Increasing the BCA Spending Limits: Characteristics of Previously Enacted Legislation

The Budget Control Act of 2011 (BCA; P.L. 112-25), enacted on August 2, 2011, generated annual statutory discretionary spending limits for defense and nondefense spending that are in effect through FY2021. If appropriations are enacted that exceed a limit for a fiscal year, across-the-board reductions (i.e., sequestration) are triggered to eliminate the excess spending within that category. The BCA further stipulates that certain discretionary spending—such as appropriations designated as emergency requirements or for overseas contingency operations—are effectively exempt from the limits. For more information on the BCA, see CRS Report R44874, The Budget Control Act: Frequently Asked Questions, by Grant A. Driessen and Megan S. Lynch.

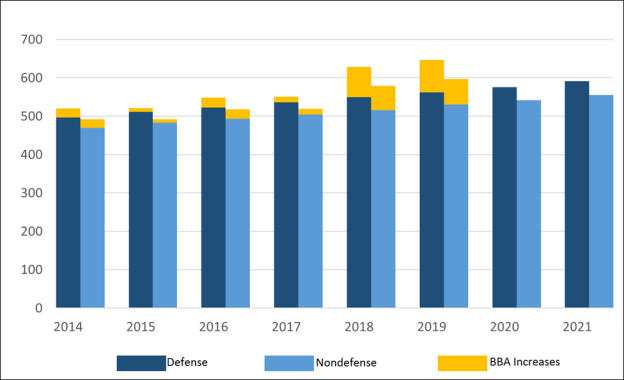

Legislation has been enacted increasing the BCA spending limits (or caps) for each year from FY2014 through FY2019. In each case, (1) the legislation increased both defense and nondefense caps (although not always by equal amounts); (2) the legislation increased the caps for two fiscal years; (3) the legislation was enacted after the start of the first fiscal year that it affected; and (4) the legislation included other components, such as provisions affecting mandatory spending.

Legislation has not been enacted modifying the discretionary budget authority limits for FY2020 or FY2021. As shown in Figure 1, under current law, the caps for FY2020 would drop by $126 billion (or 10%) relative to the budget authority caps for FY2019. That decrease would consist of a $71 billion drop in the defense cap (from $647 billion to $576 billion) and a $55 billion decrease in the nondefense cap (from $597 billion to $542 billion).

|

Figure 1. BCA Discretionary Limits, FY2014-FY2021 Budget authority in billions of nominal dollars |

|

|

Notes: BBA 2013, BBA 2015, and BBA 2018 denote the Bipartisan Budget Act of 2013 (P.L. 113-67), Bipartisan Budget Act of 2015 (P.L. 114-74), and Bipartisan Budget Act of 2018 (P.L. 115-123), respectively. |

A Brief Description of Previously Enacted Legislation Increasing the Spending Limits

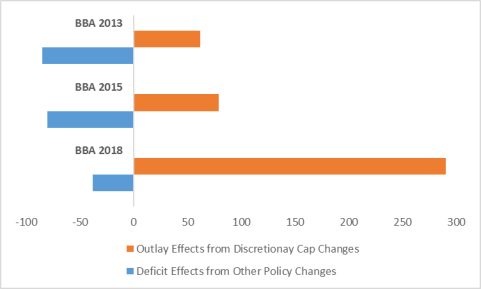

- The Bipartisan Budget Act of 2013 (BBA 2013; P.L. 113-67, referred to as the Murray-Ryan agreement) increased FY2014 discretionary spending limits for both defense and nondefense budget authority by about $22 billion each. In addition, it increased FY2015 discretionary spending limits for both defense and nondefense budget authority by about $9 billion each. The legislation was enacted in late December 2013, nearly three months into FY2014. The legislation included numerous other components with budgetary ramifications, such as the extension of the BCA's annual sequester on non-exempt mandatory spending through FY2023 and an increase in security-related aviation fees. The Congressional Budget Office's (CBO) December 2013 cost estimate projected that the changes to the BCA caps would increase projected outlays by $62 billion over the FY2014-FY2023 period and that other changes included in BBA 2013 would reduce deficits by about $85 billion over the same period.

- The Bipartisan Budget Act of 2015 (BBA 2015; P.L. 114-74) increased discretionary spending limits for both defense and nondefense for FY2016 by $25 billion each. In addition, it increased discretionary spending limits for both defense and nondefense for FY2017 by $15 billion each. The legislation was enacted in early November 2015, approximately one month into FY2016. Other components with budgetary effects in BBA 2015 included the extension of mandatory sequestration through FY2025 and the drawdown and sale of resources from the Strategic Petroleum Reserve. CBO's October 2015 cost estimate projected that the changes to the BCA caps would increase projected outlays by $79 billion over the FY2016-FY2025 period and that other changes included in BBA 2015 would reduce deficits by about $80 billion over the same period.

- The Bipartisan Budget Act of 2018 (BBA 2018; P.L. 115-123) increased nondefense and defense discretionary limits in FY2018 and FY2019. In FY2018, BBA 2018 increased the defense limit by $80 billion and increased the nondefense limit by $63 billion, and in FY2019 it increased the defense limit by $85 billion and increased the nondefense limit by $68 billion. The legislation was enacted in late March 2018, nearly halfway through FY2018. The legislation included other components, such as the creation of a temporary congressional committee tasked with significantly reforming the budget and appropriations process and the extension of mandatory sequestration through FY2027. CBO's February 2018 cost estimate projected that the changes to the BCA caps would increase projected outlays by $290 billion over the FY2018-FY2027 period and that other changes included in BBA 2018 would reduce deficits by about $38 billion over the same period.

Figure 2 shows the projected budgetary effects of BBA 2013, BBA 2015, and BBA 2018 as provided in the most recent CBO cost estimate for each piece of legislation.