Commodity Futures Trading Commission: Proposed Reauthorization in the 114th Congress

The Commodity Futures Trading Commission (CFTC), created in 1974, regulates futures, most options, and swaps markets. The CFTC administers the Commodity Exchange Act (CEA; P.L. 74-765, 7 U.S.C. §1 et seq) enacted in 1936 to monitor trading in certain derivatives markets. The CEA contains a sunset provision, meaning Congress periodically reauthorizes appropriations to carry out the CEA. If an explicit authorization of appropriations for a program or activity is present—as in the CEA—and it expires, the underlying authority in the statute to administer such a program does not, however. Thus, the CFTC continues functioning and administering the CEA even if its authorization has expired—which has been the case since the last CFTC reauthorization expired on September 30, 2013. It has not been uncommon for Congress to pass CFTC reauthorization bills several years after the prior authorization had expired.

The current CFTC reauthorization process is the first since the Dodd-Frank Wall Street Reform and Consumer Protection Act of 2010 (Dodd-Frank; P.L. 111-203) brought the roughly $400 trillion U.S. swaps market under regulatory oversight. Historically, the reauthorization process has often been one of the principal vehicles for modifying the CFTC’s regulatory authority and evaluating the efficacy of its regulatory programs. The House passed a CFTC reauthorization bill, H.R. 2289, the Commodity End-User Relief Act, on June 9, 2015, by a 246 to 171 vote. The Senate Committee on Agriculture, Nutrition and Forestry marked up and ordered to be reported an identically titled bill, S. 2917, which would also reauthorize such appropriations, as well as making other changes to the CEA. The Obama Administration threatened to veto H.R. 2289, stating that the bill “ ... undermines the efficient functioning of the CFTC by imposing a number of organizational and procedural changes and would undercut efforts taken by the CFTC over the last year to address end-user concerns.” A number of the provisions in H.R. 2289 discussed in this report do not appear in S. 2917. This report examines the following selected major provisions of H.R. 2289, and S. 2917, which have generally garnered the most attention:

H.R. 2289 expands the current 5 cost-benefit analysis provisions in the CEA to 12. It adds a requirement that the CFTC conduct quantitative as well as qualitative assessments, which appears to mark a change from previous practice.

H.R. 2289 includes a provision that would extend an exemption from certain Dodd-Frank swaps trading and clearing requirements granted to nonfinancial companies so as to also include certain of their affiliates.

H.R. 2289 would modify the definition of a “financial entity,” potentially enabling a wider range of companies to claim certain exemptions from the Dodd-Frank derivatives requirements. S. 2917 takes a different approach to modifying this definition. It directs the CFTC to issue a new rule defining the term predominantly engaged in financial activities to exclude hedging transactions.

H.R. 2289 and S. 2917 would potentially broaden the bona fide hedging definition to allow anticipated, as well as current, risks to be hedged, which might increase the number of swaps that qualify as hedges. Bona fide hedging is often used to determine which swaps count toward registration requirements, position limits, large trader reporting, and other regulatory requirements. Language in the two bills on this topic is substantially the same.

H.R. 2289 mandates that, starting 18 months from enactment, the swaps regulatory requirements of the eight largest foreign swaps markets must be considered comparable to those of the United States—unless the CFTC issued a rule finding that any of those foreign jurisdictions’ requirements were not comparable to U.S. requirements.

S. 2917 and H.R. 2289 would essentially codify the deadline for a futures commission merchant (FCM) to deposit any capital to cover residual interest as no earlier than 6:00 p.m. on the following business day.

H.R. 2289 would remove a requirement in Dodd-Frank that foreign regulators indemnify a U.S.-based swap data repository for any expenses arising from litigation related to a request for market data. Indemnification generally refers to compensating someone for harm or loss.

Commodity Futures Trading Commission: Proposed Reauthorization in the 114th Congress

Jump to Main Text of Report

Contents

- Background on the CFTC

- The CFTC Reauthorization Process

- The Commodity End-User Relief Act (H.R. 2289 and S. 2917): Selected Provisions

- Cost-Benefit Analysis (H.R. 2289)

- Existing CFTC Requirements for Cost-Benefit Analysis

- Cost-Benefit Provisions in H.R. 2289

- How Valuable Is Cost-Benefit Analysis?

- Trading by Affiliates: Amendment to the "End-User" Exception (H.R. 2289)

- Background

- Analysis: Affiliate Activities Under the End-User Exception of H.R. 2289

- Which Companies Are "Financial Entities?" (H.R. 2289)

- Who Is "Predominantly Engaged" in Financial Activities? (S. 2917)

- Changes to Definition of Bona Fide Hedging (H.R. 2289, S. 2917)

- Global Cross-Border Swaps (H.R. 2289)

- Background: Cross-Border Swaps and Extra-Territoriality

- Past CFTC Action

- H.R. 2289 on Cross-Border Swaps

- Swap Data Repository Indemnifications (H.R. 2289)

- Residual Interest (H.R. 2289, S. 2917)

Summary

The Commodity Futures Trading Commission (CFTC), created in 1974, regulates futures, most options, and swaps markets. The CFTC administers the Commodity Exchange Act (CEA; P.L. 74-765, 7 U.S.C. §1 et seq) enacted in 1936 to monitor trading in certain derivatives markets. The CEA contains a sunset provision, meaning Congress periodically reauthorizes appropriations to carry out the CEA. If an explicit authorization of appropriations for a program or activity is present—as in the CEA—and it expires, the underlying authority in the statute to administer such a program does not, however. Thus, the CFTC continues functioning and administering the CEA even if its authorization has expired—which has been the case since the last CFTC reauthorization expired on September 30, 2013. It has not been uncommon for Congress to pass CFTC reauthorization bills several years after the prior authorization had expired.

The current CFTC reauthorization process is the first since the Dodd-Frank Wall Street Reform and Consumer Protection Act of 2010 (Dodd-Frank; P.L. 111-203) brought the roughly $400 trillion U.S. swaps market under regulatory oversight. Historically, the reauthorization process has often been one of the principal vehicles for modifying the CFTC's regulatory authority and evaluating the efficacy of its regulatory programs. The House passed a CFTC reauthorization bill, H.R. 2289, the Commodity End-User Relief Act, on June 9, 2015, by a 246 to 171 vote. The Senate Committee on Agriculture, Nutrition and Forestry marked up and ordered to be reported an identically titled bill, S. 2917, which would also reauthorize such appropriations, as well as making other changes to the CEA. The Obama Administration threatened to veto H.R. 2289, stating that the bill " ... undermines the efficient functioning of the CFTC by imposing a number of organizational and procedural changes and would undercut efforts taken by the CFTC over the last year to address end-user concerns." A number of the provisions in H.R. 2289 discussed in this report do not appear in S. 2917. This report examines the following selected major provisions of H.R. 2289, and S. 2917, which have generally garnered the most attention:

- H.R. 2289 expands the current 5 cost-benefit analysis provisions in the CEA to 12. It adds a requirement that the CFTC conduct quantitative as well as qualitative assessments, which appears to mark a change from previous practice.

- H.R. 2289 includes a provision that would extend an exemption from certain Dodd-Frank swaps trading and clearing requirements granted to nonfinancial companies so as to also include certain of their affiliates.

- H.R. 2289 would modify the definition of a "financial entity," potentially enabling a wider range of companies to claim certain exemptions from the Dodd-Frank derivatives requirements. S. 2917 takes a different approach to modifying this definition. It directs the CFTC to issue a new rule defining the term predominantly engaged in financial activities to exclude hedging transactions.

- H.R. 2289 and S. 2917 would potentially broaden the bona fide hedging definition to allow anticipated, as well as current, risks to be hedged, which might increase the number of swaps that qualify as hedges. Bona fide hedging is often used to determine which swaps count toward registration requirements, position limits, large trader reporting, and other regulatory requirements. Language in the two bills on this topic is substantially the same.

- H.R. 2289 mandates that, starting 18 months from enactment, the swaps regulatory requirements of the eight largest foreign swaps markets must be considered comparable to those of the United States—unless the CFTC issued a rule finding that any of those foreign jurisdictions' requirements were not comparable to U.S. requirements.

- S. 2917 and H.R. 2289 would essentially codify the deadline for a futures commission merchant (FCM) to deposit any capital to cover residual interest as no earlier than 6:00 p.m. on the following business day.

