Continuing Resolutions: Overview of Components and Practices

The program activities of most federal agencies are generally funded on an annual basis through the enactment of regular appropriations acts. When those annual appropriations acts are not enacted by the beginning of the fiscal year (i.e., by October 1), one or more continuing appropriations acts (commonly known as continuing resolutions or CRs) may be enacted to provide temporary funding to continue certain programs and activities until action on the regular appropriations acts is completed.

Congress has included six main components in CRs. First, CRs have provided funding for certain activities (coverage), which are typically specified with reference to the prior fiscal year’s appropriations acts. Second, CRs have provided budget authority for a specified duration of time. This duration may be as short as a single day or as long as the remainder of the fiscal year. Third, CRs have provided funds based on an overall funding rate. Fourth, the use of budget authority provided in the CR has been prohibited for new activities not funded in the previous fiscal year. Fifth, the duration and amount of funds in the CR, and purposes for which they may be used for specified activities, may be adjusted through anomalies. Sixth, legislative provisions—which create, amend, or extend other laws—have been included in some instances.

This report provides detailed information on CRs beginning with FY1977, which was the first fiscal year that began on October 1. Congress has enacted one or more CRs in all but three of the last 43 fiscal years (FY1977-FY2019). In addition, in 10 of the last 18 fiscal years, the initial CR—and in some years subsequent CRs—provided continuing appropriations for all the regular appropriations acts.

After FY1997—the most recent fiscal year that all regular appropriations bills were enacted before the start of the new fiscal year—an average of at least five CRs were signed into law for each fiscal year before the appropriations process was completed for that year. During this period, CRs provided funding for an average of almost five months each fiscal year.

For some fiscal years, a CR has provided continuing appropriations (i.e., at a rate of operations) through the end of that year (often referred to as a full-year CR). Most recently, a full-year CR was enacted for most of the regular appropriations acts for FY2007, FY2011, and FY2013. In the 1980s, in contrast, some “full-year CRs” actually included the full text of certain regular appropriations acts (i.e., in the form of an omnibus appropriations act rather than a typical CR).

Continuing Resolutions: Overview of Components and Practices

Jump to Main Text of Report

Contents

- Introduction

- Main Components of Continuing Resolutions

- Coverage

- Duration

- Funding Rate

- Purpose for Funds and Restrictions on New Activities

- Exceptions to Duration, Amount, and Purposes: Anomalies

- Duration

- Amount

- Purpose

- Legislative Provisions

- The Enactment of Regular Appropriations Bills and Use of CRs, FY1977-FY2019

- Duration and Frequency of Continuing Resolutions, FY1998-FY2019

- Features of Full-Year CRs After FY1977

Tables

- Table 1. CRS Appropriations Procedure Experts

- Table 2. Enactment of Regular Appropriations Bills and Use of Continuing Resolutions (CRs): FY1977-FY2019

- Table 3. Number and Duration of Continuing Resolutions (CRs): FY1998-FY2019

- Table 4. Appropriations Acts Containing Full-Year Continuing Resolutions (CRs): FY1977-FY2019

- Table 5. Number, Page Length, and Duration of Continuing Resolutions (CRs): FY1977-FY2019

Summary

The program activities of most federal agencies are generally funded on an annual basis through the enactment of regular appropriations acts. When those annual appropriations acts are not enacted by the beginning of the fiscal year (i.e., by October 1), one or more continuing appropriations acts (commonly known as continuing resolutions or CRs) may be enacted to provide temporary funding to continue certain programs and activities until action on the regular appropriations acts is completed.

Congress has included six main components in CRs. First, CRs have provided funding for certain activities (coverage), which are typically specified with reference to the prior fiscal year's appropriations acts. Second, CRs have provided budget authority for a specified duration of time. This duration may be as short as a single day or as long as the remainder of the fiscal year. Third, CRs have provided funds based on an overall funding rate. Fourth, the use of budget authority provided in the CR has been prohibited for new activities not funded in the previous fiscal year. Fifth, the duration and amount of funds in the CR, and purposes for which they may be used for specified activities, may be adjusted through anomalies. Sixth, legislative provisions—which create, amend, or extend other laws—have been included in some instances.

This report provides detailed information on CRs beginning with FY1977, which was the first fiscal year that began on October 1. Congress has enacted one or more CRs in all but three of the last 43 fiscal years (FY1977-FY2019). In addition, in 10 of the last 18 fiscal years, the initial CR—and in some years subsequent CRs—provided continuing appropriations for all the regular appropriations acts.

After FY1997—the most recent fiscal year that all regular appropriations bills were enacted before the start of the new fiscal year—an average of at least five CRs were signed into law for each fiscal year before the appropriations process was completed for that year. During this period, CRs provided funding for an average of almost five months each fiscal year.

For some fiscal years, a CR has provided continuing appropriations (i.e., at a rate of operations) through the end of that year (often referred to as a full-year CR). Most recently, a full-year CR was enacted for most of the regular appropriations acts for FY2007, FY2011, and FY2013. In the 1980s, in contrast, some "full-year CRs" actually included the full text of certain regular appropriations acts (i.e., in the form of an omnibus appropriations act rather than a typical CR).

Introduction

The program activities of most federal agencies are generally funded on an annual basis through the enactment of 12 regular appropriations acts.1 When those annual appropriations acts are not enacted by the beginning of the fiscal year (i.e., by October 1), one or more continuing appropriations acts may be enacted to provide temporary funding to continue certain programs and activities until action on regular appropriations acts is completed. Such funding is provided for a specified period of time, which may be extended through the enactment of subsequent CRs.

A continuing appropriations act is commonly referred to as a continuing resolution or CR because it has typically been in the form of a joint resolution rather than a bill. But there is no procedural requirement as to its form. Continuing appropriations are also occasionally provided through a bill.

If appropriations are not enacted for a fiscal year through a regular appropriations act or a CR, a "funding gap" occurs until such appropriations are provided. When a funding gap occurs, federal agencies may be directed to begin a "shutdown" of the affected programs and activities.2 Agencies are generally prohibited from obligating or expending federal funds in the absence of appropriations.3

Congress has enacted one or more CRs in all but three of the 43 fiscal years since FY1977.4 Further information is available in Table 2 of this report. In total, 186 CRs were enacted into law during the period covering FY1977-FY2019, ranging from zero to 21 in any single fiscal year. On average, about four CRs were enacted each fiscal year during this interval. Table 3 and Figure 1 of this report provide more information on this aspect of CRs.

This report provides an overview of the components of CRs and information about congressional practices related to their use.5 The first section of this report explains six of the typical main components of CRs: coverage, duration, funding rate, restrictions on new activities, anomalies, and legislative provisions. The second section discusses the enactment of regular appropriations acts prior to the start of the fiscal year and the number of CRs enacted, beginning with FY1977, which was the first fiscal year that began on October 1. The third section provides information on the variation in the number and duration of CRs enacted each fiscal year after FY1997—the most recent fiscal year in which all regular appropriations were enacted before the start of the new fiscal year. Finally, the fourth section of this report discusses the features of the 15 "full-year CRs" that provided funding through the remainder of the fiscal year. For further information, see Table 4 in this report. A list of all CRs enacted between FY1977 and FY2019 is provided at the end of this report in Table 5.

This report has been updated from the previous January 2016 version to include information on FY2017, FY2018, and FY2019.

|

Area of Expertise |

Name/Title |

|

Appropriations Procedure and Budget Enforcement |

Kate P. McClanahan |

|

James V. Saturno |

|

|

Megan Lynch |

|

|

Bill Heniff Jr. |

|

|

Appropriations Status Table |

Justin Murray |

Main Components of Continuing Resolutions

Congress has included six main components in CRs. First, CRs provide funding for certain activities (coverage), which are typically specified with reference to the prior or current fiscal year's appropriations acts. Second, CRs provide budget authority for a specified duration of time.6 This duration may be as short as a single day or as long as the remainder of the fiscal year. Third, CRs typically provide funds based on an overall funding rate. Fourth, the use of budget authority provided in the CR is typically prohibited for new activities not funded in the previous fiscal year. Fifth, the duration and amount of funds in the CR, and purposes for which they may be used for specified activities, may be adjusted through anomalies. Sixth, legislative provisions—which create, amend, or extend other laws—have been included in some instances.

Although this section discusses the above components as they have been enacted in CRs under recent practice, it does not discuss their potential effects on budget execution or agency operations. For analysis of these issues, see CRS Report RL34700, Interim Continuing Resolutions (CRs): Potential Impacts on Agency Operations.

