Overview

Since the World Health Organization (WHO) first declared Covid-19 a world health emergency in January 2020, the virus has been detected in over 150 countries and all U.S. states.1 The infection has sickened more than 490,000 people, with thousands of fatalities. More than 80 countries have closed their borders to arrivals from countries with infections, ordered businesses to close, and instructed their populations to self-quarantine.2 After a delayed response, central banks have engaged in a series of interventions in financial markets and national governments are announcing spending initiatives to stimulate their economies.

On March 11, the WHO announced that the outbreak was officially a pandemic, the highest level of health emergency.3 It has become clear that the outbreak is negatively impacting global economic growth.4 The global pandemic is affecting a broad swath of international economic and trade activities, from tourism, medical supplies and other global value chains, consumer electronics, and financial markets to energy, food, and a range of social activities, to name a few. Without a clear understanding of when the global health and economic effects may peak and some understanding of the impact on economies, forecasts must necessarily be considered preliminary. Efforts to reduce social interaction to contain the spread of the virus are disrupting the daily lives of most Americans and adding to the economic costs.

The Organization for Economic Cooperation and Development (OECD) on March 2, 2020, lowered its forecast of global economic growth by 0.5% for 2020 from 2.9% to 2.4%, if the economic effects of the virus peak in the first quarter of 20205 (see Table 1). If the effects of the virus do not peak in the first quarter, as now seems unlikely, the OECD estimates that the global economy could only grow by 1.5% in 2020. On March 23, 2020, OECD Secretary General Angel Gurria stated that:

The sheer magnitude of the current shock introduces an unprecedented complexity to economic forecasting. The OECD Interim Economic Outlook, released on March 2, 2020, made a first attempt to take stock of the likely impact of COVID-19 on global growth, but it now looks like we have already moved well beyond even the more severe scenario envisaged then…. the pandemic has also set in motion a major economic crisis that will burden our societies for years to come.6

Concerns over economic and financial risks have whipsawed financial markets as investors have searched for safe-haven investments, such as the benchmark U.S. Treasury 10-year security, which experienced a historic drop in yield to below 1% on March 3, 2020.7 The yield dropped again to historic levels on March 6, 2020, and March 9, 2020, as investors moved out of stocks and into Treasury securities due in part to concerns over the impact the pandemic would have on economic growth and expectations the Federal Reserve would lower short-term interest rates for a second time in March 2020.8

In overnight trading in various sessions between March 8, and March 24, U.S. stock market indices moved sharply (both higher and lower), triggering automatic circuit breakers designed to halt trading if the indices rise or fall by more than 5% when markets are closed.9 By March 19, 2020, investors were also moving out of corporate and municipal bonds, a traditional safe-haven investment, as firms and other financial institutions attempted to increase their cash holdings. Compared to previous financial market dislocations in which stock market values declined while bond prices rose, stock and bond values fell at the same time in March, 2020 as investors reportedly adopted a "sell everything" mentality to build up cash reserves.10

|

2019 |

2020 |

2021 |

|||

|

November |

Difference |

November |

Difference |

||

|

World |

2.9 |

2.4 |

-0.5 |

3.3 |

0.3 |

|

G20 |

3.1 |

2.7 |

-0.5 |

3.5 |

0.2 |

|

Australia |

1.7 |

1.8 |

-0.5 |

2.6 |

0.3 |

|

Canada |

1.6 |

1.3 |

-0.3 |

1.9 |

0.2 |

|

Euro area |

1.2 |

0.8 |

-0.3 |

1.2 |

0.0 |

|

Germany |

0.6 |

0.3 |

-0.1 |

0.9 |

0.0 |

|

France |

1.3 |

0.9 |

-0.3 |

1.4 |

0.2 |

|

Italy |

0.2 |

0.0 |

-0.4 |

0.5 |

0.0 |

|

Japan |

0.7 |

0.2 |

-0.4 |

0.7 |

0.0 |

|

Korea |

2.0 |

2.0 |

-0.3 |

2.3 |

0.0 |

|

Mexico |

-0.1 |

0.7 |

-0.5 |

1.4 |

-0.2 |

|

Turkey |

0.9 |

2.7 |

-0.3 |

3.3 |

0.1 |

|

United Kingdom |

1.4 |

0.8 |

-0.2 |

0.8 |

-0.4 |

|

United States |

2.3 |

1.9 |

-0.1 |

2.1 |

0.1 |

|

Argentina |

-2.7 |

-2.0 |

-0.3 |

0.7 |

0.0 |

|

Brazil |

1.1 |

1.7 |

0.0 |

1.8 |

0.0 |

|

China |

6.1 |

4.9 |

-0.8 |

6.4 |

0.9 |

|

India |

4.9 |

5.1 |

-1.1 |

5.6 |

-0.8 |

|

Indonesia |

5.0 |

4.8 |

-0.2 |

5.1 |

0.0 |

|

Russia |

1.0 |

1.2 |

-0.4 |

1.3 |

-0.1 |

|

Saudi Arabia |

0.0 |

1.4 |

0.0 |

1.9 |

0.5 |

|

South Africa |

0.3 |

0.6 |

-0.6 |

1.0 |

-0.3 |

Source: OECD Interim Economic Assessment: Coronavirus: The World Economy at Risk, Organization for Economic Cooperation and Development. March 2, 2020, p. 2.

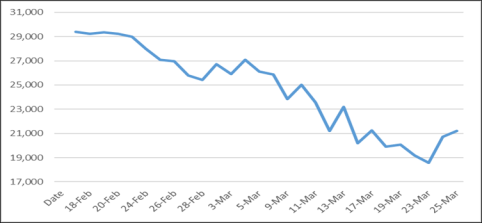

Financial markets from the United States to Asia and Europe are volatile as investors are concerned that the virus is creating a global economic and financial crisis with few metrics to indicate how prolonged and expansive the economic effects may be.11 Between February 14, 2020 and March 23, 2020, for instance, the Dow Jones Industrial Average (DJIA) lost about one-third of its value, as indicated in Figure 1. Expectations that the U.S. Congress would adopt a $2.0 trillion spending package moved the DJIA up by more than 11% on March 24, 2020. For some policymakers, the drop in equity prices has raised concerns that foreign investors might attempt to exploit the situation by increasing their purchases of firms in sectors considered important to national security. Ursula von der Leyen, president of the European Commission, urged EU members to better screen foreign investments, especially in areas such as health, medical research and critical infrastructure.12

Similar to the 2007-2009 global financial crisis, central banks are implementing a series of monetary operations to provide liquidity to their economies. These actions, however, may not be viewed entirely positively by all financial market participants who question the use of policy tools by central banks that are similar to those employed during the 2008-2009 financial crisis, despite the fact that the current and previous crisis are fundamentally different in origin. During the previous financial crisis, central banks intervened to restart credit and spending by banks that had engaged in risky assets. In the current environment, central banks are attempting to address financial market volatility and prevent large-scale corporate insolvencies that reflect the underlying economic uncertainty caused by the pandemic.