- H.R. 2289 would remove a requirement in Dodd-Frank that foreign regulators indemnify a U.S.-based swap data repository for any expenses arising from litigation related to a request for market data. Indemnification generally refers to compensating someone for harm or loss.

Background on the CFTC

The Commodity Futures Trading Commission (CFTC) was created in 1974 through enactment of the Commodity Futures Trading Commission Act1 to regulate commodities futures and options markets. At the time these markets were poised to expand beyond their traditional base in agricultural commodities to encompass contracts based on financial variables, such as interest rates and stock indexes.2 The CFTC's mission is to prevent excessive speculation, manipulation of commodity prices, and fraud. The agency administers the Commodity Exchange Act (CEA),3 which was passed in 1936. Prior to the CFTC's creation, trading in agricultural commodities regulated by the CEA was overseen by the Commodity Exchange Administration, an office within the U.S. Department of Agriculture which was also formed in 1936.

The CFTC oversees industry self-regulatory organizations (SROs)—such as the futures exchanges and the National Futures Association—and requires the registration of a range of industry firms and personnel, including futures commission merchants (or brokers), floor traders, commodity pool operators, and commodity trading advisers. The Dodd-Frank Wall Street Reform and Consumer Protection Act of 2010 (Dodd-Frank)4 significantly expanded the CFTC's jurisdiction to include over-the-counter (OTC) derivatives, also called swaps.5 As a result of Dodd-Frank, major participants in the swaps markets must register with the CFTC, and certain swaps must be cleared by clearinghouses and traded on electronic trading platforms similar to exchanges.6 Newly regulated swap market participants include swap dealers, major swap participants, swap clearing organizations, swap execution facilities, and swap data repositories. These entities are subject to new business conduct standards contained in the statute or promulgated as CFTC rules. Like the Securities and Exchange Commission (SEC), the CFTC does not generally regulate the safety and soundness of individual firms, with the exception of newly regulated swap dealers and major swap participants, for whom it will set capital standards pursuant to Dodd-Frank.

Although most derivatives trading in today's market relates to financial variables (e.g., interest rates, currency prices, and stock indexes), congressional oversight remains vested in the House and Senate Agriculture Committees in part because of the market's historical origins in agricultural commerce. Appropriations for the CFTC are under the jurisdiction of the Agriculture Appropriations Subcommittee in the House and the Financial Services and General Government Appropriations Subcommittee in the Senate.

To meet additional responsibilities for oversight of swaps, the Obama Administration has requested additional funding for the CFTC since FY2011, when the CFTC's budget was $202 million. For FY2016, the CFTC requested a budget of $322 million, and a staff of 895 full-time equivalent employees (FTEs).7 This represented an increase of $72 million (or 29%) and 149 FTEs over the FY2015 enacted appropriations amount of $250 million for the CFTC.8 The actual amount appropriated for FY2016 in P.L. 114-113 was $250 million.

For FY2017, the CFTC requested $330 million and a staff of 897 FTEs.9 This would represent an increase of $80 million or 32% over the enacted FY2016 amount. Of the requested $80 million increase, the CFTC has targeted 36% of the amount toward information technology investments, and the remaining 64% toward an increase in staffing and related support, particularly in areas such as surveillance, enforcement, economic and legal analysis, and examinations.10 The President's budget request stated that "this increase is necessary because the Commission has not received budgetary increases sufficient enough to allow full implementation of its responsibilities, which have expanded greatly due to changes and growth in the markets and the enactment of the Dodd-Frank Act as well as growth in the markets."11

The House-reported Agriculture appropriations bill for FY2017 (H.R. 5054) would provide $250 million, constant with the FY2016 enacted amount. The Senate-reported Financial Services appropriations bill (S. 3067) would provide this same amount. The Financial Services Appropriations Act is expected to carry the FY2017 CFTC appropriation, according to the alternating placement with the Agriculture Appropriations Act in recent years.

Organizationally, the CFTC is led by five commissioners appointed by the President, with the advice and consent of the Senate, to serve staggered five-year terms. No more than three commissioners at any one time may be from the same political party. The President designates one commissioner to serve as chair. The agency is organized around four divisions:12

- Clearing and Risk, which oversees derivatives clearing organizations and other major market participants;

- Enforcement, which investigates and prosecutes alleged violations of the CEA and CFTC regulations;

- Market Oversight, which conducts trade surveillance and oversees trading facilities, such as futures exchanges and swap execution facilities, and swap data repositories; and

- Swap Dealer and Intermediary Oversight, which oversees registration and compliance by SROs, such as the futures exchanges (e.g., the Chicago Mercantile Exchange), the National Futures Association, and the registration of swap dealers and major swap participants.

The CFTC Reauthorization Process

The CEA, the statute governing futures and swaps markets in which the CFTC administers, contains a sunset provision. This means Congress must periodically reauthorize appropriations to carry out the CEA.13 However, if an explicit authorization of appropriations for a program or activity is present—as in the CEA—and it expires, the underlying authority in the statute to administer such a program or engage in such an activity does not.14 In other words, the CFTC continues functioning and administering the CEA even if its authorization has expired—which has been the case since the last CFTC reauthorization expired on September 30, 2013. It has not been uncommon for Congress to pass CFTC reauthorization bills several years after the prior authorization had expired.15

The 114th Congress is considering new CFTC reauthorization bills. Historically, the reauthorization process has often been one of the principal vehicles for modifying the CFTC's regulatory authority and evaluating the efficacy of its regulatory programs. Congress often uses the reauthorization process as a vehicle to consider a wide range of issues related to the regulation of derivatives trading.

The current CFTC reauthorization process is the first since the Dodd-Frank Act's passage brought the more than $400 trillion U.S. swaps market16 under regulatory oversight.17 For some in Congress, it may be an opportunity to reexamine provisions of Dodd-Frank they feel may have created excessive regulatory burdens or industry costs. Others have been critical of any perceived weakening of derivatives oversight introduced in the wake of the financial crisis. Still others may be using the current CFTC reauthorization process to try to make changes to futures regulation that industry, or regulators themselves, have long sought.

In the 114th Congress, the House passed H.R. 2289,18 the Commodity End-User Relief Act, on June 9, 2015, by a vote of 246 to 171. Among other changes to the CEA, H.R. 2289 as passed would reauthorize appropriations for the CFTC. The bill was referred to the Senate Committee on Agriculture, Nutrition, and Forestry on June 10, 2015. The Obama Administration threatened to veto H.R. 2289, stating that the bill "undermines the efficient functioning of the CFTC by imposing a number of organizational and procedural changes and would undercut efforts taken by the CFTC over the last year to address end-user concerns."19 On April 14, 2016, the Senate Committee on Agriculture, Nutrition, and Forestry marked up and ordered to be reported a CFTC reauthorization bill, S. 2917. On May 10, 2016, S. 2917 was reported to the Senate without written report and placed on the Senate legislative calendar under general orders.

Among its other changes, H.R. 2289 as passed, and S. 2917, would amend the short Authorization of Appropriations section in the CEA (7 U.S.C. §16(d)). The section currently authorizes the appropriation of "such sums as are necessary to carry out" the chapter of the CEA "through 2013," and H.R. 2289 as passed, and S. 2917, would both amend it to read "through 2019."20

The Commodity End-User Relief Act (H.R. 2289 and S. 2917): Selected Provisions

The next sections examine more closely selected major provisions of the House CFTC reauthorization bill, H.R. 2289, and S. 2917 (each titled The Commodity End-User Relief Act), which have generally been the most actively debated—beginning with the bills' changes to required cost-benefit analysis in CFTC regulatory actions.21

Cost-Benefit Analysis (H.R. 2289)

This section analyzes the provision in H.R. 2289 that would expand the number of factors for the CFTC to consider in cost-benefit analysis, and include the need for quantitative as well as qualitative analysis, among other changes. It first examines the existing requirements for the CFTC to conduct cost-benefit analysis; then the changes in H.R. 2289; and then the academic research on how valuable cost-benefit analysis may be. S. 2917 does not have a similar provision on cost-benefit analysis.

