Tax-Preferred College Savings Plans: An Introduction to 529 Plans

Changes from March 5, 2018 to February 27, 2024

This page shows textual changes in the document between the two versions indicated in the dates above. Textual matter removed in the later version is indicated with red strikethrough and textual matter added in the later version is indicated with blue.

Contents

- Introduction

- Overview of 529 Plans

- Types of 529 Plans: Prepaid and Savings Plans

- Tax Treatment of 529 Plans

- Income Tax Treatment

- Contributions

- Distributions

- Calculating the Taxable Portion of a 529 Distribution: A Stylized Example

- Interaction with Other Education Tax Benefits

- Rollovers and Transfers

- Gift Tax

- Interaction of Assets and Distributions from 529 Plans with Federal Student Aid

Introduction

Tax-Preferred College Savings Plans: An

February 27, 2024

Introduction to 529 Plans

Brendan McDermott

Among the options families may choose to save for education (elementary and secondary as well

Analyst in Public Finance

as higher education), they may consider using tax-advantaged qualified tuition programs (QTPs),

also known as 529 plans.

529 plans, named for the section of the Internal Revenue Code (IRC) which dictates their tax treatment, are tax-advantaged investment trusts used to pay for education expenses. The specific tax advantage of a 529 plan is that distributions (i.e., withdrawals) from this savings plan are tax-free if they are used to pay for qualified higher-education expenses. In addition, up to $10,000 per beneficiary per year can be withdrawn and used for qualifying K-12 education expenses. If some or all of the distribution is used to pay for nonqualified expenses, then a portion of the distribution is taxable, and may also be subject to a 10% penalty tax.

There are two types of 529 plans: “prepaid” plans and “savings” plans. A 529 prepaid plan allows a contributor (i.e., a parent, grandparent, or nonrelative) to make lump-sum or periodic payments that entitle the beneficiary to a specified number of academic periods, course units, or a percentage of tuition costs at current prices. A 529 savings plan allows contributors to invest in a portfolio of mutual funds or other underlying investments.

While prepaid 529 plans were the first type of 529 plan established, savings plans have grown in popularity and are now the most common type of 529 plan. There are currently 17 prepaid 529 plans offered, in contrast to 94 savings plans. In addition, according to the most recent data, of the $432 billion worth of assets in 529 plans as of September 2023, 95% ($409 billion) were held in savings plans, while 5% ($23 billion) were held in prepaid plans.

This report provides an overview of the mechanics of 529 plans and examines the specific tax advantages of these plans. Specifically, this report is structured to first compare “savings” and “prepaid” 529 plans and, second, to examine the income and gift tax treatment of 529 plans, using a stylized example to illustrate key concepts. The report also examines the tax treatment of rollovers and the interaction of 529 plans with other education tax benefits and looks at how 529 plans are treated in the federal needs analysis for financial aid. Finally, the report summarizes recent legislative changes.

Congressional Research Service

link to page 4 link to page 4 link to page 5 link to page 8 link to page 10 link to page 10 link to page 10 link to page 11 link to page 12 link to page 13 link to page 13 link to page 13 link to page 13 link to page 14 link to page 14 link to page 12 link to page 7 link to page 16 Tax-Preferred College Savings Plans: An Introduction to 529 Plans

Contents

Introduction ..................................................................................................................................... 1 Overview of 529 Plans .................................................................................................................... 1 Types of 529 Plans: Prepaid and Savings Plans .............................................................................. 2 Tax Treatment of 529 Plans ............................................................................................................. 5

Income Tax Treatment ............................................................................................................... 7

Contributions ...................................................................................................................... 7 Distributions ........................................................................................................................ 7 Calculating the Taxable Portion of a 529 Distribution: A Stylized Example ...................... 8

Interaction with Other Education Tax Benefits ......................................................................... 9 Rollovers and Transfers ........................................................................................................... 10

To Another 529 Plan ......................................................................................................... 10 To an ABLE Account ........................................................................................................ 10 To a Roth IRA ................................................................................................................... 10

Gift Tax .................................................................................................................................... 11

Interaction of Assets and Distributions from 529 Plans with Federal Student Aid ........................ 11

Figures Figure 1. Calculating the Taxable Portion of a 529 Distribution: A Stylized Example ................... 9

Tables Table 1. Comparison of 529 Prepaid and Savings Plans ................................................................. 4

Contacts Author Information ........................................................................................................................ 13

Congressional Research Service

Tax-Preferred College Savings Plans: An Introduction to 529 Plans

Introduction Families may choose to save for college or elementary and secondary education expenses using tax-advantaged qualified tuition programs (QTPs), also known as 529 plans. This report provides an overview of the mechanics of 529 plans and examines the specific tax advantages of these plans. For an overview of all tax benefits for higher education, see CRS Report R41967, Higher Education Tax Benefits: Brief Overview and Budgetary Effects, by Margot L. Crandall-Hollick.

and Brendan McDermott. Overview of 529 Plans

529 plans, named for the section of the tax code which dictates their tax treatment, are tax-advantaged investment trusts used to pay for education expenses. The specific tax advantage of a 529 plan is that distributions (i.e., withdrawals) from this savings plan are tax-free if they are used to pay for qualified higher education expenses. In addition, up to $10,000 may be withdrawn tax-free per beneficiary per year and used for qualifying elementary and secondary school expenses. If some or all of theAny distribution is used to pay for nonqualified expenses, then a portion of the distribution is taxable, is taxable and may also be subject to a 10% penalty tax.11 (A description of qualified and nonqualified expenses is provided later in this report.)

Generally, a contributor, often a parent, establishes an account in a 529 plan for a designated beneficiary, often their child.22 Upon establishment of a 529 account, an account owner, who maintains ownership and control of the account, must also be designated. In many cases the parent who establishes the account for their child also names herself or himself as the account owner.

According to federal law, paymentscontributions to 529 accounts must be made in cash using after-tax dollars.33 Hence, contributions to 529 plans are not tax-deductible on federal income taxes to the contributor. The contributor and designated beneficiary cannot direct the investments of the account, and the assets in the account cannot be used as a security for a loan. A contributor can establish multiple accounts in different states for the same beneficiary.44 Contributors are not limited to how much they can contribute based on their income. With respect to higher-education expenses, beneficiaries are not limited to how much they can receive based on their income. With respect to elementary and secondary school expenses, beneficiaries can withdraw the amount of their K-12 tuition expenses up to $10,000 tax-free from a 529 plan. (This limit applies to all accounts, not each account.) However, each 529 plan has established an overall lifetime limit on the amount that can be contributed to an account, with contribution limits ranging from $250,000 to nearly $400,000 per beneficiary.5

.5

1 The tax will be paid by either the beneficiary or the owner of the 529 plan account. 2 The individual who maintains and controls the 529 account may not necessarily be a contributor. For example, a grandparent (contributor) could establish a 529 account for their grandchild (beneficiary), but have the child’s parents be the account owners who maintain and control the account.

