Introduction

The Federal Housing Administration (FHA) is an agency of the Department of Housing and Urban Development (HUD) that insures private mortgage lenders against the possibility of borrowers defaulting on certain mortgage loans.1 If a mortgage borrower defaults on a mortgage—that is, does not repay the mortgage as promised—and the home goes to foreclosure, FHA is to pay the lender the remaining amount that the borrower owes. FHA insurance protects the lender, rather than the borrower, in the event of borrower default; a borrower who defaults on an FHA-insured mortgage will still experience the consequences of foreclosure. To be eligible for FHA insurance, the mortgage must be originated by a lender that has been approved by FHA, and the mortgage and the borrower must meet certain criteria.

FHA is one of three government agencies that provide insurance or guarantees on certain home mortgages made by private lenders, along with the Department of Veterans Affairs (VA) and the United States Department of Agriculture (USDA).2 Of these federal mortgage insurance programs, FHA is the most broadly targeted. Unlike VA- and USDA-insured mortgages, the availability of FHA-insured mortgages is not limited by factors such as veteran status, income, or whether the property is located in a rural area. However, the availability or attractiveness of FHA-insured mortgages may be limited by other factors, such as the maximum mortgage amount that FHA will insure, the fees that it charges for insurance, and its eligibility standards.

This report provides background on FHA's history and market role and an overview of the basic eligibility and underwriting criteria for FHA-insured home loans. It also provides data on the number and dollar volume of mortgages that FHA insures, along with data on FHA's market share in recent years. It does not go into detail on the financial status of the FHA mortgage insurance fund. For information on FHA's financial position, see CRS Report R42875, FHA Single-Family Mortgage Insurance: Financial Status of the Mutual Mortgage Insurance Fund (MMI Fund).

Background

History

The Federal Housing Administration was created by the National Housing Act of 1934,3 during the Great Depression, to encourage lending for housing and to stimulate the construction industry.4 Prior to the creation of FHA, few mortgages exceeded 50% of the property's value and most mortgages were written for terms of five years or less. Furthermore, mortgages were typically not structured to be fully repaid by the end of the loan term; rather, at the end of the five-year term, the remaining loan balance had to be paid in a lump sum or the mortgage had to be renegotiated. During the Great Depression, lenders were unable or unwilling to refinance many of the loans that became due. Thus, many borrowers lost their homes through foreclosure, and lenders lost money because property values were falling. Lenders became wary of the mortgage market.

FHA institutionalized a new idea: 20-year mortgages on which the loan would be completely repaid at the end of the loan term. If borrowers defaulted, FHA insured that the lender would be fully repaid. By standardizing mortgage instruments and setting certain standards for mortgages, the creation of FHA was meant to instill confidence in the mortgage market and, in turn, help to stimulate investment in housing and the overall economy. Eventually, lenders began to make long-term mortgages without FHA insurance if borrowers made significant down payments. Over time, 15- and 30-year mortgages have become standard mortgage products.

When the Department of Housing and Urban Development (HUD) was created in 1965, FHA became part of HUD. Today, FHA is intended to facilitate access to affordable mortgages for some households who otherwise might not be well-served by the private market. Furthermore, it facilitates access to mortgages during economic or mortgage market downturns by continuing to insure mortgages when the availability of mortgage credit has otherwise tightened. For this reason, it is said to play a "countercyclical" role in the mortgage market—that is, it tends to insure more mortgages when the mortgage market or overall economy is weak, and fewer mortgages when the economy is strong and other types of mortgages are more readily available.

Current Role

Facilitating Access to Mortgage Credit

Some prospective homebuyers may have the income to sustain monthly mortgage payments but lack the funds to make a large down payment or otherwise have difficulty obtaining a mortgage. Borrowers with small down payments, weaker credit histories, or other characteristics that increase their credit risk might find it difficult to obtain a mortgage at an affordable interest rate or to qualify for a mortgage at all. This has raised a policy concern that some borrowers with the income to repay a mortgage might be unable to obtain affordable mortgages. FHA mortgage insurance is intended to make lenders more willing to offer affordable mortgages to these borrowers by insuring the lender against the possibility of borrower default.

