some federal grants include what are known as matching requirements. In such scenarios, federal funds or assistance are granted to awardees who are willing and able to "match" federal funds with a nonfederal contribution (such as funding from state government or private sources). This nonfederal contribution is called the "nonfederal share." Typically, matching fund requirements specify that the nonfederal share must meet or exceed a certain percentage of the federal award amount (such as 20% or 50%). Depending on the grant requirements, nonfederal matching contributions may be in cash or what is known as "in-kind" (such as computer equipment or staff time), or a combination of the two. For example, the maximum federal share of compensation in the Federal Work-Study program (which provides funding to support part-time employment of needy college and university students) is 75% (with certain exceptions). Institutions participating in the Work-Study program are required to provide the remaining 25%.46

Frequently Asked Questions

The following section includes frequently asked questions about the budget and appropriations process for ED (and closely related topics).

How much funding does the Department of Education receive annually?

ED's annual budget includes two types of spending: discretionary and mandatory. In FY2019, ED received approximately $71 billion in budget authority through the annual discretionary appropriations process.47 About three-quarters of these funds ($52 billion) were distributed to local educational agencies to provide supplementary educational and related services for disadvantaged and disabled children or to low-income postsecondary students (in the form of Pell Grants, which provide financial assistance for college).48

ED also has programs that receive mandatory funding directly through their authorizing statutes. These programs received about $2.5 billion in net funding in FY2019. However, most of ED's mandatory funding is for student loan subsidies. In some years, the net cost of student loan subsidies is positive (i.e., there is a cost to the government for providing the subsidy); in other years the net cost of student loan subsidies is negative (i.e., the government received fees and other receipts in excess of subsidy costs).49 Because of this dynamic, ED's "total" budget can vary widely from year to year. (See Table 1.)

Table 1. Discretionary, Mandatory, and Total ED Appropriations: FY2015 to FY2019

(In thousands, rounded)

|

FY2015 |

FY2016 |

FY2017 |

FY2018 |

FY2019 |

|

|

Discretionary |

67,135,576 |

68,306,763 |

68,239,156 |

70,867,406 |

71,448,416 |

|

Mandatory (net) |

20,377,890 |

8,772,739 |

47,802,686 |

(692,311) |

2,555,285 |

|

Total |

87,513,466 |

77,079,502 |

116,041,842 |

70,175,095 |

74,003,701 |

Source: Mandatory spending levels for all years and discretionary spending levels for FY2015-FY2017 are from U.S. Department of Education, Budget Tables, "President's Budget Request," FY2017-FY2019. Discretionary spending levels for FY2018 and FY2019 are from U.S. Department of Education, Budget Tables, "FY2019 Congressional Action," October 9, 2019, https://www2.ed.gov/about/overview/budget/budget19/19action.pdf.

Notes: Numbers in parentheses are negative numbers. Mandatory funding levels in Table 1 represent net cost (including both gains and expenditures). Mandatory funding levels for FY2018 and FY2019 are estimates. Discretionary funding for FY2019 is current as of the date of this report.

How much does the federal government spend on education?

In short, the answer depends on what federal accounts or activities are defined as "education spending," on the point in the fiscal year when budget authority is estimated, and which federal agency is reporting. Any aggregation of federal funding provided for educational purposes across agencies or accounts requires judgements about which activities should be counted (in whole or in part) and about how such activities should be grouped (e.g., higher education, K-12, etc.). Moreover, any such exercise may be limited by the granularity of information available about the use of the funds. Complicating the situation is the fact that federal funding for education overlaps with (but is not the same as) funding for ED.

The following sections explore and describe two commonly referenced ways that the federal government accounts for the funds it spends on education: by Treasury Department function code and as calculated and tracked in ED's Digest of Education Statistics.

Function 500

The Treasury Department classifies all federal funding according to certain numbered functions (e.g., Health (550) and Transportation (400)) and by numbered subfunctions (e.g., Health Care Services (551) and Health Research and Training (552)). The Congressional Budget Office (CBO), Office of Management and Budget (OMB), and congressional budget process also use this same taxonomy.

