The Social Security Retirement Age

Changes from February 28, 2018 to March 7, 2019

This page shows textual changes in the document between the two versions indicated in the dates above. Textual matter removed in the later version is indicated with red strikethrough and textual matter added in the later version is indicated with blue.

Contents

- Introduction

- Full Retirement Age

(FRA) - Early Eligibility Age

(EEA) - Actuarial Modification to Benefits: Claiming Before or After the FRA

- Actuarial Reduction for Claiming Benefits Before the FRA

- Delayed Retirement Credit for Claiming Benefits After the FRA

- Retirement Earnings Test

- Age Distribution of New Retired-Worker Beneficiaries

- Proposals to Increase the Retirement Age

Figures

Summary

The Social Security full retirement age (FRA) is the age at which workers can first claim full Social Security retired-worker benefits. Among other factors, a worker's monthly benefit amount is affected by the age at which he or she claims benefits relative to the FRA. Benefit adjustments are made based on the number of months before or after the FRA the worker claims benefits. The adjustments are intended to provide the worker with roughly the same total lifetime benefits, regardless of when he or she claims benefits, based on average life expectancy. Claiming benefits before the FRA results in a permanent reduction in monthly benefits (to take into account the longer expected period of benefit receipt); claiming benefits after the FRA results in ana permanent increase in monthly benefits (to take into account the shorter expected period of benefit receipt).

The FRA was 65 at the inception of Social Security in the 1930s. Under legislation enacted in 1983, the FRA is increasing gradually from 65 to 67 over a 22-year period (2000-for those reaching age 62 between 2000 and 2022). The FRA will reach 67 for workers born in 1960 or later (i.e., for workers who become eligible for retirement benefits at age 62 in 2022). Currently, the FRA is 66 and 46 months for workers who become eligible for retirement benefits in 20182019 (i.e., workers born in 19561957).

Workers can claim reduced retirement benefits as early as age 62 (the early eligibility age). Spouses can also claim reduced retirement benefits starting at age 62. Other dependents, such as widow(er)s, can claim benefits at earlier ages. For workers with an FRA of 66, for example, claiming benefits at age 62 results in a 25% reduction in monthly benefits. For workers with an FRA of 67, claiming benefits at age 62 results in a 30% benefit reduction. A majority of retired-worker beneficiaries claim benefits before the FRA. In 2016, 392017, 37% of new retired-worker beneficiaries were age 62; almost two-thirds (6664%) were under the age of 66.

Workers who delay claiming benefits until after the FRA receive a delayed retirement credit, which applies up to the age of 70. For workers with an FRA of 66, for example, claiming benefits at age 70 results in a 32% increase in monthly benefits. For workers with an FRA of 67, claiming benefits at age 70 results in a 24% benefit increase. In 20162017, almost one-fourth (23%) of new retired-worker beneficiaries were age 66; 1112% were over the age of 66.

Some lawmakers have called for increasing the Social Security retirement age in response to the system's projected financial imbalance, citing gains in life expectancy for the population overall. Other lawmakers, however, express concern that increasing the retirement age would disproportionately affect certain groups within the population, citing differences in life expectancy by socioeconomic groups. Differential gains in life expectancy are important in the context of Social Security because the actuarial adjustments for claiming benefits before or after the full retirement age are based on average life expectancy. Proposals to increase the retirement age are also met with concerns about the resulting hardship for certain workers, such as those in physically demanding occupations, who may be unable to work until older ages and may not qualify for Social Security disability benefits. For an in-depth discussion of potential changes in the Social Security retirement age in the context of life expectancy trends, see CRS Report R44846, The Growing Gap in Life Expectancy by Income: Recent Evidence and Implications for the Social Security Retirement Age.

Introduction

The Social Security full retirement age (FRA) is the age at which workers can first claim full Social Security retired-worker benefits.1 Among other factors, the age at which an individual begins receiving Social Security benefits has an impact on the size of the monthly benefits. Claiming benefits before the FRA can substantially reduce monthly benefits, whereas claiming benefits after the FRA can lead to a substantial increase in monthly benefits. Benefit adjustments are made based on the number of months before or after the FRA the worker claims benefits. The adjustments are intended to result in roughly the same total lifetime benefits, regardless of when the worker claims benefits, based on average life expectancy.

