Introduction

A range of federal incentives supports the development and deployment of alternatives to conventional fuels and engines in transportation. These incentives include tax deductions and credits for vehicle purchases and the installation of refueling systems, federal grants for conversion of older vehicles to newer technologies, mandates for the use of biofuels, and incentives for manufacturers to produce alternative fuel vehicles. Some of these incentives have expired in recent years when their authorizations expired.

Many of the policy choices presented for alternative fuel and advanced vehicle technologies originated as a response to the nation's interest in reducing petroleum imports, a goal first articulated at the time of the two oil embargoes imposed by the Organization of Petroleum Exporting Countries (OPEC) in the 1970s. While President Richard Nixon is often cited as the first President to call for "energy independence," successive Presidents and Congresses have made efforts to reduce petroleum import dependence as well.

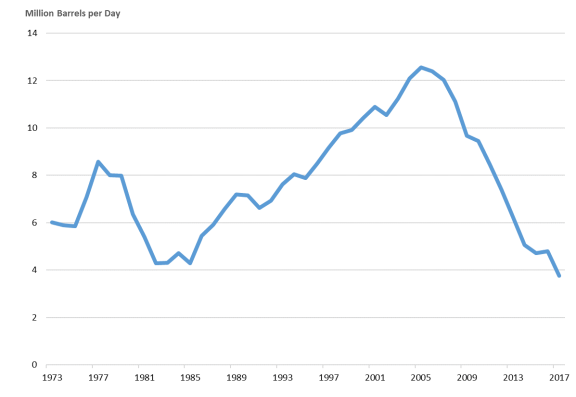

As shown in Figure 1, since peaking in 2005, net U.S. oil imports have fallen by 70%. Factors in this reversal include the last recession, which reduced domestic demand, followed by a rise in the supply of U.S. oil and oil alternatives due to increased private sector investment and federal incentives, some of which are cited in this report. In addition, the United States has become a net exporter of petroleum products (while it remains a net importer of crude oil). With declining U.S. import dependence, reliance on petroleum and petroleum products may be less of a factor in promoting alternative fuels and alternative fuel vehicles in the future.

In addition to concerns over petroleum import dependence, other factors also have driven policy on alternative fuels and advanced vehicle technologies. Federal incentives do not reflect a single, comprehensive strategy but rather an aggregative approach to a range of discrete public policy issues, including improving environmental quality, expanding domestic manufacturing, and promoting agriculture and rural development.

|

Figure 1. U.S. Net Imports of Crude Oil and Petroleum Products Annual Average |

|

|

Source: Energy Information Administration, U.S. Net Imports of Crude Oil and Petroleum Products, Washington, DC, August 31, 2018, https://www.eia.gov/dnav/pet/hist/LeafHandler.ashx?n=PET&s=MTTNTUS2&f=A. |

Factors Behind Alternative Fuels and Technologies Incentives

While a reliance on foreign sources of petroleum was an overriding concern for much of the past 40 years, other factors, such as rural development, promotion of domestic manufacturing, and environmental concerns, have also shaped congressional interest in alternative fuels and technologies. A variety of programs affecting the development and commercialization of alternative fuels and technologies have been proposed and enacted, each with its own benefits and drawbacks. (This report does not evaluate the effectiveness of alternative fuel programs and incentives.) Alternative fuels programs can be generally classified into six categories: expanding domestic ethanol production; establishing other alternative fuels; encouraging the purchase of nonpetroleum vehicles; reducing fuel consumption and greenhouse gas emissions; supporting U.S. vehicle manufacturing; and funding U.S. highways.

Developing Domestic Ethanol Production

Ethanol has been seen as a homegrown alternative to imported oil. A number of programs were put in place to encourage its domestic development (instead of importing from other ethanol producers, such as Brazil). To spur establishment of this domestic industry, Congress has enacted a number of laws, which are beneficial to states that have a large concentration of corn growers (corn being the raw material feedstock in most U.S. ethanol). Many of the incentives for ethanol production have been included in farm-related legislation and appropriations acts and hence have been administered by the U.S. Department of Agriculture (USDA), or in tax provisions administered by the Internal Revenue Service (IRS). The volumetric ethanol excise tax credit (VEETC) provided a tax credit to gasoline suppliers who blended ethanol with gasoline. The small ethanol producer tax credit provided a limited additional credit for small ethanol producers. Both credits expired at the end of 2011. Since 2005, petroleum refiners and importers have been required to supply biofuels as a share of their gasoline and diesel supply. This mandate, the Renewable Fuel Standard (RFS), has been an impetus for expanded production and use of ethanol and other biofuels.

Establishing Other New Alternative Fuels

In addition to ethanol, Congress has sought to spur development of other alternative fuels, such as biodiesel, cellulosic biofuel, hydrogen, liquefied petroleum gas (LPG), compressed natural gas (CNG), and liquefied natural gas (LNG). Some of these fuels have been supported through tax credits (such as the biodiesel tax credit), federal mandates (mainly the RFS), and R&D programs (such as the Biomass Research and Development Initiative, which provides grants for new technologies leading to the commercialization of biofuels).

Encouraging the Purchase of Nonpetroleum Vehicles

Congress has enacted laws which seek to boost consumer adoption by providing tax credits for the purchase of some vehicles that consume far less petroleum than conventional vehicles, or that do not consume petroleum at all. These tax credit programs generally are limited in duration as a way to encourage early adopters to take a risk on new kinds of vehicles. The proponents contend that once a significant number of such new cars and trucks are on the road, additional buyers would be attracted to them, the increased volume would result in lower prices, and the tax credits would no longer be needed. Currently, a credit is available for the purchase of plug-in electric vehicles. Expired credits include incentives for hybrid vehicles, fuel cell vehicles, advanced lean burn technology vehicles,1 and certain alternative fuel vehicles. Congress has also enacted tax credits to spur the expansion of infrastructure to fuel such vehicles, although these credits have likewise expired.

Reducing Fuel Consumption and Vehicle Emissions

Several agencies, including the Environmental Protection Agency (EPA) and the Department of Transportation (DOT), have been mandated by statute to address concerns over fuel consumption and vehicle emissions through programs for alternative fuels. The most significant and long-standing program to reduce vehicle fuel consumption is the Corporate Average Fuel Economy (CAFE) program administered by DOT.2 Under CAFE, each manufacturer's fleet must meet specific miles-per-gallon standards for passenger vehicles and light trucks. If a manufacturer fails to do so, it is subject to financial penalties. Manufacturers can accrue credits toward meeting CAFE standards for the production and sale of certain types of alternative fuel vehicles. A joint rulemaking process between DOT and EPA links future CAFE standards with greenhouse gas (GHG) standards promulgated under EPA's Clean Air Act authority. DOT also established the Congestion Mitigation and Air Quality Improvement Program (CMAQ) to fund programs that intended to reduce emissions in urban areas that exceed certain air quality standards. At EPA, the Diesel Emission Reduction Act (DERA) was implemented with a goal of reducing diesel emissions by funding and implementing new technologies. In addition, EPA's RFS mandates the use of renewable fuels for transportation.3 Under the RFS, some classes of biofuels must achieve GHG emission reductions relative to gasoline.

Supporting U.S. Motor Vehicle Manufacturing

The Department of Energy (DOE), in partnership with U.S. automakers, federal labs, and academic institutions, has funded and overseen research and development programs on vehicle electrification for decades, in particular research focused on how to produce economical batteries that extend electric vehicle range. These R&D programs were supplemented in the American Recovery and Reinvestment Act (ARRA; P.L. 111-5) to include grants to U.S.-based companies for facilities to manufacture advanced battery systems, component manufacturers, and software designers to boost domestic production and international competitiveness. The Advanced Technology Vehicles Manufacturing (ATVM) loan program at DOE, established by the Energy Independence and Security Act of 2007 (P.L. 110-140), has supported manufacturing plant investments to enable the development of technologies to reduce petroleum consumption, including the manufacture of electric and hybrid vehicles,4 although no new loans have been approved since 2011.

Highway Funding and Fuels Taxes

As described below (see "Motor Fuel Excise Taxes"), one of the earliest fuels-related federal programs is the motor vehicle fuels excise tax first passed in the Highway Revenue Act of 1956 to fund construction and maintenance of the interstate highway system. Originally, only gasoline and diesel were taxed, but as newer fuels became available (such as ethanol and compressed natural gas), they were added to the federal revenue program, but often at lower tax rates than gasoline or diesel. Lower tax burdens for some fuels or vehicles may effectively incentivize those choices over conventional options. However, lower tax burdens for these vehicles and fuels could compromise federal highway revenue. The vehicles responsible for lower tax revenues include traditional internal combustion engine vehicles with higher mileage per gallon as well as new technology electric and hybrid cars.

Structure and Content of the Report

The federal tax incentives and programs discussed in this report aim to support the development and deployment of alternative fuels. There is no central coordination of how these incentives interact. In general, they are independently administered by separate federal agencies, including five agencies: Department of the Treasury, DOE, DOT, EPA, and USDA.