Federal education funding is included in function 500 (Education, Training, Employment, and Social Services). Within function 500, subfunction 501 includes elementary, secondary, and vocational education; and subfunction 502 includes higher education. While these are two of the primary areas in which federal education funding is concentrated, simply adding the totals for these two subfunctions does not capture all federal funding for education. For example, other subfunctions, such as 503 (research and general education aids) and 504 (training and employment), could be considered federal education spending as well. Additionally, subfunction 506 (social services) includes ED's Rehabilitation Services and Disability Research Account.

Furthermore, only a portion of total outlays for subfunctions 501 and 502 were spent by ED, and not all ED funding is classified as function 500. For example, other agencies (such as the National Science Foundation and National Institutes of Health) provide federal funds for educational programs and activities that may be captured in the totals for subfunctions 501 and 502. In addition, some ED programs and activities are classified under other functional categories, such as the Office for Civil Rights (subfunction 751, federal law enforcement activities).

Digest of Education Statistics

ED's National Center for Education Statistics (NCES) tracks federal funding for education and related activities in the periodically updated Digest of Education Statistics (Digest). Funding data in Digest tables may represent appropriations or outlays. Major Digest federal education funding tables present data on federal support for education broken down by program, agency, state, education level, and other facets.50

As per Table 401.10, "Federal support and estimated federal tax expenditures for education, by category," the federal government provided $228.4 billion in direct budget authority (measured primarily as outlays, but sometimes as obligations) for education (broadly defined to include research grants to universities) in FY2017. If nonfederal funds generated by federal legislation are included, the amount was $322.6 billion.

Where can information be found about the President's budget request and congressional appropriations for the Department of Education?

The ED congressional budget justifications, which provide details about the President's budget request for the department, are published on the department's website.51

Appropriations for many (but not all) ED accounts are typically included in annual Departments of Labor, Health and Human Services, and Education, and Related Agencies appropriations acts. The Congressional Research Service (CRS) tracks these acts—including related bills and committee reports—each year.52

How much ED funding is in the congressional budget resolution?

As discussed in the "302(a) and 302(b) Allocations" section of this report, the budget resolution sets procedural parameters for the consideration of mandatory and discretionary spending legislation; those parameters are enforceable by points of order. The budget resolution does not provide actual funding for ED or any other purpose.

While the procedural parameters in the budget resolution do involve underlying assumptions about levels of funding for particular purposes, there are two general reasons why the amount of funding assumed for ED (or education-related purposes) in the annual congressional budget resolution cannot be determined by CRS. First, the procedural parameters in the budget resolution allocate funding by congressional committee and not by department. Because the jurisdiction of the relevant authorizing committees and appropriations subcommittees encompasses more than ED, it is not possible to determine the assumed amount of funding for ED through those allocations. Second, although the basis of those authorizing committee and appropriations subcommittee allocations is a distribution of funding based on "functional categories," those functional categories do not neatly correspond to ED or education-related purposes. (Functional categories are discussed in the section "How much does the federal government spend on education?") As a result, absent specific information with regard to the budget resolution from the House or the Senate budget committees, it is not possible for CRS to determine amounts of funding for ED or education-related purposes that are assumed by the budget resolution.

What is the difference between the amounts in appropriations bills and report language?

The answer to this question centers on the force of law. Funding levels included in House and Senate appropriations bills are proposed until enacted. That is to say, until an appropriations bill is signed by the President (i.e., it is enacted), the funding levels included therein simply represent what each appropriations committee or subcommittee—or if the bill has passed the House or the Senate, that chamber—proposes to appropriate for the various programs and agencies included in that bill. Once Congress and the President enact an appropriations measure, the funding levels included in that act are statutorily established and provide a legal basis for agencies to obligate and expend that funding. Appropriations acts, therefore, carry the force of law.

Funding levels and program directives included in House and Senate appropriations committee reports are committee recommendations and are not usually legally binding. (In some cases, report language is enacted by reference in the appropriations act that it accompanies, giving it statutory effect.)53 However, while report language itself generally is not law, agencies usually seek to comply with it because it represents congressional intent.

