Pension Benefit Guaranty Corporation (PBGC): A Primer

Changes from March 20, 2018 to March 21, 2019

This page shows textual changes in the document between the two versions indicated in the dates above. Textual matter removed in the later version is indicated with red strikethrough and textual matter added in the later version is indicated with blue.

Contents

- Pension Benefit Guaranty Corporation

- PBGC Administration

- PBGC Financing

- Premiums

- Requirements for PBGC Coverage

- Pension Benefit Guaranty

- Single-Employer Insurance Program

- Multiemployer Pension Insurance Program

- Current Financial Status

- Benefit Payments in the Single-Employer Insurance Program

- Finances of the Single-Employer Insurance Program

- Finances of the Multiemployer Insurance Program

- PBGC and the Federal Budget

- PBGC Trust Fund

- PBGC Revolving Funds

- Future Financial Condition

Figures

Tables

- Table 1. Pension Benefit Guaranty Corporation Premium Income

- Table 2. Number of Standard and Trusteed Pension Plan Terminations

- Table 3. Examples of PBGC Annual Maximum Benefits for Plans that Terminate in

20182019

- Table 4. PBGC Single and Multi-Employer Insurance Programs: Net Financial Position,

FY1998-FY2017FY1999-FY2018

- Table 5. PBGC Benefit Payments and Payees, FY2000-FY2015

- Table 6. PBGC Multiemployer Insurance Program: Financial Assistance to Pension Plans , FY1995 to FY2018

- Table A-1. PBGC Single-Employer Program Premium Levels

- Table A-2. PBGC Multiemployer Program Premium Levels

Appendixes

- Appendix. Historical PBGC Premium Rates

Summary

The Pension Benefit Guaranty Corporation (PBGC) is a federal agency established by the Employee Retirement Income Security Act of 1974 (ERISA; P.L. 93-406). It was created to protect the pensions of participants and beneficiaries covered by private sector defined benefit (DB) plans. These pension plans provide a specified monthly benefit at retirement, usually either a percentage of salary or a flat dollar amount multiplied by years of service. Defined contribution (DC) plans, such as 401(k) plans, are not insured. PBGC is chaired by the Secretary of Labor, with the Secretaries of the Treasury and Commerce serving as board members.

PBGC runs two distinct insurance programs: one for single-employer pensions and a second for multiemployer plans. Single-employer pension plans are sponsored by one employer and cover eligible workers employed by the plan sponsor. Multiemployer plans are collectively bargained plans to which more than one company makes contributions. PBGC maintains separate reserve funds for each program.

A firm must be in financial distress to end an underfunded single-employer plan and for PBGC to become the trustee of the plan. Multiemployer plans do not terminate. When a multiemployer plan becomes insolvent and is not able to pay promised benefits, PBGC provides financial assistance to the plan in the form of loans, although PBGC does not expect the loans to be repaid.

In FY2017FY2018, PBGC insured about 2425,000 DB pension plans covering approximately 4037 million people. PBGC became the trustee of 8258 newly terminated single-employer pension plans and began providing financial assistance to an additional 76 multiemployer pension plans. PBGC paid benefits to nearly 840,000861,371 participants in 4,919 single-employer pension plans and more than 63,00062,300 participants in 7278 multiemployer plans.

There is a statutory maximum benefit that PBGC can pay. Participants receive the lower of their benefit as calculated under the plan or the statutory maximum benefit. If a participant's benefit is higher than the statutory maximum benefit, the participant's benefit is reduced. Participants in single-employer plans that terminate in 20182019 and are trusteed by PBGC may receive up to $65,04567,295 per year if they begin taking their pension at the age of 65. The single-employer maximum benefit is adjusted depending on the age at which the participant begins taking the benefit and on the form of the benefit (e.g., the maximum benefit is lower for a joint-and-survivor annuity). The maximum benefit for participants in multiemployer plans that receive financial assistance depends on the number of years of service in the plan. For example, a participant with 30 years of service may receive up to $12,870 per year. MostCurrently, most workers in single-employer plans taken over by PBGC and multiemployer plans that receive financial assistance from PBGC receive the full pension benefit that they earned.

At the end of FY2017, PBGC had a total deficit of $7651.4 billion, which consisted of a $2.4of which $10.9 billion wassurplus from the single-employer program and $65.1a $53.9 billion wasdeficit from the multiemployer program. PBGC's single-employer program has been on the Government Accountability Office's (GAO's) list of high-risk government programs since 2003. PBGC's multiemployer program was added in 2009. PBGC's projections expect projects the financial position of the single-employer program to improve slightly, but the financial position of the multiemployer program is expected to worsen considerably over the next 10 years.

Pension Benefit Guaranty Corporation

The Pension Benefit Guaranty Corporation (PBGC) is a federal agency established by the Employee Retirement Income Security Act of 1974 (ERISA; P.L. 93-406). It was created to protect the pensionspensions of participants and beneficiaries covered by private sector defined benefit (DB) plans. These pension plans provide a specified monthly benefit at retirement, usually either a percentage of salary or a flat dollar amount multiplied by years of service. Defined contribution (DC) plans, such as 401(k) plans, are not insured.1

PBGC runs two distinct insurance programs: one for single-employer pension plans and a second for multiemployer plans. Single-employer pension plans are sponsored by one employer and cover eligible workers employed by the plan sponsor. Multiemployer plans are collectively bargained plans to which more than one company makes contributions. PBGC maintains separate reserve funds for each program.

In FY2017FY2018, PBGC insured nearly 24about 25,000 DB pension plans covering about 4037 million people. It paid or owed benefits to 1.54 million people.2 PBGC is the trustee of 4,845919 single-employer plans. PBGC provided financial assistance to 7278 multiemployer pensions. PBGC pays a maximum benefit to plan participants.3 Most workers in single-employer plans taken over by PBGC and multiemployer plans that receive financial assistance from PBGC receive the full pension benefit that they earned.

PBGC Administration

PBGC is a government-owned corporation. A three-member board of directors, chaired by the Secretary of Labor, administers the corporation. The Secretary of Commerce and the Secretary of the Treasury are the other members of the board of directors. The Director of PBGC is appointed by the President with the advice and consent of the Senate. ERISA also provides for a seven-member Advisory Committee, appointed by the President, for staggered three-year terms. The Advisory Committee advises PBGC on issues, such as investment of funds, plan liquidations, and other matters.

The Moving Ahead for Progress in the 21st Century Act (MAP-21; P.L. 112-141) altered some of the governance structures of PBGC. Some of these changes include setting the term of the PBGC Director at five years, unless removed by the President or by the board of directors; requiring that the Board of Directors meet at least four times each year; and establishing a Participant and Plan Sponsor Advocate within PBGC to act as a liaison between PBGC, participants in plans trusteed by PBGC, and the sponsors of pension plans insured by PBGC.