Coverage

A CR provides funds for certain activities, which are typically specified with reference to other pieces of appropriations legislation or the appropriations acts for a previous fiscal year. Most often, the coverage of a CR is defined with reference to the activities funded in prior fiscal years' appropriations acts for which the current fiscal year's regular appropriations have yet to be enacted. For example, in Section 101 of P.L. 111-68 (the first CR for FY2010), the coverage included activities funded in selected regular and supplemental appropriations acts for FY2008 and FY2009:

Sec. 101. Such amounts as may be necessary… under the authority and conditions provided in such Acts, for continuing projects or activities (including the costs of direct loans and loan guarantees) that are not otherwise specifically provided for in this joint resolution, that were conducted in fiscal year 2009, and for which appropriations, funds, or other authority were made available in the following appropriations Acts:

(1) Chapter 2 of title IX of the Supplemental Appropriations Act, 2008 (P.L. 110-252).

(2) Section 155 of division A of the Consolidated Security, Disaster Assistance, and Continuing Appropriations Act, 2009 (P.L. 110-329), except that subsections (c), (d), and (e) of such section shall not apply to funds made available under this joint resolution.

(3) Divisions C through E of the Consolidated Security, Disaster Assistance, and Continuing Appropriations Act, 2009 (P.L. 110-329).

(4) Divisions A through I of the Omnibus Appropriations Act, 2009 (P.L. 111-8), as amended by section 2 of P.L. 111-46.

(5) Titles III and VI (under the heading `Coast Guard') of the Supplemental Appropriations Act, 2009 (P.L. 111-32). [emphasis added]

Less frequently, CRs specify coverage with reference to regular appropriations bills for the current fiscal year that have yet to be enacted.7 In these instances, it is possible that an activity covered in the corresponding previous fiscal year's appropriations bill might not be covered in the CR. Alternatively, a CR might stipulate that activities funded in the previous fiscal year are covered only if they are included in a regular appropriations bill for the current fiscal year. For example, Section 101 of P.L. 105-240, the first CR for FY1999, provided that funding would continue only under such circumstances.

SEC. 101. (a) Such amounts as may be necessary under the authority and conditions provided in the applicable appropriations Act for the fiscal year 1998 for continuing projects or activities including the costs of direct loans and loan guarantees (not otherwise specifically provided for in this joint resolution) which were conducted in the fiscal year 1998 and for which appropriations, funds, or other authority would be available in the following appropriations Acts:

(1) the Agriculture, Rural Development, Food and Drug Administration, and Related Agencies Appropriations Act, 1999….

(8) the Departments of Labor, Health and Human Services, and Education, and Related Agencies Appropriations Act, 1999, the House and Senate reported versions of which shall be deemed to have passed the House and Senate respectively as of October 1, 1998, for the purposes of this joint resolution, unless a reported version is passed as of October 1, 1998, in which case the passed version shall be used in place of the reported version for purposes of this joint resolution;

(9) the Legislative Branch Appropriations Act, 1999…. [emphasis added]

CRs may be enacted as stand-alone legislative vehicles or as provisions attached to a regular appropriations bill or an omnibus bill.8 In instances in which one or more regular appropriations bills are near completion, Congress may find it expeditious to include a CR in that same legislative vehicle to cover activities in the remaining regular bills that are not yet enacted. In such instances, some activities may be covered by reference while funding for others is provided through the text of the measure. For example, Division C of P.L. 115-245—the Department of Defense and Labor, Health and Human Services, and Education Appropriations Act, 2019, and Continuing Appropriations Act, 2019—provided continuing appropriations through December 7, 2018, by referencing the FY2018 regular appropriations acts, while the other divisions of P.L. 115-245 provided full-year regular appropriations for the FY2019 Defense and Labor-HHS-ED bills.

Duration

The duration of a CR refers to the period for which budget authority is provided for covered activities. The period ends either upon the enactment of the applicable regular appropriations act or on an expiration date specified in the CR, whichever occurs first. When a CR expires prior to the completion of all regular appropriations bills for a fiscal year, one or more additional CRs may be enacted to prevent funding gaps and secure additional increments of time to complete the remaining regular appropriations bills. The duration of any further CRs may be brief, sometimes a single day, to encourage the process to conclude swiftly, or it may be for weeks or months to accommodate further negotiations or congressional recesses. In some cases, CRs have carried over into the next session of Congress.

In most of the fiscal years in which CRs have been used, a series of two or more have been enacted into law.9 Such CRs may be designated by their order (e.g., "first" CR, "second" CR) or, after the initial CR has been enacted, designated as a "further" CR. When action on the regular appropriations bills is not complete by the time when the first CR expires, subsequent CRs will often simply replace the expiration date in the preceding CR with a new expiration date. For example, Section 1 of the third CR for FY2016, P.L. 114-100, stated that "Public Law 114-53 is amended by striking the date specified in Section 106(3) and inserting 'December 22, 2015.'" This action extended the duration of the preceding CR by six days.

Funds provided by a CR will not necessarily be used by all covered activities through the date the CR expires. In practice, the budget authority provided by a CR may be superseded by the enactment of subsequent appropriations measures or the occurrence of other specified conditions. In an instance in which a regular appropriations bill was enacted prior to the expiration of a CR, the budget authority provided by the regular bill for covered activities would replace the funding provided by the CR. All other activities in the CR, however, would continue to be funded by the CR unless they were likewise superseded or the CR expired. The duration of funds for certain activities could also be shortened if other conditions that are specified in the CR occur. For example, Section 107 of P.L. 108-84, the first CR for FY2004, provided funds for 31 days or fewer:

Sec. 107. Unless otherwise provided for in this joint resolution or in the applicable appropriations Act, appropriations and funds made available and authority granted pursuant to this joint resolution shall be available until (a) enactment into law of an appropriation for any project or activity provided for in this joint resolution, or (b) the enactment into law of the applicable appropriations Act by both Houses without any provision for such project or activity, or (c) October 31, 2003, whichever first occurs. [emphasis added]

In this instance, funding for all other activities not subject to these conditions would continue under the CR until it expired or was otherwise superseded.

When a CR is attached to a regular appropriations bill, the activities covered by regular appropriations are funded through the remainder of the fiscal year, whereas the activities covered by the CR are funded through a specified date. Congress may also single out specific activities in a CR to receive funding for a specified duration that differs from the vast majority of other accounts and activities. This type of variation in duration is discussed in the "Exceptions to Duration, Amount, and Purposes: Anomalies" section.

As an alternative to the separate enactment of one or more of the regular appropriations bills for a fiscal year, a CR may provide funds for the activities covered in such bills through the remainder of the fiscal year. This type of CR is referred to as a full-year CR. Full-year CRs may provide funding for all bills that have yet to be enacted or include the full text of one or more regular appropriations bills. For example, Division A of P.L. 112-10 contained the text of the FY2011 Defense Appropriations Act, whereas the programs and activities covered by the 11 remaining regular appropriations bills were funded by the full-year CR in Division B.

Funding Rate

CRs often fund activities under a formula-type approach that provides budget authority at a restricted level but not a specified amount. This method of providing budget authority is commonly referred to as the "funding rate." Under a funding rate, the amount of budget authority for an account10 is calculated as the total amount of budget authority annually available based on a reference level (usually a dollar amount or calculation), multiplied by the fraction of the fiscal year for which the funds are made available in the CR.11 This is in contrast to regular and supplemental appropriations acts, which generally provide specific amounts for each account.

In previous years, many CRs have provided funding across accounts by reference to the amount of budget authority available in specified appropriations acts from the previous fiscal year. For example, Section 101 of P.L. 110-329, the first CR for FY2010, provided the following funding rate:

Such amounts as may be necessary, at a rate for operations as provided in the applicable appropriations Acts for fiscal year 2008 and under the authority and conditions provided in such Acts, for continuing projects or activities (including the costs of direct loans and loan guarantees) that are not otherwise specifically provided for in this joint resolution, that were conducted in fiscal year 2008, and for which appropriations, funds, or other authority were made available in the following appropriations Acts: divisions A, B, C, D, F, G, H, J, and K of the Consolidated Appropriations Act, 2008 (P.L. 110-161). [emphasis added]

Other CRs have provided funding by reference to the levels available in the previous fiscal year, with either an increase or decrease from the previous fiscal year's level. For example, Section 101(a) and (b) of P.L. 112-33, the first CR for FY2012, provided the following funding rate:

(a) Such amounts as may be necessary, at a rate for operations as provided in the applicable appropriations Acts for fiscal year 2011 and under the authority and conditions provided in such Acts, for continuing projects or activities (including the costs of direct loans and loan guarantees) that are not otherwise specifically provided for in this Act, that were conducted in fiscal year 2011, and for which appropriations, funds, or other authority were made available in the following appropriations Acts….

