Funding and Financing Highways and Public Transportation

For many years, federal surface transportation programs were funded almost entirely from taxes on motor fuels deposited in the Highway Trust Fund (HTF). Although there has been some modification to the tax system, the tax rates, which are fixed in terms of cents per gallon, have not been increased at the federal level since 1993. Prior to the recession that began in 2007, annual increases in driving, with a concomitant increase in fuel use, were sufficient in most years to keep revenue rising steadily. This is no longer the case. Although vehicle miles traveled have recently surpassed prerecession levels, future increases in fuel economy standards are expected to reduce motor fuel consumption and therefore fuel tax revenue in the years ahead.

Congress has yet to address the surface transportation program’s fundamental revenue issues, and has given limited legislative consideration to raising fuel taxes in recent years. Instead, since 2008 Congress has financed the federal surface transportation program by supplementing fuel tax revenues with transfers from the U.S. Treasury general fund. The most recent reauthorization act, the Fixing America’s Surface Transportation Act (FAST Act; P.L. 114-94), was enacted on December 4, 2015, and authorized spending on federal highway and public transportation programs through September 30, 2020. The act provided $70 billion in general fund transfers to the HTF to support the programs over the five-year life of the act. This use of general fund transfers to supplement the HTF will have been the de facto funding policy for 12 years when the FAST Act expires. The FAST Act did not address funding of surface transportation programs over the longer term. Congressional Budget Office (CBO) projections indicate that the HTF revenue shortfalls relative to spending will reemerge following expiration of the FAST Act.

The trust fund financing system (which supports both federal highway and public transportation programs) faces a number of challenges. As Congress examines possible options for financing surface transportation infrastructure, it may consider several key points:

Raising motor fuel taxes could provide the HTF with sufficient revenue to fully fund the program in the near term, but may not be a viable long-term solution due to expected declines in fuel consumption. It would also not address the equity issue arising from the increasing number of personal and commercial vehicles that are powered electrically and therefore do not pay motor fuel taxes.

Replacing the fuels tax with a mileage-based road user charge or vehicle miles traveled (VMT) charge would need to overcome a variety of financial, administrative, and privacy barriers, but could be a solution in the longer term.

Treasury general fund transfers could continue to be used to make up for the HTF’s projected shortfalls but could require budget offsets of an equal amount.

The political difficulty of adequately funding the HTF could lead Congress to consider altering the trust fund system or eliminating it altogether. This might involve a reallocation of responsibilities and obligations among federal, state, and local governments.

Private investment and federal loans can meet some surface transportation needs, but many projects are not well suited to alternative financing.

Tolling may be an effective way to finance specific roads, bridges, or tunnels that are likely to have heavy use and are located such that the tolls are difficult to evade, but tolls are unlikely to provide broad financial support for surface transportation programs.

Funding and Financing Highways and Public Transportation

Jump to Main Text of Report

Contents

- Introduction

- The Highway Trust Fund Financing Dilemma

- What Congress Faces

- The Underlying Problem: Spending Exceeds Revenues

- The Resulting Funding Shortfalls

- Existing Highway Fuel Taxes

- How the Rates Have Been Raised Since 1983

- The "Great Compromise" and the Highway "User Fee"

- 50/50 Share: Deficit Reduction/Highway Trust Fund

- More for Deficit Reduction

- Alternatives for HTF Finance

- "Fixing" the Gas Tax

- Providing a Tax Rebate to Offset a Fuels Tax Increase

- Switching to Sales Taxes

- Mileage-Based Road User Charges

- Mileage-Based Road User Charges and Non-highway Programs

- Other Options to Preserve the Highway Trust Fund

- The Future of the Trust Fund

- Making a General Fund Share Permanent

- Toll Financing of Federal-Aid System Highways

- Options for Expanded Use of Tolling

- Value Capture

- Public-Private Partnerships

- Municipal Bonds

- Transportation Infrastructure Finance and Innovation Act (TIFIA) Financing

- National Infrastructure Bank

- State Infrastructure Banks

Summary

For many years, federal surface transportation programs were funded almost entirely from taxes on motor fuels deposited in the Highway Trust Fund (HTF). Although there has been some modification to the tax system, the tax rates, which are fixed in terms of cents per gallon, have not been increased at the federal level since 1993. Prior to the recession that began in 2007, annual increases in driving, with a concomitant increase in fuel use, were sufficient in most years to keep revenue rising steadily. This is no longer the case. Although vehicle miles traveled have recently surpassed prerecession levels, future increases in fuel economy standards are expected to reduce motor fuel consumption and therefore fuel tax revenue in the years ahead.

Congress has yet to address the surface transportation program's fundamental revenue issues, and has given limited legislative consideration to raising fuel taxes in recent years. Instead, since 2008 Congress has financed the federal surface transportation program by supplementing fuel tax revenues with transfers from the U.S. Treasury general fund. The most recent reauthorization act, the Fixing America's Surface Transportation Act (FAST Act; P.L. 114-94), was enacted on December 4, 2015, and authorized spending on federal highway and public transportation programs through September 30, 2020. The act provided $70 billion in general fund transfers to the HTF to support the programs over the five-year life of the act. This use of general fund transfers to supplement the HTF will have been the de facto funding policy for 12 years when the FAST Act expires. The FAST Act did not address funding of surface transportation programs over the longer term. Congressional Budget Office (CBO) projections indicate that the HTF revenue shortfalls relative to spending will reemerge following expiration of the FAST Act.

The trust fund financing system (which supports both federal highway and public transportation programs) faces a number of challenges. As Congress examines possible options for financing surface transportation infrastructure, it may consider several key points:

- Raising motor fuel taxes could provide the HTF with sufficient revenue to fully fund the program in the near term, but may not be a viable long-term solution due to expected declines in fuel consumption. It would also not address the equity issue arising from the increasing number of personal and commercial vehicles that are powered electrically and therefore do not pay motor fuel taxes.

- Replacing the fuels tax with a mileage-based road user charge or vehicle miles traveled (VMT) charge would need to overcome a variety of financial, administrative, and privacy barriers, but could be a solution in the longer term.

- Treasury general fund transfers could continue to be used to make up for the HTF's projected shortfalls but could require budget offsets of an equal amount.

- The political difficulty of adequately funding the HTF could lead Congress to consider altering the trust fund system or eliminating it altogether. This might involve a reallocation of responsibilities and obligations among federal, state, and local governments.

- Private investment and federal loans can meet some surface transportation needs, but many projects are not well suited to alternative financing.

- Tolling may be an effective way to finance specific roads, bridges, or tunnels that are likely to have heavy use and are located such that the tolls are difficult to evade, but tolls are unlikely to provide broad financial support for surface transportation programs.

Introduction

Almost every conversation about surface transportation finance begins with a two-part question: What are the "needs" of the national transportation system, and how does the nation pay for them? This report is aimed almost entirely at discussing the "how to pay for them" question. Since 1956, federal surface transportation programs have been funded largely by taxes on motor fuels that flow into the Highway Trust Fund (HTF). A steady increase in the revenues flowing into the HTF due to increased motor vehicle use and occasional increases in fuel tax rates accommodated growth in surface transportation spending over several decades. In 2001, though, trust fund revenues stopped growing faster than spending. In 2008 Congress began providing Treasury general fund transfers to keep the HTF solvent.1

Every year since 2008, there has been a gap between the dedicated tax revenues flowing into the HTF and the cost of the surface transportation spending Congress has authorized. Congress has filled these shortfalls with a series of further transfers, largely from the Treasury's general fund. These transfers have shifted a total of $143.6 billion to the HTF. The last $70 billion of these transfers were authorized in the Fixing America's Surface Transportation Act (FAST Act; P.L. 114-94), which was signed by President Barack Obama on December 4, 2015.2 The FAST Act funds federal surface transportation programs from FY2016 through FY2020. When the act expires the de facto policy of relying on general fund transfers to sustain the HTF will be 12 years old.