Typically, report language is used to supplement legislative text at either of two stages in the congressional appropriations process. First, as noted, reports may accompany annual appropriations bills reported by the House or the Senate appropriations committees. If these committee reports differ with respect to a particular funding level or program directive (e.g., the House Appropriations Committee report recommends setting the maximum discretionary portion of Pell Grants at $5,035 and the Senate report recommends setting it at $5,135), a joint explanatory statement (JES) may be used to reconcile conflicting language and also provide additional instructions. (The JES is sometimes referred to colloquially as a conference report, though from a technical standpoint, it is not. The JES accompanies the conference report, which contains only legislative text.)54

For appropriations measures that are not reported from an appropriations committee but still receive congressional consideration—or when differences are resolved through an amendment exchange and not a conference committee process—an explanatory statement from an appropriations committee is sometimes entered into the Congressional Record. This language may be regarded similarly to report language. When this text is used during the resolving differences phase of the legislative process, such statements can serve the same purposes and function as a JES.

What happens to education funding if annual appropriations are not enacted before the start of the federal fiscal year?

It depends. First, Congress and the President may provide partial-year funding through a temporary appropriations law, often referred to as a "continuing resolution" (CR), while they negotiate agreement on annual appropriations that have yet to be enacted. CRs typically (but not always) provide appropriations at a rate based on the previous fiscal year's appropriations acts and for the same purposes as those provided in the previous fiscal year. (Adjustments in funding levels or allowable activities must be specified in the CR.) The typical effect, then, of providing federal education funding through a continuing resolution is that planned or proposed changes to federal education programs may not occur or may be delayed.55 In addition, while a CR is in effect, ED makes limited obligations until budget authority for the entire fiscal year is enacted.

If appropriations actually lapse, the effects of that lapse—including whether a shutdown of agency operations commences—will depend on a variety of factors. Several factors that might mitigate the effects of a lapse include

- the extent to which unexpired budget authority is available for ED to obligate during the period of the lapse (generally, such funding would be multiyear or no-year budget authority enacted in prior fiscal years, including as forward funds or advance appropriations);

- the extent to which ED staff who would regularly administer programs or funds are furloughed as a consequence of the lapse;

- the timing of the grant cycle for individual grant programs and the type of funds that are typically awarded and distributed; and

- the availability of alternative sources of funding that can be used (temporarily or on an ongoing basis) to sustain supported activities.56

What happens if an ED program authorization "expires"?

As discussed in the sections titled "Authorizations and Appropriations" and "Authorization of Appropriations," most of ED's enabling or organic program authorizations are permanent. Therefore, unless the program's enabling authorization specifically includes a sunset provision, or Congress and the President enact legislation repealing the enabling authorization, the program can continue so long as Congress continues to fund it through the appropriations process.

This remains true, in general (but not always), even if the program's authorization of appropriations has expired and the GEPA extension has lapsed. (See text box titled, "GEPA and Appropriations Authorizations at ED.") This is because an authorization of appropriations is a directive from Congress to itself and does not typically function as a sunset provision for the program or purpose to which it relates. An expired authorization of appropriations may, however, lead to a point of order during floor consideration against an appropriations measure or amendment under certain circumstances. They are, therefore, significant from the perspective of congressional procedure.

For More Information

Readers seeking additional information on any of the key terms, concepts, and answers to the FAQs included in this report are referred to the authors of this report and to CRS reports on budget and appropriations in general and on education funding in particular. Such reports have been footnoted and linked in the relevant sections of this report.

Additionally, readers may wish to consult glossary and budget concepts documents produced by ED, the Congressional Budget Office (CBO), Government Accountability Office (GAO), and Office of Management and Budget (OMB). These include the following:

- Department of Education, Budget Process in the U.S. Department of Education, last modified January 19, 2017, http://www2.ed.gov/about/overview/budget/process.html;

- Congressional Budget Office, Glossary, updated July 2016, https://www.cbo.gov/publication/42904;

- U.S. Government Accountability Office, A Glossary of Terms Used in the Federal Budget Progress, GAO-05-734SP, September 1, 2005, http://www.gao.gov/products/GAO-05-734SP; and

- Executive Office of the President, Office of Management and Budget, "Budget Concepts," Fiscal Year 2019 Analytical Perspectives of the U.S. Government, https://www.govinfo.gov/content/pkg/BUDGET-2019-PER/pdf/BUDGET-2019-PER-5-1.pdf.

