Crude Oil Futures Prices Turn Negative

What Happened?

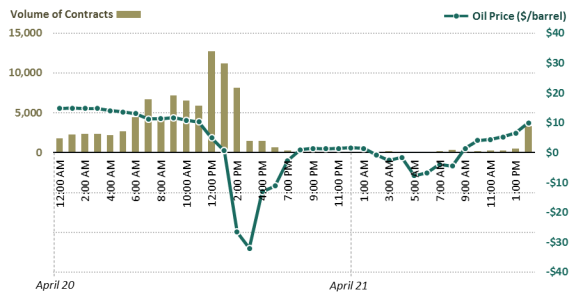

On April 20, 2020, the futures contract price for the immediate month (May) of West Texas Intermediate (WTI), the U.S. benchmark crude, went negative (see Figure 1). The May futures contract price fell $55.90 during the day, to close at negative $37.62 per barrel. The futures price is a contract, usually monthly, for delivery of a certain amount of crude oil, on a specified date in the future, and at a particular location (Cushing, OK for WTI). WTI crude oil futures contracts are traded on the New York Mercantile Exchange (NYMEX). According to data from the U.S. Energy Information Administration (EIA), this is the first time in history that WTI prices became negative. However, other commodity prices, including natural gas and propane, have previously traded negatively.

The May futures contract for WTI expired on April 21. Trading volumes shifted away from the expiring immediate month to the next month (June) contract. Any contracts remaining at the end of the day for the May futures contract will be those that can make or take delivery at Cushing, OK. As shown on Figure 1, the biggest price decline corresponded with a jump in the contract volume. Traders looking to buy were incentivized by cheaper contracts. However, as prices continued to fall, contracting dropped. One reason this may have occurred is that financial traders—traders that cannot take physical delivery of crude oil—needed to sell before the contract expiration.

Prices for other crude oil contract months also declined. The June contract for WTI dropped $4.60 to $20.43 per barrel at the close on April 20 from the previous close on April 17. Additionally, the Brent price, the main international crude oil benchmark price, for May closed at $23.35 per barrel, down $2.29; for June Brent fell to $25.57 per barrel, down $2.51. WTI futures contracts require the contract owner to take physical delivery of the crude oil soon after the futures contract expiry or face large fines, penalties, and fees. In contrast, Brent futures contracts settle financially not physically.

Why Did It Happen?

As a backdrop to the negative futures prices is a large gap between supply and demand for crude oil. The decline in demand for crude oil because of COVID-19 and economic distress is estimated by analysts to be about 30% of global crude oil consumption or about 30 million barrels per day. The transportation sector drives demand for refined petroleum products (e.g., gasoline, diesel, jet fuel), which has dropped significantly. Meanwhile, crude oil supply has been increasing largely because of the failure of OPEC, Russia, and other crude oil producers (known collectively as OPEC+) to reach an agreement to cut production at a meeting on March 6. This triggered production increases by some oil producers, especially Saudi Arabia, which contributed to the precipitous drop in oil prices at the time. Subsequently, after President Trump's urging, OPEC and non-OPEC members announced, on April 12, an agreement to collectively reduce crude oil production by different amounts over time, starting with 9.7 million barrels per day on May 1, 2020. If successful, this may reduce pressure on oil prices. Otherwise, oversupply could continue, exacerbating petroleum storage and logistical limits, possibly further depressing prices.

As available storage becomes more limited, futures prices may continue to fall as owners of crude oil discount their price in order to entice buyers, as was the case with WTI where traders grew concerned over storage availability in Cushing (the designated delivery point for NYMEX crude oil futures contracts), forcing some to sell their futures contracts. Cushing has a working storage capacity close to 76 million barrels, but recent reports indicate that access and availability of the remaining storage is shrinking and that all its capacity has been leased, so it is essentially full according to traders. Despite federal efforts to make capacity available at the Strategic Petroleum Reserve (SPR) and other measures, Cushing storage capacity is a key factor for WTI prices.

What Does It Mean?

The drop in overall crude oil prices, including the negative prices for the WTI May futures contract, indicates the market is working. According to economic theory, when the spread between supply and demand is as wide as it is now for crude oil, prices should fall significantly. The futures prices are in what industry refers to as contango: current prices are lower than future prices, which indicates a market sentiment that downward pressure on prices will continue until demand and supply come closer together and the storage constraint at Cushing is alleviated. Unless demand increases and consumers use more oil and petroleum products, the burden likely will fall on producers to reduce supply. Efforts by major oil producing nations and even U.S. state agencies to reduce production may provide some relief, but perhaps not immediately given the circumstances.

On April 21, the June WTI contract fell by 43% to $11.57 a barrel. Although still in positive territory, the drop, according to some analysts, may be indicative of lower prices to come. If Cushing storage capacity becomes physically full, there will be additional downward pressure on WTI futures contracts unless another event happens to mitigate the situation.

In the long-term, it is impossible to predict the ripple effect of these market conditions. Companies with limited capacity to adapt could default on debt obligations, reduce employment levels, or file for bankruptcy protection. Industry consolidation through mergers, acquisitions, and distressed asset transactions is also a possible outcome and may also produce further downward market pressure.