|

Figure 1. Dow Jones Industrial Average February 14, 2020 to March 25, 2020 |

|

|

Source: Financial Times. |

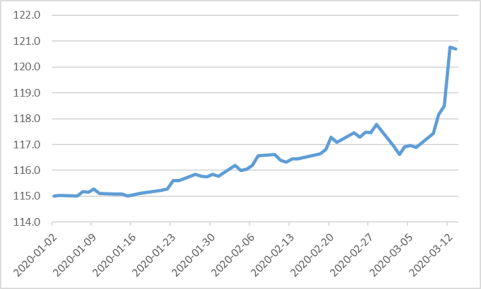

Similar to conditions during the 2007-2009 financial crisis, however, the dollar has emerged as the preferred currency by investors, given its role as the dominant global reserve currency. As indicated in Figure 2, the dollar appreciated more than 3.0% during the period between March 3, and March 13, 2020, reflecting increased international demand for the dollar and dollar-denominated assets. According to a recent survey by the Bank for International Settlements (BIS),13 the dollar accounts for 88% of global foreign exchange market turnover and is key in funding an array of financial transactions, including serving as an invoicing currency facilitating international trade, accounting for two-thirds of central bank foreign exchange holdings, half of non-U.S. banks foreign currency deposits, and two-thirds of non-U.S. corporate borrowings from banks and the corporate bond market.14 As a result, disruptions in the smooth functioning of the global dollar market can have wide-ranging repercussions on international trade and financial transactions. The international role of the dollar also increases pressure on the Federal Reserve essentially to assume the lead role as the global lender of last resort. Similar to conditions during the 2007-2009 financial crisis, the global economy has experienced a period of dollar shortage, requiring the Federal Reserve to take numerous steps to ensure the supply of dollars to the U.S. and global economies. The pandemic is also affecting global politics as world leaders are cancelling international meetings15 and some nations reportedly are stoking conspiracy theories that shift blame to other countries.16

|

Figure 2. U.S. Dollar Trade-Weighted Broad Index, Goods and Services |

|

|

Source: St. Louis Federal Reserve Bank. Notes: January 2006 = 100. |

The challenge for policymakers is to implement targeted policies that address what has been expected to be short-term problems without creating distortions in economies that can outlast the impact of the virus itself. Policymakers, however, are being overwhelmed by the quickly changing nature of the global health crisis that appears to be turning into a global trade and economic crisis whose potential effects on the global economy are rapidly growing. If the economic effects of the pandemic continue to grow, policymakers are likely to give more weight to policies that address the immediate economic effects at the expense of longer-term considerations. Initially, many policymakers felt constrained in their ability to respond to the crisis, with limited flexibility for monetary and fiscal support within conventional standards, given the broad-based synchronized slowdown in global economic growth, especially in manufacturing and trade, which had developed prior to the viral outbreak.

|

Comparing the Current Crisis and the 2008 Crisis Sharp declines in the stock market and broader financial sector turbulence; interest rate cuts and large-scale Federal Reserve intervention; and discussions of massive government stimulus packages have led some observers to compare the current market reaction to that experienced a little over a decade ago. There are similarities and important differences between the current economic crisis and the global financial crisis of 2008/2009. Foremost, the earlier crisis was rooted in structural weakness in the U.S. financial sector. Following the collapse of the U.S. housing bubble, it became impossible for firms to identify demand and hold inventories (across many sectors (construction, retail, etc.). This led to massive oversupply and sharp retail losses which extended to other sectors of the U.S. economy and eventually the global economy. Moreover, financial markets across countries were linked together by credit default swaps. As the crisis unfolded, large numbers of banks and other financial institutions were negatively affected, raising questions about capital sufficiency and reserves. The crisis, then quickly engulfed credit-rating agencies, mortgage lending companies and the real estate industry broadly. Market resolution came gradually with a range of monetary and fiscal policy measures that were closely coordinated at the global level. These were focused on putting a floor under the falling markets, stabilizing banks, and shoring up investor confidence to get spending started again. Starting in September 2007, The Federal Reserve cut interest rates from over 5% in September 2007 to between 0 and 0.25% before the end of the 2008. Once interest rates approached zero, the Fed turned to other so-called "unconventional measures," including targeted assistance to financial institutions, encouraging Congress to pass the Troubled Asset Relief Program (TARP) to prevent the collapse of the financial sector and boost consumer spending. Other measures included swap arrangements between the Federal Reserve and the European Central Bank and smaller central banks, and so-called "quantitative easing" to boost the money supply. On a global level, the United States and other countries tripled the resources of the IMF (from $250 billion to $750 billion) and coordinated domestic stimulus efforts. Unlike the 2008 crisis, the current crisis began as a supply shock. As the global economy has become more interdependent in recent decades, most products are produced as part of a global value chain (GVC), where an item such as a car or mobile device consists of parts manufactured all over the world, and involving multiple border crossings before final assembly. The earliest implications of the current crisis came in January as plant closures in China and other parts of Asia led to interruptions in the supply chain and concerns about dwindling inventories. As the virus spread from Asia to Europe, the crisis switched from supply concerns to a broader demand crisis as the measures being introduced to contain the spread of the virus (social distancing, travel restrictions, cancelling sporting events, closing shops and restaurants, and mandatory quarantine measures) prevent most forms of economic activity from occurring. Thus, unlike the 2008 crisis response, which involved liquidity and solvency-related policy measures to get people spending again, the current crisis did not start as a financial crisis, but could evolve into one if a recovery in economic activity is delayed. While larger firms may have sufficient capital to wait out a crisis, many aspects of the economy (such as restaurants or retail operations) operate on very tight margins and would likely not be able to pay employees after closures lasting more than a few days. Many people will also need to balance child care and work during quarantine or social distancing measures. During this type of crisis, while monetary policy measures play a part -- and the Federal Reserve has once again cut rates to near zero -- they cannot compensate for the physical interaction that the global economy is dependent upon. As a result, fiscal stimulus will likely play a relatively larger role in this crisis in order to prevent personal and corporate bankruptcies during the peak crisis period. Efforts to coordinate U.S. and foreign economic policy measures will also have an important role in mitigating the scale and length of any global economic downtown. |

Estimated Economic Effects

The economic situation remains highly fluid. Uncertainty about the length and depth of the health crisis-related economic effects are fueling perceptions of risk and volatility in financial markets and corporate decision-making. In addition, uncertainties concerning the global pandemic and the effectiveness of public policies intended to curtail its spread are adding to market volatility.

Before the Covid-19 outbreak, the global economy was struggling to regain a broad-based recovery as a result of the lingering impact of growing trade protectionism, trade disputes among major trading partners, falling commodity and energy prices, and economic uncertainties in Europe over the impact of the UK withdrawal from the European Union. Individually, each of these issues presented a solvable challenge for the global economy. Collectively, however, the issues weakened the global economy and reduced the available policy flexibility of many national leaders, especially among the leading developed economies. In this environment, Covid-19 could have an outsized impact. While the level of economic effects will eventually become clearer, the response to the pandemic could have a significant and enduring impact on the way businesses organize their work forces, global supply chains, and how governments respond to a global health crisis.17

The OECD estimates that increased direct and indirect economic costs through global supply chains reduced demand for goods and services, and declines in tourism and business travel mean that, "the adverse consequences of these developments for other countries (non-OECD) are significant."18 Global trade, measured by trade volumes, slowed in the last quarter of 2019 and was expected to decline further in 2020, as a result of weaker global economic activity associated with the pandemic, which is negatively affecting economic activity in various sectors, including airlines, hospitality, ports, and the shipping industry.19

In addition, the OECD argues that China's emergence as a global economic actor marks a significant departure from previous global health episodes. China's growth, in combination with globalization and the interconnected nature of economies through capital flows, supply chains, and foreign investment, magnify the cost of containing the spread of the virus through quarantines and restrictions on labor mobility and travel.20 China's global economic role and globalization mean that trade is playing a role in spreading the economic effects of Covid-19. More broadly, the economic effects of the pandemic are affecting the global economy through three trade channels: (1) directly through supply chains as reduced economic activity is spread from intermediate goods producers to finished goods producers; (2) as a result of a drop overall in economic activity, which reduces demand for goods in general, including imports; and (3) through reduced trade with commodity exporters that supply producers, which, in turn, reduces their imports and negatively affects trade and economic activity of exporters.

Initially, the economic effects of the virus were expected to be short-term supply issues as factory output fell because workers were quarantined to reduce the spread of the virus through social interaction. The drop in economic activity, initially in China, has had international repercussions as firms experienced delays in supplies of intermediate and finished goods through supply chains. Concerns have grown, however, that the virus-related supply shock is creating more prolonged and wide-ranging demand shocks as reduced activity by consumers and businesses lead to a lower rate of economic growth. As demand shocks unfold, businesses experience a decline in activity, reduced profits, and potentially escalating and binding credit and liquidity constraints. While manufacturing firms are experiencing supply chain shocks, reduced consumer activity through social distancing is affecting the services sector of the economy, which accounts for two-thirds of annual U.S. economic output. In this environment, manufacturing and service firms are hoarding cash, which affects market liquidity. In response, central banks have lowered interest rates where possible and expanded lending facilities to provide liquidity to financial markets and to firms potentially facing insolvency.