3 This can include checks, money orders, and credit card payments. Payments cannot be made in the form of securities. 4 For example, an account can be established for beneficiary X in state A’s 529 plan, and an account can be established for beneficiary X in State B’s 529 plan. These two plans for beneficiary X can be established by the same contributor or different contributors.

5 IRC §529 (b)(6) does require that 529 plans limit the amount of contributions to an amount “necessary to provide for the qualified higher education expenses of the beneficiary.” For more information, see https://www.savingforcollege.com/compare-529-plans/maximum-contributions.

Congressional Research Service

1

Tax-Preferred College Savings Plans: An Introduction to 529 Plans

Types of 529 Plans: Prepaid and Savings Plans Types of 529 Plans: Prepaid and Savings Plans

There are two types of 529 plans: "prepaid"“prepaid” plans and "savings"“savings” plans. A 529 prepaid plan allows a contributor (i.e., a parent, grandparent, or nonrelative) to make lump-sum or periodic payments that entitle the beneficiary to a specified number of academic periods, course units, or a percentage of tuition costs at current prices. Essentially, the contributor is paying for and purchasing a given amount of education today which will be used by the student in the future, providing a hedge against tuition inflation. For example, in 2010 a contributor could have purchased two years of community college education through a prepaid plan for $5,000. Even if the price doubled by the time the beneficiary attended community college, they would have already paid the tuition in 2010.

Generally, a prepaid plan is used to purchase education at a public in-state institution.66 Prepaid plans are established and maintained by a state or a state agency or by an educational institution.7,87,8 Prepaid plans tend to have certain restrictions in terms of the expenses they cover, residency requirements, and eligible educational institutions. In some states, the value of these plans is backed by the full faith and credit of the state government, implying that the state bears the risk of the account performance, not the account holder. In addition, some prepaid plans are closed to new beneficiaries, meaning a family cannot open an account in the plan.

A 529 savings plan allows contributors to invest in a portfolio of mutual funds or other underlying investments.99 Contributors can make periodic investments directly in the plan, with the ultimate value of these accounts determined by the performance of the underlying investments. In addition, 529 savings plans can be purchased directly from a plan manager ("“direct sold"”) or purchased through financial advisers ("“broker sold"”). Unlike prepaid plans, the amount of education which can ultimately be purchased using a savings plan is not guaranteed. Instead, the amount of education that can be purchased depends on both the cost of education and the performance of the underlying assets in the 529 savings plan. In addition, the value of savings plans is not limited to tuition at in-state public institutions. Savings plans are established and maintained by a state or a state agency, but tend to be less risky for the state to administer because their value is typically not guaranteed by the state.10

10

While prepaid 529 plans were the first type of 529 plan established, savings plans have grown in popularity and are now the most common type of 529 plan. There are currently 1817 prepaid 529 plans offered, only 7 of which accept new accounts and contributions,plans offered in contrast to 9094 savings plans.11 In addition, according to the most recent data, of the $275.1432 billion worth of assets in 529 plans at the end of 2016, 91.8% ($252.6 billion) were held in savings plans, while 8.2% ($22.5

6 While all 529 distributions can be used to pay for out-of-state colleges, most prepaid plans provide the greatest benefits for in-state colleges. If a student who has a 529-prepaid plan chooses to go to either an in-state private institution or an out-of-state public institution, the prepaid benefits will be set at the equivalent level of public in-state tuitions, with many prepaid plans using a weighted-average credit hour value of in-state public institutions. In addition, the value of the prepaid benefits for out-of-state and private institutions is limited to the lesser of the value of in-state tuition and fees or the actual tuition. Hence, if the tuition paid at an out-of-state institution is less than in-state tuition, the student will not receive a refund for the difference.

7 Currently, there is one prepaid program operated by an educational institution—the Private College 529 Plan. See https://www.privatecollege529.com/OFI529/.

8 States can hire outside vendors like TIAA-CREF, Merrill Lynch, or Fidelity to manage investments and administrative duties.

9 For example, a portfolio of equities and bonds whose percent composition changes automatically as the beneficiary ages, a portfolio with fixed shares of equities and bonds, or a portfolio with a guaranteed minimum rate of return.

10 Similar to prepaid plans, states can hire outside vendors to manage investments and handle administrative duties. 11 College Savings Plan Network, 529 Plan Data, September 30, 2023, http://www.collegesavings.org/529-plan-data/; Flynn, Katherine, “Your Guide to 529 Prepaid Tuition Plans,” Saving for College, November 14, 2023.

Congressional Research Service

2

link to page 7 Tax-Preferred College Savings Plans: An Introduction to 529 Plans

plans as of September 2023, 95% ($409 billion) were held in savings plans, while 5% ($23 billion) were held in prepaid plans.12

billion) were held in prepaid plans.11

There are a variety of differences between savings plans and prepaid plans which may explain the increased popularity of savings plans. States may be more inclined to offer savings plans because they may be less costly or risky for states to run. Many states back prepaid plans with their full faith and credit. In these cases, states must provide a guaranteed benefit to beneficiaries of 529 prepaid plans, even if they do not have sufficient funds in the state'’s 529 trust to pay for beneficiaries'beneficiaries’ college expenses. Hence, these plans can be riskier for states to sponsor.1213 In fact, one of the first 529 prepaid plans established, the Michigan Education Trust (MET), had to close to new beneficiaries shortly after starting because "“the program administrators had relied on overly optimistic projections of the rate of return on invested funds in relation to the trust's ’s obligation to pay for rising tuition prices. Simply put, the trust was headed toward insolvency."13

”14

Savings plans may also be more common because they are more popular with students and their families. Savings plans generally can be used for more types of expenses at a wider variety of institutions than prepaid plans, making them attractive to parents who may not know where their child will ultimately go to college or how much it may cost.1415 In addition, prepaid programs generally require that either the account owner or beneficiary meet state residency requirements, limiting who can ultimately invest in these plans. The majority of savings programs are open to contributors and beneficiaries irrespective of their residency.

