Background

This report briefly describes cotton's special treatment, relative to other traditional farm program crops, in the 2014 farm bill. It also reviews the legislative attempts—which culminated with the Bipartisan Budget Act of 2018 (P.L. 115-123; BBA)—to reintegrate cotton as a program crop eligible for major farm revenue support programs. Then, it reviews the specifics of the new seed cotton program and discusses three potential issues related to the establishment of seed cotton as a program crop.

The WTO Brazil-U.S. Cotton Trade Dispute

As a member of the World Trade Organization (WTO), the United States has committed to abide by WTO rules and disciplines.1 WTO rules covering agricultural trade and domestic support programs for agriculture have played a large role in shaping current U.S. cotton policy.2 In particular, in 2002, Brazil—a major cotton export competitor—initiated a long-running WTO dispute settlement case against U.S. cotton support programs. Brazil charged that these programs were depressing international cotton prices and thus artificially and unfairly reducing the quantity and value of Brazil's cotton exports, causing economic harm to its cotton sector. In 2004, a WTO panel ruled against the United States in the cotton case. As a result of the ruling and the potential for WTO-sanctioned retaliation, the United States made several policy changes in an attempt to bring the related programs into WTO compliance. The policy changes evolved over several years and relied on both legislative action and administrative adjustments but culminated with cotton's special treatment in the 2014 farm bill. In October 2014, the two countries signed a Memorandum of Understanding (MOU) that finalized a mutual resolution to the case based on U.S. cotton policy as enacted in the 2014 farm bill.

Cotton in the 2014 Farm Bill

Among traditional program crops, cotton was singled out for special treatment by the 2014 farm bill. Unlike other crops, upland cotton was made ineligible for new revenue support programs available to traditional program crops—referred to as covered commodities3—and was given a reduced marketing loan rate.4 Instead, upland cotton producers were eligible for new temporary transition payments and a stand-alone, county-based revenue insurance policy called the Stacked Income Protection Plan (STAX).5 Cotton producers also remained eligible for several smaller (in terms of payments) support programs that were unaffected by the WTO case.

Cotton Excluded from New Revenue Programs

The 2014 farm bill repealed the direct payment (DP), the Average Crop Revenue Election, and the counter-cyclical payment (CCP) programs from the 2008 farm bill (P.L. 110-246).6 In their place, two new support programs—the Agriculture Risk Coverage (ARC) and Price Loss Coverage (PLC) programs—were established.7 The new revenue programs provide support to U.S. agricultural producers of covered commodities through either statutory reference prices under PLC or historical revenue guarantees based on a five-year moving average of crop prices and yields under ARC. As with the DP and CCP programs, payments under ARC and PLC are decoupled from current plantings, meaning they are not based on current production. The decoupled payment feature was added in earlier farm bills to comply with WTO rules governing domestic support programs. Instead, payments are made on historical program acres (known as base acres8) for a select list of program crops (referred to as covered commodities). Cotton was explicitly removed from the list of covered crops, thus making cotton base acres (estimated at 17.6 million acres) ineligible for participation in the ARC and PLC programs.

Historical Cotton Program Acres Renamed as Generic Base

To avoid having cotton producers completely lose access to farm program benefits on their historic cotton base acres, those acres were renamed "generic base"9 and retained in a producer's total acreage base. As such, they were eligible for program payments under ARC and PLC but only if a covered crop (excluding upland cotton) was planted on the generic base.10 Thus, ARC and PLC payments made on generic base were coupled to actual plantings of program crops.11 The "coupling of payments to specific crops" provided strong incentives to plant other eligible covered crops on generic base acres in lieu of upland cotton.

Cotton-Specific Programs Remaining in the 2014 Farm Bill

Producers of upland cotton remain eligible for support under several other farm programs under the 2014 farm bill including benefits under the marketing assistance loan (MAL) program, temporary Cotton Transition Assistance Payments (CTAP), and a new revenue insurance program called STAX.12 In addition, the domestic cotton market receives support from provisions that provide economic adjustment assistance to domestic users of upland cotton (P.L. 113-79, Section 1207(c)) and cotton storage cost reimbursements (Section 1204(g)). An additional payment program—the Cotton Ginning Cost Share (CGCS) program—was added in 2016 outside of the farm bill (see below).