Congressional Budget Office (CBO) projections indicate that the imbalance between motor fuel tax receipts and HTF expenditures will reemerge and the HTF balance will approach zero in FY2021. In consequence, funding and financing surface transportation is expected to continue to be a major issue for Congress.

The Highway Trust Fund Financing Dilemma

The HTF has two separate accounts—highways and mass transit. The primary revenue sources for these accounts are an 18.3-cent-per-gallon federal tax on gasoline and a 24.3-cent-per-gallon federal tax on diesel fuel. Although the HTF has other sources of revenue, such as truck registration fees and a truck tire tax, and is also credited with interest paid on the fund balances held by the U.S. Treasury, fuel taxes in most years provides roughly 85%-90% of the amounts paid into the fund by highway users. The transit account receives 2.86 cents per gallon of fuel taxes, with the remainder of the tax revenue flowing into the highway account. An additional 0.1-cent-per-gallon fuel tax is reserved for the Leaking Underground Storage Tank (LUST) Fund, which is not part of the transportation program.

Since the trust fund was created in 1956, motor fuel taxes have increased four times: in 1959, 1982, 1990, and 1993.

Since the 1993 increase, additional changes to the taxation structure have modestly boosted trust fund revenues. The American Jobs Creation Act of 2004 (P.L. 108-357), for example, provided the trust fund with increased future income by changing elements of federal "gasohol" taxation. In 2005, the Safe, Accountable, Flexible, Efficient Transportation Equity Act: A Legacy for Users (P.L. 109-59; SAFETEA) included a number of changes designed to bolster the trust fund, mainly by addressing tax fraud. SAFETEA also provided for the transfer of some general fund revenue associated with transportation-related activities to the trust fund. It was believed at the time of SAFETEA's passage that the tax changes, a $12.5 billion unexpended balance in the trust fund, and higher fuel tax revenue due to expected economic growth would be sufficient to finance the surface transportation program through FY2009.3 This prediction proved to be incorrect. The shortfalls resulting from the overly optimistic forecasts associated with SAFETEA were rectified by Treasury general fund contributions. In September 2008, Congress enacted a bill that transferred $8 billion of Treasury general funds to shore up the HTF. Other transfers followed (see Table 1).

The era of automatic trust fund growth may be over. Annual vehicle miles traveled (VMT) are no longer increasing at the 2% average rate experienced from the 1960s until 2008; although vehicle use is growing again after slumping between 2008 and 2012 due to the sluggish economy, total mileage is projected to grow at an average of roughly 1% per year over the next 20 years.4 Meanwhile, other policy changes are weakening the link between driving activity and motor fuel tax revenues. Under new rules issued in 2012, combined new passenger car and light truck Corporate Average Fuel Economy standards are expected to reach 41.0 miles per gallon in model year 2021 and 49.7 miles per gallon in model year 2025.5 This will eventually reduce the number of gallons of fuel used, although the impact in the near term will be modest. The expanding fleets of hybrid and electric vehicles, respectively, pay less or nothing by way of fuel taxes, raising equity issues that are likely to become more prominent as the electric vehicle fleet expands.6

An increase in the existing fuel tax rates would provide immediate relief to the trust fund. As a rule of thumb, adding a penny to federal motor fuel taxes provides the trust fund with roughly $1.5 billion to $1.7 billion per year.7 The prospect of reduced motor fuel consumption, however, casts doubt on the ability of the motor fuel taxes to support increased surface transportation spending beyond the next decade, even with modest increases in tax rates.8

Table 1. Transfers to the Highway Trust Fund

(in billions of dollars; reflects sequestration for FY2013 and FY2014)

|

Public Law |

Effective Date |

Highway Account |

Mass Transit Account |

Highway Trust Fund Total |

||||||

|

Sept. 15, 2008 |

|

|

|

|||||||

|

Aug. 7, 2009 |

|

|

|

|||||||

|

Mar. 18, 2010 |

|

|

|

|||||||

|

July 6, 2012 |

|

|||||||||

|

From LUST |

For FY2012 |

|

|

|

||||||

|

From general fund |

For FY2013 |

|

|

|

||||||

|

From general fund |

For FY2014 |

|

|

|

||||||

|

Aug. 8, 2014 |

|

|

|

|||||||

|

From LUST |

Aug. 8, 2014 |

|

|

|

||||||

|

July 31, 2015 |

|

|

|

|||||||

|

|

|

|

||||||||

|

From general fund |

Dec. 4, 2015 |

|

|

|

||||||

|

From LUST |

Dec. 4, 2015 |

|

|

|

||||||

|

From LUST |

Oct. 1, 2016 |

|

|

|

||||||

|

From LUST |

Oct. 1, 2017 |

|

|

|

||||||

|

General fund total |

|

|

|

|||||||

|

LUST fund total |

|

|

|

|||||||

|

Total transfers |

|

|

|

|||||||

Sources: Public laws as indicated. Sequestration amounts from FHWA.

Notes: Transfers are from the Treasury's general fund unless indicated. LUST refers to the Leaking Underground Storage Tank Trust Fund administered by the Environmental Protection Agency.

What Congress Faces

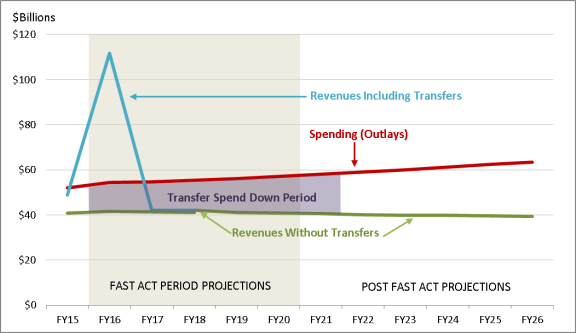

Since FY2008, the balance of federal highway user tax revenues in the HTF has been inadequate to fund the surface transportation program authorized by Congress.9 The 2015 surface transportation act addressed the HTF shortfall through FY2020 by authorizing the use of Treasury general funds for transportation purposes. CBO projects that from FY2021 to FY2026 the gap between dedicated surface transportation revenues and spending will average $20.1 billion annually (Table 2).10 In 2020, as Congress considers surface transportation reauthorization, it could again face a choice between finding new sources of income for the surface transportation program and settling for a smaller program, which might look very different from the one currently in place. Figure 1 shows the impact of the general fund transfers within the context of the underlying imbalance between HTF revenues and projected spending for FY2016-FY2026.

|

|

Source: CRS, based on CBO, Highway Trust Fund Projections: June 2017 HTF Baseline 2016-2027. Notes: Includes highway account and mass transit accounts combined. Revenues include interest on HTF balances. The shading between spending and revenues indicates the period that the HTF balance is maintained by the transfers from the general fund and the LUST fund. |

The Underlying Problem: Spending Exceeds Revenues

Table 2 provides projections of the gap between HTF receipts and outlays following the expiration of the FAST Act at the end of FY2020. In recent decades, Congress has typically sought to reauthorize surface transportation programs for periods of five or six years. As the table indicates, a five-year reauthorization beginning in FY2021 faces a projected gap between revenues and outlays of nearly $101 billion. A six-year reauthorization would face a gap of almost $125 billion.11 These projections assume that spending on federal highway and public transportation programs would remain as it is today, adjusted for anticipated inflation.

|

Fiscal Year |

HTF Revenue |

HTF Outlays |

Difference |

||||||

|

2021 |

|

|

|

||||||

|

2022 |

|

|

|

||||||

|

2023 |

|

|

|

||||||

|

2024 |

|

|

|

||||||

|

2025 |

|

|

|

||||||

|

2026 |

|

|

|

||||||

|

5-YR: FY2021-2025 total |

|

|

|

||||||

|

5-YR: FY2021-2025 average |

|

|

|

||||||

|

6-YR: FY2021-2026 total |

|

|

|

||||||

|

6-YR: FY2021-2026 average |

|

|

|

Source: CRS calculations based on CBO, Highway Trust Fund Projections: June 2017 HTF Baseline 2016-2027.