(b) The rate for operations provided by subsection (a) is hereby reduced by 1.503 percent. [emphasis added]

Although these examples illustrate the most typical types of funding rates, other types of funding rates have sometimes been used when providing continuing appropriations. For example, P.L. 105-240, the first CR for FY1999, provided a variable funding rate for covered activities. Specifically, the CR provided funds derived from three possible reference sources: the House- and Senate-passed FY1999 regular appropriations bills, the amount of the President's budget request, or "current operations" (the total amount of budget authority available for obligation for an activity during the previous fiscal year), whichever was lower. In instances where no funding was provided under the House-and Senate-passed FY1999 appropriations bills, the funding rate would be based on the lower of the President's budget request or current operations. In addition, while the first CR for a fiscal year may provide a certain funding rate, subsequent CRs sometimes may provide a different rate.

CRs have sometimes provided budget authority for some or all covered activities by incorporating the actual text of one or more regular appropriations bills for that fiscal year rather than providing funding according to the rate formula.12 For example, P.L. 112-10 provided funding for the Department of Defense through the incorporation of a regular appropriations bill in Division A, whereas Division B provided formulaic funding for all other activities for the remainder of the fiscal year.13 In this type of instance, the formula in the CR applies only to activities not covered in the text of the incorporated regular appropriations bill or bills.

Purpose for Funds and Restrictions on New Activities

CRs that provide a funding rate for activities often stipulate that funds may be used for the purposes and in the manner provided in specified appropriations acts for the previous fiscal year. CRs may also provide that the funds provided may be used only for activities funded in the previous fiscal year. In practice, this is often characterized as a prohibition on "new starts." In addition, conditions and limitations on program activity from the previous year's appropriations acts may be retained by language contained within the resolution's text. An example of such language, from P.L. 112-33, is below:

Sec. 103. Appropriations made by section 101 shall be available to the extent and in the manner that would be provided by the pertinent appropriations Act. [emphasis added]

Sec. 104. Except as otherwise provided in section 102, no appropriation or funds made available or authority granted pursuant to section 101 shall be used to initiate or resume any project or activity for which appropriations, funds, or other authority were not available during fiscal year 2011. [emphasis added]

This language prevents the initiation of new activities with the funds provided in the CR. Agencies may use appropriated funds from prior fiscal years that remain available, however, to initiate new activities in some circumstances.14

Exceptions to Duration, Amount, and Purposes: Anomalies

Even though CRs typically provide funds at a rate, they may also include provisions that enumerate exceptions to the duration, amount, or purposes for which those funds may be used for certain appropriations accounts or activities. Such provisions are commonly referred to as "anomalies." The purpose of anomalies is to preserve Congress's constitutional prerogative to provide appropriations in the manner it sees fit, even in instances when only short-term funding is provided.15

Duration

A CR may contain anomalies that designate a duration of funding for certain activities that is different from the overall duration provided. For example, Section 112 of P.L. 108-84 provided an exception to the expiration date of October 31, 2003, specified in Section 107(c) of the CR:

For entitlements and other mandatory payments whose budget authority was provided in appropriations Acts for fiscal year 2003, and for activities under the Food Stamp Act of 1977, activities shall be continued at the rate to maintain program levels under current law, under the authority and conditions provided in the applicable appropriations Act for fiscal year 2003, to be continued through the date specified in section 107(c): Provided, That notwithstanding section 107, funds shall be available and obligations for mandatory payments due on or about November 1 and December 1, 2003, may continue to be made. [emphasis added]

Amount

Anomalies may also designate a specific amount or rate of budget authority for certain accounts or activities that is different than the funding rate provided for the remainder of activities in the CR.16 Typically, such funding is specified as an annualized rate based upon a lump sum. For example, Section 120 of P.L. 112-33 provided the following anomaly for a specific account, which was an exception to the generally applicable rate in Section 101:

Notwithstanding section 101, amounts are provided for "Defense Nuclear Facilities Safety Board—Salaries and Expenses" at a rate for operations of $29,130,000. [emphasis added]

Funding adjustments can also be provided in anomalies for groups of accounts in the bill. For example, Section 121 of P.L. 112-33 provided a different rate for certain funds in a group of accounts:

Notwithstanding any other provision of this Act, except section 106, the District of Columbia may expend local funds under the heading "District of Columbia Funds" for such programs and activities under title IV of H.R. 2434 (112th Congress), as reported by the Committee on Appropriations of the House of Representatives, at the rate set forth under ''District of Columbia Funds—Summary of Expenses'' as included in the Fiscal Year 2012 Budget Request Act of 2011 (D.C. Act 19–92), as modified as of the date of the enactment of this Act. [emphasis added]

Further, anomalies may provide exceptions to amounts specified in other laws. For example, Section 121 of P.L. 110-329 provided that funds may be expended in excess of statutory limits up to an alternative rate.

Notwithstanding the limitations on administrative expenses in subsections (c)(2) and (c)(3)(A) of section 3005 of the Digital Television Transition and Public Safety Act of 2005 (P.L. 109-171; 120 Stat. 21), the Assistant Secretary (as such term is defined in section 3001(b) of such Act) may expend funds made available under sections 3006, 3008, and 3009 of such Act for additional administrative expenses of the digital-to-analog converter box program established by such section 3005 at a rate not to exceed $180,000,000 through the date specified in section 106(3) of this joint resolution. [emphasis added]

Purpose

CRs may also use anomalies to alter the purposes for which the funds may be expended. Such anomalies may allow funds to be spent for activities that would otherwise be prohibited or prohibit funds for activities that might otherwise be allowed. For example, Section 114 of P.L. 108-309, the first CR for FY2005, prohibited funds from being available to a particular department for a certain activity:

Notwithstanding any other provision of this joint resolution, except sections 107 and 108, amounts are made available for the Strategic National Stockpile ("SNS") at a rate for operations not exceeding the lower of the amount which would be made available under H.R. 5006, as passed by the House of Representatives on September 9, 2004, or S. 2810, as reported by the Committee on Appropriations of the Senate on September 15, 2004: Provided, That no funds shall be made available for the SNS to the Department of Homeland Security under this joint resolution…. [emphasis added]

Legislative Provisions

Substantive legislative provisions, which have the effect of creating new law or changing existing law, have also been included in some CRs. One reason why CRs have been attractive vehicles for such provisions is that they are often widely considered to be must-pass measures to prevent funding gaps. Legislative provisions previously included in CRs have varied considerably in length, from a short paragraph to more than 200 pages.

House and Senate rules restrict the inclusion of legislative provisions in appropriations bills, but such restrictions are applicable in different contexts. Although House rules prohibit legislative provisions from being included in general appropriations measures (including amendments or any conference report to such measures), these restrictions do not apply to CRs.17 Senate rules prohibit non-germane amendments that include legislative provisions either on the Senate floor or as an amendment between the houses.18 While these Senate restrictions do apply in the case of CRs, there is considerable leeway on when such provisions may be included, such as when the Senate amends a legislative provision included by the House.19 The rules of the House and Senate are not self-enforcing. A point of order must be raised and sustained to prevent any legislative language from being considered and enacted.20

Substantive provisions in CRs have included language that established major new policies, such as an FY1985 CR, which contained the Comprehensive Crime Control Act of 1984.21

More frequently, CRs have been used to amend or renew provisions of law. For example, Section 140 of P.L. 112-33 retroactively renewed import restrictions under the Burmese Freedom and Democracy Act of 2003 (P.L. 108-61):

(a) Renewal of Import Restrictions Under Burmese Freedom and Democracy Act of 2003.—

(1) In general.—Congress approves the renewal of the import restrictions contained in section 3(a)(1) and section 3A (b)(1) and (c)(1) of the Burmese Freedom and Democracy Act of 2003.

(2) Rule of construction.—This section shall be deemed to be a "renewal resolution" for purposes of section 9 of the Burmese Freedom and Democracy Act of 2003.

(b) Effective Date.—This section shall take effect on July 26, 2011.

CRs have also contained legislative provisions that temporarily extended expiring laws. For example, Section 136 of P.L. 115-298 extended the National Flood Insurance Program:

Sec. 136. Sections 1309(a) and 1319 of the National Flood Insurance Act of 1968 (42 U.S.C. 4016(a) and 4026) shall be applied by substituting the date specified in section 105(3) of this Act for 'December 7, 2018.'

Legislative provisions that temporarily extend expiring laws are effective through the date the CR expires, unless otherwise specified.

