The Payments in Lieu of Taxes (PILT) Program: An Overview

Changes from March 17, 2020 to April 18, 2023

This page shows textual changes in the document between the two versions indicated in the dates above. Textual matter removed in the later version is indicated with red strikethrough and textual matter added in the later version is indicated with blue.

Contents

- Introduction to the Payments in Lieu of Taxes (PILT) Program

- PILT Authorizations and Appropriations

- PILT Payments Under Section 6902

- Entitlement Lands

- Calculating Section 6902 Payments

- PILT Payments Under Sections 6904 and 6905

- Section 6904 Payments

- Section 6905 Payments

- Issues for Congress

Figures

Summary

TheThe Payments in Lieu of Taxes (PILT) Program: April 18, 2023

An Overview

Katie Hoover

The Department of the Interior’s (DOI’s) Payments in Lieu of Taxes (PILT; 31 U.S.C.

Specialist in Natural

§§6901-6907) program provides compensation for certain tax-exempt federal lands,

Resources Policy

known as entitlement lands. PILT payments are made annually to units of general local government

government—typically counties—that contain entitlement lands. Although PILT is only one of several federal programs that —typically counties—that contain entitlement lands. PILT was first enacted in 1976 () and later recodified in 1982 (P.L. 97-258). PILT is administered by the Office of the Secretary in the Department of the Interior (DOI), which is responsible for the calculation and disbursement of payments. PILT has most commonly been funded through annual discretionary appropriations, though Congress has authorized mandatory funding for PILT in certain years, which has replaced or supplemented discretionary appropriations. Since the start of the program in the late 1970s, PILT payments have totaled approximately $9.2 billion (in current dollars). From FY2015 through FY2019, authorized PILT payments averaged $489 million each year and appropriations for PILT payments averaged $485 million each year.

Although several federal programs exist to compensate counties and other local exist to compensate counties and other local

jurisdictions for the presence of federal lands within their boundaries, PILT applies to the broadest array of land types. PILT entitlement landstypes. Entitlement lands under PILT include lands administered by the Bureau of Land Management, the National Park Service, the U.S. Fish and Wildlife Service, all in the DOI; lands administered by the U.S. Forest Service in the Department of Agriculture; federal water projects; some military installations; and selected other lands. Nearly 2,000 counties and other local units of government received an annual PILT payment in FY2019.

In FY2022, DOI distributed $549.4 million in PILT payments to more than 1,900 counties across 49 states, the District of Columbia, Guam, Puerto Rico, and the Virgin Islands.

PILT comprises three separate payment mechanisms, which are named after the sections of law in which they are authorized: Section 6902 (31 U.S.C. §6902), Section 6904 (31 U.S.C. §6904), and Section 6905 (31 U.S.C. §6905). Section 6902 payments are the broadest of the three. They payment mechanisms; they account for nearly all of the funding disbursed under the PILT program and are made to all but a fewmost of the counties receiving PILT funding. In contrast, Section 6904 and Section 6905 payments are provided only under selected circumstances, account for a small fraction of PILT payments, and are made to a minority of counties (most of which also receive Section 6902 payments). In addition, whereas Section 6902 payments are provided each year based on the presence of entitlement lands, most payments under Section 6904 and Section 6905 are provided only for a short duration after certain land acquisitions.

Section 6902 payments are determined based on a multipart formula (31 U.S.C. §6903). Payments are calculated according to several factors, including (1) the number of acres of entitlement acresland present within a localthe unit of local government’s jurisdiction; (2) a per-acre calculation determined by one of two alternatives (Alternative A, also called the standard rate, or Alternative B, also called the minimum provision); (3) a population-based maximum payment (ceiling); (4) selected prior-year payments made to the counties pursuant to certain other federal compensation programs; and (5) the amount appropriated to cover the payments. Section 6904 and Section 6905 payments are provided to counties after the federal acquisition of specific types of entitlement lands (Section 6904) or entitlement lands located in specific areas (Section 6905) and are based on the fair market value of the acquisitions. If the appropriated amount is insufficient to cover the total payment amounts authorized in Sections 6902, 6904, and 6905, payments are prorated in proportion to the authorized rate. Annual discretionary appropriations bills generally also have included additional provisions dictating the terms of payments.

Before FY2008, PILT was funded through the annual discretionary appropriations process. In some of those years, the appropriation was less than the authorized full funding level, so each county received a prorated payment in those years. Since FY2008, however, PILT has been funded entirely through mandatory appropriations for all years except three (FY2015, FY2016, and FY2017), including the FY2023 payment set to be made around June 2023. In FY2015, PILT was funded through both mandatory and discretionary funding. In FY2016 and FY2017, PILT was funded entirely through discretionary appropriations.

PILT is of perennial interest to many Members of Congress and stakeholders throughout the country, and many local governments consider PILT payments to be an integral part of their annual budgets. In contemplating the future of PILT, Congress may consider topics and legislation related to the eligibility of various federal lands for entitlement under PILT (such as Indian lands or other lands currently excluded from compensation), amendments to the formula for calculating payments (especially under Section 6902), and issues related to funding PILT, among other matters.

Introduction to the Payments in Lieu of Taxes (PILT) Program

The

Congressional Research Service

link to page 4 link to page 6 link to page 9 link to page 9 link to page 10 link to page 15 link to page 15 link to page 16 link to page 16 link to page 8 link to page 11 link to page 13 link to page 13 link to page 7 link to page 18 The Payments in Lieu of Taxes (PILT) Program: An Overview

Contents

Payments in Lieu of Taxes (PILT) Introduction .............................................................................. 1 PILT Authorizations and Appropriations ......................................................................................... 3 PILT Payments Under Section 6902 ................................................................................................ 6

Entitlement Lands ..................................................................................................................... 6 Calculating Section 6902 Payments .......................................................................................... 7

PILT Payments Under Sections 6904 and 6905 ............................................................................ 12

Section 6904 Payments ........................................................................................................... 12 Section 6905 Payments ........................................................................................................... 13

Issues for Congress ........................................................................................................................ 13

Figures Figure 1. PILT Authorizations and Appropriations, FY1993-FY2022 ............................................ 5 Figure 2. Steps in Calculating PILT Section 6902 Payments (FY2022 Rates) ............................... 8 Figure 3. PILT Population-Based Ceiling Calculation .................................................................. 10 Figure 4. FY2022 PILT Population-Based Ceilings ...................................................................... 10

Tables Table 1. PILT Appropriations and Funding, FY2005-FY2023 ........................................................ 4

Contacts Author Information ........................................................................................................................ 15

Congressional Research Service

The Payments in Lieu of Taxes (PILT) Program: An Overview

Payments in Lieu of Taxes (PILT) Introduction The Department of the Interior’s (DOI’s) Payments in Lieu of Taxes (PILT) program provides compensation for certain entitlement lands that are exempt from state and local taxes.1 These lands include selected federal lands administered by the Bureau of Land Management, the National Park Service, and the U.S. Fish and Wildlife Service, all in the Department of the Interior (DOI)DOI; lands administered by the U.S. Forest Service in the Department of Agriculture; federal water projects; dredge disposal areas; and some military installations.12 Enacted in 1976,23 PILT is the broadest—in terms of federal land types covered—of several federal programs enacted to provide compensation to state or local governments for the presence of tax-exempt federal lands within their jurisdictions.3

4

PILT was enacted in response to a shift in federal policy from one that prioritized disposal of federal lands—one in which federal ownership was considered to be temporary—to one that prioritized retention of federal lands, in perpetuity, for public benefit.45 This shift began in the late 19th19th century and continued into the 20th20th century. Along with this shift came the understanding that, because these lands were exempt from state and local taxation and were no longer likely to return to the tax base in the foreseeable future, some compensation should be provided to the impacted local governments. Following several decades of commissions, studies, and proposed legislation, Congress passed PILT to at least partially ameliorate this hardship.56 PILT payments generally can be used for "“any governmental purpose,"6”7 which couldmay include assisting local governments with paying for local services, such as "“firefighting and police protection, construction of public schools and roads, and search-and-rescue operations."7

”8

1 The Department of Energy also implements a separate Payments in Lieu of Taxes (PILT) program, as authorized by the Atomic Energy Act of 1954 (P.L. 83-703, 42 U.S.C. §2208), not discussed in this report. This report also does not discuss the payments made to PILT counties through the Local Assistance and Tribal Consistency Fund (LATCF), established in the American Rescue Plan (P.L. 117-2, Sec. 9901). Receiving PILT payments was one factor for determining eligibility to receive a payment through the LATCF. Under the LATCF, eligible counties received $750 million in FY2022 and FY2023. In addition, certain eligible consolidated local governments are to receive $10.5 million in FY2023 and FY2024. For more information, see the Department of Treasury’s LATCF website at https://home.treasury.gov/policy-issues/coronavirus/assistance-for-state-local-and-tribal-governments/local-assistance-and-tribal-consistency-fund.