Notes: Includes combined figures from both the highway account and the mass transit account. The "HTF Revenue" column includes interest on the HTF balances.

The Resulting Funding Shortfalls

When the FAST Act expires at the end of FY2020, the balance in the HTF resulting from previous years' income is expected to be $12.1 billion—an amount equal to approximately two and a half months of outlays. CBO projects that this balance, plus incoming revenue, will allow the Federal Highway Administration (FHWA) and the Federal Transit Administration (FTA) to pay their obligations to states and transit agencies until sometime in FY2021. However, without a reduction in the size of the surface transportation programs, an increase in revenues, or further general fund transfers, the balance in the HTF is projected to be close to zero near the end of FY2021 (see Table 3). At that point, both FHWA and FTA would likely have to delay payments for completed work.12

|

2021 |

2022 |

2023 |

2024 |

2025 |

2026 |

|||||||||||||

|

Start-of-year HTF balancea |

|

|

|

|

|

|

||||||||||||

|

Revenues minus outlays |

|

|

|

|

|

|

||||||||||||

|

End-of-year HTF shortfall |

|

|

|

|

|

|

Based strictly on projected income and expenses, the HTF would move from a positive balance of $12.1 billion at the start of FY2021 to a negative balance of $88.5 billion at the end of FY2025. However, current law does not allow the HTF to incur negative balances. Unless this is changed, $88.5 billion represents the minimum amount the House Ways and Means Committee and the Senate Committee on Finance would need to find over the FY2021-FY2025 period in some combination of additional revenue and budget offsets for general fund transfers, should Congress choose to continue funding surface transportation at the current, or "baseline," level, adjusted for inflation.13 Because the HTF currently provides all but about $2 billion of annual spending authorized for the highway and transit programs (the main exception being the FTA Capital Investment Grants Program), these numbers have implications for the size of the program Congress may approve to follow the FAST Act.

Highway and transit spending based solely on the revenue projected to flow into the HTF under current law would be limited to roughly $41 billion in FY2021, significantly less than the "baseline" FY2021 outlays of roughly $58 billion. The projected year-to-year decline in HTF revenue implies that FHWA and FTA would have less contract authority each year to spend on projects through FY2026.14

Reducing expenditures might not provide immediate relief from the demands on the HTF. Because transportation projects can take years to complete, both the highway and public transportation programs must make payments in future years pursuant to commitments that have already been incurred. As of FY2018, obligated but unspent contract authority for highway projects in progress is projected to be roughly $64 billion. This does not count another $24 billion in available but unobligated contract authority. For public transportation programs the equivalent figures for FY2018 are projected to be almost $16 billion in unpaid obligations and another $10 billion in unobligated contract authority.15 The obligated amounts represent legal obligations of the U.S. government and must be paid out of future years' HTF receipts.

Existing Highway Fuel Taxes16

The first federal tax on gasoline (1 cent per gallon) was imposed in 1932, during the Hoover Administration, as a deficit-reduction measure following the depression-induced fall in general revenues. The rate was raised to help pay for World War II (to 1.5 cents per gallon) and raised again during the Korean War (to 2 cents per gallon). The Highway Revenue Act of 1956 (P.L. 84-627) established the HTF and raised the rate to 3 cents per gallon to pay for the construction of the Interstate Highway System. The Federal-Aid Highway Act of 1959 (P.L. 86-342) raised the rate to 4 cents per gallon. The gasoline tax remained at 4 cents from October 1, 1959, until March 31, 1983. During this period, revenues grew automatically from year to year as fuel consumption grew along with increases in vehicle miles traveled.

Since 1983 lawmakers have passed legislation raising the tax rates on highway fuel use three times. Although infrequent, these rate increases were quite large in a proportional sense. The gasoline tax was raised on April 1, 1983, from 4 to 9 cents per gallon, a 125% increase; on September 1, 1990, from 9 to 14 cents (not counting the additional 0.1 cent for LUST), or 55%; and on October 1, 1993, from 14 to 18.3 cents, or 31%.17

How the Rates Have Been Raised Since 1983

Increasing the rate of the fuel taxes has never been popular. The last three increases were accomplished with difficulty and were influenced by the broader budgetary environment and the politics of the time.18

The "Great Compromise" and the Highway "User Fee"

The increase in the fuel tax rate under the Surface Transportation Assistance Act of 1982 (STAA; P.L. 97-424, Title V) occurred in the lame-duck session of the 97th Congress. In the "Great Compromise," supporters of increased highway spending had come to an agreement with transit supporters (mostly from the Northeast) that a penny of a proposed 5-cents-per-gallon increase would be dedicated to a new mass transit account within the HTF. This meant that support for the bill during the lame-duck session was widespread and bipartisan. During the congressional elections of 1982 the Democrats had picked up 26 seats in the House of Representatives. The economy was experiencing a major recession, and some argued that increased highway spending would stimulate the economy. President Reagan's opposition to an increase in the "gas tax" softened during the lame-duck session. On November 23, 1982, he announced that he would support passage of STAA, even though it would "mean an increase in the highway user fee, or gas tax, of 5 cents a gallon.... Our country's outstanding highway system was built on the user fee principle—that those who benefit from a use should share in its cost."19 Nonetheless, the bill faced a series of filibusters in the Senate, which were eventually overcome by four cloture votes. The conference report was again filibustered, and President Reagan helped secure the votes needed for cloture. President Reagan signed STAA into law on January 6, 1983, more than doubling the highway fuel tax to 9 cents per gallon.20

50/50 Share: Deficit Reduction/Highway Trust Fund

The Omnibus Budget Reconciliation Act of 1990 (OBRA90; P.L. 101-508), enacted November 5, 1990, was passed under the pressure of impending final FY1991 sequestration orders issued by President George H. W. Bush under Title II of P.L. 99-177, the Balanced Budget and Emergency Deficit Control Act of 1985, known as the Gramm-Rudman-Hollings Act (GRH). OBRA90 included budget cuts, tax changes, and the Budget Enforcement Act (P.L. 101-508), which rescinded the FY1991 sequestration orders. OBRA90 also raised the tax on gasoline by 5 cents per gallon, to 14 cents. Half the increase went to the HTF (2 cents to the highway account and 0.5 cents to the mass transit account), with the other 2.5 cents per gallon to be deposited in the general fund for deficit reduction. This was the first time since 1957 the motor fuel tax had been used as a source of general revenue. Section 9001 expressed the sense of Congress that all motor fuel taxes should be directed to the HTF as soon as possible.

More for Deficit Reduction

The Omnibus Budget Reconciliation Act of 1993 (OBRA93; P.L. 103-66) Section 13241(a) made further changes in regard to fuel taxes:

- The 2.5-cents-per-gallon fuel tax dedicated to deficit reduction in OBRA90 was redirected to the HTF beginning October 1, 1995, and its authorization was extended to September 30, 1999.

- The highway account received 2 cents per gallon and the mass transit account 0.5 cents per gallon of the rededicated amount.

- An additional permanent 4.3-cents-per-gallon fuel tax took effect in October 1993 and was dedicated to deficit reduction.

This brought the gasoline tax to 18.3 cents per gallon, although for two years (October 1, 1993, to October 1, 1995) 6.8 cents per gallon of this was deposited in the general fund, dedicated to deficit reduction. On October 1, 1995, the amount going to the general fund dropped to 4.3 cents per gallon, and the amount dedicated to the HTF increased to 14 cents per gallon. Subsequently, under the Taxpayer Relief Act of 1997 (P.L. 105-34), all motor fuel tax revenue was redirected to the HTF (3.45 cents per gallon to the highway account and 0.85 cents to the mass transit account), effective October 1, 1997. (The LUST fund continues to receive the revenue from an additional 0.1 cents-per-gallon tax.)