The Enactment of Regular Appropriations Bills and Use of CRs, FY1977-FY2019

As mentioned previously, regular appropriations were enacted after October 1 in all but four fiscal years between FY1977 and FY2019. Consequently, CRs have been needed in almost all of these years to prevent one or more funding gaps from occurring.22

Table 2 provides an overview of the enactment of regular appropriations bills and the use of CRs between FY1977 and FY2019. All appropriations were enacted before the start of the new fiscal year four times during this period: FY1977, FY1989, FY1995, and FY1997. Over half of the regular appropriations bills for a fiscal year were enacted before the start of the new fiscal year in only one instance (FY1978). In all other fiscal years, fewer than six regular appropriations acts were enacted on or before October 1. In addition, in 15 out of the 43 years during this period, no regular appropriations bills were enacted prior to the start of the fiscal year. Ten of these fiscal years have occurred in the interval since FY2001.

Table 2. Enactment of Regular Appropriations Bills and

Use of Continuing Resolutions (CRs): FY1977-FY2019

|

Fiscal Year |

Number of Regular Appropriations Billsa |

Regular Appropriations Bills Enacted on or Before October 1 |

CRs Enactedb |

|

1977 |

13 |

13 |

2c |

|

1978 |

13 |

9 |

3 |

|

1979 |

13 |

5 |

1 |

|

1980 |

13 |

3 |

2 |

|

1981 |

13 |

1 |

3 |

|

1982 |

13 |

1 |

4 |

|

1983 |

13 |

1 |

2 |

|

1984 |

13 |

4 |

2 |

|

1985 |

13 |

4 |

5 |

|

1986 |

13 |

0 |

5 |

|

1987 |

13 |

0 |

6 |

|

1988 |

13 |

0 |

5 |

|

1989 |

13 |

13 |

0 |

|

1990 |

13 |

1 |

3 |

|

1991 |

13 |

0 |

5 |

|

1992 |

13 |

3 |

4 |

|

1993 |

13 |

1 |

1 |

|

1994 |

13 |

2 |

3 |

|

1995 |

13 |

13 |

0 |

|

1996 |

13 |

0 |

13 |

|

1997 |

13 |

13 |

0 |

|

1998 |

13 |

1 |

6 |

|

1999 |

13 |

1 |

6 |

|

2000 |

13 |

4 |

7 |

|

2001 |

13 |

2 |

21 |

|

2002 |

13 |

0 |

8 |

|

2003 |

13 |

0 |

8 |

|

2004 |

13 |

3 |

5 |

|

2005 |

13 |

1 |

3 |

|

2006 |

11 |

2 |

3 |

|

2007 |

11 |

1 |

4 |

|

2008 |

12 |

0 |

4 |

|

2009 |

12 |

3 |

2 |

|

2010 |

12 |

1 |

2 |

|

2011 |

12 |

0 |

8 |

|

2012 |

12 |

0 |

5 |

|

2013 |

12 |

0 |

2 |

|

2014 |

12 |

0 |

4 |

|

2015 |

12 |

0 |

5 |

|

2016 |

12 |

0 |

3 |

|

2017 |

12 |

1 |

3 |

|

2018 |

12 |

0 |

5 |

|

2019 |

12 |

5 |

3 |

Sources: U.S. Congress, Senate Committee on Appropriations, Appropriations, Budget Estimates, Etc., 94th Congress, 2nd session-104th Congress, 1st session (Washington: GPO, 1976-1995). U.S. Congress, House of Representatives, Calendars of the U.S. House of Representatives and History of Legislation, 104th Congress, 1st session-113th Congress, 1st session (Washington: GPO, 1995-2012). CRS appropriations status tables (FY1999-FY2019), http://www.crs.gov/pages/AppropriationsStatusTable.aspx.

a. Between the 95th and 108th Congresses, there were 13 House and Senate Appropriations subcommittees responsible for one regular appropriations bill each. During the 109th Congress, due to subcommittee realignment, the total number of regular appropriations bills was effectively reduced to 11 during each year of the Congress. Beginning in the 110th Congress, subcommittee jurisdictions were again realigned for a total of 12 subcommittees, each of which is currently responsible for a single regular appropriations bill. For further information on subcommittee realignment during this period, see CRS Report RL31572, Appropriations Subcommittee Structure: History of Changes from 1920 to 2019.

b. For further information on each of these CRs, see Table 3.

c. Although all 13 FY1977 regular appropriations bills became law on or before the start of the fiscal year, two CRs were enacted to provide funding generally for certain activities that had not been included in the regular appropriations acts.

CRs were enacted in all but three of these fiscal years (FY1989, FY1995, and FY1997). In FY1977, although all 13 regular appropriations bills became law on or before the start of the fiscal year, two CRs were enacted to provide funding for certain activities that had not been included in the regular appropriations acts.

Duration and Frequency of Continuing Resolutions, FY1998-FY2019

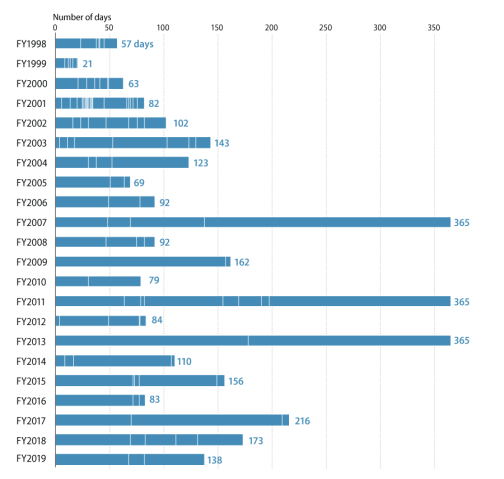

CRs have been a significant element of the recent annual appropriations process.23 As shown in Table 3, a total of 117 CRs were enacted into law from FY1998 to FY2019. While the average number of such measures enacted per year was about five, the number enacted ranged from two measures (for FY2009, FY2010, and FY2013) to 21 (for FY2001).

During the past 22 fiscal years, Congress provided funding by means of a CR for an average of almost five months (143 days) each fiscal year. Taking into account the total duration of all CRs for each fiscal year, the period for which continuing appropriations were provided ranged from 21 days to 365 days. On average, each of the 117 CRs lasted for about 39 days; 53 of these were for seven days or fewer.24 Three full-year CRs were used during this period, for FY2007, FY2011, and FY2013.

In the first four instances (FY1998-FY2001), the expiration date of the final CR was set in the first quarter of the fiscal year on a date occurring between October 21 and December 21. The expiration date in the final CR for the next three fiscal years (FY2002-FY2004) and FY2019, however, was set in the following session of Congress on a date occurring between January 10 and February 20. In six of the next 12 fiscal years (FY2005, FY2006, FY2008, FY2010, FY2012, and FY2016), the expiration dates were in the first quarter of the fiscal year on a date occurring between December 8 and December 31. For the remaining fiscal years, the final CRs were enacted during the next session of Congress. In one instance, the final CR for the fiscal year expired during the month of January (FY2014). In three instances, the final CR expired in March (FY2009, FY2015, and FY2018). Three other final CRs—for FY2007, FY2011, and FY2013—provided funding through the end of the fiscal year.

|

Fiscal Year |

Number of |

Total |

Average |

Final |

|

1998 |

6 |

57 |

9.5 |

11-26-1997 |

|

1999 |

6 |

21 |

3.5 |

10-21-1998 |

|

2000 |

7 |

63 |

9.0 |

12-02-1999 |

|

2001 |

21 |

82 |

3.9 |

12-21-2000 |

|

2002 |

8 |

102 |

12.8 |

01-10-2002 |

|

2003 |

8 |

143 |

17.9 |

02-20-2003 |

|

2004 |

5c |

123 |

24.6 |

01-31-2004 |

|

2005 |

3 |

69 |

23.0 |

12-08-2004 |

|

2006 |

3 |

92 |

30.7 |

12-31-2005 |

|

2007 |

4 |

365 |

91.3 |

09-30-2007 |

|

2008 |

4 |

92 |

23.0 |

12-31-2007 |

|

2009 |

2 |

162 |

81.0 |

03-11-2009 |

|

2010 |

2 |

79 |

39.5 |

12-18-2009 |

|

2011 |

8 |

365 |

45.6 |

9-30-2011 |

|

2012 |

5 |

84 |

16.8 |

12-23-2011 |

|

2013 |

2 |

365 |

182.5 |

9-30-2013 |

|

2014 |

4d |

110d |

27.5 |

01-18-2014 |

|

2015 |

5 |

156 |

31.3 |

03-06-2015 |

|

2016 |

3 |

83 |

27.7 |

12-22-2015 |

|

2017 |

3 |

216 |

72.0 |

05-05-2017 |

|

2018 |

5 |

173 |

34.6 |

03-23-2018 |

|

2019 |

3 |

138 |

46.0 |

02-15-2019 |

|

Total |

117 |

3,140 |

— |

— |

|

Annual Average |

5.3 |

142.7 |

38.8 |

— |

Sources: Prepared by the Congressional Research Service using data from the Legislative Information System; Congressional Research Service, appropriations status tables (various fiscal years), available at http://crs.gov/Pages/appover.aspx; and various other sources.