FHA-insured loans have lower down payment requirements than most conventional mortgages. (Conventional mortgages are mortgages that are not insured by FHA or guaranteed by another government agency, such as VA or USDA.5) Because saving for a down payment is often the biggest barrier to homeownership for first-time homebuyers and lower- or moderate-income homebuyers, the smaller down payment requirement for FHA-insured loans may allow some households to obtain a mortgage earlier than they otherwise could. (Borrowers with down payments of less than 20% could also obtain non-FHA mortgages with private mortgage insurance. See the nearby text box on "FHA and Private Mortgage Insurance.") FHA-insured mortgages also have less stringent requirements related to credit history than many conventional loans. This might make FHA-insured mortgages attractive to borrowers without traditional credit histories or with weaker credit histories, who would either find it difficult to take out a mortgage absent FHA insurance or may find it more expensive to do so.

|

FHA and Private Mortgage Insurance Another option for borrowers with small down payments might be to obtain mortgage insurance from a private company, rather than from a government agency like FHA. This is known as private mortgage insurance (PMI). Conventional mortgages with down payments of less than 20% are generally required to carry PMI.6 Therefore, borrowers with a down payment of less than 20% may find themselves choosing between a conventional mortgage with PMI or an FHA-insured mortgage.7 Whether PMI or FHA insurance is a more attractive option for a specific borrower will depend on a number of factors, including the borrower's circumstances, the respective underwriting standards, and the fees charged by FHA and PMI companies at a given point in time, which can be affected by economic conditions and the features of the mortgage itself. |

FHA-insured mortgages play a particularly large role for first-time homebuyers, low- and moderate-income households, and minorities. For example, 83% of FHA-insured mortgages made to purchase a home (rather than to refinance an existing mortgage) in FY2018 were obtained by first-time homebuyers. Over one-third of all FHA loans (both purchase and refinance loans) were obtained by minority households, and FHA-insured mortgages accounted for about 57% of all forward mortgages made to low- or moderate-income borrowers during the year.8

Since FHA-insured mortgages are often obtained by borrowers who cannot make large down payments or those with weaker credit histories, some have questioned whether FHA-insured mortgages are similar to subprime mortgages.9 Like subprime mortgages, FHA-insured mortgages are often obtained by borrowers with lower credit scores, though some borrowers with higher credit scores also obtain FHA-insured mortgages.10 However, FHA-insured mortgages are prohibited from carrying the full range of features that many subprime mortgages could carry. For example, FHA-insured loans must be fully documented, and they cannot include features such as negative amortization.11 (FHA mortgages can include adjustable interest rates.) Some of these types of features appear to have contributed to high default and foreclosure rates on subprime mortgages. Nevertheless, some have suggested that FHA-insured mortgages are too risky, and that they can harm borrowers by providing mortgages that often have a higher likelihood of default than other mortgages due to combinations of risk factors such as low down payments and lower credit scores.12

Countercyclical Role

Traditionally, FHA plays a countercyclical role in the mortgage market, meaning that it tends to insure more mortgages when mortgage credit markets are tight and fewer mortgages when mortgage credit is more widely available. A major reason for this is that FHA continues to insure mortgages that meet its standards even during market downturns or in regions experiencing economic turmoil. When the economy is weak and lenders and private mortgage insurers tighten credit standards and reduce lending activity, FHA-insured mortgages may be the only mortgages available to some borrowers, or may have more favorable terms than mortgages that lenders are willing to make without FHA insurance. When the economy is strong and mortgage credit is more widely available, many borrowers may find it easier to qualify for affordable conventional mortgages.

Features of FHA-Insured Mortgages

This section briefly describes some of the major features of FHA-insured mortgages for purchasing or refinancing a single-family home.13 Single-family homes are defined as properties with one to four separate dwelling units.14

Eligibility and Underwriting Guidelines

FHA-insured loans are available to borrowers who intend to be owner-occupants and who can demonstrate the ability to repay the loan according to the terms of the contract. FHA-insured loans must be underwritten in accordance with accepted practices of prudent lending institutions and FHA requirements. Lenders must examine factors such as the applicant's credit, financial status, monthly shelter expenses, funds required for closing expenses, effective monthly income, and debts and obligations. In general, individuals who have previously been subject to a mortgage foreclosure are not eligible for FHA-insured loans for at least three years after the foreclosure.15

As a general rule, the applicant's prospective mortgage payment should not exceed 31% of gross effective monthly income. The applicant's total obligations, including the proposed housing expenses, should not exceed 43% of gross effective monthly income. If these ratios are not met, the borrower may be able to present the presence of certain compensating factors, such as cash reserves, in order to qualify for an FHA-insured loan.16

Since October 4, 2010, FHA has required a minimum credit score of 500, and has required higher down payments from borrowers with credit scores below 580 than from borrowers with credit scores above that threshold.17 See the "Down Payment" section for more information on down payment requirements for FHA-insured loans.