Since 2001, revenue flowing into the HTF has not met expectations in most years, and has generally lagged inflation since FY2007.21 In some years, HTF revenue has declined even in nominal terms (unadjusted for inflation) due to reduced vehicle travel. Because of the fixed nature of the cents-per-gallon gasoline and diesel taxes, the only way the taxes can generate additional revenue for the HTF is if motor-fuel consumption rises. In recent years, as gasoline prices have fallen, the vehicle miles traveled have increased, and gasoline sales have exceeded 2007 levels.22 An improving U.S. job market and wage growth may have contributed to record high VMT. The renewed popularity of vehicles with relatively low fuel economy suggests demand for motor fuel may remain stronger than anticipated a few years ago. However, to date CBO continues to forecast declines in gasoline tax revenues through FY2027.23

Alternatives for HTF Finance

The political difficulty of increasing motor fuel taxes has led to interest in alternative approaches for supporting the HTF. These involve tying motor fuel tax rates to the price of fuel, changing the structure of the current fuel taxes, and charging drivers for the distance they drive rather than the fuel they consume, as well as freight-related charges and a variety of options unrelated to transportation.

"Fixing" the Gas Tax

A differently designed gas tax might be indexed to both inflation (either inflation generally or highway construction cost inflation) and fuel-efficiency improvements.24 This new design would be imposed after raising the current gas tax rate to compensate for the loss in purchasing power since the last rate increase in 1993.25

If the motor fuels taxes for gasoline and diesel had been adjusted in 2016 to keep pace with the change in the Bureau of Labor Statistics' consumer price index since 1993, the 18.3-cents-per-gallon gasoline tax would now be 31 cents per gallon, and the 24.3-cents-per-gallon diesel tax would be 41.1 cents per gallon. Consequently, the first step in implementing this method of "fixing" the gas tax would be to raise the base tax rate for gasoline by roughly 13 cents per gallon and to raise the rate for diesel by roughly 17 cents per gallon. Future adjustments would depend on the inflation rate in future years.

Tax-rate adjustments to make up for revenue lost due to greater fuel efficiency could be determined by dividing miles driven by vehicle category by the total amount of fuel consumed by that category and comparing the quotient to the previous year. Although fuel-economy standards for new vehicles are to rise sharply over the next few years, the average efficiency of the entire vehicle fleet will rise slowly because of the large number of older vehicles on the road. Consequently, an annual efficiency adjustment to the fuel tax rates would likely be small.

Providing a Tax Rebate to Offset a Fuels Tax Increase

One approach to reducing the political obstacles to higher fuel taxes is to couple a fuels-tax increase with income-tax rebates approximating the average cost of the fuels tax increase to the typical driver. The cost of the rebates would be less than the additional taxes collected because truckers, other commercial users, and individuals who do not file income-tax returns would not receive the rebates. The rebates could be phased out after several years while the higher tax rates would continue.

This solution raises a number of issues. The proposal could be seen, in effect, as a general fund transfer. Depending on the language of the House and Senate budget resolutions, the rebates might have to be offset by spending reductions elsewhere in the federal budget. Also, unless the higher tax rates were indexed for inflation, revenues would again be on a downward slope after the tax increase occurs.

Switching to Sales Taxes

Under the sales tax concept, the federal motor fuel tax would be assessed as a percentage of the retail price of fuel rather than as a fixed amount per gallon. Some states already levy taxes on motor fuels in this way, either alongside or in place of fixed cents-per-gallon taxes on motor fuel purchases.

If fuel prices rise in the future, sales tax revenues could rise from year to year even if consumption does not increase. Conversely, however, a decline in motor fuel prices could lead to a drop in sales tax revenue. Many states that tied fuel taxes to prices after the price shocks of the 1970s encountered revenue shortfalls in the 1980s, when fuel prices fell dramatically. Over a 20-year period, most of these variable state fuel taxes disappeared.26 Recently, however, Virginia eliminated its cents-per-gallon fuel taxes in favor of a sales tax on fuel and a general sales tax increase that was dedicated to transportation purposes. The Virginia law mandates that the tax be imposed on the average wholesale price (calculated twice each year) but sets price floors; if prices of motor fuels fall beneath those floors, the amount of fuel tax charged per gallon is not reduced further.27

A federal sales tax on motor fuel would likely be at best an interim solution to the long-term problem of financing transportation infrastructure because, as with the current motor fuel tax, it relies on fuel consumption to fund transportation programs. To the extent that improved vehicle efficiency or adoption of hybrid or electric vehicles leads to long-term declines in fuel usage, a sales tax on fuel may not lead to increases in trust fund revenues. In addition, a sales tax calibrated to produce a desired amount of revenue in an environment of high motor fuel prices could significantly underperform if fuel prices were to be lower than anticipated.28

Mileage-Based Road User Charges

Economists have long favored mileage-based user charges as an alternative source of highway funding. Under the user charge concept, motorists would pay fees based on distance driven and, perhaps, on other costs of road use, such as wear and tear on roads, traffic congestion, and air pollution. The funds collected would be spent for surface transportation purposes.29

The concept is not new: federal motor fuel taxes are a form of indirect road user charge insofar as road use is loosely related to fuel consumption. Some states have charged trucks by the mile for many years, and toll roads charge drivers based on miles traveled and the number of axles on a vehicle, which is used as a proxy for weight. Recent technological developments, as well as the evident shortcomings of motor fuel taxes, have led to renewed interest in the user charge concept, including establishment of a pilot program in legislation enacted in 2015.

Mileage-based road user charges (often referred to as vehicle miles traveled charges, or VMTs) could range from a flat cent-per-mile charge based on a simple odometer reading to a variable charge based on vehicle movements tracked by the Global Positioning System (GPS). Other proposals envision mileage-based road user charges that would mimic the way Americans now pay their fuel taxes by collecting the charge at the pump. Most road user charge proposals would require electric vehicle users to pay for their use of the roads.

Implementation of a mileage-based road user charge would have to overcome a number of potential disadvantages relative to the motor fuels tax, including public concern about personal privacy; the higher costs to establish, collect, and enforce this charge (estimates range from 5% to 13% of collections); the administrative challenge of the billing process given the size of the vehicle fleet (estimated at roughly 263 million vehicles); and the setting and adjusting of the road user charge rates, which would likely be as controversial as increasing the motor fuels taxes. Another barrier to implementation is how to fairly charge the "unbanked," those who have no bank accounts or credit/debit cards.

A nationwide mileage-based road user charge would be analogous to a national toll. This raises the prospect that vehicles using toll roads might be charged twice, although this effectively happens now in that toll road users also pay tax on the motor fuel they consume while using the toll road. Technically, it would be possible for a road user charge to replace an existing toll, but this could cause complications with respect to the servicing of bonds funded by toll-road revenue.

Mileage-Based Road User Charges and Non-highway Programs

Since 1982, the HTF has financed most federal public transportation programs as well as highway programs. If a mileage-based road user charge were to be used strictly for highway purposes, it might reasonably be characterized as a user fee even if the amount paid by each individual driver does not correspond precisely to the social cost (such as pollution and traffic congestion costs) of that user's driving. A road user charge that funded both highways and public transportation might arguably be seen more as a tax than a user fee. This distinction raises a number of legal issues.30 Any legislation establishing a road user charge would have to clearly identify what the charge would be spent on. If the existing HTF were to be retained, legislation would have to specify what share of the revenue would be credited to the separate highway and mass transit accounts within the fund.

Other Options to Preserve the Highway Trust Fund

In addition to options discussed above, a wide range of additional proposals has been suggested to generate revenue for the HTF. These proposals largely originated from the work of the two SAFETEA congressional commissions and of groups such as the American Association of State Highway and Transportation Officials (AASHTO) and Transportation Research Board (TRB).31 For example, AASHTO's Matrix of Illustrative Surface Transportation Revenue Options lists 33 potential HTF revenue options with yield estimates in tabular form.32 Many of these options involve taxes on freight movements or energy. It should be emphasized that the revenue estimates from these exercises are merely suggestive; the revenue obtained from any given measure would depend on changes in the price of motor fuels, growth in the number of annual auto registrations, and other factors.