a. Duration in days is measured, in the case of the first CR for a fiscal year, from the first day of the year (October 1). For example, a CR enacted on September 30 that provided funding through October 12 would be measured as having a12-day duration. For subsequent CRs for a fiscal year, duration in days is measured from the day after the expiration of the preceding CR.

b. The final expiration date is the date the CR expired. In some of these instances, the CR had previously been superseded by the enactment of the remaining regular appropriations acts for that fiscal year. For example, in FY2014, the expiration date of P.L. 113-73, the fourth CR for FY2014, was January 18, 2014. However, final regular appropriations were enacted the previous day in the Consolidated Appropriations Act, 2014 (P.L. 113-76).

c. The fifth CR for FY2004 did not change the expiration date of January 31, 2004, established in the preceding CR.

d. A total of four CRs were enacted for FY2014. This count includes two CRs that provided funding for only specific programs and activities during the FY2014 funding gap. The Pay Our Military Act (P.L. 113-39) was enacted on September 30, 2013. The Department of Defense Survivor Benefits Continuing Appropriations Resolution, 2014 (P.L. 113-44), was enacted on October 10, 2013. The funding provided by both of these CRs was terminated on October 17, 2013, through the enactment of at third CR, P.L. 113-46, which broadly funded the previous fiscal year's activities through January 15, 2014. The funding provided by this third CR was extended through January 18 through the enactment of a fourth CR (P.L. 113-73). Section 118 of P.L. 113-46 provided that the time covered by that act was to have begun on October 1, 2013. To preserve counting consistency, the FY2014 duration of days for the purposes of this table and Figure 1 begins on October 1 and ends on January 18, 2014. For further information on the FY2014 funding gap and congressional action on CRs, see CRS Report RS20348, Federal Funding Gaps: A Brief Overview.

Figure 1 presents a representation of the duration of CRs for FY1998-FY2019. As the figure shows, there is no significant correlation between these two variables. For example, six CRs were enacted for both FY1998 and FY1999, but the same number of measures lasted for a period of 57 days for FY1998 and only 21 days for FY1999. The largest number of CRs enacted for a single fiscal year during this period—21 for FY2001—covered a period lasting 82 days at an average duration of about four days per act. The smallest number enacted—two each for FY2009, FY2010, and FY2013—covered 162 days, 79 days, and 365 days, respectively.

Figure 1 also shows considerable mix in the use of shorter-term and longer-term CRs for a single fiscal year. For example, for FY2001, 21 CRs covered the first 82 days of the fiscal year. The first 25 days were covered by a series of four CRs lasting between five and eight days each. The next 10 days, a period of intense legislative negotiations leading up to the national elections on November 7, 2000, were covered by a series of 10 one-day CRs. The next 31 days were covered by two CRs, the first lasting 10 days and the second lasting 21 days. The first of these two CRs was enacted into law on November 4, the Saturday before the election, and extended through November 14, the second day of a lame-duck session. The second CR was enacted into law on November 15 and expired on December 5, which was 10 days before the lame-duck session ended. The remaining five CRs, which ranged in duration from one to six days, covered the remainder of the lame-duck session and several days beyond (as the final appropriations measures passed by Congress were being processed for the President's approval).25

Table 5 provides more detailed information on the number, length, and duration of CRs enacted for FY1977-FY2019. As indicated previously, this represents the period after the start of the federal fiscal year was moved from July 1 to October 1 by the Congressional Budget Act.

|

Figure 1. Duration of Continuing Resolutions (CRs): FY1998-FY2019 |

|

|

Notes: Each segment of a bar for a fiscal year represents the duration in days of one CR. The left-most segment represents the first CR, effective beginning on October 1 (the start of the fiscal year). In the case of the initial CR for a fiscal year, duration in days is measured from the first day of the year through the expiration date. For subsequent CRs for a fiscal year, duration in days is measured from the day after the expiration of the preceding CR. Please see the notes to Table 3 in this report for a further explanation of the methodology for this figure. |

Features of Full-Year CRs After FY1977

Full-year CRs have been used to provide annual discretionary spending on a number of occasions. Prior to the full implementation of the Congressional Budget Act in FY1977, full-year CRs were used occasionally, particularly in the 1970s. Full-year CRs were enacted into law for four of the six preceding fiscal years (FY1971, FY1973, FY1975, and FY1976).26 Following the successful completion of all 13 regular appropriations acts prior to the start of FY1977, full-year CRs were used in each of the 11 succeeding fiscal years (FY1978-FY1988) to cover at least one regular appropriations act. Three years later, another full-year CR was enacted for FY1992. Most recently, full-year CRs were enacted for FY2007, FY2011, and FY2013.

Table 4 identifies the 15 full-year CRs enacted for the period since FY1977. Nine of the 15 full-year CRs during this period were enacted in the first quarter of the fiscal year—three in October, two in November, and four in December. The six remaining measures, however, were enacted during the following session between February 15 and June 5.

The full-year CRs enacted during this period also varied in terms of length and the form of funding provided. Full-year CRs prior to FY1983 were relatively short measures, ranging in length from one to four pages in the Statutes-at-Large. Beginning with FY1983 and extending through FY1988, however, the measures became much lengthier, ranging from 19 to 451 pages. The greater page length of full-year CRs enacted for the period covering FY1983-FY1988 may be explained by two factors. First, full-year CRs enacted prior to FY1983 generally established funding levels by formulaic reference. Beginning with FY1983, however, Congress began to incorporate the full text of some or all of the covered regular appropriations acts, thereby increasing its length considerably. None of the full-year CRs enacted between 1985 and 1988 used formulaic funding provisions. Secondly, the number of regular appropriations acts covered by full-year CRs increased significantly during the FY1983-FY1988 period. For the period covering FY1978-FY1982, the number of regular appropriations acts covered by CRs for the full fiscal year ranged from one to six (averaging about three). Beginning with FY1983 and extending through FY1988, the number of covered acts ranged from five to 13, averaging about 10.

The next two full-year CRs, for FY1992 and FY2007, returned to the earlier practice of using formulaic references and anomalies to establish funding levels. Both CRs provided funding only through this means. As a consequence, the length of these measures was considerably shorter than the FY1983 through FY1988 full-year CRs.

The two most recent full-year CRs, for FY2011 and FY2013, in some respects were a hybrid of the earlier and recent approaches. The FY2011 full-year CR provided funding for 11 bills through formulaic provisions and anomalies. It also carried the full text of one regular appropriations bill in a separate division of the act (the FY2011 Department of Defense Appropriations Act). Similarly, the FY2013 CR contained the texts of five regular appropriations bills in Divisions A through E of the act—the FY2013 Agriculture, Rural Development, Food and Drug Administration, and Related Agencies Appropriations Act; the Commerce, Justice, Science, and Related Agencies Appropriations Act; the Department of Defense Appropriations Act; the Department of Homeland Security Appropriations Act; and the Military Construction and Veterans Affairs and Related Agencies Appropriations Act. In addition, Division F was characterized as providing continuing appropriations for the remaining seven regular appropriations bills through formulaic provisions and anomalies. Unlike previous years, the formula for providing continuing appropriations was based on the amount provided in FY2012 rather than a rate.

|

Fiscal |

Public Law |

Enactment |

Page Length |

Included |

Number of Appropriations Acts Covered or Contained in the Acta |

|

1978 |

12-09-1977 |

2 |

No |

2/13b |

|

|

1979 |

10-18-1978 |

4 |

No |

1/13 |

|

|

1980 |

11-20-1979 |

4 |

Yes |

6/13c |

|

|

1981 |

06-05-1981 |

2d |

Yes |

5/13d |

|

|

1982 |

03-31-1982 |

1 |

Yes |

3/13e |

|

|

1983 |

12-21-1982 |

95 |

Yes |

7/13 |

|

|

1984 |

11-14-1983 |

19 |

Yes |

5/13f |

|

|

1985 |

10-12-1984 |

363 |

No |

9/13g |

|

|

1986 |

12-19-1985 |

142 |

No |

8/13h |

|

|

1987 |

10-30-1986 |

391 |

No |

13/13 |

|

|

1988 |

12-22-1987 |

451 |

No |

13/13 |

|

|

1992 |

04-01-1992 |

8 |

Yes |

1/13i |

|

|

2007 |

02-15-2007 |

53 |

Yes |

9/11j |

|

|

2011 |

04-15-2011 |

98 |

Yes |

12/12k |

|

|

2013 |

03-26-2013 |

240 |

Yes |

12/12l |

Sources: Prepared by the Congressional Research Service using data from the Legislative Information System; Congressional Research Service, appropriations status tables (various fiscal years), available at http://crs.gov/Pages/appover.aspx; and various other sources.