PBGC Financing

PBGC is required by ERISA to be self-supporting and receives no appropriations from general revenue. ERISA states that the "United States is not liable for any obligation or liability incurred by the corporation,"25 and some Members of Congress have expressed a reluctance to consider providing financial assistance to PBGC.36 The most reliable source of PBGC revenue is the premiums set by Congress and paid by the private-sector employers that sponsor DB pension plans. Other sources of income are assets from terminated plans taken over by PBGC, investment income, and recoveries collected from companies when they end underfunded pension plans. The Multiemployer Pension Plan Amendments Act of 1980 (P.L. 96-364) requires that PBGC's receipts and disbursements be included in federal budget totals.

Premiums

The sponsors of private-sector pension plans pay a variety of premiums to PBGC. The sponsors of single-employer and multiemployer pension plans pay a flat-rate, per-participant premium. The sponsors of underfunded single-employer pension plans pay an additional premium that is based on the amount of plan underfunding. In addition, pension plans that are terminated in certain situations pay a per-participant premium per year for three years after termination.

The premiums for 20182019 are as follows:

- Single-employer flat-rate premium: The sponsors of single-employer DB pension plans pay an annual premium of $

7480 for each participant in the plan. - Single-employer variable-rate premium: In addition to the flat-rate premium, the sponsors of underfunded single-employer DB pension plans pay an additional annual premium of $

3843 for each $1,000 of unfunded vested benefits.47 There is a per-participant limit of $523541 for this premium. - Single-employer termination premium: The sponsors of single-employer DB pension plans that end in certain situations

58 pay an annual premium of $1,250 per participant per year for three years following plan termination.69

- Multiemployer flat-rate premium: The sponsors of multiemployer DB pension plans pay an annual premium of $

2829 for each participant in the plan in20182019.

In the Appendix, Table A-1 and Table A-2 provide a history of PBGC premium rates.

Table 1 details the amounts of premium income in FY2016 and FY2017FY2017 and FY2018.

Table 1. Pension Benefit Guaranty Corporation Premium Income

(FY2016 and FY2017FY2017 and FY2018 by type of premium in millions of dollars)

|

FY2016 |

FY2017 |

||||

|

Single-Employer |

|||||

|

Flat-Rate Premium |

|

|

|||

|

Variable-Rate Premium |

|

|

|||

|

Termination Premium |

|

|

|||

|

Multiemployer |

|||||

|

Flat-Rate Premium |

|

|

|||

Source: PBGC FY2017FY2018 Annual Report, Note 11: Premiums.

Requirements for PBGC Coverage

PBGC covers only those DB plans that meet the qualification requirements of Section 401 of the Internal Revenue Code (IRC).7 10 DC plans (such as 401(k) and 403(b) plans) are not insured by PBGC. Plans must meet these requirements to receive the tax benefits available to qualified pension plans. If a plan meets the requirements of IRC Section 401, the employer's contributions to the plan are treated as a tax-deductible business expense, and neither the employer's contributions to the plan nor the investment earnings of the plan are treated as taxable income to the participants. When a pension plan participant begins to receive income from the plan, it is taxed as ordinary income.

In general, to be qualified under the IRC, a pension plan must be established with the intent of being a permanent and continuing arrangement; must provide definitely determinable benefits;811 may not discriminate in favor of highly compensated employees with respect to coverage, contributions, or benefits; and must cover a minimum number or percentage of employees.

Pension plans specifically excluded by law from being insured by PBGC include governmental plans, church plans, plans of fraternal societies financed entirely by member contributions, plans maintained by certain professionals (such as physicians, attorneys, and artists) with 25 or fewer participants, and plans established and maintained exclusively for substantial owners of businesses.9 In addition, DC plans (such as 401(k) and 403(b) plans) are not insured by PBGC.

Pension Benefit Guaranty

PBGC's single-employer and multiemployer insurance programs operate differently and PBGC maintains separate reserve funds for each program. Funds from the reserve of one program may not be used for the other program.

In the single-employer program, PBGC becomes the trustee of the terminated, underfunded single-employer DB pension plans. The assets of the terminated plan are placed in a trust fund operated by PBGC. The participants in the trusteed plans receive their benefits from PBGC.

In the multiemployer program, PBGC does not become the trustee of plans. PBGC makes loans to multiemployer DB pension plans when the plans become insolvent. An insolvent multiemployer plan has insufficient assets available from which to pay participant benefits.

Single-Employer Insurance Program

An employer can voluntarily terminate a single-employer plan in either a standard or distress termination.1013 The participants and PBGC must be notified of the termination. PBGC may involuntarily terminate an underfunded plan if the sponsor is unable to fund its pension obligations.

Standard Terminations

A company may voluntarily end its pension plan if the plan's assets are sufficient to cover benefit liabilities. In such cases, PBGC does not pay any benefits to plan participants. Its role is to confirm that the requirements for termination have been met by the plan. Generally, benefit liabilities equal all benefits earned to date by plan participants, including vested and nonvested benefits (which automatically become vested at the time of termination), plus certain early retirement supplements and subsidies. Benefit liabilities also may include certain contingent benefits.1114 If assets are sufficient to cover benefit liabilities (and other termination requirements, such as notice to employees, have not been violated), the plan distributes benefits to participants. The plan provides for the benefit payments it owes by purchasing annuity contracts from an insurance company, or otherwise providing for the payment of benefits, for example, by providing the benefits in lump-sum distributions.

Assets in excess of the amounts necessary to cover benefit liabilities may be recovered by the employer in an asset reversion.1215 The asset reversion is included in the employer's gross income and is subject to a nondeductible excise tax. The excise tax is 20% of the amount of the reversion if the employer establishes a qualified replacement plan or provides certain benefit increases in connection with the termination. Otherwise, the excise tax is 50% of the reversion amount.

PBGC Trusteeship

When an underfunded plan terminates in a distress or involuntary termination, the plan goes into PBGC receivership. PBGC becomes the trustee of the plan, takes control of any plan assets, and assumes responsibility for liabilities under the plan. PBGC makes payments for benefit liabilities promised under the plan with assets received from two sources: (1) assets in the plan before termination and (2) assets recovered from employers. The balance, if any, of guaranteed benefits owed to beneficiaries is paid from PBGC's revolving funds.

Distress Terminations

If assets in the plan are not sufficient to cover benefit liabilities, the employer may not terminate the plan unless the employer meets one of four criteria necessary for a "distress" termination:

- 1. The plan sponsor, and every member of the controlled group (companies with the same ownership) of which the sponsor is a member, has filed or had filed against it a petition seeking liquidation in bankruptcy or any similar federal law or other similar state insolvency proceedings;

- 2. The plan sponsor, and every member of the sponsor's controlled group, has filed or had filed against it a petition to reorganize in bankruptcy or similar state proceedings. This criterion is also met if the bankruptcy court (or other appropriate court) determines that, unless the plan is terminated, the employer will be unable to continue in business outside the reorganization process and approves the plan termination;

- 3. PBGC determines that termination is necessary to allow the employer to pay its debts when due; or

- 4. PBGC determines that termination is necessary to avoid unreasonably burdensome pension costs caused solely by a decline in the employer's work force.