If the economic effects persist, they can be spread through trade and financial linkages to an ever-broadening group of countries, firms and households. This potentially can further increase liquidity constraints and credit market tightening in global financial markets as firms hoard cash, with negative fallout effects on economic growth. In some financial markets, fund managers reportedly are selling government securities to increase their cash reserves. At the same time, financial markets are factoring in an increase in government bond issuance in the United States and Europe as government debt levels are set to rise to meet spending obligations during an expected economic recession and increased fiscal spending to fight the effects of Covid-19. Unlike the 2008-2009 financial crisis, reduced demand by consumers, labor market issues, and a reduced level of activity among businesses, rather than risky trading by global banks, has led to corporate credit issues and potential insolvency. These market dynamics have led some observers to question if these events mark the beginning of a full-scale global financial crisis.21

Liquidity and credit market issues present policymakers with a different set of challenges than addressing supply-side constraints. As a result, the focus of government policy has expanded from a health crisis to macroeconomic and financial market issues that are being addressed through a combination of monetary, fiscal, and other policies, including border closures, quarantines, and restrictions on social interactions. Essentially, while businesses are attempting to address worker and output issues at the firm level, national leaders are attempting to implement fiscal policies to prevent economic growth from falling sharply by assisting workers and businesses that are facing financial strains, and central bankers are adjusting monetary policies to address mounting credit market issues.

So far, households have not experienced the same kind of loss in wealth they saw during the 2007-2009 financial crisis when the value of their primary residence dropped sharply. Losses in the value of most equity markets in the U.S. Asia, and Europe, however, could affect household wealth, especially retirees living on a fixed income those and others who own equities. Job losses also could result in defaults on mortgage payments, which could have a negative impact on the market for mortgage-backed securities and, in turn, on the availability of funds for mortgages. Investors that trade in mortgage-backed securities reportedly have been reducing their holdings while the Federal Reserve has been attempting to support the market.22 In the current environment, even traditional policy tools, such as monetary accommodation, apparently are not being processed by markets in a traditional manner, with equity market indices displaying heightened, rather than lower, levels of uncertainty following the Federal Reserve's cut in interest rates. Such volatility is adding to uncertainties about what governments can do to address weaknesses in the global economy.

Policy Response

In response to growing concerns over the global economic impact of the pandemic, G-7 finance ministers and central bankers released a statement on March 3, 2020, indicating they will "use all appropriate policy tools" to sustain economic growth.23 The Finance Ministers also pledged fiscal support to ensure health systems can sustain efforts to fight the outbreak.24 In most cases, however, countries have pursued their own divergent strategies, in some cases including banning exports of medical equipment. Following the G-7 statement, the U.S. Federal Reserve (Fed) lowered its federal funds rate by 50 basis points, or 0.5%, to a range of 1.0% to 1.25% due to concerns about the "evolving risks to economic activity of the coronavirus."25 At the time, the cut was the largest one-time reduction in the interest rate by the Fed since the financial crisis of 2008.

After a delayed response, other central banks have begun to follow the actions of the G-7 countries. Most central banks have lowered interest rates and acted to increase liquidity in their financial systems through a combination of measures, including lowering capital buffers and reserve requirements, creating temporary lending facilities for banks and businesses, and easing loan terms. In addition, national governments have adopted various fiscal measures to sustain economic activity. In general, these measures include making payments directly to households, temporarily deferring tax payments, extending unemployment insurance, and increasing guarantees and loans to businesses.

See the Appendix to this report for detailed information about the policy actions by governments.26

The United States

In a sign of growing concern over strains in financial markets and economic growth, the Federal Reserve (Fed) has taken a number of steps to promote economic and financial stability involving the Fed's monetary policy and "lender of last resort" roles. Some of these actions are intended to stimulate economic activity by reducing interest rates and others are intended to provide liquidity to financial markets so that firms have access to needed funding. In announcing its decisions, the Fed indicated that "….The coronavirus outbreak has harmed communities and disrupted economic activity in many countries, including the United States. Global financial conditions have also been significantly affected.27"

Monetary Policy 28

Forward Guidance

Forward guidance refers to Fed public communications on its future plans for short-term interest rates, and it took many forms following the 2008 financial crisis. As monetary policy returned to normal in recent years, forward guidance was phased out. It is being used again today. For example, when the Fed reduced short-term rates to zero on March 15, it announced that it "expects to maintain this target range until it is confident that the economy has weathered recent events and is on track to achieve its maximum employment and price stability goals."

Quantitative Easing

Large-scale asset purchases, popularly referred to as quantitative easing or QE, were also used during the financial crisis. Under QE, the Fed expanded its balance sheet by purchasing securities. Three rounds of QE from 2009 to 2014 increased the Fed's securities holdings by $3.7 trillion.

On March 23, the Fed announced that it would increase its purchases of Treasury securities and mortgage-backed securities (MBS)—including commercial MBS—issued by government agencies or government-sponsored enterprises to "the amounts needed to support smooth market functioning and effective transmission of monetary policy.... " These would be undertaken at the unprecedented rate of up to $125 billion daily during the week of March 23. As a result, the value of the Fed's balance sheet is projected to exceed its post-financial crisis peak of $4.5 trillion. One notable difference from previous rounds of QE is that the Fed is purchasing securities of different maturities, so the effect likely will not be concentrated on long-term rates.

Actions to Provide Liquidity

Reserve Requirements

On March 15, the Fed announced that it was reducing reserve requirements—the amount of vault cash or deposits at the Fed that banks must hold against deposits—to zero for the first time ever. As the Fed noted in its announcement, because bank reserves are currently so abundant, reserve requirements "do not play a significant role" in monetary policy.

Term Repos

The Fed can temporarily provide liquidity to financial markets by lending cash through repurchase agreements (repos) with primary dealers (i.e., large government securities dealers who are market makers). Before the financial crisis, this was the Fed's routine method for targeting the federal funds rate. Following the financial crisis, the Fed's large balance sheet meant that repos were no longer needed, until they were revived in September 2019. On March 12, the Fed announced it would offer a three-month repo of $500 billion and a one-month repo of $500 billion on a weekly basis through the end of the month in addition to the shorter-term repos it had already been offering. These repos would be larger and longer than those offered since September.

Discount Window

In its March 15 announcement, the Fed encouraged banks (insured depository institutions) to borrow from the Fed's discount window to meet their liquidity needs. This is the Fed's traditional tool in its "lender of last resort" function. The Fed also encouraged banks to use intraday credit available through the Fed's payment systems as a source of liquidity.

Foreign Central Bank Swap Lines

Both domestic and foreign commercial banks rely on short-term borrowing markets to access U.S. dollars needed to fund their operations and meet their cash flow needs. But in an environment of strained liquidity, only banks operating in the United States can access the discount window. Therefore, the Fed has standing "swap lines" with major foreign central banks to provide central banks with U.S. dollar funding that they can in turn lend to private banks in their jurisdictions. On March 15, the Fed reduced the cost of using those swap lines and on March 19 it extended swap lines to nine more central banks.

Emergency Credit Facilities for the Nonbank Financial System

In 2008, the Fed created a series of emergency credit facilities to support liquidity in the nonbank financial system. This extended the Fed's traditional role as lender of last resort from the banking system to the overall financial system for the first time since the Great Depression. To create these facilities, the Fed relied on its emergency lending authority (Section 13(3) of the Federal Reserve Act). To date, the Fed has created six facilities—some new, and some reviving 2008 facilities—in response to COVID-19.

- On March 17, the Fed revived the commercial paper funding facility to purchase commercial paper, which is an important source of short-term funding for financial firms, nonfinancial firms, and asset-backed securities (ABS).

- Like banks, primary dealers are heavily reliant on short-term lending markets in their role as securities market makers. Unlike banks, they cannot access the discount window. On March 17, the Fed revived the primary dealer credit facility, which is akin to a discount window for primary dealers. Like the discount window, it provides short-term, fully collateralized loans to primary dealers.