a. Between the 95th and 108th Congresses, there were 13 House and Senate Appropriations subcommittees responsible for one regular appropriations bill each. During the 109th Congress, due to subcommittee realignment, the total number of regular appropriations bills was effectively reduced to 11 during each year of the Congress. Beginning in the 110th Congress, subcommittee jurisdictions were again realigned for a total of 12 subcommittees, each of which is currently responsible for a single regular appropriations bill. For further information on subcommittee realignment during this period, see CRS Report RL31572, Appropriations Subcommittee Structure: History of Changes from 1920 to 2019, by James V. Saturno.

b. This full-year continuing appropriations for the District of Columbia provided by this act were later superseded by a standalone regular appropriations act (P.L. 95-288).

c. Some of the appropriations acts covered by this full-year CR were later superseded by standalone regular appropriations acts for Interior and Related Agencies (P.L. 96-126); Military Construction (96-130); Department of Defense (P.L. 96-154); and Transportation (P.L. 96-131).

d. This full-year CR was contained within the FY1981 Supplemental Appropriations and Rescissions Act 1981 (P.L. 97-12, see Title IV, "Further Continuing Appropriations"). Title IV extended through the end of the fiscal year the expiration of P.L. 96-536, which covered the appropriations acts that had not yet been enacted for Foreign Assistance; the Legislative Branch; Departments of Labor, Health and Human Services, Education, and Related Agencies; Departments of State, Justice, and Commerce, the Judiciary, and Related Agencies; the Treasury, Postal Service and General Government.

e. This full-year CR extended through the end of the fiscal year the expiration date of P.L. 97-92, which covered the appropriations acts that had not yet been enacted for the Treasury, Postal Service and General Government; Departments of Commerce, Justice, and State, the Judiciary; and Departments of Labor, Health and Human Services, Education, and Related Agencies.

f. Some of the appropriations acts covered by this full-year CR were later superseded by standalone regular appropriations acts for the Department of Defense (P.L. 98-121); Commerce, Justice, and State, the Judiciary, and Related Agencies (P.L. 98-166); and the Treasury, Postal Service and General Government (P.L. 98-151).

g. The full-year continuing appropriations for the Departments of Labor, Health and Human Services, Education, and Related Agencies that were provided by this act were later superseded by a standalone regular appropriations act (P.L. 98-619).

h. The Departments of Labor, Health and Human Services, Education, and Related Agencies provided by the CR were superseded by the enactment of P.L. 99-178.

i. This full-year CR extended through the end of FY1992 the expiration date of P.L. 102-163, which covered appropriations that had not yet been enacted for Foreign Operations, Export Financing, and Related Programs.

j. Despite the reorganization of the House and Senate Appropriations subcommittees at the beginning of the 110th Congress, the FY2007 CR (P.L. 110-5), which was enacted on February 15, 2007, reflected the subcommittee jurisdictions in the 109th Congress.

k. P.L. 112-10, Division B, provided continuing appropriations through the end of the fiscal year for Agriculture, Rural Development, Food and Drug Administration, and Related Agencies; Commerce, Justice, Science, and Related Agencies; Energy and Water Development and Related Agencies; Financial Services and General Government; Department of Homeland Security; Department of the Interior, Environment, and Related Agencies; Departments of Labor, Health and Human Services, Education, and Related Agencies; Legislative Branch; Military Construction and Veterans Affairs and Related Agencies; Department of State, Foreign Operations, and Related Programs; and Transportation, Housing and Urban Development, and Related Agencies. Division A contained the text of the Department of Defense Appropriations Act.

l. P.L. 113-6, Division F, provided continuing appropriations for FY2013 for Energy and Water Development and Related Agencies; Financial Services and General Government; Department of the Interior, Environment, and Related Agencies; Departments of Labor, Health and Human Services, Education, and Related Agencies; Legislative Branch; Department of State, Foreign Operations, and Related Programs; and Transportation, Housing and Urban Development, and Related Agencies. Divisions A through E contained the texts of the Agriculture, Rural Development, Food and Drug Administration, and Related Agencies Appropriations Act; Commerce, Justice, Science, and Related Agencies Appropriations Act; the Department of Defense Appropriations Act; Department of Homeland Security Appropriations Act; and Military Construction and Veterans Affairs and Related Agencies Appropriations Act.