This report focuses strictly on programs that directly support alternative fuels or advanced vehicles. It does not address more general programs (e.g., general manufacturing loans, rural development loans), or programs that have been authorized but never funded. The programs are presented by agency, starting with those that generally address the above factors, followed by those that are fuel- or technology-specific. Programs that expired or were repealed on or after December 31, 2017, are included in Appendix A, Recently Expired or Repealed Programs.5 Congress may explore whether to reinstate these expired programs or establish similar programs.

Appendix B contains four tables:

- 1. a summary of the programs discussed in the body of the report, listed by agency (Table B-1);

- 2. a listing of programs and incentives for alternative fuels, by fuel type (Table B-2);

- 3. a listing of programs and incentives for advanced technology vehicles, by vehicle type (Table B-3); and

- 4. a listing of recently expired programs by agency (Table B-4).

Current Federal Incentives

Department of the Treasury

Idle Reduction Equipment Tax Exemption6

|

Administered by |

IRS |

|

Authority |

Established by the Energy Improvement and Extension Act of 2008 (P.L. 110-343), Division B, Title II, §206(a). |

|

Annual Funding |

Joint Committee on Taxation (JCT) estimated budget effect for FY2018: $17 million7 |

|

Scheduled Termination |

No expiration date8 |

|

Description |

Section 4053 of the U.S. tax code exempts certain vehicle idling reduction devices from the federal excise tax on heavy trucks and trailers. Eligible devices are determined by the Administrator of the EPA in consultation with the Secretary of Energy and the Secretary of Transportation. |

|

Qualified Applicant(s) |

Sellers or users or heavy trucks, trailers, or tractors |

|

Applicable Fuel/Technology |

Devices that have been identified as reducing idling of a heavy truck or trailer at a motor vehicle rest stop or other location where such vehicles are temporarily parked or remain stationary9 |

|

For More Information |

See IRS Publication 510; and the Alternative Fuels Data Center's (AFDC's) web page for the Idle Reduction Equipment Excise Tax Exemption. For a list of eligible devices, see the U.S. Environmental Protection Agency's (EPA's) web page "Learn About Federal Excise Tax Exemption." |

|

Related CRS Reports |

None |

Motor Fuel Excise Taxes10

|

Administered by |

Internal Revenue Service (IRS) |

|

Authority |

Most motor fuels taxes (some of which were initially enacted in 1932) were included in the Highway Revenue Act of 1956 (P.L. 84-627) primarily to support the Highway Trust Fund, except for the tax on compressed natural gas, which was enacted in 1993 (Omnibus Budget Reconciliation Act of 1993; P.L. 103-66). Taxes that support the Highway Trust Fund have been extended numerous times, most recently through September 30, 2022, by the Fixing America's Surface Transportation (FAST) Act (P.L. 114-94).11 |

|

Annual Funding |

JCT estimated tax expenditure for FY2017-FY2021: N/A12 |

|

Scheduled Termination |

4.3 cents per gallon of the gasoline/diesel fuel tax is permanent; the rest of the motor fuels taxes expire on September 30, 2022, when major highway-related taxes expire. |

|

Description |

Taxes vary by fuel: gasoline, 18.4 cents per gallon; diesel fuel, 24.4 cents per gallon; biodiesel, 24.4 cents per gallon; ethanol, 18.4 cents per gallon; P-series fuels, 18.4 cents per gallon; hydrogen, 18.4 cents per gallon equivalent; liquefied petroleum gas (LPG), 18.3 cents per gallon equivalent; compressed natural gas (CNG), 18.3 cents per gallon equivalent; liquefied natural gas (LNG), 24.3 cents per gallon equivalent. Alternative fuel tax credits are or were available against many of these.13 Electricity for electric vehicles is untaxed. These exemptions/credits effectively incentivize selected fuels/vehicles relative to conventional options. |

|

Qualified Applicant(s) |

Manufacturers who produce applicable fuel types14 |

|

Applicable Fuel/Technology |

Gasoline, diesel, hydrogen, liquefied petroleum gas, liquefied natural gas, compressed natural gas, ethanol and methanol (electricity is exempt) |

|

For More Information |

See IRS publication 510, Excise Taxes; and Federal Highway Administration, Funding Federal-aid Highways, Appendix K. |

|

Related CRS Reports |

CRS Report RL30304, The Federal Excise Tax on Motor Fuels and the Highway Trust Fund: Current Law and Legislative History, by Sean Lowry, and CRS Report R44674, Funding and Financing Highways and Public Transportation, by Robert S. Kirk and William J. Mallett |

Plug-In Electric Drive Vehicle Credit15

|

Administered by |

IRS |

|

Authority |

Established by the Energy Improvement and Extension Act of 2008, 26 U.S.C. 38(b)(35), 30D, P.L. 110-343, Div. B, Title II, §205(a). The American Recovery and Reinvestment Act of 2009 (P.L. 111-5, §141) amended Section 30D effective for vehicles acquired after December 31, 2009. |

|

Annual Funding |

JCT estimated tax expenditure for FY2017-2021:16 $6.9 billion17 |

|

Scheduled Termination |

Phased out separately for each automaker when that automaker has sold a total of 200,000 qualified vehicles18 |

|

Description |

Purchasers of plug-in electric vehicles may file to obtain a tax credit of up to $7,500 per vehicle, depending on battery capacity. The vehicle must be acquired for use or lease and not for resale. Additionally, the original use of the vehicle must commence with the taxpayer and the vehicle must be used predominantly in the United States. For purposes of the 30D credit, a vehicle is not considered acquired prior to the time when title to the vehicle passes to the taxpayer under state law. |

|

Qualified Applicant(s) |

Purchasers of qualified vehicles |

|

Applicable Fuel/Technology |

Plug-in electric vehicles |

|

For More Information |

See the IRS web page for the Plug-In Electric Drive Vehicle Credit (IRC 30D); and the Qualified Plug-In Electric Vehicle (PEV) Tax Credit web page on the U.S. Department of Energy's (DOE's) Alternative Fuels Data Center (AFDC) website. |

|

Related CRS Reports |

CRS Report R41769, Energy Tax Policy: Issues in the 112th Congress, by Molly F. Sherlock and Margot L. Crandall-Hollick (available to congressional clients upon request) |

Department of Energy

Advanced Technology Vehicles Manufacturing Loan Program (ATVM)

|

Administered by |

Loan Programs Office (LPO) |

|

Authority |

Authorized by the Energy Independence and Security Act of 2007 §136 (P.L. 110-140), funded by the Consolidated Security, Disaster Assistance, and Continuing Appropriations Act (P.L. 110-329) |

|

Annual Funding |

$5 million for FY2018 (for program administration) |

|

Scheduled Termination |

Facilities funded must be placed in service by the end of 2020. The Trump Administration recommended in its FY2019 budget that the ATVM program be eliminated and administration expenses reduced to $1 million; Congress did not approve the budget rescission. |

|

Description |

The Advanced Technology Vehicles Manufacturing (ATVM) Loan Program was established in 2007 to help automakers meet mandated vehicle fuel economy standards and to encourage domestic production of more fuel-efficient cars and light trucks. It provides up to $25 billion in revolving loans to qualified automakers for investment in their manufacturing operations. In FY2008, $7.51 billion was appropriated for the direct loans—$7.5 billion for the loan subsidies (available until expended) and $10 million for administration. Although appropriations are provided annually for administration, Congress approved the program loan subsidy authority one time. Currently, loans have been made to five companies, using $8.4 billion of the $25 billion loan authority. No projects have been funded with ATVM loans since March 2011. |

|

Qualified Applicant(s) |

An automotive manufacturer satisfying specified fuel economy requirements or a manufacturer of qualifying components. To be financially eligible for an ATVM loan, an applicant must be financially viable without the receipt of additional federal funding for the proposed project. |

|

Applicable Fuel/Technology |

No limitations on specific technologies; rather, limits are stipulated for vehicle emissions and fuel consumption |

|

For More Information |

DOE's LPO website; DOE's ATVM website; LPO's Advanced Vehicles Manufacturing Projects' website; and the ATVM 1-Page Summary |

|

Related CRS Reports |

CRS Report R42064, The Advanced Technology Vehicles Manufacturing (ATVM) Loan Program: Status and Issues, by Bill Canis and Brent D. Yacobucci |