Existing CFTC Requirements for Cost-Benefit Analysis

The CFTC already has certain requirements to perform cost-benefit analysis in its rulemakings under the CEA. The CFTC and other independent regulatory agencies22 (such as the SEC) are not subject to the general requirements that apply to other government agencies to conduct cost-benefit analysis under Executive Order 12866.23

For the CFTC, Section 15(a) of the CEA requires that "before promulgating a regulation under this chapter or issuing an order (except as provided in paragraph (3)), the Commission shall consider the costs and benefits of the action of the Commission."24 In addition,

the costs and benefits of the proposed Commission action shall be evaluated in light of:

(A) considerations of protection of market participants and the public;

(B) considerations of the efficiency, competitiveness, and financial integrity of futures markets;

(C) considerations of price discovery;

(D) considerations of sound risk management practices; and

(E) other public interest considerations.25

The CFTC also may have additional required considerations when issuing a particular rule. Section 15(a) of the CEA applies more broadly than E.O. 12866, which applies only to rules deemed to reach a certain "significance" threshold—Section 15(a) applies to all rules issued by the CFTC.

In practice, the CFTC relies on guidance provided by the Office of Management and Budget's (OMB's) Office of Information and Regulatory Affairs (OIRA) when considering costs and benefits under Section 15(a) of the CEA, although it is not required to do so. This practice is documented in a May 2012 Memorandum of Understanding (MOU) between OIRA and CFTC regarding implementation of the Dodd-Frank Act.26 OIRA has issued a variety of documents to assist agencies in conducting their cost-benefit analyses, including OMB Circular A-4 and accompanying guidance documents. Thus, while the CFTC is not subject to the executive order's requirements, the CFTC's analyses conducted pursuant to the CEA likely share some similarities with analyses that are completed pursuant to the executive order.27

Cost-Benefit Provisions in H.R. 2289

Section 202 of H.R. 2289 expands the CEA's current 5 cost-benefit analysis provisions listed above to 12 considerations. Some of the considerations are similar to requirements other agencies are subject to under E.O. 12866, and some are currently in Section 15(a) of the CEA.

H.R. 2289 includes the following factors:

(A) considerations of protection of market participants and the public;

(B) considerations of the efficiency, competitiveness, and financial integrity of futures and swaps markets;

(C) considerations of the impact on market liquidity in the futures and swaps markets;

(D) considerations of price discovery;

(E) considerations of sound risk-management practices;

(F) available alternatives to direct regulation;

(G) the degree and nature of the risks posed by various activities within the scope of its jurisdiction;

(H) the costs of complying with the proposed regulation or order by all regulated entities, including a methodology for quantifying the costs (recognizing that some costs are difficult to quantify);

(I) whether the proposed regulation or order is inconsistent, incompatible, or duplicative of other federal regulations or orders;

(J) the cost to the Commission of implementing the proposed regulation or order by the Commission staff, including a methodology for quantifying the costs;

(K) whether, in choosing among alternative regulatory approaches, those approaches maximize net benefits (including potential economic and other benefits, distributive impacts, and equity); and

(L) other public interest considerations.

Arguably, at least some of these considerations, such as liquidity and market efficiency, incorporate the existing statutory mission of the CFTC.

In addition, Section 202 adds a requirement that the CFTC conduct quantitative as well as qualitative assessments of costs and benefits.28 The requirement for quantitative cost-benefit analysis appears to mark a change from previous practice.29 It also raises the question of how accurately one may quantify benefits involving economic externalities. In economics, an externality refers to a consequence of an economic activity that is experienced by unrelated third parties; it can be either positive or negative. Pollution is often used as an example of a negative externality, in which the effects may be widely dissipated and hard to quantify. Risks to the financial system could be another example of a negative externality.

Quantifications of such externalities may involve judgments or estimates as to the value of intangible or speculative benefits that might be experienced differently by individuals, such as the value of financial stability, or, in the case of pollution, the value of avoiding certain diseases.30 In the realm of financial regulation, benefits are often widely dissipated (for instance, prospective investors broadly benefit from fuller and more accurate corporate disclosures and related investor protections), and are sometimes speculative (e.g., trying to measure the benefit of avoiding potential financial fraud). This, according to critics, can make benefits harder to reliably quantify. Costs of compliance, meanwhile, may be more easily measurable (e.g., through payment-hours for accountants, lawyers, and staff).31

How Valuable Is Cost-Benefit Analysis?

Proponents of cost-benefit analysis argue that it can force agencies to focus on and clarify the benefits of their proposed rulemakings and better weigh the costs they will impose against those benefits.32 According to this line of reasoning, by putting cost-benefit requirements in statute, such as those in the CEA and those proposed in H.R. 2289, Congress can have some influence over the considerations and outcomes in agency rulemakings.33

By contrast, some administrative law scholars have argued that the increased use of cost-benefit analysis has "ossified" the rulemaking process, slowing down the process or causing agencies to issue guidance documents rather than regulations, thereby avoiding rulemaking requirements altogether.34 Some academics argue that, particularly for financial rulemakings, costs can be easier to quantify than widely dispersed potential benefits (such as "a safer financial system" or "better investor disclosure"), and that this may lead to an overstatement of costs over benefits.35 Finally, critics argue that the practice opens the agency's rules to court challenges by industry groups on the grounds of inadequate cost-benefit analysis, tying up agency resources and at times leading to the invalidation of regulations.36

Trading by Affiliates: Amendment to the "End-User" Exception (H.R. 2289)37

Background

Sections 301 and 306 of H.R. 2289, taken together, would expand the exception from certain Dodd-Frank swaps trading and clearing requirements granted to nonfinancial companies. Under current language, the Dodd-Frank Act requires many swaps deals to be cleared through a clearinghouse and traded on an electronic exchange.38 But it provides an exception from these two requirements to nonfinancial firms when certain conditions are met. The exception is commonly referred to as the end-user exception.

Section 723 of Dodd-Frank states that the clearing and exchange-trading requirements shall not apply to the swap if one of the counterparties to the swap is "not a financial entity" and is using the swap to hedge or mitigate commercial risk.39 The exception applies to affiliates of non-financial entities when those affiliates are using the swap to hedge or mitigate the commercial risk of the non-financial entity. H.R. 2289 would expand the exception by amending the definition of financial entities ineligible to use the exception and by expanding the types of activities in which eligible affiliates may engage while using the exception. S. 2917 does not contain a provision involving trading by affiliates.

Who Is an Eligible Affiliate?

As noted above, the Dodd-Frank Act requires many swap transactions to be cleared and traded on exchanges, but provides an exception for swaps and security-based swaps. The exception applies when one of the parties to the transaction is not a financial entity, is using swaps to hedge or mitigate commercial risk, and properly notifies the CFTC regarding how it meets its financial obligations.40 The exception is commonly referred to as the end-user exception. The statute currently allows affiliates of end-users to use the exception, but only "if the affiliate, acting on behalf of the person and as an agent, uses the swap to hedge or mitigate the commercial risk of the person or other affiliate of the person that is not a financial entity."41

Without further definition, the term "affiliated companies" can loosely refer to companies that are related to each other in some way, including foreign affiliates. However, the Dodd-Frank Act does provide that an affiliate cannot use the exception if the affiliate is a swap dealer; a security-based swap dealer; a major swap participant; a major security-based swap participant; a hedge fund; a commodity pool; or a bank holding company with more than $50 billion in consolidated assets.42

Proponents of a broader exception have argued that the hedging activities of corporate treasury units of non-financial parent companies could potentially be disqualified from using the exception.43 Treasury units aggregate similar risks within various parts of a parent company, and often consolidate the mitigation of those risks by engaging in one swap transaction that covers it all. Treasury units may serve other financial functions for an overall non-financial parent company as well.44

Under current statutory language, treasury units could engage in swaps activity with non-financial affiliates without clearing the swap because the affiliate itself could use the end-user exception. The treasury unit could also engage in an uncleared swap with another financial entity if it did so acting on behalf of a non-financial entity and as its agent. However, treasury units often hedge risks with other financial entities on their own behalf, as a result of the risks they have aggregated from the non-financial entities within the parent company. Consequently, these entities may not be able to use the "affiliate" end-user exception, and they may not be able to use the end user exception in their own right because they "predominantly engage in activities that are in the business of banking" which makes them "financial entities" that cannot use the exception. Any inability of treasury affiliates of non-financial entities to use the end-user exception would make it more expensive for their parent corporation to hedge risks using derivatives.45

Policy Issues and CFTC Actions

A key question for policymakers in deciding whether to extend any exception for affiliates is: how widely? Would risks be posed to the financial system or to parent companies if the exception from derivatives clearing and exchange-trading requirements were extended to non-financial affiliates of financial companies? And under what circumstances should such exception be extended to financial affiliates of non-financial companies to minimize such risks?