|

Fiscal |

Number of Acts by Fiscal Year |

Number |

Public Law Number |

Statutes-at-Large |

Page Length |

Enactment Date |

Expiration Date |

Duration |

|

1977 |

1 |

1 |

90 Stat. 2065-2067 |

3 |

10-11-1976 |

03-31-1977 |

183 |

|

|

2 |

2 |

91 Stat. 28 |

1 |

04-01-1977 |

04-30-1977 |

30 |

||

|

1978 |

1 |

3 |

91 Stat. 1153-1154 |

2 |

10-13-1977 |

10-31-1977 |

31 |

|

|

2 |

4 |

91 Stat. 1323-1324 |

2 |

11-09-1977 |

11-30-1977 |

30 |

||

|

3 |

5 |

91 Stat. 1460-1461 |

2 |

12-09-1977 |

09-30-1978 |

304 |

||

|

1979 |

1 |

6 |

92 Stat. 1603-1605 |

3 |

10-18-1978 |

09-30-1979 |

365 |

|

|

1980 |

1 |

7 |

93 Stat. 656-663 |

8 |

10-12-1979 |

11-20-1979 |

51 |

|

|

2 |

8 |

93 Stat. 923-926 |

4 |

11-20-1979 |

09-30-1980 |

315 |

||

|

1981 |

1 |

9 |

94 Stat. 1351-1359 |

9 |

10-01-1980 |

12-15-1980 |

76 |

|

|

2 |

10 |

94 Stat. 3166-3172 |

7 |

12-16-1980 |

06-05-1981 |

172 |

||

|

3 |

11 |

95 Stat. 95-96 |

2 |

06-05-1981 |

09-30-1981 |

117 |

||

|

1982 |

1 |

12 |

95 Stat. 958-968 |

11 |

10-01-1981 |

11-20-1981 |

51 |

|

|

2 |

13 |

95 Stat. 1098 |

1 |

11-23-1981 |

12-15-1981 |

22 |

||

|

3 |

14 |

95 Stat. 1183-1203 |

21 |

12-15-1981 |

03-31-1982 |

106 |

||

|

4 |

15 |

96 Stat. 22 |

1 |

03-31-1982 |

09-30-1982 |

183 |

||

|

1983 |

1 |

16 |

96 Stat. 1186-1205 |

20 |

10-02-1982 |

12-17-1982 |

78 |

|

|

2 |

17 |

96 Stat. 1830-1924 |

95c |

12-17-1982 |

09-30-1983 |

287 |

||

|

1984 |

1 |

18 |

97 Stat. 733-743 |

11 |

10-01-1983 |

11-10-1983 |

41 |

|

|

2 |

19 |

97 Stat. 964-982 |

19 |

11-14-1983 |

09-30-1984 |

321 |

||

|

1985 |

1 |

20 |

98 Stat. 1699-1701 |

3 |

10-03-1984 |

10-03-1984 |

3 |

|

|

2 |

21 |

98 Stat. 1731 |

1 |

10-05-1984 |

10-05-1984 |

2 |

||

|

3 |

22 |

98 Stat. 1747 |

1 |

10-06-1984 |

10-09-1984 |

4 |

||

|

4 |

23 |

98 Stat. 1814 |

1 |

10-10-1984 |

10-11-1984 |

2 |

||

|

5 |

24 |

98 Stat. 1837-1976 |

140d |

10-12-1984 |

09-30-1985 |

354 |

||

|

1986 |

1 |

25 |

99 Stat. 471-473 |

3 |

09-30-1985 |

11-14-1985 |

45 |

|

|

2 |

26 |

99 Stat. 813 |

1 |

11-14-1985 |

12-12-1985 |

28 |

||

|

3 |

27 |

99 Stat. 1135 |

1 |

12-13-1985 |

12-16-1985 |

4 |

||

|

4 |

28 |

99 Stat. 1176 |

1 |

12-17-1985 |

12-19-1985 |

3 |

||

|

5 |

29 |

99 Stat. 1185-1326 |

142e |

12-19-1985 |

09-30-1986 |

285 |

||

|

1987 |

1 |

30 |

100 Stat. 1076-1079 |

4 |

10-01-1986 |

10-08-1986 |

8 |

|

|

2 |

31 |

100 Stat. 1185-1188 |

4 |

10-09-1986 |

10-10-1986 |

2 |

||

|

3 |

32 |

100 Stat. 1189 |

1 |

10-11-1986 |

10-15-1986 |

5 |

||

|

4 |

33 |

100 Stat. 1239 |

1 |

10-16-1986 |

10-16-1986 |

1 |

||

|

5 |

34 |

100 Stat. 1783 through 1783-385 |

386 |

10-18-1986 |

09-30-1987 |

349 |

||

|

6 |

35 |

100 Stat. 3341 through 3341-389 |

390 |

10-30-1986 |

[n/a]f |

— |

||

|

1988 |

1 |

36 |

101 Stat. 789-791 |

3 |

09-30-1987 |

11-10-1987 |

41 |

|

|

2 |

37 |

101 Stat. 903 |

1 |

11-10-1987 |

12-16-1987 |

36 |

||

|

3 |

38 |

101 Stat. 1310 |

1 |

12-16-1987 |

12-18-1987 |

2 |

||

|

4 |

39 |

101 Stat. 1314 |

1 |

12-20-1987 |

12-21-1987 |

3 |

||

|

5 |

40 |

101 Stat. 1329 through 1329-450 |

451g |

12-22-1987 |

09-30-1988 |

284 |

||

|

1989 |

[none] |

— |

— |

— |

— |

— |

— |

— |

|

1990 |

1 |

41 |

103 Stat. 638-640 |

3 |

09-29-1989 |

10-25-1989 |

25 |

|

|

2 |

42 |

103 Stat. 775-776 |

2 |

10-26-1989 |

11-15-1989 |

21 |

||

|

3 |

43 |

103 Stat. 934 |

1 |

11-15-1989 |

11-20-1989 |

5 |

||

|

1991 |

1 |

44 |

104 Stat. 867-870 |

4h |

10-01-1990 |

10-05-1990 |

5 |

|

|

2 |

45 |

104 Stat. 894-897 |

4 |

10-09-1990 |

10-19-1990 |

14 |

||

|

3 |

46 |

104 Stat. 1030-1033 |

4 |

10-19-1990 |

10-24-1990 |

5 |

||

|

4 |

47 |

104 Stat. 1075-1078 |

4 |

10-25-1990 |

10-27-1990 |

3 |

||

|

5 |

48 |

104 Stat. 1086-1087 |

2 |

10-28-1990 |

11-05-1990 |

9 |

||

|

1992 |

1 |

49 |

105 Stat. 551-554 |

4 |

09-30-1991 |

10-29-1991 |

29 |

|

|

2 |

50 |

105 Stat. 968-871 |

4 |

10-28-1991 |

11-14-1991 |

16i |

||

|

3 |

51 |

105 Stat. 1048 |

1 |

11-15-1991 |

11-26-1991 |

12 |

||

|

4 |

52 |

106 Stat. 92-99 |

8 |

04-01-1992 |

09-30-1992 |

183 |

||

|

1993 |

1 |

53 |

106 Stat. 1311-1314 |

4 |

10-01-1992 |

10-05-1992 |

5 |

|

|

1994 |

1 |

54 |

107 Stat. 977-980 |

4 |

09-30-1993 |

10-21-1993 |

21 |

|

|

2 |

55 |

107 Stat. 1114 |

1 |

10-21-1993 |

10-28-1993 |

7 |

||

|

3 |

56 |

107 Stat. 1355 |

1 |

10-29-1993 |

11-10-1993 |

13 |

||

|

1995 |

[none] |

— |

— |

— |

— |

— |

— |

— |

|

1996 |

1 |

57 |

109 Stat. 278-282 |

5 |

09-30-1995 |

11-13-1995 |

44 |

|

|

2 |

58 |

109 Stat. 540-545 |

6 |

11-19-1995 |

11-20-1995 |

7 |

||

|

3 |

59 |

109 Stat. 548-553 |

6 |

11-20-1995 |

12-15-1995 |

25 |

||

|

4 |

60 |

109 Stat. 767-772 |

6 |

12-22-1995 |

01-03-1996 |

19 |

||

|

5 |

61 |

110 Stat. 3-6 |

4 |

01-04-1996 |

01-25-1996 |

22 |

||

|

6 |

62 |

110 Stat. 10-14 |

5 |

01-06-1996 |

09-30-1996 |

290j |

||

|

7 |

63 |

110 Stat. 16-24 |

9 |

01-06-1996 |

09-30-1996 |

290 |

||

|

8 |

64 |

110 Stat. 25 |

1 |

01-06-1996 |

01-26-1996 |

42 |

||

|

9 |

65 |

110 Stat. 26-47 |

22 |

01-26-1996 |

03-15-1996 |

49j |

||

|

10 |

66 |

110 Stat. 826 |

1 |

03-15-1996 |

03-22-1996 |

7 |

||

|

11 |

67 |

110 Stat. 829 |

1 |

03-22-1996 |

03-29-1996 |

7 |

||

|

12 |

68 |

110 Stat. 876-878 |

3 |

03-29-1996 |

04-24-1996 |

26j |

||

|

13 |

69 |

110 Stat. 1213 |

1 |

04-24-1996 |

04-25-1996 |

1 |

||

|

1997 |

[none] |

— |

— |

— |

— |

— |

— |

— |

|

1998 |

1 |

70 |

111 Stat. 1153-1158 |

6 |

09-30-1997 |

10-23-1997 |

23 |

|

|

2 |

71 |

111 Stat. 1343 |

1 |

10-23-1997 |

11-07-1997 |

15 |

||

|

3 |

72 |

111 Stat. 1453 |

1 |

11-07-1997 |

11-09-1997 |

2 |

||

|

4 |

73 |

111 Stat. 1454 |

1 |

11-09-1997 |

11-10-1997 |

1 |

||

|

5 |

74 |

111 Stat. 1456 |

1 |

11-10-1997 |

11-14-1997 |

4 |

||

|

6 |

75 |

111 Stat. 1628 |

1 |

11-14-1997 |

11-26-1997 |

12 |

||

|

1999 |

1 |

76 |

112 Stat. 1566-1571 |

6 |

09-25-1998 |

10-09-1998 |

9 |

|

|

2 |

77 |

112 Stat. 1868 |

1 |

10-09-1998 |

10-12-1998 |

3 |

||

|

3 |

78 |

112 Stat. 1888 |

1 |

10-12-1998 |

10-14-1998 |

2 |

||

|

4 |

79 |

112 Stat. 1901 |

1 |

