Social Services Block Grant: Background and Funding

The Social Services Block Grant (SSBG) is a flexible source of funds that states use to support a wide variety of social services activities. States have broad discretion over the use of these funds. In FY2014, the most recent year for which expenditure data are available, the largest expenditures for services under the SSBG were for foster care, child protective services, child care, and special services for the disabled.

Since FY2002, annual appropriations laws have funded the SSBG at its authorized level of $1.700 billion. However, starting in FY2013, SSBG appropriations have been subject to sequestration, a spending reduction process by which budgetary resources are canceled to enforce budget policy goals. Most recently, temporary FY2017 funding for the SSBG has been provided through December 9, 2016, by a continuing resolution (P.L. 114-223, Division C). The FY2017 continuing resolution provided funding for the SSBG at current-law levels ($1.7 billion, less sequestration) under the same authorities and conditions as in FY2016. The FY2016 operating level for the SSBG was roughly $1.584 billion post-sequester. This is roughly $116 million (7%) less than the SSBG’s FY2016 pre-sequester funding level of $1.700 billion and $9 million (0.5%) more than the SSBG’s FY2015 post-sequester operating level of $1.576 billion.

In addition to annual appropriations, the SSBG occasionally receives supplemental appropriations to assist states and territories in responding to natural disasters. Most recently, the SSBG received supplemental funding of $474.5 million (post-sequester) in FY2013 to support states affected by Hurricane Sandy. (These funds were in addition to the $1.613 billion, post-sequester, appropriated in the FY2013 annual appropriations law.)

Annual appropriations laws since FY2001 have included a provision allowing states to transfer up to 10% of their Temporary Assistance for Needy Families (TANF) block grants to the SSBG.

The SSBG is permanently authorized in Title XX, Subtitle A, of the Social Security Act (SSA). The 111th Congress amended Title XX of the SSA in the health care reform legislation signed into law by President Obama on March 23, 2010, the Patient Protection and Affordable Care Act (ACA; P.L. 111-148). This law inserted a new subtitle on elder justice into Title XX, which was itself re-titled as Block Grants to States for Social Services and Elder Justice. The health reform law also amended Title XX by establishing two demonstration projects to address the workforce needs of health care professionals and a new competitive grant program to support the early detection of medical conditions related to environmental health hazards. The purpose of this report is to provide background and funding information about the SSBG; the report does not provide detailed information on other programs authorized within Title XX of the SSA.

Social Services Block Grant: Background and Funding

Jump to Main Text of Report

Contents

- Introduction

- Use of Funds

- Goals

- Services

- Prohibited Uses

- Eligibility

- Transfer of TANF Funds to SSBG

- FY2017 Funding

- Continuing Resolution

- Preliminary Congressional Action

- Obama Administration Request

- FY2016 Funding

- Zika Supplemental

- Final Appropriations

- Preliminary Congressional Action

- Budget Resolution

- Obama Administration Request

- Additional Appropriations History

- Allocation of Funds

- State Reporting Requirements

- Recent Expenditures

- Recent Legislative Action

- Proposal to Repeal the SSBG in the 112th Congress

- How Did Health Reform Affect the SSBG?

- New Subtitle on Elder Justice

- New Programs Authorized within the SSBG Subtitle of Title XX

Tables

- Table 1. SSBG Funding, FY1985-FY2016

- Table 2. FY2014-FY2016 SSBG Allotments to States and Territories

- Table 3. Total SSBG Expenditures by Service Category, FY2014

- Table A-1. TANF Transfers to the SSBG in FY2015

- Table B-1. State Allocations and Spending from the FY2013 Supplemental

- Table B-2. State Allocations and Spending from the FY2008 SSBG Supplemental

- Table B-3. State Spending from the FY2006 SSBG Supplemental

Summary

The Social Services Block Grant (SSBG) is a flexible source of funds that states use to support a wide variety of social services activities. States have broad discretion over the use of these funds. In FY2014, the most recent year for which expenditure data are available, the largest expenditures for services under the SSBG were for foster care, child protective services, child care, and special services for the disabled.

Since FY2002, annual appropriations laws have funded the SSBG at its authorized level of $1.700 billion. However, starting in FY2013, SSBG appropriations have been subject to sequestration, a spending reduction process by which budgetary resources are canceled to enforce budget policy goals. Most recently, temporary FY2017 funding for the SSBG has been provided through December 9, 2016, by a continuing resolution (P.L. 114-223, Division C). The FY2017 continuing resolution provided funding for the SSBG at current-law levels ($1.7 billion, less sequestration) under the same authorities and conditions as in FY2016. The FY2016 operating level for the SSBG was roughly $1.584 billion post-sequester. This is roughly $116 million (7%) less than the SSBG's FY2016 pre-sequester funding level of $1.700 billion and $9 million (0.5%) more than the SSBG's FY2015 post-sequester operating level of $1.576 billion.

In addition to annual appropriations, the SSBG occasionally receives supplemental appropriations to assist states and territories in responding to natural disasters. Most recently, the SSBG received supplemental funding of $474.5 million (post-sequester) in FY2013 to support states affected by Hurricane Sandy. (These funds were in addition to the $1.613 billion, post-sequester, appropriated in the FY2013 annual appropriations law.)

Annual appropriations laws since FY2001 have included a provision allowing states to transfer up to 10% of their Temporary Assistance for Needy Families (TANF) block grants to the SSBG.

The SSBG is permanently authorized in Title XX, Subtitle A, of the Social Security Act (SSA). The 111th Congress amended Title XX of the SSA in the health care reform legislation signed into law by President Obama on March 23, 2010, the Patient Protection and Affordable Care Act (ACA; P.L. 111-148). This law inserted a new subtitle on elder justice into Title XX, which was itself re-titled as Block Grants to States for Social Services and Elder Justice. The health reform law also amended Title XX by establishing two demonstration projects to address the workforce needs of health care professionals and a new competitive grant program to support the early detection of medical conditions related to environmental health hazards. The purpose of this report is to provide background and funding information about the SSBG; the report does not provide detailed information on other programs authorized within Title XX of the SSA.

Introduction

The Social Services Block Grant (SSBG) is permanently authorized by Title XX, Subtitle A, of the Social Security Act as a "capped" entitlement to states. This means that states (and territories) are entitled to their share of funds, as determined by formula, out of an amount that is capped in statute at a specific level (also known as a funding ceiling). Although social services for certain welfare recipients have been authorized under various titles of the Social Security Act since 1956, the SSBG in its current form was created in 1981 (P.L. 97-35). Block grant funds are given to states to achieve a wide range of social policy goals, which include promoting self-sufficiency, preventing child abuse, and supporting community-based care for the elderly and disabled.

Since FY2002, annual appropriations laws have funded the SSBG at its authorized level of $1.7 billion. However, starting in FY2013, SSBG appropriations have been subject to sequestration, a spending reduction process by which budgetary resources are canceled to enforce budget policy goals. Full-year FY2017 appropriations were not enacted prior to the start of the fiscal year. Instead, temporary funding for the SSBG has been provided through December 9, 2016, by a continuing resolution (P.L. 114-223, Division C). The continuing resolution (CR) maintained SSBG funding at current-law levels ($1.7 billion, less sequestration). Annual appropriations laws since FY2001 have included a provision allowing states to transfer up to 10% of their Temporary Assistance for Needy Families (TANF) block grants to the SSBG. In addition to annual appropriations, the SSBG occasionally receives supplemental appropriations to assist states and territories in responding to natural disasters, including in FY2006, FY2008, and FY2013 (for more information, see Appendix B).

Health reform legislation enacted into law (P.L. 111-148) in March 2010 amended Title XX of the Social Security Act to include a subtitle on elder justice and to establish several other programs. Although these changes, briefly reviewed later, have technical importance for the statutory citations of the SSBG, they did not substantively amend the provisions within Title XX that govern the SSBG itself and they are not discussed at length in this report. Likewise, this report does not discuss the special SSBG program for enterprise communities and empowerment zones that was authorized in 1993 (P.L. 103-66), but is not currently funded.

At the federal level, the SSBG is administered by the U.S. Department of Health and Human Services (HHS). Legislation amending Title XX is typically reported by the House Ways and Means Committee and the Senate Finance Committee.

Use of Funds

Goals

Federal law establishes the five broad goals for the SSBG. Social services funded by states must be linked to one or more of these goals. The five goals are

- achieving or maintaining economic self-support to prevent, reduce, or eliminate dependency;

- achieving or maintaining self-sufficiency, including reduction or prevention of dependency;

- preventing or remedying neglect, abuse, or exploitation of children and adults unable to protect their own interests, or preserving, rehabilitating, or reuniting families;

- preventing or reducing inappropriate institutional care by providing for community-based care, home-based care, or other forms of less intensive care; and

- securing referral or admission for institutional care when other forms of care are not appropriate, or providing services to individuals in institutions.