The FRA was 65 at the inception of Social Security in the 1930s. As part of legislation enacted in 1983, the FRA is increasing gradually from 65 to 67 over a 22-year period that started for those who turned age 62 in 2000. The increase in the FRA will be fully phased- in (the FRA will reach 67) for workers born in 1960 or later (i.e., for workers who become eligible for retirement benefits at age 62 in 2022). For workers who become eligible for retirement benefits in 20182019 (i.e., workers born in 19561957), the FRA is 66 and 46 months.

Workers can claim Social Security retired-worker benefits as early as age 62, the early eligibility age (EEA). However, workers who claim benefits before the FRA are subject to a permanent reduction in their benefits. Spouses can also claim reduced retirement benefits as early as age 62. Other types of dependents can claim benefits before the age of 62.2

Workers who claim benefits after the FRA receive a delayed retirement credit that results in a permanent increase in their monthly benefits. The credit applies up to the age of 70. Claiming benefits after attainment of age 70 does not result in any further increase in monthly benefits.3

Full Retirement Age (FRA)

The FRA was 65 at the inception of Social Security. According to Robert Myers, who worked on the creation of the Social Security program in 1934 and later served in various senior and appointed capacities at the Social Security Administration (SSA), "[a]ge 65 was picked because 60 was too young and 70 was too old. So we split the difference."4 On the other hand, SSA suggests that the Committee on Economic Security (CES) made the proposal of 65 as the retirement age due to the prevalence of private and state pensionspension systems using 65 as the retirement age and the favorable actuarial outcomes for 65 as the retirement age.5

In 1983, Congress increased the FRA as part of the Social Security Amendments of 1983,6 which made major changes to Social Security's financing and benefit structure to address the system's financial imbalance at the time.7 Among other changes, the FRA was increased gradually from 65 to 67 for workers born in 1938 or later. Under the scheduled increases enacted in 1983, the FRA increases to 65 and 2 months for workers born in 1938. The FRA continues to increase by two months every birth year until the FRA reaches 66 for workers born in 1943 to 1954. Starting with workers born in 1955, the FRA increases again in two-month increments until the FRA reaches 67 for workers born in 1960 or later. The increase in the FRA, one of many provisions in the 1983 amendments designed to improve the system's financial outlook, was based on the rationale that it would reflect increases in longevity and improvements in the health status of workers.8 The 1983 amendments did not change the early eligibility age of 62 (discussed below); however, the increase in the FRA results in larger benefit reductions for workers who claim benefits between the age of 62 and the FRA.9 Table 1 shows the FRA by worker's year of birth under current law.

|

Year of Birth |

Full Retirement Age (FRA) |

|

1937 or earlier |

65 |

|

1938 |

65 and 2 months |

|

1939 |

65 and 4 months |

|

1940 |

65 and 6 months |

|

1941 |

65 and 8 months |

|

1942 |

65 and 10 months |

|

1943-1954 |

66 |

|

1955 |

66 and 2 months |

|

1956 |

66 and 4 months |

|

1957 |

66 and 6 months |

|

1958 |

66 and 8 months |

|

1959 |

66 and 10 months |

|

1960 or later |

67 |

Source: Social Security Administration, https://www.ssa.gov/planners/retire/retirechart.html.

Notes: Persons born on January 1 of any year should refer to the previous year of birth.

Early Eligibility Age (EEA)

Currently, the EEA is 62 for workers and spouses; this is the earliest age at which they can claim retirement benefits. Benefits claimed between age 62 and the FRA, however, are subject to a permanent reduction for "early retirement." When the original Social Security Act was enacted in 1935,10 the earliest age to receive retirement benefits was the FRA (age 65). In 1956, the eligibility age was lowered from 65 to 62 for female workers, wives, widows, and female dependent parents.11 This was to allow wives, who traditionally were younger than their husbands, to qualify for benefits at the same time as their husbands.12 Benefits for female workers and wives were subject to reduction if claimed between the ages of 62 and 65; the reduction did not apply to benefits for widows and female dependent parents.