These requirements were added by the Single Employer Pension Plan Amendments Act of 1986 (SEPPAA; P.L. 99-272) and modified by the Omnibus Budget Reconciliation Act of 1987 (P.L. 100-203) and the Retirement Protection Act of 1994 (RPA; P.L. 103-465). They are designed to ensure that the liabilities of an underfunded plan remain the responsibility of the employer, rather than PBGC, unless the employer meets strict standards of financial need indicating genuine inability to continue funding the plan.

Involuntary Terminations

PBGC may terminate a plan involuntarily, either by agreement with the plan sponsor or pursuant to a federal court order. PBGC may institute such proceedings only if the plan in question has not met the minimum funding standards,

the plan will be unable to pay benefits when due,

the plan has a substantial owner who has received a distribution greater than $10,000 (other than by reason of death) and the plan has unfunded vested benefits, or

the long-run loss to PBGC with respect to the plan is expected to increase unreasonably if the plan is not terminated. PBGC must terminate a plan if the plan is unable to pay benefits that are currently due. A federal court may order termination of the plan to protect the interests of participants, to avoid unreasonable deterioration of the plan's financial condition, or to avoid an unreasonable increase in PBGC's liability under the plan.

Table 2 provides information on the number of terminations since 1974 by single-employer DB pension plans and the number of these terminations that resulted in PBGC becoming trustee of the pension plan. From FY1974 through FY2017FY2016, PBGC became the trustee of 4,845769 single-employer DB pension plans. The number of single-employer plan terminations that result in claims against PBGC is a relatively small fraction of all plan terminations. Most pension plan terminations are standard terminations.

|

Fiscal Year |

Number of Standard Termination Filings |

Trusteed Terminations |

||

|

1974-1979 |

7,955 |

586 |

||

|

1980-1984 |

28,025 |

622 |

||

|

1985-1989 |

42,599 |

537 |

||

|

1990-1994 |

24,171 |

694 |

||

|

1995-1999 |

15,089 |

444 |

||

|

2000-2004 |

7,493 |

714 |

||

|

2005 |

1,108 |

129 |

||

|

2006 |

1,247 |

89 |

||

|

2007 |

1,233 |

78 |

||

|

2008 |

1,405 |

83 |

||

|

2009 |

1,294 |

191 |

||

|

2010 |

1,308 |

156 |

||

|

2011 |

1,400 |

99 |

||

|

2012 |

1,332 |

117 |

||

|

2013 |

1,481 |

89 |

||

|

2014 |

1,373 |

52 |

||

|

2015 |

1,197 |

26

|

2016

|

1,225 36 |

|

Total |

139,710 |

4, |

Source: Table S-3 Pension Benefit Guaranty Corporation Pension Insurance Data Book, 20152016.

Notes: In a standard termination, a pension plan has sufficient assets from which to pay 100% of the participants' promised benefits. In a trusteed termination, PBGC becomes trustee of the plan and participants receive their benefits, up to a statutory maximum amount, from PBGC. Data for terminations in FY2016 and FY2017 isFY2017 and FY2018 are not yet available.

Employer Liability to PBGC

Following a distress or involuntary termination, the plan's sponsor and every member of that sponsor's controlled group are liable to PBGC for the plan's shortfall. The shortfall is measured as the value of the plan's liabilities as of the date of the plan's termination minus the fair market value of the plan's assets on the date of termination. The liability is joint and several, meaning that each member of the controlled group can be held responsible for the entire liability. Generally, the obligation is payable in cash or negotiable securities to PBGC on the date of termination. Failure to pay this amount upon demand by PBGC may trigger a lien on the property of the contributing employer's controlled group. Often, however, a plan undergoing a distress termination is sponsored by a company that is in bankruptcy proceedings, in which case PBGC does not have legal authority to create (or perfect) a lien against the plan sponsor. In such instances, PBGC has the same legal standing as other creditors of the plan sponsor, and its ability to recover assets is limited.

Benefit Payments

When an underfunded plan terminates, the benefits PBGC will pay depend on the statutory limit on guaranteed benefits, the amount of the terminated plan's assets, and recoveries by PBGC from the employer that sponsored the terminated plan.

Guaranteed Benefits

Within limits set by Congress, PBGC guarantees any retirement benefit that was nonforfeitable (vested) on the date of plan termination other than benefits that vest solely on account of the termination, and any death, survivor, or disability benefit that was owed or was in payment status at the date of plan termination. Generally, only that part of the retirement benefit that is payable in monthly installments (rather than, for example, lump-sum benefits payable to encourage early retirement) is guaranteed. Retirement benefits that commence before the plan's normal age of retirement are guaranteed, provided they meet the other conditions of guarantee. Contingent benefits (for example, early retirement benefits provided only if a plant shuts down) are guaranteed only if the triggering event occurs before plan termination. Following enactment of the Pension Protection Act of 2006 (PPA; P.L. 109-280), PBGC guarantee for such benefits is phased in over a five-year period commencing when the event occurs.13

Maximum Benefits for Participants in Single-Employer Pension Plans

ERISA sets a maximum on the individual benefit amount that PBGC can guarantee.14

The ceiling for single-employer plans is adjusted annually for national wage growth. The maximum pension guarantee is $65,04567,295 a year for workers aged 65 in plans that terminate in 20182019. This amount is adjusted annually and is decreased if a participant begins receiving the benefit before the age of 65 (reflecting the fact that they will receive more monthly pension checks over their expected lifetime) or if the pension plan provides benefits in some form other than equal monthly payments for the life of the retiree.1518 The benefit is increased if a participant begins receiving the benefit after the age of 65 (reflecting the fact that they will receive fewer monthly pension checks over their expected lifetime). Table 3 contains examples of PBGC's annual maximum benefit for individuals who begin receiving benefits at the ages of 60, 65, or 70 and who receive either a straight-life annuity or a joint and 50% survivor annuity.

|

Benefit Begins at Age |

|||

|

60 |

65 |

70 |

|

|

Straight-Life Annuity |

$ |

$ |

$ |

|

Joint and 50% Survivor Annuity, Assuming Both Spouses Are the Same Age |

$ |

$ |

$ |

Source: PBGC, Maximum Monthly Guarantee Tables, available at http://www.pbgc.gov/wr/benefits/guaranteed-benefits/maximum-guarantee.html.

The reduction in the maximum guarantee for benefits paid before the age of 65 is 7% for each of the first 5 years under age 65, 4% for each of the next 5 years, and 2% for each of the next 10 years.1619 The reduction in the maximum guarantee for benefits paid in a form other than a straight-life annuity depends on the type of benefit, and if there is a survivor's benefit, the percentage of the benefit continuing to the surviving spouse and the age difference between the participant and spouse.17

Only "basic benefits" are guaranteed. These include benefits beginning at normal retirement age (usually 65), certain early retirement and disability benefits, and benefits for survivors of deceased plan participants. Only vested benefits are insured. The average monthly benefit received by retirees in FY2015 was $606.1821 In a study released in 2008, PBGC indicated that more than 80% of PBGC recipients in single-employer plans trusteed by PBGC received their full benefits.19

Assets of a terminated plan are allocated to pay benefits according to a priority schedule established by statute. Under this schedule, some nonguaranteed benefits are payable from plan assets before certain guaranteed benefits. For example, benefits of participants who have been receiving pension payments for more than three years have priority over guaranteed benefits of participants not yet receiving payments.

