Legislative Procedures for Adjusting the Public Debt Limit: A Brief Overview

Nearly all of the outstanding debt of the federal government is subject to a statutory limit, which is set forth as a dollar limitation in 31 U.S.C. 3101(b). From time to time, Congress considers and passes legislation to adjust or suspend this limit.

The annual budget resolution is required to include appropriate levels of the public debt for each fiscal year covered by the resolution. The budget resolution, however, does not become law. Therefore, the enactment of subsequent legislation is necessary in order to implement budget resolution policies, including changes to the statutory limit on the public debt. In addition, Congress may consider adjustments to the public debt limit outside the context of the budget resolution, such as when the House and Senate are unable to agree on a budget resolution or when the current debt limit is not sufficient to meet existing financial obligations.

Under current legislative procedures, the House and Senate may originate and consider legislation adjusting the debt limit in several different ways. They may consider such legislation under regular legislative procedures, either as freestanding legislation or as a part of a measure dealing with other topics. Alternatively, they may change the debt limit as part of the budget reconciliation process provided for under the Congressional Budget Act of 1974. The House also has originated debt limit legislation under its former House Rule XXVIII (the so-called “Gephardt rule”); the House repealed the rule at the beginning of the 112th Congress (2011-2012). In addition, Congress has twice established special procedures for congressional disapproval of adjustments to the debt limit authorized by certain statutes.

During the period from 1940 to the present, Congress and the President have enacted a total of 96 measures adjusting the public debt limit—77 under regular legislative procedures in both chambers, 15 under the Gephardt rule, and 4 under reconciliation procedures.

This report will be updated as developments warrant.

Legislative Procedures for Adjusting the Public Debt Limit: A Brief Overview

Jump to Main Text of Report

Contents

- Introduction

- Legislative Procedures for Adjusting the Public Debt Limit

- Regular Legislative Procedures in Both Chambers

- The Budget Reconciliation Process

- "Gephardt Rule" Procedures

- Congressional Disapproval Procedures

- Measures Adjusting the Public Debt Limit

Figures

Summary

Nearly all of the outstanding debt of the federal government is subject to a statutory limit, which is set forth as a dollar limitation in 31 U.S.C. 3101(b). From time to time, Congress considers and passes legislation to adjust or suspend this limit.

The annual budget resolution is required to include appropriate levels of the public debt for each fiscal year covered by the resolution. The budget resolution, however, does not become law. Therefore, the enactment of subsequent legislation is necessary in order to implement budget resolution policies, including changes to the statutory limit on the public debt. In addition, Congress may consider adjustments to the public debt limit outside the context of the budget resolution, such as when the House and Senate are unable to agree on a budget resolution or when the current debt limit is not sufficient to meet existing financial obligations.

Under current legislative procedures, the House and Senate may originate and consider legislation adjusting the debt limit in several different ways. They may consider such legislation under regular legislative procedures, either as freestanding legislation or as a part of a measure dealing with other topics. Alternatively, they may change the debt limit as part of the budget reconciliation process provided for under the Congressional Budget Act of 1974. The House also has originated debt limit legislation under its former House Rule XXVIII (the so-called "Gephardt rule"); the House repealed the rule at the beginning of the 112th Congress (2011-2012). In addition, Congress has twice established special procedures for congressional disapproval of adjustments to the debt limit authorized by certain statutes.

During the period from 1940 to the present, Congress and the President have enacted a total of 96 measures adjusting the public debt limit—77 under regular legislative procedures in both chambers, 15 under the Gephardt rule, and 4 under reconciliation procedures.

This report will be updated as developments warrant.

Introduction

Nearly all of the outstanding debt of the federal government is subject to a statutory limit.1 For years, the public debt limit has been codified in Section 3101(b) of Title 31 of the United States Code. Periodic adjustments to the debt limit typically have taken the form of amendments to 31 U.S.C. 3101(b), usually by striking the current dollar limitation and inserting a new one. In recent years, such legislation has taken the form of suspending the debt limit through a date certain, with an increase to the dollar limit made administratively at the end of the suspension period.2

The congressional budget process provides for the annual adoption of a concurrent resolution on the budget, which sets forth appropriate levels of the public debt—along with levels of revenues, spending, and the deficit or surplus—for the upcoming fiscal year and at least four additional years.3 The budget resolution, however, does not become law. Therefore, subsequent legislation is necessary in order to implement budget resolution policies, including changes to the statutory limit on the public debt. In addition, Congress may consider adjustments to the public debt limit outside the context of the budget resolution, such as when the House and Senate are unable to agree on a budget resolution or when the current debt limit is not sufficient to meet existing financial obligations.