Services

States have broad discretion in spending SSBG funds to support these broad goals. The following are examples of social services, as specified in law, that relate to the SSBG's broad goals:

child care, protective services for children and adults, services for children and adults in foster care, services related to the management and maintenance of the home, adult day care, transportation, family planning, training and related services, employment services, referral and counseling services, meal preparation delivery, health support services, and services to meet the special needs of children, the aged, the mentally retarded, the blind, the emotionally disturbed, the physically handicapped, and alcoholics and drug addicts.

In 1993, HHS issued a regulation establishing uniform definitions for 28 SSBG service categories. State spending is not limited to these services; instead, these service categories are used as guidelines for reporting purposes. (Spending on an activity that falls outside the scope of services defined in regulation is characterized under "other services" on annual reports.) In addition to supporting social services, SSBG funds may be used for administration, planning, evaluation, and training. (See Table 3 for a full list of the service categories reported on by states.) States may also transfer up to 10% of their SSBG allotments to block grants for health activities and low-income home energy assistance.

Prohibited Uses

Although SSBG funds can be used for a broad array of activities, some restrictions are placed on the use of these funds. Funds cannot be used for the following: (1) purchase of land, construction, or major capital improvements; (2) cash payments as a service or for costs of subsistence or room and board (other than costs of subsistence during rehabilitation, temporary emergency shelter provided as a protective service, or in the case of vouchers for certain families as allowed under welfare reform); (3) payment of wages as a social service (except wages of welfare recipients employed in child day care); (4) most medical care (except family planning, rehabilitation services, initial detoxification of certain individuals, or medical care provided as an "integral but subordinate component of a social service"); (5) social services for residents of institutions (including hospitals, nursing homes, and prisons); (6) educational services generally provided by public schools; (7) child care that does not meet applicable state or local standards; (8) services provided by anyone excluded from participation in Medicare or certain other Social Security Act programs; or (9) items or services related to assisted suicide (this provision was added in 1997, under P.L. 105-12).1 Under extraordinary circumstances, the law does allow HHS to waive two of these prohibitions (use of the SSBG for the purchase of land or capital improvements, or for the provision of medical care).

Eligibility

There are no federal eligibility criteria for SSBG participants. Thus, states have total discretion to set their own eligibility criteria. One exception is that welfare reform established an income limit of 200% of poverty for recipients of services funded by TANF allotments that are transferred to the SSBG.

Transfer of TANF Funds to SSBG

The 1996 welfare reform law replaced Aid to Families with Dependent Children (AFDC) with a block grant to states, called Temporary Assistance for Needy Families (TANF), under Title IV-A of the Social Security Act. The law allowed states to transfer up to 10% of their annual TANF allotments into the SSBG. Under provisions of the Transportation Equity Act of 1998 (P.L. 105-178), the amount that states could transfer into SSBG was reduced to 4.25% of their annual TANF allotments, beginning in FY2001. However, this provision was superseded in FY2001 by the FY2001 Consolidated Appropriations Act, which maintained the 10% transfer authority level.

Likewise, the FY2002 appropriations bill presented to the President maintained the 10% transfer authority for FY2002. Earlier, the House had passed its version of a Labor, HHS, Education appropriations bill (H.R. 3061) proposing to maintain the 10% transfer authority, while the Senate's amended version proposed a 5.7% transfer level. Ultimately, appropriations acts maintained the transfer authority at 10% in FY2003-FY2016 as well.

There has been some confusion about whether or not the Deficit Reduction Act (DRA, P.L. 109-171) permanently reinstated the 10% transfer authority. This law extended the TANF program, through the end of FY2010, in the manner authorized for FY2004.2 In that fiscal year, the Social Security Act capped states' authority to transfer TANF funds to the SSBG at 4.25%, but this law was superseded by the FY2004 Consolidated Appropriations Act (P.L. 108-199), which maintained the practice of allowing 10% transfers from TANF to the SSBG. In the wake of the DRA, Congress has continued to ensure that the transfer ceiling stays at 10% by including language to that effect in appropriations legislation.

Over the course of FY1998-FY2015, states annually transferred roughly $1 billion of their TANF funds to the SSBG. In FY2015 alone, 38 states (including the District of Columbia) transferred a combined $1.2 billion to the SSBG, with 28 of those states taking advantage of the higher transfer ceiling by moving more than 4.25% of their TANF funds to the SSBG (see Table A-1 in Appendix A for FY2015 state-by-state data).3 Funds transferred from TANF to the SSBG can be used only for children and families whose income is less than 200% of the federal poverty guidelines. Under welfare reform law, states also may use SSBG funds for vouchers for families that are not eligible for cash assistance because of time limits under the welfare reform program, or for children who are denied cash assistance because they were born into families already receiving benefits for another child.

FY2017 Funding

Continuing Resolution

On September 29, 2016, President Obama signed into law H.R. 5325, which contains the Continuing Appropriations Act, 2017, in Division C (P.L. 114-223). This law generally funds annually appropriated entitlements, like the SSBG, at their current-law levels through December 9, 2016, or until full-year appropriations are enacted. In the case of SSBG, the current-law level is $1.7 billion, reduced by an estimated 6.9% due to sequestration (see text box).4 The FY2017 CR maintains the authorities and conditions placed on appropriations in FY2016. For the SSBG, this would presumably include the provision, carried in annual appropriations laws since FY2001, allowing states to transfer up to 10% of their TANF block grants to the SSBG.

Preliminary Congressional Action

Before the passage of the FY2017 continuing resolution, both the House and Senate appropriations committees initiated action on full-year appropriations bills for the Departments of Labor, HHS, Education, and Related Agencies (LHHS). On July 14, 2016, the House Appropriations Committee approved its FY2017 LHHS appropriations bill by a voice vote (H.R. 5926; H.Rept. 114-699). On June 6, 2016, the Senate Appropriations Committee approved its FY2017 LHHS bill by a vote of 30-0. Both bills included $1.7 billion for the SSBG (pre-sequester).

Obama Administration Request

On February 9, 2016, the Obama Administration released the FY2017 President's budget, which requested $1.7 billion in basic funding for the SSBG. The FY2017 President's budget proposed new language to give HHS the authority to reserve up to 1.5% of SSBG funds for research, evaluation, and demonstration activities. Under the President's proposal, a share of these funds ($10 million) would be reserved for a pilot project to provide low-income families with access to an adequate supply of diapers. The President's budget also included a new legislative proposal that, if enacted, would require all SSBG funds used for child care services to meet the minimum health and safety standards (including monitoring and background checks) required by the Child Care and Development Block Grant Act, as amended.

In addition, the President's budget once again proposed funding for an Upward Mobility Project, which would allow up to 10 communities, states, or consortia to combine funds from up to four existing block grants: SSBG, Community Services Block Grant, Community Development Block Grant, and the HOME program. Participating jurisdictions would be eligible to apply for new competitive grant funds to assist with project implementation and cross-program community planning. The President's budget requested $300 million for FY2017 and $1.5 billion over five years for these new competitive grants, which would be funded through the SSBG account and awarded jointly by HHS and the U.S. Department of Housing and Urban Development. The Upward Mobility Project was first proposed in the FY2016 President's budget submission.

|

A Note on Sequestration Readers should note that starting in FY2013, annual SSBG appropriations have been affected by automatic budget reduction procedures known as "sequestration." These procedures are authorized by the Budget Control Act of 2011 (BCA, P.L. 112-25) and the Balanced Budget and Emergency Deficit Control Act of 1985 (P.L. 99-177), as amended. The BCA, which was signed into law on August 2, 2011, established a Joint Select Committee on Deficit Reduction, charged with the task of achieving at least $1.2 trillion in deficit reduction.5 The Joint Committee did not achieve this goal, triggering an automatic budget reduction process consisting of a combination of sequestration and lower discretionary spending limits.6 For FY2013, the BCA called for sequestration of both mandatory and discretionary spending programs. For FY2014-FY2025, the law calls for continued sequestration for mandatory programs and lower spending limits for discretionary programs. Annual SSBG appropriations consist of mandatory funding and thus, in the absence of congressional action, are expected to be subject to sequestration through FY2025. |

FY2016 Funding

Zika Supplemental

On September 29, 2016, President Obama signed into law H.R. 5325, which contains the Zika Preparedness and Response Act, 2016, in Division B (P.L. 114-223). This appropriations act did not contain supplemental funding for the SSBG, in contrast to some earlier legislative efforts.