The CFTC, in its 2012 final rule on the end-user exception, addressed some of the questions involved in deciding which entities to appropriately exclude from the end-user exception, as financial entities.46 The CFTC found that treasury units that operate as separate legal entities and whose primary function is financial in nature would be precluded from the "end user" exception, but treasury units housed within a non-financial corporation, and in which the non-financial company enters into the swaps in its own name, could be eligible to use the end user exception.47 The CFTC also noted that some commenters had argued that the end-user exception "should be narrowly tailored to businesses that produce, refine, process, market, or consume underlying commodities and to counterparties transacting with non-financial counterparties";48 and that a number of form letters had argued that extending the end user exception to certain financial entities could increase systemic financial risks from derivatives trading.49

More questions regarding the proper application of the end-user exception to treasury affiliates continued to arise, however, and in 2014, the CFTC attempted to address them. The CFTC indicated that it would not bring enforcement actions against certain treasury affiliates in its November 26, 2014, no-action letter on centralized treasury units.50 The CFTC defines an "eligible treasury affiliate"—which would qualify for the enforcement forbearance—as entities meeting each of six conditions. The conditions include, among other things, that the affiliate is neither affiliated with nor is itself a swap dealer or a major swap participant. The CFTC also requires that the affiliate's "ultimate parent" is not a financial entity (and defines this as the topmost, direct or indirect, majority owner of the entity).51

Some industry participants have not been satisfied by the "no-action" letter, however.52 Treasury affiliates that rely on the no-action letter for swaps which they neither clear, nor execute on an exchange, are technically in violation of the Dodd-Frank Act's clearing requirement as interpreted by the CFTC. The CFTC's No-action Letter (NAL), while it assures those that qualify to rely on it that they will not face an enforcement action for violating the clearing and exchange trading requirements, does not actually change the statute. Consequently, proponents of the language in Section 301 have argued that a statutory amendment is necessary to provide clarity and certainty to end-users that use treasury affiliates to hedge their commercial risk.53 Sections 301 and 306 of H.R. 2289 appear to attempt to address those concerns, though they may expand the exception beyond those entities covered by the CFTC's NAL as well.

Broader Issues and H.R. 2289

At issue for Congress in deciding whether to expand the existing exception is whether derivatives trading between affiliates within the same umbrella organization could pose substantial risk of losses to either the affiliate or the parent, or spread losses outside the organization. Various questions for policymakers to consider include the following:

- Might one affiliate have an incentive to gain through a swaps trade at another affiliate's expense?

- What repercussions could this have within the conglomerate?

- What would be the best way to control risks of excessive losses by a single affiliate from such trades?

- Is any proposed legislative exemption tailored narrowly enough to meet concerns from regulators that large swap market players might funnel swaps through an affiliate to avoid U.S. derivatives requirements?

- Would a legislative provision allow overseas affiliates to use this exception, and if so, what would be the cross-border regulatory implications?

Proponents of the provision in H.R. 2289 argue that it would prevent the redundant regulation of inter-affiliate transactions and prevent capital from being tied up unnecessarily, such as through the duplicative posting of margin for derivatives trades.54 The expansion of the exception, they argue, would allow businesses that centralize their hedging activities to reduce costs, simplify financial dealings, and reduce their counterparty credit risk. Proponents contend that the provision would allow affiliates—such as centralized treasury units—within a corporate entity to trade swaps under the end-user exception to the clearing and exchange-trading requirements both within and outside the umbrella organization.55

Opponents of the provision in H.R. 2289 argue that it would allow financial firms with commercial business affiliates to "take advantage of exemptions from key Dodd-Frank risk controls that were meant to apply only to commercial end users."56 Opponents of widening the exception as it applies to affiliates from the Dodd-Frank requirements have also stated that "the potential for affiliates to cause massive losses to their parent companies cannot be denied."57 They cite examples such as the derivatives losses incurred by the large insurance conglomerate American International Group Inc.'s (AIG's) overseas affiliate in London and derivatives losses incurred by J.P. Morgan's so-called London Whale trading losses in its London affiliate. They argue that any expansions of the exception should be restricted only to 100%-owned subsidiaries of a parent company, and be subject to strict risk management controls.58

Analysis: Affiliate Activities Under the End-User Exception of H.R. 2289

Section 301 of H.R. 2289 seemingly would expand the hedging activities in which affiliates of non-financial entities could engage while being able to use the end-user exception. Under current statutory language, affiliates may use the end-user exception "only if the affiliate, acting on behalf of the [non-financial entity] and as an agent, uses the swap to hedge or mitigate the commercial risk of the person or other affiliate."59

Section 301 would expand that language by allowing affiliates to engage in more hedging activities while using the exception. Specifically, Section 301 would permit affiliates to use the end-user exception "only if the affiliate enters into the swap to hedge or mitigate the commercial risk of the person or other affiliate of the person that is not a financial entity, provided that if the hedge or mitigation of such commercial risk is addressed by entering into a swap with a swap dealer or major swap participant, an appropriate credit support measure or other mechanism must be utilized."60 Removing the requirement that the affiliate act on behalf of the non-financial entity and as an agent could permit the affiliate to act in its own capacity as an independent entity while hedging the commercial risk of the non-financial entity.

As noted above, affiliates of end users cannot use the end-user exception if they are swap dealers, security-based swap dealers, major swap participants (MSPs), major security-based swap participants, hedge funds, commodity pool operators (CPOs), or large bank holding companies (BHCs) with more than $50 billion in assets. This portion of the statute appears to prevent large BHCs, swap dealers, MSPs, hedge funds, and CPOs affiliated with a non-financial firm from using the end-user exception even if H.R. 2289 became law.61 However, barring further action from the regulators, this part of the statute would not appear to prevent affiliated financial firms with less than $50 billion in assets, or who did not otherwise fall into these categories, from using this end-user exemption from the derivatives requirements.

Section 301 does not apparently restrict with whom the affiliate trades. It states only that the affiliate of the nonfinancial firm or end user may qualify for the end-user exception itself "only if the affiliate enters into the swap to hedge or mitigate the commercial risk of the person or other affiliate of the person that is not a financial entity." H.R. 2289 does not specify that such trades must occur within an umbrella organization.

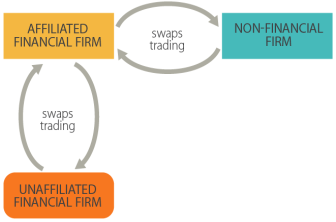

|

|

Source: Congressional Research Service. |

The hypothetical scenario in Figure 1 illustrates the issues: If a nonfinancial firm, such as an energy or metals business, had an affiliate that was a financial firm, could that financial firm engage in swaps trading with an unaffiliated large financial firm and still use the end-user exception under Section 301? While no restriction appears in Section 301 to prevent this scenario so long as the financial affiliate engaged in the swap "to hedge or mitigate the commercial risk of the person or other affiliate of the person that is not a financial entity," the prohibition on certain affiliates in Section 723 of Dodd-Frank would appear to preclude affiliates that were large banks with more than $50 billion in assets, or were swap dealers or MSPs, hedge funds,62 or commodity pool operators (CPOs), from using the end-user exemption as an affiliate even if H.R. 2289 passed. Financial firms with fewer assets (and that are not swap dealers, MSPs, hedge funds, or CPOs), however, would not appear to be prohibited from using the exception, so long as the standard for hedging or mitigating the commercial risk of the non-financial affiliate was met.

Which Companies Are "Financial Entities?" (H.R. 2289)

Section 306 of H.R. 2289 as passed by the House would modify the definition of a financial entity, potentially enabling a wider range of companies to claim the end-user exception to the clearing requirement in the Dodd-Frank Act. As discussed above, the end-user exception is limited to a company that "is not a financial entity,"63 as the term financial entity is defined by H.R. 2289. Section 306 of H.R. 2289 would potentially allow certain nonbank financial entities to use the end-user exception even when trading on behalf of another financial entity, so long as neither entity has a prudential regulator.