Legislative Procedures for Adjusting the Public Debt Limit

Under current legislative procedures, the House and Senate may originate and consider legislation adjusting the debt limit in several different ways. They may consider such legislation under regular legislative procedures, either as freestanding legislation or as a part of a measure dealing with other topics. Alternatively, they may change the debt limit as part of the budget reconciliation process provided for under the Congressional Budget Act of 1974.4 In addition, Congress has twice established special procedures for congressional disapproval of adjustments to the debt limit authorized by certain statutes. Finally, the House has originated debt limit legislation under its former House Rule XXVIII (the so-called Gephardt rule); the House repealed the rule at the beginning of the 112th Congress (2011-2012).

Although the Constitution requires that revenue measures originate in the House, this requirement is not considered to apply to debt limit measures.5 Over the years, however, most debt limit legislation has originated in the House.6 The House Ways and Means Committee and the Senate Finance Committee exercise jurisdiction over debt limit legislation.

It is extremely difficult for Congress to effectively influence fiscal and budgetary policy through action on legislation adjusting the debt limit. The need to raise (or lower) the limit during a session is driven by many previous decisions regarding revenues and spending stemming from legislation enacted earlier in the session or in prior years. Nevertheless, the consideration of debt limit legislation often is viewed as an opportunity to reexamine fiscal and budgetary policy and is marked by controversy. Consequently, House and Senate action on legislation adjusting the debt limit often is complicated, hindered by political difficulties, and subject to delay.

The three ways the House and Senate have originated and considered debt limit legislation, as well as the congressional disapproval procedures first established under the Budget Control Act of 2011, are discussed briefly below.

Regular Legislative Procedures in Both Chambers

The House and Senate may develop and consider legislation adjusting the debt limit under regular legislative procedures in both chambers, either as freestanding legislation or as a part of a measure dealing with other topics. The House Ways and Means Committee and the Senate Finance Committee may originate measures adjusting the debt limit at any time. The Senate usually acts on legislation originated by the House. However, in 2002 and 2004, for example, the Senate originated debt limit legislation (S. 2578 and S. 2986, respectively), which became P.L. 107-199 and P.L. 108-415, respectively.

Consideration of a debt limit measure in the House usually is subject to a special rule, reported by the House Rules Committee, that may include debate limitations, restrictions on the offering of amendments, and other expediting features. In the Senate, consideration of debt limit measures is generally not subject to expedited procedures; nongermane amendments may be offered and the measures may be debated at length unless cloture is invoked or other limitations are agreed to by unanimous consent.

In 2009, for instance, an adjustment to the public debt limit (Section 1604, Div. B, P.L. 111-5) was considered under the regular legislative process as part of the economic stimulus legislation in the early part of 2009. The House passed (on January 28) its version of the economic stimulus legislation (H.R. 1, the American Recovery and Reinvestment Act of 2009) without any provision increasing the public debt limit. The Senate, however, included an increase to the public debt limit in its version passed on February 10. The House and Senate subsequently agreed to the conference report to accompany H.R. 1, which included the Senate's provision to increase the public debt limit, on February 13. President Barack Obama signed the legislation on February 17, 2009 (P.L. 111-5).

The Budget Reconciliation Process

The budget reconciliation process is an optional procedure associated with the congressional budget resolution; the budget reconciliation process may be used only if the House and Senate agree to a budget resolution that contains reconciliation directives.7 The budget reconciliation process, as provided for by the Congressional Budget Act, is intended to facilitate the timely consideration and enactment of legislation that implements, in whole or in part, the budget policies reflected in the budget resolution, including changes to the debt limit. Reconciliation legislation is subject to expedited consideration in both chambers. In the Senate, where the expedited procedures have the most impact, debate on reconciliation legislation is limited, amendments must be germane, and extraneous matter is prohibited.

Although the predominant focus of reconciliation legislation has been to change revenue and spending levels, four such measures also were used to adjust the debt limit:

- the Omnibus Budget Reconciliation Act of 1986 (P.L. 99-509; October 21, 1986), Section 8201 (100 Stat. 1968);

- the Omnibus Budget Reconciliation Act of 1990 (P.L. 101-508; November 5, 1990), Section 11901 (104 Stat. 1388-560);

- the Omnibus Budget Reconciliation Act of 1993 (P.L. 103-66; August 10, 1993), Section 13411 (107 Stat. 565); and

- the Balanced Budget Act of 1997 (P.L. 105-33; August 5, 1997), Section 5701 (111 Stat. 648).