Over the course of 2016, the House and Senate each considered legislation in response to the Obama Administration's request for supplemental appropriations to respond to threats posed by the spread of the Zika virus. On May 18, the House passed a measure (H.R. 5243) that contained no supplemental funding for SSBG. On May 19, the Senate passed a measure (S.Amdt. 3900 to H.R. 2577) that would have provided $75 million in supplemental funding to the SSBG "for health services in territories with active or local transmission cases of the Zika virus."

Subsequently, a conference report was filed in the House on June 22 (H.Rept. 114-640 to accompany H.R. 2577). The conference agreement would have provided $95 million to the SSBG "for health services provided by public health departments, hospitals, or reimbursed through public health plans ... in States, territories, or tribal lands with active or local transmission cases of the Zika virus." This provision was the object of much scrutiny.7 Among other things, some expressed concern that designating funds for only these specific entities could prevent states or territories from directing SSBG funds to other types of entities that offer family planning and women's health services, such as certain Planned Parenthood affiliated health centers.8 Ultimately, the conference agreement was adopted in the House, but not in the Senate, and the final Zika package contained in P.L. 114-223 did not contain supplemental funds for the SSBG.

Final Appropriations

On December 18, 2015, the President signed into law the Consolidated Appropriations Act, 2016 (P.L. 114-113). This law appropriated $1.7 billion for the SSBG. However, SSBG funds are subject to sequestration in FY2016 (see text box). The sequester reduced SSBG funding by 6.8% in FY2016, resulting in an estimated operating level of $1.584 billion.9 The FY2016 appropriations law maintained a provision, included in annual appropriations laws since FY2001, allowing states to transfer up to 10% of their TANF block grants to the SSBG.

Preliminary Congressional Action

Prior to the enactment of the FY2016 Consolidated Appropriations Act (P.L. 114-113), temporary funding for the SSBG had been provided by three short-term continuing resolutions (P.L. 114-100, P.L. 114-96, P.L. 114-53).

Before the passage of the first continuing resolution, both the House and Senate Appropriations Committees initiated action on full-year funding bills for the Departments of Labor, HHS, Education, and Related Agencies (L-HHS-ED). On June 25, the Senate Appropriations Committee approved its FY2016 LHHS appropriations bill by a vote of 16-14 (S. 1695; S.Rept. 114-74). On June 24, the House Appropriations Committee approved its FY2016 LHHS bill by a vote of 30-21 (H.R. 3020; H.Rept. 114-195). Both bills included $1.700 billion for the SSBG, pre-sequester.

Budget Resolution

Final action on the FY2016 budget resolution (S.Con.Res. 11, H.Rept. 114-96) occurred on May 5, 2015. None of the materials associated with the conference version of the FY2016 budget resolution make specific reference to the SSBG. However, the report (H.Rept. 114-47) accompanying an earlier version of the FY2016 budget resolution (H.Con.Res. 27) adopted in the House, specifically recommended eliminating funding for the SSBG.10 In its critique of the SSBG, the committee report noted that states are not required to match federal SSBG allotments or to demonstrate outcomes ("evidence of effectiveness") from their SSBG spending. The report called the SSBG a "duplicative" funding stream, noting that many services supported by the SSBG may also be supported by other federal programs.

Obama Administration Request

On February 2, 2015, the Obama Administration released the FY2016 President's budget, which requested $1.7 billion in basic funding for the SSBG. The President's budget further proposed new language to give HHS the authority to reserve a share ($8.5 million) of the total SSBG appropriation for research and evaluation activities.

In addition, the President's budget proposed a new Upward Mobility Project that would allow up to 10 communities, states, or consortia to combine funds from up to four existing block grants: SSBG, Community Services Block Grant, Community Development Block Grant, and the HOME program. Participating jurisdictions would also be eligible to apply for new competitive grant funds to assist with project implementation and cross-program community planning. The President's budget requested $300 million for FY2016 and $1.5 billion over five years for these new competitive grants, which would be funded through the SSBG account and awarded jointly by HHS and the U.S. Department of Housing and Urban Development.

Additional Appropriations History

Table 1 shows SSBG funding levels from 1985 on, including the high of $2.8 billion, which was provided annually from FY1991-FY1995. Although $2.8 billion was the originally authorized entitlement ceiling for FY1996, Congress reduced funding to $2.38 billion in that year. Welfare reform legislation (P.L. 104-193) subsequently set the annual SSBG entitlement ceiling at $2.38 billion in each of fiscal years 1997 through 2002. Under the welfare reform law, the ceiling was scheduled to return to a permanent level of $2.8 billion in FY2003.

After welfare reform was enacted, Congress passed an appropriations measure for FY1997 (P.L. 104-208) that contained $2.5 billion for the SSBG, exceeding the ceiling established in the welfare reform law. For FY1998, President Clinton requested that the amount authorized by welfare reform ($2.38 billion) be appropriated. However, Congress approved an FY1998 appropriations bill (P.L. 105-78) containing $2.299 billion for the SSBG. The Senate Appropriations Committee explained the reduction by stating that funding is provided for social services through other federal programs (S.Rept. 105-58). The House Appropriations Committee expressed concern that HHS lacks information on the effectiveness of SSBG-funded activities (H.Rept. 105-205).

In 1998, the Transportation Equity Act (TEA, P.L. 105-178) permanently reduced the SSBG entitlement ceiling to $1.7 billion, beginning in FY2001. However, the entitlement ceiling has not always reflected the actual appropriation. For example, the $1.725 billion appropriation level for FY2001 (H.R. 4577) exceeded the $1.7 billion ceiling by $25 million. In addition, a TEA provision limited the authority for states to transfer TANF funds to the SSBG beginning in FY2001 (reducing the transfer cap from 10%, as established in welfare reform, to 4.25%). However, each annual appropriation from FY2001 onward has included override to reinstate the higher cap, effectively enabling states to transfer up to 10% of their TANF funds to the SSBG.

In addition to annual appropriations, the SSBG occasionally receives supplemental appropriations, including in FY2006, FY2008, and FY2013. See Appendix B for additional information on these recent supplemental appropriations.

Table 1 shows SSBG entitlement ceilings and appropriations from FY1985-FY2016. Also shown for FY1997-FY2015 are the amounts transferred from TANF to SSBG.

|

Fiscal Year |

Ceiling |

Appropriation |

Fiscal Year |

Ceiling |

Appropriation |

Transfer from TANF |

|

1985 |

2.7 |

2.725a |

1997 |

2.380 |

2.5 |

0.36 |

|

1986 |

2.7 |

2.584b |

1998 |

2.380 |

2.299 |

1.12 |

|

1987 |

2.7 |

2.7 |

1999 |

2.380 |

1.909 |

1.32 |

|

1988 |

2.750c |

2.7 |

2000 |

2.380 |

1.775 |

1.10 |

|

1989 |

2.7 |

2.7 |

2001 |

1.700 |

1.725 |

0.93 |

|

1990 |

2.8 |

2.762d |

2002 |

1.700 |

1.700 |

1.03 |

|

1991 |

2.8 |

2.8 |

2003 |

1.700 |

1.700 |

0.93 |

|

1992 |

2.8 |

2.8 |

2004 |

1.700 |

1.700 |

0.77 |

|

1993 |

2.8 |

2.8 |

2005 |

1.700 |

1.700 |

0.92 |

|

1994 |

2.8 |

2.8 |

2006 |

1.700 |

1.700+0.550e |

0.97 |

|

1995 |

2.8 |

2.8 |

2007 |

1.700 |

1.700 |

1.17 |

|

1996 |

2.381 |

2.381 |

2008 |

1.700 |

1.700+0.600f |

1.18 |

|

2009 |

1.700 |

1.700 |

1.21 |

|||

|

2010 |

1.700 |

1.700 |

1.22 |

|||

|

2011 |

1.700 |

1.700 |

1.14 |

|||

|

2012 |

1.700 |

1.700 |

1.13 |

|||

|

2013 |

1.700 |

1.613+0.475g |

1.13 |

|||

|

2014 |

1.700 |

1.578h |

1.16 |

|||

|

2015 |

1.700 |

1.576i |

1.17 |

|||

|

2016 |

1.700 |

1.584j |

not avail |

Source: Table prepared by the Congressional Research Service (CRS) based on budget documents and HHS

data. In this table, TANF transfer figures reflect data from TANF spending reports; amounts may

not necessarily match transfer amounts shown in annual SSBG reports.