- MAL Program for Cotton Producers. The MAL program provides both a floor price and interim financing for so-called loan commodities. A participating producer may put a harvested "loan" crop under a nine-month, nonrecourse loan valued at a statutory commodity loan rate. The loan uses the crop as collateral, and the loan rate, in effect, establishes a price guarantee. Special benefits are available if the adjusted world price—announced weekly by USDA—falls below the cotton loan rate. The 2014 farm bill changed the loan rate for upland cotton from $0.52 per pound to the simple average of the adjusted prevailing world price for the immediately preceding two market years but not less than $0.45 per pound or more than $0.52 per pound.13 During the first two years of the 2014 farm bill, cotton producers received $700 million in payments under the MAL program—$372 million in 2014 and $328 million in 2015. More recent data are not yet available.

- CTAP. The 2014 farm bill also established CTAP as an offset for the loss of ARC and PLC program eligibility. Upland cotton producers were eligible for CTAP payments on a percentage of former cotton base acres for crop years 2014 and 2015—60% of base received payments in 2014, 36.5% of base in 2015. CTAP outlays were a combined $484 million during 2014 and 2015. Transition payments ended after the 2015 crop.

- CGCS. In 2016, USDA used its administrative authority under the Commodity Credit Corporation (CCC) Charter Act to offer U.S. upland cotton producers CGCS payments valued at $328 million. The CGCS program provided cost-share payments for cotton producers' cotton ginning costs based on their 2015 cotton plantings multiplied by 40% of average regional ginning costs. The CGCS program was offered again in 2018 with similar payment terms.14

- Economic Adjustment Assistance for Domestic Users (EAAU) Program. EAAU payments are made to domestic users for all documented use of upland cotton on a monthly basis regardless of the origin of the upland cotton. The payment rate is $0.03 per pound and results in CCC outlays of about $49 million per year. Although the payments are made to cotton users, at least a portion of the payment is likely returned to producers in the form of higher prices associated with the increased demand from domestic users.

- STAX. STAX was offered as a shallow-loss, area-wide revenue insurance product that could indemnify losses in county revenue of greater than 10% of expected revenue depending on the coverage level selected by a producer.15 To encourage participation, USDA pays 80% of the policy premium for STAX. In contrast to the revenue guarantees available under ARC and PLC, which have a statutorily fixed lower price bound (equal to the PLC reference price), the revenue guarantee under STAX is recalculated each year and has decreased significantly following several years of cotton market declines since 2014. As a result, participation in STAX has been low and has declined each year that it has been available (29.3% in 2015, 25.3% in 2016, and 23.3% in 2017).

Industry Push for Cotton Reintegration into ARC/PLC Programs

Economic conditions in the U.S. farm economy steadily declined from mid-2014 into 2018, including both lower farm commodity prices and income.16 Under these conditions, the new ARC and PLC programs, which function in a counter-cyclical manner relative to market conditions, have triggered substantial payments to agricultural producers to help offset their economic losses. During the first three years of the 2014 farm bill, ARC and PLC paid out nearly $20 billion to eligible program crops ($5.3 billion in 2014, $7.8 billion in 2015, and $6.9 billion in 2016).17 Cotton producers could only indirectly benefit via coupled ARC and PLC payments made to other program crops planted on generic base acres. Meanwhile, net indemnity payments (indemnities minus producer-paid premium) under the new cotton revenue insurance program, STAX, were relatively small at $20.2 million in 2015 and $37.3 million in 2016.18

In 2014, following the downturn in the U.S. cotton market, the National Cotton Council (NCC) claimed that lower per-acre cotton revenues coincided with elevated costs of production and that additional economic relief was needed.19 The U.S. cotton sector was also concerned about having resources redirected to other program crops planted on generic base. In response to its exclusion from PLC program eligibility, the U.S. cotton sector actively sought to regain cotton's former status as a "covered commodity" but on the basis of cottonseed rather than cotton lint.

