COVID-19 and Stock Market Stress

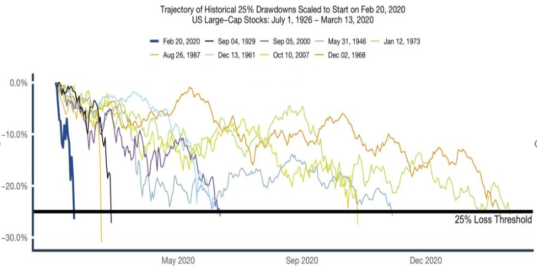

Induced by the Coronavirus Disease 2019 (COVID-19) pandemic, the longest U.S. stock market bull run of 11 years ended in mid-March, the quickest drawdown on record (Figure 1). The market subsequently rebounded, responding to the $2 trillion coronavirus relief package (P.L. 116-136). The swing of stock prices has created unprecedented volatility, a risk metric that measures the degree of price dispersion. This Insight explains the function of the U.S. stock market, the different ways to view stock pricing, and how certain pandemic-induced conditions could affect policymaking. The Securities and Exchange Commission (SEC) is the primary regulator of U.S. capital markets.

|

|

Source: ReSolve Asset Management. |

The Stock Market Size and Importance

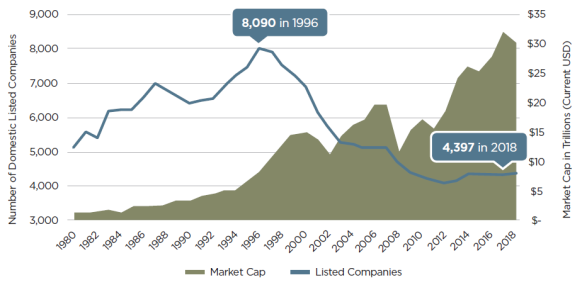

Stocks, also called equities, are shares of ownership in a public company. The U.S. stock market generally refers to the market of public securities offerings that are listed on national securities exchanges. The market consists of around 4,400 companies with a combined market capitalization of more than $30 trillion (Figure 2), as compared to 2018 U.S. gross domestic product (GDP) of $20 trillion. The broader reference to the stock market also includes the public offering and trading of investment funds and other financial instruments. Around half of U.S. households own stock investments.

|

Figure 2. U.S. Stock Market: Publicly Listed Companies and Their Market Capitalization |

|

|

Source: SEC and the World Bank. |

The stock market exists to provide fundraising and trading for businesses and investors. These activities direct money into areas of business operations that the investment community believes to be the most promising for growth and returns. As such, the stock market functions to allocate assets, drive economic growth, provide liquidity, facilitate savings and investments, and offer an economic barometer for the health of the real economy.

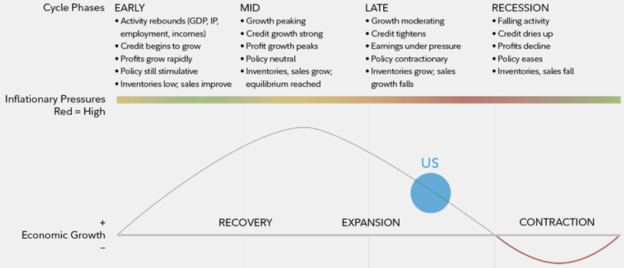

The media often uses the Dow Jones Industrial Average or S&P 500 (indexes that comprise 30 and 500 large listed companies, respectively) to gauge the stock market's movements. The overall stock market performance generally tracks underlying business and economic lifecycles (Figure 3) to enter bull or bear runs.

|

Figure 3. Business Cycles and the Phases of the Economy Hypothetical Illustration of the U.S. Economy in Late Cycle in March 2019 |

|

|

Source: Fidelity Investments. |

Securities Valuation During Market Stress

Stock prices are forward looking, with the price of stocks reflecting the market's expectations of a company's worth. These expectations are informed by different methods of determining a company's underlying value, including the discounted cash flow model that calculates the current value of a company's future income stream or multiples analysis that gauges a company's worth using multiples of its existing earnings or sales, among other measures. These fundamental analyses aim to calculate a firm's intrinsic value for comparison with a firm's stock price.