The Senate adopted a rule prohibiting the consideration of a budget reconciliation bill pursuant to the FY2016 budget resolution that "would increase the public debt limit" (see Section 2001(b) of S.Con.Res. 11, 114th Congress).

"Gephardt Rule" Procedures

The House also has originated debt limit legislation pursuant to its former House Rule XXVIII, commonly referred to as the "Gephardt rule" (named after its author, Representative Richard Gephardt).8 The House, as noted above, repealed this rule at the beginning of the 112th Congress (2011-2012).9

The rule provided for the automatic engrossment of a House joint resolution changing the statutory limit on the public debt when Congress had completed action on the congressional budget resolution. The joint resolution was deemed to have passed the House by the same vote as the conference report on the budget resolution.

The Senate has never had a comparable procedure. If the Senate chose to consider a House joint resolution originated pursuant to the Gephardt rule, it did so under the regular legislative process. Under the regular legislative process, as noted above, consideration of debt limit measures, even those originated by the Gephardt rule, generally is not subject to expedited procedures; nongermane amendments may be offered, and the measures may be debated at length, unless cloture is invoked or other limitations are agreed to by unanimous consent.

The Senate sometimes has considered such debt limit measures for days and amended them. In 1985, for example, the Senate added extensive budget enforcement procedures (the Balanced Budget and Emergency Deficit Control Act of 1985, also known as "Gramm-Rudman-Hollings") to H.J.Res 372, a measure that the House had originated under the Gephardt rule. More recently, in 2010, the Senate added statutory "pay-as-you-go" enforcement procedures (often referred to as PAYGO) to H.J.Res 45, a measure that the House had originated under the Gephardt rule pursuant to the adoption of the FY2010 budget resolution (S.Con.Res. 13, 111th Congress). The Senate passed the measure, as amended, on January 28, 2010, and the House subsequently passed the measure without further amendment on February 4, 2010.10 In such cases that the Senate amended the rule-initiated debt limit legislation, the House was required to vote on the Senate-amended legislation before it was sent to the President.

Overall, from the time the rule was established in 1980 to the end of the 111th Congress (2010), the House had originated 20 joint resolutions under this procedure. The Senate had passed 16 of these joint resolutions, passing 10 without amendment and six with amendments.11 Of the 20 joint resolutions originated by the House under the Gephardt rule, 15 have been enacted into law.12

In 11 of the 31 years between 1980 and 2010, the rule was either suspended (1988, 1990-1991, 1994-1997, and 1999-2000) or repealed (2001-2002) by the House. In most cases, the House suspended the rule because legislation changing the statutory limit was not necessary at the time. In addition, in four years, the House and Senate did not complete action on a budget resolution for that year (1998, 2004, 2006, and 2010).

Congressional Disapproval Procedures

In the past six years, legislation adjusting the debt limit twice has included congressional disapproval procedures, effectively providing Congress with a second opportunity to consider the adjustment to the debt limit.

In the first instance, enacted as part of the Budget Control Act of 2011 (P.L. 112-25), signed into law on August 2, 2011, special procedures allowed for congressional disapproval of the increases to the debt limit authorized by the act. The act authorized increases to the debt limit by at least $2.1 trillion (and up to $2.4 trillion) in three installments. First, upon the certification by the President that the debt subject to limit was within $100 billion of the debt limit, the debt limit was increased by $400 billion immediately.13 Second, if Congress did not enact into law a joint resolution of disapproval within 50 calendar days of receipt of the certification, the debt limit was to be increased by an additional $500 billion. The House passed a disapproval resolution (H.J.Res. 77), but the Senate did not.14 If Congress had enacted a joint resolution of disapproval (presumably over a presidential veto), the debt limit would not have been increased by the additional $500 billion, and the Office of Management and Budget would have been required to sequester budgetary resources on a "pro rata" basis, subject to sequestration procedures and exemptions provided in Sections 253, 255, and 256 of the Balanced Budget and Emergency Deficit Control Act of 1985, as amended.15

Third, after the debt limit had been increased by the first $900 billion and upon another certification that the debt subject to limit was again within $100 billion of the debt limit, Congress had 15 calendar days to enact into law a joint resolution of disapproval to prevent the third automatic increase in the debt limit (again over a presumed presidential veto).16 If Congress did not enact such resolution, the debt limit was to be increased by one of three amounts: (1) $1.2 trillion; (2) an amount between $1.2 trillion and $1.5 trillion if Congress passed and the President signed into law legislation introduced by the Joint Select Committee on Deficit Reduction;17 or (3) $1.5 trillion, if a constitutional amendment requiring a balanced budget was submitted to the states for ratification. The House again adopted another disapproval resolution (H.J.Res 98), but the Senate subsequently rejected a motion to proceed to the resolution. Therefore, the debt limit was increased by $1.2 trillion, because other criteria that would have allowed for a larger amount were not met.