Owner Occupancy

In general, borrowers must intend to occupy the property as a principal residence.18

Eligible Loan Purposes

FHA-insured loans may be used to purchase one-family detached homes, townhomes, rowhouses, two- to four-unit buildings, manufactured homes and lots, and condominiums in developments approved by FHA.19 FHA-insured loans may also be obtained to build a home; to repair, alter, or improve a home; to refinance an existing home loan; to simultaneously purchase and improve a home; or to make certain energy efficiency or weatherization improvements in conjunction with a home purchase or mortgage refinance.20

Loan Term

FHA-insured mortgages may be obtained with loan terms of up to 30 years.21

Interest Rates

The interest rate on an FHA-insured loan is negotiated between the borrower and lender. The borrower has the option of selecting a loan with an interest rate that is fixed for the life of the loan or one on which the rate may be adjusted annually.

Down Payment

FHA requires a lower down payment than many other types of mortgages. Under changes made by the Housing and Economic Recovery Act of 2008 (HERA, P.L. 110-289), borrowers are required to contribute at least 3.5% in cash or its equivalent to the cost of acquiring a property with an FHA-insured mortgage. (Prior law had required borrowers to contribute at least 3% in cash or its equivalent.) Prohibited sources of the required funds include the home seller, any entity that financially benefits from the transaction, and any third party that is directly or indirectly reimbursed by the seller or by anyone that would financially benefit from the transaction.22 HUD has interpreted the 3.5% cash contribution as a down payment requirement and has specified that contributions toward closing costs cannot be counted toward it.23

Since October 4, 2010, FHA has required a 10% down payment from borrowers with credit scores between 500 and 579, while borrowers with credit scores of 580 or above are still required to make a down payment of at least 3.5%. FHA no longer insures loans made to borrowers with credit scores below 500.24

Maximum Mortgage Amount

There is no income limit for borrowers seeking FHA-insured loans. However, FHA-insured mortgages cannot exceed a maximum mortgage amount set by law.25 The maximum mortgage amounts allowed for FHA-insured loans vary by area, based on a percentage of area median home prices.26 Different limits are in effect for one-unit, two-unit, three-unit, and four-unit properties. The limits are subject to a statutory floor and ceiling; that is, the maximum mortgage amount that FHA will insure in a given area cannot be lower than the floor, nor can it be higher than the ceiling.

In 2008, Congress temporarily increased the maximum mortgage amounts in response to turmoil in the housing and mortgage markets, with the intention of allowing more households to qualify for FHA-insured mortgages during a period of tighter credit availability.27 New permanent maximum mortgage amounts were later established by the Housing and Economic Recovery Act of 2008. The maximum mortgage amounts established by HERA were higher than the previous permanent limits, but in many cases lower than the temporarily increased limits. However, the higher temporary limits were extended for several years, until they expired at the end of calendar year 2013.28

Since January 1, 2014, the maximum mortgage amounts have been set at the permanent HERA levels. For a one-unit home, HERA established the maximum mortgage amounts at 115% of area median home prices, with a floor set at 65% of the Freddie Mac conforming loan limit and a ceiling set at 150% of the Freddie Mac conforming loan limit. For calendar year 2019, the floor is $314,827 and the ceiling is $726,525.29 (That is, FHA will insure mortgages with principal balances up to $314,827 in all areas of the country. In higher-cost areas, it will insure mortgages with principal balances up to 115% of the area median home price, up to a cap of $726,525 in the highest-cost areas.) These maximum mortgage amounts, and the maximum mortgage amounts for 2-4 unit homes, are shown in Table 1.

|

Property Size |

Maximum Mortgage Amount Floora |

Maximum Mortgage Amount in Areas Between the Floor and the Ceiling |

Maximum Mortgage Amount Ceilingb |

|

1-unit |

$314,827 |

115% of area median home prices for a one-unit property |

$726,525 |

|

2-unit |

$403,125 |

115% of area median home prices for a two-unit property |

$930,300 |

|

3-unit |

$487,250 |

115% of area median home prices for a three-unit property |

$1,124,475 |

|

4-unit |

$605,525 |

115% of area median home prices for a four-unit property |

$1,397,400 |

Source: 12 U.S.C. 1709(b)(2), Section II.A.2.a of HUD Handbook 4000.1, FHA Single Family Housing Policy Handbook, and FHA Mortgagee Letter 2018-11.