Author Contact Information

Acknowledgments

Heather Gonzalez, CRS Specialist in Social Policy, co-authored an earlier version of this report.

Footnotes

| 1. | |

| 2. |

U.S. Department of Education, "About ED," http://www2.ed.gov/about/landing.jhtml, accessed December 28, 2018. |

| 3. |

Such funds are not typically included in the annual discretionary appropriations act for ED, which is the primary focus of this report. Congressional readers seeking such information are referred to the many publications on these topics at http://www.crs.gov. |

| 4. |

An account is a separate financial reporting unit for budget, management, and/or accounting purposes. For more information on accounts, see U.S. Government Accountability Office, A Glossary of Terms Used in the Federal Budget Process, GAO-05-734SP, September 1, 2005, http://www.gao.gov/products/GAO-05-734SP. |

| 5. |

Consisting of $660 million in unobligated balances brought forward, $10.841 billion in advance appropriations from FY2016, and $5.303 billion in current-year (FY2017) appropriations. See Executive Office of the President, Office of Management and Budget, "Department of Education," The Appendix: Budget of the United States Government, Fiscal Year 2019, https://www.govinfo.gov/content/pkg/BUDGET-2019-APP/pdf/BUDGET-2019-APP-1-9.pdf. |

| 6. |

This account includes programs such as Elementary and Secondary Education Act (ESEA) Title I-A Grants to Local Educational Agencies, School Improvement Grants, and Migrant Education Program grants. |

| 7. |

Executive Office of the President, Office of Management and Budget, "Department of Education, " The Appendix: Budget of the United States Government, Fiscal Year 2019, p. 333, https://www.govinfo.gov/content/pkg/BUDGET-2019-APP/pdf/BUDGET-2019-APP-1-9.pdf. |

| 8. |

31 U.S.C. §1552(a). For a detailed discussion of these general principles, see GAO, Principles of Appropriations Law, 3rd Ed., pp. 5-71 to 5-75, http://www.gao.gov/assets/210/202437.pdf. |

| 9. |

More information about the distinction between types of authorizations, and between authorizations and appropriations, is available in U.S. Government Accountability Office, "Chapter 2: The Legal Framework," Principles of Federal Appropriations Law, GAO-16-464SP, 4th ed., 2016 Revision, pp. 2-54 – 2-56, at http://www.gao.gov/legal/redbook/redbook.html. See also the section entitled, "What happens if an ED program authorization "expires"?" |

| 10. |

In certain instances, federal programs can receive appropriations through their authorizing acts instead of (or in addition to) the budget authority they receive through annual appropriations acts. This process is described more fully in the section on "Discretionary and Mandatory Spending (Including Appropriated Mandatory Spending)." |

| 11. |

The department also receives budget authority through other provisions of law. This amount represents only the amount it received through the annual regular appropriations process. See section on "Discretionary and Mandatory Spending (Including Appropriated Mandatory Spending)" for more information on this distinction. |

| 12. |

In some years, Congress combines two or more of these bills into what may be referred to as an "omnibus" or "consolidated" appropriations act. |

| 13. |

In general, supplemental funding may be provided to address cases where resources provided through the annual appropriations process are determined to be inadequate or not timely. |

| 14. |

There can be exceptions to this rule. For example, from September 30, 2015, to December 18, 2015, ED curtailed the operations of the federal Perkins Loan program. ED took this step because the department considered the authorization of appropriations provision under HEA Section 461(b)(1) to control the duration of the program. ED interpreted this section, along with the automatic one-year extension under the General Education Provisions Act (GEPA) Section 422, to mean that the Perkins Loan program was authorized through September 30, 2015. The program resumed after Congress enacted the Federal Perkins Loan Program Extension Act of 2015 (the Extension Act; P.L. 114-105), which extended ED's authorization to make new Perkins Loans to eligible students through September 30, 2017. See CRS Report R44343, The Federal Perkins Loan Program Extension Act of 2015: In Brief. |

| 15. |

U.S. Government Accountability Office, "Chapter 2: The Legal Framework," Principles of Federal Appropriations Law, GAO-16-464SP, 4th ed., 2016 Revision, p. 2-56, at http://www.gao.gov/legal/redbook/redbook.html. |