2 31 U.S.C. §§6901-6907. PILT implementing regulations are provided at 43 C.F.R. Part 44. 3 PILT was originally enacted in 1976 through P.L. 94-565. In 1982, PILT was “revised, codified, and enacted” in Title 31 of the U.S. Code pursuant to Chapter 69 of P.L. 97-258. PILT has been amended multiple times.

4 Although PILT is the broadest of these compensatory programs, it is not the oldest, and PILT provides compensation for defined entitlement lands only (31 U.S.C. §6901(1)). Other programs may include additional lands as defined by those programs. Several of those programs may be partially offset in PILT through the consideration of prior-year payments. Those programs are listed at 31 U.S.C. §6903(a)(1).

5 For more information, see Public Land Law Review Commission, One Third of the Nation’s Land: A Report to the President and to the Congress, June 1970, pp. 235-241. This report was produced pursuant to P.L. 88-606.

6 For more information, see U.S. Congress, House Committee on Interior and Insular Affairs, Payments In Lieu of Taxes Act, report to accompany H.R. 9719, 94th Cong., 2nd sess., May 7, 1976, H.Rept. 94-1106; and U.S. Congress, Senate Committee on Interior and Insular Affairs, Providing for Payments to Local Governments Based upon the Amount of Certain Public Lands Within the Boundaries of Each Such Government, report to accompany H.R. 9719, 94th Cong., 2nd sess., September 20, 1976, S.Rept. 94-1262.

7 31 U.S.C. §6902(a), 31 U.S.C. §6904(b), and 31 U.S.C. §6905(a) and (b)(3). However, both §6904 and §6905 require that certain funds provided through these sections are made available to school districts and other local governmental units within the local jurisdiction.

8 For more information, see Department of the Interior (DOI), Fiscal Year 2022 Payments In Lieu of Taxes, National Summary, available at https://www.doi.gov/pilt (hereinafter, National Summary FY2022).

Congressional Research Service

1

link to page 9 link to page 9 The Payments in Lieu of Taxes (PILT) Program: An Overview

The Office of the Secretary in DOI is responsible for the calculation and disbursement of payments under PILT.89 Payments under PILT are made annually to units of general local governmentgovernment—typically counties, though other types of governmental units also may be used (hereinafter, counties refers to units of general local government)—containing entitlement lands. PILT comprises three separate payment mechanisms: Section 6902, Section 6904, and Section 6905 payments, all named for the sections of law in which they are authorized.910 Section 6902 payments account for nearly all payments made through PILT. The Section 6902 authorized payment amount for each county is calculated according to a statutory formula that is subject to a maximum payment based on the county'’s population (see "“PILT Payments Under Section 6902").106902”).11 The remaining payments are provided through Section 6904 and Section 6905 under selected circumstances and typically are limited in duration. Through FY2019FY2022, PILT payments have totaled approximately $10.8 billion.12

have totaled approximately $9.2 billion (in current dollars).11

Members of Congress routinely consider amending PILT within both appropriations and authorizing legislation. For example, legislation in the 116th Congress would amend how PILT appropriations are provided and would change how payments are calculated under Section 6902.12 In addition, Members of Congress may address issues related to which federal lands should be eligible for payments under PILT.

This report provides an overview of the PILT payment program and includes sections on

PILT' PILT’s authorization and appropriations, which discusses the history of how Congress has provided funding for PILT;-

Section 6902 payments, which includes a breakdown of how Section 6902

payments are calculated;

- Section 6904 and Section 6905 payments, which outlines what situations result in payments under these mechanisms; and

-

issues for Congress, which discusses several topics that have been or may be of

interest to Members of Congress when considering the

future of PILT.

PILT program. Selected Terms Used in This Report

Authorized payment: the amount a county is eligible to receive based on the formula/requirements specified in statute, prior to any reductions for administrative costs or due to insufficient appropriations. Entitlement lands: statutorily defined federally owned lands that are exempt from state and local taxes and are eligible to be the basis for determining a county Full statutory calculation: the sum of authorized payments under Section 6902, Section 6904, and Section 6905 for all counties in a given year. Inflation: used here to refer to the statutorily required annual adjustment to the per-acre payment rates and the population payment rate. The adjustment is made to reflect changes in the Consumer Price Index published by the Bureau of Labor Statistics of the Department of Labor for the previous 12 months ending June 30. This provision is required pursuant to 31 U.S.C. §6903(d). Per-acre payment Population-based ceiling: the maximum payment a county is eligible to receive under Section 6902. This figure is calculated by multiplying the county

Prior-year payments: payments received by a county for federally owned lands in its jurisdiction through certain federal compensation programs other than PILT. These programs refer to one of the Prorated payment: the actual payment received by a county when appropriated funds are insufficient to cover the authorized payments. The prorated payment is determined by the amount appropriated for PILT that is available to cover payments and is proportional to the authorized payment for each county. Unit of general local government (hereinafter, referred to as county): jurisdictional entity eligible to receive payments under PILT. These entities are most often counties but may include other jurisdictional units such as parishes, boroughs, census areas, the District of Columbia, Guam, Puerto Rico, and the Virgin Islands. This term is defined in statute at 31 U.S.C. §6901(2).

|

PILT Authorizations and Appropriations

Congress has funded PILT through both discretionary and mandatory appropriations at various times since the program was first authorized. Some stakeholders and policymakers have routinely expressed concern about changes in the appropriations source, authority, including both the process of switching between mandatory and discretionary appropriations and the uncertainty that may accompany such changes.

From 1982 to 2008, Section 6906 provided an "“Authorization of Appropriations"” for PILT, which stated, "Necessarystated that “necessary amounts may be appropriated to the Secretary of the Interior to carry out [PILT]."13”13 Further, it clarified that "“amounts are available only as provided in appropriation laws."14”14 Congress amended this language in 2008 and changed the section title from "“Authorization of Appropriations"” to "“Funding."15”15 Further, Congress changed the text to read

For each of fiscal years 2008 through 2012-

(1) each county or other eligible unit of local government shall be entitled to payment under this chapter; and

(2) sums shall be made available to the Secretary of the Interior for obligation or this chapter; and

(2) sums shall be made available to the Secretary of the Interior for obligation or expenditure in accordance with this chapter.16

16

This amendment effectively changed PILT funding from being discretionary to being mandatory for the years specified (seesee Table 1 for PILT funding since FY2005). Since 2008, Congress has amended Section 6906 several times by changing the fiscal year in the first line through both annual discretionary appropriations laws and other legislative vehiclesvehicles (Table 1).

Table 1. PILT Appropriations and Funding, FY2005-FY2020

.