- On March 19, the Fed created the Money Market Mutual Fund Liquidity Facility (MMLF), similar to a facility created during the 2008 financial crisis. The MMLF makes loans to financial institutions to purchase assets that money market funds are selling to meet redemptions.

- On March 23, the Fed created two facilities to support corporate bond markets—the Primary Market Corporate Credit Facility to purchase newly issued corporate debt and the Secondary Market Corporate Credit Facility to purchase existing corporate debt on secondary markets.

- On March 23, the Fed revived the Term Asset-Backed Securities Loan Facility to make nonrecourse loans to private investors to purchase ABS backed by various nonmortgage consumer loans.

Many of these facilities are structured as special purpose vehicles controlled by the Fed because of restrictions on the types of securities that the Fed can purchase. Although there were no losses from these facilities during the financial crisis, assets of the Treasury's Exchange Stabilization Fund have been pledged to backstop any losses on several of the facilities today.

Fiscal Policy

In terms of a fiscal stimulus, Congress H.R. 6074 on March 5, 2020 (P.L. 116-123), to appropriate $8.3 billion in emergency funding to support efforts to fight Covid-19; President Trump signed the measure on March 6, 2020. President Trump also signed on March 18, H.R. 6201 (P.L. 116-127), the Families First Coronavirus Response Act, that provides paid sick leave and free coronavirus testing, expands food assistance and unemployment benefits, and requires employers to provide additional protections for health care workers. Other countries have indicated they will also provide assistance to workers and to some businesses. Congress also is considering other possible measures, including contingency plans for agencies to implement offsite telework for employees, financial assistance to the shale oil industry, a reduction in the payroll tax,29 and extended of the tax filing deadline.30 President Trump has taken additional actions, including:

- Announcing on March 11, 2020, restrictions on all travel from Europe to the United States for 30 days, directed the Small Business Administration (SBA) to offer low-interest loans to small businesses, and directed the Treasury Department to defer tax payments penalty-free for affected businesses.31

- Declaring on March 13, a state of emergency that frees up disaster relief funding to assist state and local governments to address the effects of the pandemic. The President also announced additional testing for the virus, a website to help individuals identify symptoms, increased oil purchases for the Strategic Oil Reserve, and a waiver on interest payments on student loans.32

- Invoking on March 18, 2020, the Defense Production Act (DPA) that gives him the authority to require some U.S. businesses to increase production of medical equipment and supplies that are in short supply.33

On March 19, the Senate introduced a bill, the Coronavirus Aid, Relief, and Economic Security Act (S. 3548), to formally consider President Trump's proposal by providing direct payments to taxpayers, loans and guarantees to airlines and other industries, and assistance for small businesses, actions similar to those of various foreign governments. The bill, set to be adopted March 25, 2020, would:

- Provide funding for $1,200 tax rebates to individuals, with additional $500 payments per qualifying child. The rebate begins phasing out when incomes exceed $75,000 (or $150,000 for joint filers).

- Assist small businesses by providing funding for, forgivable bridge loans; and additional funding for grants and technical assistance; authorizes emergency loans to distressed businesses, including air carriers, and suspends certain aviation excise taxes.

- Create a $367 billion loan program for small businesses, establish a $500 billion lending fund for industries, cities and states, a $150 billion for state and local stimulus funds, and $130 billion for hospitals.

- Increase unemployment insurance benefits, expand eligibility and offer workers an additional $600 a week for four month, in addition to state unemployment programs.

- Establish special rules for certain tax-favored withdrawals from retirement plans; delays due dates for employer payroll taxes and estimated tax payments for corporations; and revise other provisions, including those related to losses, charitable deductions, and business interest.

- Provide additional funding for the prevention, diagnosis, and treatment of COVID-19; limit liability for volunteer health care professionals; prioritize Food and Drug Administration (FDA) review of certain drugs; allow emergency use of certain diagnostic tests that are not approved by the FDA; expand health-insurance coverage for diagnostic testing and requires coverage for preventative services and vaccines; and revise other provisions, including those regarding the medical supply chain, the national stockpile, the health care workforce, the Healthy Start program, telehealth services, nutrition services, Medicare, and Medicaid.

- Temporarily suspend payments for federal student loans and revise provisions related to campus-based aid, supplemental educational-opportunity grants, federal work-study, subsidized loans, Pell grants, and foreign institutions.

- Authorize the Department of the Treasury temporarily to guarantee money-market funds.

For additional information about the impact of Covid-19 on the U.S. economy see CRS Insight IN11235, COVID-19: Potential Economic Effects.34

Europe

To date, European countries have not had the kind of synchronized policy response they developed during the 2008-2009 global financial crisis. Instead, they have used a combination of quarantines and required business closures, travel and border restrictions, tax holidays for businesses, extensions of certain payments and loan guarantees, and subsidies for workers and businesses. The economic effects of the pandemic reportedly are having a significant impact on business activity in Europe, with some indexes falling farther then they had during the height of the financial crisis and others indicating that Europe may well experience a deep economic recession in 2020.35 EU countries have issued travel warnings, banning all but essential travel across borders, raising concerns that even much-needed medical supplies could stall at borders affected by traffic backups.36

The European Commission announced that it was relaxing rules on government debt to allow countries more flexibility in using fiscal policies. The European Central Bank (ECB) announced that it was ready to take "appropriate and targeted measures," if needed. France, Italy, Spain and six other Eurozone countries have argued for creating a "coronabond," a joint common European debt instrument. Similar attempts to create a common Eurozone-wide debt instrument have been opposed by Germany and the Netherland, among other Eurozone members.37 With interest rates already low, however, it indicated that it would expand its program of providing loans to EU banks, or buying debt from EU firms, and possibly lowering its deposit rate further into negative territory in an attempt to shore up the Euro's exchange rate.38 ECB President-designate Christine Lagarde called on EU leaders to take more urgent action to avoid the spread of Covid-19 triggering a serious economic slowdown. The European Commission indicated that it was creating a $30 billion investment fund to address Covid-19 issues.39 In other actions:

- On March 12, 2020, the ECB decided to: (1) expand its longer-term refinance operations (LTRO) to provide low-cost loans to Eurozone banks to increase bank liquidity; (2) extend targeted longer-term refinance operations (TLTRO) to provide loans at below-market rates to businesses, especially small and medium-sized businesses, directly affected by Covid-19; (3) provide an additional €120 billion (about $130 billion) for the Bank's asset purchase program to provide liquidity to firms that was in addition to €20 billion a month it previously had committed to purchasing.40

- On March 13, 2020, financial market regulators in the UK, Italy, and Spain intervened in stock and bond markets to stabilize prices after historic swings in indexes on March 12, 2020.41 In addition, the ECB announced that it would do more to assist financial markets in distress, including altering self-imposed rules on purchases of sovereign debt.42

- Germany's Economic Minister announced on March 13, 2020, that Germany would provide unlimited loans to businesses experiencing negative economic activity (initially providing $555 billion), tax breaks for businesses,43 and export credits and guarantees.44

- On March 18, the ECB indicated that it would: create a €750 billion (about $800 billion) Pandemic Emergency Purchase Program to purchase public and private securities; expand the securities it will purchase to include nonfinancial commercial paper; and ease some collateral standards.45 In announcing the program, President-designate Lagarde indicated that the ECB would, "do everything necessary." In creating the program, the ECB removed or significantly loosened almost all constraints that applied to previous asset-purchase programs, including a self-imposed limit of buying no more one-third of any one country's eligible bonds, a move that should benefit Italy.

- The ECB also indicated that it would make available up to €3 trillion in liquidity through refinancing operations.46 Britain ($400 billion) and France ($50 billion) also announced plans to increase spending to blunt the economic effects of the virus. Recent forecasts indicate that the economic effect of Covid-19 could push the Eurozone into an economic recession in 2020.47

- On March 23, 2020, Germany announced that it would adopt a €750 billion (over $800 billion) package in economic stimulus funding.

