Major Railroad Mergers and Acquisitions

On July 29, 2025, Union Pacific Railroad (UP) announced that it had agreed to acquire Norfolk Southern Railway (NS). If the transaction is approved, it would reduce the number of U.S. Class I railroads—defined as having annual operating revenues of $900 million or more in inflation-adjusted 2019 dollars—from four to three (see Table 1). Two additional Class I Canadian railroads provide transcontinental service across southern Canada, own track in the United States that connects to some northern tier U.S. ports, and also own track that parallels the Mississippi River with connections to and into Mexico.

|

Railroad and Region |

Operating Revenue ($ Millions) |

Route Miles Operated |

Employees |

|

UP (West) |

$24,189 |

32,880 |

32,388 |

|

BNSF (West) |

$23,747 |

32,897 |

36,958 |

|

CSX (East) |

$13,278 |

19,701 |

19,471 |

|

NS (East) |

$12,122 |

19,154 |

20,236 |

Source: Association of American Railroads, Railroad Fact Book, December 2025.

Notes: UP = Union Pacific, NS = Norfolk Southern. Not shown are two Class I Canadian railroads that own track in the United States through U.S. subsidiaries. Class I railroads are defined as having annual operating revenues of $900 million or more in inflation-adjusted 2019 dollars.

Prior railroad mergers have enabled the surviving railroads to consolidate their networks by abandoning or selling off parallel lines. End-to-end mergers have also allowed railroads to improve profitability by carrying long-haul traffic greater distances. A wave of mergers in the 1970s through the 1990s left seven Class I carriers controlling almost all long-distance freight rail traffic in the United States and Canada; some of these resulted in periods of poor service reliability as rail networks combined. The merger between Canadian Pacific Railway (CP) and Kansas City Southern Railway (KCS), approved in 2023 (see below), further reduced the number of Class I carriers to six.

The volume of freight transported by rail has broadly declined over the last 20 years, as has the overall share of freight transported by rail compared with other transportation modes. Coal traffic, the single largest bulk commodity transported by rail, has declined as the amount mined and consumed has decreased. Freight rail growth has been strongest in intermodal container traffic, which can be moved between ships, trains, and trucks when it is economically advantageous. Mergers and acquisitions can offer carriers opportunities to increase profits through operating efficiencies, even if traffic volumes do not increase.

Surface Transportation Board Jurisdiction

Rail merger and acquisition applications must be filed with the five-member Surface Transportation Board (STB, or the Board), which has exclusive authority to make a final decision on an application. These applications include detailed proposals regarding how the combined railroad would operate. Some of the operations proposed in the applications typically are designed to reduce opposition to the proposed transaction. For example, customers might be concerned about higher shipping rates, railroad employees might be concerned about job cuts, other railroads might seek to preserve access to certain markets, and state and local governments might have concerns about the local impacts of higher or lower rail traffic volume.

After considering an application and soliciting comments from affected parties and the public, the Board is to decide whether to approve or reject the transaction and whether it will base its approval on specific conditions or commitments. If an applicant perceives the conditions required by the Board to be too burdensome, it can withdraw its application. Historically, it has taken a year or more from the time an application is accepted for the Board to reach a decision.

The Board has authority to make major changes as conditions of the proposed merger in order to protect rail customers, employees, and other railroads from possible adverse impacts from the proposed merger. Such changes can significantly affect the future operation of the combined railroad and its relations with its customers and with other railroads. Further, the Board has authority to oversee future operations indefinitely and to reopen a case for further adjustments if conditions change.

Evaluating Railroad Combinations

Federal law directs the STB to approve railroad mergers and acquisitions that it deems to be "consistent with the public interest." The STB revised its merger regulations in 2001, creating a higher bar for "major" transactions, defined as those involving multiple Class I railroads. Under previous standards, Class I railroads planning to merge had to demonstrate to the STB that the level of competition would remain unchanged following the transaction, but since 2001, the STB has held that it would approve such transactions only if the parties can demonstrate that competition will be enhanced as a result.