13 31 U.S.C. §6906, prior to the enactment of P.L. 110-343. Between 1976 and 1982, the authorization of appropriations from PILT was codified at 31 U.S.C. §1607 and read, “There are authorized to be appropriated for carrying out the provisions of this Act such sums as may be necessary: Provided, That, notwithstanding any other provision of this Act no funds may be made available except to the extent provided in advance in appropriations.” P.L. 94-565, §7.

14 31 U.S.C. §6906, prior to the enactment of P.L. 110-343. 15 P.L. 110-343, Div. C, Title VI, §601(c)(1). 16 P.L. 110-343, Div. C, Title VI, §601(c)(1).

Congressional Research Service

3

link to page 7 link to page 7 link to page 7 link to page 7 link to page 7 link to page 7 link to page 7 link to page 7 link to page 7 link to page 7 link to page 7 link to page 8 link to page 8 The Payments in Lieu of Taxes (PILT) Program: An Overview

Table 1. PILT Appropriations and Funding, FY2005-FY2023

(nominal dollars)

Total

Total

Authorized

Appropriated

Fiscal

Amount

Amount

%

Year

Statute

Funding Type

(millions)

(millions)

Appropriateda

FY2005

P.L. 108-447 Discretionary

$332.0

$226.8

68.3%

FY2006

P.L. 109-54

Discretionary

$344.4

$232.5

67.5%

FY2007

P.L. 110-5

Discretionary

$358.3

$232.5

64.9%

FY2008-

P.L. 110-343 Mandatory

Set in PILT

Set in PILT

100%

FY2012

formula

formula

FY2013

P.L. 112-141 Mandatory

$421.7

$400.2

94.9%b

FY2014

P.L. 113-79

Mandatory

$437.3

$437.3

100%

FY2015

P.L. 113-235 Discretionary ($372.0 mil ion)

$451.5

$439.5

97.3%c

P.L. 113-291 Mandatory ($33.0 mil ion and

—

—

—

$34.5 mil ion)c

FY2016

P.L. 114-113 Discretionary

$459.5

$452.0

98.4%

FY2017

P.L. 115-31

Discretionary

$465.9

$465.0

99.8%

FY2018

P.L. 115-141 Mandatoryd

$553.2

$553.2

100%

FY2019

P.L. 116-6

Mandatoryd

$515.1

$515.1

100%

FY2020

P.L. 116-94

Mandatoryd

$514.8

$514.8

100%

FY2021

P.L. 116-260

Mandatoryd

$529.6

$529.7e

100%

FY2022

P.L. 117-103

Mandatoryd

$549.8

$549.8

100%

FY2023

P.L. 117-328

Mandatoryd

TBDf

TBDf

100%

(nominal dollars)

|

Fiscal Year |

Statute |

Funding Type |

Total Authorized Amount (millions) |

Total Appropriated Amount (millions) |

| ||||||

|

FY2005 |

Discretionary |

|

|

| |||||||

|

FY2006 |

Discretionary |

|

|

| |||||||

|

FY2007 |

Discretionary |

|

|

| |||||||

|

FY2008-FY2012 |

Mandatory |

|

|

100% |

|||||||

|

FY2013 |

Mandatory |

|

|

| |||||||

|

FY2014 |

Mandatory |

|

|

100% |

|||||||

|

FY2015 |

Discretionary ($372.0 million) |

|

|

| |||||||

|

|

|

| ||||||||

|

FY2016 |

Discretionary |

|

|

| |||||||

|

FY2017 |

Discretionary |

|

|

| |||||||

|

FY2018 |

|

|

|

100% |

|||||||

|

FY2019 |

|

|

|

100% |

|||||||

|

FY2020 |

|

|

|

100% |

Source: CRS, with data from listed public laws and relevant annual reports, available at https://www.doi.gov/pilt/resources/annual-reports.

. Notes: Appropriated amounts may include rescissions as provided in relevant statutes.

a. Figures are presented in nominal dol ars, though note that the PILT payment formula incorporates an annual inflation adjustment. a. This column represents the percentage of the authorized amount that was appropriated for a given year.

Even for years in which 100% of the authorized amount was appropriated, counties may have received a prorated payment due to part of the appropriation being set aside for uses other than payments (e.g., for administration).

b.

b. PILT appropriations in FY2013 were impacted by sequestration pursuant to the Balanced Budget and

Emergency Deficit Control Act (2 U.S.C. §§900 et seq.), as amended by the Budget Control Act of 2011 ((P.L. 112-25).

c. ).

c. For FY2015 PILT payments, Congress provided $70 millionmil ion in mandatory appropriations (P.L. 113-291). This

appropriation was split, with $33 millionmil ion to be provided in FY2015 and $37 millionmil ion to be available in October 2015, which, while paid in FY2016, was for FY2015 payments. Of the $70 millionmil ion in mandatory appropriations, the $37 millionmil ion available in October 2015 (FY2016) was subject to sequestration, which reduced the appropriated amount to $34.5 million.

d. For FY2018, FY2019, and FY2020mil ion.

d. For FY2018 through FY2023, PILT funding was provided by amending 31 U.S.C. §6906 ("Funding"“Funding”) each

fiscal year. As a result, the funding for PILT was treated as mandatory spending in these years. These amendments required funding for PILT for each of these years to be provided at the amount of the full ful statutory calculation.

e.

e. Appropriations for FY2021 included additional funds ($43,751) for adjustments to errors in prior year

payments.

Congressional Research Service

4

link to page 7 link to page 7 link to page 8

The Payments in Lieu of Taxes (PILT) Program: An Overview

f.

Although appropriations for PILT payments were enacted at the full ful statutory level pursuant to Section 115 114 of Title 1 of Division DG in P.L. 116-94117-328, the exact amount that will wil be appropriated will wil not be known until it is calculated by the DOI in FY2020.

DOI issues the FY2023 payments and reports.

PILT was funded through discretionary appropriations from its enactment through FY2007. Since FY2008, Congress has provided funding for PILT through both discretionary and mandatory appropriationsappropriations (Table 1). From FY2008 through FY2014, Congress authorized mandatory funding for PILT through several laws.17 Since FY2015, funding has been provided, at least partially, through the annual appropriations process. In FY2015, PILT received both discretionary and mandatory appropriations.18 For FY2016 through FY2020FY2023, Congress funded PILT through the annual appropriations process. In bills, though the funding was considered mandatory in some years. In FY2016 and FY2017, the appropriations laws provided specific funding levels for PILT, which was treated as discretionary spending.19 In FY2018, FY2019, and FY2020 From FY2018 through FY2023, the appropriations laws provided funding for PILT by amending the authority provided in 31 U.S.C. §6906, which was treated as mandatory spending.20 In each of these three years, the years PILT received mandatory appropriations, funding was provided for PILT at the full statutory calculation levels.

Since FY2008, Congress has provided funding for PILT through both one-year and multiyear appropriations. Congress'’s actions have resulted in full funding and partial funding in different years (Table 1 and Figure 1). These types of changes from year to year may have implications for counties that rely on PILT funding as part of their annual budgets.

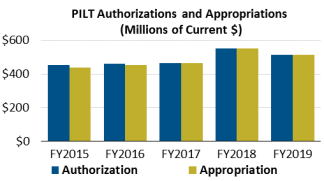

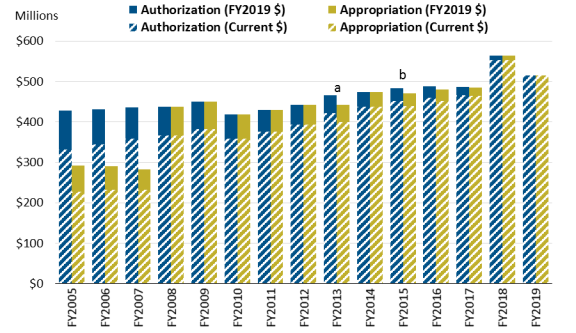

Figure 1. PILT Authorizations and Appropriations, FY1993-FY2022

(in current and inflation-adjusted |

|

Source: CRS, with data from PILT National Summaries,

|

).