The United Kingdom

The Bank of England announced on March 11, 2020, that it would adopt a package of four measures to deal with any economic disruptions associated with Covid-19. The measures include: an unscheduled cut in the benchmark interest rate by 50 basis points (0.5%) to a historic low of 0.25%; reintroduce the Term Funding Scheme for Small and Medium-sized Enterprises (TFSME) that provides banks with over $110 billion for loans at low interest rates; lower banks' countercyclical capital buffer to zero percent, which is estimated to support over $200 billion of bank lending to businesses; and freeze banks' dividend payments.48

UK Chancellor of the Exchequer Rishi Sunak proposed a national budget on March 11, 2020, that includes nearly $3.5 billion in fiscal spending to counter adverse economic effects of the pandemic and includes an increase in statutory sick leave by about $2.5 billion in funds to small and medium businesses to provide up to 14 days of sick leave for affected employees. The plan also proposes to give affected workers up to 80% of their salary up to £2,500 a month (about $2,800) if they are laid off. Some estimates indicate that UK spending to support its economy could rise to about $60 billion this year.49 Prime Minister Johnson also announced that all pubs, cafés, restaurants, theatres, cinemas, nightclubs, gyms and leisure centers would be closed.50 Part of the fiscal spending package includes open-ended funding for the National Health Service (NHS), $6 billion in emergency funds to the NHS, $600 million hardship fund to assist vulnerable people, and tax cuts and tax holidays for small businesses in certain affected sectors.51 The Bank of England also reduced its main interest rate and supplied the financial markets with additional liquidity.52

Japan

The Bank of Japan, with already-low interest rates, injected $4.6 billion in liquidity into Japanese banks to provide short-term loans for purchases of corporate bonds and commercial paper and twice that amount into exchange traded funds to aid Japanese businesses. The Japanese government also pledged to provide wage subsidies for parents forced to take time off due to school closures.53 On March 24, 2020, Japan announced that the Summer Olympics set to take place in Tokyo would be postponed by a year, delaying an expected boost to the Japanese economy that was expected from the event.

China

According to a recent CRS InFocus, 54 China's economic growth could go negative in the first quarter of 2020 and fall below 5% for the year, with more serious effects if the outbreak continues. In early February, China's central bank pumped $57 billion into the banking system, capped banks' interest rates on loans for major firms, and extended deadlines for banks to curb shadow lending. The central bank has been setting the reference rate for China's currency stronger than its official close rate to keep it stable. On March 13, 2020, The People's Bank of China announced that it would provide $78.8 billion in funding, primarily to small businesses, by reducing bank's reserve requirements.55

The International Monetary Fund (IMF) is providing funding to poor and emerging market economies that are short on financial resources.56 If the economic effects of the virus persist, countries may need to be proactive in coordinating fiscal and monetary policy responses, similar to actions taken by of the G-20 following the 2008-2009 global financial crisis.

Multilateral Response

International Monetary Fund

The IMF initially announced that it is making available about $50 billion for the global crisis response.57 Following a G20 ministerial call on March 23, IMF Managing Director Kristalina Georgieva announced that the Fund stands ready to deploy all of its $1trillion capacity. The Fund is also exploring options to quickly raise financing foremost of which is finalizing agreement on a 2019 agreement to renew and augment the IMF's New Arrangements to Borrow (NAB), a credit line that augments IMF quota resources. Other options to increase IMF resources include a new allocation of special drawing rights (SDRs), sale of IMF gold holdings, selling IMF bonds, developing an expanded network of central bank swap arrangements centered at the IMF.

For low-income countries, the IMF is providing rapid-disbursing emergency financing of up to $10 billion (50% of quota of eligible members) that can be accessed without a full-fledged IMF program. Other IMF members can access emergency financing through the Fund's Rapid Financing Instrument (RFI). This facility could provide about $40 billion for emerging markets facing fiscal pressures from COVID-19. Separate from these resources, the IMF has a Catastrophe Containment and Relief Trust (CCRT), which provides eligible countries with up-front grants for relief on IMF debt service falling due. The CCRT was used during the 2014 Ebola outbreak, but is now underfunded, according to IMF Managing Director Georgieva with just over $200 million available against possible needs of over $1 billion. 58 On March 11, 2020, the United Kingdom announced that it will contribute £150 million (about $170 million) to the CCRT. To date, the United States has not contributed to the CCRT.59

World Bank and Regional Development Banks

The World Bank announced that it is making up to $12 billion in financing ($8 billion of which is new) immediately available to help impacted developing countries.60 This support comprises up to $2.7 billion in new financing from the International Bank for Reconstruction and Development (IBRD), the World Bank's market-rate lending facility for middle-income developing countries, and $1.3 billion from the International Development Association (IDA), the World Bank's concessional facility for low-income countries. In addition, the Bank is reprioritizing $2 billion of the Bank's existing portfolio. The International Finance Corporation (IFC), the Bank's private-sector lending arm is making available up to $6 billion. According to the Bank, support will cover a wide range of activities, including strengthening health services and primary health care, bolstering disease monitoring and reporting, training front line health workers, encouraging community engagement to maintain public trust, and improving access to treatment for the poorest patients.

Several years ago, the World Bank introduced pandemic bonds, a novel form of catastrophe financing.61 The Bank sold two classes of bonds worth $320 million in a program designed to provide financing to developing countries facing an acute epidemic crisis if certain triggers are met. Once these conditions are met, bondholders no longer receive interest payments on their investments, the money is no longer repaid in full, and funds are used to support the particular crisis. In the case of Covid-19, for the bonds to be triggered, the epidemic must be continuing to grow 12 weeks after the first day of the outbreak. Critics have raised a range of concerns about the bonds, arguing that the terms are too restrictive and that the length of time needs to be shortened before triggering the bonds.62 Others stress that the proposal remains valid – shifting the cost of pandemic assistance from governments to the private sector, especially in light of the failure of past efforts to rally donor support to establish multilateral pandemic funds.

The Asian Development Bank (ADB) has approved a total of $4 million to help developing countries in Asia and the Pacific.63 Of the total, $2 million is for improving the immediate response capacity in Cambodia, China, Laos, Myanmar, Thailand, and Vietnam; $2 million will be available to all ADB developing member countries in updating and implementing their pandemic response plans. The ADB also provided a private sector loan of up to $18.6 million to Wuhan-based Jointown Pharmaceutical Group Co. Ltd. to enhance the distribution and supply of essential medicines and protective equipment.

International Economic Cooperation

On March 16, 2020, the leaders of the G-7 countries (Canada, France, Germany, Italy, Japan, the United Kingdom, and the United States) held an emergency summit by teleconference to discuss and coordinate their policy responses to the economic fallout from the global spread of Covid-19. In the joint statement released by the G-7 leaders after the emergency teleconference summit, the leaders stressed they are committed to doing "whatever is necessary to ensure a strong global response through closer cooperation and enhanced cooperation of efforts."64 The countries pledged to coordinate research efforts, increase the availability of medical equipment; mobilize "the full range" of policy instruments, including monetary and fiscal measures as well as targeted actions, to support workers, companies, and sectors most affected by the spread of Covid-19; task the finance ministers to coordinate on a weekly basis, and direct the IMF and the World Bank Group, as well as other international organizations, to support countries worldwide as part of a coordinated global response.65

News reports indicate that Saudi Arabia, the 2020 chair of the G-20, intends to call an emergency G-20 summit in coming days.66 The G-20 is a broader group of economies, including the G-7 countries and several major emerging markets.67 During the global financial crisis, world leaders decided that henceforth the G-20 would be the premiere forum for international economic cooperation. Some analysts have been surprised that the G-7 has been in front of the G-20 in responding to Covid-19, while other analysts have questioned whether the larger size and diversity of economies in the G-20 can make coordination more difficult.68

Analysts are hopeful that the recent G-7 summit, and movement towards a G-20 summit, will mark a shift towards greater international cooperation at the highest (leader) levels in combatting the economic fallout from the spread of Covid-19.69 An emergency meeting of G-7 finance ministers on March 3, 2020, fell short of the aggressive and concrete coordinated action that investors and economists had been hoping for, and U.S. and European stock markets fell after the meeting.70 More generally, governments have been divided over the appropriate response and in some cases have acted unilaterally, particularly when closing borders and imposing export restrictions on medical equipment and medicine. Some experts argue that a large, early, and coordinated response is needed to address the economic fallout from Covid-19, but several concerns loom about the G-20's ability to deliver.71 Their concerns focus on the Trump Administration's prioritization of an "America First" foreign policy over one committed to multilateralism; the 2020 chair of the G-20, Saudi Arabia, is embroiled in its own domestic political issues and oil price war; and U.S.-China tensions make G-20 consensus more difficult.