Section 306 would exclude from the definition of financial entity one "who is not supervised by a prudential regulator, and is not described in any of subclauses (I) through (VII)64 ... and is a commercial market participant, or enters into swaps, contracts for future delivery, and other derivatives on behalf of, or to hedge or mitigate the commercial risk of, whether directly or in the aggregate, affiliates that are not so supervised or described."65 Section 306 would define a commercial market participant as "any producer, processor, merchant, or commercial user of an exempt or agricultural commodity, or the products or byproducts of such a commodity."66

Under this language, entities that are not supervised by a prudential regulator and are not swap dealers, MSPs, hedge funds, large banks, or other enumerated financial entities that enter into swaps to hedge the commercial risk of other affiliates that also are not supervised by a prudential regulator and are not among the types of entities listed in subclauses I-VII of the Commodity Exchange Act (Section 2(h)(7)(C)) are not considered financial entities for the purposes of qualifying for the end-user exception. If these entities are not financial entities, then they may use the end-user exception in their own right and need not meet the affiliate requirements of Section 723 of the Dodd-Frank Act, as it would be amended by Section 301 of H.R. 2289. To use the clearing and exchange-trading exceptions, these entities would only need to use the swaps to hedge or mitigate commercial risk of other qualifying nonfinancial entities and to notify the CFTC in accordance with agency regulations.

H.R. 2289 would create a broader, statutory exception from the Dodd-Frank clearing and exchange-trading requirements. It potentially would allow certain nonbank financial entities that do not have banking regulators to be eligible for the exception if these entities could show that they were "commercial market participants" or that they met the requirements for trading on behalf of other non-prudentially supervised affiliates. The bill leaves to the CFTC to further clarify who would be a commercial market participant and to determine which types of nonbank financial firms would qualify for the end-user exception. S. 2917 takes a different approach to modifying the definition of a financial entity. This approach is discussed below.

Who Is "Predominantly Engaged" in Financial Activities? (S. 2917)

Section 206 of S. 2917 addresses the question of what it means, for the purposes of the Commodity Exchange Act section discussed above67 to be "predominantly engaged" in financial activities. This question is relevant for determining the scope of the end-user exception to the clearing requirement set out in the Dodd-Frank Act. Unlike H.R. 2289, S. 2917 does not delete any of the eight prongs in Section 2(h)(7)(C) of the CEA, which controls the entities considered financial entities.

Instead, S. 2917 adds a requirement at the end of Section 2(h)(7)(C) directing the CFTC to issue a new rule defining the term predominantly engaged in financial activities. S. 2917 also requires that, in its new rule, the CFTC must not consider an entity to be predominantly engaged in financial activities if the consolidated revenue derived from such activities constitutes less than 85% of the entity's total consolidated revenue. In addition, S. 2917 adds a requirement that, for the purpose of the new CFTC rule, all revenue that results from "transactions used to hedge or mitigate commercial risk shall be excluded" from the 85% threshold calculation.

Changes to Definition of Bona Fide Hedging (H.R. 2289, S. 2917)

Section 313 of H.R. 2289 as passed by the House and Section 306 of S. 2917 would make changes to the definition of bona fide hedging in the CEA.68 Language in the two bills on this topic is substantially the same. The concept of bona fide hedging refers to transactions that in some way genuinely offset commercial risks. The CFTC relies on its established rules and guidance on what constitutes a bona fide hedge to help determine which types of swaps count toward the requirement to register as a swap dealer or MSP. The agency also uses the concept to determine which derivatives count toward limits on position size, referred to as position limits, and, similarly, which transactions count toward large trader reporting.69

Large trader reporting requirements refer to a system the CFTC uses to monitor how large any one trading party's position size is. The broad purpose of this system is to ensure that no one entity wields excessive market power.70 The CFTC has the discretion to raise or lower the large trader reporting levels in specific markets to strike a balance between collecting sufficient information to oversee the markets and minimizing the reporting burden on market participants.71 Similarly, a position limit broadly refers to the maximum position in any one type of future, option, or swap for one commodity that may be held or controlled by one person.72

The current definition of a bona fide hedge in the CEA specifies, among other factors, that

(2) For the purposes of implementation of subsection (a)(2) for contracts of sale for future delivery or options on the contracts or commodities, the Commission shall define what constitutes a bona fide hedging transaction or position as a transaction or position that—

(A) (i) represents a substitute for transactions made or to be made or positions taken or to be taken at a later time in a physical marketing channel;

(ii) is economically appropriate to the reduction of risks in the conduct and management of a commercial enterprise; and... 73

Among other changes, H.R. 2289's Section 313 and S. 2917 would change (A)(ii) above so as to read:

(ii) is economically appropriate to the reduction or management of current or anticipated risks in the conduct and management of a commercial enterprise; and... [emphasis added].

This change could potentially broaden the bona fide hedging definition so as to allow anticipated, as well as current, risks. In addition, it could potentially allow trades that were needed not only to reduce risks but also simply to manage risks. This change could potentially enable many more types of trades to be permitted under this bona fide hedging definition, in which case more swap trades potentially would not count toward the registration requirements or restrictions on position size.

Global Cross-Border Swaps (H.R. 2289)

Background: Cross-Border Swaps and Extra-Territoriality

The topic of cross-border swaps broadly relates to the question of to what degree did Congress intend, and did the Dodd-Frank Act authorize, the CFTC to regulate swaps that may extend beyond U.S. borders or be transacted between U.S. and non-U.S. persons? Because the swaps market is international in nature, with considerable cross-border trading, this question is material. Section 722(d) of the Dodd-Frank Act stated that swaps reforms shall not apply to activities outside the United States unless the activities have "a direct and significant connection with activities in, or effect on, commerce of the United States."

This mandate left much discretion to the CFTC as to how to interpret it. Former CFTC Chair Gary Gensler, under whom the CFTC first issued rules and interpretations implementing Section 722, stated that "Failing to bring swaps market reform to transactions with overseas branches and overseas affiliates guaranteed by U.S. entities would mean American jobs and markets would likely move offshore, but, particularly in times of crisis, risk would come crashing back to our economy." Gensler and others have noted that derivatives trading by overseas affiliates of U.S. financial conglomerates can and has resulted in significant losses to U.S.-based entities. They cite examples such as AIG's London-based Financial Products Group, which sold credit default swap derivatives related to mortgage-backed securities that incurred losses during the financial crisis, or the more recent J.P. Morgan "London Whale" derivatives trading losses of roughly $6 billion.74

By contrast, industry participants have warned that if CFTC rules were too burdensome or out of sync with other countries'—putting in place requirements that other jurisdictions lacked—then "swap business will migrate, in the short term, away from U.S. financial institutions to other jurisdictions that are putting in place similar regulatory reform initiatives but are not as far advanced in doing so as the United States"—and have warned that, once gone, such business would be unlikely to return to U.S. companies.75

Past CFTC Action

The CFTC issued proposed guidance76 on the cross-border application of Title VII of Dodd-Frank. In it, the agency sought to clarify who would count as a "U.S. person" for the purposes of meeting the requirements of Dodd-Frank, such as the clearing requirement for swaps, among other questions. Subsequently, on December 21, 2012, the agency issued a temporary exemption, extending the deadline for meeting all the requirements for cross-border swaps, while it continued to try to work with foreign regulators to create a more uniform system of requirements.77 Then, on May 1, 2013, the SEC proposed a rule and interpretive guidance on cross-border security-based swaps—swaps related to a security, such as an equity—which the SEC regulates. The SEC's proposed rule has been widely interpreted as taking a narrower approach to defining who is a U.S. person than did the CFTC—and thus restricting the reach of Dodd-Frank requirements on security-based swaps to fewer overseas transactions or entities.78

The CFTC issued its final guidance on July 26, 2013, setting out the scope of the term U.S. person, the general framework for determining which entities had to register as swap dealers and major swap participants (MSPs), and which swaps involving non-U.S. persons who were guaranteed by U.S. persons were subject to U.S. requirements.79 On November 14, 2013, the CFTC issued a staff advisory80 aimed at determining when to apply U.S.-derivatives requirements to trades that were booked in an offshore affiliate, but in which the non-U.S. affiliate used U.S. personnel to arrange, negotiate, or execute the swap.