Notes: Actual mortgage limits in specific areas can be found at https://entp.hud.gov/idapp/html/hicostlook.cfm.

a. This is the maximum mortgage amount in areas where 115% of area median home prices is lower than 65% of the Freddie Mac limit.

b. This is the maximum mortgage amount in areas where 115% of area median home prices is equal to or higher than 150% of the Freddie Mac limit. The National Housing Act provides that FHA may adjust the mortgage limits for loans in Alaska, Hawaii, Guam, and the Virgin Islands to up to 150% of the ceiling.

Mortgage Insurance Fees (Premiums)

Borrowers of FHA-insured loans pay an up-front mortgage insurance premium (MIP) and annual mortgage insurance premiums in exchange for FHA insurance. These premiums are set as a percentage of the loan amount. The maximum amounts that FHA is allowed to charge for the annual and the upfront premiums are set in statute. However, since these are maximum amounts, HUD has the discretion to set the premiums at lower levels.

Up-Front Mortgage Insurance Premiums

The maximum up-front premium that FHA may charge is 3% of the mortgage amount, or 2.75% of the mortgage amount for a first-time homebuyer who has received homeownership counseling.30 Currently, FHA is charging the same up-front premiums to first-time homebuyers who receive homeownership counseling and all other borrowers.

Since April 9, 2012, HUD has set the up-front premium at 1.75% of the loan amount, whether or not the borrower is a first-time homebuyer who received homeownership counseling.31 This premium applies to most single-family mortgages.32

Annual Mortgage Insurance Premiums

The amount of the maximum annual premium varies based on the loan's initial loan-to-value ratio. For most loans, (1) if the loan-to-value ratio is above 95%, the maximum annual premium is 1.55% of the loan balance, and (2) if the loan-to-value ratio is 95% or below, the maximum annual premium is 1.5% of the loan balance.33

FHA increased the actual annual premiums that it charges several times in recent years in order to bring more money into the FHA insurance fund and ensure that it has sufficient funds to pay for defaulted loans.34 However, in January 2015, FHA announced a decrease in the annual premium for most single-family loans. For most FHA case numbers assigned on or after January 26, 2015, the annual premiums are 0.85% of the outstanding loan balance if the initial loan-to-value ratio is above 95% and 0.80% of the outstanding loan balance if the initial loan-to-value ratio is 95% or below.35 This is a decrease from 1.35% and 1.30%, respectively, which is what FHA had been charging from April 1, 2013, until January 26, 2015.36 These premiums apply to most single-family mortgages; FHA charges different annual premiums in certain circumstances, including for loans with shorter loan terms or higher principal balances.37

Table 2 shows the up-front and annual mortgage insurance premiums that have been in effect for most loans since January 26, 2015.

|

Annual Premium |

Up-Front Premium |

|

|

Initial LTV <= 95% |

0.80% |

1.75% |

|

Initial LTV > 95% |

0.85% |

1.75% |

Source: FHA Mortgagee Letters 12-04 and 15-01.

Notes: These premiums apply to most FHA-insured single-family loans, with certain exceptions (such as certain streamline refinance transactions and FHA-insured reverse mortgages). Different annual premiums apply for mortgages with loan terms of 15 years or less or mortgages with initial principal balances above $625,500.

Premium Refunds and Cancellations

In the past, if borrowers prepaid their loans, they may have been due refunds of part of the up-front insurance premium that was not "earned" by FHA. The refund amount depended on when the mortgage closed and declined as the loan matured. The Consolidated Appropriations Act 2005 (P.L. 108-447) amended the National Housing Act to provide that, for mortgages insured on or after December 8, 2004, borrowers are not eligible for refunds of up-front mortgage insurance premiums except when borrowers are refinancing existing FHA-insured loans with new FHA-insured loans. After three years, the entire up-front insurance premium paid by borrowers who refinance existing FHA-insured loans with new FHA-insured loans is considered "earned" by FHA, and these borrowers are not eligible for any refunds.38