In summary, while an initial increase in the debt limit of $400 billion was effective immediately and not subject to congressional disapproval, subsequent additional increases of $500 billion and $1.2 trillion were subject to congressional disapproval. That is, for either of the two subsequent additional increases in the debt limit, if Congress had enacted a joint resolution of disapproval, the debt limit would not have been increased.

Expedited procedures that limited debate and prevented amendments were established for the joint resolution of disapproval to ensure timely consideration. Although only a majority of each chamber would have been necessary to agree to a resolution of disapproval, to prevent an increase, supermajority support would have been necessary. This is because if the Treasury had advised the President that further borrowing was required to meet existing commitments, the President might normally be expected to veto the congressional resolution of disapproval. Congress can override a presidential veto, but to do so would require the support of two-thirds of each chamber.

In 2013, similar congressional disapproval procedures were included in legislation suspending the debt limit through February 7, 2014 (H.R. 2775, 113th Congress). In this instance, Congress had 22 calendar days to enact, presumably over the President's veto, legislation disapproving the suspension and subsequent adjustment to the debt limit authorized by the Default Prevention Act of 2013 (Section 1002 of P.L. 113-46, Continuing Appropriations Act, 2014, enacted on October 17, 2013). On October 30, pursuant to the act and H.Res. 391, the House passed a joint resolution disapproving the suspension of the debt limit by a vote of 222-191.18 On October 29, 2013, however, the Senate rejected a motion to proceed to its own disapproval resolution (S.J.Res. 26) by a vote of 45-54, effectively precluding any further congressional action.19

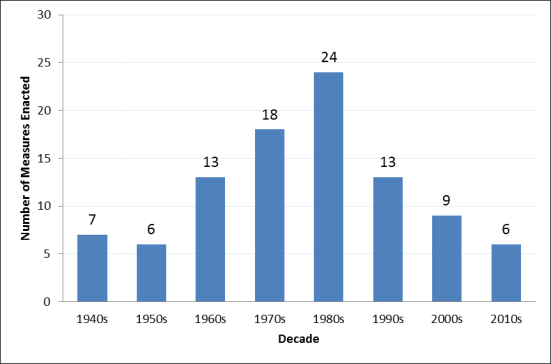

Measures Adjusting the Public Debt Limit

A total of 96 debt limit measures have been enacted into law since 1940 (see Figure 1). The number of laws rose steadily from the 1950s through the 1980s, from six to 24, but dropped to 13 in the 1990s. Six of the 13 laws enacted in the 1990s were temporary extensions over a three-month period in 1990, enacted largely to accommodate lengthy negotiations during a budget summit between Congress and the President. Nine debt limit laws were enacted in the 2000s, and six debt limit laws have been enacted so far in this decade.

As mentioned previously, debt limit legislation has been developed and considered under regular legislative procedures in both chambers, pursuant to the House's so-called Gephardt rule, or as part of the budget reconciliation process. Of the total 96 debt limit measures enacted into law since 1940, 77 were considered under regular legislative procedures, 15 were initiated pursuant to the Gephardt rule, and four were considered as part of omnibus budget reconciliation legislation. Compared with regular legislative procedures, the Gephardt rule accelerates action in the House (but not the Senate), and the budget reconciliation process expedites consideration in both chambers.