The Future of the Trust Fund

If Congress chooses not to impose new taxes and fees dedicated to the HTF, it could still maintain or expand the surface transportation program with general fund monies. Any of the financing options discussed above could be used to sustain the existing federal financing mechanism, the HTF, but could also be used to support the general fund if Congress considers alternatives to the trust fund financing model. This would weaken the historical link between the taxes and fees paid by highway users and spending on the nation's highways and bridges.

The Highway Trust Fund was set up as a temporary device that was supposed to disappear when the Interstate System was finished. It has endured, and its breadth of financing has expanded well beyond the Interstates, most significantly with the 1982 creation of the mass transit account within the fund to support public transportation spending. But the HTF is certainly not essential to a federal role in transportation funding. Congress routinely funds large infrastructure projects, such as those constructed by the Army Corps of Engineers, from general fund appropriations. Before 1956, it funded highway projects using annual appropriations. As recently as the 1990s, significant highway programs such as the Appalachian Development Highway System were funded from the general fund.

One alternative would be to eliminate the trust fund structure, thereby doing away with its complicated budget framework of contract authority, obligations, and apportionments.33 Eliminating the trust fund would force surface transportation to compete with other federal programs for funding each year, possibly leading to less spending on transportation.

There could be advantages to moving away from trust fund financing of surface transportation. Until recently, one of the most intractable arguments in reauthorization debates concerned which states were "donors" to transportation programs and which were "donees." Donor states were states whose highway users were estimated to pay more to the highway account of the HTF than they received. Donee states received more than they paid. The donor-donee dispute was unique to the federal highway program, and occurred largely because of the ability to track federal fuel tax revenues by state. This issue has faded as injections of general fund revenues into the HTF have made all states donees, and would likely disappear if transportation-related taxes were deposited into the general fund instead of the trust fund. Treating fuel taxes as just another source of federal revenue would also dampen the long-standing link between road user charges and program spending. This would provide Congress with greater flexibility to allocate funding among various transportation modes and between transportation and nontransportation uses.

Most trust-fund outlays take the form of formula grants over which states have a great deal of spending discretion. While there are numerous federal requirements attached to trust fund expenditures, there have been until recently relatively few performance-oriented goals that the states are required to meet in selecting projects to be undertaken with federal monies. Performance measures might be easier to implement without formula programs that automatically apportion funding to the states.

Eliminating the trust fund might also allow for creativity in thinking about the provision of transportation infrastructure across the modal boundaries that now define much of federal transportation spending. Historically, important parts of U.S. transportation infrastructure, such as the transcontinental railroads and the Panama Canal, were authorized by specific congressional enactments rather than grant programs. Reconsidering the trust fund structure might reopen discussion of this approach.

Another alternative would be to again devote all trust fund revenues exclusively to highway spending. This would leave transit and other surface transportation programs to be funded exclusively by annual appropriations of general funds. Such a change would have political implications. Since the early 1990s, public transportation and cycling advocates, environmentalists, and a wide range of other groups have become full-fledged supporters of the surface transportation program, as it has benefited their interests. The expanded coalition supporting the surface transportation program played an important role in the hard-fought political battles since the early 1990s to pass multiyear surface transportation bills.

As was made clear by passage of the FAST Act, Congress has chosen to support the current HTF funding model by transferring funds, mostly from the Treasury general fund. Whether such general fund support should continue is likely to become a major point of contention when Congress debates reauthorizing surface transportation programs beyond FY2020.

Making a General Fund Share Permanent

By FY2020, the last year of the FAST Act, federal highway programs will have been funded for 12 years under a de facto policy of providing a Treasury general fund share. Congress could address the inadequacy of motor fuel taxes to meet surface transportation needs by making the general fund share permanent.

The public transportation titles of surface transportation bills already fund the New Starts program with general fund appropriated funds. The Federal Aviation Administration (FAA) budget is also supported by a combination of trust funds and general funds; the general fund amount is supposed to approximate the value of the airways system to military and other government users and to "societal" nonusers (people who do not fly but, for example, benefit from the delivery of freight via aircraft).34 A similar argument could be made regarding the public good benefits of a well-functioning highway system to justify an annual general fund appropriation to support spending on roads.35

Should Congress agree on a future policy of providing an annual general fund share for federal highway funding, the financing structure of the federal-aid highways program could change. Congress would have the choice of appropriating the general fund share to the HTF and maintaining the programmatic status quo, or it could fund some programs from the trust fund and fund others via appropriations. Congress could also consider a two-pronged approach to authorization. It could authorize the trust funded programs separately from the appropriated programs. This would give Congress the option of trust funding a very long (perhaps as much as 10-year) authorization bill for programs that fund projects that typically take many years to plan and complete. The long-term authorization could be paired with a series of short-term bills funded with appropriated general funds for programs whose projects are more likely to be completed quickly.36

Toll Financing of Federal-Aid System Highways

Toll roads have a long history in the United States, going back to the early days of the republic. During the 18th century, most were local roads or bridges that could not be built or improved with local government tax revenue alone. However, beginning with the Federal Aid Road Act of 1916 (39 Stat. 355), federal law has included a prohibition on the tolling of roads that benefited from federal funds.37 During the late 1940s and early 1950s, the prospect of toll revenues allowed states to build thousands of miles of limited-access highways without federal aid and much sooner than would have been the case with traditional funding. Despite this, the tolling prohibition was reiterated in the Federal-Aid Highway Act and Highway Revenue Act of 1956 (70 Stat. 374), which authorized funds for the Interstate System, created the HTF, and raised the fuel taxes to pay for their construction. Over the last three decades the prohibition has been moderated so that exceptions to the general ban on tolling now cover the vast majority of federal-aid roads and bridges. There remains a ban on the tolling of existing Interstate System highway surface lane capacity. While new toll facilities have opened in several states, some of those projects have struggled financially.

Generally, there are three levels of restrictions on tolling of federal-aid highways. Non-Interstate System highways and bridges may be converted to toll roads but only after reconstruction or replacement. Existing Interstate System surface lane capacity may not be converted to toll roads except under the auspices of two small pilot programs. However, Interstate System bridges and tunnels may be converted if they are reconstructed or replaced. New capacity on the federal-aid highway system generally may be tolled. There are no federal restrictions on tolling of roads off of the federal-aid system.

Options for Expanded Use of Tolling

Highway toll revenue nationwide came to $14.025 billion in FY2015, according to FHWA. While the amount of toll revenue has grown significantly in recent years, toll revenue as a share of total spending on highways has been relatively steady for more than half a century, in the range of roughly 5% to 6%.38 On average, facility owners collected $2.38 million per mile of toll road or bridge in FY2015, but revenue per mile varies greatly among toll facilities.39 All revenue from tolls flows to the state or local agencies or private entities that operate tolled facilities; the federal government does not collect any revenue from tolls. However, a major expansion of tolling might reduce the need for federal expenditures on roads. There are three possible means of increasing revenue from tolling:

- Increase the Extent of Toll Roads. FHWA statistics identify 5,882 tolled miles of roads, bridges, and tunnels as of January 1, 2016,40 a net increase of 1,161 miles, or 25%, over 1990.41 Toll-road mileage comprises only 0.6% of the 1,016,964 miles of public roads eligible for federal highway aid.42 While there may be many existing roads on which tolling would be financially feasible, the vast majority of mileage on the federal-aid system probably has too little traffic to make toll collection economically viable.

- Increase Toll-Road Usage. The financing of many of the toll roads constructed in the 20th century was based on the assumption that the new roads would lead to increased vehicle usage. Although vehicles miles traveled declined in the wake of the recession that began in 2007, vehicle use has been rising again since 2014. If this trend continues it bodes well for toll revenues, which would rise with increasing traffic. On the other hand, if demographic trends and social changes, such as the increased popularity of center-city living, eventually lead to slower growth in personal motor vehicle use, then toll revenues may be constrained in the longer term.43 If that proves to be the case, higher traffic volume may contribute little to increased toll revenues.