The annual mortgage insurance premiums are not refundable. However, beginning with loans closed on or after January 1, 2001, FHA had followed a policy of automatically cancelling the annual mortgage insurance premium when, based on the initial amortization schedule, the loan balance reached 78% of the initial property value.39 However, for loans with FHA case numbers assigned on or after June 3, 2013, FHA will continue to charge the annual mortgage insurance premium for the life of the loan for most mortgages.40 This change responded to concerns about the financial status of the FHA insurance fund. FHA has stated that, since it continues to insure the entire remaining mortgage amount for the life of the loan, and since premiums were cancelled on the basis of the loan amortizing to a percentage of the initial property value rather than the current value of the home, FHA has at times had to pay insurance claims on defaulted mortgages where the borrowers were no longer paying annual mortgage insurance premiums.41

Options for FHA-Insured Loans in Default

An FHA-insured mortgage is considered delinquent any time a payment is due and not paid. Once the borrower is 30 days late in making a payment, the mortgage is considered to be in default. In general, mortgage servicers may initiate foreclosure on an FHA-insured loan when three monthly installments are due and unpaid, and they must initiate foreclosure when six monthly installments are due and unpaid, except when prohibited by law.42

A program of loss mitigation strategies was authorized by Congress in 1996 to minimize the number of FHA loans entering foreclosure,43 and has since been revised and expanded to include additional loss mitigation options. Prior to initiating foreclosure, mortgage servicers must attempt to make contact with borrowers and evaluate whether they qualify for any of these loss mitigation options. The options must be considered in a specific order, and specific eligibility criteria apply to each option. Some loss mitigation options, referred to as home retention options, are intended to help borrowers remain in their homes. Other loss mitigation options, referred to as home disposition options, will result in the borrower losing his or her home, but avoiding some of the costs of foreclosure. The loss mitigation options that servicers are instructed to pursue on FHA-insured loans are summarized in Table 3.44

Additional loss mitigation options are available for certain populations of borrowers. For example, defaulted borrowers in military service may be eligible to suspend the principal portion of monthly payments and pay only interest for the period of military service, plus three months.45 On resumption of payment, loan payments are adjusted so that the loan will be paid in full according to the original amortization.46 Certain loss mitigation options are also available in areas affected by presidentially declared major disasters.47

|

Possible Remedies for FHA Loans in Default |

|

|

Forbearance |

Forbearance agreements allow a borrower to make partial mortgage payments, or to suspend mortgage payments, for a specified period of time. FHA forbearance options include informal forbearance plans, formal forbearance plans, and a special forbearance option for unemployed borrowers. |

|

FHA-Home Affordable Modification Program (FHA-HAMP) |

FHA-HAMP uses a loan modification, a partial claim, or a combination of the two to bring a borrower's mortgage current and provide for affordable mortgage payments.

|

|

Pre-foreclosure sale |

Pre-foreclosure sales allow a borrower to sell the property and use the proceeds to satisfy the mortgage debt, even if the sale amount is less than the remaining amount owed on the mortgage. |

|

Deed-in-lieu of foreclosure |

Deeds-in-lieu of foreclosure allow a borrower to deed the property to FHA in exchange for being released from the mortgage obligation. |

Sources: 24 C.F.R. 203, HUD Handbook 4000.1, Section III.A.2, and FHA Mortgagee Letter 2016-14.

Program Funding

FHA's single-family mortgage insurance program is funded through FHA's Mutual Mortgage Insurance Fund (MMI Fund). Cash flows into the MMI Fund primarily from insurance premiums and proceeds from the sale of foreclosed homes. Cash flows out of the MMI Fund primarily to pay claims to lenders for mortgages that have defaulted.

This section provides a brief overview of (1) how the FHA-insured mortgages insured under the MMI Fund are accounted for in the federal budget and (2) the MMI Fund's compliance with a statutory capital ratio requirement. For more detailed information on the financial status of the MMI Fund, see CRS Report R42875, FHA Single-Family Mortgage Insurance: Financial Status of the Mutual Mortgage Insurance Fund (MMI Fund).

FHA Home Loans in the Federal Budget

The Federal Credit Reform Act of 1990 (FCRA) specifies the way in which the costs of federal loan guarantees, including FHA-insured loans, are recorded in the federal budget.48 The FCRA requires that the estimated lifetime cost of guaranteed loans (in net present value terms) be recorded in the federal budget in the year that the loans are insured. When the present value of the lifetime cash flows associated with the guaranteed loans is expected to result in more money coming into the account than flowing out of it, the program is said to generate negative credit subsidy. When the present value of the lifetime cash flows associated with the guaranteed loans is expected to result in less money coming into the account than flowing out of it, the program is said to generate positive credit subsidy. Programs that generate negative credit subsidy result in offsetting receipts for the federal government, while programs that generate positive credit subsidy require an appropriation to cover the cost of new loan guarantees.49

The MMI Fund has historically been estimated to generate negative credit subsidy in the year that the loans are insured and therefore has not required appropriations to cover the expected costs of loans to be insured. The MMI Fund does receive appropriations to cover salaries and administrative contract expenses.