In addition to appropriating funding for the program, Congress routinelyregularly provides other guidance on PILT withinto DOI on implementing PILT through the annual appropriations process, such as minimum payment thresholds, set-asides for program administration, and provisions for prorating payments.21

Congressional Research Service

5

link to page 8 The Payments in Lieu of Taxes (PILT) Program: An Overview

payments.17 When appropriated funding is insufficient to cover the full amount forof authorized payments under Sections 6902, 6904, and 6905, counties typically receive a proportional payment known as a prorated payment (Figure 1 shows the disparity between the authorized amount and the appropriated amount in recentcertain years). Even in years in which appropriations are set equal to 100% of the full statutory calculation, payments to counties may be prorated if funding is set aside for purposes other than payments, such as administration.

PILT Payments Under Section 6902

Section 6902 payments are provided to units of local government jurisdictions (referred to as counties in this report)counties across the United States to compensate for the presence of entitlement lands within their boundaries. Section 6902 payments also are provided to states, the District of Columbia, Guam, Puerto Rico, and the Virgin Islands.2218 Section 6902 payments account for nearly all of the payments made under PILT. In FY2019FY2022, 99.8589% of all PILT payments were made through Section 6902.2319 Further, more counties are eligible for Section 6902 payments than either Section 6904 or Section 6905 payments. In FY2019, FY2022, 1,936 of the 1,9401,931 counties that received PILT payments, 1,927 received payments under received Section 6902 payments, and 128, and 134 received payments under Section 6904 and/or Section 6905 (130four counties received payments under both Section 6902 and Section 6904 and/or Section 6905).24

but did not receive Section 6902 payments).20 Entitlement Lands

There are nine categories of federal lands identified as entitlement lands in the PILT statute.25

1.21 1. Lands in the National Park System2.(administered by the National Park Service, in DOI) 2. Lands in the National Forest System3.(administered by the U.S. Forest Service, in the U.S. Department of Agriculture (USDA)) 3. Lands administered by the Bureau of Land Management (BLM)4.4. Lands in the National Wildlife Refuge System (NWRS) that are withdrawn from the public domain5.(administered by the U.S. Fish and Wildlife Service, in DOI) 5. Lands dedicated to the use of federal water resources developmentprojects266.projects22 6. Dredge disposal areas under the jurisdiction of the U.S. Army Corps of Engineers7.7. Lands located in the vicinity of Purgatory River Canyon and Piñon Canyon, CO, that were acquired after December 31, 1981, to expand the Fort Carson militaryreservation8.reservation 17 For example, in FY2020, provisions were included in Title I of Division D in P.L. 116-94 that specified that no payment is to be made if the authorized payment is less than $100; to authorize DOI to retain up to $400,000 from the authorized payment for administrative expenses; to allow for payments to be reduced proportionally if the appropriated amount is insufficient; and to correct for prior over- or underpayments. Although similar provisions have routinely been included in appropriations acts, the specific text of these provisions has varied. 18 31 U.S.C. §6901(2). 19 National Summary FY2022, p. 8. 20 National Summary FY2022, Schedule 1. The four counties that received FY2022 PILT payments under §6904 and/or §6905 but did not receive §6902 payments: Berkshire County, MA; Beaufort County, SC; Hancock County, ME; and Rutland County, VT. 21 31 U.S.C. §6901(1). 22 Most of these lands are under the jurisdiction of the Bureau of Reclamation. Congressional Research Service 6 link to page 11 The Payments in Lieu of Taxes (PILT) Program: An Overview 8. Lands on which are located semi-active or inactive Army installations used forLands on which are located semi-active or inactive Army installations used formobilization and for reserve component training9.9. Certain lands acquired by DOI or theDepartment of AgricultureUSDA under the Southern Nevada Public Land Management Act (P.L. 105-263)

)

Of these categories, the first three (National Park System, National Forest System, and lands administered by BLM) largely account for all of the lands managed by the relevant administering agencies. The remaining categories are either lands tied to specific laws or actions (categories 7 and 9, above) or lands that represent a subset of the lands administered by a particular agency. For example, entitlement lands that are included within the NWRS (category 4) only account for lands within the system that have been withdrawn from the public domain, which excludes lands that have been purchased as additions to the NWRS.2723 Further, lands administered by the U.S. Fish and Wildlife Service that are not included in the NWRS are not included within the definition of entitlement lands. Similarly, lands in the other categories (5, 6, and 8, above) may not include all, or even the majority of, lands administered by particular agencies or departments.

Calculating Section 6902 Payments

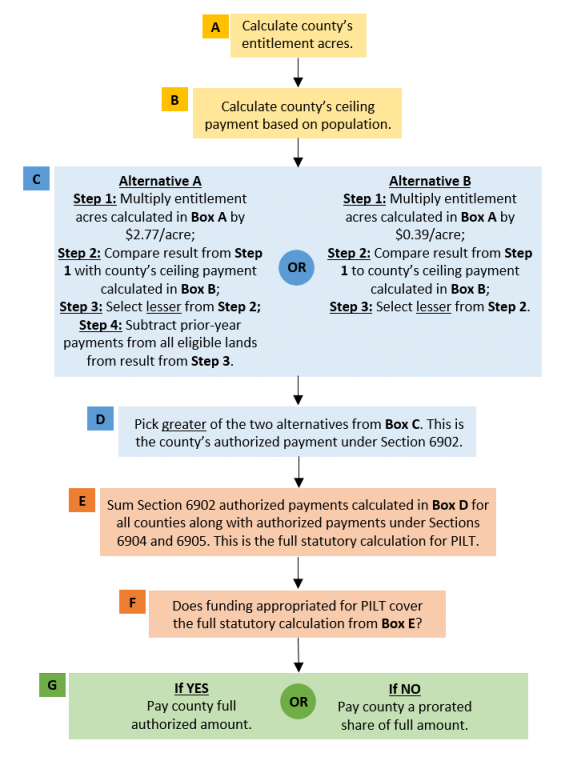

Section 6902 payments are determined based on a multipart formula (seesee Figure 2). The DOI Office of the Secretary calculates PILT payments according to several factors, including

-

the number of entitlement acres;

- a per-acre calculation determined by one of two alternatives (Alternative A, also

called the standard rate, or Alternative B, also called the minimum provision);

-

a population-based maximum payment (ceiling);

- certain prior-year payments pursuant to other compensation programs; and

- the amount available to cover PILT payments.

To calculate a particular county'’s PILT payment, the DOI Office of the Secretary first must collect data from several federal agencies and the county'’s state to answer the following questions:

- How many acres of eligible lands are in the county?

- What is the population of the county?

- What was the increase in the Consumer Price Index for the 12 months ending the preceding June 30?

-

What were the prior year

'’s payments, if any,forto the county under the other payment programs of federal agencies?28 Does the state have any laws requiring the payments from24 Do any state laws require payments under other federal landpaymentcompensation lawslawsto be passed through to other local government entities, such as school districts, rather than stay with the county government?

|

|

https://www.doi.gov/pilt. Note: For more information on Box B (ceiling payments), |

The first step in calculating a county'’s Section 6902 payment is to determine the number of entitlement acres within the county (Figure 2, Box A).29

The acreage figures are reported to DOI by the various federal agencies that administer the entitlement lands.