In September 2015, the NCC proposed that the Secretary of Agriculture treat cotton lint and cottonseed separately for purposes of the ARC and PLC programs. Instead of focusing on lint as done by past farm policy, the Secretary of Agriculture could use his apparent authority granted under the 2014 farm bill to designate cottonseed as an "other oilseed." Then cottonseed would be eligible for support as a minor oilseed with a PLC reference price of $20.15 per hundredweight (cwt.) and a MAL loan rate of $10.09 per cwt.20

|

Cotton Co-Products: Lint and Cottonseed The successful cultivation of cotton results in two products, fiber (or lint) and cottonseed, which are separated from the un-ginned cotton boll by ginning the harvested cotton. In 2017, the United States produced 9.8 billion pounds of lint21 from upland cotton valued at $6.7 billion and 13.5 billion pounds of cottonseed22 valued at $1 billion.23 About 78% of U.S. upland cotton lint production is exported while the balance is used domestically. According to the NCC, more than half of U.S. upland cotton lint production (57%) goes into apparel, 36% into home furnishings, and 7% into industrial products.24 In contrast, cottonseed goes almost entirely to domestic users—about two-thirds is fed whole to livestock (primarily dairy cows), while the remaining seed is crushed, producing a high-grade salad oil and a high protein meal for livestock, dairy, and poultry feed. |

Under Section 1111 of the 2014 farm bill, the term other oilseed is defined as a crop of sunflower seed, rapeseed, canola, safflower, flaxseed, mustard seed, crambe, sesame seed, or any oilseed designated by the Secretary. The NCC contended that this definition provided the Secretary with sufficient authority to designate cottonseed as an "other oilseed" and thus to extend eligibility for PLC or ARC to upland cotton producers.

This proposal had the potential to increase federal outlays because the price of cottonseed is historically well below the "other oilseed" reference price, and PLC payments for cottonseed could approach $1 billion per year if made on generic base acres.25 Several members of the House Agriculture Committee agreed with the NCC proposal. In December 2015 several Members of Congress urged then-Secretary of Agriculture Tom Vilsack to use his authority under the farm bill to designate cottonseed as a covered oilseed, thus allowing cottonseed to be a "covered commodity" eligible for the ARC and PLC programs immediately and without further action by Congress.26

In response, Vilsack contended that he did not have such authority because Congress had explicitly removed cotton from the list of eligible "covered commodities" and given it two special programs—STAX and CTAP, although CTAP expired in 2015. Furthermore, Vilsack argued that Congress could amend the farm bill to explicitly allow upland cotton producers to participate in ARC or PLC, or, alternatively, it could remove a provision that has appeared since FY2012 in annual appropriations acts (e.g., §715 of P.L. 115-31, the FY2017 agriculture appropriation) that effectively prohibits USDA from providing emergency assistance through the CCC.

Seed Cotton as Program Crop: Legislative Evolution

Since USDA said that it lacked the authority to designate cottonseed as an "other oilseed," cotton's proponents determined the path forward would be through an act of Congress.27 Furthermore, such an act of Congress would have budgetary implications. The general view of the agricultural community was that, if a new cotton program were to be incorporated into the next farm bill, it would likely have a budgetary cost, thus requiring possibly difficult budgetary offsets.

