U.S. Crude Oil Exports and Retail Gasoline Prices

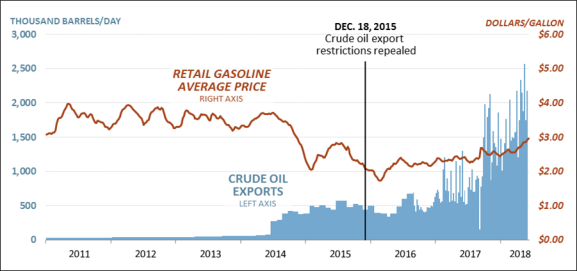

Since the beginning of 2018, average U.S. retail gasoline prices have risen approximately 18% and were nearly $3.00 per gallon at the end of May (see Figure 1). Over the same period, U.S. crude oil exports—for which restrictions were repealed in December 2015—have reached record levels. Average weekly export volumes from January to May 2018 have nearly doubled from average exports in all of 2017, to 1.7 million barrels per day (bpd). As a result, there has been congressional interest in understanding this tandem upward movement and the degree to which increasing crude oil exports might have contributed to rising gasoline prices.

Numerous and interrelated domestic and global factors influence crude oil and petroleum product (e.g., gasoline) prices. Therefore, quantitatively determining the existence of a direct relationship between U.S. crude oil export volumes and prices paid by U.S. consumers for retail gasoline is challenging and is beyond the scope of this Insight. Rather, research conducted for this analysis explores the potential relationship between crude oil exports and domestic crude oil price levels. This analysis explores further how that price relationship may or may not be reflected in retail gasoline prices.

|

Figure 1. U.S. Retail Gasoline Price and Crude Oil Export Volumes |

|

|

Source: CRS, based on data from the Energy Information Administration. Notes: In 2016, EIA changed its methodology for estimating weekly crude oil exports. https://www.eia.gov/todayinenergy/detail.php?id=27752. |

Domestic Crude Oil Price Effects

From 1984 until 2011, West Texas Intermediate (WTI) and Brent—an international benchmark—crude oil prices were closely linked. Price differentials between the two crude oil benchmarks were in the range of $2 to $4 per barrel. During the majority of this period, WTI was priced higher than Brent. As U.S. tight/shale oil production in North Dakota and Texas started to grow, coupled with increasing crude oil imports from Canada, transportation bottlenecks at Cushing, OK (the WTI price point) emerged, resulting in WTI price discounts that reached nearly $30 per barrel in September 2011 compared to the Brent price. As the pipeline system reconfigured, price differentials eventually returned to the historical range. Nevertheless, these large price discounts along with the potential for rapid growth of light/sweet crude oil production—a crude oil type several U.S. refiners were not optimally configured to process in large volumes—resulted in market conditions that motivated interest in repealing the 1975 crude oil export prohibition.

By allowing exports, and assuming the transportation system is totally efficient, the Brent-WTI differential would likely equilibrate to reflect the cost of transportation. Following the export prohibition repeal, the Brent-WTI price differential ranged from -$1 to $6 per barrel until the end of 2017. If allowing exports creates conditions for domestic and global prices to equilibrate, then it is reasonable to conclude that as more domestic volumes are exported, upward pressure on domestic crude oil prices would result. In its March 2018 Short Term Energy Outlook, the Energy Information Administration (EIA) indicated that crude oil exports "could be contributing to near-term price support for U.S. light sweet crude oil." However, additional volumes of crude oil entering the global market would tend to exert downward pressure on international crude oil prices.

Since approximately 55% to 60% of the price of gasoline is related to the price of crude oil, then it is logical to conclude that higher domestic oil prices would translate into potentially higher domestic gasoline prices. However, the quantitative degree to which this price relationship might exist is uncertain.

Retail Gasoline Price Effects

Prior to the crude oil export prohibition repeal, U.S. oil and petroleum product prices were linked to global markets through imports of crude oil and petroleum products and exports of petroleum products such as gasoline. How U.S. crude oil exports might affect U.S. gasoline prices was an important aspect of the crude oil export prohibition repeal debate. Multiple economic studies by various organizations were conducted that assessed the potential impact to U.S. gasoline prices (see Appendix B of this CRS report). Generally, study results indicated that U.S. gasoline prices would decline. However, at least one study suggested that allowing crude oil exports may result in higher domestic gasoline prices.

In October 2014, EIA published a statistical analysis report that explored various drivers of U.S. gasoline prices. The study concluded that international crude oil prices are more important than domestic crude oil prices for determining U.S. gasoline and petroleum product prices. In February 2018 EIA reiterated this study conclusion by stating that "EIA research indicates that U.S. gasoline prices usually move with Brent prices, the international benchmark."

Policy Considerations

Export prohibition repeal legislation that was signed into law (P.L. 114-113) in December 2015 includes an exception provision that empowers the President to restrict crude oil exports if the Secretary of Commerce determines that (1) U.S. crude oil exports have resulted in oil supply shortages or oil prices significantly higher than global prices, and (2) supply shortages and price increases have or will result in adverse employment effects in the United States. Application of this provision will depend on how terms such as "supply shortages" and "oil prices" are defined.

While it is difficult to directly attribute supply and price levels in a 100 million bpd global market to export volumes from a single country, some general observations may be of interest. Currently, the WTI domestic crude oil price benchmark is approximately $10 less than the Brent international benchmark. This differential is largely attributed to pipeline and port infrastructure limitations. With regard to supply, the definition of "shortage" is likely to be important. For example, U.S. refiners currently import 7.5 to 8 million bpd of crude oil and the U.S. does not produce enough crude oil to satisfy refinery throughput and domestic product demand. Exports may seem counterintuitive given the large volumes of imports. However, exports respond to price differentials for crude oils with similar quality characteristics. Should domestic shortages of certain types of crude oil occur, price benchmarks would likely adjust and exports would likely decline or perhaps be eliminated in response to market and price conditions.