In 1961, the eligibility age was lowered from 65 to 62 for men as well.13 Benefits for male workers and husbands were subject to reduction if claimed between the ages of 62 and 65; the reduction did not apply to widowers and male dependent parents. Although the eligibility age was made consistent for male and female workers, an inconsistency remained in the calculation of benefits. A man the same age as a woman needed more Social Security credits to qualify for benefits, and, if his earnings were identical to hers, usually received a lower benefit because his earnings were averaged over a longer period. This inconsistency was addressed in legislation enacted in 1972 which provided that retirement benefits would be computed the same way for men and women (the provision was fully effective for men reaching age 62 in 1975 or later).14

In subsequent years, further adjustments were made to the eligibility age for surviving spouses.15 The eligibility age was lowered to age 60 for widows (1965),16 age 50 for disabled widow(er)s (1967),17 and age 60 for widowers (1972).18

Actuarial Modification to Benefits: Claiming Before or After the FRA

Benefits are adjusted based on the age at which a person claims benefits to provide roughly the same total lifetime benefits regardless of when a person begins receiving benefits, based on average life expectancy. The earlier a worker begins receiving benefits (before the FRA), the lower the monthly benefit will be, to offset the longer expected period of benefit receipt. Conversely, the longer a worker delays claiming benefits (past the FRA), the higher the monthly benefit will be, to take into account the shorter expected period of benefit receipt. The benefit adjustment is based on the number of months between the month the worker attains the FRA and the month he or she claims benefits. The day of birth is ignored for adjustment purposes, except for those born on the first of the month. Workers born on the first of the month base their FRA as if their birthday was in the previous month (e.g., someone born on February 1, 1980, who has an FRA of 67, can apply for full retirement benefits in January 2047). A calculator on SSA's website allows the user to enter his or her date of birth and the expected month of initial benefit receipt to see the effect of early or delayed retirement; the effect is shown as a percentage of the full benefit payable at the FRA.19

Actuarial Reduction for Claiming Benefits Before the FRA

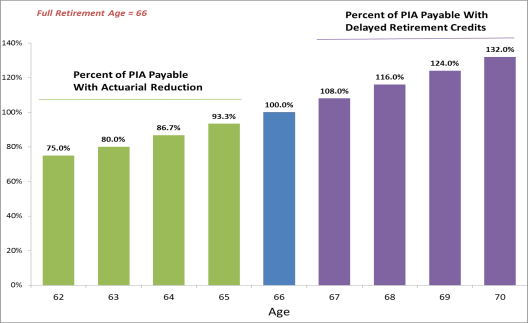

When a worker claims benefits before the FRA, there is an actuarial reduction in monthly benefits. The reduction for claiming benefits before the FRA can be sizable and it is permanent; all future monthly benefits are payable at the actuarially reduced amount. For each of the 36 months immediately preceding the FRA, the monthly rate of reduction from the full retirement benefit is five-ninths of 1%. This equals a 6⅔% reduction each year. For each month earlier than three years (36 months) before the FRA, the monthly rate of reduction is five-twelfths of 1%. This equals a 5% reduction each year. The earliest a worker can claim retirement benefits is age 62. For a worker with an FRA of 67, claiming benefits at 62 results in a 30% reduction in their monthly benefit. Table 2 shows the actuarial reduction applied to retired-worker benefits based on the FRA and the age at which benefits are claimed.20

|

Full Retirement Age |

Actuarial Reduction to Monthly Amount if Worker Claims at Age… |

||||

|

62 |

63 |

64 |

65 |

66 |

|

|

65 |

20% |

13 1⁄3% |

6 2⁄3% |

0% |

-a |

|

66 |

25% |

20% |

13 1⁄3% |

6 2⁄3% |

0% |

|

67 |

30% |

25% |

20% |

13 1⁄3% |

6 2⁄3% |

Source: Social Security Administration, https://www.ssa.gov/planners/retire/retirechart.html.

a. With an FRA of 65, claiming retired-worker benefits at age 66 leads to a delayed retirement credit, resulting in an increase in monthly benefits, as opposed to a reduction.