Note: not avail = data not yet available.

a. Amount includes $25 million earmarked for training of daycare providers, licensing officials, and parents, including training in the prevention of child abuse in child care settings (P.L. 98-473).

b. The entitlement ceiling for FY1986 was $2.7 billion. However, the Gramm-Rudman-Hollings legislation sequestration of funds for that period reduced the funding by $116 million.

c. The 1987 Budget Reconciliation Act (P.L. 100-203) included a $50 million increase in the Title XX entitlement ceiling for FY1988; however, these additional funds were not appropriated.

d. The FY1990 appropriation included a supplemental appropriation of $100 million (P.L. 101-198). The Gramm-Rudman-Hollings legislation sequestration of funds for FY1990 reduced funding by $37.8 million to $2.762 billion.

e. The FY2006 Labor-HHS-Education Appropriations Act maintained regular SSBG funding at $1.7 billion. The FY2006 Defense Appropriations Act (P.L. 109-148) provided an additional $550 million in SSBG funding, for necessary expenses related to the consequences of hurricanes in 2005.

f. The Consolidated Appropriations Act, 2008 (P.L. 110-161) maintained regular SSBG funding at $1.7 billion. However, the first FY2009 CR (P.L. 110-329) included, as Division B, the Disaster Relief and Recovery Supplemental Appropriations Act of 2008, which provided $600 million in supplemental SSBG funds. These funds were appropriated on the last day of FY2008, but not allotted to states until FY2009.

g. The Consolidated and Further Continuing Appropriations Act, 2013 (P.L. 113-6) appropriated $1.700 billion for the SSBG, but this amount was reduced to $1.613 billion due to sequestration. In response to Hurricane Sandy, the Disaster Relief Appropriations Act, 2013 (P.L. 113-2), reserved roughly $500 million ($474.5 million post-sequester) for the SSBG.

h. The Consolidated Appropriations Act, 2014 (P.L. 113-76) appropriated $1.7 billion for the SSBG, but this amount was reduced to $1.578 billion due to sequestration.

i. The Consolidated and Further Continuing Appropriations Act, 2015 (P.L. 113-235) appropriated $1.7 billion for the SSBG, but this amount was reduced to $1.576 billion due to sequestration.

j. The Consolidated and Further Continuing Appropriations Act, 2016 (P.L. 114-113) appropriated $1.7 billion for the SSBG, but this amount was reduced to $1.584 billion due to sequestration.

Allocation of Funds

SSBG funds are allocated to states according to the relative size of each state's population. Grants to Puerto Rico, Guam, the Virgin Islands, and Northern Mariana Islands are based on their share of Title XX funds in FY1981, while grants to American Samoa are based on the relative size of their population compared to the population of the Northern Mariana Islands. No match is required for federal SSBG funds, and federal law does not specify a sub-state allocation formula. In other words, states have complete discretion for the distribution of SSBG funds within their borders. Table 2 displays FY2014-FY2016 SSBG allotments by state.

|

State / Territory |

FY2014 |

FY2015 |

FY2016 |

|

Alabama |

24,098,066 |

23,961,439 |

23,961,910 |

|

Alaska |

3,655,417 |

3,644,153 |

3,640,366 |

|

Arizona |

32,749,900 |

32,849,106 |

33,261,842 |

|

Arkansas |

14,738,286 |

14,670,028 |

14,657,526 |

|

California |

190,112,095 |

190,019,689 |

191,732,260 |

|

Colorado |

25,924,678 |

26,116,035 |

26,464,591 |

|

Connecticut |

17,942,764 |

17,826,274 |

17,772,025 |

|

Delaware |

4,583,168 |

4,589,068 |

4,623,088 |

|

District of Columbia |

3,160,035 |

3,204,538 |

3,255,745 |

|

Florida |

96,539,571 |

96,926,273 |

98,297,450 |

|

Georgia |

49,574,938 |

49,532,575 |

49,893,342 |

|

Hawaii |

6,958,086 |

6,960,093 |

7,014,384 |

|

Idaho |

7,974,653 |

7,991,585 |

8,076,270 |

|

Illinois |

64,344,103 |

63,858,552 |

63,645,969 |

|

Indiana |

32,670,335 |

32,572,884 |

32,596,609 |

|

Iowa |

15,363,248 |

15,319,626 |

15,353,039 |

|

Kansas |

14,422,314 |

14,345,751 |

14,349,449 |

|

Kentucky |

21,891,130 |

21,788,094 |

21,807,927 |

|

Louisiana |

22,997,966 |

22,929,104 |

22,975,140 |

|

Maine |

6,642,639 |

6,584,580 |

6,572,282 |

|

Maryland |

29,408,111 |

29,389,964 |

29,530,830 |

|

Massachusetts |

33,214,113 |

33,177,268 |

33,331,644 |

|

Michigan |

49,392,104 |

49,053,988 |

48,967,028 |

|

Minnesota |

26,882,254 |

26,869,585 |

26,965,173 |

|

Mississippi |

14,917,172 |

14,827,833 |

14,794,447 |

|

Missouri |

30094893 |

29,961,804 |

29,961,617 |

|

Montana |

5,023,193 |

5,032,315 |

5,057,744 |

|

Nebraska |

9,272,989 |

9,262,496 |

9,296,948 |

|

Nevada |

13,787,761 |

13,831,096 |

14,028,655 |

|

New Hampshire |

6,600,290 |

6,560,572 |

6,556,094 |

|

New Jersey |

44,300,800 |

44,115,273 |

44,165,621 |

|

New Mexico |

10,422,479 |

10,337,060 |

10,305,301 |

|

New York |

97,802,404 |

97,413,396 |

97,570,743 |

|

North Carolina |

48,735,997 |

48,818,216 |

49,135,460 |

|

North Dakota |

3,496,392 |

3,585,961 |

3,653,954 |

|

Ohio |

57,692,279 |

57,358,120 |

57,289,481 |

|

Oklahoma |

19,064,568 |

19,087,806 |

19,162,360 |

|

Oregon |

19,487,022 |

19,481,884 |

19,617,883 |

|

Pennsylvania |

63,785,787 |

63,321,525 |

63,184,601 |

|

Rhode Island |

5,248,836 |

5,212,488 |

5,212,857 |

|

South Carolina |

23,606,812 |

23,669,547 |

23,878,428 |

|

South Dakota |

4,164,688 |

4,188,174 |

4,215,738 |

|

Tennessee |

32,265,083 |

32,201,475 |

32,361,886 |

|

Texas |

130,230,901 |

131,107,407 |

133,200,657 |

|

Utah |

14,269,300 |

14,380,030 |

14,541,570 |

|

Vermont |

3,128,491 |

3,106,293 |

3,095,990 |

|

Virginia |

40,908,881 |

40,947,988 |

41,142,148 |

|

Washington |

34,467,826 |

34,558,238 |

34,892,677 |

|

West Virginia |

9,272,429 |

9,192,045 |

9,142,895 |

|

Wisconsin |

28,617,681 |

28,467,435 |

28,449,475 |

|

Wyoming |

2,880,620 |

2,888,318 |

2,886,437 |

|

American Samoa |

56,052 |

55,991 |

56,293 |

|

Guam |

272,000 |

271,707 |

273,172 |

|

Northern Mariana Islands |

54,400 |

54,341 |

54,635 |

|

Puerto Rico |

8,160,000 |

8,151,207 |

8,195,172 |

|

Virgin Islands |

272,000 |

271,707 |

273,172 |

|

Total |

1,577,600,000 |

1,575,900,000 |

1,584,400,000 |

Source: Table prepared by the Congressional Research Service (CRS) based on data in annual congressional justifications produced by the HHS Administration for Children and Families. FY2014 allocations are taken from the FY2016 congressional justification; FY2015-FY2016 allocations are from the FY2017 congressional justification. The justifications are available online at http://www.acf.hhs.gov/programs/olab/budget.

Notes: Amounts are based on the annual SSBG appropriations as reduced by sequestration.

State Reporting Requirements

Each year, states are required to submit an intended use plan, often called a "pre-expenditure report," as a prerequisite to receive SSBG funds. The pre-expenditure report must be submitted 30 days prior to the start of the fiscal year.11 States must also submit a revised report if their planned uses for SSBG funds change during the course of the year. In pre-expenditure reports, states outline their plans for SSBG funds, including the types of services to be supported, and the categories and characteristics of individuals to be served (e.g., children, adults 59 and younger, adults 60 and older, and the disabled).

States are also required to report annually on their actual SSBG expenditures in each of the 29 service categories. For this report, submitted within six months after the end of the reporting period, states use a standard post-expenditure reporting form.12 HHS published regulations (November 15, 1993) to implement this requirement and to provide states with a uniform set of service category definitions.