Notably, while there are many differences between prepaid and savings plans, the tax treatment of these plans (which will be described later in this report) is identical. Hence, there is not a greater tax benefit per dollar saved associated with one plan rather than another and contributors. Contributors may compare other features of these plans detailed inin Table 1 when deciding which plan is the most appropriate type for their needs.15

|

Prepaid |

Savings |

|

|

Number |

18 |

90 |

|

Qualified Expenses |

Generally they cover tuition and required fees, in most cases at undergraduate institutions. |

, as well as fees, books, supplies, and equipment required for participation in a registered apprenticeship. In addition, up to $10,000 can be withdrawn for a given beneficiary in a given year and used for tuition expenses at elementary or secondary schools. Holders can also withdraw up to $10,000 to make student loan payments for the qualified beneficiary.

Residency

Account owner or beneficiary generally has

Account owner or beneficiary generally does

Requirements

to meet state residency requirements.

|

|

Residency Requirements |

Account owner or beneficiary generally has to meet state residency requirements. |

|

|

Institutional Limitations |

In-state public institution (if used for out-of-state school, the amount is generally limited to in-state tuition and fees at public institution). |

|

|

Refund |

If not all of the amount is used by the student, contributors can request a refund, although the refund amount is determined by the 529 plan. |

An amount not used can be taken out as a nonqualified distribution. The amount withdrawn as a refund is ultimately determined by plan performance. |

|

Distributions Go To |

Directly to institution. |

Beneficiary or account owner or directly to institution. |

|

Time Limitation |

Most prepaid plans can only be used for a limited duration, generally a given number of years from the beneficiary's expected matriculation date. |

Generally, there is no program-imposed limit on how long the account may remain open (as long as the beneficiary is living). |

|

Enrollment period |

Generally yes. Each year, contributors must purchase future college education during a given period. Prices are adjusted annually before each enrollment period. |

No |

|

Who Bears Risk? |

In some states, the plans are backed by the full faith and credit of the state government, meaning the state bears the risk. |

Contributors bear the risk because the performance of the plan is determined by the performance of the underlying assets. |

Sources: Internal Revenue Code (IRC) §529; Internal Revenue Service, Publication 970: Tax Benefits for Education, 2011, http://www.irs.gov/pub/irs-pdf/p970.pdf;; Joseph F. Hurley, The Best Way to Save for College: A Complete Guide to 529 Plans 2011-2012 (Pittsford, NY: JFH Innovative LLC, 2011); text of P.L. 115-97; and the CollegeCol ege Savings Plan Network.

Savings Plan Network.

|

Glossary of Selected Terms16 Account Owner: The person with ownership and control of the 529 account. This individual is usually a contributor to the account. Basis: The sum of all the cash contributed or paid into the account. Designated Beneficiary: The individual for whom the account is established. Distribution: An amount of cash withdrawn from a 529 account (or in the case of prepaid plans, the value of the education benefits paid by the plan). Earnings: The total account value minus the basis. |

Tax Treatment of 529 Plans

Tax Treatment of 529 Plans As previously mentioned, the specific tax advantage of a 529 plan is that the withdrawals from these plans are excludable from gross income, and hence not subject to the income tax, if they are used to pay for certain education expenses incurred in a given year. These expenses are referred to as adjusted qualified education expenses (AQEE—see shaded text box below). Any amount withdrawn from a 529 account which does not go toward these expenses is subject to income taxation and may be subject to an additional 10% penalty tax.

Glossary of Selected Terms

Account Owner: The person with ownership and control of the 529 account. This individual is usually a contributor to the account. Basis: The sum of all the cash contributed or paid into the account. It does not include investment returns. Designated Beneficiary: The individual for whom the account is established. Distribution: An amount of cash withdrawn from a 529 account (or in the case of prepaid plans, the value of the education benefits paid by the plan). Earnings: The total account value minus the basis.

Logically, a taxpayer who receives a 529 distribution (often the beneficiary or the account owner) would seek to minimize their income tax liability by withdrawing just enough money from their 529 account to cover AQEE and no more. However, this is not as straightforward as it may seem due to a variety of factors, including the availability of other education tax benefits and student aid.1717 In order to understand the complex decisions taxpayers must consider when determining the amount of money they should withdraw from a 529 plan, this section details the income tax treatment of 529 distributions, including the definition of AQEE; when 529 distributions may be taxable; and the interaction of 529 distributions with other education tax benefits. (An overview of basic gift tax rules is also included.)

17 Timing issues may also introduce more complexity. Specifically, education expenses are incurred over an academic year, which does not correspond with a tax year (tax years are generally calendar years).

Congressional Research Service

5

link to page 12 Tax-Preferred College Savings Plans: An Introduction to 529 Plans

Adjusted Qualified Education Expenses

Adjusted qualified education expenses include certain higher education expenses and K-12 expenses. Higher Education Qualified higher education expenses are expenses related to

Elementary and Secondary School ;20 and

•

fees, books, supplies, and equipment required for an apprenticeship program registered and certified by the Department of Labor or a state apprenticeship agency recognized by the department.

Elementary and Secondary School Qualified K-12 expenses include up to $10,000 per beneficiary per year for tuition expenses at a public, private, or religious elementary school. To determine the amount of adjusted qualified education expenses, qualified education expenses must be reduced by the amount of any tax-free educational assistance. Tax-free educational assistance includes the tax-free portion of scholarships and fellowships, veterans |

”). Student Loans Qualified student loan repayments include payments of principal and interest on student loans eligible for the student loan interest deduction. Withdrawals of up to $10,000 over the beneficiary’s lifetime qualify. An additional $10,000 limit applies to qualified student loan repayments of a sibling of the beneficiary. Taxpayers cannot claim the student loan interest deduction for any interest paid using tax-free withdrawals from a 529 plan. Rollovers to ABLE Account Through 2025, account managers can choose to transfer the assets within a 529 plan into an ABLE account for the beneficiary or the beneficiary’s family member. ABLE accounts are tax-advantaged savings accounts for individuals with disabilities.21 The withdrawal from the 529 plan would not face any tax or penalty at the time of withdrawal provided the transfer is completed within 60 days. The rol over applies toward the general contribution limits applicable to ABLE accounts defined in IRC §529A(b)(2)(B)(i ). Rollover to Roth IRA Starting in 2024, some 529 plans can be rol ed over into a Roth Individual Retirement Account (IRA) for the same beneficiary. These rol overs cannot exceed the amount contributed to the account within the past five years, along

with any earnings on those contributions. They are also subject to the annual contribution limit for Roth IRAs, which is $7,000 in 2024. There is also a lifetime limit of $35,000 for rol overs from a 529 plan to a Roth IRA. The distribution must come from a plan “of a designated beneficiary which has been maintained for the 15-year period ending on the date of such distribution.” Some have expressed concerns about whether those who rol assets in

18 An eligible education institution for purposes of 529 plans is any college, university, vocational school, or other postsecondary educational institution eligible to participate in a student aid program administered by the U.S. Department of Education.