The CFTC continues to issue rules aimed at clarifying how to apply Dodd-Frank derivatives requirements to cross-border trades. Other issues that have arisen more recently include the need for U.S. and foreign regulators to recognize one another's derivatives clearinghouses, trading exchanges, and data repositories for reporting trades as "equivalent," so that one trade spanning multiple jurisdictions need only be cleared, traded, and reported one time. This has proven challenging, as, among other things, the European Union has thus far not granted such an "equivalence" determination to U.S. clearinghouses and trading facilities.81

H.R. 2289 on Cross-Border Swaps

Section 314 of H.R. 2289 bears some similarities to H.R. 1256 in the 113th Congress.82 H.R. 2289 drops the earlier bill's requirement that the CFTC and SEC must jointly issue a cross-border rule. But, similarly to H.R. 1256, the current bill mandates that, starting 18 months from its enactment, the swaps regulatory requirements of the eight largest foreign swaps markets83 must be considered comparable to those of the United States—unless the CFTC issues a rule or order finding that any of those foreign jurisdictions' requirements are not comparable to or as comprehensive as those of the United States.84

It is not, however, immediately straightforward to list who those eight largest jurisdictions would be. For one thing, it would depend on how regulators treated the member countries of the European Union, for purposes of the statute. For another, the total notional value of swaps traded in a jurisdiction fluctuates over time, so how the 12-month period was drawn would likely impact the results. Further, regulators would have to determine "where" a swap is traded—that is, in whose jurisdiction it would fall—when a large portion of the market is considered "cross-border" in nature. This is essentially the same problem U.S. regulators are already facing in deciding when a swap qualifies as a "U.S. transaction."

Under H.R. 2289, if the CFTC were not to make such a determination (of non-comparability), then "a non-United States person or a transaction between two non-United States persons shall be exempt from United States swaps requirements" as long as they are in compliance with any of the eight permitted foreign jurisdictions.85 Effectively, the bill appears to substitute as a default, for trades that involved a non-U.S. person, the swaps requirements of the eight largest foreign swaps markets (which would encompass most of the world of swaps trading, particularly if countries in the European Union were treated as one swaps jurisdiction) for U.S. requirements—unless the CFTC found a foreign jurisdiction to be lacking.

One question that would presumably be left to the CFTC to determine in a rulemaking would be how widely to apply this provision to "a non-United States person or a transaction between two non-United States persons," were the provision enacted. For instance, would any swap in which a non-U.S. person were at least one counterparty potentially be encompassed? If so, that would potentially encompass a large majority of swaps, the bulk of which appear to be transacted in some way between a U.S. and non-U.S. person.86 It would presumably be left to the regulator to interpret and clarify its application.

Section 314 also includes a definition of a U.S. person, which, among other factors, includes "any other person as the Commission may further define to more effectively carry out the purposes of this section"—thereby apparently giving the CFTC some leeway.87 However, Section 314 also specifies that, in developing its cross-border rules, the CFTC "shall not take into account, for the purposes of determining the applicability of United States swaps requirements, the location of personnel that arrange, negotiate, or execute swaps."88 This requirement drew some criticism in congressional debate over the bill.89

The provision would appear to overturn CFTC Advisory 13-69,90 which had drawn much industry opposition.91 The advisory was aimed at resolving questions regarding the precise conditions in which swaps between U.S. and non-U.S. persons would be subject to Dodd-Frank requirements. The advisory, which technically represented the opinion of only one division of the CFTC, held that the Dodd-Frank requirements would apply to a swap between a non-U.S. swap dealer—even if it were an affiliate of a U.S. swap dealer—and a non-U.S. person, as long as the foreign swap dealer used "personnel or agents located in the U.S. to arrange, negotiate, or execute such swap."92 The advisory proved controversial and drew strong industry opposition.93 The CFTC has delayed its actual implementation several times. Presumably, H.R. 2289 would overturn it.

Swap Data Repository Indemnifications (H.R. 2289)94

Section 302 of H.R. 2289 would remove a requirement added in the Dodd-Frank Act's Title VII that foreign regulators indemnify a U.S.-based swap data repository (SDR) and the Commodity Futures Trading Commission (CFTC) for any expenses arising from litigation related to a request for market data.95 Indemnification generally refers to compensating someone for harm or loss. The provision instead requires the SDR and the CFTC, prior to sharing information, to first receive written agreements from the foreign regulator promising to abide by confidentiality requirements with respect to the data. The provision also does the same for security-based swap data repositories and for the SEC's information-sharing on security-based swaps with foreign regulators.

In an effort to improve transparency in the opaque swaps market, Title VII of Dodd-Frank required all swaps to be reported to SDRs. Dodd-Frank included provisions requiring foreign regulators to indemnify U.S.-based SDRs, and the CFTC, for expenses arising from litigation related to requests for swaps transactions data.96 The original purpose of this Dodd-Frank provision appeared to be to try to encourage foreign regulators to more closely protect any shared information related to swaps by making it potentially more costly for them, should any information be leaked.

In subsequent years after Dodd-Frank's passage, however, regulators testified that the indemnification requirement was creating barriers to information sharing with foreign regulators.97 At a February 12, 2015, House Agriculture Committee hearing, CFTC Chair Massad, questioned about this indemnification provision, noted that "If the legislation did remove this provision, this indemnification requirement, then it would facilitate the sharing of information ... across borders. Again, that would just make it easier for regulators to work together."98

In the 114th Congress, H.R. 1847, which is substantially similar to the provision in H.R. 2289 repealing the indemnification provision, passed the House on July 14, 2015, on a voice vote. Substantially the same provision was also included in Section 86001 of the conference report on the Fixing America's Surface Transportation Act (H.R. 22, H.Rept. 114-357). This provision in the Fixing America's Surface Transportation (FAST) Act was signed into law as P.L. 114-94 on December 4, 2015. It removed the requirement added in the Dodd-Frank Act's Title VII99 that foreign regulators indemnify a U.S.-based swap data repository (SDR) and the CFTC for any expenses arising from litigation related to a request for market data.100

In House floor debate over H.R. 1847, proponents of the bill stated that the concept of indemnification did not exist in some foreign jurisdictions, making it impossible for some foreign regulators to agree to these requirements before sharing information, and thus hindering the sharing of market information between U.S. and foreign regulators.101 The provision in H.R. 2289, as in H.R. 1847, repeals the indemnification requirement but maintains the existing provisions that require confidentiality agreements to be signed prior to information sharing. H.R. 742Officials from the SEC have also testified that they recommended removing this provision, which they viewed as a barrier to information sharing.102

Residual Interest (H.R. 2289, S. 2917)

The term residual interest generally refers to capital from a futures commission merchant (FCM) committed to temporarily make up the difference for insufficient margin in a customer's account.103 Both bills, S. 2917 in Section 104 and H.R. 2289 in Section 104, would essentially codify the deadline for FCMs to deposit any capital to cover residual interest as no earlier than 6:00 p.m. on the following business day.104 This move is broadly in line with the CFTC's March 17, 2015, final rule on residual interest.

The CFTC's Regulation 1.22 sets the deadline for posting residual interest.105 That deadline then affects when customers are required to post their collateral to cover insufficient margin amounts. Regulation 1.22 provided that the deadline, currently set for 6:00 p.m. on the following day, would automatically become earlier in a couple of years, without further CFTC action.106 The CFTC's final rule on March 17, 2015, amended Regulation 1.22 so that the FCM's deadline to post residual interest would not become earlier than 6:00 p.m. the following day without an affirmative CFTC action or rulemaking that included an opportunity for public comment.107

CFTC Chair Massad noted in a statement on this rule that an earlier deadline could help to ensure that FCMs always held sufficient margin and did not use one customer's margin to support another customer's. But such a practice could also impose costs on customers who must deliver margin sooner.108 The March 17, 2015, final rule included a plan for the CFTC to conduct a study of how well the current rule and deadline function, the practicability of changing the deadline, and the costs and benefits of any change.