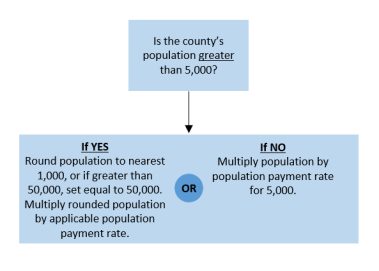

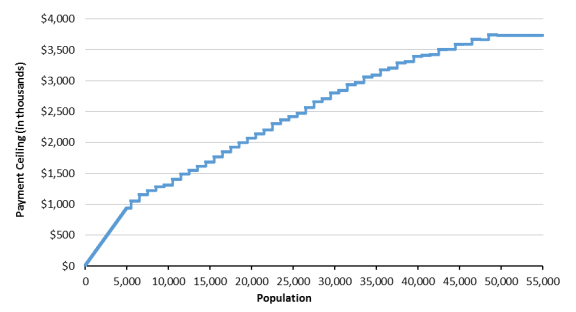

The next step is to calculate the population-based ceiling by multiplying the county'’s population by the population payment rate (Figure 2, Box B). County population data are provided by the U.S. Census Bureau. The population number for this calculation differs based on the county’s population level (Figure 3):

Congressional Research Service

8

link to page 13 The Payments in Lieu of Taxes (PILT) Program: An Overview

U.S. Census Bureau. For this calculation, counties with different populations are treated differently (Figure 3):

- For counties with populations

smallerfewer than 5,000,athe county'’s actual population is used in the calculation. - .

For counties with populations

largerequal to or greater than 5,000,athe county's’s population is rounded to the nearest 1,000, and this rounded population is used in the calculation. -

All counties with populations greater than 50,000, regardless of their actual

populations, are considered to have a population equal to 50,000 for the purposes of calculating the ceiling.

The population payment rate is adjusted annually for inflation based on the change in the Consumer Price Index for the 12 months ending on the preceding June 30.25

of calculating the ceiling.

The population payment rate generally declines as population increases in 1,000 -person increments (per statute), although the population-based ceiling generally increases (Figure 4).3026 However, this is not always the case. For example, in FY2019FY2022, payment rates for several populations arewere the same despite increasing populations, such as the rates for populations of 26,000; 27,000; and 28,000, which are all $94.98. Further, some100.72. For FY2022, the population payment rates ranged from $197.84 per person for counties with populations of less than 5,000 to $79.14 per person for counties with populations of 50,000 or greater.27

Some payment ceilings do not increase with increasing populations. For example, counties with populations of 50,000 have a lower ceiling than those with populations of 49,000 (49,000 × $76.33 = $3,740,170FY2022 payment rate of $80.95 = $3,966,550; and 50,000 × $74.63 = $3,731,500, or $8,670FY2022 payment rate of $79.14 = $3,957,000, or $9,550 less for the more populous county).

25 31 U.S.C. §6903(d). 26 Even though the population payment rate declines as county population size increases, payment ceilings generally are higher for counties with larger populations. For example, in FY2022, the population payment rate for a population of 5,000 was $197.84 and the rate for a population of 6,000 was $185.28, a decrease of $12.56 in the rate for the more populous county. When multiplied by the population, however, the ceiling is higher for the county with the larger population: 5,000 × $197.84 = $989,200, versus 6,000 × $185.28 = $1,111,680, or $122,480 more for the more populous county.

27 The per capita payment rates are included in the PILT national summary each year. For example, the National Summary FY2022, p. 14, includes the payment rates for FY2022.

Congressional Research Service

9

link to page 11

The Payments in Lieu of Taxes (PILT) Program: An Overview

Figure 3. PILT Population-Based Ceiling Calculation

less for the more populous county).

The population payment rate is adjusted annually for inflation based on the change in the Consumer Price Index for the 12 months ending on the preceding June 30.31 For FY2019, the population payment rates ranged from $186.56 per person for counties with populations of 5,000 or fewer to $74.63 per person for counties with populations of 50,000 or greater.32

|

|

|

Source: CRS, with information from 16 U.S.C. §6903. |

|

|

Source: CRS, with data from Department of the Interior, Fiscal Year Notes: Ceiling calculations for counties with populations greater than 5,000 are based on the county |

The next step is to calculate the payment level under alternativesAlternatives A and B (Figure 2, BoxBox C). Alternative A has a higher per-acre payment rate than Alternative B, but Alternative A is subject to a deduction for prior-year payments. Prior-For FY2022, the per-acre payment rates were $2.94 per acre of entitlement land for Alternative A and $0.42 per acre of entitlement land for Alternative B.

Congressional Research Service

10

link to page 11 link to page 15 link to page 11 link to page 11 link to page 6 The Payments in Lieu of Taxes (PILT) Program: An Overview

For calculations under Alternative A, DOI deducts certain prior-year payments. Qualifying prior-year payments are those payments from the federal payment programs listed in statute:33

- 28 the Act of June 20, 1910 (ch. 310, 36 Stat. 557);

- Section 33 of the Bankhead-Jones Farm Tenant Act (7 U.S.C. §1012);

- the Act of May 23, 1908 (16 U.S.C. §500), or the Secure Rural Schools and Community Self-Determination Act of 2000 (16 U.S.C. §§7101 et seq.);

- 29

Section 5 of the Act of June 22, 1948 (16 U.S.C. §§577g

-577g–1); - –577g-1); Section 401(c)(2) of the Act of June 15, 1935 (16 U.S.C. §715s(c)(2));

- Section 17 of the Federal Power Act (16 U.S.C. §810);

- Section 35 of the Act of February 25, 1920 (30 U.S.C. §191);

- Section 6 of the Mineral Leasing Act for Acquired Lands (30 U.S.C. §355);

- Section 3 of the Act of July 31, 1947 (30 U.S.C. §603); and

- Section 10 of the Act of June 28, 1934 (known as the Taylor Grazing Act) (43 U.S.C. §315i).

However, if a state has a pass--through law that requires some or all of these prior-year payments to be paid directly to a sub-county recipient (e.g., a school district), the amount passed through from these payments areis not deducted from subsequent PILT payments in the following year.30

As noted, Alternative B is calculated without deducting prior-year payments, but it uses a lower per-acre payment rate.

Once each alternative is calculated, the greater of the two is the Section 6902 authorized payment for the county (Figure 2, Box D). However, if the per-acre calculated Section 6902 authorized payment is greater than the population-based ceiling, then the population-based ceiling replaces the per-acre calculated amount.31

not deducted from subsequent PILT payments in the following year.34

Alternative B is calculated using a lower per-acre payment rate, but prior-year payments are not deducted. For FY2019, the per-acre payment rates were $2.77 per acre of entitlement land for Alternative A and $0.39 per acre of entitlement land for Alternative B. If the per-acre payment (number of acres multiplied by the per-acre payment rate) calculated under either alternative is greater than the population-based ceiling, then the population-based ceiling replaces the calculated amount.35

Once each alternative is calculated, the greater of the two is the Section 6902 authorized payment for the county (Figure 2, Box D).

The Section 6902 authorized payments are calculated for every county, and this amount is added to the Section 6904 and Section 6905 authorized payments (for more information on Sections 6904 and 6905, see "“PILT Payments Under Sections 6904 and 6905”"). This summed amount is the full statutory calculation for a given fiscal year (Figure 2, BoxBox E). DOI compares the full statutory calculation with the amount appropriated and available for PILT payments to determine whether Congress has provided adequate funding to cover the full statutory calculationcalculation (Figure 2, Box F).3632 If sufficient funding is available, each county receives its authorized amount;37 if 33 if

28 31 U.S.C. §6903(a)(1). 29 For more information, see CRS Report R41303, The Secure Rural Schools and Community Self-Determination Act: Background and Issues.

30 National Summary FY2022, p. 10. According to DOI

Only the amount of Federal land payments actually received by units of government in the prior fiscal year is deducted. If a unit receives a Federal land payment but is required by State law to pass all or part of it to financially and politically independent school districts, or to any other single or special purpose district, payments are considered to have not been received by the unit of local government and are not deducted from the Section 6902 payment.

31 If the population-based ceiling replaces the per-acre calculation under Alternative A, prior-year payments are then deducted from the population-based ceiling to determine the final amount for Alternative A.