19 A student is considered “enrolled half-time” if he or she is enrolled for at least half the full-time workload for his or her course of study, as determined by the educational institution’s standards. 20 Room and board expenses cannot be more than the greater of (1) the allowance of room and board that was included in the cost of attendance for federal financial aid purposes for a particular academic period and living arrangement of the student or (2) the actual amount of room and board charged if the student resided in housing owned or operated by the eligible educational institution.

21 For more, see CRS In Focus IF10363, Achieving a Better Life Experience (ABLE) Programs, by William R. Morton and Kirsten J. Colello.

Congressional Research Service

6

Tax-Preferred College Savings Plans: An Introduction to 529 Plans

one 529 plan into another can count the years the assets spent in the first account toward the 15-year limitation, as well as the treatment of repaid early withdrawals when meeting the past five years limitation.22

Income Tax Treatment Income Tax Treatment

Contributors to 529 plans receive no federal income tax benefit from funding a 529 plan. Instead , the main beneficiaries (in terms of reduced income taxes) of 529 plans are the recipients of 529 distributions, who may be able to exclude the entire 529 withdrawal from income taxation. In most cases, the recipient of the 529 distribution (and hence the person who may be liable to pay tax on the distribution) is either the designated beneficiary or the account owner.21

Contributions

23

Contributions

Contributions made to 529 plans are not deductible from income, meaning that contributions to these plans are made using after-tax dollars. Additionally, this implies that contributors to 529 plans receive no federal tax benefit from contributing to a 529 plan. In contrast, many states allow residents to deduct part or all of their 529 contributions from their state income taxes if they contribute to an in-state plan. All 529 plan contributions are allowed to grow tax-free in the 529 account. Hence, unlike the typical bank savings account, where interest income is annually subject to income taxes, the increase in asset values in a 529 plan account is not subject to current income taxes while the funds are in the account.

Distributions

Distributions

Distributions from 529 plans are not subject to federal income taxes if, for a given year, the withdrawal entirely covers AQEE. In other words, if the amount of the distribution is less than or equalequal to the AQEE, the entire distribution is tax free. In addition to this limitation, only a maximum of $10,000 per beneficiary per year may be used for K-12 tuition expenses. Hence, if a child'child’s K-12 education expenses were $7,000, but their parents withdrew $10,000 from her 529 account, a portion of the excess ($3,000) would be subject to taxation. A portion of any amount that is in excess of $10,000 will be taxable.

When a distribution is used to pay for nonqualified expenses, the earnings portion of the withdrawal is subject to the income tax and may be subject to a 10% penalty tax. In other words, if the amount of a 529 withdrawal is greater than the beneficiary'’s AQEE, then some of the earnings portion of the distribution is taxable. The earnings portion of a distribution reflects the growth of the value of the 529 plan and not amounts originally contributed (which are sometimes referred to as basis). The percentage of the earnings portion subject to taxation is equal to the ratio of the difference of the total distribution amount and AQEE to the total distribution amount. To ultimately calculate the amount of tax the taxpayer will owe, the taxpayer'’s marginal tax rate must be applied to this taxable income. In addition, in many cases, a 10% penalty tax will also be applied to this taxable income.22

24

22 For example, see Chris Stack, “Tax-Free 529 to Roth IRA Transfers are Here, But Questions Remain,” Saving for College, January 18, 2024.

23 In the case of a prepaid 529 plan, the payment goes directly to the institution, instead of the beneficiary or the account owner.

24 The 10% penalty tax is waived in the following cases: (1) the distribution is paid to the beneficiary after their death; (2) the distribution is made because the beneficiary is disabled (the beneficiary is considered disabled if he shows proof (continued...)

Congressional Research Service

7

link to page 12 link to page 12 Tax-Preferred College Savings Plans: An Introduction to 529 Plans

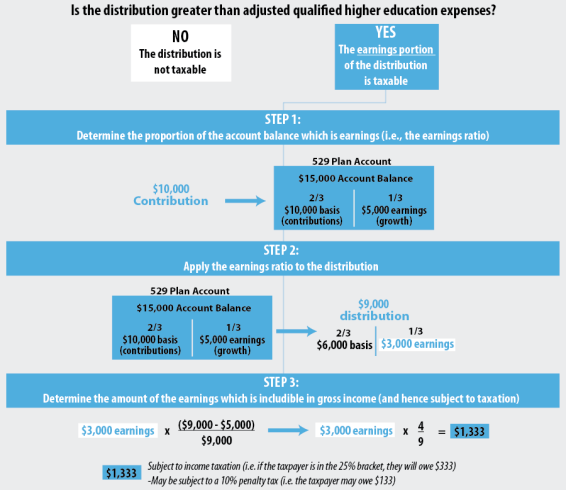

Calculating the Taxable Portion of a 529 Distribution: A Stylized Example

Calculating the Taxable Portion of a 529 Distribution: A Stylized Example

Mr. Smith establishes an account in a 529 plan for his daughter Sara. He is the account owner and his daughter is the designated beneficiary. He makes a one-time contribution (i.e., basis) of $10,000. Five years later the account balance is $15,000 (i.e., it has increased in value by $5,000) and Mr. Smith takes a $9,000 distribution for his daughter'’s $9,000 tuition payment. But Sara also receives a $4,000 tax-free scholarship. Hence, Sara has $5,000 in AQEE ($9,000 of tuition minus $4,000 in tax-free aid). Notably, Mr. Smith pays Sara'’s tuition costs and also designates himself as the recipient of the 529 distribution, implying he (and not his daughter) will be liable to pay any taxes on the 529 distribution.23

25

The steps to calculate the taxable portion of the distribution—and it is taxable because adjusted qualified education expenses ($5,000) are less than the 529 distribution ($9,000)—are outlined in Figure 1.