States are not required to submit pre-expenditure reports using a standard format like the one required for post-expenditure reporting (e.g., states may simply submit a narrative or chart of their proposed activities and the individuals to be served). However, HHS issued a new Information Memorandum in December 2008, asking states to voluntarily include additional documentation as part of their pre-expenditure reports.13 Specifically, HHS requested that states submit a copy of the form used for post-expenditure reports, completed with estimated (rather than actual) expenditures and recipient data. The reason for this request was to allow for a more accurate analysis of the extent to which states are spending their SSBG funds "in a manner consistent" with their intended use plans. HHS issued a second Information Memorandum on this topic in June 2010, again encouraging states to submit pre-expenditure estimates using the same reporting form that is required for post-expenditure reports.14

Finally, in February 2012, HHS issued an Information Memorandum about a new performance measure that will compare spending plans with actual spending.15 To support implementation of the performance measure, HHS requested that states submit pre- and post-expenditure reports in Excel using standard reporting forms. HHS also requested that states choosing not to use the standard pre-expenditure reporting form (since the standard form is not technically required) provide a crosswalk to SSBG service categories. In addition, HHS requested that states differentiate in their pre-expenditure reports between estimated spending from the state's SSBG allocation and estimated state spending from projected TANF transfers, because the performance measure will apply only to those funds provided as part of a state's SSBG allocation.

Recent Expenditures

Table 3 shows national SSBG expenditures for FY2014, the most recent year for which SSBG data are available. Expenditures are separated into those made from the annual SSBG allocation and those made from funds transferred from the TANF block grant, and are displayed by service category. In FY2014, the largest expenditures for services under the SSBG were for foster care services for children (16%), protective services for children (12%), child care (11%), and special services for the disabled (10%).

|

SSBG Expenditures Made From: |

||||

|

Service Category |

SSBG |

Funds Transferred from TANF ($) |

Total SSBG Expenditures ($) |

Percentage of |

|

Adoption Services |

29,188,016 |

7,593,316 |

36,781,332 |

1% |

|

Case Management |

118,649,661 |

70,222,933 |

188,872,594 |

7% |

|

Congregate Meals |

1,523,613 |

5,092 |

1,528,705 |

0% |

|

Counseling Services |

24,638,372 |

4,202,730 |

28,841,102 |

1% |

|

Day Care—Adults |

25,892,717 |

16,652 |

25,909,369 |

1% |

|

Day Care—Children |

62,634,401 |

237,124,614 |

299,759,015 |

11% |

|

Education and Training Services |

5,433,799 |

4,295,153 |

9,728,952 |

0% |

|

Employment Services |

6,021,571 |

457,795 |

6,479,366 |

0% |

|

Family Planning Services |

6,379,137 |

0 |

6,379,137 |

0% |

|

Foster Care Services—Adults |

29,602,434 |

4,943,573 |

34,546,007 |

1% |

|

Foster Care Services—Children |

118,479,349 |

308,450,599 |

426,929,948 |

16% |

|

Health-Related Services |

15,042,505 |

5,562,985 |

20,605,490 |

1% |

|

Home-Based Services |

143,182,396 |

5,935,690 |

149,118,086 |

5% |

|

Home-Delivered Meals |

22,806,553 |

9,747 |

22,816,300 |

1% |

|

Housing Services |

9,558,308 |

3,900,324 |

13,458,632 |

1% |

|

Independent/Transitional Living |

8,298,004 |

672,476 |

8,970,480 |

0% |

|

Information and Referral |

17,485,504 |

3,690,643 |

21,176,147 |

1% |

|

Legal Services |

16,063,332 |

579,734 |

16,643,066 |

1% |

|

Pregnancy and Parenting |

6,499,323 |

18,291 |

6,517,614 |

0% |

|

Prevention and Intervention |

61,179,799 |

145,060,520 |

206,240,319 |

8% |

|

Protective Services—Adults |

189,847,125 |

1,201,091 |

191,048,216 |

7% |

|

Protective Services—Children |

138,522,061 |

190,095,391 |

328,617,452 |

12% |

|

Recreation Services |

871,896 |

78,455 |

950,351 |

0% |

|

Residential Treatment |

58,029,683 |

33,738,670 |

91,768,353 |

3% |

|

Special Services—Disabled |

199,910,492 |

77,311,767 |

277,222,259 |

10% |

|

Special Services—Youth at Risk |

62,524,745 |

3,719,156 |

66,243,901 |

2% |

|

Substance Abuse Services |

13,154,438 |

297,693 |

13,452,131 |

0% |

|

Transportation |

19,121,351 |

3,427,742 |

22,549,093 |

1% |

|

Other Services |

104,170,488 |

45,593,646 |

149,764,134 |

5% |

|

Administrative Costs |

58,260,185 |

4,511,368 |

62,771,553 |

2% |

|

Total SSBG Expenditures |

1,572,971,258 |

1,162,717,846 |

2,735,689,104 |

100% |

Source: Prepared by CRS based on data included in the Social Services Block Grant Program Annual Report 2014 (note that TANF transfer data from this source may differ from data in TANF financial reports, as shown in Table 1). Full report available athttp://www.acf.hhs.gov/ocs/resource/ssbg-annual-report-fy-2014.

Note: Totals may not sum due to rounding.

a. In this column, 0% represents a value that rounded to less than 1%.

Recent Legislative Action

Other than appropriations legislation, no bills in the 109th Congress or 110th Congress that proposed changes to the SSBG were enacted into law. Notably, however, several bills from the 109th Congress included proposals that, if enacted, would have increased funding for the SSBG (see S. 6, S. 667, and H.R. 751 from the 109th Congress).

Subsequently, several bills (S. 795, H.R. 2006, S. 1796, H.R. 3590) were introduced in the 111th Congress that sought to amend Title XX of the Social Security Act (SSA)—the authorizing statute for the SSBG—to establish new programs to address the prevention, detection, and treatment of elder abuse or elder justice. Ultimately, the health care reform legislation passed by Congress in March 2010 included three provisions amending Title XX of the SSA (addressed briefly below), including one on elder justice.

Separately, there have been several proposals in recent Congresses to reduce or eliminate funding for the SSBG. In the 114th Congress, for instance, the House Committee on Ways and Means reported out a bill (H.R. 4724) to repeal the SSBG. Previously, in the 112th Congress, a bill containing similar provisions (H.R. 5652) passed the House, but the measure was not taken up in the Senate. There have also been calls to repeal the SSBG in the 112th, 113th, and 114th Congresses associated with various budget resolutions adopted by the House, and as part of the House Budget Committee's July 2014 discussion draft on Expanding Opportunity in America.16 However, none of these activities have received the attention H.R. 5652 received in the 112th Congress and, as such, are not discussed here.

Proposal to Repeal the SSBG in the 112th Congress

On May 10, 2012, the House passed the Sequester Replacement Reconciliation Act of 2012 (H.R. 5652 in the 112th Congress) by a recorded vote of 218-199. This bill included a provision (§621) that, if enacted, would have repealed the SSBG, effective October 1, 2012. However, the Senate did not take up this measure prior to the end of the 112th Congress.

The Sequester Replacement Reconciliation Act of 2012 was a budget reconciliation bill. Budget reconciliation is an optional process that may be used by Congress to bring existing spending, revenue, and debt-limit laws into compliance with fiscal priorities established in the annual budget resolution.17 The FY2013 House budget resolution included a reconciliation directive in Section 201. To comply with this directive, on April 18, 2012, the House Ways and Means Committee marked up legislation to meet its deficit reduction targets. This legislation included a provision to repeal the SSBG that was agreed to by the committee by a vote of 22-14.18 The House Budget Committee compiled this legislation, along with submissions from other House committees, into the Sequester Replacement Reconciliation Act of 2012 and reported the bill out of committee (H.Rept. 112-470) on May 9, 2012.19

The report accompanying the Sequester Replacement Reconciliation Act of 2012 (H.Rept. 112-470) included text explaining the decision to repeal the SSBG.20 The report called the SSBG a duplicative funding stream lacking in focus and accountability. The report also criticized the SSBG for not requiring states to match federal SSBG allotments. Committee reports accompanying House budget resolutions for FY2012 and FY2013 included similar critiques of the SSBG and, in each year, recommended that the program be eliminated.21 Similar arguments had previously been made by the George W. Bush Administration in proposing, as part of annual budget requests, to reduce and eventually eliminate funding for the SSBG.22

The committee report accompanying H.R. 5652 also included a summary of dissenting views, which focused largely on how the elimination of the SSBG might affect the vulnerable individuals served by these funds.23 Similar concerns were raised by other critics of the proposal to eliminate the SSBG, such as the National Conference of State Legislatures (NCSL).24 The NCSL argued that the flexible nature of the SSBG allows states to address the needs of vulnerable populations and respond to local concerns, arguing that eliminating the SSBG might shift costs of such services directly to states.25

How Did Health Reform Affect the SSBG?