32 Congress provides funding for PILT through either discretionary or mandatory appropriations, or both, in any given year. See “PILT Authorizations and Appropriations” for more information. 33 Payments may be subject to any additional provisions included in appropriations language, such as minimum

Congressional Research Service

11

link to page 11

The Payments in Lieu of Taxes (PILT) Program: An Overview

funding is insufficient, each county receives a prorated payment that is proportional to its authorized payment (Figure 2, BoxBox G).34

G).38

The full statutory calculation and the amount available for PILT payments determine proration. Although there are additional adjustments made in the PILT proration calculation resulting from small idiosyncrasies related to the requirements for PILT payments—namely, the requirement of a minimum threshold of $100 for PILT payments39payments35—the proration is fundamentally the ratio of the appropriated funding available for PILT payments to the full statutory calculation:

As a result, counties may receive less than their authorized PILT payment in years when appropriated funding is insufficient to cover the full statutory calculation. This scenario can occur even when total PILT appropriations match the full statutory calculation; this has been the case in years with mandatory appropriations, when part of the appropriated amount is set aside for a use other than county payments.40 For example, laws providing appropriations for PILT routinely have allowed DOI to retain a small portion of PILT appropriations for administrative expenses.

36 PILT Payments Under Sections 6904 and 6905

Section 6904 and Section 6905 payments account for a small fraction of total PILT payments.41 In FY201937 In FY2022, these payments were made to 134128 counties and accounted for 0.1511% of PILT payments ($629,856 of $549.4($750,605 of $514.7 million in total payments made).42 Once38 When a county receives Section 6904 andand/or Section 6905 payments, it is to disburse paymentsthe funds to governmental units and school districts within the county in proportion to the amount of property taxes lost because of the federal ownership of the entitled lands, as enumerated under these sections.43 County units and school districts may use these payments39 The funds may be used for any governmental purpose.

Section 6904 Payments

Section 6904 authorizes the Secretary of the Interior to make payments to counties that contain certain lands, or interests in lands, that are part of the National Park System and National Forest Wilderness Areas.44

payment thresholds or adjustments for under- or overpayments in previous years. PILT provisions in appropriations laws generally have required a minimum payment threshold of $100. For example, the FY2022 appropriations act included a $100 minimum payment clause (P.L. 117-103, Division G, Title I). In FY2022, less than 200 counties had an authorized payment of less than $100; these counties did not receive payments, per the FY2022 appropriations act.

34 The provision for a prorated payment is not included in the PILT statutory language (31 U.S.C. §§6901-6907), but it has been included in certain appropriations laws for PILT.

35 The requirement of a minimum threshold of $100 for PILT payments is routinely included in appropriations language related to PILT (e.g., for FY2022, Title I of Division G in P.L. 117-103) and also is in regulation (43 C.F.R. §44.51).

36 For example, DOI is allowed to retain up to $400,000 of the appropriations for PILT for administrative expenses in FY2023 (Title I of Division G in P.L. 117-328).

37 31 U.S.C. §§6904 and 6905. 38 National Summary FY2022, p. 8. This source reports §6904 and §6905 payments together, and further disaggregation is not possible from the information provided.

39 43 C.F.R. §44.50.

Congressional Research Service

12

link to page 6 link to page 6 The Payments in Lieu of Taxes (PILT) Program: An Overview

Wilderness Areas.40 However, Section 6904 specifies that these lands, or interests, are eligible only if (1) they have been acquired by the U.S. government for addition to these systems and (2) they were subject to local property taxes in the five-year period prior to this acquisition. 41 Payment under Section 6904 is calculated as 1% of the fair market value of the land at the time it was acquired, not to exceed the amount of property taxes levied on the property during the fiscal year prior to its acquisition.42 Further, Section 6904 payments are made annually only for the five fiscal years after the land, or interest, is acquired by the U.S. government, unless otherwise mandated by law.

Section 6905 Payments

Section 6905 authorizes the Secretary of the Interior to make payments to counties that contain lands, or interests in lands, that are part of the Redwood National Park and are owned by the U.S. government or that are acquired by the U.S. government in the Lake Tahoe Basin under the Act of December 23, 1980.4543 Section 6905 payments are paid at a rate of (1) 1% of the fair market value of the acquired land or interests or (2) the amount of taxes levied on the land in the year prior to acquisition, whichever is lesserless. Payments on these lands continue for five years or until payments have totaled 5% of the fair market value of the land.46

, whichever is later.44 Issues for Congress

PILT is of perennial interest to many in Congress and to stakeholders throughout the country. County governments are particularly interested in the degree of certainty of PILT payments, as well as in how payments are calculated, because many consider PILT payments to be an integral part of their annual budgets. Congressional and stakeholder interests include questions of how PILT should be funded, what lands should be included as entitlement lands, and how authorized payment levels are calculated under PILT, among others.

Congress annually addresses questions of how funding should be provided to PILT. Congress has funded PILT through both mandatory and discretionary appropriations (see "“PILT Authorizations and Appropriations"). More often than not,”). PILT funding typically has been provided through the discretionary appropriations process for one fiscal year at a time, even when the funding has been considered mandatory spending. Although PILT has consistently received funding since its enactment, the appropriations process has created uncertainty among some stakeholders about the level of annual funding. Stakeholders have expressed a desire for more certaintyfunding.47 Stakeholders also have asserted that greater certainty, in terms of both the guarantee of funding and the amount of funding (i.e., the full statutory calculation) would be better.48

.45

40 31 U.S.C. §6904. For more information on the National Park System, see CRS Report R41816, National Park System: What Do the Different Park Titles Signify?. For more information on wilderness areas, see CRS Report RL31447, Wilderness: Overview, Management, and Statistics.

41 31 U.S.C. §6904(a). 42 31 U.S.C. §6904(c). 43 31 U.S.C. §6905. The Act of December 23, 1980, is P.L. 96-586. 44 43 C.F.R. §44.40. Payments may extend beyond five years when taxes levied in the year prior to acquisition account for less than 1% of the fair market value of the acquired land. However, any portion of a payment not made because Congress did not appropriate sufficient funds is not deferred to later payments.

45 National Association of Counties (NACo), Provide Full Mandatory Funding for the Payments in Lieu of Taxes (PILT) Program, February 1, 2023, at https://www.naco.org/resources/provide-full-mandatory-funding-payments-lieu-taxes-pilt-program.

Congressional Research Service

13

link to page 9 The Payments in Lieu of Taxes (PILT) Program: An Overview

Members of Congress typically contemplate the implications and tradeoffs of discretionary versus mandatory spending and may have different views than the counties that receive PILT payments. Congress, for example, may weigh itsthe flexibility of having discretion to review and fund PILT on an annual basis through the appropriations process against the certainty of funding for specific activities that accompany mandatory appropriations.4946 Several bills have been introduced to amend how PILT is funded. For example, legislation has beenwas introduced in the 116th116th Congress that would requirehave required mandatory funding for PILT, either for for either a set period of time (e.g., 10 additional years) or indefinitely.50

47

The question of which lands should be eligible for PILT payments is also of interest to many Members and stakeholders. In law, entitlement lands are restricted to the listed federal land types (see "“Entitlement Lands")”). However, this definition does not fully encompass the types of lands that are held by the federal government, nor does it account for the full suite of lands that are exempt from state and local taxes. Although counties may receive compensation for some of these other lands may receive compensation through other federal programs, not all dofederal lands exempt from taxation are covered by a federal compensation program, which may cause financial hardships for counties that otherwise might receive revenue from that land through taxation. To address this concern, some Members of Congress have contemplated amending the definition of entitlement lands under PILT. For example, past Congresses have introduced legislation that would have amended PILT by expanding the definition of entitlement land to include

-

land

"“that is held in trust by the United States for the benefit of a federally recognized Indian tribe or an individual Indian";51 - ”;48

lands under the jurisdiction of the Department of the Defense, other than those

already included in PILT;

52 - 49

lands acquired by the federal government for addition to the National Wildlife

Refuge System;

53 and - 50 and

lands administered by the Department of Homeland Security,

5451 among others.