Bioenergy Technologies Program (formerly the Biomass and Biorefinery Systems R&D Program)

|

Administered by |

Office of Energy Efficiency and Renewable Energy (EERE) |

|

Authority |

Federal Nonnuclear Energy Research and Development Act of 1974 (P.L. 93-577) Energy Policy and Conservation Act of 1975 (EPCA; P.L. 94-163) Energy Conservation and Production Act of 1976 (ECPA; P.L. 94-385) Department of Energy Organization Act of 1977 (P.L. 95-91) Energy Tax Act (P.L. 95-618) National Energy Conservation Policy Act of 1978 (NECPA; P.L. 95-619) Powerplant and Industrial Fuel Use Act of 1978 (P.L. 95-620) Energy Security Act of 1980 (P.L. 96-294) National Appliance Energy Conservation Act of 1987 (P.L. 100-12) Federal Energy Management Improvement Act of 1988 (P.L. 100-615) Renewable Energy and Energy Efficiency Technology Competitiveness Act of 1989 (P.L. 101-218) Clean Air Act Amendments of 1990 (P.L. 101-549) Solar, Wind, Waste, and Geothermal Power Production Incentives Act of 1990 (P.L. 101-575) Energy Policy Act of 1992 (EPACT; P.L. 102-486) Biomass Research and Development Act of 2000 (Title III of Agricultural Risk Protection Act of 2000; P.L. 106-224) Farm Security and Rural Investment Act of 2002 (P.L. 107-171) Healthy Forest Restoration Act of 2003 (P.L. 108-148) Energy Policy Act of 2005 (EPACT 2005; P.L. 109-58) Energy Independence and Security Act of 2007 (EISA; P.L. 110-140) The Food, Conservation, and Energy Act of 2008 (P.L. 110-234) American Recovery and Reinvestment Act of 2009 (ARRA; P.L. 111-5) |

|

Annual Funding |

$203.6 million for FY2018 |

|

Scheduled Termination |

None |

|

Description |

The Bioenergy Technologies Program works with a broad spectrum of partners (government, industrial, academic, agricultural, and nonprofit), primarily focusing on research, development, demonstration, and deployment (RDD&D) of commercially viable, high-performance biofuels, bioproducts, and biopower made from renewable biomass resources. Other nontransportation applications for biomass and bioenergy systems also are studied under this program. |

|

Qualified Applicant(s) |

Universities and businesses |

|

Applicable Fuel/Technology |

Biofuels |

|

For More Information |

See EERE's Bioenergy Technologies Office (BTO's) website; BTO's Bioenergy FAQ web page; and BTO's Strategic Plan For a Thriving and Sustainable Bioeconomy |

|

Related CRS Reports |

CRS Report R41440, Biopower: Background and Federal Support, by Kelsi Bracmort; CRS Report R43416, Energy Provisions in the 2014 Farm Bill (P.L. 113-79): Status and Funding, by Kelsi Bracmort |

Clean Cities Program

|

Administered by |

EERE and sponsored by the Vehicle Technologies Program |

|

Authority |

Established by the Alternative Motor Fuels Act of 1988 (P.L. 100-494), and amended by the Energy Policy Act of 1992 (P.L. 102-486) |

|

Annual Funding |

$37.8 million for FY2018 |

|

Scheduled Termination |

None |

|

Description |

Initially started in 1993 as a DOE program to promote alternative fuel vehicles among the states, it is now a broader program to reduce petroleum consumption in transportation, with 100 Clean Cities coalitions that focus on deployment of alternative and renewable fuels, idle-reduction measures, fuel economy improvements, and emerging transportation technologies. Clean Cities provides technical, informational, and financial assistance to communities. |

|

Qualified Applicant(s) |

Businesses, fuel providers, vehicle fleets, state and local government agencies, and community organizations, led by nearly 100 Vehicle Technologies Program Clean Cities coordinators |

|

Applicable Fuel/Technology |

Electricity, natural gas, propane, bio-methane, ethanol, biodiesel, hydrogen |

|

For More Information |

See DOE's Clean Cities website; and EERE's Clean Cities Overview factsheet. |

|

Related CRS Reports |

None |

Hydrogen and Fuel Cell Technologies Program

|

Administered by |

EERE |

|

Authority |

Federal Energy Administration Act of 1974 (P.L. 93-275) Federal Nonnuclear Energy Research and Development Act of 1974 (P.L. 93-577) Energy Policy and Conservation Act of 1975 (EPCA; P.L. 94-163) Electric and Hybrid Vehicle Research, Development and Demonstration Act (P.L. 94-413) Department of Energy Organization Act of 1977 (P.L. 95-91) Automotive Propulsion Research and Development Act of 1978 (Title III of Department of Energy Act of 1978-Civilian Applications; P.L. 95-238) Methane Transportation Research, Development and Demonstration Act of 1980 (P.L. 96-512) Energy Security Act of 1980 (P.L. 96-294) Alternative Motor Fuels Act of 1988 (P.L. 100-494) Spark M. Matsunaga Hydrogen Research, Development, and Demonstration Act of 1990 (P.L. 101-566) Energy Policy Act of 1992 (EPACT; P.L. 102-486) Hydrogen Future Act of 1996 (P.L. 104-271) Energy Policy Act of 2005 (EPACT 2005; P.L. 109-58) Energy Independence and Security Act of 2007 (EISA; P.L. 110-140) American Recovery and Reinvestment Act of 2009 (ARRA; P.L. 111-5) |

|

Annual Funding |

$100.3 million for FY2018 |

|

Scheduled Termination |

None |

|

Description |

This program works with industry, national laboratories, universities, government agencies, and other partners to overcome barriers to the use of hydrogen and fuel cells. It includes a research and development (R&D) effort focused on advancing the performance and reducing the cost of these technologies. R&D applies to both transportation and stationary applications. |

|

Qualified Applicant(s) |

Federal government, national laboratories, colleges and universities, and for-profit organizations |

|

Applicable Fuel/Technology |

Hydrogen, fuel cells |

|

For More Information |

See EERE's Fuel Cell Technologies website; the Fuel Cell Technologies Office's Publication & Product Library, including annual progress reports for the program. |

|

Related CRS Reports |

[Archived] CRS Report R40168, Alternative Fuels and Advanced Technology Vehicles: Issues in Congress, by Brent D. Yacobucci |

Vehicle Technologies Program (VTP)

|

Administered by |

EERE |

|

Authority |

Authorized by the Energy Independence and Security Act of 2007 §136 (P.L. 110-140), funded by the Consolidated Security, Disaster Assistance, and Continuing Appropriations Act (P.L. 110-329) |

|

Annual Funding |

$304.9 million for FY2018—of that amount not less than $160 million for Batteries and Electric Drive Technology programs |

|

Scheduled Termination |

None |

|

Description |

Through research and development, VTP supports partnerships with other public and private organizations to enhance energy efficiency and productivity and bring clean, affordable technologies to market. It supports research on electric batteries, more efficient engines, and advanced lightweight materials. In addition, it supports, and works through, two major government-industry endeavors: the US DRIVE Partnership and the 21st century Truck Partnership. |

|

Qualified Applicant(s) |

Universities, vehicle and engine manufacturers, material suppliers, nonprofit technology organizations, energy suppliers, and national laboratories |

|

Applicable Fuel/Technology |

Advanced batteries, power electronics and electric motors, advanced combustion, lightweight materials, vehicle-to-grid interaction, and fuel cell and hydrogen technologies |

|

For More Information |

See EERE's Vehicle Technology Office website; and annual progress reports for the Vehicle Technologies Office and its six R&D subprograms. |

|

Related CRS Reports |

CRS Report R42064, The Advanced Technology Vehicles Manufacturing (ATVM) Loan Program: Status and Issues, by Bill Canis and Brent D. Yacobucci |

Department of Transportation

Congestion Mitigation and Air Quality Improvement Program

|

Administered by |

Federal Highway Administration (FHWA) and Federal Transit Administration (FTA) |

|

Authority |

Established by the Intermodal Surface Transportation Efficiency Act (ISTEA) of 1991 (P.L. 102-240); reauthorized multiple times, most recently by the Safe, Accountable, Flexible, and Efficient Transportation Equity Act: A Legacy for Users (SAFETEA-LU) of 2005 (P.L. 109-59); extended multiple times, most recently by the Highway and Transportation Funding Act of 2014 (P.L. 113-159), and Fixing America's Surface Transportation Act (FAST Act, P.L. 114-94) |

|

Annual Funding |

$2.40 billion in FY2018; $2.45 billion requested for FY2019 |

|

Scheduled Termination |

Reauthorized through FY2020 |

|

Description |

Congestion Mitigation and Air Quality Improvement (CMAQ) provides funds to states for transportation projects designed to reduce traffic congestion and improve air quality, particularly in areas of the country that do not attain National Ambient Air Quality Standards. In particular, it authorizes funding for programs and projects intended to reduce carbon monoxide, particulate matter, and ozone. CMAQ funds are apportioned in accordance with a formula based largely on a state's population and pollution reduction needs. |

|

Qualified Applicant(s) |

State departments of transportation and metropolitan planning organizations (MPOs) |

|

Applicable Fuel/Technology |

Any transportation project or technology that can lead to reductions in congestion or help improve air quality |

|

For More Information |

See FHWA's CMAQ website. |

|

Related CRS Reports |

CRS Report R44388, Surface Transportation Funding and Programs Under the Fixing America's Surface Transportation Act (FAST Act; P.L. 114-94), coordinated by Robert S. Kirk |