Meanwhile, international organizations including the IMF and multilateral development banks, have tried to forge ahead with economic support given their current resources. Additionally, the Financial Stability Board (FSB), an international body including the United States that monitors the global financial system and makes regulations to ensure stability, released a statement on March 20, 2020 that its members are actively cooperating to maintain financial stability during market stress related to Covid-19.72 The FSB is encouraging governments to use flexibility within existing international standards to provide continued access to funding for market participants and for businesses and households facing temporary difficulties from Covid-19, while noting that many FSB members have already taken action to release available capital and liquidity buffers.

Estimated Effects on Developed and Major Economies

Among most developed and major developing economies, economic growth at the beginning of 2020 was tepid, but still was estimated to be positive. Countries highly dependent on trade—Canada, Germany, Italy, Japan, Mexico, and South Korea—and commodity exporters are now projected to be the most negatively affected by the slowdown in economic activity associated with the virus.73 In addition, travel bans and quarantines are taking a heavy economic toll on a broad range of countries. The OECD notes that production declines in China have spillover effects around the world given China's role in producing computers, electronics, pharmaceuticals and transport equipment, and as a primary source of demand for many commodities.74

In early January 2020, before the coronavirus outbreak, economic growth in developing economies as a whole was projected by the International Monetary Fund (IMF) to be slightly more positive than in 2019. This outlook was based on progress being made in U.S.-China trade talks that were expected to roll back some tariffs and an increase in India's rate of growth. Growth rates in Latin America and the Middle East were also projected to be positive in 2020.75 These projections likely will be revised downward due to the slowdown in global trade associated with Covid-19, lower energy and commodity prices, an increase in the foreign exchange value of the dollar, and other secondary effects that could curtail growth. Commodity exporting countries, in particular, likely will experience a greater slowdown in growth than forecasted in earlier projections as a result of a slowdown on trade with China and lower commodity prices.

Emerging Markets

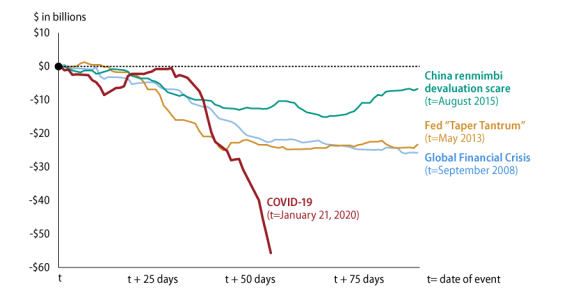

The combined impact of Covid-19, an increase in the value of the dollar, and an oil price war between Saudi Arabia and Russia are hitting developing and emerging economies hard. Not all of these countries have the resources or policy flexibility to respond effectively. According to figures compiled by the Institute for International Finance (IIF), cumulative capital outflows from developing countries since January 2020 are double the level experienced during the 2008/2009 crisis and substantially higher than recent market events (Figure 3).76

|

Figure 3. Capital Flows to Emerging Markets in Global Shocks |

|

|

Source: : Original graphic and data from International Institute for Finance using data from Haver. Edited by CRS for clarification. |

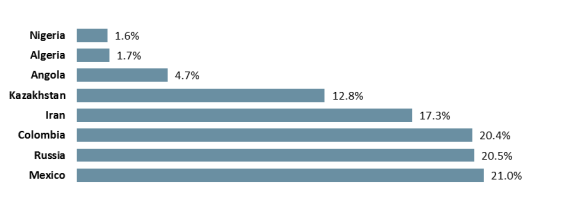

The impact of the price war and lower energy demand associated with a Covid-19-related economic slowdown is especially hard on oil and gas exporters, some of whose currencies are at record lows (Figure 4). Oil importers, such as South Africa and Turkey, have also been hit hard; South Africa's rand has fallen 18%77 against the dollar since the beginning of 2020 and the Turkish lira has lost 8.5%.78

Depending on individual levels of foreign exchange reserves and the duration of the capital flow slowdown, some countries may have sufficient buffers to weather the slowdown, while others will likely need to make some form of current account adjustment (reduce spending, raise taxes, etc.). Several countries, such as Iran and Venezuela, have already asked the IMF for financial assistance and others are likely to follow.79 (Venezuela's request was quickly rebuffed due to disagreement among the IMF membership over who is recognized as Venezuela's legitimate leader: Nicolás Maduro or Juan Guaidó.80)

|

Figure 4. Depreciation Against the Dollar Since Jan. 1, 2020 |

|

|

Source: Created by CRS. Data from Bloomberg. |

Looming Debt Crises

Covid-19 could trigger a wave of defaults around the world.81 In Q3 2019—before the outbreak of Covid-19—global debt levels reached an all-time high of nearly $253 trillion, about 320% of global GDP.82 About 70% of global debt is held by advanced economies and about 30% is held by emerging markets. Globally, most debt is held by nonfinancial corporations (29%), governments (27%) and financial corporations (24%), followed by households (19%). Debt in emerging markets has nearly doubled since 2010, primarily driven by borrowing from state-owned enterprises.

High debt levels make borrowers vulnerable to shocks that disrupt revenue and inflows of new financing. The disruption in economic activity associated with Covid-19 is a wide-scale exogenous shock that will make it significantly more difficult for many private borrowers (corporations and households) and public borrowers (governments) around the world to repay their debts. Covid-19 has hit the revenue of corporations in a range of industries: factories are ceasing production, brick-and-mortar retail stores and restaurants are closing, commodity prices have plunged (Bloomberg commodity price index—a basket of oil, metals, and food prices—has dropped 27% since the start of the year and is now at its lowest level since 1986), and overseas and in some cases domestic travel is being curtailed.83

Households are facing a rapid increase in unemployment and, in many developing countries, a decline in remittances. With fewer resources, corporations and households may default on their debts, absent government intervention. These defaults will result in a decline in bank assets, making it difficult for banks to extend new loans during the crisis or, more severely, creating solvency problems for banks. Meanwhile, many governments are dramatically increasing spending to combat the pandemic, and are likely to face sharp reductions in revenue, putting pressure on public finances and raising the likelihood of sovereign (government) defaults. Debt dynamics are particularly problematic in emerging economies, where debt obligations denominated in foreign currencies (usually U.S. dollars). Many emerging market currencies have depreciated since the outbreak of the pandemic, raising the value of their debts in terms of local currency.

Governments will face difficult choices if there is a widespread wave of defaults. Most governments have signaled a commitment to or already implemented policies to support those economically impacted by the pandemic. These governments face decisions about the type of assistance to provide (loans versus direct payments), the amount of assistance to provide, how to allocate rescue funds, and what conditions if any to attach to funds. In terms of defaults by governments (sovereign defaults), emergency assistance is generally provided by the IMF, and sometimes paired with additional rescue funds from other governments on a bilateral basis. The IMF and other potential donor countries will need to consider whether the IMF has adequate resources to respond to the crisis, how to allocate funding if the demand for funding exceeds the amount available, what conditions should be attached to rescue funding, and whether IMF programs should be paired with a restructuring of the government's debt ("burden sharing" with private investors).

Other Affected Sectors

Public concerns over the spread of the virus have led to self-quarantines, reductions in airline and cruise liner travel, the closing of such institutions as the Louvre, and the rescheduling of theatrical releases of movies, including the sequel in the iconic James Bond series (titled, "No Time to Die").84 School closures are affecting millions of children worldwide, challenging parental leave policies.85 Other countries are limiting the size of public gatherings.