- Increase the Average Toll per Mile. Raising tolls can be politically challenging, especially when revenue is used for purposes other than building and maintaining the toll facility. Trucking interests frequently raise opposition to rate changes that increase truck tolls relative to automobile tolls. Where roads are operated by private concessionaires, the operators' contracts with state governments typically specify the maximum rate at which tolls can rise. Additionally, large increases can encourage motorists to use competing nontolled routes.

These factors suggest that imposing tolls on individual transportation facilities is likely to be of only limited use in supporting the overall level of highway capital spending. Furthermore, some states, particularly those with low population densities, may have few or no facilities suitable for tolling. Toll collection itself can be costly; collection costs on many existing toll roads exceed 10% of revenues. For these reasons, while tolls may be an effective way of financing specific facilities—especially major roads, bridges, or tunnels that are likely to be used heavily and are located such that the tolls are difficult to evade—they would likely be less effective in providing broad financial support for surface transportation programs.

Value Capture

Value capture represents an attempt to cover part or all of the cost of transportation improvements from landowners or developers who benefit from the resulting increase in the value of real property. Value capture revenue mechanisms include tax increment financing, special assessments, development impact fees, negotiated exactions, and joint development.44 The federal role in value capture strategies may be limited, as the Government Accountability Office (GAO) has noted,45 but it is worth describing these strategies to provide a fuller picture of the ways in which they might supplement or supplant more commonly used funding and financing mechanisms.

Value capture is not a new idea. Land developers built and operated streetcar systems in the late 19th century as a way to sell houses on the urban fringe, for example. Much of the recent experience with value capture has been associated with public transit. GAO found that the most widely used mechanism is joint development, in which a real estate project at or near a transit station is pursued cooperatively between the public and private sectors. An example might involve a transit agency leasing the unused space over a station, its "air rights," to a developer in exchange for a regular payment.

GAO found that joint development has generated relatively small amounts of money for transit agencies. For example, the Washington Metropolitan Area Transit Authority received about $10 million from joint development in FY2016, about 1% of its operating revenue.46 However, less widely used strategies, such as special assessment districts, are estimated to generate significant amounts of funding for specific projects. In a special assessment district, properties within a defined area are assessed a special tax for a specific purpose. A special assessment district in Seattle produced $25 million of the $53 million (47%) needed to fund the South Lake Union streetcar project.47

There has been less use of value capture in highway projects, but this appears to be changing. Texas, for example, has authorized the use of tax increment financing through the creation of transportation reinvestment zones to help fund highway projects.48 Special assessment districts also have been set up in several states, including Florida and Virginia, to fund highway projects. In Virginia a special assessment district was used to help fund the expansion of Route 28 near Washington Dulles International Airport beginning in the late 1980s.49

Public-Private Partnerships

Growing demands on the transportation system and constraints on public resources have led to calls for more private-sector involvement in the provision of highway and transit infrastructure through public-private partnerships (P3s), which can be designed to lessen demands on public-sector funding.50 Private involvement can take a variety of forms, including design-build and design-build-finance-operate agreements. Typically, the "public" in public-private partnerships refers to a state government, local government, or transit agency. The federal government, nevertheless, exerts influence over the prevalence and structure of P3s through its transportation programs, funding, and regulatory oversight.51

To be viable, P3s involving private financing typically require an anticipated project-related revenue stream from a source such as vehicle tolls, freight container fees, or, in the case of transit station development, building rents. Private-sector resources may come from an initial payment to lease an existing asset in exchange for future revenue, as with the Indiana Toll Road and Chicago Skyway, or they may arise from a newly developed asset that creates a new revenue stream. Either way, a facility user fee, such as a toll, is often the key to unlocking private-sector participation and resources.

In some cases, private-sector financing is backed by "availability payments," regular payments made by government to the private entity based on negotiated quality and performance standards of the facility. Aversion in the private sector to the risk that too few users will be willing to pay for use of a new facility has made availability payment P3s more common over the past few years. As a result, state and local governments are retaining this risk, known as demand risk, more often.52

It is widely believed that hundreds of billions of dollars of private monies are available globally for infrastructure investment, such as surface transportation.53 To date, however, the number of transportation P3s in the United States is relatively small, as is the amount of long-term private financing provided. According to one source, from 1993 through September 2017 there were 30 surface transportation P3s involving long-term financing, with total project costs totaling $39 billion. This includes the 99-year lease of the Chicago Skyway; the I-595 managed lanes project in Florida; and the Purple Line light rail transit project in Maryland.54 P3s and private investment in surface transportation are relatively larger in many other countries, including Portugal, Spain, and Australia.55

It is quite possible that private investment will grow in the future, but many impediments remain. Some of the major ones include the relative attractiveness of the tax-exempt financing available to state and local government, political opposition to tolling and privatization, and difficulties associated with project development. Private-sector financing generated through P3s might best be seen as a supplement to traditional public-sector funding rather than as a substitute.

In addition to attracting private capital, P3s may generate new resources for highway and transit infrastructure in at least two ways. First, P3s may improve efficiency through better management and innovation in construction, maintenance, and operation—in effect providing more infrastructure for the same price. Private companies may be more able to examine the full life-cycle cost of investments, whereas public agency decisions are often tied to short-term budget cycles. Such cost reductions may not materialize, however, if the public sector has to spend a substantial amount of time on procurement, oversight, dispute resolution, and litigation. GAO argues that most state governments lack the capacity to manage P3 contracts.56

Second, P3s may reduce government agencies' costs by transferring the financial risks of building, maintaining, and operating infrastructure to private investors. These risks include construction delays, unexpectedly high maintenance costs, and the possibility that demand will be less than forecast. There is a danger, however, that this transfer of risk may prove illusory if major miscalculations force the public agency to renegotiate contracts or provide financial guarantees.57 Moreover, as GAO points out, not all the risks can or should be shifted to the private sector. For instance, private investors are unlikely to accept the risk of higher construction costs due to delays in the environmental review process.58

Municipal Bonds

Municipal bonds, debt instruments used by states and all types of local government, are a major source of financing for transportation infrastructure. The interest on municipal bonds is generally exempt from federal income tax; consequently, an investor will usually accept a lower interest rate than on a non-tax-exempt bond, and the borrower can finance a project at a lower cost. The forgone tax revenue is the federal government's contribution to a project financed with municipal bonds.

Private activity bonds (PABs) are a type of municipal bond in which a state or local government acts as a financial intermediary for a business or individual.59 PABs are not eligible for federal tax exemption unless Congress grants an exception for a certain purpose and other requirements are met. Congress has approved limited use of tax-exempt private activity bonds for airports, docks and wharves, mass commuting facilities, high-speed intercity rail facilities, and qualified highway or surface freight transfer facilities (26 U.S.C. §142). In the case of qualified highway or surface freight transfer facilities, the Secretary of Transportation must approve the issuance of PABs, and the aggregate amount allocated must not exceed $15 billion (26 U.S.C. §142(m)(2)). As of January 2017, $6.6 billion of the $15 billion had been issued to finance 17 projects, and another $4.3 billion had been allocated to eight other projects.60 There have been proposals to increase the bond issuance cap so that PABs, which are seen as an important support for P3 deals, can continue to be issued in the future.

While municipal bonds are a popular financing method, there are a number of potential disadvantages to their use. Because they are issued by state and local government, the federal government has less control over the types of projects supported and the amount of the federal contribution than it does with grant and loan programs. Tax-exempt bonds, moreover, can be an inefficient way to subsidize state and local debt because borrowing costs are reduced by less than the forgone revenue. As the Congressional Budget Office notes, "the remainder of that tax expenditure accrues to bond buyers in the highest income tax brackets."61 Also, tax-exempt bonds are unattractive to investors that do not have a federal tax liability, such as pension funds and foreign individuals and organizations, shrinking the potential funds available to state and local governments.