| 16. |

See the section on "Discretionary and Mandatory Spending (Including Appropriated Mandatory Spending)" for more information about discretionary appropriations. |

| 17. |

A point of order is an objection that the pending proposal or proceeding is in violation of House or Senate rules. For further information with regard to these rules, see CRS Report R42098, Authorization of Appropriations: Procedural and Legal Issues, pp. 4-8. |

| 18. |

Entitlement payments are legal obligations of the federal government, and eligible beneficiaries may have legal recourse if full payment under the law is not provided. |

| 19. |

For further information about the Pell Grant program, see CRS Report R45418, Federal Pell Grant Program of the Higher Education Act: Primer. |

| 20. |

For more information, see CRS Report R43855, Rehabilitation Act: Vocational Rehabilitation State Grants. |

| 21. |

In the absence of agreement on a budget resolution, Congress may employ alternative legislative tools to serve as a substitute for a budget resolution. These substitutes are typically referred to as "deeming resolutions," because they are deemed to serve in place of an annual budget resolution for the purposes of establishing enforceable budget levels for the upcoming fiscal year. For further information, see CRS Report R44296, Deeming Resolutions: Budget Enforcement in the Absence of a Budget Resolution. |

| 22. |

2 U.S.C. §621 et seq. |

| 23. |

This refers to §302(a) of the CBA. Typically, these 302(a) allocations are provided in the joint explanatory statement that accompanies the conference report on the budget resolution. |

| 24. |

This refers to §302(b) of the CBA. These 302(b) suballocations are reported by the House and the Senate appropriations committees. |

| 25. |

The 302(a) allocation for the House Appropriations Committee was entered into the Congressional Record by the House Budget Committee Chair pursuant to authority granted by Section 30104 of the Bipartisan Budget Act of 2018 (P.L. 115-123). See "Publication of Budgetary Material," Congressional Record, daily edition, vol. 164, part 76 (May 10, 2018), p. H3926. The initial LHHS 302(b) suballocation for FY2019 is in H.Rept. 115-710. |

| 26. |

Funds may also be made available for more than one year ("multiyear" funds) or without fiscal year limitation ("no year" funds). For further information on the appropriations process, see CRS Report R42388, The Congressional Appropriations Process: An Introduction. |

| 27. |

Schools and colleges follow their own separate fiscal years. A typical fiscal year for an elementary and secondary school is July 1 to June 30. Fiscal years at institutions of higher education tend to vary. |

| 28. |

For more information, see CRS Report R43482, Advance Appropriations, Forward Funding, and Advance Funding: Concepts, Practice, and Budget Process Considerations. |

| 29. |

For more information about the BCA, see CRS Report R42506, The Budget Control Act of 2011 as Amended: Budgetary Effects; and CRS Report R44874, The Budget Control Act: Frequently Asked Questions. |

| 30. |

For information on the budget functions, see CRS Report 98-280, Functional Categories of the Federal Budget. |

| 31. |

Procedures for discretionary spending sequestration are provided in the Balanced Budget and Emergency Deficit Control Act of 1985 (BBEDCA), Sections 251 and 256. Exempt programs and activities, including the Pell Grant program, are listed in BBEDCA, Section 255. |

| 32. |

The lowering of the limits was triggered when the BCA "joint committee" process did not result in the enactment of legislation to achieve a targeted level of spending reductions. For information on this process, see CRS Report R41965, The Budget Control Act of 2011. |

| 33. |

The procedures through which these limits are reduced are in Section 251A of the Balanced Budget and Emergency Deficit Control Act of 1985 (BBEDCA). For a description of these procedures and how they were initially carried out for the FY2014 reductions, see OMB Report to Congress on the Joint Committee Reductions for Fiscal Year 2014, pp. 11-16, https://obamawhitehouse.archives.gov/sites/default/files/omb/assets/legislative_reports/fy14_preview_and_joint_committee_reductions_reports_05202013.pdf. |

| 34. |

For further information, see CRS Insight IN10861, Discretionary Spending Levels Under the Bipartisan Budget Act of 2018. |