10-14-1998 |

10-16-1998 |

2 |

||

|

5 |

80 |

112 Stat. 1919 |

1 |

10-16-1998 |

10-20-1998 |

4 |

||

|

6 |

81 |

112 Stat. 2418 |

1 |

10-20-1998 |

10-21-1998 |

1 |

||

|

2000 |

1 |

82 |

113 Stat. 505-509 |

5 |

09-30-1999 |

10-21-1999 |

21 |

|

|

2 |

83 |

113 Stat. 1125 |

1 |

10-21-1999 |

10-29-1999 |

8 |

||

|

3 |

84 |

113 Stat. 1297 |

1 |

10-29-1999 |

11-05-1999 |

7 |

||

|

4 |

85 |

113 Stat. 1304 |

1 |

11-05-1999 |

11-10-1999 |

5 |

||

|

5 |

86 |

113 Stat. 1311 |

1 |

11-10-1999 |

11-17-1999 |

7 |

||

|

6 |

87 |

113 Stat. 1484 |

1 |

11-18-1999 |

11-18-1999 |

1 |

||

|

7 |

88 |

113 Stat. 1485 |

1 |

11-19-1999 |

12-02-1999 |

14 |

||

|

2001 |

1 |

89 |

114 Stat. 808-811 |

4 |

09-29-2000 |

10-06-2000 |

6 |

|

|

2 |

90 |

114 Stat. 866 |

1 |

10-06-2000 |

10-14-2000 |

8 |

||

|

3 |

91 |

114 Stat. 1073 |

1 |

10-13-2000 |

10-20-2000 |

6 |

||

|

4 |

92 |

114 Stat. 1318 |

1 |

10-20-2000 |

10-25-2000 |

5 |

||

|

5 |

93 |

114 Stat. 1397 |

1 |

10-26-2000 |

10-26-2000 |

1 |

||

|

6 |

94 |

114 Stat. 1398 |

1 |

10-26-2000 |

10-27-2000 |

1 |

||

|

7 |

95 |

114 Stat. 1450 |

1 |

10-27-2000 |

10-28-2000 |

1 |

||

|

8 |

96 |

114 Stat. 1550 |

1 |

10-28-2000 |

10-29-2000 |

1 |

||

|

9 |

97 |

114 Stat. 1551 |

1 |

10-29-2000 |

10-30-2000 |

1 |

||

|

10 |

98 |

114 Stat. 1676 |

1 |

10-30-2000 |

10-31-2000 |

1 |

||

|

11 |

99 |

114 Stat. 1741 |

1 |

11-01-2000 |

11-01-2000 |

1 |

||

|

12 |

100 |

114 Stat. 1811 |

1 |

11-01-2000 |

11-02-2000 |

1 |

||

|

13 |

101 |

114 Stat. 1897 |

1 |

11-03-2000 |

11-03-2000 |

1 |

||

|

14 |

102 |

114 Stat. 1898 |

1 |

11-04-2000 |

11-04-2000 |

1 |

||

|

15 |

103 |

114 Stat. 1899 |

1 |

11-04-2000 |

11-14-2000 |

10 |

||

|

16 |

104 |

114 Stat. 2436-2437 |

2 |

11-15-2000 |

12-05-2000 |

21 |

||

|

17 |

105 |

114 Stat. 2562 |

1 |

12-05-2000 |

12-07-2000 |

2 |

||

|

18 |

106 |

114 Stat. 2570 |

1 |

12-07-2000 |

12-08-2000 |

1 |

||

|

19 |

107 |

114 Stat. 2571 |

1 |

12-08-2000 |

12-11-2000 |

3 |

||

|

20 |

108 |

114 Stat. 2713 |

1 |

12-11-2000 |

12-15-2000 |

4 |

||

|

21 |

109 |

114 Stat. 2714 |

1 |

12-15-2000 |

12-21-2000 |

6 |

||

|

2002 |

1 |

110 |

115 Stat. 253-257 |

5 |

09-28-2001 |

10-16-2001 |

16 |

|

|

2 |

111 |

115 Stat. 261 |

1 |

10-12-2001 |

10-23-2001 |

7 |

||

|

3 |

112 |

115 Stat. 269 |

1 |

10-22-2001 |

10-31-2001 |

8 |

||

|

4 |

113 |

115 Stat. 406 |

1 |

10-31-2001 |

11-16-2001 |

16 |

||

|

5 |

114 |

115 Stat. 596 |

1 |

11-17-2001 |

12-07-2001 |

21 |

||

|

6 |

115 |

115 Stat. 809 |

1 |

12-07-2001 |

12-15-2001 |

8 |

||

|

7 |

116 |

115 Stat. 822 |

1 |

12-15-2001 |

12-21-2001 |

6 |

||

|

8 |

117 |

115 Stat. 960 |

1 |

12-21-2001 |

01-10-2002 |

20 |

||

|

2003 |

1 |

118 |

116 Stat. 1465-1468 |

4 |

09-30-2002 |

10-04-2002 |

4 |

|

|

2 |

119 |

116 Stat. 1482 |

1 |

10-04-2002 |

10-11-2002 |

7 |

||

|

3 |

120 |

116 Stat. 1492-1495 |

4 |

10-11-2002 |

10-18-2002 |

7 |

||

|

4 |

121 |

116 Stat. 1503 |

1 |

10-18-2002 |

11-22-2002 |

35 |

||

|

5 |

122 |

116 Stat. 2062-2063 |

2 |

11-23-2002 |

01-11-2003 |

50 |

||

|

6 |

123 |

117 Stat. 5-6 |

2 |

01-10-2003 |

01-31-2003 |

20 |

||

|

7 |

124 |

117 Stat. 8 |

1 |

01-31-2003 |

02-07-2003 |

7 |

||

|

8 |

125 |

117 Stat. 9 |

1 |

02-07-2003 |

02-20-2003 |

13 |

||

|

2004 |

1 |

126 |

117 Stat. 1042-1047 |

6 |

09-30-2003 |

10-31-2003 |

31 |

|

|

2 |

127 |

117 Stat. 1200 |

1 |

10-31-2003 |

11-07-2003 |

7 |

||

|

3 |

128 |

117 Stat. 1240 |

1 |

11-07-2003 |

11-21-2003 |

14 |

||

|

4 |

129 |

117 Stat. 1391 |

1 |

11-22-2003 |

01-31-2004 |

71 |

||

|

5 |

130 |

117 Stat. 2684 |

1 |

12-16-2003 |

[n/a]k |

— |

||

|

2005 |

1 |

131 |

118 Stat. 1137-1143 |

7 |

09-30-2004 |

11-20-2004 |

51 |

|

|

2 |

132 |

118 Stat. 2338 |

1 |

11-21-2004 |

12-03-2004 |

13 |

||

|

3 |

133 |

118 Stat. 2614 |

1 |

12-03-2004 |

12-08-2004 |

5 |

||

|

2006 |

1 |

134 |

119 Stat. 2037-2042 |

6 |

09-30-2005 |

11-18-2005 |

49 |

|

|

2 |

135 |

119 Stat. 2287 |

1 |

11-19-2005 |

12-17-2005 |

29 |

||

|

3 |

136 |

119 Stat. 2549 |

1 |

12-18-2005 |

12-31-2005 |

14 |

||

|

2007 |

1 |

137 |

120 Stat. 1311-1316 |

6 |

09-29-2006 |

11-17-2006 |

48 |

|

|

2 |

138 |

120 Stat. 2642 |

1 |

11-17-2006 |

12-08-2006 |

21 |

||

|

3 |

139 |

120 Stat. 2678 |

1 |

12-09-2006 |

02-15-2007 |

69 |

||

|

4 |

140 |

121 Stat. 8-60 |

53 |

02-15-2007 |

09-30-2007 |

227 |

||

|

2008 |

1 |

141 |

121 Stat. 989-998 |

10 |

09-29-2007 |

11-16-2007 |

47 |

|

|

2 |

142 |

121 Stat. 1341-1344 |

4 |

11-13-2007 |

12-14-2007 |

28 |

||

|

3 |

143 |

121 Stat. 1454 |

1 |

12-14-2007 |

12-21-2007 |

7 |

||

|

4 |

144 |

121 Stat. 1819 |

1 |

12-21-2007 |

12-31-2007 |

10 |

||

|

2009 |

1 |

145 |

122 Stat. 3574-3716 |

143 |

09-30-2008 |

03-06-2009 |

157 |

|

|

2 |

146 |

123 Stat. 522 |

1 |

03-06-2009 |

03-11-2009 |

5 |

||

|

2010 |

1 |

147 |

123 Stat. 2043-2053 |

11 |

10-01-2009 |

10-31-2009 |

31 |

|

|

2 |

148 |

123 Stat. 2972-2974 |

3 |

10-30-2009 |

12-18-2009 |

48 |

||

|

2011 |

1 |

149 |

124 Stat. 2607-2616 |

10 |

12-03-2010 |

64 |

||

|

2 |

150 |

124 Stat. 3063 |

1 |

12-04-2010 |

12-18-2010 |

15 |

||

|

3 |

151 |

124 Stat. 3454 |

1 |

12-18-2010 |

12-21-2010 |

3 |

||

|

4 |

152 |

124 Stat. 3518-3521 |

4 |

12-22-2010 |

03-04-2011 |

73 |

||

|

5 |

153 |

125 Stat. 6-13 |

8 |

03-02-2011 |

03-18-2011 |

14 |

||

|

6 |

154 |

125 Stat. 23-30 |

8 |

03-18-2011 |

04-08-2011 |

21 |

||

|

7 |

155 |

125 Stat. 34-35 |

2 |

04-09-2011 |

04-15-2011 |

7 |

||

|

8 |

156 |

125 Stat. 102-199 |

98 |

04-15-2011 |

09-30-2011 |

168 |

||

|

2012 |

1 |

157 |

125 Stat. 363-368 |

6 |

09-30-2011 |

10-04-2011 |

4 |

|

|

2 |

158 |

125 Stat. 386-391 |

6 |

10-05-2011 |

11-18-2011 |

45 |

||

|

3 |

159 |

125 Stat. 710 |

1 |

11-18-2011 |

12-16-2011 |

28 |

||

|

4 |

160 |

125 Stat. 769 |

1 |

12-16-2011 |

12-17-2011 |

1 |

||

|

5 |

161 |

125 Stat. 770 |

1 |

12-17-2011 |

12-23-2011 |

6 |

||

|

2013 |

1 |

162 |

126 Stat. 1313 |

12 |

09-28-2012 |

03-27-2013 |

178 |

|

|

2 |

163 |

127 Stat. 198-437 |

240 |

03-26-2013 |

09-30-2013 |

(365)s |