Table 1 provides information on the 28 measures adjusting the public debt limit enacted since 1990. Of these 28 measures, 21 were considered under regular legislative procedures in both chambers either as stand-alone legislation (9 measures) or as part of legislation involving other matters (12 measures), 4 were initiated pursuant to the Gephardt rule, and 3 were considered as part of omnibus budget reconciliation legislation. In two instances, the debt limit legislation also included procedures to provide for a congressional disapproval process.

|

Bill Number |

Procedure |

Title of Act |

Nature of Adjustment |

Public Law (Date Enacted) |

|

Regular legislative procedures |

To provide for a temporary increase in the public debt limit |

Temporary increase |

P.L. 101-350 |

|

|

Regular legislative procedures |

To extend the temporary increase in the public debt limit |

Temporary increase |

P.L. 101-405 |

|

|

Regular legislative procedures |

Making further continuing appropriations for the fiscal year 1991, and for other purposes |

Temporary increase |

P.L. 101-412 |

|

|

Regular legislative procedures |

Making further continuing appropriations for the fiscal year 1991, and for other purposes |

Temporary increase |

P.L. 101-444 |

|

|

Regular legislative procedures |

Making further continuing appropriations for the fiscal year 1991, and for other purposes |

Temporary increase |

P.L. 101-461 |

|

|

Regular legislative procedures |

Making further continuing appropriations for the fiscal year 1991, and for other purposes |

Temporary increase |

P.L. 101-467 |

|

|

Reconciliation process |

Omnibus Budget Reconciliation Act of 1990 |

Permanent increase |

P.L. 101-508 |

|

|

Regular legislative procedures |

To provide for a temporary increase in the public debt limit |

Temporary increase |

P.L. 103-12 |

|

|

Reconciliation process |

Omnibus Budget Reconciliation Act of 1993 |

Permanent increase |

P.L. 103-66 |

|

|

Regular legislative procedures |

To guarantee the timely payment of Social Security benefits in March 1996 |

Temporary exemption for certain borrowing |

P.L. 104-103 |

|

|

Regular legislative procedures |

To guarantee the continuing full investment of Social Security and other federal funds in obligations of the United States |

Temporary exemption for certain borrowing |

P.L. 104-115 |

|

|

Regular legislative procedures |

Contract with America Advancement Act of 1996 |

Permanent increase |

P.L. 104-121 |

|

|

Reconciliation process |

Balanced Budget Act of 1997 |

Permanent increase |

P.L. 105-33 |

|

|

Regular legislative procedures |

A bill to amend title 31 of the United States Code to increase the public debt limit |

Permanent increase |

P.L. 107-199 |

|

|

"Gephardt rule" procedures |

Increasing the statutory limit on the public debt |

Permanent increase |

P.L. 108-24 |

|

|

Regular legislative procedures |

A bill to amend title 31 of the United States Code to increase the public debt limit |

Permanent increase |

P.L. 108-415 |

|

|

"Gephardt rule" procedures |

Increasing the statutory limit on the public debt |

Permanent increase |

P.L. 109-182 |

|

|

"Gephardt rule" procedures |

Increasing the statutory limit on the public debt |

Permanent increase |

P.L. 110-91 |

|

|

Regular legislative procedures |

Housing and Economic Recovery Act of 2008 |

Permanent increase |

P.L. 110-289 |

|

|

Regular legislative procedures |

Emergency Economic Stabilization Act of 2008 |

Permanent increase |

P.L. 110-343 |

|

|

Regular legislative procedures |

American Recovery and Reinvestment Act of 2009 |

Permanent increase |

P.L. 111-5 |

|

|

Regular legislative procedures |

To permit continued financing of government operations |

Permanent increase |

P.L. 111-123 |

|

|

"Gephardt rule" procedures |

Increasing the statutory limit on the public debt |

Permanent increase |

P.L. 111-139 |

|

|

Regular legislative procedures |

Budget Control Act of 2011 |

Permanent increase, in three installments, subject to congressional disapproval process |

P.L. 112-25 |

|

|

Regular legislative procedures |

No Budget, No Pay Act of 2013 |

Suspended statutory limit through May 18, 2013, with adjustment to limit at end of suspension period |

P.L. 113-3 |

|

|

Regular legislative procedures |

Default Prevention Act of 2013 (Section 1002 of Continuing Appropriations Act, 2014) |

Suspended statutory limit through February 7, 2014, with adjustment to limit at end of suspension period, subject to congressional disapproval process |

P.L. 113-46 |

|

|

Regular legislative procedures |

Temporary Debt Limit Extension Act |

Suspended statutory limit through March 15, 2015, with adjustment to limit at end of suspension period |

P.L. 113-83 |

|

|

Regular legislative procedures |

Bipartisan Budget Act of 2015 |

Suspended statutory limit through March 15, 2017, with adjustment to limit at end of suspension period |

P.L. 114-74 |

Sources: Office of Management and Budget, Budget of the United States Government, Fiscal Year 2017, Historical Tables, Table 7.3; and the Legislative Information System (LIS).