PBGC also is required to pay participants a portion of their unfunded, nonguaranteed benefits based on a ratio of assets recovered from the employer to the amount of PBGC's claim on employer assets (called Section 4022(c) benefits).

Multiemployer Pension Insurance Program

In the case of multiemployer plans, PBGC insures plan insolvency, rather than plan termination. Accordingly, a multiemployer plan need not be terminated to qualify for PBGC financial assistance. A plan is insolvent when its available resources are not sufficient to pay the plan benefits for the plan year in question, or when the sponsor of a plan in reorganization reasonably determines, taking into account the plan's recent and anticipated financial experience, that the plan's available resources will not be sufficient to pay benefits that come due in the next plan year.

If it appears that available resources will not support the payment of benefits at the guaranteed level, PBGC will provide the additional resources needed as a loan, which PBGC indicates are rarely repaid.2023 PBGC may provide loans to the plan year after year. If the plan recovers from insolvency, it must begin repaying loans on reasonable terms in accordance with regulations. Only one multiemployer plan has repaid any of its financial assistance.21

Benefits for Participants in Multiemployer Pension Plans

PBGC guarantees benefits to multiemployer plans as it does for single-employer plans, although a different guarantee ceiling applies. Multiemployer plans determine benefits by multiplying a flat dollar rate by years of service, so the benefit guarantee ceiling is tied to this formula. The benefit guarantee limit for participants in multiemployer plans equals a participant's years of service multiplied by the sum of (1) 100% of the first $11 of the monthly benefit rate and (2) 75% of the next $33 of the benefit rate.2225 For a participant with 30 years of service, the guaranteed limit is $12,870.2326 This benefit formula is not adjusted for increases in the national wage index. PBGC estimated in 2015 that 79% of participants in multiemployer plans that receive financial assistance received their full benefit. However, in plans that may need financial assistance in the future, only 49% of participants would receive their full benefit payment.24

Current Financial Status

The most commonly used measure of PBGC's financial status is its net financial position, which is the difference between PBGC's assets and its liabilities. At the end of FY2017FY2018, PBGC's assets were $108.5112.3 billion, PBGC liabilities were $184.4163.7 billion, and its net financial position was -$76 51.4 billion.25

PBGC's main assets are the value of its trust fund and revolving funds.2630 The trust fund contains the assets of the pension plans of which PBGC becomes trustee and the returns on the trust fund investments. The revolving funds contain the premiums that plan sponsors pay to PBGC, transfers from the trust fund that are used to pay for participants' benefits, and returns on the revolving funds' investments in U.S. Treasury securities.

PBGC's main liabilities are the estimated present values of (1) future benefits payments in the single-employer program and (2) future financial assistance to insolvent plans in the multiemployer program.27

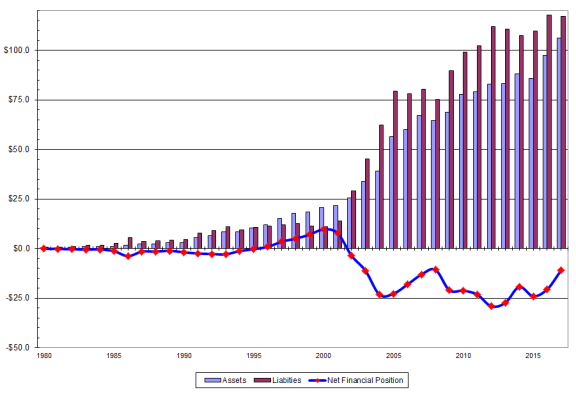

Table 4 provides information on the net financial position of PBGC from FY1998FY1999 through FY2017FY2018. PBGC has had an end of fiscal year deficit each year since FY2002.

Table 4. PBGC Single and Multi-Employer Insurance Programs: Net Financial Position, FY1998-FY2017

(billions of dollars)

|

Fiscal Year |

Single-Employer Program |

Multiemployer Program |

Total PBGC Surplus / Deficit |

|||||||

|

1998 |

|

|

| |||||||

1999 |

|

|

|

|||||||

|

2000 |

|

|

|

|||||||

|

2001 |

|

|

|

|||||||

|

2002 |

-3.6 |

0.2 |

-3.5 |

|||||||

|

2003 |

-11.2 |

-0.3 |

-11.5 |

|||||||

|

2004 |

-23.3 |

-0.2 |

-23.5 |

|||||||

|

2005 |

-22.8 |

-0.3 |

-23.1 |

|||||||

|

2006 |

-18.1 |

-0.7 |

-18.9 |

|||||||

|

2007 |

-13.1 |

-1.0 |

-14.1 |

|||||||

|

2008 |

-10.7 |

-0.5 |

-11.2 |

|||||||

|

2009 |

-21.1 |

-0.9 |

-21.9 |

|||||||

|

2010 |

-21.6 |

-1.4 |

-23.0 |

|||||||

|

2011 |

-23.3 |

-2.8 |

-26.0 |

|||||||

|

2012 |

-29.1 |

-5.2 |

-34.3 |

|||||||

|

2013 |

-27.4 |

-8.3 |

-35.7 |

|||||||

|

2014 |

-19.3 |

-42.4 |

-61.7 |

|||||||

|

2015 |

-24.0 |

-52.3 |

-76.3 |

|||||||

|

2016 |

-20.6 |

-58.8 |

-79.4 |

|||||||

|

2017 |

-10.9 |

-65.1 |

-76.0 |

|||||||

|

2018 |

2.4 |

-53.9 |

-51.4 |

|||||||

Source: PBGC Pension Insurance Data Books and FY 2017FY2018 Annual Reports.