Amending the definition of entitlement lands could have several implications. Adding additional acres of entitlement lands could increase the authorized amount of payments under PILT for the counties in which those lands are located. Depending how the definition was amended, these additional entitlement lands may be eligible for compensation under other federal compensation programs. This could, in turn, further affect PILT payment calculations through the adjustment for prior-year payments deducted from Alternative A.

46 For more information, see CRS Report R44582, Overview of Funding Mechanisms in the Federal Budget Process, and Selected Examples.

47 For example, S. 2480 would have required mandatory PILT funding through FY2029, and H.R. 3043 would have required mandatory PILT funding indefinitely. Both bills were introduced in the 116th Congress.

48 For example, H.R. 7251 in the 110th Congress. 49 For example, H.R. 4710 in the 113th Congress. 50 For example, S. 2626 in the 113th Congress. 51 For example, H.R. 543 in the 112th Congress.

Congressional Research Service

14

The Payments in Lieu of Taxes (PILT) Program: An Overview

The authorized payment level under Section 6902, which accounts for nearly all payments under PILT, is calculated pursuant to the statutory requirements. This section has remained largely unchanged since the requirement to adjust for inflation was added in 1994, among other changes.52 The inflation adjustment clause has resulted in increasing payment and ceiling rates since that time.53 Congress routinely considers whether the current formula is the best means of calculating payments under PILT or whether the formula should be amended. For example, in the 116th Congress, bills were introduced that would have adjusted the payment structure for counties with a population of less than 5,000.54 This adjustment would have had implications for how the population ceiling or entitlement land acreage would be incorporated into calculating PILT payments and whether PILT payments were provided in an equitable manner. In the 117th Congress, bills were introduced that would have directed the Secretary to develop, study, and report on a modeling tool to calculate tax equivalency payments.55

In addition to the above issues, Congress may consider other issues related to PILT and how the program fits into the landscape of federal programs that compensate for the presence of tax-exempt federal lands.56

Author Information

Katie Hoover

Specialist in Natural Resources Policy

Acknowledgments

R. Eliot Crafton, who is no longer with CRS, wrote the original version of this report.

52 P.L. 103-397 amended 31 U.S.C. §6903 in several ways. Since then, §6903 has been amended once; P.L. 106-393 amended the definition of payment law at 31 U.S.C. §6903(a)(1)(C). That amendment added the Secure Rural Schools and Community Self-Determination Act of 2000 (16 U.S.C. §§7101 et seq.) to the list of payment laws, which are included in determining prior-year payments.

53 P.L. 103-397 added the requirement to adjust for inflation. 54 For example, S. 2108 and H.R. 3716 in the 116th Congress. 55 For example, S. 1008 and H.R. 2755 in the 117th Congress. 56 For more discussion on these issues, see CRS Report R42439, Compensating State and Local Governments for the Tax-Exempt Status of Federal Lands: What Is Fair and Consistent?.

Congressional Research Service

15

The Payments in Lieu of Taxes (PILT) Program: An Overview

Disclaimer

This document was prepared by the Congressional Research Service (CRS). CRS serves as nonpartisan shared staff to congressional committees and Members of Congress. It operates solely at the behest of and under the direction of Congress. Information in a CRS Report should not be relied upon for purposes other than public understanding of information that has been provided by CRS to Members of Congress in connection with CRS’s institutional role. CRS Reports, as a work of the United States Government, are not subject to copyright protection in the United States. Any CRS Report may be reproduced and distributed in its entirety without permission from CRS. However, as a CRS Report may include copyrighted images or material from a third party, you may need to obtain the permission of the copyright holder if you wish to copy or otherwise use copyrighted material.

Congressional Research Service

R46260 · VERSION 10 · UPDATED

16 entitlement lands could increase the authorized amount of payments under PILT, which likely would benefit those states with the added lands but not states that lack additional lands. This, in turn, could influence how Congress elects to fund PILT. Additional entitled lands may be eligible for other compensation programs, which could further affect PILT payments.

The authorized payment level under Section 6902, which accounts for nearly all payments under PILT, is calculated pursuant to the statutory requirements. This section has remained largely unchanged since it was amended in 1994 to add the requirement to adjust for inflation, among other changes.55 The inflation adjustment clause has resulted in increasing payment and ceiling rates since that time.56 Congress routinely considers whether the current formula is the best means of calculating payments under PILT or whether the formula should be amended. For example, in the 116th Congress, bills have been introduced that would adjust the payment structure for counties with a population of less than 5,000.57 This adjustment would have implications for how population or area would be incorporated into calculating PILT payments and whether PILT payments were provided in an equitable manner.

PILT is of interest to a large number of counties and other state and local entities across the country, and it may remain of interest to many Members of Congress. In addition to the above issues, Congress may consider other issues related to PILT and how the program fits into the landscape of federal programs that compensate for the presence of tax-exempt federal lands.

Author Contact Information

Footnotes

| 1. |

31 U.S.C. §§6901-6907. Implementing regulations for the Payments in Lieu of Taxes (PILT) program are provided at 43 C.F.R. Part 44. |

| 2. |

PILT was originally enacted in 1976 through P.L. 94-565. In 1982, PILT was "revised, codified, and enacted" in Title 31 of the U.S. Code pursuant to Chapter 69 of P.L. 97-258. PILT has been amended multiple times. |

| 3. |

Although PILT is the broadest of these compensatory programs, it is not the oldest, and PILT provides compensation for defined entitlement lands only (31 U.S.C. §6901(1)). Other programs may include additional lands as defined by those programs. Several of those programs may be partially offset in PILT through the consideration of prior-year payments. Those programs are listed at 31 U.S.C. §6903(a)(1). |

| 4. |

For more information, see Public Land Law Review Commission, One Third of the Nation's Land: A Report to the President and to the Congress, June 1970, pp. 235-241. This report was produced pursuant to P.L. 88-606. |

| 5. |

For more information, see U.S. Congress, House Committee on Interior and Insular Affairs, Payments In Lieu of Taxes Act, report to accompany H.R. 9719, 94th Cong., 2nd sess., May 7, 1976, H.Rept. 94-1106; and U.S. Congress, Senate Committee on Interior and Insular Affairs, Providing for Payments to Local Governments Based upon the Amount of Certain Public Lands Within the Boundaries of Each Such Government, report to accompany H.R. 9719, 94th Cong., 2nd sess., September 20, 1976, S.Rept. 94-1262. |

| 6. |

31 U.S.C. §6902(a), 31 U.S.C. §6904(b), and 31 U.S.C. §6905(a) and (b)(3). However, both §6904 and §6905 require that certain funds provided through these sections are made available to school districts and other local governmental units within the local jurisdiction. |

| 7. |

For more information, see Department of the Interior (DOI), Fiscal Year 2019 Payments In Lieu of Taxes, National Summary, June 2019, p. 1, at https://www.doi.gov/sites/doi.gov/files/uploads/2019_national_summary_pilt_0.pdf (hereinafter, National Summary FY2019). |

| 8. |

Although the DOI Office of the Secretary administers the payments, it relies upon data from federal agencies within and outside of DOI (e.g., the federal land management agencies and the Census Bureau in the Department of Commerce) and state agencies to calculate the annual payments. |

| 9. |

These sections refer to 31 U.S.C. §§6902, 6904, and 6905. |

| 10. |

PILT payments may be subject to additional requirements provided in appropriations laws. For example, provisions for prorated payments, set-aside, and minimum payments were all included in Title I of Division D in P.L. 116-94 for FY2020. |