Author Contact Information

Footnotes

| 1. | |

| 2. |

Futures, options, and swaps are examples of derivatives. Derivatives are financial instruments with one feature in common: their value is linked to changes in some underlying variable, such as the price of a physical commodity, a stock index, or an interest rate. Derivatives contracts—futures contracts, options, and swaps—gain or lose value as the underlying rates or prices change, even though the holder may not actually own the underlying asset. |

| 3. |

P.L. 74-765, 7 U.S.C. §1 et seq. |

| 4. | |

| 5. |

A swap is an exchange of one asset or liability for a similar asset or liability for the general purpose of shifting risks. The basic terms of a swap often require two counterparties to exchange payments periodically for a prearranged duration of time. For instance, one party may pay a fixed rate payment stream and receive in return a variable rate payment stream from their swap counterparty (or vice versa) for a certain time period. |

| 6. |

These platforms are called swap execution facilities. |

| 7. |

See Commodity Futures Trading Commission (CFTC), President's Budget Fiscal Year 2016, p. 3, available at http://www.cftc.gov/About/CFTCReports/ssLINK/cftcbudget2016. |

| 8. |

Ibid. |

| 9. |

CFTC, President's Budget Fiscal Year 2017, prepared for the Committee on Appropriations, February, 2016, p. 2, available at http://www.cftc.gov/idc/groups/public/@newsroom/documents/file/cftcbudget2017.pdf. |

| 10. |

Ibid., p. 3. |

| 11. |

The CFTC Chair's Transmittal Letter in the CFTC: President's Budget Fiscal Year 2017, prepared for the Committee on Appropriations states, for instance, that since the Dodd Frank Act was passed, the CFTC has primary oversight over the over-the-counter swaps market, estimated at $400 trillion to $600 trillion globally, in terms of notional amount, and that the futures and options markets the CFTC has traditionally overseen have grown substantially in size, sophistication and technological complexity as well. Available at http://www.cftc.gov/idc/groups/public/@newsroom/documents/file/cftcbudget2017.pdf. |

| 12. |

Please see "CFTC Organization," available at http://www.cftc.gov/About/CFTCOrganization/index.htm. |

| 13. |

An authorization may generally be described as a statutory provision that defines the authority of the government to act. The primary purpose of authorization statutes or provisions is to provide authority for an agency to administer a program or engage in an activity. For further information, see CRS Report R42098, Authorization of Appropriations: Procedural and Legal Issues, by Jessica Tollestrup and Brian T. Yeh. |

| 14. |

The Government Accountability Office (GAO) guidance states that "the existence of a statute (organic legislation) imposing substantive functions upon an agency that require funding for their performance is itself sufficient legal authorization for the necessary appropriations, regardless of whether the statute addresses the question of subsequent appropriations." (GAO Red Book, Volume I, at 2-41, 2-69 [3d ed. 2004]). |

| 15. |

For a closer look at some of the past CFTC reauthorizations, see, e.g., CRS Report 89-520E Commodity Futures Trading Commission Reauthorization in 1982 and 1986: Major Issues in Futures Regulations by Mark Jickling (out-of-print report; available to congressional clients from the author upon request.) |

| 16. |

The $400 trillion figure is measured in terms of notional value. Please see Testimony of Chairman Timothy G. Massad before the U.S. Senate Committee on Agriculture, Nutrition & Forestry, Washington, DC, May 14, 2015, which says in part: "In addition to the challenges posed by the growth and increasing complexity of the futures and options market, our responsibilities now include overseeing the swaps market, an over $400 trillion market in the U.S., measured by notional amount." Available at http://www.cftc.gov/PressRoom/SpeechesTestimony/opamassad-22. |

| 17. |

Since Dodd-Frank, (P.L. 111-203) oversight of the swaps market is divided between the CFTC, which oversees the vast majority of swaps, and the Securities and Exchange Commission (SEC), which regulates a smaller subset of swaps called security-based swaps (SBS). SBS are swaps based on a single security or loan or a narrow-based group or index of securities (or events relating to a single issuer or issuers of securities in a narrow-based security). See U.S. Securities and Exchange Commission, Derivatives, Background, available at https://www.sec.gov/spotlight/dodd-frank/derivatives.shtml. |

| 18. |

For a comprehensive summary of each of H.R. 2289's provisions, see CRS Summary, May 29, 2015, at http://www.lis.gov/cgi-lis/bdquery/D?d114:1:./temp/~bdpQ7D:@@@D&summ2=m&:dbs=n:|/billsumm/billsumm.php?id=2|. |

| 19. |

Executive Office of the President, Office of Management and Budget, Statement of Administration Policy on H.R. 2289—Commodity End-User Relief Act, June 2, 2105, at https://www.whitehouse.gov/sites/default/files/omb/legislative/sap/114/saphr2289r_20150602.pdf. |

| 20. |

7 U.S.C. §16(d) currently reads "(d) Authorization of appropriations—There are authorized to be appropriated such sums as are necessary to carry out this chapter for each of the fiscal years 2008 through 2013." |

| 21. |

This is a selective, not a comprehensive list of issues. For a comprehensive summary of each of H.R. 2289's provisions, see CRS Summary, May 29, 2015, available at http://www.lis.gov/cgi-lis/bdquery/D?d114:1:./temp/~bdaf0x:@@@D&summ2=m&:dbs=n:|/billsumm/billsumm.php?id=2|. |

| 22. |

As defined in 44 U.S.C. §3502. |

| 23. |

Under E.O. 12866, the Office of Management and Budget's (OMB's) Office of Information and Regulatory Affairs (OIRA) reviews "significant" proposed and final regulations for agencies that are covered, and those agencies are required to conduct a cost-benefit analysis if they deem a rule to be "economically significant" (e.g., if it has a $100 million effect on the economy). For a more detailed examination of cost-benefit analysis, see CRS Report R41974, Cost-Benefit and Other Analysis Requirements in the Rulemaking Process, coordinated by Maeve P. Carey. |

| 24. |

7 U.S.C. §19(a). |

| 25. |

7 U.S.C. §19(a). Subsection (a) (3) in 7 U.S.C. §19(a) also states that these requirements do not apply to "(A) An order that initiates, is part of, or is the result of an adjudicatory or investigative process of the Commission. (B) An emergency action. (C) A finding of fact regarding compliance with a requirement of the Commission." |

| 26. |

Memorandum of Understanding Between Office of Information and Regulatory Affairs, Executive Office of the President, and U.S. Commodity Futures Trading Commission, May 9, 2012, available at https://www.whitehouse.gov/ ... /oira_cftc_mou_2012.pdf. |

| 27. |

In September 2010, the CFTC Office of General Counsel and Office of Chief Economist created a template for a uniform cost-benefit analysis methodology to be used in Dodd-Frank Act proposed rules. That template stated, in part, that Section 15(a) "does not require the Commission to quantify the costs and benefits of a rule or to determine whether the benefits of the order outweigh its costs; rather, it requires that the Commission 'consider' the costs and benefits of its actions." It went on to say that CFTC "could in its discretion determine that, notwithstanding its costs, a particular rule is necessary or appropriate to protect the public interest or to effectuate any of the provisions or accomplish any of the purposes of the Act." See Office of the Inspector General, U.S. Commodity Futures Trading Commission, "A Review of Cost-Benefit Analyses Performed by the Commodity Futures Trading Commission in Connection with Rulemakings Undertaken Pursuant to the Dodd-Frank Act," June 13, 2011, p. 3, available at http://www.cftc.gov/ucm/groups/public/@aboutcftc/documents/file/oig_investigation_061311.pdf. |

| 28. |

"The Commission, through the Office of the Chief Economist, shall assess and publish in the regulation or order the costs and benefits, both qualitative and quantitative, of the proposed regulation or order, and the proposed regulation or order shall state its statutory justification." H.R. 2289, The Commodity End User Relief Act, 114th Congress, §202. |

| 29. |

See Office of the Inspector General, U.S. Commodity Futures Trading Commission, "A Review of Cost-Benefit Analyses Performed by the Commodity Futures Trading Commission in Connection with Rulemakings Undertaken Pursuant to the Dodd-Frank Act," June 13, 2011, p. 3, available at http://www.cftc.gov/ucm/groups/public/@aboutcftc/documents/file/oig_investigation_061311.pdf. |

| 30. |

For an analysis of these issues, see Tosihiro Oka, Effectiveness and Limitations of Cost-benefit Analysis in Policy Appraisal, p. 26, available at http://www.jbaudit.go.jp/english/exchange/pdf/e10d02.pdf. |