Delayed Retirement Credit for Claiming Benefits After the FRA

Workers who claim benefits after the FRA receive a delayed retirement credit (DRC). As with the actuarial reduction for early retirement, the delayed retirement credit is permanent. The DRC has been modified over the years. Initially, the Social Security Amendments of 197221 provided a delayed retirement credit that increased benefits by one-twelfth of 1% for each month between ages 65 and 72 that a worker did not claim benefits (i.e., 1% per year). The credit, which was effective after 1970, applied only to the worker's benefit; it did not apply to a widow(er)'s benefit payable on the worker's record. The Social Security Amendments of 197722 increased the credit to 3% per year and included the credit in the computation of a widow(er)'s benefit.

The credit was further increased under the Social Security Amendments of 1983.23 As shown in Table 3, under current law, the amount of the credit varies based on the worker's year of birth (i.e., when the worker becomes eligible for benefits at age 62). The credit increases gradually until it reaches 8% per year (two-thirds of 1% per month) for workers born in 1943 or later (i.e., workers who becomebecame eligible for retirement benefits in 2005 or later). In addition, the maximum age at which the DRC applies was lowered from 72 to 70. Any further delay in claiming benefits past age 70 does not result in a higher benefit. The increase in the DRC was intended to ensure that workers who claim benefits after the FRA receive roughly the same total lifetime benefits as if they had claimed benefits earlier (based on average life expectancy). A worker with an FRA of 66, for example, receives a 32% benefit increase if he or she claims benefits at age 70; a worker with an FRA of 67 receives a 24% benefit increase.

|

Year of Birth |

Monthly Credit |

Annual Credit |

|

1916 or earlier |

1⁄12 of 1% |

1% |

|

1917-1924 |

1⁄4 of 1% |

3% |

|

1925-1926 |

7⁄24 of 1% |

3.5% |

|

1927-1928 |

1⁄3 of 1% |

4% |

|

1929-1930 |

3⁄8 of 1% |

4.5% |

|

1931-1932 |

5⁄12 of 1% |

5% |

|

1933-1934 |

11⁄24 of 1% |

5.5% |

|

1935-1936 |

1⁄2 of 1% |

6% |

|

1937-1938 |

13⁄24 of 1% |

6.5% |

|

1939-1940 |

7⁄12 of 1% |

7% |

|

1941-1942 |

5⁄8 of 1% |

7.5% |

|

1943 or later |

2⁄3 of 1% |

8% |

Source: Social Security Administration, https://www.ssa.gov/OP_Home/cfr20/404/404-0313.htm.

Note: Persons born on January 1 of any year should refer to the previous year of birth.

Figure 1 illustrates the effect of claiming age on benefit levels based on an FRA of 66. If the worker claims retirement benefits at age 62, for example, his or her benefit would be equal to 75% of the full benefit amount—a 25% permanent reduction based on claiming retirement benefits four years before attaining the FRA. If the worker delays claiming retirement benefits until age 70, however, his or her benefit would be equal to 132% of the full benefit amount—a 32% permanent increase for claiming benefits four years after the FRA.

Retirement Earnings Test

The decision to claim Social Security benefits before the FRA results in a permanent reduction in monthly benefits for early retirement. In addition, if a Social Security beneficiary is below the FRA and has current earnings, he or she is subject to the retirement earnings test (RET). Stated generally, Social Security benefits are withheld partially or fully, for one or more months, if current earnings exceed specified thresholds.

There are two separate earnings thresholds (or exempt amounts) under the RET. The first (lower) threshold applies to beneficiaries who are below the FRA and will not attain the FRA during the year. In 20182019, the lower earnings threshold is $17,040640.24 If a beneficiary has earnings that exceed the lower threshold, SSA withholds $1 of benefits for every $2 of earnings above the threshold.