Corporate Average Fuel Economy Program Alternative Fuel Vehicle Credits

|

Administered by |

National Highway Traffic Safety Administration (NHTSA) |

|

Authority |

Corporate Average Fuel Economy (CAFE) program established in the Energy Policy and Conservation Act (EPCA) of 1975 (P.L. 94-163); alternative fuels incentives established in the Alternative Motor Fuels Act (P.L. 100-494); amended multiple times, most recently by the Energy Independence and Security Act of 2007, §109 (P.L. 110-140), to extend the expiration date through model year 2019 for dual fueled vehicles |

|

Annual Funding |

N/A |

|

Scheduled Termination |

No expiration for dedicated vehicles; after model year (MY) 2019 for dual fueled vehicles |

|

Description |

Automakers that sell passenger cars and light trucks in the United States must comply with federal CAFE standards. Those standards set fuel economy targets which automakers must meet, averaged across their car and light truck fleets. Those targets vary by vehicle class and size. To promote the production and sale of alternative fuel vehicles and provide flexibility in compliance, automakers may accrue CAFE credits by selling alternative fuel vehicles. For dedicated vehicles (i.e., vehicles that run solely on alternative fuel), credits are unlimited. For dual fueled vehicles (i.e., that may run on conventional or alternative fuel), credits are limited: The maximum fuel economy increase allowed through the use of dual fueled vehicle credits is 1.2 miles per gallon through model year (MY) 2014. After 2014 the credits are phased down and completely eliminated after MY 2019. The Trump Administration has proposed to retain MY 2020 CAFE standards through MY 2026, reversing increases proposed by the Obama Administration. |

|

Qualified Applicant(s) |

Automakers that produce vehicles for sale in the United States |

|

Applicable Fuel/Technology |

Incentives apply to vehicles capable of operating on methanol (at least 85%), ethanol (at least 85%), natural gas, liquefied petroleum gas, hydrogen, coal-derived liquid fuels, biologically derived fuels, and electricity. |

|

For More Information |

See NHTSA's CAFE website. |

|

Related CRS Reports |

CRS Report R45204, Vehicle Fuel Economy and Greenhouse Gas Standards: Frequently Asked Questions, by Richard K. Lattanzio, Linda Tsang, and Bill Canis |

Low or No Emission Vehicle Program

|

Administered by |

Federal Transit Administration (FTA) |

|

Authority |

Established by the Fixing America's Surface Transportation Act (FAST Act) of 2015, P.L. 114-94, §3017, amending 49 U.S.C. 5339 |

|

Annual Funding |

$55 million per year through FY2020. An additional $29.5 million was appropriated for FY2018 for a total of $84.5 million |

|

Scheduled Termination |

End of FY2020 |

|

Description |

The Low or No Emission Vehicle program provides funding to state and local governmental authorities for the purchase or lease of zero-emission and low-emission transit buses as well as acquisition, construction, and leasing of required supporting facilities. The federal share of the cost of leasing or purchasing a transit bus is not to exceed 85% of the total transit bus cost. The federal share in the cost of leasing or acquiring low- or no-emission bus-related equipment and facilities is 90% of the net project cost. |

|

Qualified Applicant(s) |

Eligible applicants include direct recipients of FTA grants under the Section 5307 Urbanized Area Formula program, states, and Indian Tribes. Except for projects proposed by Indian Tribes, proposals for funding eligible projects in rural (nonurbanized) areas must be submitted as part of a consolidated state proposal. |

|

Applicable Fuel/Technology |

Proposed vehicles must make greater reductions in energy consumption and harmful emissions, including direct carbon emissions, than comparable standard buses. Eligible technologies include buses and fueling infrastructure for vehicles powered by electricity, CNG, propane, fuel cells, and hybrid fuels, such as diesel-electric buses. |

|

For More Information |

See FTA's Low or No Emission Vehicle Program website. |

|

Related CRS Reports |

CRS Report R44388, Surface Transportation Funding and Programs Under the Fixing America's Surface Transportation Act (FAST Act; P.L. 114-94), coordinated by Robert S. Kirk |

Environmental Protection Agency

National Clean Diesel Campaign

|

Administered by |

Office of Transportation and Air Quality (OTAQ) |

|

Authority |

Established in 2005 by the Energy Policy Act of 2005 (P.L. 109-58), §§791-797; amended in 2008 by P.L. 110-255, §3; and amended in 2011 by the Diesel Emissions Reduction Act of 2010 (P.L. 111-364), §2 |

|

Annual Funding |

$59.6 million for FY2018 |

|

Scheduled Termination |

None (last authorized through FY2016, but the program is still active and receiving funding) |

|

Description |

The National Clean Diesel Campaign (NCDC) promotes clean air strategies by working with manufacturers, fleet operators, air quality professionals, environmental and community organizations, and state and local officials to reduce diesel emissions. States are allocated funds for their clean diesel programs through the Diesel Emission Reduction Act (DERA). |

|

Qualified Applicant(s) |

Manufacturers, fleet operators, air quality professionals, environmental and community organizations, and state and local governments |

|

Applicable Fuel/Technology |

Technologies that significantly reduce emissions (EPA maintains a list of verified retrofit technologies and emerging technologies at http://www.epa.gov/cleandiesel/verification/verif-list.htm). |

|

For More Information |

See EPA's National Clean Diesel Campaign website. |

|

Related CRS Reports |

None |

Renewable Fuel Standard

|

Administered by |

OTAQ |

|

Authority |

Established in 2005 by the Energy Policy Act of 2005, §1501 (P.L. 109-58); expanded by the Energy Independence and Security Act of 2007, §202 (P.L. 110-140) |

|

Annual Funding |

N/A |

|

Scheduled Termination |

None |

|

Description |

The Energy Policy Act of 2005 established a renewable fuel standard (RFS) for automotive fuels. The RFS was expanded by the Energy Independence and Security Act of 2007. The RFS requires the use of renewable fuels (including ethanol and biodiesel) in transportation fuel. In 2011, fuel suppliers were required to include 13.95 billion gallons of renewable fuels in the national transportation fuel supply; this requirement increases annually to 36 billion gallons in 2022. The expanded RFS also specifically mandates the use of "advanced biofuels"—fuels produced from noncorn feedstocks and with 50% lower lifecycle greenhouse gas emissions than petroleum fuel—starting in 2009. Of the 36 billion gallons required in 2022, at least 21 billion gallons must be advanced biofuels. There are also specific quotas for cellulosic biofuels and for biomass-based diesel fuel. On May 1, 2007, EPA issued a final rule on the original RFS program detailing compliance standards for fuel suppliers, as well as a system to trade renewable fuel credits between suppliers. On March 26, 2010, EPA issued final rules for the expanded program (RFS2), including lifecycle analysis methods necessary to categorize fuels as advanced biofuels, and new rules for credit verification and trading. While this program is not a direct subsidy for the construction of biofuels plants, the guaranteed market created by the RFS is believed to have stimulated growth of the biofuels industry and raised prices above where they would have been in the absence of the mandate. In certain circumstances, EPA has the authority to waive portions of the RFS mandates. Since 2014, the total renewable fuel statutory target has not been met, with the advanced biofuel portion falling below the statutory target by a large margin since 2015. |

|

Qualified Applicant(s) |

Gasoline and diesel fuel suppliers—generally refiners, but other entities may also be covered |

|

Applicable Fuel/Technology |

All biofuels (conventional ethanol, biodiesel, renewable diesel, cellulosic biofuels, advanced biofuels) |

|

For More Information |

See EPA's Renewable Fuel Standard (RFS) website. |

|

Related CRS Reports |

CRS Report R43325, The Renewable Fuel Standard (RFS): An Overview, by Kelsi Bracmort; CRS Report R44045, The Renewable Fuel Standard (RFS): Waiver Authority and Modification of Volumes, by Kelsi Bracmort; CRS Recorded Event WRE00231, An Overview of the Renewable Fuel Standard (RFS), by Kelsi Bracmort and Brent D. Yacobucci; and CRS Report R41106, The Renewable Fuel Standard (RFS): Cellulosic Biofuels, by Kelsi Bracmort |