First, Mr. Smith must calculate the proportion of the distribution that is earnings. Since one-third of the account balance ($5,000) reflects earnings (two-thirds of the account balance reflects $10,000 of contributions), one-third of the distribution is attributable to earnings. Second, Mr. Smith applies the earnings ratio (in this case, one-third) to the distribution. Hence, of the $9,000 distribution, one-third or $3,000 reflects earnings. Finally, Mr. Smith calculates the proportion of the $3,000 earnings portion that is subject to taxation. The percentage of the earnings portion that is subject to taxation is equal to the ratio of the difference of the total distribution amount ($9,000) and AQEE ($5,000) to the total distribution amount ($9,000). Ultimately, as Figure 1 illustrates, of the $9,000 distribution, $1,333 of it is includible in Mr. Smith'’s income and thus subject to taxation on his income tax return.

that the he cannot do any substantial gainful activity because of a disability. A physician must determine that the disability is either life threatening or will have an indefinite duration); (3) the distribution is greater than qualified education expenses (and hence the earning portion is taxable) because the beneficiary received tax-free educational assistance as long as distribution is not more than the tax-free assistance; (4) the distribution was made as a result of the beneficiary’s attendance at a U.S. military academy to the extent that the distribution is not greater than the cost of attendance at such an academy; (5) the distribution was taxable as a result of reducing qualified expenses in order to claim higher education tax credits.

25 The account owner of a 529 account selects the recipient of the distribution when filing out the program’s withdrawal request form.

Congressional Research Service

8

Tax-Preferred College Savings Plans: An Introduction to 529 Plans

Figure 1. Calculating the Taxable Portion of a 529 Distribution: A Stylized Example

Sources |

|

|

Interaction with Other Education Tax Benefits

In addition to 529 plans, there are a variety of other tax benefits taxpayers (either the beneficiary or the account owner) may use to lower their income tax bill based on education expenses.24 Notably, taxpayers may be eligible to claim either the American Opportunity tax credit (AOTC),25 the Lifetime Learning credit, or the tuition and fees deduction.26Tax Credit (AOTC)26 or the Lifetime Learning Credit. A taxpayer cannot claim more than one of these tax benefits for the same student in a given year.

To determine if any of their 529 distribution is taxable, a taxpayer must reduce their 529 qualified education expenses by any amounts used to claim either the AOTC or the Lifetime Learning creditCredit. The qualified education expenses as defined for 529 plans are not identical to the qualified higher education expenses of education tax credits. However, since some expenses do overlap (such as tuition and fees at higher education institutions, course-related books, supplies, and

26 For more information on the AOTC, see CRS Report R42561, The American Opportunity Tax Credit: Overview, Analysis, and Policy Options, by Margot L. Crandall-Hollick.

Congressional Research Service

9

Tax-Preferred College Savings Plans: An Introduction to 529 Plans

equipment), some taxpayers may (mistakenly) try to claim both an education tax credit and a tax-free 529 distribution for such expenses.

higher education expenses of education tax credits. The qualified higher education expenses common to both 529 plans and education tax credits are tuition and fees, and hence these are the expenses which taxpayers may (mistakenly) try to use to claim both an education tax credit and a tax-free 529 distribution. (Other expenses, like room and board, which are a qualified expense for 529 plans, are not a qualified expense for education tax credits and hence would not be used to claim an education tax credit.) For example, if an eligible taxpayer has $10,000 of tuition payments of which they used $4,000 to qualify for an American Opportunity tax creditAOTC, the amount of qualified higher education expenses used to determine if their 529 distribution is tax free is $6,000. Thus, if a 529 distribution is less than or equal to $6,000, none of the distribution is subject to taxation because the distribution covered all of their AQEE.

Rollovers and Transfers

To Another 529 Plan

AQEE.

Instead of an education tax credit, a taxpayer may choose to both take a 529 distribution and claim the tuition and fees deduction for the same student in the same year. Taxpayers who take a 529 distribution and also choose to claim the tuition and fees deduction must reduce the amount of expenses used for the tuition and fees deduction by the earnings portion of the 529 distribution (not the entire amount of the distribution).27

Rollovers and Transfers

Any distribution from a 529 plan for a given beneficiary which is rolled over into a different 529 plan for either the same beneficiary28beneficiary27 or a member of the beneficiary's family29’s family28 is not taxable. A distribution is considered "“rolled over"” if it is paid to another 529 plan within 60 days of the distribution. A rollover between 529 plans for the same beneficiary is limited to once every 12 months. In addition, if the designated beneficiary of an account is changed to a member of the beneficiary'beneficiary’s family, the transfer of funds is not taxable.

To an ABLE Account

Additionally, account holders can roll 529 plan assets into an ABLE account held by the same beneficiary as the 529 plan. ABLE accounts are tax-advantaged savings accounts for individuals with disabilities. States create qualified ABLE programs, and the federal government recognizes them for tax purposes. Contributions are not eligible for a tax deduction, but qualified withdrawals are excluded from the beneficiary’s income subject to tax. To open an ABLE account, the beneficiary must have a qualifying impairment that began before age 26 (this limit will rise to 46 in 2026 under current law). In addition to the tax benefit, these accounts benefit holders because the federal government excludes some or all of the assets in ABLE accounts from asset tests used for some means-tested federal benefits, such as Supplemental Security Income. Rollovers from 529 plans are subject to the annual contribution limit to ABLE accounts ($18,000 in 2024) and to any state limits on aggregate 529 plan contributions.

To a Roth IRA

Federal law also permits qualified rollovers from 529 plans to Roth IRAs. Roth IRAs are retirement accounts in which individuals contribute using after-tax income, but qualified withdrawals are tax-free.29 Qualified withdrawals from Roth IRA plans include any made after the taxpayer turns age 59½. Nonqualified withdrawals are subject to tax and a 10% penalty, although this penalty is waived under certain circumstances, such as if used for higher education

27 Only one rollover from one 529 plan to a different 529 plan for the same beneficiary is allowed in a 12-month period. 28 For the purposes of a 529 plan, the beneficiary’s family includes the following: the beneficiary’s son, daughter, stepchild, foster child, adopted child (or decedent of any of these children); brother, sister, stepbrother, stepsister; father, mother, or their ancestors; son or daughter of a brother or sister; brother or sister of father or mother; son-in-law, daughter-in-law, father-in-law, mother-in-law, brother-in-law, or sister-in-law; the spouse of any of the individuals previously listed (including the beneficiary’s spouse); and first cousin. 29 For more about Roth IRAs, see CRS Report RL34397, Traditional and Roth Individual Retirement Accounts (IRAs): A Primer, by Elizabeth A. Myers.

Congressional Research Service

10

Tax-Preferred College Savings Plans: An Introduction to 529 Plans

expenses; health insurance premiums for uninsured beneficiaries; or to build, buy, or rebuild a first home (subject to a $10,000 limit).