The weakness in the economy in 2001, particularly in the steel and airline industries, led to large and expensive plan terminations that created a deficit for PBGC. By the end of 2004, the single-employer program had a deficit of $23.3 billion. The multiemployer program had a surplus from FY1982 to FY2002, but PBGC reported deficits each year since. Some policymakers are concerned with the financial condition of the multiemployer program.28For the first time since FY2001, partly as a result of increases to the premiums that employers pay, the single-employer program showed a surplus in FY2018.32

The multiemployer program had a surplus from FY1982 to FY2002, but PBGC reported deficits each year since. PBGC projects that the multiemployer program will be likely become insolvent in FY2025 and there is a less than 1% chance that the program will remain solvent in FY2026. Both the single-employer and multiemployer programs are on the Government Accountability Office's (GAO's) list of high-risk government programs.29

Benefit Payments in the Single-Employer Insurance Program

Table 5 shows that approximately 828825,000 participants received monthly payments from PBGC in FY2015 (the most recent year for which comprehensive data on benefit payments are available).3034 The average monthly payment was $536 and the median monthly payment was $279. Among retiree payees, the average monthly benefit was $606 and among beneficiary payees, the average monthly benefit was $309.31307.35 Approximately 40,000 participants received a lump-sum payment in FY2015, and the average amount of the lump-sum payment was $2,054.32

|

Periodic Pension Payments |

Lump-Sum Payments |

|||||||||||||||

|

Fiscal Year |

Annual Total |

Number of Payees in Year (thousands) |

Average Monthly Payment |

Median Monthly Payment |

Annual Total |

Number of Payees in Year (thousands) |

Average Payment |

Number of Deferred Payees (thousands) |

||||||||

|

2000 |

|

|

|

|

|

|

|

|

||||||||

|

2001 |

|

|

|

|

|

|

|

|

||||||||

|

2002 |

|

|

|

|

|

|

|

|

||||||||

|

2003 |

|

|

|

|

|

|

|

|

||||||||

|

2004 |

|

|

|

|

|

|

|

|

||||||||

|

2005 |

|

|

|

|

|

|

|

|

||||||||

|

2006 |

|

|

|

|

|

|

|

|

||||||||

|

2007 |

|

|

|

|

|

|

|

|

||||||||

|

2008 |

|

|

|

|

|

|

|

|

||||||||

|

2009 |

|

|

|

|

|

|

|

|

||||||||

|

2010 |

|

|

|

|

|

|

|

|

||||||||

|

2011 |

|

|

|

|

|

|

|

|

||||||||

|

2012 |

|

|

|

|

|

|

|

|

||||||||

|

2013 |

|

|

|

|

|

|

|

|

||||||||

|

2014 |

|

|

|

|

|

|

|

|

||||||||

|

2015 |

|

|

|

|

|

|

|

|

||||||||

Source: Table S-20 Pension Benefit Guaranty Corporation Pension Insurance Data Book, 2015.

Notes: Deferred payees are participants who are owed, but not yet receiving, benefits under the plan. Data for FY2016 and FY2017 are not available. Due to rounding of individual items, the average monthly payment may not be exactly equal to the total payments divided by the number of payees. Average monthly payment is not equal to annual total payments divided by number of payees because some payees did not receive benefits for all 12 months in a year.

Finances of the Single-Employer Insurance Program

Figure 1 displays the net financial position of PBGC's single-employer program from FY1980 to FY2017FY2018. In FY1996, PBGC showed a surplus in its single-employer program for the first time in its history. That surplus peaked at $9.7 billion in FY2000, helped by the strong performance of the equity markets in the mid- and late 1990s.

Finances of the Multiemployer Insurance Program

Table 6 indicates that 72provides data on the number of plans that have received financial assistance and the annual amounts of the financial assistance from FY1995 to FY2018. Seventy-eight multiemployer plans received financial assistance in FY2017. The FY2017FY2018. The FY2018 annual report indicated that approximately 63,00062,300 multiemployer plan participants received financial assistance in FY2017FY2018 and that approximately 30,00027,800 participants will receive benefits in the future because they are in plans that are currently receiving financial assistance.33

Table 6. PBGC Multiemployer Insurance Program:

Financial Assistance to Pension Plans

|

Year |

Number of Plans Receiving Financial Assistance |

Total Amount of Financial Assistance (millions) |

||||||

|

1995 |

9 |

|

||||||

|

1996 |

12 |

|

||||||

|

1997 |

14 |

|

||||||

|

1998 |

18 |

|

||||||

|

1999 |

21 |

|

||||||

|

2000 |

21 |

|

||||||

|

2001 |

22 |

|

||||||

|

2002 |

23 |

|

||||||

|

2003 |

24 |

|

||||||

|

2004 |

27 |

|

||||||

|

2005 |

29 |

|

||||||

|

2006 |

33 |

|

||||||

|

2007 |

36 |

|

||||||

|

2008 |

42 |

|

||||||

|

2009 |

43 |

|

||||||

|

2010 |

50 |

|

||||||

|

2011 |

49 |

|

||||||

|

2012 |

49 |

|

||||||

|

2013 |

44 |

|

||||||

|

2014 |

53 |

|

||||||

|

2015 |

57 |

|

||||||

|

2016 |

65 |

|

||||||

|

2017 |

72 |

|

2018

|

78

|

Source: PBGC Pension Insurance Data Books and FY2016, FY2017, and FY2018 and FY2017 Annual Reports.

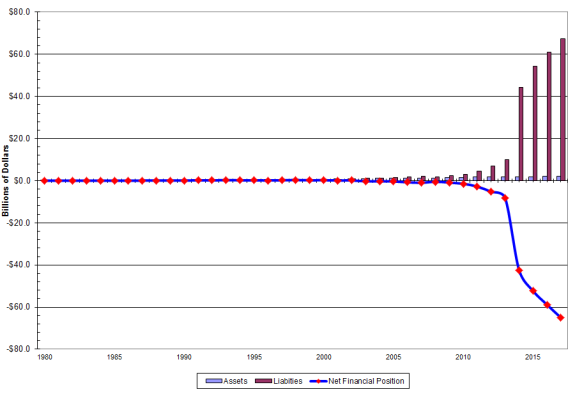

Figure 2 indicates that the financial condition of the multiemployer insurance program has been worsening. The deficit in the multiemployer insurance program increased from $8.3 billion in FY2013 to $42.4 billion in FY2014, and $65.1 billion in FY2017. It decreased to $53.8 billion in FY2018. The large increase in the deficit in FY2014 was the result of the increase in the likelihood of the insolvency of several large multiemployer pension plans in financial distress.

PBGC and the Federal Budget

PBGC's budgetary cash flows are based on its premium income, interest income, benefit outlays, and the interaction of PBGC's trust and revolving funds.34 The trust fund contains the assets of the pension plans of which PBGC becomes trustee and the returns on the trust fund investments. 39 Revolving funds contain the premiums that plan sponsors pay to PBGC, transfers from the trust fund that are used to pay for participants' benefits, and returns on the revolving funds' investments in U.S. Treasury securities.

PBGC Trust Fund

When PBGC becomes trustee of a single-employer pension plan, the assets of the terminated pension plan are transferred to PBGC and placed in a nonbudgetary trust fund.40 Transfers of assets to the trust fund do not appear in the federal budget and the assets of this trust fund do not appear on the federal balance sheet. The assets of the trust fund are managed by private-sector money managers in accordance with an investment policy established by PBGC's Board of Directors. The current investment policy establishes assets allocations of 30% for equities and other non-fixednonfixed income assets, and 70% for fixed income.3541 Trust fund investments totaled $69.170.2 billion at the end of FY2017.36

PBGC Revolving Funds

ERISA authorized the creation of seven revolving funds for PBGC, although only three revolving funds have been used by PBGC. The revolving funds contain the premiums paid by single-employer and multiemployer pension plan sponsors, returns on revolving funds' investments, and transfers from the trust fund that are used to pay benefits. Each year, PBGC transfers funds from the trust fund to the revolving funds to pay for a share of participants' benefits.37

The investments of the revolving funds are, by law, invested exclusively in U.S. Treasury securities. The revolving funds' assets at the end of FY2017FY2018 were $1.78 billion for Fund 1, $2.1 billion for Fund 2, and $26.129.3 billion for Fund 7, for a total of $29.933.2 billion.38

The revolving funds are on-budget accounts: increases or decreases in the revolving funds appear as on-budget federal receipts and outlays. The funds' gross outlays include PBGC benefit payments and administrative expenses and receipts include premiums paid, interest on federal securities, and reimbursements from the trust fund.