Since the revised regulations were implemented, most railroad mergers and acquisitions have involved smaller carriers. Some Class I carriers explored potential mergers but never formally applied for STB approval. For example, Canadian Class I railroad CP explored mergers with CSX Transportation (CSX) in 2014 and with NS in 2016, but neither deal was submitted to the STB. The first major transaction to be approved after the rules were revised was decided in 2023, but it was evaluated under the pre-2001 rules. The 2001 rulemaking preemptively granted KCS—the smallest of the Class I railroads at the time—a waiver that allowed it to meet the older, less stringent standards for merger proposal evaluation. The Board's reasoning at the time was that KCS was small enough that its involvement in a merger would present less risk of anticompetitive effects than a merger between any two of the six larger railroads. Although KCS merged with CP in 2023, the resulting CPKC Railroad is still the smallest Class I carrier.

The Board is directed by statute to afford "substantial weight" to the recommendations of the Department of Justice (DOJ) in evaluating transactions, but any opinion would be purely advisory. For example, in the 2023 merger involving KCS, the Board approved the transaction even though the DOJ opposed it.

Features of the Proposed Transaction

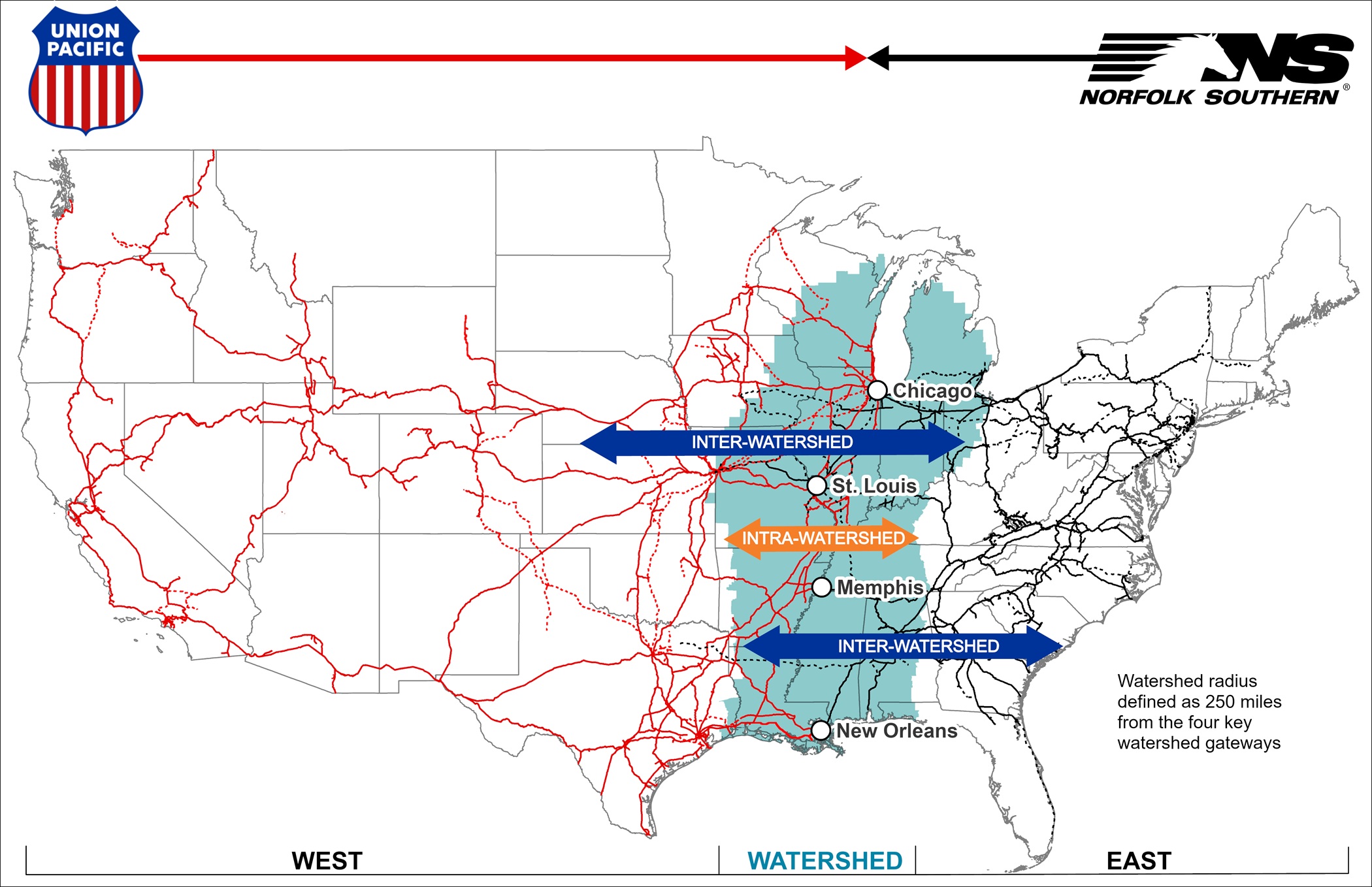

If the UP acquisition of NS is approved, the combined railroad would be the first to offer uninterrupted service between the East and West Coasts of the United States by a single carrier (see Figure 1 for a map of states served by UP and NS).

Currently, rail shipments moving between areas served by Eastern and Western railroads tend to be transferred from one carrier to another at a limited number of interchange points. This can lengthen delivery times as railcars, locomotives, and crews are exchanged, especially if multiple trains are waiting to use the same facility. Delays can be especially noticeable for shipments originating and/or terminating within what UP and NS refer to as the "Watershed" region—several hundred miles wide and roughly centered on a handful of "Gateway" cities on or near the Mississippi River. UP and NS claim that by offering single-line service (i.e., without changing carriers) across the Watershed, they will be able to offer trip times that are competitive with both other Class I railroads and trucks. Diversion of freight from trucks to trains is a factor in how the application intends to meet the STB's "public interest" and "enhanced competition" tests.