Author Contact Information

Acknowledgments

This report was originally written with Robert Keith, former specialist in American National Government at CRS. The current author, however, assumes responsibility for its current content.

Footnotes

| 1. |

In a few instances, agencies such as the Tennessee Valley Authority operate within their own borrowing limits established separately in law. For a discussion of federal debt, the debt limit, and debt management practices, see the Office of Management and Budget, Budget of the United States Government, Fiscal Year 2016, Analytical Perspectives, pp. 31-46. For an additional discussion of issues related to increasing the debt limit, see CRS Report RL31967, The Debt Limit: History and Recent Increases. |

| 2. |

See, for example, H.R. 1314, which suspended the debt limit through March 15, 2017 (P.L. 114-74, enacted on November 2, 2015). For further information on recent debt limit legislation, see CRS Report R43389, The Debt Limit Since 2011. |

| 3. |

The congressional budget process is provided for by the Congressional Budget Act of 1974, as amended (codified at 2 U.S.C. 601-688). |

| 4. |

The Senate adopted a rule prohibiting the consideration of a budget reconciliation bill pursuant to the FY2016 budget resolution that "would increase the public debt limit" (see Section 2001(b) of S.Con.Res. 11, 114th Congress). |

| 5. |

See the discussion under section "Other Legislation and the Origination Clause" of CRS Report RL31399, The Origination Clause of the U.S. Constitution: Interpretation and Enforcement. |

| 6. |

The Senate, as noted below, also has originated debt limit legislation. |

| 7. |

For more information on the budget reconciliation process, see CRS Report RL33030, The Budget Reconciliation Process: House and Senate Procedures. |

| 8. |

For further information, see archived CRS Report RL31913, Debt Limit Legislation: The House "Gephardt Rule". |

| 9. |

The "Gephardt rule" was established by P.L. 96-78 (93 Stat. 589-591; September 29, 1979) and first applied in calendar year 1980. It originally was designated as House Rule XLIX. The House recodified the rule as House Rule XXIII at the beginning of the 106th Congress (1999-2000), repealed it at the beginning of the 107th Congress (2001-2002), and reinstated it, as new Rule XXVII, at the beginning of the 108th Congress (2003-2004). The rule was redesignated (without change) as Rule XXVIII during the 110th Congress (2007-2008) upon the enactment of the Honest Leadership and Open Government Act of 2007 (S. 1, P.L. 110-81, September 14, 2007; see Section 301(a)). |

| 10. |

President Obama signed it into law on February 12, 2010 (P.L. 111-139). |

| 11. |

Of the remaining four joint resolutions originated pursuant to the Gephardt rule, the Senate began consideration on one but came to no resolution on it, and it took no action on three. |

| 12. |

In other words, only one of the 16 joint resolutions passed by the Senate was not signed into law. Specifically, during the second session of the 99th Congress, the Senate passed, as amended, the joint resolution (H.J.Res. 668) automatically engrossed by the House and requested a conference with the House, but no further action was taken. |

| 13. |

President Obama submitted such certification on August 2, 2011. It is available at http://www.whitehouse.gov/the-press-office/2011/08/02/message-president-us-congress. |

| 14. |

The House passed H.J.Res. 77 on September 14, 2011. See Congressional Record, daily edition, vol. 157 (September 14, 2011), pp. H6156-H6168. The Senate, however, did not take any action on this joint resolution. It had previously rejected a motion to proceed to a Senate disapproval resolution (S.J.Res. 25) on September 8, 2011. See Congressional Record, daily edition, vol. 157 (September 8, 2011), p. S5466. |

| 15. |

Sequestration is a process of automatic, largely across-the-board spending cuts to non-exempt programs. Under the specified procedures, the cuts would be equally split between defense and non-defense nonexempt programs. |

| 16. |

President Obama submitted such certification on January 12, 2012. It is available at http://www.whitehouse.gov/the-press-office/2012/01/12/letter-president-speaker-house-representatives-and-president-senate-rega. |

| 17. |

The debt limit increase would have been equal to the amount by which the legislation reduces the deficit, if such amount exceeded $1.2 trillion, up to $1.5 trillion. |

| 18. |

See Congressional Record, daily edition, vol. 159 (October 29-30, 2013), pp. H6872-H6876, H6928. |

| 19. |

See Congressional Record, daily edition, vol. 159 (October 29, 2013), pp. S7585-S7595. |