Qualified 529 plan rollovers cannot exceed 529 plan contributions in the beneficiary’s name in the preceding 5 years, in addition to any earnings on those same contributions. The 529 plan must have been in the beneficiary’s name for the preceding 15 years. Rollovers for a designated beneficiary are subject to a lifetime limit of $35,000. Additionally, the rollovers may not exceed the annual contribution limit to IRAs ($7,000 for individuals under age 50 in 2024), minus the aggregate contributions made to all individual retirement plans in that year.

These limitations present ambiguities that the IRS and Congress have yet to clarify. For example, it is unclear whether a beneficiary could roll over assets held in an account that is eight years old, but includes assets rolled over from another 529 plan held in the beneficiary’s name for eight years prior.30

Gift Tax A contribution to a 529 plan is generally not subject to the gift tax if the amount contributed is less than the annual gift tax exclusion.31 For 2024, the annual gift tax exclusion is $18,000.32 For example, a grandparent could contribute $18,000 to each of their seven grandchildren’s 529 accounts without being subject to the gift tax.33 In addition, a contributor may be able to deposit more than the annual exclusion amount into a 529 plan without being subject to the gift tax.34 The IRC allows a donor to make a contribution larger than the annual gift tax exclusion by treating the contribution as if it were made ratably over five years. In other words, a contributor could have opened a 529 savings plan for a beneficiary in 2024 and contributed up to $90,000 (five times $18,000) without being subject to the gift tax. The contributor could not make another excludable gift to that beneficiary’s 529 plan until 2029. In addition to these gift tax rules, for the purposes of the estate tax, a donor can exclude the value of the 529 plan from their gross estate, even though they maintain control of the account.

Interaction of Assets and Distributions from 529 Plans with Federal Student Aid In addition to the tax advantages of 529 plans, these plans are also treated more favorably than other types of college savings or investments when determining a student’s eligibility for federal need-based student aid. For instance, 529 plans generally have a minimal impact on a student’s federal expected family contribution (EFC). The EFC is the amount that, according to the federal need analysis methodology, can be contributed by a student and the student’s family toward the student’s cost of education. All else being equal, the higher a student’s EFC, the lower the amount of federal student need-based aid he or she will receive. A variety of financial resources are

30 Chris Stack, “Tax-Free 529 to Roth IRA Transfers are Here, But Questions Remain,” Saving for College, January 18, 2024.

31 Contributions to 529 plans treated as a completed gift which implies the transfer of ownership from the contributor to the beneficiary, even though contributors to 529 plans maintain control of the accounts.

32 $36,000 for a married couple using gift-splitting. 33 Each grandparent could contribute $18,000, meaning they could deposit $36,000 per grandchild as a couple without being subject to the gift tax.

34 For an overview of the current law of the gift tax, see CRS Report R42959, Recent Changes in the Estate and Gift Tax Provisions, by Jane G. Gravelle.

Congressional Research Service

11

Tax-Preferred College Savings Plans: An Introduction to 529 Plans

reported by students and their families on the Free Application for Federal Student Aid (FAFSA). These resources are assessed at differing rates under the federal need analysis methodology.35

Distributions from 529 plans are generally not considered income in the federal need analysis calculation and are therefore not reported on the FAFSA.36 However, the value of the 529 plan may be considered an asset in the federal need analysis methodology.37 When calculating a student’s EFC, the federal need analysis methodology considers a percentage of the student’s assets and a percentage of the parents’ assets (above an “asset protection allowance”) reported on the FAFSA.

This rate is typically lower for parents of students who are classified as dependent students for FAFSA purposes (which differs from the classification of dependent for tax purposes)38 than it is for the dependent students themselves (who also receive no asset protection allowance). 529 plans with a dependent student as beneficiary are considered an asset of the parent, as long as the custodial ownership of the plan belongs to either the parent or the student. Dependent students can therefore benefit from a lower EFC and the potential for more federal need-based student aid than they might receive if the asset was considered their own. For students who are classified as independent students for FAFSA purposes, 529 plans are treated as an asset of the student, as long as the custodial ownership of the plan belongs either to the student or student’s spouse (if applicable).39

529 plans that are owned by someone other than the student, parent, or spouse are not reported as an asset on the FAFSA. Distributions from these 529 plans were previously reported as untaxed income for the beneficiary on the FAFSA, meaning they were assessed at a higher rate than assets in federal need analysis methodology. However, under the FAFSA Simplification Act (passed as Division FF of P.L. 116-260), such 529 plans do not need to be reported on the FAFSA. This change was scheduled to take effect in the 2023-2024 aid year, but Congress delayed it to the 2024-2025 aid year in the FAFSA Simplification Act Technical Corrections Act (passed as Division R of P.L. 117-103).

35 The details of the federal need analysis methodology are beyond the scope of this report. For more on the topic, see CRS Report R44503, Federal Student Aid: Need Analysis Formulas and Expected Family Contribution, by Benjamin Collins and CRS Report R46909, The FAFSA Simplification Act, by Benjamin Collins and Cassandria Dortch.

36 Additionally, distributions from 529 plans are not considered a resource when calculating other estimated financial assistance (EFA) during the federal aid packaging process. For more information on EFA and the packaging of aid, see the 2024-2025 Federal Student Aid Handbook at https://fsapartners.ed.gov/knowledge-center/fsa-handbook/2024-2025.

37 For prepaid 529 plans, the asset value is the refund value of the plan. 38 For the purposes of taxes, IRC §152 defines dependents. The definition includes (but is not limited to) a requirement that the dependent has the same principal residence as the taxpayer for more than half the year, and that the dependent has not provided over one-half of their support. In contrast, a student aged under 24 is generally considered a dependent for financial aid purposes. If certain criteria are met, the student is considered an independent student for financial aid purposes. A student can determine their dependency status for financial aid at http://www.finaid.org/calculators/dependency.phtml.

39 The treatment of assets held by independent students differs by whether the student has dependents of their own (besides a spouse) for the purposes of FAFSA. Generally, for students with assets above the asset protection allowance, increasing the assets of those with such dependents causes their EFCs to rise by less than a similar increase in assets would for students who do not have such dependents. See Tables 2, 3, and 4 of CRS Report R44503, Federal Student Aid: Need Analysis Formulas and Expected Family Contribution, by Benjamin Collins.

Congressional Research Service

12

Tax-Preferred College Savings Plans: An Introduction to 529 Plans

Author Information

Brendan McDermott

Analyst in Public Finance

Acknowledgments

Margot Crandall-Hollick wrote a prior version of this report.