Tax credit bonds, an alternative type of tax-preferred municipal bond, might help to overcome some of these limitations. Tax credit bonds typically do not pay interest. Instead, the investor receives a tax credit, an amount that is the same for investors in different tax brackets. Tax credit bonds, therefore, are more efficient than tax-exempt bonds because the revenue forgone by the federal government equals the reduction in borrowing costs that state and local governments receive. Unused tax credits may be carried forward to another year or sold to another entity with tax liability. With some types of tax credit bonds known as issuer credit or direct pay bonds, the credit is paid to the issuer and the investor gets interest similar to taxable securities. Consequently, tax credit bonds can be attractive to investors with no federal tax liability.

Federal authority exists for state and local governments to issue some types of tax credit bonds, but none can be used to finance transportation projects. Tax credit bonds authorized by the American Recovery and Reinvestment Act of 2009 (P.L. 111-5), known as Build America Bonds, were used to finance a wide range of projects including transportation. The authorization to issue these bonds expired December 31, 2010.

Transportation Infrastructure Finance and Innovation Act (TIFIA) Financing

An existing federal mechanism for providing credit assistance to relatively large transportation infrastructure projects is financing under the Transportation Infrastructure Finance and Innovation Act (TIFIA) program, enacted in 1998.62 TIFIA provides federal credit assistance in the form of secured loans, loan guarantees, and lines of credit.

Federal credit assistance reduces borrowers' costs and lowers project risk, thereby helping to secure other financing at rates lower than would otherwise be possible. Another purpose of TIFIA funding is to leverage nonfederal funding, including investment from the private sector. Loans must be repaid with a dedicated revenue stream, typically a project-related user fee, such as a toll, but sometimes dedicated tax revenue. As of January 2018, according to DOT, TIFIA had provided assistance of nearly $30 billion to more than 70 projects. The overall cost of the projects supported is estimated to be $107 billion.63

The FAST Act reduced funding for the TIFIA program after it had been greatly increased under the previous authorization, the Moving Ahead for Progress in the 21st Century Act (MAP-21; P.L. 112-141), enacted in July 2012. Prior to MAP-21, the TIFIA authorization was $122 million annually. This was increased to $750 million in FY2013 and $1 billion in FY2014 and FY2015.64 Under the FAST Act, the direct authorization for TIFIA was $275 million in both FY2016 and FY2017, $285 million in FY2018, and $300 million in both FY2019 and FY2020. Because the government expects its loans to be repaid, an appropriation need cover only administrative costs and the subsidy cost of credit assistance. According to the Federal Credit Reform Act of 1990, the subsidy cost is "the estimated long-term cost to the government of a direct loan or a loan guarantee, calculated on a net present value basis, excluding administrative costs."65 According to DOT, $1 in TIFIA funding historically has provided about $10 in credit assistance, a 10% subsidy cost, although in recent years each dollar has provided closer to $14.66

Seen in isolation, the cut in the TIFIA authorization reduced DOT's capacity to issue loans by approximately $7.25 billion in FY2016, assuming a 10% subsidy cost. However, the FAST Act also allowed states to use funds they receive from two other highway programs to pay for the subsidy and administrative costs of credit assistance. These two programs are the Nationally Significant Freight and Highway Projects Program (NSFHPP), authorized at $800 million in FY2016, and the National Highway Performance Program (NHPP), authorized at $22.3 billion in FY2016. If states decide to use their formula funding in this way, the potential amount of loans and other credit assistance may be much greater than would be possible using the $275 million direct authorization alone. The Transportation Investment Generating Economic Recovery (TIGER) Grant Program, funded by general fund appropriations, also can be used by grant recipients to pay the subsidy and administrative costs of a TIFIA loan.67

Several changes to the TIFIA program in the FAST Act were aimed at making it easier to finance smaller projects, particularly those in rural areas. These provisions included

- providing authority for a TIFIA loan to a state infrastructure bank (SIB) to capitalize a "rural project fund";

- adding transit-oriented development (TOD) infrastructure as an eligible project (TOD infrastructure is a "project to improve or construct public infrastructure that is located within walking distance of, and accessible to, a fixed guideway transit facility,68 passenger rail station, intercity bus station, or intermodal facility");69

- allowing up to $2 million of TIFIA budget authority each fiscal year to pay the application fees for projects costing $75 million or less instead of requiring payment by the project sponsor;

- modifying or setting the minimum project cost thresholds for credit assistance at $10 million for TOD projects, the capitalization of a rural project fund, and local government infrastructure projects; and

- providing for a streamlined application process for loans of $100 million or less.

In addition, the FAST Act authorized the creation of a new National Surface Transportation and Innovative Finance Bureau within DOT to administer federal transportation financing programs, specifically the TIFIA program, the SIB program, the Railroad Rehabilitation and Improvement Financing (RRIF) Program, and the allocation of authority to issue private activity bonds for qualified highway or surface freight transfer facilities. To fulfill this mandate, DOT established the Build America Bureau in July 2016. The bureau also will be responsible for establishing and promoting best practices for innovative financing and P3s, and for providing advice and technical expertise in these areas. The bureau will administer the new discretionary Nationally Significant Freight and Highway Projects grant program, known as INFRA grants, and will have responsibilities related to procurement and project environmental review and permitting.

National Infrastructure Bank

Congress has considered several proposals to create a national infrastructure bank to help finance infrastructure projects. One purported advantage of a national infrastructure bank over other loan programs, such as TIFIA, is that it would have more independence in its operation, such as in project selection, and have greater expertise at its disposal. Additionally, a national infrastructure bank would likely be set up to help a much wider range of infrastructure projects, including water, energy, and telecommunications infrastructure. Proponents claim that the best projects, or at least those that are the most financially viable, would be selected from across these sectors.

In many formulations, capitalization of a national infrastructure bank comes from an appropriation, but in others the bank is authorized to raise its own capital through bond issuance. By issuing securities that are not tax exempt, it could tap pools of private capital that do not invest in tax-exempt bonds, such as pension funds and foreign citizens, the traditional source of much project finance. Tax-exempt municipal securities are unattractive to some investors, either because individual issues are too small to interest them or because the investors do not benefit from the tax preference. Taxable bonds with long maturities might be attractive to some of these investors.70 An infrastructure bank also might reduce the federal government's share of project costs, putting greater reliance on nonfederal capital and user fees.

Most infrastructure bank proposals assume the bank would improve the allocation of public resources by funding projects with the highest economic returns regardless of infrastructure system or type. Selection of the projects with the highest returns, however, might conflict with the traditional desire of Congress to assure funding for various purposes. In the extreme case, major transportation projects might not be funded if the bank were to exhaust its lending authority on water or energy projects offering higher returns.

Limitations of a national infrastructure bank include its duplication of existing programs like TIFIA and the Wastewater and Drinking Water State Revolving Funds. An infrastructure bank may not be the lowest-cost means of increasing infrastructure spending. CBO has pointed out that a special entity that issues its own debt would not be able to match the lower interest and issuance costs of the U.S. Treasury.71 In some formulations, a national infrastructure bank exposes the federal government to the risk of default.72

State Infrastructure Banks

SIBs already exist in many states. In 32 states and Puerto Rico, SIBs were created pursuant to a federal program originally established in surface transportation law in 1995 (P.L. 104-59).73 Several other states, among them California, Florida, Georgia, Kansas, Ohio, and Virginia, have state investment banks that are unconnected to the federal program.74 Local governments have also begun to embrace the idea. The City of Chicago has established a nonprofit organization, the Chicago Infrastructure Trust, as a way to attract private investment for public works projects,75 and Dauphin County, PA, has established an infrastructure bank funded from a state tax on liquid fuels to make loans to the 40 municipalities and private project sponsors within its borders.76

One of the biggest stumbling blocks to federally authorized SIBs has been capitalization. States can capitalize the banks using some of their apportioned and allocated highway and transit funds, and any amount of rail program funds. Under the FAST Act, capitalization of a rural project fund may now be made by a loan from the TIFIA program. Federal funds have to be matched with state funds, generally on an 80% federal, 20% state basis. Authority to use federal transportation funds for this purpose lapsed between the beginning of FY2010 and enactment of the FAST Act in December 2015, and few states took advantage of this authority prior to FY2010 because they preferred to use their federal grant funds for other purposes.