The amount of money that loans insured in a given year actually earn for or cost the government over the course of their lifetime is likely to be different from the original credit subsidy estimates. Therefore, each year as part of the annual budget process, each prior year's credit subsidy rates are re-estimated based on the actual performance of the loans and other factors, such as updated economic projections. These re-estimates affect the way in which funds are held in the MMI Fund's two primary accounts: the Financing Account and the Capital Reserve Account. The Financing Account holds funds to cover expected future costs of FHA-insured loans. The Capital Reserve Account holds additional funds to cover any additional unexpected future costs. Funds are transferred between the two accounts each year on the basis of the re-estimated credit subsidy rates to ensure that enough is held in the Financing Account to cover updated projections of expected costs of insured loans.

If FHA ever needs to transfer more funds to the Financing Account than it has in the Capital Reserve Account, it can receive funds from Treasury to make this transfer under existing authority and without any additional congressional action.50 This occurred for the first time at the end of FY2013, when FHA received $1.7 billion from Treasury to make a required transfer of funds between the accounts. The funds that FHA received from Treasury did not need to be spent immediately, but were to be held in the Financing Account and used to pay insurance claims, if necessary, only after the remaining funds in the Financing Account were spent. The MMI Fund has not needed any additional funds from Treasury to make required transfers of funds between the two accounts since that time.

The Capital Ratio

The MMI Fund is also required by statute to maintain a capital ratio of at least 2%, which is intended to ensure that the fund is able to withstand some increases in the costs of loans guaranteed under the insurance fund.51 The capital ratio measures the amount of funds that the MMI Fund currently has on hand, plus the net present value of the expected future cash flows associated with the mortgages that FHA currently insures (e.g., the amounts it expects to earn through premiums and lose through claims paid). It then expresses this amount as a percentage of the total dollar volume of mortgages that FHA currently insures. In other words, the capital ratio is a measure of the amount of funds that would remain in the MMI Fund after all expected future cash flows on the loans that it currently insures have been realized, assuming that FHA did not insure any more loans going forward.

Beginning in FY2009, and for several years thereafter, the capital ratio was estimated to be below this mandated 2% level. The capital ratio again exceeded the 2% threshold in FY2015, when it was estimated to be 2.07%.52 This represented an improvement from an estimated capital ratio of 0.41% at the end of FY2014,53 and from negative estimated capital ratios at the ends of FY2013 and FY2012.54 The capital ratio has remained above 2% since that time, and was estimated to be 2.76% in FY2018.

A low or negative capital ratio does not in itself trigger any special assistance from Treasury, but it raises concerns that FHA could need assistance in order to continue to hold enough funds in the Financing Account to cover expected future losses. In the years since the housing market turmoil that began around 2007, FHA has taken a number of steps designed to strengthen the insurance fund.55 These steps have included increasing the mortgage insurance premiums charged to borrowers; strengthening underwriting requirements, such as by instituting higher down payment requirements for borrowers with the lowest credit scores; and increasing oversight of FHA-approved lenders.

Program Activity

Number of Mortgages Insured

The number of new mortgages insured by FHA in a given year depends on a variety of factors. In general, the number of new mortgages insured by FHA increased during the housing market turmoil (and resulting contraction of mortgage credit) that began around 2007, reaching a peak of 1.8 million mortgages in FY2009 before beginning to decrease somewhat. FY2014 was the only year since FY2007 that FHA insured fewer than 1 million new mortgages.

As shown in Table 4, FHA insured just over 1 million new single-family purchase and refinance mortgages in FY2018. Together, these mortgages had an initial loan balance of $209 billion. About 77% (776,284) of the mortgages were for home purchases, while about 23% (238,325) were for refinancing an existing mortgage.56 The overall number of mortgages insured by FHA in FY2018 represented a decrease from FY2017, when it insured 1.25 million mortgages.

|

Purchase |

Refinance |

Total |

|

|

Number of Mortgages |

776,284 |

238,325 |

1,014,609 |

Source: FHA's FY2018 Annual Report to Congress on the Financial Status of the MMI Fund, p. 96.