Disclaimer

This document was prepared by the Congressional Research Service (CRS). CRS serves as nonpartisan shared staff to congressional committees and Members of Congress. It operates solely at the behest of and under the direction of Congress. Information in a CRS Report should not be relied upon for purposes other than public understanding of information that has been provided by CRS to Members of Congress in connection with CRS’s institutional role. CRS Reports, as a work of the United States Government, are not subject to copyright protection in the United States. Any CRS Report may be reproduced and distributed in its entirety without permission from CRS. However, as a CRS Report may include copyrighted images or material from a third party, you may need to obtain the permission of the copyright holder if you wish to copy or otherwise use copyrighted material.

Congressional Research Service

R42807 · VERSION 11 · UPDATED

13 s family, the transfer of funds is not taxable.

Gift Tax

A contribution to a 529 plan is generally not subject to the gift tax if the amount contributed is less than the annual gift tax exclusion.30 For 2017, the annual gift tax exclusion was $14,000.31 For example, a grandparent could contribute $14,000 to each of their seven grandchildren's 529 accounts without being subject to the gift tax.32 In addition, a contributor may be able to deposit more than the annual exclusion amount into a 529 plan without being subject to the gift tax.33 The Internal Revenue Code (IRC) allows a donor to make a contribution larger than the annual gift tax exclusion by treating the contribution as if it were made ratably over five years. In other words, a contributor could have opened a 529 savings plan for a beneficiary in 2017 and contributed up to $70,000 (five times $14,000) without being subject to the gift tax. The contributor could not make another excludable gift to that beneficiary's 529 plan until 2022. In addition to these gift tax rules, for the purposes of the estate tax, a donor can exclude the value of the 529 plan from their gross estate, even though they maintain control of the account.

Interaction of Assets and Distributions from 529 Plans with Federal Student Aid34

In addition to the tax advantages of 529 plans, these plans are also treated more favorably than other types of college savings or investments when determining a student's eligibility for federal need-based student aid. For instance, 529 plans generally have a minimal impact on a student's federal expected family contribution (EFC). The EFC is the amount that, according to the federal need analysis methodology, can be contributed by a student and the student's family toward the student's cost of education. All else being equal, the higher a student's EFC, the lower the amount of federal student need-based aid he or she will receive. A variety of financial resources are reported by students and their families on the Free Application for Federal Student Aid (FAFSA). These resources are assessed at differing rates under the federal need analysis methodology.35

Distributions36 from 529 plans are generally not considered income in the federal need analysis calculation and are therefore not reported on the FAFSA, although the value37 of the 529 plan is considered an asset in the federal need analysis methodology and should be reported on the FAFSA.38

When calculating a student's EFC, the federal need analysis methodology considers a percentage of the student's assets and a percentage of the parents' assets reported on the FAFSA. A student's assets are assessed at a flat rate of 20%, while parents' assets are assessed on a sliding scale, resulting in a maximum effective rate of up to 5.64%.39 Therefore, the ownership of the asset is important when determining how it will affect a student's EFC. For students who are classified as dependent students for FAFSA purposes (which differs from the classification of dependent for tax purposes),40 the 529 plans are considered an asset of the parent, as long as the custodial ownership of the plan belongs either to the parent or student. Therefore, dependent students benefit from a lower assessment rate on 529 plans, which, all else being equal, results in a lower EFC and the potential for more federal need-based student aid. For students who are classified as independent students for FAFSA purposes, 529 plans are treated as an asset of the student, as long as the custodial ownership of the plan belongs either to the student or student's spouse (if applicable). 529 plans that are owned by someone other than the student, parent, or spouse are not reported as an asset on the FAFSA, but distributions from these 529 plans are reported as untaxed income for the beneficiary on the FAFSA.41 In general, income is assessed at a higher rate compared to assets in the federal need analysis methodology.

Author Contact Information

Footnotes

| 1. |

The tax will be paid by either the beneficiary or the owner of the 529 plan account. |

| 2. |

The individual who maintains and controls the 529 account may not necessarily be a contributor. For example, a grandparent (contributor) could establish a 529 account for their grandchild (beneficiary), but have the child's parents be the account owners who maintain and control the account. |

| 3. |

This can include checks, money orders, and credit card payments. Payments cannot be made in the form of securities. |

| 4. |

For example, an account can be established for beneficiary X in state A's 529 plan, and an account can be established for beneficiary X in State B's 529 plan. These two plans for beneficiary X can be established by the same contributor or different contributors. |

| 5. |

The Internal Revenue Code (IRC) § 529 (b)(6) does require that 529 plans limit the amount of contributions to an account to an amount "necessary to provide for the qualified higher education expenses of the beneficiary." For more information, see http://www.savingforcollege.com/compare_529_plans/index.php?plan_question_ids%5B%5D=308&mode=Compare&page=compare_plan_questions&plan_type_id=. |

| 6. |

While all 529 distributions can be used to pay for out-of-state colleges, most prepaid plans provide the greatest benefits for in-state colleges. If a student who has a 529-prepaid plan chooses to go to either an in-state private institution or an out-of state public institution, the prepaid benefits will be set at the equivalent level of public in-state tuitions, with many prepaid plans using a weighted-average credit hour value of in-state public institutions. In addition, the value of the prepaid benefits for out-of-state and private institutions is limited to the lesser of the value of in-state tuition and fees or the actual tuition. Hence, if the tuition paid at an out-of state institution is less than in-state tuition, the student will not receive a refund for the difference. |

| 7. |

|

| 8. |

States can hire outside vendors like TIAA-CREF, Merrill Lynch, or Fidelity to manage investments and administrative duties. |

| 9. |

For example, a portfolio of equities and bonds whose percent composition changes automatically as the beneficiary ages, a portfolio with fixed shares of equities and bonds, or a portfolio with a guaranteed minimum rate of return. |

| 10. |

Similar to prepaid plans, states can hire outside vendors to manage investments and handle administrative duties. |

| 11. |

College Savings Plan Network, 529 Plan Data, December 31, 2016, http://www.collegesavings.org/529-plan-data/. |

| 12. |

In spite of the greater popularity of savings plans, prepaid plans tend to be less risk for parents than savings plans. Unlike 529 savings plans, the purchasing power of prepaid plans is guaranteed. In other words, if you purchase one semester of education at today's prices, you will be able to purchase one semester of education when the child attends college. |

| 13. |

Joseph F. Hurley, The Best Way to Save for College: A Complete Guide to 529 Plans 2011-2012 (Pittsford, NY: JFH Innovative LLC, 2011), p. 12. The program later resumed and is again operational after adjusting its pricing. |

