Tax Cuts as Fiscal Stimulus: Comparing a Payroll Tax Cut to a One-Time Tax Rebate

The Trump Administration and certain Members of Congress have expressed interest in a temporary payroll tax reduction as a fiscal stimulus response to economic concerns resulting from the coronavirus disease 2019 (COVID-19). Other lawmakers have emphasized that, with respect to tax-relief proposals, "everything's on the table." This sentiment reflects potential uncertainty in both the current economic outlook and what tax policy options might be most effective as the coronavirus outbreak evolves. An alternative to a temporary payroll tax reduction that might be considered, and has been used in the past, is a lump-sum tax rebate.

Temporary payroll tax cuts and lump-sum tax rebates have been used in response to past periods of economic weakness. In 2011 and 2012, employee payroll taxes were reduced by two percentage points, providing tax relief to any individual with earned income. General fund revenue was transferred to Social Security trust funds to ensure that those funds were not affected by the payroll tax cut.

In the first half of 2008, individual tax relief was provided through "recovery rebates"—a new tax credit for 2008 income taxes owed. Generally, individuals received the credit in the form of a rebate check in advance of filing their 2008 tax returns. Because the tax credit was an advance on taxpayers' 2008 tax returns, the IRS estimated its value using tax returns filed for the 2007 tax year.

The credit equaled a taxpayer's income tax liability up to $600 ($1,200 for joint filers). A $300 fully refundable credit was available for low-income taxpayers with at least $3,000 in earned income, Social Security benefits, or veteran's disability payments. The tax credits were phased out for higher-income households, phasing out by 5% for every dollar of earnings above $75,000 for individuals ($150,000 for couples). Individuals who were eligible for the credit could also receive an additional $300 fully refundable tax credit for each qualifying dependent child (which was also phased out). An individual did not have to be currently working to receive a tax benefit.

The merits of these respective approaches may depend on how various policy objectives are prioritized. One issue might be how quickly benefits can reach individuals. Another might be how effective the measure was as economic stimulus in the past. Additionally, there may be distributional considerations. The range of fiscal policy options is not limited to the tax policy options discussed here. If speed of delivery is of paramount importance, for example, expanded unemployment compensation is better suited than tax policy to meet the objective. Expanded unemployment compensation, however, would not address the economic weakness caused by reduced consumption and spending among the employed population.

Speed of Delivery

There is general consensus that if an economic stimulus is warranted, the sooner the package reaches its recipients the better. Both a payroll tax cut and a one-time rebate have been implemented in the middle of a tax year, making them potentially attractive options if speed of delivery is a goal. The IRS was able to implement the 2008 rebate in 62 days, and the 2011 payroll tax cut was implemented within a month.

Despite a shorter implementation period, a payroll tax cut would likely take longer to be fully delivered than a one-time rebate. This is because the payroll tax cut would be paid out over an extended time frame relative to a one-time rebate. For example, it would take more than nine weeks for a worker earning the median weekly wage in the fourth quarter of 2019 to receive $500 in stimulus from a 6.2 percentage point reduction in payroll taxes, while a one-time rebate could deliver $500 in stimulus immediately upon delivery.

Effectiveness of Stimulus: Empirical Evidence

A number of empirical studies have attempted to measure the economic effects of a payroll tax cut (Graziani, van der Klaauw, and Zafar 2016; Coronado, Lupton, and Sheiner 2005; and Souleles 2001) and a one-time rebate (Misra and Surico 2014; Parker et al. 2013; Shapiro and Slemrod 2009; and Shapiro and Slemrod 2003) or to compare the two options (Chambers and Spencer 2008). Taken as a whole, these papers and research on economic multipliers find that both of these policies are among the more effective tax policy options to stimulate the economy. The studies' empirical results do not strongly support the assertion that, all else equal, a payroll tax rate reduction is more likely to be spent than a one-time rebate. The studies also generally conclude that allowing for refundability and targeting lower-income populations results in greater stimulative effects.

Distributional Considerations

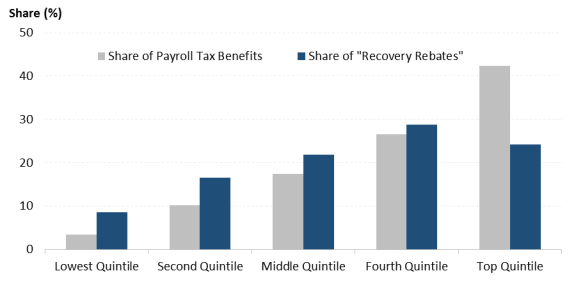

The design of the 2008 "recovery rebates" led to a larger share of those benefits going toward the lower part of the income distribution (Figure 1). Allowing a refundable tax credit provided benefits to those without income tax liability, as well as those receiving Social Security benefits but not having earnings. Additionally, the "recovery rebate" was phased out for higher-income taxpayers. In contrast, the amount of a taxpayer's payroll tax cut is tied to wage earnings. The payroll tax does not apply to earnings above the taxable earnings base ($106,800 in 2011). For taxpayers with earnings above this amount, instead of phasing out, the payroll tax cut was capped at the maximum amount (2% of $106,800, or $2,136 in 2011). As a result, when compared to the "recovery rebate," a larger proportion went to taxpayers in higher income quintiles.

|

Figure 1. Estimated Distribution of Payroll Tax Cut and "Recovery Rebates," by Income Quintile |

|

|

Source: CRS using Tax Policy Center's model distributional estimates for the 2 percentage point employee payroll tax reduction and 2008 tax rebates. Notes: The estimated payroll tax cut benefits are distributed across income quintiles for the 2012 calendar year. The estimated benefits of the "recovery rebates" are distributed across income quintiles for the 2008 calendar year. |