The second (higher) threshold applies to beneficiaries who are below the FRA and will attain the FRA during the year. In 20182019, the higher earnings threshold is $45,36046,920. If a beneficiary has earnings that exceed the higher threshold, SSA withholds $1 of benefits for every $3 of earnings above the threshold. The RET no longer applies beginning with the month the beneficiary attains the FRA. OnceIn other words, once the beneficiary attains the FRA, his or her benefits are no longer subject to withholding based on earnings.25

During the first year of benefit receipt, a special monthly earnings test applies.26 Regardless of the amount of annual earnings in the first year of benefit receipt, benefits are not withheld for any month in which earnings do not exceed a monthly exempt amount (the monthly exempt amount is equal to 1/12 of the annual exempt amount). In 20182019, the monthly exempt amounts are $1,420470 ($17,040640/12) and $3,780 ($45,360910 ($46,920/12).

For example, consider a worker who claims benefits at age 62 in January 20182019 and has no earnings during the year except for a consulting project that pays $20,000 in July. Although the beneficiary's annual earnings ($20,000) exceed the annual exempt amount ($17,040640), benefits are withheld only for the month of July. The beneficiary has $0 earnings in all other months; July is the only month in which earnings exceed the monthly exempt amount ($1,420470).

Benefits withheld under the RET are not "lost" on a permanent basis. When a beneficiary attains the FRA and is no longer subject to the RET, SSA automatically recalculates the benefit, taking into account any months for which benefits were partially or fully withheld under the RET. Stated generally, there is no actuarial reduction for early retirement for any month in which benefits were partially or fully withheld under the RET. The recalculation results in a higher monthly benefit going forward.27 Starting at the FRA, the beneficiary begins to recoup the value of benefits withheld under the RET; the beneficiary recoups the full value of those benefits if he or she lives to average life expectancy.28

Age Distribution of New Retired-Worker Beneficiaries

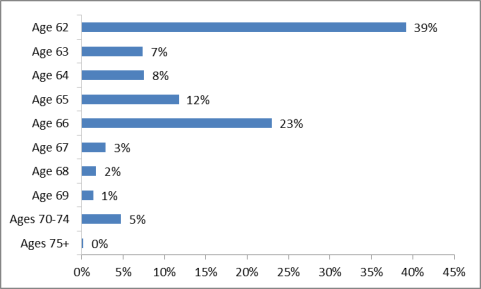

Statistics published by SSA show that a majority of retired-worker beneficiaries claim benefits before the FRA.29 Figure 2 shows the age distribution of new retired-worker beneficiaries in 20162017.30 Among nearly 2.52.4 million new retired-worker beneficiaries that year, 3937% claimed benefits at age 62 (the first year of eligibility) and 6664% were under the age of 66. About one-fourth (23%) of new retired-worker beneficiaries claimed benefits at age 66, while 1112% were age 67 or older. The percentage of retired-worker beneficiaries who claim benefits at earlier ages has declined in recent years. In 2010, for example, more than one-half (52%) of new retired-worker beneficiaries were age 62 and 81% were under the age of 66.31

|

Figure 2. Age Distribution of New Retired-Worker Beneficiaries in |

|

|

Source: Social Security Administration, Annual Statistical Supplement, Notes: Figure does not include disabled-worker beneficiaries who were automatically converted to retired-worker beneficiaries upon attaining the FRA. |

Proposals to Increase the Retirement Age

The Social Security full retirement age was 65 when the program was established in the 1930s. It remained 65 until 1983, when Congress included an increase in the FRA among many provisions in the Social Security Amendments of 1983,32 which were designed to address serious near-term and long-range financing problems. The 1983 Amendments became law on April 20, 1983. Without legislative action, it was anticipated that Social Security benefits could not be paid on time beginning in July 1983.33 The 1983 provision that increased the FRA from 65 to 67 continues to be phased- in; it will be fully phased- in by 2022.34

The Social Security system once again faces projected long-range funding shortfalls. The Social Security Board of Trustees (the Trustees) projects that full Social Security benefits can be paid on time until 2034 with a combination of annual Social Security tax revenues and asset reserves held by the Social Security trust funds. After the projected depletion of trust fund reserves in 2034, however, annual tax revenues are projected to cover about three-fourths of benefits scheduled under current law.35