Department of Agriculture19

Bioenergy Program for Advanced Biofuels20

|

Administered by |

Rural Development |

|

Authority |

Established by the Farm Security and Rural Investment Act of 2002 (P.L. 107-171). Most recently amended by Title IX, Section 9005 of the Agriculture Improvement Act of 2018 (P.L. 115-334). |

|

Annual Funding |

Mandatory: The 2018 farm bill (P.L. 115-334) authorized mandatory Commodity Credit Corporation (CCC) funding of $7 million annually for FY2019-FY2023 to remain available until expended. The 2014 farm bill (P.L. 113-79) authorized mandatory CCC funding of $15 million annually for FY2014-FY2018 to remain available until expended. Discretionary: Discretionary funding of $20 million annually for FY2014-FY2023 is authorized to be appropriated. No discretionary funding has been appropriated for the Bioenergy Program for Advanced Biofuels through FY2018. |

|

Scheduled Termination |

Authorized through FY2023 |

|

Description |

The purpose of the program is to support and ensure an expanding production of advanced biofuels by providing payments to eligible advanced biofuel producers. Participating producers are paid on a quarterly basis for the quantity of eligible advanced biofuels produced in that quarter. Producers who increase their annual production over the previous fiscal year may also be eligible for additional incremental payments issued annually. Not more than 5% of total payments made in a given fiscal year may go to producers for production at facilities with a total refining capacity exceeding 150 million gallons a year. The 2018 farm bill limited the proportion of total payments made for biofuels derived from a single eligible commodity to not more than one third of total funds available in a given fiscal year. |

|

Qualified Applicant(s) |

Producers of advanced biofuels |

|

Applicable Fuel/Technology |

Payments will be made to eligible advanced biofuel producers for the production of fuel derived from renewable biomass, other than corn kernel starch, to include biofuel derived from cellulose, hemicellulose, or lignin; biofuel derived from sugar and starch (other than ethanol derived from corn kernel starch); biofuel derived from waste material, including crop residue, other vegetative waste material, animal waste, food waste, and yard waste; diesel-equivalent fuel derived from renewable biomass, including vegetable oil and animal fat; biogas (including landfill gas and sewage waste treatment gas) produced through the conversion of organic matter from renewable biomass; butanol or other alcohols produced through the conversion of organic matter from renewable biomass; and other fuel derived from cellulosic biomass. |

|

For More Information |

See the USDA program website and program number 10.867 on the beta.SAM.gov website. |

|

Related CRS Reports |

CRS Report R40913, Renewable Energy and Energy Efficiency Incentives: A Summary of Federal Programs, by Lynn J. Cunningham |

Biomass Crop Assistance Program (BCAP; §9011)21

|

Administered by |

Farm Service Agency (FSA) |

|

Authority |

Established by the Food, Conservation, and Energy Act of 2008 (P.L. 110-246). Most recently amended by Title IX, Section 9010 of the Agriculture Improvement Act of 2018 (P.L. 115-334). |

|

Annual Funding |

Mandatory: The 2018 farm bill provided no mandatory funding. The 2014 farm bill authorized mandatory CCC funding of $25 million annually from FY2014 through FY2018. Discretionary: Discretionary funding of $25 million annually for FY2014-FY2023 is authorized to be appropriated. |

|

Scheduled Termination |

Authorized through FY2023 |

|

Description |

BCAP provides assistance to support the production of eligible biomass crops on land within approved BCAP project areas. In exchange for growing eligible crops, the FSA is to provide annual payments through 5- to 15-year contracts. Under these contracts up to 50% of establishment costs may also be provided. FSA also is to provide matching payments to eligible material owners at a rate of $1 for each $1 per dry ton paid by a qualified biomass conversion facility. Payments may not exceed $20 per ton for a two-year period, and matching payments are available for no more than two years per participant. |

|

Qualified Applicant(s) |

Producer of an eligible crop in a BCAP project area; Person with the right to collect or harvest eligible material. |

|

Applicable Fuel/Technology |

Eligible crops and eligible material, both of which have exclusions specified in statute. Eligible material for a matching payment is renewable biomass with several important exclusions including harvested grains, fiber, or other commodities eligible to receive payments under the Commodity Title (Title I) of the 2014 farm bill (the residues of these commodities, however, are eligible and may qualify for payment); animal waste and animal waste byproducts including fats, oils, greases, and manure; food waste, and yard waste. The 2018 farm bill includes algae as an eligible material; algae was previously an eligible crop but not an eligible material. Eligible crops for annual payments include renewable biomass, with the exception of crops eligible to receive a payment under Title I of the 2014 farm bill and plants that are invasive or noxious, or have the potential to become invasive or noxious. |

|

For More Information |

See program number 10.087 on the beta.SAM.gov website. |

|

Related CRS Reports |

CRS Report R40913, Renewable Energy and Energy Efficiency Incentives: A Summary of Federal Programs, by Lynn J. Cunningham; and CRS Report R41296, Biomass Crop Assistance Program (BCAP): Status and Issues, by Mark A. McMinimy |

Biomass Research and Development (BRDI)22

|

Administered by |

National Institute of Food and Agriculture (NIFA) |

|

Authority |

Established by the Biomass Research and Development Act of 2000, §307 (P.L. 106-224). Most recently amended by Section 7507 of the Agriculture Improvement Act of 2018 (P.L. 115-334). |

|

Annual Funding |

Mandatory: The 2018 farm bill provided no mandatory funding. The 2014 farm bill authorizes mandatory funding (to remain available until expended) of $3 million for four fiscal years—FY2014-FY2017—with baseline funding authority expiring after FY2017. Discretionary: Discretionary funding of $20 million is authorized to be appropriated annually for FY2014-FY2023. However, no discretionary funding was appropriated for BRDI through FY2018. A DOE funding match of up to $3 million of discretionary funding is subject to annual appropriations; DOE contributed up to $3 million for FY2017.23 |

|

Scheduled Termination |

Authorized through FY2023 |

|

Description |

Competitive funding including grants, contracts, and financial assistance for biomass research, development, and demonstration projects. A minimum of 15% of funding must go to each of three program areas: feedstock development, biofuels and biobased products development, and biofuels development analysis. |

|

Qualified Applicant(s) |

Institutions of higher learning (colleges and universities), national laboratories, federal or state research entities, private-sector entities, and nonprofit organizations |

|

Applicable Fuel/Technology |

Biomass; biofuels |

|

For More Information |

See the USDA program website. |

Biorefinery, Renewable Chemical, and Biobased Product Manufacturing Assistance Program (formerly the Biorefinery Assistance Program)24

|

Administered by |

Rural Development |

|

Authority |

Established by Title IX of the Farm Security and Rural Investment Act of 2002 (FSRIA, P.L. 107-171). Most recently amended by Title IX Section 9003 of the Agriculture Improvement Act of 2018 (P.L. 115-334). |

|

Annual Funding |

Mandatory: Under the 2018 farm bill, mandatory CCC funding of $50 million in FY2019 and $25 million in FY2020 (to remain available until expended) was authorized for loan guarantees. There is no new baseline funding after FY2020. The 2014 farm bill authorized mandatory CCC funding of $100 million in FY2014 and $50 million each for FY2015 and FY2016. Funding for grants was eliminated in 2014. Discretionary: Discretionary funds of $75 million annually are authorized to be appropriated for FY2014-FY2023. No discretionary funding has been appropriated for this program through FY2018. |

|

Scheduled Termination |

Authorized through FY2023 |

|

Description |

The purpose of the program is to assist in the development of new and emerging technologies for the development of advanced biofuels, renewable chemicals, and biobased product manufacturing so as to increase the energy independence of the United States; promote resource conservation, public health, and the environment; diversify markets for agricultural and forestry products and agriculture waste material; and create jobs and enhance the economic development of the rural economy. Loan guarantees are made to fund the development, construction, and retrofitting of commercial-scale biorefineries using eligible technology. The maximum loan guarantee is $250 million. |

|

Qualified Applicant(s) |

Individuals, entities, Indian tribes, state or local governments, corporations, farm cooperatives, farmer cooperative organizations, associations of agricultural producers, national laboratories, institutions of higher education, rural electric cooperatives, public power entities, and consortia of any of the previous entities |

|

Applicable Fuel/Technology |

Technologies being adopted in a viable commercial-scale operation of a biorefinery that produces an advanced biofuel, renewable chemical, or biobased product; technologies that have been demonstrated to have technical and economic potential for commercial application in a biorefinery that produces one or more of these products. |

|

For More Information |

See the USDA program website; and program number 10.865 on the beta.SAM.gov website. |