| 11. |

National Summary FY2019, p. 1. |

| 12. |

For example, see S. 2480, H.R. 3043, S. 2108, and H.R. 3716 in the 116th Congress. |

| 13. |

31 U.S.C. §6906, prior to the enactment of P.L. 110-343. Between 1976 and 1982, the authorization of appropriations from PILT was codified at 31 U.S.C. §1607 and read, "There are authorized to be appropriated for carrying out the provisions of this Act such sums as may be necessary: Provided, That, notwithstanding any other provision of this Act no funds may be made available except to the extent provided in advance in appropriations." P.L. 94-565, §7. |

| 14. |

31 U.S.C. §6906, prior to the enactment of P.L. 110-343. |

| 15. |

P.L. 110-343, Div. C, Title VI, §601(c)(1). |

| 16. |

P.L. 110-343, Div. C, Title VI, §601(c)(1). |

| 17. |

P.L. 110-343, P.L. 112-141, and P.L. 113-79. |

| 18. |

P.L. 113-235 and P.L. 113-291. |

| 19. |

P.L. 114-113 and P.L. 115-31. |

| 20. |

P.L. 115-141, P.L. 116-6, and P.L. 116-94. |

| 21. |

For example, in FY2020, provisions were included in Title I of Division D in P.L. 116-94 that specified that no payment is to be made if the authorized payment is less than $100; to authorize DOI to retain up to $400,000 from the authorized payment for administrative expenses; to allow for payments to be reduced proportionally if the appropriated amount is insufficient; and to correct for prior over- or underpayments. Although similar provisions have routinely been included in appropriations acts, the specific text of these provisions has varied. |

| 22. |

31 U.S.C. §6901(2). |

| 23. |

National Summary FY2019, p. 7. |

| 24. |

National Summary FY2019, Schedule 1. Four counties received payments under §6904 and/or §6905 but did not receive §6902 payments: Berkshire County, MA; Windsor County, VT; Beaufort County, SC; and Hancock County, ME. |

| 25. |

31 U.S.C. §6901(1). |

| 26. |

Most of these lands are under the jurisdiction of the Bureau of Reclamation. |

| 27. |

Public domain lands "refers to public lands the United States obtained title to through treaty, purchase, or annexation that have never left federal ownership." For more information public domain and acquired lands, see U.S. Fish and Wildlife Service, Statistical Data Tables for Fish &Wildlife Service Lands (as of 9/30/2019), at https://www.fws.gov/refuges/land/PDF/2019_Annual_Report_Data_Tables(508-Compliant).pdf. |

| 28. |

Prior-year payment programs that may affect PILT payments are listed at 16 U.S.C. §6903(a)(1). |

| 29. |

National Summary FY2019, p. 115. As noted, the number of acres is provided to the Office of the Secretary by the various federal agencies that administer the entitlement lands. |

| 30. |

Even though the population payment rate declines as county population size increases, payment ceilings generally are higher for counties with larger populations. For example, in FY2019, the population payment rate for a population of 5,000 was $186.56 and the rate for a population of 6,000 was $174.71, a decrease of $11.85 for the more populous county. When multiplied by the population, however, the ceiling is higher for the county with the larger population: 5,000 × $186.56 = $932,800, versus 6,000 × $174.71 = $1,048,260, or $115,460 more for the more populous county. |

| 31. |

31 U.S.C. §6903(d). |

| 32. |

The per capita payment rates are included in the PILT national summary each year. For example, the National Summary FY2019, p. 14, includes the payment rates for FY2019. |

| 33. |

31 U.S.C. §6903(a)(1). |

| 34. |

National Summary FY2019, p. 9. According to DOI Only the amount of Federal land payments actually received by units of government in the prior fiscal year is deducted. If a unit receives a Federal land payment but is required by State law to pass all or part of it to financially and politically independent school districts, or to any other single or special purpose district, payments are considered to have not been received by the unit of local government and are not deducted from the Section 6902 payment. |

| 35. |

If the population-based ceiling replaces the per-acre calculation under Alternative A, prior-year payments are then deducted from the population-based ceiling to determine the final amount for Alternative A. |

| 36. |

Congress provides funding for PILT through either discretionary or mandatory appropriations, or both, in any given year. See "PILT Authorizations and Appropriations" for more information. |

| 37. |

Payments may be subject to any additional provisions included in appropriations language, such as minimum payment thresholds or adjustments for under- or overpayments in previous years. PILT provisions in appropriations laws generally have required a minimum payment threshold of $100. For example, the FY2019 appropriations language included a $100 minimum payment clause (P.L. 116-6, Division E, Title I). In FY2019, 202 counties had an authorized payment of less than $100; these counties did not receive payments, per the FY2019 appropriations language. |

| 38. |

The provision for a prorated payment is not included in the PILT statutory language (31 U.S.C. §§6901-6907), but it has been included in certain appropriations legislation for PILT. |

| 39. |

The requirement of a minimum threshold of $100 for PILT payments is routinely included in appropriations language related to PILT (e.g., for FY2020, Title I of Division D in P.L. 116-94) and also is in regulation (43 C.F.R. §44.51). |

| 40. |

A set-aside for administrative expenses routinely has been included in PILT appropriations language. For example, DOI is allowed to retain up to $400,000 of the appropriations for PILT for administrative expenses in FY2020 (Title I of Division D in P.L. 116-94). |

| 41. |

31 U.S.C. §§6904 and 6905. |

| 42. |

National Summary FY2019, p. 7. This source reports §6904 and §6905 payments together, and further disaggregation is not possible from the information provided. |

| 43. |

43 C.F.R. §44.50. |

| 44. |

31 U.S.C. §6904. For more information on the National Park System, see CRS Report R41816, National Park System: What Do the Different Park Titles Signify?, by Laura B. Comay. For more information on wilderness areas, see CRS Report RL31447, Wilderness: Overview, Management, and Statistics, by Anne A. Riddle and Katie Hoover. |

| 45. |

31 U.S.C. §6905. The Act of December 23, 1980 is P.L. 96-586. |

| 46. |

43 C.F.R. §44.40. Payments may extend beyond five years when taxes levied in the year prior to acquisition account for less than 1% of the fair market value of the acquired land. However, any portion of a payment not made because Congress did not appropriate sufficient funds is not deferred to later payments. |

| 47. |

National Association of Counties (NACo), Provide Full Mandatory Funding for the Payments in Lieu of Taxes (PILT) Program, September 1, 2019, at https://www.naco.org/resources/provide-full-mandatory-funding-payments-lieu-taxes-pilt-program. |

| 48. |

NACo, Counties to Congress: Reauthorize the Secure Rural Schools (SRS) program and fully fund Payments in Lieu of Taxes (PILT), April 11, 2017, at https://www.naco.org/blog/counties-congress-reauthorize-secure-rural-schools-srs-program-and-fully-fund-payments-lieu. |

| 49. |

For more information, see CRS Report R44582, Overview of Funding Mechanisms in the Federal Budget Process, and Selected Examples, by Jessica Tollestrup. |

| 50. |

S. 2480 would require mandatory PILT funding through FY2029, and H.R. 3043 would require mandatory PILT funding indefinitely. |

| 51. |

For example, H.R. 7251 in the 110th Congress. |

| 52. |

For example, H.R. 4710 in the 113th Congress. |

| 53. |

For example, S. 2626 in the 113th Congress. |

| 54. |

For example, H.R. 543 in the 112th Congress. |

| 55. |

P.L. 103-397 amended 31 U.S.C. §6903 in several ways. Since then, §6903 has been amended once; P.L. 106-393 amended the definition of payment law at 31 U.S.C. §6903(a)(1)(C). That amendment added the Secure Rural Schools and Community Self-Determination Act of 2000 (16 U.S.C. §§7101 et seq.) to the list of payment laws, which are included in determining prior-year payments. |

| 56. |

P.L. 103-397 added the requirement to adjust for inflation. |

| 57. |