Over the years, there have been many proposalsmany proposals have been designed to improve Social Security's financial outlook as well as achieve other policy goals. A common proposal is to increase the early eligibility age and/or further increase the full retirement age. As in the past, lawmakers who support increasing the retirement age point to gains in average life expectancy as an indicator that people can work until older ages. Those who oppose this type of policy change, however, point out that gains in life expectancy have not been shared equally across different segments of the population. They cite research showing that life expectancy is lower for individuals with lower socioeconomic status (SES) compared to those with higher SES, and that the gap in life expectancy by SES has been growing over time.36

Differential gains in life expectancy are important in the context of Social Security. The actuarial adjustments to benefits for early or delayed retirement (i.e., for claiming benefits before or after the full retirement ageFRA) are based on average life expectancy. That is, the actuarial adjustments are designed to provide a person with roughly the same total lifetime benefits, regardless of the age at which he or she claims benefits, assuming the person lives to average life expectancy. Research has shown that differential gains in life expectancy have resulted in a widening gap in the value of lifetime Social Security retirement benefits between low earners and high earners.37

In recentOver the years, deficit reduction commissions and other policymakers have recommended an increase in the Social Security retirement age. In 2010, for example, The recent proposals, for example, included the S.O.S. Act of 2016 (H.R. 5747, the 114th Congress), which proposed increasing the FRA among other changes. Under the proposal, after the FRA reaches 67 for those attaining 62 in 2022, the FRA would increase by two months per year until the FRA reaches 69 for those attaining 62 in 2034. Thereafter, the FRA would increase one month every year. SSA's Office of the Chief Actuary (OCACT) projects that this option would improve the Social Security trust fund outlook by eliminating 39% of the system's projected long-range funding shortfall (based on the 2018 Annual Report of the Social Security Board of Trustees, intermediate assumptions).38

Another recent proposal from the Bipartisan Policy Center in 2016 recommended, among other changes, to increase the FRA by one month every two years after the FRA reaches 67 for those attaining age 62 in 2022 until the FRA reaches 69, and also increase the age up to which the DRC may be earned at the same rate (from 70 to 72). This option contains no change in the EEA. OCACT estimates that this option would improve the Social Security trust fund outlook by eliminating 19% of the system's projected long-range funding shortfall (based on the 2018 Annual Report of the Social Security Board of Trustees, intermediate assumptions).39

In 2010, the National Commission on Fiscal Responsibility and Reform (also called the Simpson-Bowles Commission after co-chairs Alan Simpson and Erskine Bowles) recommended increasing both the early eligibility age (EEA) and the full retirement age (FRA)EEA and the FRA, among other Social Security changes. Under the commission's recommendations, after the FRA reaches 67 in 2027, both the EEA and the FRA would be indexed to increases in life expectancy. The commission estimated that the FRA would reach 68 by about 2050, and 69 by about 2075. The EEA would increase to 63 and 64 in step with increases in the FRA.38

In conjunction with proposed increases in the EEA and FRA, the commission recommended policies that would provide people with more flexibility in claiming benefits. Specifically, the commission recommended allowing people to claim up to half of their benefits at age 62 (with an actuarial reduction) and the other half at a later age (with a smaller actuarial reduction). This option was intended to provide a smoother transition for those interested in phased retirement or for households where one member has retired and another continues to work.3942 In general, it could provide a stream of income for those with financial difficulties by allowing them to claim a portion of their benefits early and avoid taking a permanent reduction on the full benefit amount.