Some businesses are considering new approaches to managing their workforces and work methods. These techniques build on, or in some places replace, such standard techniques as self-quarantines and travel bans. Some firms are adopting an open-leave policy to ensure employees receive sick pay if they are, or suspect they are, infected. Other firms are adopting paid sick leave policies to encourage sick employees to stay home and are adopting remote working policies.86 Microsoft and Amazon have instructed all of their Seattle-based employees to work from home until the end of March 2020.87

The drop in business and tourist travel is causing a sharp drop in scheduled airline flights by as much as 10%; airlines are estimating they could lose $113 billion in 2020 (an estimate that could prove optimistic given the Trump Administration's announced restrictions on flights from Europe to the United States and the growing list of countries that ae similarly restricting flights),88 while airports in Europe estimate they could lose $4.3 billion in revenue due to fewer flights.89 Industry experts estimate that many airlines will be in bankruptcy by May 2020 under current conditions as a result of travel restrictions imposed by a growing number of countries.90 The loss of Chinese tourists is another economic blow to countries in Asia and elsewhere that have benefitted from the growing market for Chinese tourists and the stimulus such tourism has provided.

The decline in industrial activity has reduced demand for energy products such as crude oil, causing prices to drop sharply, which negatively affects energy producers, renewable energy producers, and electric vehicle manufacturers, but generally is positive for consumers and businesses. Saudi Arabia is pushing other OPEC (Organization of the Petroleum Exporting Countries) members collectively to reduce output by 1.5 million barrels a day to raise market prices. U.S. shale oil producers, who are not represented by OPEC, support the move to raise prices.91 An unwillingness by Russia to agree to output reductions added to other downward pressures on oil prices and caused Saudi Arabia to engage in a price war with Russia that has driven oil prices below $30 per barrel, well below the estimated $50 per barrel break-even point for most oil producing countries.92 In 2019, low energy prices combined with high debt levels reportedly caused U.S. energy producers to reduce their spending on capital equipment, reduced their profits and, in some cases, led to bankruptcies.93 Reportedly, in late 2019 and early 2020, bond and equity investors, as well as banks, reduced their lending to shale oil producers and other energy producers that typically use oil and gas reserves as collateral.94

Disruptions to industrial activity in China reportedly are causing delays in shipments of computers, cell phones, toys, and medical equipment.95 Factory output in China, the United States, Japan, and South Korea all declined in the first months of 2020.96 Reduced Chinese agricultural exports, including to Japan, are leading to shortages in some commodities. In addition, numerous auto producers are facing shortages in parts and other supplies that have been sourced in China. Reductions in international trade have also affected ocean freight prices. Some freight companies argue that they could be forced to shutter if prices do not rebound quickly.97 Disruptions in the movements of goods and people reportedly are causing some companies to reassess how international they want their supply chains to be.98 According to some estimates, nearly every member of the Fortune 1000 is being affected by disruptions in production in China.99

Conclusions

The quickly evolving nature of the Covid-19 crisis creates a number of issues that make it difficult to estimate the full cost to global economic activity. These issues include, but are not limited to:

- How long will the crisis last?

- How many workers will be affected both temporarily and permanently?

- How many countries will be infected and how much economic activity will be reduced?

- When will the economic effects peak?

- How much economic activity will be lost as a result of the viral outbreak?

- What are the most effective monetary and fiscal policies at the national and global level to address the crisis?

- What temporary and permanent effects will the crisis have on how businesses organize their work forces?

- Many of the public health measures taken by countries such as Italy, Taiwan, South Korea, Hong Kong, and China have sharply impacted their economies (with plant closures, travel restrictions, and so forth). How are the tradeoffs between public health and the economic impact of policies to contain the spread of the virus being weighed?

Appendix. Table A-1. Select Measures Implemented and Announced by Major Economies in Response to Covid-19

|

U.S. Federal Reserve March 3: Cut the target range for the federal funds rate by 0.5 percentage point. March 12: Expanded reverse repo operations, adding $1.5 trillion of liquidity to the banking system. March 15: Cut the target range for the federal funds rate by a full percentage point to a range of 0.00% to 0.25% and restarted quantitative easing with the purchase of at least $500 billion in Treasury securities and $200 billion in mortgage-backed securities. March 16: Increased reverse repo operations by another $500 billion. March 17: U.S. Treasury Secretary Mnuchin approved the Federal Reserve's creation of a "Commercial Paper Funding Facility," (CPFF) through March 17, 2021, which will allows the Fed to create a corporation which can purchase commercial paper, short-term, unsecured loans made by businesses for everyday expenses and authorized up to $10 billion from the Treasury to help cover loan losses incurred under this program. March 17: Relaunched the Primary Dealer Credit Facility (PDCF) for at least six months. Starting March 20, the PDCF will offer short-term loans to banks secured by collateral such as municipal bonds or investment-grade corporate debt. March 18: Launched the Money Market Mutual Fund Liquidity Facility (MMLF) through the end of September, a new program to lend money to banks so they can purchase assets from money market funds. Treasury is offering up to $10 billion to cover loan losses the Fed incurs from the program. March 23: Announced a series of measures designed to stabilize markets, enhance liquidity and stimulate growth. The measures included the roll out of 2 new facilities, the Primary Market Corporate Credit Facility (PMCCF) for new bond and loan issuance and the Secondary Market Corporate Credit Facility (SMCCF) to provide liquidity for outstanding corporate bonds. The FOMC removed its caps on planned QE purchases and will now purchase Treasuries and agency mortgage-backed securities "in the amounts needed to support smooth market functioning and effective transmission of monetary policy to broader financial conditions and the economy." U.S. Congress March 5: Passed, and the President signed, a bill providing $8.3 billion in emergency funding for federal agencies to respond to the coronavirus outbreak (H.R. 6074: Coronavirus Preparedness and Response Supplemental Appropriations Act 2020). March 13: The House of Representatives passed a coronavirus response package (H.R. 6201; P.L. 116-127, Families First Coronavirus Response Act); measure was signed by President Trump on March 18, 2020. March 19: The Senate introduced the Coronavirus Aid, Relief, and Economic Security Act (S. 3548) to provide $2.0 trillion in assistance to businesses and workers. Trump Administration March 13: President Trump declared a state of emergency, allowing the Federal Government to distribute up to $50 billion in aid to states, cities, and territories. March 17: The Internal Revenue Service postponed the April 15 tax-payment deadline for 90 days and will waive interest and penalties. (The extension and waiver is available only to individuals and corporations that owe $1 million or $10 million or less, respectively.) March 17: Administration officials begin negotiations with Members of Congress on a third stimulus package. |

|

|

Argentina |

Central Bank of Argentina March 19: Indicated that it would lower reserve requirements for banks that extended special credit lines to small and medium-sized enterprises at a maximum annual interest rate of 24% in a bid to offset the impact of coronavirus. Government of Argentina March 19: Announced a fiscal stimulus package of 700 billion pesos ($11.3 billion) to mitigate the impact of the COVID-19 and support the economy. The main measures include providing credit to productive activities (350 billion pesos), increasing public investments (100 billion pesos), and waiving payroll taxes for firms affected by the coronavirus. |

|

Armenia |

March 17: The Central Bank of Armenia cut its key refinancing rate by 25 basis points to 5.25% from 5.5% due to the effects of the coronavirus outbreak on the economy. |

