Tax Reform: The Child Credit and the Child Care Credit

The current tax code has two credits that offset the costs of raising children: the child tax credit (sometimes referred to as the "child credit," or CTC) and the child and dependent care credit (sometimes referred to as the "child care credit," or CDCTC). These are two distinct tax credits. H.R. 1, as introduced, would, among other things, increase the child tax credit to $1,600 per child; set the maximum amount of the refundable portion at $1,000 per child, allowing this amount to increase over time with inflation to $1,600 per child; and increase the income level at which the credit would begin to phase out. The bill would retain and make no legislative changes to the child care credit.

This Insight provides background to help assess who would be assisted by potential changes to either credit. It shows what types of families with children receive both credits and how the credits are distributed across the income distribution.

The CTC provides taxpayers with $1,000 for each qualified child under age 17. It is a refundable credit, meaning that those who otherwise would have no federal income tax liability can receive some or all of the credit as a refund. To receive the credit as a refund, a family must have annual earnings in excess of $3,000 per year. The refundable portion of the credit, often referred to as the additional child tax credit, or ACTC, is calculated as 15% of earnings above $3,000, not to exceed $1,000 times the number of qualifying children. The CTC phases out for higher-income taxpayers whose modified adjusted gross income is above $110,000 for a married couple, and $75,000 for most others.

The CDCTC is a nonrefundable credit that helps families with the cost of a specific expense related to children, namely child care. Since the child care credit is not refundable, it can only reduce the federal income tax liability of families that would otherwise owe taxes. The child care credit also requires that a family have their children in paid child care. In general, for married couples, both spouses have to be working to qualify for the credit.

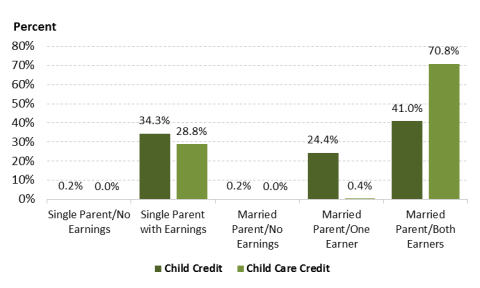

The types of families that claim the CTC and CDCTC reflect the requirements and limitations associated with the respective credits. The CTC is claimed by all types of families with earnings (the refundable part requires earnings, and most families with children have earnings), including married couples with a single earner. The CDCTC, on the other hand, is mostly claimed by single-parent families with earnings and married couples with both spouses working. Married couples with one spouse working can qualify for the CDCTC only under limited circumstances, as noted above. Figure 1 shows the distribution of credit claims for the CTC and CDCTC across family types.

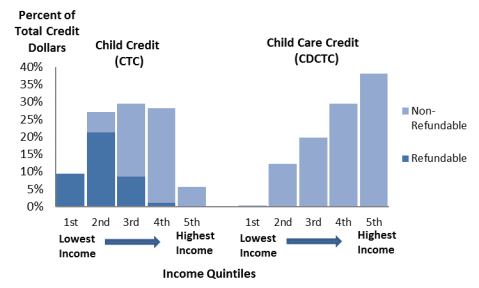

Figure 2 shows how the credits are distributed across the income distribution under current law. The CTC is widely distributed across the income distribution, with families in all quintiles benefiting. Lower-income families benefit from the CTC because of its refundability. The benefit to upper-income families is limited because the CTC is phased out at higher income levels.

The benefits of the CDCTC, on the other hand, are concentrated in the middle and upper income groups. The current CDCTC does not reach the lowest-income families because they tend to owe no federal taxes and thus cannot claim a nonrefundable credit. Additionally, lower-income families are less likely to have paid child care.

|

Figure 2. Estimated Distribution of CTC and CDCTC Benefits, by Income Quintile (2014) |

|

|

Source: Estimated by the Congressional Research Service. See text box below for an explanation of methodology. |

Potential changes to both credits could alter the distributions illustrated here. For example, proposals to raise the phase-out income thresholds for the CTC would shift more of its benefit to the upper income quintiles. Conversely, if the CDCTC were made refundable, more of its benefit would be shifted to the lower income quintiles.

|

A Brief Note About Methodology Unless otherwise specified, the Congressional Research Service (CRS) derived the estimates in this Insight using sample data from the Census Bureau's March 2015 Annual Social and Economic Supplement (ASEC) to the Current Population Survey and the TRIM3 microsimulation model. Since there are no data on characteristics of every American family (e.g., population data), including their child care spending, benefit receipt, and socioeconomic and demographic characteristics, researchers must use survey data from samples of families to estimate these characteristics. Additionally, some of the information needed for this analysis is not available directly from the Census household survey (e.g., tax liabilities and benefits) and has been estimated using microsimulation techniques. As with all models, estimates derived from TRIM are subject to a number of caveats and limitations. Since these are estimates, generated from a sample of the population and a quantitative model, there is potential for sampling error and model error (e.g., errors related to how benefit receipt is assigned). Estimates derived using the TRIM3 model and presented in this Insight may differ from administrative data. For instance, IRS data on tax units claiming various credits tend to be higher than TRIM3 estimates due to misreporting on the Census survey. Income Quintile: An income quintile is constructed by first ordering taxpayers from lowest to highest income and then selecting 20% of tax units for each quintile. (Income is defined as cash income.) The lowest income levels for each quintile in this analysis are provided below.

Source: Estimated by the Congressional Research Service using TRIM3. a The lowest income (bottom of quintile 1) is a negative number, as business losses for the self-employed are negative earnings. |