Rural Energy for America Program (REAP) Grants and Loans25

|

Administered by |

Rural Development |

|

Authority |

Established by Title IX, Sections 9005 and 9006 of the Farm Security and Rural Investment Act of 2002 (FSIRA, P.L. 107-171). Most recently amended by Title IX, Section 9007 of Agriculture Improvement Act of 2018 (P.L. 115-334). |

|

Annual Funding |

Mandatory: The 2018 farm bill retains mandatory funding of $50 million for FY2014 and each fiscal year thereafter (therefore REAP's mandatory funding authority does not expire with the 2014 farm bill). Mandatory funds are to remain available until expended. Discretionary: Discretionary funding of $20 million annually is authorized to be appropriated for FY2014-FY2023. Actual discretionary appropriations have been $3.5 million in FY2014; and $1.35 million in FY2015; $500,000 in FY2016; $352,000 in FY2017; and $293,000 in FY2018. |

|

Scheduled Termination |

Authorized with no expiration |

|

Description |

REAP promotes energy efficiency and renewable energy for agricultural producers and rural small businesses through the use of (1) grants for energy audits and renewable energy development assistance, and (2) financial assistance for renewable energy systems and energy efficiency improvements. The 2018 farm bill added new funding for equipment that exceeds energy efficiency standards and capped funding for this category of loan guarantees at 15% of total funds. The 2014 farm bill excluded the use of REAP funds for installing retail energy dispensing equipment, such as blender pumps. |

|

Qualified Applicant(s) |

Eligible entities to receive grants to provide energy audits and renewable development assistance to agricultural producers and rural small businesses include state, tribal, or local governments; land-grant colleges or other institutions of higher education; rural electric cooperatives; public power entities; councils; and other similar entities. Agricultural producers and rural small businesses are eligible to receive direct financial assistance for energy efficiency improvements and renewable energy systems. |

|

Applicable Fuel/Technology |

Biofuels (see description above), among other technologies. |

|

For More Information |

See the USDA program website; and program number 10.868 on the beta.SAM.gov website. |

|

Related CRS Reports |

CRS Report RL31837, An Overview of USDA Rural Development Programs, by Tadlock Cowan; CRS Report R40913, Renewable Energy and Energy Efficiency Incentives: A Summary of Federal Programs, by Lynn J. Cunningham |

Appendix A. Recently Expired or Repealed Programs26

Alternative Fuel Refueling Property Credit27

|

Administered by |

IRS |

|

Authority |

Established by the Energy Policy Act of 2005 (P.L. 109-58), Title XIII, §1342(a). Amended by P.L. 109-135, Title IV, §402(k), 412(d), P.L. 110-172, §6(b), P.L. 113-295, and P.L. 115-141. The temporary alternative fuel refueling property credit has expired and subsequently has been extended retroactively on multiple occasions, most recently through 2017 by the Bipartisan Budget Act of 2018 (P.L. 115-123). |

|

Annual Funding |

JCT estimated budget effect for FY2018: $49 million. JCT estimated budget effect for FY2018-FY2022: $63 million.28 |

|

Termination Date |

December 31, 2017 |

|

Description |

Consumers or businesses who installed qualified fueling equipment received a 30% tax credit of up to $30,000 for properties subject to an allowance for depreciation and $1,000 for all other properties. |

|

Qualified Applicant(s) |

Consumers or businesses who installed qualifying equipment/property. |

|

Applicable Fuel/Technology |

Natural gas, liquefied petroleum gas, hydrogen, electricity, E85, or diesel fuel blends containing a minimum of 20% biodiesel. |

|

For More Information |

See IRS Form 8911. |

|

Related CRS Reports |

CRS Report R44990, Energy Tax Provisions That Expired in 2017 ("Tax Extenders"), by Molly F. Sherlock, Donald J. Marples, and Margot L. Crandall-Hollick |

Alternative Motor Vehicle Credit29

|

Administered by |

IRS |

|

Authority |

Established by the Energy Policy Act of 2005 (P.L. 109-58 §1341(a)), American Recovery and Reinvestment Act of 2009 (P.L. 111-5, Div. B, §1141-1144). The Consolidated Appropriations Act of 2016 (P.L. 114-113) extended through 2016 (retroactive for 2015) the alternative motor vehicle credit for qualified fuel cell motor vehicles only; further extended by the Bipartisan Budget Act of 2018 (P.L. 115-123) through 2017 |

|

Annual Funding |

JCT estimated tax expenditure for FY2017-2021: $100 million30 |

|

Termination Date |

December 31, 2017, for fuel cell vehicles; expired December 31, 2010, or earlier for all other vehicles. |

|

Description |

Enacted in the Energy Policy Act of 2005, the provision included separate credits for four distinct types of vehicles: those using fuel cells, advanced lean burn technologies, qualified hybrid technologies, and qualified alternative fuels technologies. |

|

Qualified Applicant(s) |

Taxpayers purchasing a qualified fuel or technology |

|

Applicable Fuel/Technology |

Hybrid gasoline-electric; diesel; battery-electric; alternative fuel and fuel cell vehicles; and advanced lean-burn technology vehicles |

|

For More Information |

See IRS Form 8910: Alternative Motor Vehicle Credit and IRS Notice 2008-33. |

|

Related CRS Reports |

CRS Report R44990, Energy Tax Provisions That Expired in 2017 ("Tax Extenders"), by Molly F. Sherlock, Donald J. Marples, and Margot L. Crandall-Hollick |

Biodiesel or Renewable Diesel Income Tax Credit31

|

Administered by |

IRS |

|

Authority |

Established in 2005 by the American Jobs Creation Act of 2004, §302 (P.L. 108-357); extended by the Energy Policy Act of 2005, §1344 (P.L. 109-58); amended by the Energy Improvement and Extension Act of 2008 (P.L. 110-343, Division B), §202-203; The temporary income tax credits for biodiesel and renewable diesel fuels have expired and subsequently have been extended retroactively on multiple occasions, most recently through 2017 by the Bipartisan Budget Act of 2018 (P.L. 115-123) |

|

Annual Funding |

JCT estimated budget effect for FY2018: $3.25 billion32 |

|

Termination Date |

December 31, 2017 |

|

Description |

Producers, blenders, or retailers of biodiesel, renewable diesel,33 or "agri-biodiesel"34 (biodiesel produced from virgin agricultural products such as soybean oil or animal fats) could claim a per-gallon income tax credit through the end of 2017 for fuel sold or used by the taxpayer, whether delivered pure or in a qualified mixture. The credit was valued at $1.00 per gallon. Before amendment by P.L. 110-343, the credit was valued at $1.00 per gallon of agri-biodiesel or 50 cents per gallon of biodiesel produced from previously used agricultural products (e.g., recycled fryer grease). |

|

Qualified Applicant(s) |

Biodiesel producers and blenders |

|

Applicable Fuel/Technology |

Biodiesel, renewable biodiesel, agri-biodiesel |

|

For More Information |

See IRS Publication 510, Chapter 2: Fuel Tax Credits and Refunds; and AFDC's entry for the Biodiesel Mixture Excise Tax Credit on its "Expired, Repealed, and Archived Incentives and Laws" web page. |

|

Related CRS Reports |

CRS Report R44990, Energy Tax Provisions That Expired in 2017 ("Tax Extenders"), by Molly F. Sherlock, Donald J. Marples, and Margot L. Crandall-Hollick |

Biodiesel or Renewable Diesel Mixture Tax Credit35

|

Administered by |

IRS |

|

Authority |

Established in 2005 by the Energy Policy Act of 2005 (P.L. 109-58), §1346; amended by the Energy Improvement and Extension Act of 2008 (P.L. 110-343, Division B), §202-203. The temporary excise tax credits for biodiesel and renewable diesel fuels have expired and subsequently have been extended retroactively on multiple occasions, most recently through 2017 by the Bipartisan Budget Act of 2018 (P.L. 115-123) |

|

Annual Funding |

JCT estimated budget effect for FY2018: $3.25 billion36 |

|

Termination Date |

December 31, 2017 |

|

Description |

Biodiesel and renewable diesel blenders (or producers of diesel/biodiesel blends) could claim a $1.00 per gallon tax credit through the end of 2017 for biodiesel or renewable diesel used to produce a qualified biodiesel mixture. The credit was claimed as a credit against the blender's motor fuels excise taxes; any excess credit beyond the taxpayer's excise tax liability was claimed as direct payments from the IRS. |

|

Qualified Applicant(s) |

Biodiesel, renewable biodiesel, and agri-biodiesel producers and blenders |

|

Applicable Fuel/Technology |

Biodiesel, renewable biodiesel, agri-biodiesel |

|

For More Information |

See IRS Publication 510, Chapter 2: Fuel Tax Credits and Refunds; and AFDC's entry for the Biodiesel Mixture Excise Tax Credit on its "Expired, Repealed, and Archived Incentives and Laws" web page. |

|

Related CRS Reports |

CRS Report R44990, Energy Tax Provisions That Expired in 2017 ("Tax Extenders"), by Molly F. Sherlock, Donald J. Marples, and Margot L. Crandall-Hollick |

