Charitable Conservation Contributions: Potential for Abuse?

Taxpayers may be able to claim a charitable deduction for the value of qualified conservation contributions, which include conservation easements. In recent years, deductions for conservation contributions have increased. There are concerns that some of this increase has been driven by syndicated conservation easements, where a pass-through business entity acquires real property on behalf of investors, makes a conservation contribution to a qualified organization, and then allocates the tax benefits among the investors. Conservation contributions made through syndicated conservation easement transactions often have seemingly inflated property appraisals, which could generate excessive tax deductions for investors.

What Are Charitable Conservation Contributions?

Qualified conservation contributions are charitable donations to qualified organizations of a real property interest designated for conservation purposes. Taxpayers do not have to donate their full interest in the property to claim a deduction. A deduction may be claimed for donations that are conservation easements, where use restrictions serve a conservation purpose. In these cases, the value of the deduction is the foregone land value associated with the use restrictions. For individuals, conservation contributions are allowed in a given tax year as long as they do not exceed 50% of the taxpayer's income (100% for farmers and ranchers), and unused contributions can be carried forward for 15 years. (Generally, deductions of gifts of appreciated property are limited to 30% of income and can be carried forward for five years.)

A conservation purpose may be the preservation of open land or natural habitats, for example. Conservation contributions may also include façade easements, where the donation preserves a historically important structure. Qualified recipient organizations include charitable organizations or governments.

Syndicated conservation easement transactions allow multiple taxpayers to claim a deduction for a particular conservation easement. Typically, with a syndicated easement, a pass-through entity owns the property for which the easement contribution is being made. Investors share in the charitable contribution deduction, the value of which may reflect adjacent improvements made by the pass-through entity. As discussed further below, there are concerns that syndicated conservation easement transactions are associated with abuse of the charitable conservation easement deduction.

The Charitable Deduction for Qualified Conservation Contributions: Data

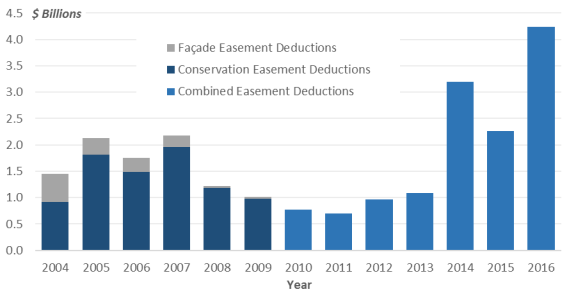

Experts have observed that the charitable deduction for conservation contributions has been a "critical tool in protecting environmentally and historically important land." In recent years, the amount claimed in deductions has increased, as have the number of easements for which the deduction was claimed as well as the number of taxpayers claiming the deduction. In 2016, the amount deducted was $4.2 billion, a near four-fold increase over the 2013 deduction amount of $1.1 billion (see Figure 1). However, while the amount in conservation easement deductions has increased in recent years, the amount that was claimed in 2015 is similar in magnitude to what was claimed in 2007, just before the Great Recession.

|

Figure 1. Charitable Conservation Easement Deductions, 2004-2016 |

|

|

Source: Internal Revenue Service (IRS), Statistics of Income (SOI), Individual Noncash Charitable Contributions. Notes: Amounts for conservation easements and façade easements are listed separately from 2004 through 2009. After 2009, the total amount deducted includes deductions for conservation contributions and façade easements. |

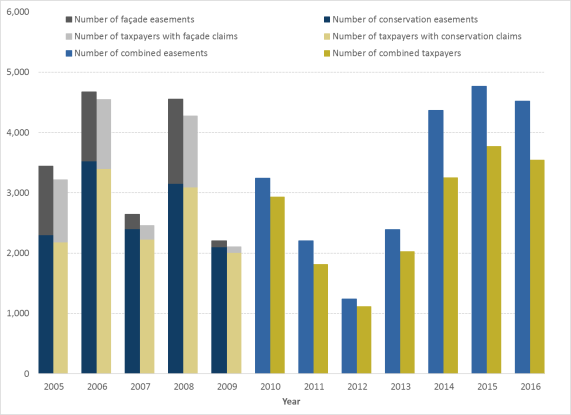

In 2016, 3,540 taxpayers claimed a deduction for conservation contributions, and deductions were claimed for a total of 4,518 easements (see Figure 2). The number of taxpayers claiming a deduction for easement contributions and the number of easements for which deductions were claimed both rose steadily from 2012 through 2015, then declined slightly in 2016.

Through the mid-2000s, a substantial portion of conservation contributions were for façade easements. The Pension Protection Act of 2006 (P.L. 109-280) added new requirements for façade easement contributions, effective July 25, 2006. The amount deducted for façade easements declined as a result, and the IRS stopped reporting data on façade easements separately from conservation easements.

|

Figure 2. Number of Easements and Number of Taxpayers with Easements, 2005-2016 Façade Easements and Conservation Easements |

|

|

Source: IRS SOI Individual Noncash Charitable Contributions. Notes: The total number of and number of taxpayers claiming conservation easements and façade easements are listed separately from 2005 through 2009. After 2009, the total number of easements and total number of taxpayers claiming deductions includes conservation contributions and façade easements. |

Is the Deduction Subject to Abuse?

There are concerns that the rise in charitable conservation contributions may be driven by syndicated conservation easement transactions, where inflated valuations lead to excessive deductions or the conservation value of the donation is questionable. Inflated values are believed to occur when investors purchase land, and later claim conservation contributions based on a subsequent valuation well in excess of the purchase price. Charitable deductions have also been claimed for contributions of conservation easements on land being used as a golf course, leading some to question whether preventing future development while simultaneously using the land for this recreational purpose provides a public conservation benefit. Another concern is that syndicated land conservation transactions lead to the selling of federal tax deductions.

In December 2016, the IRS identified syndicated conservation easements and similar transactions as possible tax-avoidance transactions. Effective December 23, 2016, syndicated conservation easement transactions are "listed transactions," and must be disclosed to the IRS. Failure to disclose such transactions may lead to penalties. In December 2018, the Department of Justice filed a complaint against EcoVest Capital Inc., alleging an abusive syndicated conservation easement tax scheme.

Action in the 116th Congress

The Charitable Conservation Easement Program Integrity Act of 2019 (S. 170/H.R. 1992) would attempt to address abuse in syndicated conservation easement transactions by limiting the amount that could be deducted. Specifically, under this proposal, the charitable deduction claimed could not exceed 2.5 times the amount initially invested in the property (the taxpayer's basis in the property). The limitation would apply for three years after an individual becomes a partner in a partnership engaging in a syndicated conservation easement transaction. The Joint Committee on Taxation estimates that this legislation would generate $6.6 billion in additional revenue between fiscal years 2019 and 2022. In addition to this legislative proposal, in March 2019, Senators Grassley and Wyden announced an investigation into the potential abuse of syndicated conservation easement transactions.

This Insight was coauthored with Sydney Keenan, Intern with the Government and Finance Division, during summer 2019. The listed author is available to answer questions from congressional clients.