Because increases in the premiums paid by pension plan sponsors to PBGC are increases in federal revenue, some stakeholders and policymakers have criticized recent PBGC premium increases because they feel increases in premiums are used to offset other federal spending, do not address the financial condition of PBGC, and may discourage employers from maintaining their DB pension plans.39

Future Financial Condition

In its FY2016FY2017 Projections Report,4046 PBGC estimated its financial condition over the next 10 years. The report indicated that the single-employer program's deficit is likely to shrink and the multiemployer program is likely to run out of money. Although PBGC currently operates with a financial deficit, retirees' benefits in the single-employer program are not at immediate risk because the benefit obligations are paid out over several decades.

PBGC estimated in FY2025. PBGC projected that the single-employer program's deficit is likely to shrink over the next 4 years and that the program will show a surplus after that was likely to emerge from deficit by FY2018 (which it did). The average estimate of PBGC's simulations was a $9.626 billion surplus for the single-employer program in 10 years.41

PBGC estimatedprojected that there is a 7590% chance that the multiemployer program will be insolvent by 2025before the end of FY2025 and a 99% chance that the multiemployer program will be insolvent by 2035.422026.48 This is a result of the likely insolvency of several large multiemployer pension plans. PBGC's FY2017FY2018 Annual Report indicated that the multiemployer program's probable exposure to future financial assistance would be $62.753.8 billion.4349 Premium levels are likely inadequate to provide continued financial assistance to insolvent multiemployer plans. The financial assistance to these plans could exhaust PBGC's ability to guarantee participants' benefits. PBGC has indicated that once resources are exhausted in the PGBC's multiemployer program, insolvent plans would be required to reduce benefits to levels that could be sustained through premium collections only.44

The Multiemployer Pension Reform Act of 2014 (MPRA, enacted as part of P.L. 113-235), allowed, allows, among other provisions, multiemployer DB pension plans that expect to become insolvent to reduce benefits to participants in these plans. An insolvent plan has no assets from which to pay any benefits. Plans that reduce benefits to forestall insolvency would not require financial assistance from PBGC, and would reduce the amount of future financial assistance PBGC would expect to provide. This would likely improve PBGC's financial condition. PBGC indicated that there is uncertainty in how the provisions of MPRA that allow benefit suspensions and plan partitions will be used. PBGC estimated that the effect of MPRA would likely not change PBGC projections of future solvency.45

Appendix.

51

In response to the increasing concerns of policymakers and stakeholders (such as participants, participating employers, and plans), the Bipartisan Budget Act of 2018 (P.L. 115-123) created a new joint select committee of the House and Senate: The Joint Select Committee on Solvency of Multiemployer Pension Plans.52 The committee was tasked with formulating recommendations and legislative language by November 30, 2018, that would "significantly improve the solvency of multiemployer pension plans and the Pension Benefit Guaranty Corporation."53 The committee did not release a report containing recommendations or legislative language by the deadline.54

Appendix. Historical PBGC Premium RatesTable A-1 provides historical data on the single-employer program premium levels.

|

Authorizing Statute |

Flat-Rate Premium |

Variable-Rate Premium |

Termination Premium |

|||||

|

September 2, 1974-1977 |

Employee Retirement Income Security Act of 1974 |

$1.00 |

- |

- |

||||

|

1978-1985 |

Multiemployer Pension Plan Amendments Act of 1980 (MPPAA, P.L. 96-364) |

$2.60 |

- |

- |

||||

|

1986-1987 |

Consolidated Omnibus Budget Reconciliation Act of 1985 |

$8.50 |

- |

- |

||||

|

1988-1990 |

Omnibus Budget Reconciliation Act of 1987 |

$16.00 |

$6.00 |

- |

||||

|

1991-2005 |

Omnibus Budget Reconciliation Act of 1990 |

$19,00 |

$9.00 |

- |

||||

|

2006 |

Deficit Reduction Act of 2005 (P.L. 109-171)b |

$30.00 |

$9.00 |

$1,250.00c |

||||

|

2007 |

$31.00 |

$9.00 |

$1,250.00 |

|||||

|

2008 |

$33.00 |

$9.00 |

$1,250.00 |

|||||

|

2009 |

$34.00 |

$9.00 |

$1,250.00 |

|||||

|

2010-2012 |

$35.00 |

$9.00 |

$1,250.00 |

|||||

|

2013 |

MAP-21 (P.L. 112-141)d |

$42.00 |

$9.00 |

|

||||

|

2014 |

|

$14.00 |

$1,250.00 |

|||||

|

2015 |

Continuing Appropriations Resolution, 2014 (P.L. 113-67) |

|

$24.00 |

$1,250.00 |

||||

|

2016 |

|

|

$1,250.00 |

|||||

|

2017 |

Bipartisan Budget Act of 2015 (P.L. 114-74)e |

|

|

$1,250.00 |

||||

|

2018 |

|

|

$1,250.00 |

|||||

|

2019 |

|

|

$1,250.00 |

Source: Congressional Research Service (CRS).

a. The Employee Retirement Income Security Act of 1974 (ERISA; P.L. 93-406) established the initial premium rate of $1.00 per participant.

b. The Deficit Reduction Act of 2005 (P.L. 109-171) adjusted the flat-rate premium annually for increases in the national wage index beginning in 2007.

c. The Pension Protection Act of 2006 (PPA; P.L. 109-280) provided for a special termination premium of $2,500 per participant for pension plans of commercial airlines that terminated within a five-year period that began with the year that a commercial airline plan adopted funding rules made available to commercial airlines in the PPA.

d. MAP-21 (P.L. 112-141) increased the variable-rate premium by $4 (after the 2013 level is adjusted for changes in the national wage index) per $1,000 of unfunded benefits in 2014, and by another $5 (after the 2014 level is adjusted for changes in the national wage index) per $1,000 of unfunded vested benefits in 2015. The Continuing Appropriations Resolution, 2014 (P.L. 113-67) increased the variable-rate premium in 2015 by $10 (after the 2014 level is adjusted for changes in the national wage index) per $1,000 of unfunded benefit and by another $5 in 2016 (after the 2015 premium is adjusted for changes in the national wage index).

e. The Bipartisan Budget Act of 2015 (P.L. 114-74) increased the flat-rate premium to $69 in 2017, $74 in 2018, and $80 in 2019, and increased the variable-rate premium by $3 in 2017, an additional $4 in 2018, and an additional $4 in 2019.

f. The variable-rate premium in 2019 may be higher than $42 if the increase in the national wage index warrants a change in the premium.