Incentives for Alternative Fuel and Alternative Fuel Mixtures37

|

Administered by |

IRS |

|

Authority |

Established by the Safe, Accountable, Flexible, Efficient Transportation Equity Act: A Legacy for Users (SAFETEA; P.L. 109-59); Section 5 of the Tax Technical Corrections Act of 2007 (P.L. 110-172) modified the rules for filing excise tax refund claims for alternative fuel mixtures and the definition of alternative fuels relating to hydrogen and carbon resources. The temporary excise tax credits for alternative fuels and alternative fuel mixtures have expired and subsequently been extended retroactively on multiple occasions, most recently through 2017 by the Bipartisan Budget Act of 2018 (P.L. 115-123)38 |

|

Annual Funding |

JCT estimated budget effect for FY2018: $555 million39 |

|

Termination Date |

December 31, 2017 |

|

Description |

The Alternative Fuel Excise Tax Credit was a 50-cents-per gallon excise tax credit for certain alternative fuels used as fuel in a motor vehicle, motor boat, or airplane, and a related provision established a 50-cents-per-gallon credit for alternative fuels mixed with a traditional fuel (gasoline, diesel, or kerosene) for use as a fuel. |

|

Qualified Applicant(s) |

Taxpayers who supplied or mixed qualifying fuel types |

|

Applicable Fuel/Technology |

Liquefied petroleum gas, P Series fuels, compressed or liquefied natural gas, any liquefied fuel derived from coal or peat, liquefied hydrocarbons derived from biomass, liquefied hydrogen. (Ethanol, methanol, and biodiesel do not qualify for the alternative fuel or alternative fuel mixture credit.) |

|

For More Information |

See IRS Publication 510 and IRS Forms 637, 720, 4136, and 8849 on the IRS website. |

|

Related CRS Reports |

CRS Report R44990, Energy Tax Provisions That Expired in 2017 ("Tax Extenders"), by Molly F. Sherlock, Donald J. Marples, and Margot L. Crandall-Hollick |

Plug-In Electric Vehicle Credit (Two- or Three-Wheeled)40

|

Administered by |

IRS |

|

Authority |

American Recovery and Reinvestment Act, P.L. 111-5, §1142 amended by the American Taxpayer Relief Act of 2012 (P.L. 112-240 §403). This temporary credit has expired and subsequently has been extended retroactively on multiple occasions, most recently through 2017 by the Bipartisan Budget Act of 2018 (P.L. 115-123) |

|

Annual Funding |

JCT estimated budget effect for FY2018: Less than $50 million |

|

Termination Date |

Expired December 31, 2017 for two-wheeled vehicles. Expired December 31, 2013 for three-wheeled vehicles. |

|

Description |

Internal Revenue Code Section 30D provided a tax credit for qualified plug-in electric vehicles. The credit was equal to 10% of the cost of a qualified plug-in electric vehicle and limited to $2,500. Qualified vehicles included vehicles that have two or three wheels. The vehicle must have been acquired for use or lease and not for resale. The original use of the vehicle had to commence with the taxpayer and the vehicle had to be used predominantly in the United States. |

|

Qualified Applicant(s) |

Taxpayers purchasing qualifying vehicles |

|

Applicable Fuel/Technology |

Two- or three-wheeled plug-in electric vehicles |

|

For More Information |

See IRS Notice 2013-67 and IRS form 8936. |

|

Related CRS Reports |

CRS Report R44990, Energy Tax Provisions That Expired in 2017 ("Tax Extenders"), by Molly F. Sherlock, Donald J. Marples, and Margot L. Crandall-Hollick |

Repowering Assistance Program41

|

Administered by |

Rural Development |

|

Authority |

Established by the Food, Conservation, and Energy Act of 2008 (P.L. 110-246). Repealed by the Agriculture Improvement Act of 2018 (P.L. 115-334). |

|

Annual Funding |

Mandatory: Under the 2014 farm bill, mandatory CCC funding of $12 million for FY2014 was authorized, to remain available until expended (i.e., no new baseline funding after FY2014). Discretionary: The 2014 farm bill authorized discretionary funding of $10 million annually to be appropriated for FY2014-FY2018. |

|

Termination Date |

Repealed on December 20, 2018 |

|

Description |

The Repowering Assistance Program (RAP) made payments to eligible biorefineries to encourage the use of renewable biomass as a replacement for fossil fuels used to provide heat for processing or power in the operation of these eligible biorefineries. Not more than 5% of the funds was to be made available to eligible producers with a refining capacity exceeding 150 million gallons of advanced biofuel per year. |

|

Qualified Applicant(s) |

Eligible biorefinery. The biorefinery must have been in existence on or before June 18, 2008. |

|

Applicable Fuel/Technology |

Renewable Biomass |

|

For More Information |

See the USDA program website; and program number 10.866 on the beta.SAM.gov website. |

|

Related CRS Reports |

CRS Report R43416, Energy Provisions in the 2014 Farm Bill (P.L. 113-79): Status and Funding, by Kelsi Bracmort; CRS Report R40913, Renewable Energy and Energy Efficiency Incentives: A Summary of Federal Programs, by Lynn J. Cunningham |

Second Generation Biofuel Producer Credit (previously the Credit for Production of Cellulosic and Algae-Based Biofuel)42

|

Administered by |

IRS |

|

Authority |

Established on January 1, 2009, by the Food, Conservation, and Energy Act of 2008, §15321 (P.L. 110-246); amended by the Health Care and Education Reconciliation Act of 2010 (P.L. 111-152), §1408; amended by the Small Business Jobs Act of 2010 (P.L. 111-240), §2121; amended by the American Taxpayer Relief Act of 2012 (P.L. 112-240 §404). This temporary credit has expired and subsequently has been extended retroactively on multiple occasions, most recently through 2017 by the Bipartisan Budget Act of 2018 (P.L. 115-123) |

|

Annual Funding |

JCT estimated tax expenditure for FY2017-FY2021: Less than $50 million total |

|

Termination Date |

December 31, 2017 |

|

Description |

Producers of cellulosic biofuel could claim a tax credit of $1.01 per gallon. For cellulosic ethanol producers, the value of the production tax credit was reduced by the value of the volumetric ethanol excise tax credit and the small ethanol producer credit; the credit was last valued at $1.01 cents per gallon (the offsetting tax credits have expired). P.L. 112-240 amended the credit to include noncellulosic fuel produced from algae feedstocks. The credit applied to fuel produced after December 31, 2008. |

|

Qualified Applicant(s) |

Cellulosic biofuel producers and algae-based biofuel producers |

|

Applicable Fuel/Technology |

Cellulosic biofuels and algae-based biofuels |

|

For More Information |

See AFDC's entry for the Second Generation Biofuel Producer Tax Credit on its "Expired, Repealed, and Archived Incentives and Laws" web page; and IRS Publication 510 and IRS Forms 637 and 6478, which are available via the IRS website. |

|

Related CRS Reports |

CRS Report R42122, Algae's Potential as a Transportation Biofuel, by Kelsi Bracmort; and CRS Report R44990, Energy Tax Provisions That Expired in 2017 ("Tax Extenders"), by Molly F. Sherlock, Donald J. Marples, and Margot L. Crandall-Hollick |

Small Agri-Biodiesel Producer Credit43

|

Administered by |

IRS |

|

Authority |

Established in 2005 by the Energy Policy Act of 2005, §1345 (P.L. 109-58); amended by the Energy Improvement and Extension Act of 2008 (P.L. 110-343, Division B), §202-203. This temporary credit has expired and subsequently has been extended retroactively on multiple occasions, most recently through 2017 by the Bipartisan Budget Act of 2018 (P.L. 115-123). |

|

Annual Funding |

JCT estimated tax expenditure for FY2017-2021: JCT has not estimated this expenditure44 |

|

Termination Date |

December 31, 2017 |

|

Description |

The small agri-biodiesel producer credit was valued at 10 cents per gallon of "agri-biodiesel" (see Biodiesel Tax Credit, above) produced. The credit could be claimed on the first 15 million gallons of ethanol produced by a small producer in a given year through the end of 2017. Agri-biodiesel is defined as biodiesel derived solely from virgin oils, including esters derived from virgin vegetable oils from corn, soybeans, sunflower seeds, cottonseeds, canola, crambe, rapeseeds, safflowers, flaxseeds, rice bran, mustard seeds, and camelina, and from animal fats. |

|

Qualified Applicant(s) |

Any agri-biodiesel producers with production capacity less than 60 million gallons per year |

|

Applicable Fuel/Technology |

Biodiesel |

|

For More Information |

See IRS Publication 510, Chapter 2: Fuel Tax Credits and Refund; and IRS Form 8864, and Instructions for Form 8864. |

|

Related CRS Reports |

CRS Report R41631, The Market for Biomass-Based Diesel Fuel in the Renewable Fuel Standard (RFS), by Brent D. Yacobucci; and CRS Report R44990, Energy Tax Provisions That Expired in 2017 ("Tax Extenders"), by Molly F. Sherlock, Donald J. Marples, and Margot L. Crandall-Hollick |