On March 23, 2010, President Obama signed into law a comprehensive health care reform bill, the Patient Protection and Affordable Care Act (ACA; P.L. 111-148). This law included three provisions that amended the SSBG's authorizing legislation, Title XX of the SSA. These provisions, discussed briefly below, created new programs related to elder justice, the health care workforce, and environmental health hazards. Notably, these changes were primarily of technical importance with respect to the SSBG. That is, they affected statutory citations for the SSBG, but they did not substantively amend the provisions within Title XX that govern the SSBG itself.

New Subtitle on Elder Justice

The health reform law re-titled Title XX as Block Grants to States for Social Services and Elder Justice (formerly, Title XX was entitled Block Grants to States for Social Services). The law also divided Title XX into two subtitles: Subtitle A retained provisions related to the SSBG, while Subtitle B comprised a series of new provisions related to elder justice.26 The elder justice provisions established (1) an Elder Justice Coordinating Council; (2) an Advisory Board on Elder Abuse, Neglect, and Exploitation; (3) a new grant program for stationary and mobile forensic centers to develop forensic expertise pertaining to elder abuse, neglect, and exploitation; and (4) several new grant programs (and other activities) to promote elder justice.27

New Programs Authorized within the SSBG Subtitle of Title XX

The health care reform law (P.L. 111-148) also included provisions establishing two new sections within Subtitle A of Title XX. The first created two demonstration projects related to the health care workforce. The second called for HHS to establish a competitive grant program for the early detection of medical conditions related to environmental health hazards. The health reform law established these new programs within the SSBG subtitle of Title XX and subjected their funding to the same prohibited uses as SSBG funds (though the new law made two exceptions28 to this rule). However, these new programs do not substantively alter the SSBG itself. The funding for these programs was provided separately in the health reform law (through mandatory pre-appropriations) and is not subject to the SSBG allocation formula.

Appendix A. TANF Transfers to SSBG in FY2015

|

State |

Total Federal TANF Fundsa |

TANF Funds Transferred to SSBG |

Percent of TANF Funds Transferred to SSBG |

SSBG Allocation |

Total SSBG Funds With TANF Transfer |

|

Alabama |

93,315,207 |

9,331,520 |

10.00% |

23,961,439 |

33,292,959 |

|

Alaska |

44,607,376 |

4,460,737 |

10.00% |

3,644,153 |

8,104,890 |

|

Arizona |

200,141,298 |

20,014,130 |

10.00% |

32,849,106 |

52,863,236 |

|

Arkansas |

56,732,858 |

0 |

0.00% |

14,670,028 |

14,670,028 |

|

California |

3,653,771,968 |

365,119,521 |

9.99% |

190,019,689 |

555,139,210 |

|

Colorado |

136,056,690 |

13,605,669 |

10.00% |

26,116,035 |

39,721,704 |

|

Connecticut |

266,788,107 |

26,678,810 |

10.00% |

17,826,274 |

44,505,084 |

|

Delaware |

32,290,981 |

0 |

0.00% |

4,589,068 |

4,589,068 |

|

District of Columbia |

92,609,814 |

3,935,917 |

4.25% |

3,204,538 |

7,140,455 |

|

Florida |

562,340,120 |

56,234,011 |

10.00% |

96,926,273 |

153,160,284 |

|

Georgia |

330,741,739 |

6,723,084 |

2.03% |

49,532,575 |

56,255,659 |

|

Hawaii |

98,904,788 |

9,890,000 |

10.00% |

6,960,093 |

16,850,093 |

|

Idaho |

30,412,562 |

323,133 |

1.06% |

7,991,585 |

8,314,718 |

|

Illinois |

585,056,960 |

1,200,000 |

0.21% |

63,858,552 |

65,058,552 |

|

Indiana |

206,799,108 |

0 |

0.00% |

32,572,884 |

32,572,884 |

|

Iowa |

131,028,542 |

12,962,008 |

9.89% |

15,319,626 |

28,281,634 |

|

Kansas |

101,931,061 |

10,193,106 |

10.00% |

14,345,751 |

24,538,857 |

|

Kentucky |

181,287,668 |

0 |

0.00% |

21,788,094 |

21,788,094 |

|

Louisiana |

163,971,985 |

16,397,198 |

10.00% |

22,929,104 |

39,326,302 |

|

Maine |

78,120,889 |

0 |

0.00% |

6,584,580 |

6,584,580 |

|

Maryland |

229,098,032 |

22,909,803 |

10.00% |

29,389,964 |

52,299,767 |

|

Massachusetts |

459,371,116 |

45,937,110 |

10.00% |

33,177,268 |

79,114,378 |

|

Michigan |

775,352,858 |

77,535,285 |

10.00% |

49,053,988 |

126,589,273 |

|

Minnesota |

261,969,844 |

4,790,000 |

1.83% |

26,869,585 |

31,659,585 |

|

Mississippi |

86,767,577 |

8,676,758 |

10.00% |

14,827,833 |

23,504,591 |

|

Missouri |

217,051,740 |

21,701,176 |

10.00% |

29,961,804 |

51,662,980 |

|

Montana |

38,039,116 |

2,575,839 |

6.77% |

5,032,315 |

7,608,154 |

|

Nebraska |

56,833,778 |

0 |

0.00% |

9,262,496 |

9,262,496 |

|

Nevada |

43,907,516 |

0 |

0.00% |

13,831,096 |

13,831,096 |

|

New Hampshire |

38,521,261 |

936,937 |

2.43% |

6,560,572 |

7,497,509 |

|

New Jersey |

404,034,823 |

16,938,000 |

4.19% |

44,115,273 |

61,053,273 |

|

New Mexico |

110,578,100 |

0 |

0.00% |

10,337,060 |

10,337,060 |

|

New York |

2,442,930,602 |

181,119,543 |

7.41% |

97,413,396 |

278,532,939 |

|

North Carolina |

301,434,977 |

12,239,700 |

4.06% |

48,818,216 |

61,057,916 |

|

North Dakota |

26,399,809 |

0 |

0.00% |

3,585,961 |

3,585,961 |

|

Ohio |

727,968,260 |

72,796,826 |

10.00% |

57,358,120 |

130,154,946 |

|

Oklahoma |

145,281,442 |

14,528,144 |

10.00% |

19,087,806 |

33,615,950 |

|

Oregon |

166,798,629 |

0 |

0.00% |

19,481,884 |

19,481,884 |

|

Pennsylvania |

719,499,305 |

23,232,750 |

3.23% |

63,321,525 |

86,554,275 |

|

Rhode Island |

95,021,587 |

7,126,618 |

7.50% |

5,212,488 |

12,339,106 |

|

South Carolina |

99,967,824 |

0 |

0.00% |

23,669,547 |

23,669,547 |

|

South Dakota |

21,279,651 |

2,127,965 |

10.00% |

4,188,174 |

6,316,139 |

|

Tennessee |

191,523,797 |

0 |

0.00% |

32,201,475 |

32,201,475 |

|

Texas |

486,256,752 |

33,573,455 |

6.90% |

131,107,407 |

164,680,862 |

|

Utah |

75,609,475 |

7,560,947 |

10.00% |

14,380,030 |

21,940,977 |

|

Vermont |

47,353,181 |

4,735,318 |

10.00% |

3,106,293 |

7,841,611 |

|

Virginia |

158,285,172 |

15,825,500 |

10.00% |

40,947,988 |

56,773,488 |

|

Washington |

380,544,968 |

4,675,000 |

1.23% |

34,558,238 |

39,233,238 |

|

West Virginia |

110,176,310 |

11,017,631 |

10.00% |

9,192,045 |

20,209,676 |

|

Wisconsin |

313,896,001 |

15,443,200 |

4.92% |

28,467,435 |

43,910,635 |

|

Wyoming |

18,500,530 |

0 |

0.00% |

2,888,318 |

2,888,318 |

|

Total |

16,297,163,754 |

1,165,072,349 |

— |

1,567,095,047 |

2,732,167,396 |

Source: Table prepared by the Congressional Research Service (CRS) based on data reported by HHS. TANF financial data reflect FY2015 TANF funds transferred to the SSBG during FY2015, whereas SSBG data are FY2015 allocations. TANF financial data are point-in-time estimates based on reports retrieved on October 12, 2016, from http://www.acf.hhs.gov/programs/ofa/programs/tanf/data-reports. SSBG allocation data are from the FY2017 congressional justification for the HHS Administration for Children and Families, available at http://www.acf.hhs.gov/programs/olab/budget.

a. Amounts in this column reflect FY2015 state financial assistance grants and do not include contingency funds or tribal grants (see Table E.2 of FY2015 TANF financial data).