Author Contact Information

Footnotes

| 1. |

Based on Federal Highway Administration (FHWA) data. Balances in the HTF accrued in previous years were large enough to keep the fund sufficient until FY2008. |

| 2. |

CRS Report R44388, Surface Transportation Funding and Programs Under the Fixing America's Surface Transportation Act (FAST Act; P.L. 114-94), coordinated by [author name scrubbed]. |

| 3. |

U.S. Congress, House Committee of Conference, Safe, Accountable, Flexible, Efficient Transportation Equity Act: A Legacy for Users, conference report on H.R. 3, 109th Cong., 1st sess., July 28, 2005, H.Rept. 109-203, pp. 1136-1138. |

| 4. |

Federal Highway Administration, FHWA Forecasts of Vehicle Miles Traveled (VMT): Spring 2016, Washington, DC, May 4, 2017, http://www.fhwa.dot.gov/policyinformation/tables/vmt/vmt_forecast_sum.pdf. |

| 5. |

CRS Report R42721, Automobile and Truck Fuel Economy (CAFE) and Greenhouse Gas Standards, by [author name scrubbed], [author name scrubbed], and [author name scrubbed]. See also CRS Report R40506, Cars, Trucks, Aircraft, and EPA Climate Regulations, by [author name scrubbed] and [author name scrubbed]. |

| 6. |

Congressional Budget Office, How Would Proposed Fuel Economy Standards Affect the Highway Trust Fund?, May 2012, http://cbo.gov/sites/default/files/cbofiles/attachments/05-02-CAFE_brief.pdf. Because of the gradual turnover in the car and truck fleet and because the new standards will not take effect until model year 2017, CBO estimates that the standards will reduce "gasoline tax revenues between 2012 and 2022 by less than 1 percent." |

| 7. |

Joseph Kile, Testimony: The Status of the Highway Trust Fund and Options for Paying for Highway Spending, Congressional Budget Office, June 18, 2015, p. 9, https://www.cbo.gov/sites/default/files/114th-congress-2015-2016/reports/50297-TransportationTestimony-Senate.pdf. |

| 8. |

Despite this, two commissions established in SAFETEA, the National Surface Transportation Policy and Revenue Study Commission and the National Surface Transportation Infrastructure Financing Commission, called for increases in federal fuel taxes as the near-term solution; the latter also urged indexing of fuel taxes for inflation and an eventual shift to a financing system based on vehicle miles traveled. See http://www.transportationfortomorrow.com/final_report/index.htm and http://financecommission.dot.gov/Documents/NSTIF_Commission_Final_Report_Mar09FNL.pdf. MAP-21 did not call for additional studies on this subject. |

| 9. |

CRS In Focus IF10495, Highway and Public Transit Funding Issues, by [author name scrubbed] and [author name scrubbed]. |

| 10. |

Congressional Budget Office, Projections of Highway Trust Fund Accounts Under CBO's August 2016 Baseline, September 2016, https://www.cbo.gov/sites/default/files/51300-2016-03-HighwayTrustFund.pdf. The $20.5 billion figure represents the average annual gap between projected receipts from the motor fuel and other excise taxes that flow into the Highway Trust Fund and the anticipated cost of maintaining the surface transportation program at its current "baseline" level. Because of beginning of year (BOY) HTF balances for FY2021, a five-year surface transportation bill (FY2021-FY2025) could be funded with roughly $80 billion in transfers or increased revenues. |

| 11. |

Since the early 1990s Congress has begun the reauthorization debates with a goal of a six-year bill. The most recent bill, the FAST Act, however, provided five years of funding. |

| 12. |

Federal Highway Administration, Action: Procedures for Reimbursements During a Cash Shortfall, July 1, 2014, https://www.transportation.gov/sites/dot.gov/files/docs/Guidance-Memo-Cash-Allocation-Final-3.pdf. |

| 13. |

FHWA estimates that it must also maintain a working balance of $5 billion. Maintaining this working balance increases the funding shortfall five-year total to $93.5 billion. |

| 14. |

Contract authority is a type of budget authority that is available for obligation even without an appropriation. However, appropriators must eventually provide liquidating appropriation authority, which is not recorded as budget authority, to permit the eventual outlays. Contract authority is the type of budget authority used by the HTF. |

| 15. |

Office of Management and Budget, Budget of the U.S. Government FY2018: Appendix (Washington, DC: 2017), pp. 871, 895. Estimates are for start of year FY2018. |

| 16. |

This discussion tracks the changes in the rate of the gasoline tax. Over time other fuels such as diesel have been taxed at different rates. For instance, the current tax on diesel fuel is 6 cents per gallon higher than the gasoline tax. For a tabular history of the rates of the various federal fuel taxes, see Federal Highway Administration, Highway Statistics: Table FE101-A, http://www.fhwa.dot.gov/policyinformation/statistics/2009/fe101a.cfm. |

| 17. |

CRS Report RL30304, The Federal Excise Tax on Motor Fuels and the Highway Trust Fund: Current Law and Legislative History, by [author name scrubbed]. |

| 18. |

Federal Highway Administration, Financing Federal-aid Highways; Appendix M, Federal Excise Taxes on Highway Motor Fuel, last modified February 20, 2015, http://www.fhwa.dot.gov/reports/fifahiwy/ffahappm.htm. |

| 19. |

U.S. President (Reagan), "Remarks to Reporters Announcing the Administration's Proposal for a Highway and Bridge Repair Program: Nov. 23, 1982," The American Presidency Project; Public Papers. |

| 20. |

See Jeff Davis, Reagan Devolution: The Real Story of the 1982 Gas Tax Increase, Eno Center for Transportation, Washington, DC, 2015, pp. 1-40. |

| 21. |

See Congressional Budget Office, How Would Proposed Fuel Economy Standards Affect the Highway Trust Fund?, May 2012, p. 3. A drop in outlays in FY2006 helped bring the HTF briefly into balance in FY2006-FY2007. |

| 22. |

Eric Morath, "Americans Drive to a New Record in Gasoline Consumption," Wall Street Journal, September 7, 2016, http://blogs.wsj.com/economics/2016/09/07/americans-drive-to-a-new-record-in-gasoline-consumption/. |

| 23. |

CBO, as reported in "CBO Updates Highway Trust Fund Spending/Revenue Forecast," Eno Transportation Weekly, July 7, 2017, p. 15. |

| 24. |

There are many inflation indexes that could be used. Which one is most appropriate might become an issue of controversy. The most commonly used index is the U.S. Bureau of Labor Statistics' consumer price index (CPI), which, for example, is used to adjust certain aviation user fees. Other examples are the Bureau of Economic Analysis price indexes for gross government fixed investment and the Federal Highway Administration's National Highway Construction Cost Index (NHCCI). |

| 25. |

Institute on Taxation and Economic Policy, A Federal Gas Tax for the Future, Washington, DC, September 2013, pp. 1-13, http://www.itep.org/pdf/fedgastax0913.pdf. |

| 26. |

Jeffrey Ang-Olson, Martin Wachs, and Brian D. Taylor, Variable-Rate State Gasoline Taxes, Institute of Transportation Studies, University of California, Berkeley, Working Paper, UCB-ITS-WP-99-3, July 1999. See also, M. Madowitz and K. Novan, "Gasoline taxes and revenue volatility: An Application to California," Energy Policy, vol. 59, 2013, pp 663-673, http://www.sciencedirect.com/science/article/pii/S0301421513002577. |

| 27. |

Virginia House Bill 2313, 2013 session. The price floor is the wholesale price as of February 20, 2013. The taxes are paid when the fuel is removed from a refinery or tank farm terminal. This is often referred to as collecting at the "rack." |

| 28. |

A fuel price floor could be established, but its impact would depend on how high the floor is set and whether the floor is indexed to inflation. The outcome could still fail to meet revenue expectations. |

| 29. |