Notes: These data do not include FHA-insured reverse mortgages. Numbers reflect FHA's activity during FY2018. FHA activity can also be reported for a calendar year rather than a fiscal year; the market share data included in the Appendix reflect FHA activity during calendar years rather than fiscal years.

Many FHA-insured mortgages are obtained by first-time homebuyers, lower-and moderate-income homebuyers, and minority homebuyers. Of the home purchase mortgages insured by FHA in FY2018, about 83% were made to first-time homebuyers. Over a third of all mortgages (both for home purchases and refinances) insured by FHA in FY2018 were made to minority borrowers.57

As shown in Table 5, at the end of FY2018 FHA was insuring a total of over 8 million single-family loans that together had an outstanding balance of nearly $1.2 trillion.58 Since it was first established in 1934, FHA has insured a total of over 47.5 million home loans.59

|

Total |

|

|

Number of Mortgages |

8,048,639 |

|

Dollar Volume of Mortgages |

$1.196 trillion |

Source: FHA Production Report, September 2018, https://www.hud.gov/program_offices/housing/hsgrroom/fhaprodrpt.

Note: Figures show the number and dollar volume of single-family insurance-in-force as of the end of FY2018, excluding FHA-insured reverse mortgages.

Market Share

Measuring Market Share

FHA's share of the mortgage market is the amount of mortgages that are insured by FHA compared to the total amount of mortgages originated or outstanding in a given time period. FHA's market share can be measured in a number of different ways. Therefore, when evaluating FHA's market share, it is important to recognize which of several different figures is being reported.

First, FHA's share of the mortgage market can be computed as the number of FHA-insured mortgages divided by the total number of mortgages, or as the dollar volume of FHA-insured mortgages divided by the total dollar volume of mortgages.

Furthermore, FHA's market share is sometimes reported as a share of all mortgages, and sometimes only as a share of home purchase mortgages (as opposed to both mortgages made to purchase a home and mortgages made to refinance an existing mortgage).

A market share figure can be reported as a share of all mortgages originated within a specific time period, such as a given year, or as a share of all mortgages outstanding at a point in time, regardless of when they were originated.

Finally, FHA's market share is sometimes also reported as a share of the total number of mortgages that have some kind of mortgage insurance (including mortgages with private mortgage insurance and mortgages insured by another government agency) rather than as a share of all mortgages regardless of whether or not they have mortgage insurance.

FHA's Share of the Mortgage Market

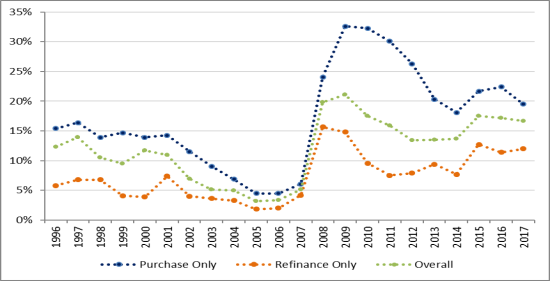

FHA's market share tends to fluctuate in response to economic conditions and other factors. Between calendar years 1996 and 2002, FHA's market share averaged about 14% of the home purchase mortgage market and about 11% of the overall mortgage market (both home purchase mortgages and refinance mortgages), as measured by number of mortgages. However, by 2005 FHA's market share had fallen to less than 5% of home-purchase mortgages and about 3% of the overall mortgage market. Subsequently, as economic conditions worsened and mortgage credit tightened in response to housing market turmoil that began around 2007, FHA's market share rose sharply, peaking at over 30% of home-purchase mortgages in 2009 and 2010, and over 20% of all mortgages (including both home purchases and refinances) in 2009. In 2017, FHA insured 19.5% of new home purchase mortgages and about 16.7% of new mortgages overall, a small decrease compared to its market share in 2016.60

Figure 1 shows FHA's market share as a percentage of the total number of new mortgages originated for each calendar year between 1996 and 2017. As described, FHA's market share can be measured in a number of different ways. The figure shows FHA's share of (1) all newly originated mortgages, (2) just newly originated purchase mortgages, and (3) just newly originated refinance mortgages. FHA's share of home purchase mortgages tends to be the highest, largely because borrowers who refinance are more likely to have built up a greater amount of equity in their homes and, therefore, might be more likely to obtain conventional mortgages. For the number of mortgages insured by FHA in each year calendar since 1996, see the Appendix.