Appendix B. Recent Supplemental Appropriations

This appendix presents background and spending information on supplemental appropriations to the SSBG in FY2013, FY2008, and FY2006.

FY2013 Supplemental: Hurricane Sandy

On January 29, 2013, the President signed into law the Disaster Relief Appropriations Act, 2013 (P.L. 113-2), in response to Hurricane Sandy. This law reserved roughly $500 million ($474.5 million when accounting for sequestration) for the SSBG.29 The supplemental stipulated that these funds were to be used to address necessary expenses resulting from Hurricane Sandy, including social, health, and mental health services for individuals; and for repair, renovation, and rebuilding of health care facilities (including mental health facilities), child care facilities, and other social services facilities. The supplemental also included a provision giving states up to three years to expend these funds, one year longer than the SSBG's standard two-year expenditure period.

On March 28, 2013, HHS issued an information memorandum regarding the availability of these supplemental funds.30 According to this memorandum, five states were allocated supplemental funds based on their relative share of Hurricane Sandy Individual Assistance registrants, as reported by the Federal Emergency Management Agency (FEMA) on March 18, 2013. These states were Connecticut ($10.6 million), Maryland ($1.2 million), New Jersey ($226.8 million), New York ($235.4 million), and Rhode Island ($0.5 million).

HHS subsequently released a number of additional SSBG resources related to Hurricane Sandy, including two new information memoranda on reporting requirements, two rounds of Questions and Answers, copies of states' intended use plans, and various other resources.31 Of note, the most recent information memorandum (Transmittal No. 01-2015) revised the expenditure deadline for these funds to September 30, 2017, which represents an extension of two fiscal years from the previous deadline of September 30, 2015.32

Prior to the enactment of P.L. 113-2, the Obama Administration had submitted a request to Congress on December 7, 2012, for disaster relief to support states affected by Hurricane Sandy. As part of this request, the Administration called for Congress to provide $500 million in supplemental funding for the SSBG.33 On December 28, 2012, the Senate approved this request as part of a disaster supplemental package (introduced as an amendment to H.R. 1), with some special provisions not included in the President's request. However, the House took no action on this bill.

|

State |

Allocation ($) |

Percentage Spent |

|

Connecticut |

$10,569,192 |

48% |

|

Maryland |

1,185,675 |

63% |

|

New Jersey |

226,794,105 |

86% |

|

New York |

235,434,600 |

67% |

|

Rhode Island |

516,428 |

30% |

|

Total |

474,500,000 |

76% |

Source: Table prepared by the Congressional Research Service (CRS) based on data from HHS. Allocation data are available in SSBG Information Memorandum Transmittal No. 01-2013, March 28, 2013.

FY2008 Supplemental: Major Disasters of 2008 (and Hurricanes Katrina and Rita)

The first FY2009 CR (P.L. 110-329) included, as Division B, the Disaster Relief and Recovery Supplemental Appropriations Act of 2008. This law provided $600 million in supplemental funds for the SSBG in FY2008. These funds were appropriated on the last day of FY2008 and were not allotted to states by HHS until FY2009. The supplemental funds were appropriated for necessary expenses resulting from "major disasters" (as declared by the President and defined in Title IV of the Stafford Act) occurring during 2008, including hurricanes, floods, and other natural disasters. The appropriation also made these funds available for necessary expenses resulting from Hurricanes Katrina and Rita.

The appropriations language specified that in addition to other uses permitted by Title XX of the Social Security Act, states could use their supplemental SSBG funds to provide social and health services (including mental health services) for individuals, as well as to support the repair, renovation, or construction of health care facilities, mental health facilities, child care centers, and other social services facilities affected by related disasters.

Allocation of Funds

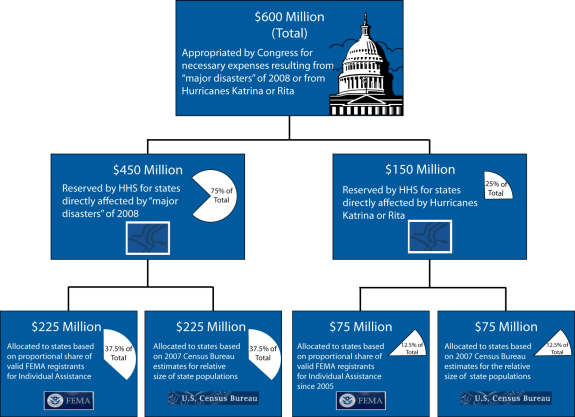

The appropriations language explicitly required HHS to distribute funding to eligible states based on "demonstrated need in accordance with objective criteria that are made available to the public." HHS outlined their criteria in Information Memorandum Transmittal No. 02-2009, FY2008 SSBG Supplemental Appropriation of Disaster Assistance Funds Awarded in FY2009, which was issued by the Department on January 6, 2009.34 Figure B-1 illustrates how the criteria selected by HHS were used to allocate funds to states.

|

Figure B-1. HHS Allocation Methodology for the FY2008 SSBG Supplemental Funding |

|

|

Source: Figure prepared by the Congressional Research Service based on data from HHS. |

As specified in the Information Memorandum, HHS identified criteria to determine which disasters qualified for supplemental SSBG funds. First, HHS specified that qualifying major disasters were those that occurred between January 1, 2008, and the date of enactment of the supplemental appropriation (September 30, 2008); in addition, Hurricanes Katrina and Rita were considered to qualify automatically based on appropriations language. Second, HHS restricted qualifying disasters to those which triggered authorizations for Federal Emergency Management Agency (FEMA) Individual Assistance. The FEMA Individual Assistance program provides money or direct assistance to individuals, families, and businesses in an affected area whose property has been damaged or destroyed and whose losses are not covered by insurance. HHS chose Individual Assistance data to serve as a proxy for "demonstrated need," noting that these data represent individual households that have declared a loss associated with the disaster and who have registered for assistance.

Twenty states (including the Commonwealth of Puerto Rico) were directly affected by qualifying disasters in 2008, as determined by the HHS criteria. Based on these same criteria, four states were deemed to be eligible for supplemental funds as a result of the lasting effects of Hurricanes Katrina and Rita (all but one of these states had also been affected by disasters in 2008). In total, 21 states (including Puerto Rico) were eligible to receive some share of the $600 million in supplemental funds under the HHS methodology.

As shown in Figure B-1, the HHS methodology called for three-fourths of the supplemental funds ($450 million) to be reserved for the states that were directly affected by major disasters occurring in 2008. One-fourth of the supplemental ($150 million) was then dedicated to the states facing ongoing needs as a result of Hurricanes Katrina and Rita. From there, funds in each category were allocated to states using two equally weighted sets of data: (1) the proportional share of FEMA registrants for Individual Assistance (that is, individuals from affected communities who validly registered with FEMA after the natural disaster), and (2) the relative size of state populations according to 2007 data from the Census Bureau's American Community Survey. Table B-2 displays the amount allocated to each state.

Expenditure of Funds

Typically, SSBG funds are subject to a two-year expenditure period—meaning that funds must be spent by the end of the fiscal year subsequent to the fiscal year in which they were allotted to states.35 The funds from this supplemental were allotted to states in FY2009, giving states until the last day of FY2010 (September 30, 2010) to spend them. However, most states had not spent all of their supplemental funds by the end of FY2010. Recognizing this, Congress passed a bill (S. 3774), which the President signed into law (P.L. 111-285) on November 24, 2010, extending the expenditure deadline for these funds by one fiscal year (to September 30, 2011).36

According to expenditure data from HHS, states spent more than $522 million (or 87%) of the $600 million in supplemental funds prior to the extended expenditure deadline. As shown in Table B-2, six states (Alabama, Indiana, Kentucky, Louisiana, Maine, and Mississippi) spent all of the supplemental funds they were allotted, while two states (Oklahoma and West Virginia) spent none. The remaining states (plus Puerto Rico) spent some portion of their funds, ranging from 3.5% of Arkansas's allotment to 99.8% of Texas's.