|

Australia |

Reserve Bank of Australia (RBA) March 3: Cut its benchmark interest rate by 25 basis points to 0.5% due to the significant effect of the coronavirus outbreak on the Australian economy. March 19: Cut its cash rate by 25 basis points to 0.25% and and introduced a series of measures: (1) targeting the 3-year government bond yield at 0.25% via purchases in the secondary market, (2) providing a three-year term funding facility to authorized deposit-taking institutions worth at least AU$90 billion at a fixed rate of 0.25%, aiming to support credit to small and medium-sized enterprises, (3) fixing the exchange settle balances at the central bank at 10 basis points. It will also continue to provide liquidity by conducting one-month and three-month repo operations until further notice. Longer-term repo operations of six-month maturity or longer would be undertaken at least weekly. The central bank also set out forward guidance, saying that it will not increase the cash rate until progress is made towards full employment and confident that inflation is sustainably within its target band. March 19: Through its daily money market operation, it has injected cash into the banking system (through repurchasing agreements), aiming to ease liquidity constraints in the stressed bond market: AU$12.7 billion (March 19), AU$10.7 billion (March 18), AU$8.8 (March 17), AU$5.9 billion (March 16), and AU$8.8 (March 13). Government of Australia March 12: The government announced a AU$17.6 billion ($11.4 billion) stimulus package that includes support for business investment, cash flow assistance for small and medium sized business and employees, and household stimulus payments. March 16: The Australian Securities and Investments Commission ordered large equity market participants to reduce their number of executed trades by 25% from the levels executed on March 13, 2020, until further notice. March 19: Announced that the Australian Office of Financial Management (AOFM) will be provided with an investment capacity of $15 billion to enable smaller lenders to continue supporting Australian consumers and small businesses. (AOFM will be able to purchase residential mortgage backed securities and invest in a range of other asset backed securities and warehouse facilities over the next 12 months.) March 22: Announced an additional AU$66.4 billion ($38.5 billion) fiscal package, which extends income support measures for existing welfare and newly unemployed workers, and boosted previously announced measures for businesses such as cash flow and wage subsidies. The government is also expected to give local businesses AU$100,000 if the company has a turnover of less than AU$50 million each year and underwrite 50% of up AU$40 billion in loans offered by local lenders to small and medium sized companies. |

|

Austria |

March 14: The government set up an initial 4 billion euro ($4.4 billion) "corona crisis fund" to cover, among other things, benefits for affected workers, as well as bridge loans and credit guarantees to shore up businesses' liquidity. March 18: The government announced that it will spend up to 38 billion euros ($42 billion) to secure jobs and keep companies afloat, and it will provide another 9 billion euros in guarantees and warranties, 15 billion euros in emergency aid, and 10 billion euros in tax deferrals. |

|

Bosnia and Herzegovina |

March 17: The prime minister met with the IMF Resident Representative in Bosnia to request assistance from the IMF. The IMF indicated that it may extend a 165 million euros ($181 million) loan to Bosnia under a Rapid Financing Instrument (RFI) to finance the increasing costs sustained by the country's health system in combating COVID-19. |

|

Brazil |

Central Bank of Brazil March 18: Cut its benchmark interest rate by 50 basis points to 3.75% to cushion the economic blow of the coronavirus pandemic. It also sold $830 million in two rounds of spot foreign exchange intervention and announced a repurchase program for dollar-denominated sovereign bonds held by Brazilian banks, which will be carried out in conjunction with the Treasury. Government of Brazil March 16: Announced a fiscal stimulus package of 147.1 billion reais ($28.6 billion) to mitigate the impact of the coronavirus and boost the economy. It does not contain new money, but is a range of measures that aim to protect the most vulnerable population through social assistance payments (83.4 billion reais), support domestic companies and defer business taxes (59.4 billion reais), and increase investments in healthcare to combat the coronavirus (4.5 billion reais). The government also announced a 3.1 billion reais boost to the "Bolsa Família" assistance for some of Brazil's poorest families. March 16: The National Monetary Council (CMN) approved the measures that will allow banks to (1) increase loans and offer better terms to firms and households over the next six months and (2) extend certain loan maturities for the next six months. It also lowered capital requirements for banks. |

|

Canada |

Bank of Canada March 4: Lowered its target for the overnight rate by 50 basis points to 1.25% (setting the bank rate to 1.5% and the deposit rate to 1%). March 12: Announced that it will broaden the scope of the current Government of Canada bond buyback program and temporarily add new Term Repo operations. March 13: Lowered its benchmark overnight rate to 1.25% from 1.75% in response to the epidemic. March 13: Announced its intention to launch the Bankers' Acceptance Purchase Facility (BAPF), starting the week of March 23, 2020, in an effort to support the continuous functioning of financial markets; it will conduct secondary market purchases of one-month Bankers' Acceptances issued and guaranteed by any Canadian bank and of sufficiently high quality. BAPF operations will be conducted weekly with the purchase amount and reserve rate being adjusted to reflect market conditions. (For the first operation, the Bank of Canada will purchase up to $10 billion of one-month Bankers' Acceptances with a reserve rate of the overnight index swap rate plus 20 basis points.) March 16: Announced that it will broaden eligible collateral for its term repo facility and increase purchases of mortgage-backed securities (Canada Mortgage Bonds). Canadian Government March 6: Announced an investment of CA$27 million to fund coronavirus research and accelerate the development, testing, and implementation of measures to deal with the COVID-19 outbreak. March 11: Unveiled CA$1 billion ($750 million) in funding for vaccine research and health measures. March 13: Established a Business Credit Availability Program (BCAP) to support financing in the private sector through the Business Development Bank of Canada (BDC) and Export Development Canada (EDC); it will allow BDC and EDC to provide more than $10 billion of additional support to businesses. March 13: The Office of the Superintendent of Financial Institutions (OSFI) lowered the Domestic Stability Buffer requirement for domestic systemically important banks by 1.25% of risk weighted assets; it will increase the lending capacity of Canada's large banks and support the supply of credit to the economy by more than CA$300 billion. |

|

Chile |

Central Bank of Chile March 16: Cut its benchmark rate by 75 basis points to 1% on Monday and announced measures to inject liquidity, including allocating $4 billion to purchase inflation-linked bank bonds and providing additional credit to banks. Government of Chile March 19: The government announced a stimulus package of $11.75 bn to mitigate the negative economic impact of the outbreak of coronavirus and civil unrest. The measures include extending unemployment insurance to those who are sick or unable to work from home, delaying tax payments for small businesses, a cash bonus for approximately 2 million workers who lack formal employment, and emergency funds for municipalities. |

|

China |

People's Bank of China (PBOC) February 3: Expanded reverse repo operations by $174 billion; added another $71 billion on February 4. February 16: Cut the one-year medium-term lending facility rate by 10 basis points. February 20: Cut the one-year and five-year prime rates by 10 and 5 basis points, respectively. March 13: Lowered bank reserve requirements, freeing up about $79 billion to be lent out. PRC Government February: Asked banks to extend the terms of business loans and commercial landlords to reduce rents. February 24: The Asian Infrastructure Investment Bank (AIIB) contributed $1 million in medical equipment to help China control the spread of COVID-19. February 27: Announced a number of tax relief measures to tackle coronavirus disruption, including a temporary reduction its value-added tax (VAT) and the elimination of VAT on medical, catering, accommodation, hairdressing, and laundry services as well as on masks and protective clothing. March: Earmarked $15.9 billion to fight the epidemic. March 21: Announced that it would cut fees on a large scale to stimulate private-sector investment and also accelerate the development of "new infrastructure" to help spur the economy. March 19: Is reportedly considering a fiscal stimulus package worth trillions of yuan to revive the economy amid the coronavirus pandemic. The ramped-up spending will aim to spur infrastructure investment, backed by as much as 2.8 trillion yuan ($394 billion) of local government special bonds. |

|

Colombia |

Central Bank of Colombia March 18: The Central Bank of Colombia announced a $400 million dollar to peso swap to take place on March 19, and that it would increase the resources available to financial institutions and ease rules on which institutions can have access to funds. Government of Colombia March 18: The government announced that it has 14.8 trillion pesos ($3.65 billion) to spend on emergency measures to ease the economic fallout from coronavirus, but it will not take on additional debt to finance the efforts (12.1 trillion pesos will come from the country's savings programs). It will initially spend 1 trillion pesos on the healthcare system and 500 billion pesos on additional payments to social welfare programs for families, young people and the elderly, accelerate a plan to return value added tax to the neediest Colombians from April, and make 48 trillion pesos available to give credit guarantees to small and medium-sized businesses and households. |

|

Congo-Kinshasa (Democratic Republic of the Congo) |