Special Depreciation Allowance for Second Generation (Cellulosic and Algae-Based) Biofuel Plant Property45

|

Administered by |

IRS |

|

Authority |

Established in 2006 by the Tax Relief and Health Care Act of 2006 (P.L. 109-432), §209; amended by the Energy Improvement and Extension Act of 2008 (P.L. 110-343, Division B), §201; modified by the Tax Relief, Unemployment Insurance Reauthorization, and Job Creation Act of 2010 (P.L. 111-312), §401; amended by the American Taxpayer Relief Act of 2012 (P.L. 112-240, §410). This temporary credit has expired and subsequently has been extended retroactively on multiple occasions, most recently through 2017 by the Bipartisan Budget Act of 2018 (P.L. 115-123). |

|

Annual Funding |

JCT estimated tax expenditure for FY2017-FY2021: Less than $50 million total |

|

Termination Date |

December 31, 2017 |

|

Description |

A taxpayer could take a depreciation deduction of 50% of the adjusted basis of a new cellulosic or algae-based biofuel plant in the year it was put in service. Any portion of the cost financed through tax-exempt bonds was exempted from the depreciation allowance. Before amendment by P.L. 110-343 the accelerated depreciation applied only to cellulosic ethanol plants that break down cellulose through enzymatic processes—the amended provision applied to all cellulosic biofuel plants. Before amendment by P.L. 112-240 the provision did not apply to algae-based biofuel plants: the incentive for algae-based plants applies to property was placed in service after January 2, 2013. |

|

Qualified Applicant(s) |

Any cellulosic biofuel plant acquired after December 20, 2006, and placed in service before January 1, 2014, and any algae-based biofuel plant placed in service between January 2, 2013, and December 31, 2017. Any plant that had a binding contract for acquisition before December 20, 2006, did not qualify. |

|

Applicable Fuel/Technology |

Cellulosic and algae-based biofuels |

|

For More Information |

See Senate Finance Committee, Summary of House-Senate Agreement on Tax, Trade, Health, and Other Provisions, December 7, 2006. |

|

Related CRS Reports |

CRS Report R42122, Algae's Potential as a Transportation Biofuel, by Kelsi Bracmort; and CRS Report R44990, Energy Tax Provisions That Expired in 2017 ("Tax Extenders"), by Molly F. Sherlock, Donald J. Marples, and Margot L. Crandall-Hollick |

Appendix B contains four tables

- Table B-1 provides a summary of the programs discussed in the body of the report, listed by agency;

- Table B-2 lists programs and incentives for alternative fuels, by fuel type;

- Table B-3 lists programs and incentives for advanced technology vehicles, by vehicle type; and

- Table B-4 lists programs by agency that have expired or were repealed since December 31, 2017.

|

Program |

Description |

FY2018 Appropriation |

Expiration Date |

Eligible Fuels or Technologies |

|

Internal Revenue Service |

||||

|

Idle Reduction Equipment Tax Exemption |

The Idle Reduction Equipment Tax Exemption exempts certain vehicle idling reduction devices from the federal excise tax on heavy trucks and trailers. |

$17 million |

None |

Devices that have been identified by the Administrator of the EPA as reducing idling of a heavy truck or trailer at a motor vehicle rest stop or other location where such vehicles are temporarily parked or remain stationary |

|

Motor Fuels Excise Taxes |

The motor fuels taxes that were included in the Highway Revenue Act of 1956 (P.L. 84-627) were dedicated to supporting the Highway Trust Fund, except for the tax on compressed natural gas, which was enacted in 1993. The federal excise tax on most of these fuels was last raised by Congress in 1993. Taxes vary by fuel: gasoline, 18.4 cents per gallon; diesel fuel, 24.4 cents per gallon; biodiesel, 24.4 cents per gallon; ethanol, 18.4 cents per gallon; P-series fuels, 18.4 cents per gallon; hydrogen, 18.4 cents per gallon equivalent; liquefied petroleum gas (LPG), 18.3 cents per gallon equivalent; compressed natural gas (CNG), 18.3 cents per gallon equivalent; liquefied natural gas (LNG), 24.3 cents per gallon equivalent. Alternative fuel tax credits are or were available against many of these (see "Incentives for Alternative Fuel and Alternative Fuel Mixtures" and "Biodiesel or Renewable Diesel Mixture Tax Credit"). Electricity for electric vehicles is untaxed. These exemptions/credits effectively incentivize selected fuels/vehicles relative to conventional options |

N/Aa |

4.3 cents per gallon of the gasoline/ diesel fuel tax is permanent; the rest of the motor fuels taxes expire on September 30, 2022, when many current highway-related taxes expire |

Gasoline, diesel, liquefied petroleum gas, liquefied natural gas, fuels with methanol from natural gas, P Series fuels, and compressed natural gas |

|

Plug-in Electric Drive Vehicle Credit |

Purchasers of plug-in electric vehicles may file to obtain a tax credit of up to $7,500 per vehicle, depending on battery capacity. |

$1.2 billion |

The credit is phased out when an automaker has sold a total of 200,000 qualified vehicles |

Plug-in electric vehicles |

|

Department of Energy |

||||

|

Advanced Technology Vehicles Manufacturing (ATVM) Program |

ATVM was established in 2007 to help automakers meet mandated vehicle fuel economy standards and to encourage domestic production of more fuel-efficient cars and light trucks. It was first funded in 2008 to provide $25 billion in revolving loans to qualified automakers for investment in their manufacturing operations. In FY2008, $7.51 billion was appropriated for the direct loans—$7.5 billion for the loan subsidies (available until expended) and $10 million for administration. Currently, loans have been made to five companies, using $8.4 billion of the $25 billion loan authority. |

$5 million (for administration) |

Facilities funded must be placed in service by December 31, 2020 |

No limitations on specific technologies; rather, limits are stipulated for vehicle emissions and fuel consumption |

|

Biomass and Biorefinery Systems Program |

The Biomass Program primarily focuses on research, development, demonstration, and deployment (RDD&D) to ensure that cellulosic ethanol is commercially viable by 2012 and that biobased aviation fuel, diesel fuel, and gasoline are price competitive by 2017. |

$203.6 million |

None |

Biofuels |

|

Clean Cities Program |

Initially started in 1993 as a DOE program to promote alternative fuel vehicles among the states, it is now a broader program to reduce petroleum consumption in transportation, with 100 Clean Cities coalitions that focus on deployment of alternative and renewable fuels, idle-reduction measures, fuel economy improvements, and emerging transportation technologies. Clean Cities provides technical, informational, and financial assistance to communities. |

$37.8 million |

None |

Electricity, natural gas, propane, bio-methane, ethanol, biodiesel, hydrogen |

|

Hydrogen and Fuel Cell Technologies Program |

The DOE Hydrogen Program works with industry, national laboratories, universities, government agencies, and other partners to overcome the barriers to the use of hydrogen and fuel cells. It includes a research and development (R&D) effort focused on advancing the performance and reducing the cost of these technologies. |

$100.3 million |

None |

Hydrogen, fuel cells |

|

Vehicle Technologies Program (VTP) |

Through research and development, VTP supports partnerships with other public and private organizations that will enhance energy efficiency and productivity, bring clean and affordable technologies to market, and enhance advanced technology vehicle choices for consumers. |

$304.9 million—of that not less than $160 million for Batteries and Electric Drive Technology program |

None |

Advanced batteries, power electronics and electric motors, advanced combustion, lightweight materials, vehicle-to-grid interaction, and fuel cell and hydrogen technologies |

|

Department of Transportation |

||||

|

Congestion Mitigation and Air Quality Improvement Program (CMAQ) |

Congress directed the DOT to establish the CMAQ program to provide funds for projects and programs that may reduce the emissions of transportation-related pollutants that may cause an area within a state to exceed certain air quality standards. |

$2.4 billion |

September 30, 2020 |

Not limited to alternative fuels or advanced technologies |

|

Corporate Average Fuel Economy (CAFE) Incentives for Alternative Fuel Vehicles |

Automakers subject to Corporate Average Fuel Economy (CAFE) standards may accrue credits under that program for the production and sale of alternative fuel vehicles. For dedicated vehicles (i.e., vehicles that run solely on alternative fuel) credits are unlimited. For dual fueled vehicles (i.e., that may run on conventional or alternative fuel) credits are limited: The maximum fuel economy increase allowed through the use of these credits is 1.2 miles per gallon through model year (MY) 2014. After 2014 the credits are phased down and completely eliminated after MY 2019. |

N/A |

No expiration for dedicated vehicles; after MY 2019 for dual fueled vehicles |

Methanol (at least 85%), ethanol (at least 85%), natural gas, liquefied petroleum gas, hydrogen, coal-derived liquid fuels, biologically derived fuels, and electricity |

|

Low or No Emission Vehicle Program |

The Low or No Emission Vehicle program provides funding to state and local governmental authorities for the purchase or lease of zero-emission and low-emission transit buses as well as acquisition, construction, and leasing of required supporting facilities. The federal share of the cost of leasing or purchasing a transit bus is not to exceed 85% of the total transit bus cost. The federal share in the cost of leasing or acquiring low- or no-emission bus-related equipment and facilities is 90% of the net project cost |

$84.5 million |

September 30, 2020 |

Eligible technologies include buses and fueling infrastructure for vehicles powered by electricity, CNG, propane, fuel cells and hybrid fuels such as diesel-electric buses |

|

Environmental Protection Agency |

||||

|

National Clean Diesel Campaign |