| 31. |

For a more detailed discussion of the debate over cost-benefit analysis, see CRS Report R42821, Independent Regulatory Agencies, Cost-Benefit Analysis, and Presidential Review of Regulations, by Maeve P. Carey and Michelle D. Christensen. |

| 32. |

See, e.g., Robert W. Hahn and Paul C. Tetlock, "Has Economic Analysis Improved Regulatory Decisions?" Journal of Economic Perspectives, vol. 22, no. 1 (Winter 2008), p. 68. |

| 33. |

See, e.g., Cass R. Sunstein, The Cost-Benefit State: The Future of Regulatory Protection (Chicago: American Bar Association, 2002), pp. 6-10. |

| 34. |

For two main proponents of the ossification thesis, see Thomas O. McGarity, "Some Thoughts on 'Deossifying' the Rulemaking Process," Duke Law Journal, vol. 41, no. 6 (June 1992), pp. 1385-1462; and Richard J. Pierce, Jr., "Seven Ways to Deossify Agency Rulemaking," Administrative Law Review, vol. 47, no. 1 (Winter 1995), pp. 59-98. |

| 35. |

See, e.g., Dennis Kelleher, Stephen Hall, and Katelynn Bradley, Setting the Record Straight on Cost-Benefit Analysis and Financial Reform at the SEC, Better Markets, Inc., July 30, 2012. |

| 36. |

Dennis Kelleher, Cost Benefit Analysis and Financial Reform: Overview, Better Markets, available at http://ourfinancialsecurity.org/wp-content/uploads/2012/05/DENNIS-KELLEHER-PPT.pdf. |

| 37. |

Additional bills on this topic in the 114th Congress, which do not include a reauthorization of the CFTC, include H.R. 1317, which was marked up and ordered to be reported by the House Financial Services Committee on July 29, 2015; and was marked up and ordered to be reported by the House Agriculture Committee on September 30, 2015; and S. 876; and H.R. 37 in §201. |

| 38. |

Or on an exchange-like facility called a swap execution facility. |

| 39. |

Codified at 7 U.S.C. §2(h)(7). |

| 40. |

7 U.S.C. §2(h)(7)(D). |

| 41. |

P.L. 111-203 §723. |

| 42. |

P.L. 111-203 §723, codified at 7 U.S.C. §2(h)(7)(D)(ii). |

| 43. |

Among other commenters, the CFTC cited comment letters from Shell Energy North America, Kraft, Philip Morris and Siemens, as making such arguments, at 77 FR 42563 (July 19, 2012). |

| 44. |

Without additional definition, however, the term treasury unit does not necessarily refer to a unit only within a non-financial parent company. Financial companies can and do have "treasury units" as well. |

| 45. |

See, e.g., comment letters from Shell Energy North America, Kraft, Philip Morris and Siemens, as making such arguments, at 77 FR 42563 (July 19, 2012). |

| 46. |

See 77 FR 42560 (July 19, 2012), "End-User Exception to the Clearing Requirement for Swaps," CFTC Final Rule at 42561 and at 42563, available at http://www.cftc.gov/ucm/groups/public/@lrfederalregister/documents/file/2012-17291a.pdf. |

| 47. |

"However, the Commission notes that it is important to distinguish where the treasury function operates in the corporate structure. Treasury affiliates that are separate legal entities and whose sole or primary function is to undertake activities that are financial in nature as defined under Section 4(k) of the Bank Holding Company Act are financial entities as defined in Section 2(h)(7)(C)(VIII) of the CEA because they are ''predominantly engaged'' in such activities. If, on the other hand, the treasury function through which hedging or mitigating the commercial risks of an entire corporate group is undertaken by the parent or another corporate entity, and that parent or other entity is entering into swaps in its own name, then the application of the end-user exception to those swaps would be analyzed from the perspective of the parent or other corporate entity of the parent or other corporate entity directly." 77 FR 42563 (July 19, 2012). |

| 48. |

CFTC citing comment letter from Idaho Petroleum Marketers & Convenience Store Association (IPM&CSA) at FR 42560 (July 19, 2012). |

| 49. |

"We must not broaden this narrow, commonsense exception to include financial and commercial institutions that want to gamble in the derivatives markets. Doing so would allow systemically important companies to enter into risky trades in a market with zero transparency and accountability.'' CFTC citing Form Letters received as comments at 77 FR 42560 (July 19, 2012). |

| 50. |

CFTC Letter No. 14-144, "No Action Relief from the Clearing Requirement for Swaps Entered into by Eligible Treasury Affiliates," (November 26, 2014), available at http://www.cftc.gov/ucm/groups/public/@lrlettergeneral/documents/letter/14-144.pdf. |

| 51. |

CFTC Letter No. 14-144, pp. 3-7. |

| 52. |

See, e.g., Letter from the United State Chamber Of Commerce, June 8, 2015, entered into the Congressional Record, daily edition, vol. 161, No. 91 (June 9, 2015), p. H3937, during House Floor Debate on H.R. 2289, 114th Cong., 1st sess. Available at https://www.congress.gov/crec/2015/06/09/CREC-2015-06-09.pdf. and Letter from the National Association of Manufacturers, June 5, 2015, entered into the Congressional Record, daily edition, vol. 161, no. 91 (June 9, 2015), p. H3933, during House floor debate on H.R. 2289, 114th Cong., 1st sess., available at https://www.congress.gov/crec/2015/06/09/CREC-2015-06-09.pdf. |

| 53. |

See, e.g., Letter from the United State Chamber Of Commerce, June 8, 2015, entered into the Congressional Record, daily edition, and vol. 161, no. 91 (June 9, 2015), p. H3937, during House floor debate on H.R. 2289, 114th Cong., 1st sess. ("Non-financial companies that use centralized treasury units to manage their enterprise-wide risk should not be penalized for adopting this risk reducing structure, and H.R. 2289 acknowledges and would address this issue.") Available at https://www.congress.gov/crec/2015/06/09/CREC-2015-06-09.pdf. |

| 54. |

See, e.g., Letter from the United State Chamber Of Commerce, June 8, 2015, entered into the Congressional Record, daily edition, and vol. 161, no. 91 (June 9, 2015), p. H3937, during House floor debate on H.R. 2289, 114th Cong., 1st sess., available at https://www.congress.gov/crec/2015/06/09/CREC-2015-06-09.pdf. |

| 55. |

Letter from the National Association of Manufacturers, June 5, 2015, entered into the Congressional Record, daily edition, vol. 161, no. 91 (June 9, 2015), p. H3933, during House floor debate on H.R. 2289, 114th Cong., 1st sess., available at https://www.congress.gov/crec/2015/06/09/CREC-2015-06-09.pdf. |

| 56. |

Americans for Financial Reform, June 3, 2015, Letter to Congress, available, at http://ourfinancialsecurity.org/2015/06/letter-to-congress-afr-urges-congress-to-keep-our-markets-safe-reject-hr-2289/. |

| 57. |

Better Markets, Letter Re. Proposed Clearing Exemption for Swaps Between Certain Affiliated Entities, September 21, 2012, p. 4, available at http://www.bettermarkets.com/sites/default/files/documents/CFTC-CL-%20Proposed%20Clearing%20Exeption%20for%20Swaps%20Between%20Certain%20Affiliated%20Entities-%209-21-12.pdf. |

| 58. |

Better Markets, p. 5. |

| 59. |

7 U.S.C. §2(h)(7)(D). |

| 60. |

H.R. 2289 §301 has a similar provision for security-based swaps, which fall under the jurisdiction of the SEC. |

| 61. |

Again, using the end-user exception means the entity would not be required to clear its swaps through a derivatives clearinghouse nor trade the swaps on an exchange or swap execution facility, which is similar to an exchange. |

| 62. |

As per the Commodity Exchange Act's Prohibition on Affiliates, in 7 U.S.C. §2(h)(7)(D)(ii), what would commonly be referred to as a hedge fund is defined as, "an issuer that would be an investment company, as defined in section 3 of the Investment Company Act of 1940 (15 U.S.C. 80a–3), but for paragraph (1) or (7) of subsection (c) of that Act [8] (15 U.S.C. §80a–3(c))." |

| 63. |

7 U.S.C. §2(h) (7) (A). |

| 64. |