{kind=link}

Shippers that use UP or NS in combination with another Class I railroad for cross-country journeys could be concerned about the effect that having one option for interline service may have on prices at interchange points. For this group of customers, the application proposes to maintain competitiveness by implementing consistent pricing at interchange points with all Class I railroads. This pricing strategy would be applied only during the STB's oversight period. The application also states that three facilities are to see direct access to rail carriers drop from two to one as a result of the transaction and declares an intent to preserve access to a different carrier in those cases.

Parties in Support and Opposition

Customers shipping intermodal containers, such as the Port of Los Angeles/Long Beach, have voiced support for the UP-NS transaction, citing gains in efficiency that can result from a consolidated network. Other shippers, including the American Chemistry Council, the American Farm Bureau Federation, the American Iron and Steel Institute, and the National Industrial Transportation League, have opposed the combination, citing the potential for price increases and service disruptions. Some rail shippers may be wary of publicly criticizing the proposed transaction if they believe that UP or NS could retaliate against them in the form of higher freight rates or less reliable service.

Early reactions from major railroad labor unions were mixed. One major railroad labor union endorsed the deal after reaching a job protection agreement with UP and NS for its members. Other labor organizations have publicly opposed the transaction or have withheld judgment.

Considerations for Congress

If Congress is concerned that a successful UP-NS combination could precipitate more mergers that would further reduce the number of U.S. Class I railroads, it could enact a moratorium on major transactions, such as the one adopted by the STB in 2000 in the run-up to its 2001 rulemaking. Alternatively, Congress could consider legislative proposals to make it easier for shippers to petition the STB for relief from substandard service or abuse of market dominance, or Congress could take no action until the STB has rendered a decision.

Members of Congress can and have submitted letters to the STB expressing support or opposition to the transaction or to specific conditions of approval. These letters become part of the public record, and the Board is required to consider them in making its decision.