Table B-2. State Allocations and Spending from the FY2008 SSBG Supplemental

(As of October 27, 2013)

|

State |

Allocation ($) |

Percentage Spent |

|

Alabama |

13,092,588 |

100.0% |

|

Arkansas |

7,386,653 |

3.5% |

|

Colorado |

8,931,072 |

26.4% |

|

Florida |

35,384,592 |

43.3% |

|

Georgia |

18,111,127 |

22.6% |

|

Illinois |

30,502,439 |

87.6% |

|

Indiana |

18,139,459 |

100.0% |

|

Iowa |

11,157,944 |

100.0% |

|

Kentucky |

7,732,381 |

100.0% |

|

Louisiana |

129,737,880 |

100.0% |

|

Maine |

2,425,722 |

100.0% |

|

Mississippi |

28,136,577 |

100.0% |

|

Missouri |

12,188,291 |

99.6% |

|

Nebraska |

3,570,592 |

57.1% |

|

Nevada |

4,640,930 |

68.3% |

|

Oklahoma |

6,540,619 |

0.0% |

|

Puerto Rico |

12,427,602 |

71.3% |

|

Tennessee |

11,689,137 |

64.2% |

|

Texas |

218,852,848 |

99.8% |

|

West Virginia |

3,386,574 |

0.0% |

|

Wisconsin |

15,964,973 |

67.7% |

|

Total |

600,000,000 |

87.0% |

Source: Table prepared by the Congressional Research Service (CRS) based on data from HHS.

FY2006 Supplemental: Gulf Coast Hurricanes of 2005

The FY2006 Defense Appropriations Act (P.L. 109-148) included supplemental SSBG funding in the amount of $550 million. These funds were for expenses related to the consequences of the Gulf Coast hurricanes of 2005. The Defense Appropriations Act expanded the potential services for which the additional $550 million could be used to include "health services (including mental health services) and for repair, renovation and construction of health facilities."

Allocation of Funds

Factors used to allocate these supplemental funds included the number of FEMA registrants from hurricanes Katrina, Rita, and Wilma, as well as the percentage of individuals in poverty in each state. HHS distributed funds to all states that took in evacuees, not just the states that were directly affected, noting in a February 8, 2006, press release that the Bush Administration had promised no state would be unfairly disadvantaged for providing services to those affected by the storms.37 Although all states received a portion, Louisiana ($221 million), Mississippi ($128 million), Texas ($88 million), Florida ($54 million), and Alabama ($28 million) received the bulk of funding from the supplemental (94%).

Expenditure of Funds

On May 25, 2007, an FY2007 supplemental appropriations act was signed into law (P.L. 110-28), extending the availability of the supplemental SSBG funds for expenditure through the end of FY2009. In practical terms, this provision gave states until September 30, 2009, to spend all of their supplemental funds.38 According to HHS, states failed to spend approximately $28.7 million (or 5%) of the $550 million in supplemental funds prior to the expenditure deadline. This means that about 95% of the supplemental funds were spent prior to the close of FY2009 (see Table B-3 for state-by-state data). Unspent funds were to revert to the U.S. Treasury.

The 2009 SSBG annual report (most recent available) indicates that states spent supplemental funds on 28 of the 29 SSBG service categories defined in federal regulation, including education and training, counseling services, and health-related services.39 The report shows that most of the supplemental funds were spent in the "other services" category, including expenditures for certain construction and renovation costs, as well as costs for certain health and mental health services.

|

State |

Allocation ($) |

Percentage Spent |

|

Alabama |

27,852,254 |

99.94% |

|

Alaska |

37,554 |

0.00% |

|

Arizona |

487,931 |

62.55% |

|

Arkansas |

3,603,505 |

22.84% |

|

California |

3,051,021 |

36.22% |

|

Colorado |

545,168 |

79.30% |

|

Connecticut |

113,858 |

100.00% |

|

Delaware |

39,178 |

100.00% |

|

District of Columbia |

328,256 |

100.00% |

|

Florida |

53,808,916 |

69.44% |

|

Georgia |

6,325,537 |

80.31% |

|

Hawaii |

34,153 |

0.00% |

|

Idaho |

35,224 |

63.68% |

|

Illinois |

1,351,677 |

99.78% |

|

Indiana |

381,125 |

39.22% |

|

Iowa |

126,200 |

65.16% |

|

Kansas |

191,975 |

100.00% |

|

Kentucky |

525,110 |

100.00% |

|

Louisiana |

220,901,534 |

99.92% |

|

Maine |

67,995 |

100.00% |

|

Maryland |

380,188 |

99.50% |

|

Massachusetts |

331,948 |

14.32% |

|

Michigan |

734,927 |

81.65% |

|

Minnesota |

153,936 |

44.04% |

|

Mississippi |

128,398,427 |

100.00% |

|

Missouri |

797,091 |

100.00% |

|

Montana |

41,786 |

0.00% |

|

Nebraska |

114,925 |

100.00% |

|

Nevada |

273,291 |

20.27% |

|

New Hampshire |

23,717 |

0.00% |

|

New Jersey |

259,599 |

100.00% |

|

New Mexico |

265,277 |

0.00% |

|

New York |

1,182,346 |

0.00% |

|

North Carolina |

1,310,272 |

55.87% |

|

North Dakota |

13,009 |

100.00% |

|

Ohio |

556,283 |

10.66% |

|

Oklahoma |

932,353 |

0.00% |

|

Oregon |

177,170 |

100.00% |

|

Pennsylvania |

402,568 |

89.71% |

|

Rhode Island |

69,382 |

100.00% |

|

South Carolina |

696,901 |

66.30% |

|

South Dakota |

21,624 |

100.00% |

|

Tennessee |

3,470,718 |

100.00% |

|

Texas |

87,951,690 |

100.00% |

|

Utah |

92,669 |

99.98% |

|

Vermont |

23,272 |

0.00% |

|

Virginia |

808,855 |

0.00% |

|

Washington |

326,206 |

100.00% |

|

West Virginia |

132,912 |

76.50% |

|

Wisconsin |

227,555 |

96.00% |

|

Wyoming |

20,932 |

0.00% |

|

Total |

550,000,000 |

94.78% |

Source: Table prepared by the Congressional Research Service (CRS) based on data from HHS.

Notes: These funds were appropriated in the FY2006 Defense Appropriations Act (P.L. 109-148). A supplemental appropriations act for FY2007 (P.L. 110-28) extended the expenditure deadline for these funds, giving states until the end of FY2009 (September 30, 2009) to spend their allotments. Under the Terms and Conditions of their grant agreements, states had 90 days after the end of the grant period to finalize spending for funds that were obligated as of September 30, 2009. The numbers above (reported on April 1, 2010) should reflect final expenditures from the FY2006 supplemental. By law, unspent funds revert to the U.S. Treasury.

Author Contact Information

Footnotes

| 1. |

See Section 2005(a) of the Social Security Act. |

| 2. |

The conference report for the DRA notes that the House version of the bill increased the maximum transfer to SSBG to 10%, while the Senate bill had no provision. The conference report recedes to the Senate with regard to the transfer authority. |

| 3. |

FY2015 TANF financial data are available at http://www.acf.hhs.gov/programs/ofa/programs/tanf/data-reports. Calculation is based on dollars transferred to the SSBG in FY2015 from the FY2015 TANF State Family Assistance Grant award. |

| 4. |

OMB Report to the Congress on the Joint Committee Reductions for Fiscal Year 2017, February 9, 2016, p. 6, https://www.whitehouse.gov/sites/default/files/omb/assets/legislative_reports/sequestration/jc_sequestration_report_2017_house.pdf. |

| 5. |

For a comprehensive discussion of the BCA, see CRS Report R41965, The Budget Control Act of 2011, by Bill Heniff Jr., Elizabeth Rybicki, and Shannon M. Mahan. |

| 6. |

The discretionary limits were later modified by the American Taxpayer Relief Act of 2012 (ATRA, P.L. 112-250) and the Bipartisan Budget Act of 2013 (BBA, Division A of P.L. 113-6). |

| 7. |

Ali Rogin, "Senate Zika Bill Falls Apart Largely over Planned Parenthood Objections," ABC News, June 28, 2016, http://abcnews.go.com/Politics/senate-zika-bill-falls-largely-planned-parenthood-objections/story?id=40193006. |

| 8. |

It is not clear whether public health departments or hospitals would have been able to subcontract with Planned Parenthood or other entities, though under the terms of the conference agreement it might have been possible for some states or territories to provide these funds to Planned Parenthood affiliated health centers that are eligible providers in a public health plan, such as Medicaid. However, there are cases in which this would not be possible. For instance, Puerto Rico's International Planned Parenthood Federation affiliate, Profamilias, does not receive Medicaid funding. |

| 9. |