Recognizing that some workers may be physically unable to work beyond the current EEA (62) and may not qualify for Social Security disability benefits, the commission also recommended a hardship exemption for up to 20% of retirees. Under the proposal, as the EEA and FRA increase, certain beneficiaries could continue to claim benefits at age 62 and their benefits would not be subject to additional actuarial reductions. The commission specified that SSA would design the policy taking into consideration factors such as the physical demands of labor and lifetime earnings in developing eligibility criteria.4043 Concerns regarding the effects of increasing the retirement age, especially on certain segments of the population, are not new. The Social Security Amendments of 1983, which increased the retirement age gradually from 65 to 67, mandated a study to examine the effects of increasing the retirement age on workers in physically demanding jobs and/or ill health.41

Social Security legislative proposals offered over the years have included changes to the retirement age. SSA's Office of the Chief Actuary (OCACT) provides trust fund solvency projections for selected proposals on their website (see Proposals Affecting Trust Fund Solvency).42 For example, projections for the Social Security changes proposed by the National Commission on Fiscal Responsibility and Reform can be found by scrolling down to Fiscal Commission under the column heading Developer(s) of Proposal.

In addition, OCACT provides trust fund solvency projections for individual provisions to change the retirement age (see Individual Changes Modifying Social Security, Category C: Retirement Age).43 Under the first option, for example, the FRA would increase gradually from 67 to 68 (see Number C1.1 - After the normal retirement age (NRA) reaches 67 for those age 62 in 2022, increase the NRA 1 month every 2 years until the NRA reaches 68). OCACT projects that this option would improve the Social Security trust fund outlook by eliminating 13% of the system's projected long-range funding shortfall (based on the 2017 Annual Report of the Social Security Board of Trustees, intermediate assumptions).

Author Contact Information

Acknowledgments

The previous author of the report was CRS specialist [author name scrubbed]Specialist Dawn Nuschler. An earlier version was written by former CRS analysts [author name scrubbed]Analysts Wayne Liou and Alison Shelton.

Footnotes

| 1. |

The full retirement age is also referred to as the normal retirement age (NRA). In statute, the term "retirement age" is used; see Social Security Act, §216(l) [42 U.S.C. §416(l)]. |

|||

| 2. |

Widow(er)'s benefits can be claimed as early as age 60; disabled widow(er)'s benefits can be claimed as early as age 50. These benefits are also subject to reduction if claimed before the FRA. There is no minimum eligibility age for dependent child's benefits. For more details, see "Benefits for the Worker's Family Members" in CRS Report R42035, Social Security Primer. |

|||

| 3. |

The |

|||

| 4. |

Robert J. Myers and Richard L. Vernaci, Within the System: My Half Century in Social Security (Winsted, CT: ACTEX Publications, 1992), pp. 93-94. |

|||

| 5. |

Social Security Administration (SSA), "Age 65 Retirement," at https://www.ssa.gov/history/age65.html. The actuarial studies in the 1930s showed that using age 65 produced a manageable system that could easily be made self-sustaining with only modest levels of payroll taxation. |

|||

| 6. | ||||

| 7. |

An increase in the FRA is a form of benefit reduction. Those who claim benefits at the higher FRA, for example, receive fewer months of benefits and a reduction in the total amount of lifetime Social Security benefits holding everything else constant. |

|||

| 8. |

For example, see Rep. Elliott H. Levitas, "Social Security Amendments of 1983," House debate, Congressional Record, vol. 129, part 4 (March 9, 1983), p. 4517; Rep. Beryl Anthony, Jr., "Social Security Amendments of 1983," House debate, Congressional Record, vol. 129, part 4 (March 9, 1983), p. 4600. |

|||

| 9. |

For example, retired-worker benefits claimed at age 62 are reduced by 20% if the worker's FRA is 65, by 25% if the worker's FRA is 66, and by 30% if the worker's FRA is 67. |

|||

| 10. |

P.L. 74-271, Social Security Act. |

|||

| 11. |

P.L. 84-880, Social Security Amendments of 1956. |

|||

| 12. |

For example, see Rep. Thomas A. Jenkins, "Social Security Amendments of 1955," House debate, Congressional Record, vol. 101, part 8 (July 18, 1955), p. 10778; Rep. Wilbur Mills, "Social Security Amendments of 1955," House debate, Congressional Record, vol. 101, part 8 (July 18, 1955), p. 10785. |

|||

| 13. |

P.L. 87-64, Social Security Amendments of 1961. |

|||

| 14. |

P.L. 92-603, Social Security Amendments of 1972. |

|||

| 15. |

Benefits for surviving spouses are subject to reduction if claimed before the FRA (and other factors); see "Benefits for the Worker's Family Members" in CRS Report R42035, Social Security Primer. |