Table A-2 provides historical data on the multiemployer program premium levels.

|

Year |

Authorizing Statute |

Premium Rate |

|

September 2, 1974-1980 |

Employee Retirement Income Security Act of 1974 |

$0.50 |

|

September 1, 1979-September 26, 1980 |

Multiemployer Pension Plan Amendments Act of 1980 |

$0.50-$1.00a |

|

September 27, 1980-September 26, 1984 |

$1.40 |

|

|

September 27, 1984-September 26, 1986 |

$1.80 |

|

|

September 27, 1986-September 26, 1988 |

$2.20 |

|

|

September 27, 1988-December 31, 2005 |

$2.60 |

|

|

2006-2007 |

Deficit Reduction Act of 2005 (P.L. 109-171) |

$8.00b |

|

2008-2012 |

$9.00 |

|

|

2013 |

MAP-21 (P.L. 112-141) |

$12.00 |

|

2014 |

$12.00 |

|

|

2015 |

The Multiemployer Pension Reform Act of 2014 (P.L. 113-235) |

$26.00 |

|

2016 |

$27.00 |

|

|

2017 |

$28.00 |

|

|

2018 |

$28.00 |

|

|

2019 |

$ |

Source: Table M-16 Pension Benefit Guaranty Corporation Pension Insurance Data Book, 2015.

a. $0.50 for plan year beginning in September 1979, growing gradually to $1.00 for plan years beginning September 1, 1980, to September 26, 1980.

b. From 2007 to 2012, this amount was adjusted annually based on the national average wage index and rounded to the nearest multiple of $1.

c. The multiemployer premium in 2019 may be higher than $42 if the increase in the national wage index warrants a change in the premium.

Author Contact Information

Acknowledgments

Emma Sifre provided research assistance to update this report.

Footnotes

| 1. |

These plans are authorized in §401(k) of the Internal Revenue Code. |

|||||

| 2. |

See Pension Benefit Guaranty Corporation (PBGC), PBGC Annual Report 2018, p. 30, https://www.pbgc.gov/sites/default/files/pbgc-annual-report-2018.pdf.

See Pension Benefit Guaranty Corporation (PBGC), PBGC Annual Report 2018, pp. 31-32, https://www.pbgc.gov/sites/default/files/pbgc-annual-report-2018.pdf. See Pension Benefit Guaranty Study, PBGC's Multiemployer Guarantee, March 2015, https://www.pbgc.gov/documents/2015-ME-Guarantee-Study-Final.pdf. |

|||||

|

For example, Chairman Phil Roe and then-Ranking Member Robert Andrews, of the Subcommittee on Health, Employment, Labor, and Pensions in the House Education and Workforce Committee, both expressed reservations about providing government financial assistance for PBGC. See U.S. Congress, House Committee on Education and the Workforce, Subcommittee on Health, Employment, Labor, and Pensions, Examining the Challenges Facing PBGC and Defined Benefit Pension Plans, 112th Cong., 2nd sess., February 2, 2012, 112-50 (Washington: GPO, 2012) and U.S. Congress, House Committee on Education and the Workforce, Subcommittee on Health, Employment, Labor, and Pensions, Strengthening the Multiemployer Pension System: What Reforms Should Policymakers Consider?, 113th Cong., 1st sess., June 12, 2013. |

||||||

|

Vested benefits are those benefits that a participant has earned a right to receive from a pension plan. Participants are entitled to their vested benefits even if they leave the pension plan or if the plan terminates. |

||||||

|

The termination premium applies to plans that end in distress terminations in which ERISA §4044(c) applies, unless certain conditions about the plan's sponsors apply. For more information, see Termination Premium Payment Package, including PBGC Form T, available from PBGC at http://www.pbgc.gov/documents/Form-T-package-2014.pdf. |

||||||

|

The termination premium was authorized in Deficit Reduction Act of 2005 (P.L. 109-171). The termination premium is $2,500 for airlines that chose the funding relief available under §402 of the Pension Protection Act of 2006 (PPA; P.L. 109-280) if the plan terminated within five years of choosing the funding relief. |

||||||

|

See 26 U.S.C. §401. |

||||||

|

See 25 U.S.C. §401(a)(25) and 26 |

||||||

|

See 29 U.S.C. §1321. |

||||||

|

More information is available in CRS Report RS22624, The Pension Benefit Guaranty Corporation and Single-Employer Plan Terminations |

||||||

|

Contingent benefits are benefits that are available when certain specified events occur. For example, a plan might provide "shutdown benefits," which are additional benefits should a plant or facility close. |

||||||

|

An asset reversion is cash and property received by the sponsor of a DB pension plan. See 26 U.S.C. §4980(c)(2). |

||||||

|

For example, PBGC pays 20% of a participant's shutdown benefit if the benefit was adopted within one year prior to plan termination. The percentage increases from year to year. If the benefit was adopted more than five years prior to plan termination, PBGC pays 100% of the participant's shutdown benefit. For more information, see PBGC, "Benefits Payable in Terminated Single-Employer Plans; Limitations on Guaranteed Benefits; Shutdown and Similar Benefits," 79 Federal Register 25667-25675, May 6, 2014. |

||||||

|

The maximum benefit is different for participants in terminated single-employer pension plans compared with participants in insolvent multiemployer pension plans. |

||||||

|

A straight-life annuity pays the monthly benefit until the participant dies. A joint and 50% survivor annuity provides a participant with fixed monthly lifetime benefit payments and, upon death, continues lifetime payments reduced by 50% to the spouse or other beneficiary. |

||||||

|

Further information on the maximum benefit is available in 29 C.F.R. §4022.23, Computation of Maximum Guaranteeable Benefits. |

||||||

|

A single life annuity is a benefit that pays an equal monthly benefit for the life of the participant. A survivor's annuity pays an equal monthly benefit for the longer of the life of the participant and the participant's spouse. The monthly payment in a survivor's annuity is typically less than the amount of the single life annuity. |

||||||

|

See Pension Benefit Guaranty Corporation, Pension Insurance Data Book, 2015, Table S-24, https://www.pbgc.gov/sites/default/files/2015-pension-data-tables.pdf. Data for the average benefit in 2016 are not available. |

||||||

|

PBGC studied 125 single-employer plans that were terminated prior to 2006. See Pension Benefit Guaranty Corporation, PBGC's Guarantee Limits—an Update, September 2008, http://www.pbgc.gov/docs/guaranteelimits.pdf. CRS is not aware of a more recent study regarding the percentage of participants who receive their full pension benefits. |

||||||

|

See Pension Benefit Guaranty Corporation (PBGC), PBGC Annual Report 2017, p. 41, https://www.pbgc.gov/sites/default/files/pbgc-annual-report-2017.pdf. |

||||||

|

See PBGC, 2015 Pension Insurance Data Tables, table M-4, https://www.pbgc.gov/sites/default/files/2015-pension-data-tables.pdf. |

||||||

|

An accrual rate is a factor in the pension benefit formula (expressed either as a dollar amount or as a percentage of salary) at which a pension benefit is earned. In single-employer pension plans, the pension benefits formula is typically expressed as the number of years participating in the plan times the accrual rate (e.g., 1% or 2%) times a measure of salary (e.g., the average of the participant's highest five years of salary). In multiemployer pension plans, the pension benefits formula is typically expressed as the number of months or years of service times a dollar amount. |

||||||

|

This is calculated as [30 × ((100% × $11) + (75% ×$33)] = $1,072.50 per month, which is $12,870 per year. |

||||||

|

See Pension Benefit Guaranty Study, PBGC's Multiemployer Guarantee, March 2015, https://www.pbgc.gov/documents/2015-ME-Guarantee-Study-Final.pdf. |

||||||

|

|

29.