| 35. |

For the FY2013 sequestration of nondefense discretionary spending, a total reduction of $25.798 billion or 5% of such spending was required. The circumstances that triggered discretionary spending sequestration during FY2013 were somewhat different than the circumstances that could trigger sequestration in future fiscal years, but the basic principles discussed in this paragraph as to how sequestration would be carried out continue to apply. For further information with regard to the FY2013 sequestration, including the reductions to particular accounts, see OMB Report to the Congress on the Joint Committee Sequestration for Fiscal Year 2013, March 1, 2013, https://obamawhitehouse.archives.gov/sites/default/files/omb/assets/legislative_reports/fy13ombjcsequestrationreport.pdf. |

| 36. |

Executive Office of the President, Office of Management and Budget, OMB Report to the Congress on the Joint Committee Reductions for Fiscal Year 2018, May 23, 2017, https://www.whitehouse.gov/sites/whitehouse.gov/files/omb/sequestration_reports/2018_jc_sequestration_report_may2017_potus.pdf. |

| 37. |

Executive Office of the President, Office of Management and Budget, OMB Report to the Congress on the Joint Committee Reductions for Fiscal Year 2019, February 12, 2018, https://www.whitehouse.gov/wp-content/uploads/2018/02/Sequestration_Report_February_2018.pdf. |

| 38. |

For more information, see CRS Report R40122, Federal Student Loans Made Under the Federal Family Education Loan Program and the William D. Ford Federal Direct Loan Program: Terms and Conditions for Borrowers. |

| 39. |

P.L. 115-245, Division B, Title III, §302. |

| 40. |

See Department of Education, "Fiscal Year 2018 Justifications of Appropriations Estimates to the Congress: Volume II," p. R-38, https://www2.ed.gov/about/overview/budget/budget18/justifications/r-highered.pdf. |

| 41. |

P.L. 115-245, Division B, Title III, §5. |

| 42. |

See CRS Report R44164, ESEA Title I-A Formulas: In Brief. |

| 43. |

More information about the Innovative Approaches to Literacy Program is available at https://www2.ed.gov/programs/innovapproaches-literacy/index.html. |

| 44. |

For more information about block and categorical grants (in general), see CRS Report R40486, Block Grants: Perspectives and Controversies. |

| 45. |

CRS In Focus IF10333, The Every Student Succeeds Act (ESSA) and ESEA Reauthorization: Summary of Selected Key Issues. |

| 46. |

The required match in the Federal Work-Study program can be as high as one-half of the federal share or as low as zero, depending on the type of employment. For more information, see CRS Report RL31618, Campus-Based Student Financial Aid Programs Under the Higher Education Act. |

| 47. |

This amount includes only funds appropriated to the department through the annual appropriations process. |

| 48. |

For more information on these programs, see CRS Report RL31618, Campus-Based Student Financial Aid Programs Under the Higher Education Act; and CRS Report R41833, The Individuals with Disabilities Education Act (IDEA), Part B: Key Statutory and Regulatory Provisions. |

| 49. |

The costs of student loan and other federal credit program subsidies are calculated in accordance with the Federal Credit Reform Act of 1990 (FCRA). For a comparison of the FCRA accounting method and the alternative fair-value method, see CRS Report R44193, Federal Credit Programs: Comparing Fair Value and the Federal Credit Reform Act (FCRA). |

| 50. |

These tables may be found at http://nces.ed.gov/programs/digest/current_tables.asp. |

| 51. |

Available at http://www2.ed.gov/about/overview/budget/index.html. |

| 52. |

See the "Appropriations Status Table" on CRS.gov, http://www.crs.gov/AppropriationsStatusTable/Index. |

| 53. |

For further information about appropriations report language, see CRS Report R44124, Appropriations Report Language: Overview of Development, Components, and Issues for Congress. |

| 54. |

A conference report contains the formal legislative language on which the conference committee has agreed. A JES explains the various elements of the conferees' agreement. For further information, see CRS Report 98-382, Conference Reports and Joint Explanatory Statements. |

| 55. |

For further information on CRs, see CRS Report R42647, Continuing Resolutions: Overview of Components and Recent Practices. |

| 56. |

For further information on funding lapses and government shutdowns, including a discussion of some of the factors listed in this report, see CRS Report RL34680, Shutdown of the Federal Government: Causes, Processes, and Effects. |