|||

| 16. |

P.L. 89-97, Social Security Amendments of 1965. |

|||

| 17. |

P.L. 90-248, Social Security Amendments of 1967. |

|||

| 18. |

P.L. 92-603, Social Security Amendments of 1972. |

|||

| 19. |

The calculator is available at https://www.ssa.gov/oact/quickcalc/early_late.html#calculator. |

|||

| 20. |

Actuarial reductions for spouses and widow(er)s are different; see SSA, "Benefit Reduction for Early Retirement," at https://www.ssa.gov/oact/quickcalc/earlyretire.html. |

|||

| 21. |

P.L. 92-603. |

|||

| 22. | ||||

| 23. | ||||

| 24. |

The earnings thresholds generally increase each year based on average wage growth in the economy. See SSA, "Exempt Amounts Under the Earnings Test," at https://www.ssa.gov/OACT/COLA/rtea.html. |

|||

| 25. |

The Senior Citizens' Freedom to Work Act of 2000 (P.L. 106-182) eliminated the RET for beneficiaries at the FRA or older. |

|||

| 26. |

A person may claim retired-worker benefits in the middle of the year, for example, and have already earned more than the annual earnings limit under the RET. |

|||

| 27. |

For more information, see CRS Report R41242, Social Security Retirement Earnings Test: How Earnings Affect Benefits. |

|||

| 28. |

For more information, see SSA, Office of Retirement Policy, "Retirement Earnings Test," at https://www.ssa.gov/retirementpolicy/program/retirement-earnings-test.html. |

|||

| 29. |

SSA, Annual Statistical Supplement, |

|||

| 30. |

In |

|||

| 31. |

SSA, Annual Statistical Supplement, 2011, Table 6.A4, at https://www.ssa.gov/policy/docs/statcomps/supplement/2011/6a.pdf. For more information of age distribution Social Security benefit claims, see CRS In Focus IF11115, Social Security Benefit Claiming Age. |

|||

| 32. | ||||

| 33. |

Social Security Amendments of 1983: Legislative History and Summary of Provisions, Social Security Bulletin, July 1983, |

|||

| 34. |

The FRA is 67 for workers born in 1960 or later. A worker born in 1960 becomes eligible for reduced retirement benefits at age 62 in 2022 and eligible for full retirement benefits at age 67 in 2027. |

|||

| 35. |

The projections are from the |

|||

| 36. |

CRS Report R44846, The Growing Gap in Life Expectancy by Income: Recent Evidence and Implications for the Social Security Retirement Age. |

|||

| 37. |

Ibid. |

|||

| 38. |

SSA, Office of the Chief Actuary (OCACT), option C1.4, at https://www.ssa.gov/OACT/solvency/provisions/retireage.html.

SSA, OCACT, option C1.6. | |||

| 41.

|

|

SSA, OCACT, option C2.3, at https://www.ssa.gov/OACT/solvency/provisions/retireage.html. The estimate also includes an option of "hardship exemption" with no EEA/NRA change for workers with 25 years of earnings (with four quarters of coverage each year), and average indexed monthly earnings (AIME) less than 250% of the poverty level (wage-indexed from 2013). The hardship exemption is phased out for those with AIME above 400% of the poverty level. |

The Moment of Truth, p. 51. |

|

|

|

||||

|

The report prepared by the U.S. Department of Health and Human Services, Social Security Administration, is reprinted in the Social Security Bulletin. See Increasing the Social Security Retirement Age: Older Workers in Physically Demanding Occupations or Ill Health, Social Security Bulletin, vol. 49, no. 10 (October 1986), at https://www.ssa.gov/policy/docs/ssb/v49n10/v49n10p5.pdf. |

||||

| 42. |

SSA, OCACT, https://www.ssa.gov/OACT/solvency/index.html. |

|||

| 43. |

SSA, OCACT, https://www.ssa.gov/OACT/solvency/provisions/index.html. |