The average monthly benefit in terminated plans that are likely to receive PBGC financial assistance was $383.33; in plans that were projected to become insolvent within 10 years it was $546.17; and in remaining, ongoing plans it was $1,010.44. See Pension Benefit Guaranty Corporation, PBGC's Multiemployer Guarantee, March 2015, Figure 4, https://www.pbgc.gov/documents/2015-ME-Guarantee-Study-Final.pdf. |

The dollar amounts do not sum because of rounding. As reported |

||||

|

Other assets include securities lending collateral and receivables. |

||||||

|

Other liabilities include payables. PBGC's benefit obligations are spread out over many years in the future. These future benefits are calculated and reported as current dollar values (also called present value). Benefits that are expected to be paid in a particular year in the future are calculated so they can be expressed as a current value. The process is called discounting and it is the reverse of the process of compounding, which projects how much a dollar amount will be worth at a point in the future. For more information, see the appendix in CRS Report R43305, Multiemployer Defined Benefit (DB) Pension Plans: A Primer |

||||||

|

|

||||||

|

More information is available at http://www.gao.gov/highrisk/pension_benefit/why_did_study. |

||||||

|

Table A-2 reports data from PBGC's Data Book. PBGC's FY2017 Annual Report indicated that approximately 840,000 participants were receiving monthly benefits at the end of FY2017. |

||||||

|

See Tables S-24 and S-25 Pension Benefit Guaranty Corporation Pension Insurance Data Book, 2015 https://www.pbgc.gov/sites/default/files/2015-pension-data-tables.pdf. |

||||||

|

See Table S-20 Pension Benefit Guaranty Corporation Pension Insurance Data Book, 2015 https://www.pbgc.gov/sites/default/files/2015-pension-data-tables.pdf. The data book does not provide similar information for multiemployer plans. In the multiemployer program, PBGC does not provide benefits directly to participants, but to the plans. |

||||||

|

See Pension Benefit Guaranty Corporation, |

||||||

|

For more information, see Congressional Budget Office, A Guide to Understanding the Pension Benefit Guaranty Corporation, September 2005, http://www.cbo.gov/sites/default/files/cbofiles/ftpdocs/66xx/doc6657/09-23-guidetopbgc.pdf. |

||||||

| 35. |

See Pension Benefit Guaranty Corporation, "PBGC Board of Directors Approves New Investment Policy," press release, May 26, 2011, http://www.pbgc.gov/news/press/releases/investment-policy.html. |

|||||

|

|

When PBGC becomes trustee of a single-employer pension plan, the plan typically has assets in it. These assets are transferred to PBGC trust fund. PBGC does not become trustee of multiemployer plans, so it does not take any multiemployer plan assets. 41.

|

|

See Pension Benefit Guaranty Corporation, "Pension Benefit Guaranty Corporation Investment Policy Statement – September 2016," https://www.pbgc.gov/documents/Investment-Policy-Statement.pdf. |

See Pension Benefit Guaranty Corporation, PBGC Annual Report |

||

|

A GAO report indicated that the formula for the transfer is net trust fund assets divided by the present value of future benefits excluding probable terminations. See GAO, Pension Benefit Guaranty Corporation: Asset Management Needs Better Stewardship, GAO-11-271, June 2011, http://www.gao.gov/new.items/d11271.pdf. |

||||||

|

See Pension Benefit Guaranty Corporation, PBGC Annual Report |

||||||

|

See, e.g., Rep. Jim Renacci, "Renacci, Pocan Introduce the Pension and Budget Integrity Act," press release, January 31, 2017, https://renacci.house.gov/index.cfm/press-releases?ID=1F1896CA-3D93-477C-8B71-0DDF8C672920.Sean Forbes, "House Approves Budget Agreement That Includes Hikes in PBGC Premiums," Pension & Benefits Reporter, December 17, 2013, or Interindustry Forecasting at the University of Maryland, Increasing. Pension. Premiums: The Impact on Jobs and Economic Growth, May 2014, http://www.nam.org/~/media/0948C22BD34742678A3DA9078EA28915/Increasing_Pension_Premiums_Full_Report_MAY2014.pdf. |

||||||

|

The Projections Report was formerly called the Exposure Report. It is available at http://www.pbgc.gov/about/projections-report.html. |

||||||

|

To estimate the likelihood of PBGC's future financial condition, PBGC uses an internally developed computer modelling program that it calls the Pension Insurance Modelling System (SIMS). Separate models are used for the single-employer program (SE-SIMS) and the multiemployer program (ME-SIMS). For more discussion of SIMS, see Jeffrey R. Brown, Douglas J. Elliott, and Tracy Gordon, et al., A Review of the Pension Benefit Guaranty Corporation Pension Insurance Modeling System, Brookings Institution, September 11, 2013, http://www.brookings.edu/research/papers/2013/09/11-review-pension-benefit-guaranty-corporation-pension. |

||||||

|

See |

||||||

|

Plans are classified as probable (for future financial assistance) if the plan is ongoing but is projected to be insolvent within 10 years. |

||||||

|

See Pension Benefit Guaranty Corporation, PBGC Insurance of Multiemployer Pension Plans, March, 2016, https://www.pbgc.gov/documents/Five-Year-Report-2016.pdf. |

||||||

|

This improvement in the deficit is not larger because the application by one of the largest multiemployer DB pension plans to reduce benefits was rejected by the U.S. Treasury in May 2016 and this plan is likely to become insolvent within 10 years. See Pension Benefit Guaranty Corporation, FY2016 Projections Report, |

||||||

| 52. |

See CRS Report R45107, Joint Select Committee on Solvency of Multiemployer Pension Plans: Structure, Procedures, and CRS Experts. |

|||||

| 53. |

For more information on the policy issues relevant to the work of the committee, see CRS Report R45311, Policy Options for Multiemployer Defined Benefit Pension Plans. |

|||||

| 54. |

See Joint Select Committee on Solvency of Multiemployer Pension Plans, "Hatch, Brown Commit to Continued Work on Pension Crisis Past Nov. 30," press release, November 29, 2018, https://www.pensions.senate.gov/content/hatch-brown-commit-continued-work-pension-crisis-past-nov-30. |