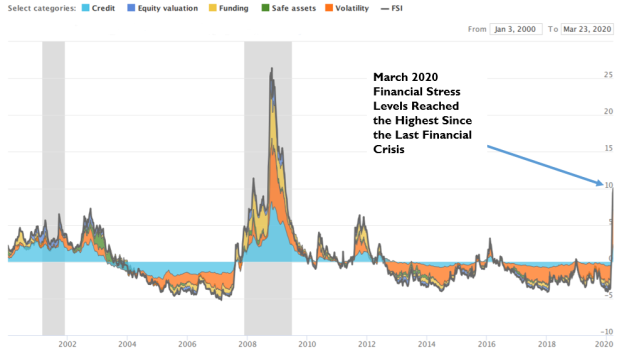

In the context of the coronavirus-induced market stress (Figure 4), does the market volatility mean that the companies' underlying financial conditions suddenly changed or are there other factors coming into play? The answer seems mixed. Earnings estimates and other factors feeding into valuation estimates certainly have changed. For example, the coronavirus directly reduced economic activities in certain industries. The virus could also indirectly reduce the companies' outlook through macroeconomic conditions (e.g., higher unemployment rate, reduced spending, and the threat of widespread bankruptcies), further suppressing the stock price. Such economic effects, however, do not tell the whole story. Stock prices often decouple from underlying corporate fundamentals during market turmoil, with market psychology and liquidity crunches adding to the stress levels. Reactions to market stress can also seize up the financial plumbing, as firms desperate for cash rush to liquidate stocks, further distancing immediate stock prices from firms' underlying valuations.

|

Figure 4. Office of Financial Research Financial Stress Index |

|

|

Source: Office of Financial Research, U.S. Department of the Treasury. Note: Shaded areas indicate U.S. recessions. |

SEC Responses and Related Discussions

The SEC has existing tools to help manage market volatility, including circuit breakers and limit up-limit down mechanisms. These cross-market temporary halts were triggered multiple times in March 2020; their effects are debated. Other discussions include banning short sales or revisiting the SEC's uptick rule. Some argue that shutting down the stock market or opening it for a shorter trading day may also calm extreme market volatility. Additionally, the SEC temporarily relaxed certain inter-fund lending rules for registered funds (e.g., mutual funds) to expand liquidity and ease their redemption pressure.

The coronavirus pandemic has created operational challenges for capital markets and the SEC. The publicly traded companies have obligations to file their periodic financial disclosures and hold annual shareholder meetings. With the risks and uncertainties in the current situation, these obligations could be challenging to fulfill. The SEC has provided conditional regulatory relief for the filing obligations of the affected public companies. It has also provided guidance to encourage virtual annual meetings for shareholder engagements. For the Consolidated Audit Trail, a large multi-year data project, the agency has also issued a temporary coronavirus no-action letter to provide more rollout time. The New York Stock Exchange has temporarily closed its human trading floor to switch to fully electronic operation to avoid contagion and the SEC has published a related notice. The SEC Coronavirus (COVID-19) Response page posts more details on these and other actions.

Legislative Proposals

The Coronavirus Aid, Relief, and Economic Security Act (CARES Act; P.L. 116-136), enacted on March 27, provides both fiscal stimulus and liquidity support to respond to the pandemic. The stock market initially responded positively to the $2 trillion (10% of GDP) in total direct relief in P.L. 116-136. Provisions in Title IV of P.L. 116-136 that may particularly influence financial markets include allowing the Treasury Department to provide loans, loan guarantees, and other backstops for businesses and Federal Reserve facilities; and providing financial assistance to segments of the economy, conditioned upon government equity stakes, executive compensation restrictions, and a ban on stock buybacks. Other broad relief legislation that has significant financial market provisions includes H.R. 6321, which proposes to mandate securities disclosures on supply chain disruption and global pandemic risk and to require the SEC to provide pandemic guidance, testing, and reporting.