| 14. |

Andrew P. Roth, "Who Benefits from States' College Savings Plans?" Chronicle of Higher Education, January 1, 2001. |

| 15. |

Contributors may also look at other attributes of the plans which are specific to each plan, including the fees associated with each plan, when deciding the most appropriate 529 plan. |

| 16. |

Adapted from Joseph F. Hurley, The Best Way to Save for College: A Complete Guide to 529 Plans 2011-2012 (Pittsford, NY: JFH Innovative LLC, 2011), p. 9. |

| 17. |

Timing issues may also introduce more complexity. Specifically, education expenses are incurred over an academic year, which does not correspond with a tax year (tax years are generally calendar years). |

| 18. |

An eligible education institution for purposes of 529 plans is any college, university, vocational school, or other postsecondary educational institution eligible to participate in a student aid program administered by the U.S. Department of Education. |

| 19. |

A student is considered "enrolled half-time" if he or she is enrolled for at least half the full-time workload for his or her course of study, as determined by the educational institution's standards. |

| 20. |

Room and board expenses cannot be more than the greater of (1) the allowance of room and board that was included in the cost of attendance for federal financial aid purposes for a particular academic period and living arrangement of the student or (2) the actual amount of room and board charged if the student resided in housing owned or operated by the eligible educational institution. |

| 21. |

In the case of a prepaid 529 plan, the payment goes directly to the institution, instead of the beneficiary or the account owner. |

| 22. |

The 10% penalty tax is waived in the following cases: (1) the distribution is paid to the beneficiary after their death; (2) the distribution is made because the beneficiary is disabled (the beneficiary is considered disabled if he shows proof that the he cannot do any substantial gainful activity because of a disability. A physician must determine that the disability is either life threatening or will have an indefinite duration); (3) the distribution is greater than qualified education expenses (and hence the earning portion is taxable) because the beneficiary received tax-free educational assistance as long as distribution is not more than the tax-free assistance; (4) the distribution was made as a result of the beneficiary's attendance at a U.S. military academy to the extent that the distribution is not greater than the cost of attendance at such an academy; (5) the distribution was taxable as a result of reducing qualified expenses in order to claim higher education tax credits. |

| 23. |

The account owner of a 529 account selects the recipient of the distribution when filing out the program's withdrawal request form. |

| 24. |

As a result of a temporary provision, from 2002 through 2012, taxpayers can make contributions to both a 529 and Coverdell for the same beneficiary in the same year. However, beginning in 2013, this temporary provision is scheduled to expire. Hence, if a taxpayer makes a contribution to both a 529 and Coverdell for the same beneficiary in the same year, the contribution to the Coverdell will be considered an excess payment and be subject to income taxation and a penalty tax. |

| 25. |

For more information on the AOTC, see CRS Report R42561, The American Opportunity Tax Credit: Overview, Analysis, and Policy Options, by Margot L. Crandall-Hollick. |

| 26. |

Under current law, the tuition and fees deduction expired at the end of 2017. Hence, barring any legislative changes, taxpayers will be ineligible from claiming this above-the-line deduction on their tax returns, beginning with their 2018 tax return. |

| 27. |

The Internal Revenue Code (IRC) and IRS Publication 970 provide different explanations on how to coordinate 529 distributions and the tuition and fees deduction for a given student. Since IRS Publication 970 does not have the force of law, the literal interpretation of the IRC is described in this report. According to IRC § 222(c)(2)(B), the total amount of qualified tuition and related expenses used to claim the tuition and fees deduction must be reduced by the earnings portion of a 529 distribution used for the same expenses. In contrast, according to Publication 970, a taxpayer reduces the amount of AQEE used to calculate the taxable portion of a 529 distribution by the amount of tuition and fees used to claim the tuition and fees deduction. In some cases, the tax savings of these two different approaches may differ. |

| 28. |

Only one rollover from one 529 plan to a different 529 plan for the same beneficiary is allowed in a 12-month period. |

| 29. |

For the purposes of a 529 plan, the beneficiary's family includes the following: the beneficiary's son, daughter, stepchild, foster child, adopted child (or decedent of any of these children); brother, sister, stepbrother, stepsister; father, mother, or their ancestors; son or daughter of a brother or sister; brother or sister of father or mother; son-in-law, daughter-in-law, father-in-law, mother-in-law, brother-in-law, or sister-in-law; the spouse of any of the individuals previously listed (including the beneficiary's spouse); and first cousin. |

| 30. |

Contributions to 529 plans treated as a completed gift which implies the transfer of ownership from the contributor to the beneficiary, even though contributors to Section 529 plans maintain control of the accounts. |

| 31. |

$28,000 for a married couple using gift-splitting. |

| 32. |

Each grandparent could contribute $14,000 each, meaning they could deposit $28,000 per grandchild as a couple without being subject to the gift tax. |

| 33. |

For an overview of the current law of the gift tax, see CRS Report 95-416, The Federal Estate, Gift, and Generation-Skipping Transfer Taxes, by Emily M. Lanza. |

| 34. |

For further description of federal need analysis, see CRS Report R42446, Federal Pell Grant Program of the Higher Education Act: How the Program Works and Recent Legislative Changes, by Cassandria Dortch. |

| 35. |

The details of the federal need analysis methodology are beyond the scope of this report. |

| 36. |

Additionally, distributions from 529 plans are not considered a resource when calculating other estimated financial assistance (EFA) during the federal aid packaging process. For more information on EFA and the packaging of aid, see the AY2012-13 Federal Student Aid Handbook, Volume 3, at http://ifap.ed.gov/fsahandbook/1213FSAHbVol3.html. |

| 37. |

For 529 plans that are considered pre-paid tuition plans, the asset value is equal to the refund value. |

| 38. |

For prepaid 529 plans, the asset value is the refund value of the plan. |

| 39. |

Parental assets are also protected by an asset protection allowance, which means that a certain amount of assets are not considered in evaluating the effective family contribution (EFC). |

| 40. |

For the purposes of taxes, IRC §152 defines dependents which includes (but is not limited to) a requirement that the dependent has the same principal residence as the taxpayer for more than half the year, and that the dependent has not provided over one-half of their support. In contrast, student under 24 are generally considered a dependent for financial aid purposes. If certain criteria are met, the student is considered an independent student for financial aid purposes. A student can determine their dependency status for financial aid at http://www.finaid.org/calculators/dependency.phtml. |

| 41. |

For more information, see http://www.finaid.org/savings/loophole.phtml. |