|

Figure 1. FHA's Share of the Mortgage Market, CY1996-CY2017 Percentage of total number of mortgages originated in each year |

|

|

Source: Figure created by CRS using data in HUD's FHA Single-Family Mortgage Market Share Report, 2018 Q2, http://portal.hud.gov/hudportal/HUD?src=/program_offices/housing/rmra/oe/rpts/fhamktsh/fhamktqtrly. |

The increase in FHA's market share after 2007 was due to a variety of factors related to the housing market turmoil and broader economic instability that was taking place at the time. Housing and economic conditions led many banks to limit their lending activities, including lending for mortgages. Similarly, private mortgage insurance companies, facing steep losses from past mortgages, began tightening the underwriting criteria for mortgages that they would insure.61 Furthermore, in 2008 Congress increased the maximum mortgage amounts that FHA can insure, which may have made FHA-insured mortgages a more viable option for some borrowers in certain areas.

More recently, FHA's market share has decreased somewhat from its peak during the housing market turmoil, although it generally remains somewhat higher than it was in the late 1990s and early 2000s. A number of factors may have contributed to this decrease, including lower loan limits in some high-cost areas, higher mortgage insurance premiums,62 and greater availability of non-FHA-insured mortgages. While not the focus of this report, the appropriate market share for FHA has been a subject of ongoing debate among policymakers. It is likely to continue to be a topic of debate, both in the context of policies specifically related to FHA as well as part of broader debate about the future of the U.S. housing finance system.

Appendix. FHA's Market Share Since 1996

Table A-1 provides data on the number of mortgages insured by FHA in each calendar year since 1996, along with FHA's overall market share in each calendar year.

|

Calendar |

FHA-Insured Home Purchase Mortgages |

FHA-Insured Refinance Mortgages |

Total FHA-Insured Mortgages |

Total Mortgage Market |

FHA Share of Mortgage Originations |

|

1996 |

697,000 |

123,000 |

820,000 |

6,672,000 |

12.3% |

|

1997 |

759,000 |

110,000 |

869,000 |

6,233,000 |

13.9% |

|

1998 |

788,000 |

348,000 |

1,136,000 |

10,795,000 |

10.5% |

|

1999 |

913,000 |

245,000 |

1,158,000 |

12,182,000 |

9.5% |

|

2000 |

845,000 |

66,000 |

911,000 |

7,767,000 |

11.7% |

|

2001 |

870,000 |

407,000 |

1,277,000 |

11,627,000 |

11.0% |

|

2002 |

764,000 |

412,000 |

1,176,000 |

16,922,000 |

7.0% |

|

2003 |

630,000 |

653,000 |

1,283,000 |

24,887,000 |

5.2% |

|

2004 |

467,000 |

248,000 |

716,000 |

14,319,000 |

5.0% |

|

2005 |

323,000 |

133,000 |

456,000 |

14,485,000 |

3.1% |

|

2006 |

295,000 |

116,000 |

411,000 |

12,330,000 |

3.3% |

|

2007 |

317,000 |

211,000 |

528,000 |

10,294,000 |

5.1% |

|

2008 |

845,000 |

561,000 |

1,406,000 |

7,092,000 |

19.8% |

|

2009 |

1,088,000 |

897,000 |

1,985,000 |

9,391,000 |

21.1% |

|

2010 |

944,000 |

519,000 |

1,463,000 |

8,359,000 |

17.5% |

|

2011 |

760,000 |

322,000 |

1,082,000 |

6,825,000 |

15.9% |

|

2012 |

738,000 |

527,000 |

1,265,000 |

9,471,000 |

13.4% |

|

2013 |

665,000 |

507,000 |

1,172,000 |

8,690,000 |

13.5% |

|

2014 |

601,000 |

182,000 |

783,000 |

5,703,000 |

13.7% |

|

2015 |

811,000 |

410,000 |

1,221,000 |

6,959,000 |

17.5% |

|

2016 |

891,000 |

413,000 |

1,304,000 |

7,584,000 |

17.2% |

|

2017 |

851,000 |

309,000 |

1,160,224 |

6,927,000 |

16.7% |

Source: U.S. Department of Housing and Urban Development, FHA Single-Family Market Share 2018 Q2, http://portal.hud.gov/hudportal/HUD?src=/program_offices/housing/rmra/oe/rpts/fhamktsh/fhamktqtrly.

Notes: This table reflects FHA activity during calendar years. Data can also be reported for fiscal years; the FHA program activity data reported in Table 4 in this report reflect fiscal year rather than calendar year activity.