|

PAYGO Budgetary Restrictions on Changes to the Farm Bill Title I farm programs, in general, receive mandatory funding. Under mandatory funding, the authorizing legislation (i.e., the farm bill) defines both who is eligible to participate and how a program payment is triggered. The farm bill does not impose any spending limit on mandatory funding. Instead, program outlays are determined by producer participation, weather, and market forces. In contrast, for discretionary spending the farm bill sets program parameters and specifies funding levels. Discretionary funding levels are determined by the appropriating committees through the annual federal budget process. Thus, budget enforcement of discretionary spending is through future appropriations and budget resolutions. Outlays for mandatory programs under a new farm bill are evaluated by the Congressional Budget Office (CBO) using multiyear "baseline" projections and are enforced through "PAYGO" budget rules.28 CBO baseline projections involve five- and 10-year budget estimates calculated under the assumption that current law is extended for the life of the projection period. CBO's five- and 10-year cost estimates establish a program's baseline funding.29 The baseline is the benchmark against which proposed changes from current law that would affect mandatory spending are measured. The baseline cost impact of a proposed program change is referred to as its budget score. Any proposed program change from current law that increases outlays from CBO's baseline (such as the designation of cottonseed as an "other oilseed") that is determined to have a positive score and under PAYGO must be offset by reductions in outlays under other current-law programs to preserve baseline neutrality. |

FY2017 Appropriations Bill (115th Congress)

Proponents of reintegrating cotton into the ARC and PLC programs, including House Agriculture Committee Chairman Mike Conaway, began pursuing a legislative track that sought to use the annual appropriations process as the legislative vehicle to contain their proposal. The idea was to include an amendment to the FY2017 appropriations bill that would build off the 2015 NCC cottonseed proposal.30

During the debate preceding the final agreement for the FY2017 consolidated appropriations bill in spring 2017, a proposal emerged for including cottonseed as a covered commodity with its own policy parameters—a MAL loan rate of $8.00 per cwt. and a PLC reference price of $15.88 per cwt. Because the cottonseed PLC reference price of $15.88 per cwt. is below the "other oilseed" reference price of $20.15, it was thought that the cost (i.e., the positive baseline score) for the inclusion of cottonseed would be more manageable. House negotiators identified two potential budget offsets for the cottonseed proposal: (1) declaring producers who participate in the cottonseed ARC or PLC program ineligible for STAX and (2) reallocating generic acres back to cottonseed base and away from other program crops. In the first three years of the 2014 farm bill, over $1 billion in ARC and PLC payments had been made to crops planted on generic base (Table 1).

To facilitate the inclusion of the cottonseed proposal, it would not be authorized to begin, or receive any funding, until FY2018. Thus it would have imposed no budget cost on the FY2017 appropriations bill under consideration. However, the cottonseed proposal became linked to proposed changes to the new dairy program, the Margin Protection Program (MPP). Similar to the cotton sector, dairy producers considered their 2014 farm bill program—MPP—as inadequate in responding to the dairy sector's economic difficulties. Senate allies of the dairy industry sought additional baseline funding to make adjustments to the MPP program in response to the dairy industry's concerns but were unable to reach a budget compromise.31

|

Crop Year |

Total Generic Basea (1,000 Acres) |

Generic Base with Payments (1,000 Acres) |

Payments on Generic Base ($ Million) |

||||||||||||||||||

|

ARC |

PLC |

Total |

ARC |

PLC |

Total |

||||||||||||||||

|

2014 |

|

|

|

|

|

|

|

|

|

||||||||||||

|

2015 |

|

|

|

|

|

|

|

|

|

||||||||||||

|

2016 |

|

|

|

|

|

|

|

|

|

||||||||||||

|

Total |

|

|

|

|

|

|

|

|

|

||||||||||||

Source: FSA, "ARC/PLC Program," https://www.fsa.usda.gov/programs-and-services/arcplc_program/index.

Notes:

a. When base acres are aggregated by county by crop year, they add to 19.1 million acres in each of 2014 and 2015 as a result of double-cropping on generic base acres. FSA, "ARC/PLC Election Data," as of May 29, 2015, https://www.fsa.usda.gov/Assets/USDA-FSA-Public/usdafiles/arc-plc/excel/arc_plc_election_data.xlsx.

Ultimately, the FY2017 appropriations bill that became law (Consolidated Appropriations Act of 2017, P.L. 115-31; May 5, 2017) included neither the cottonseed nor MPP proposal. Instead, the explanatory statement32 accompanying P.L. 115-31 directed USDA to prepare a report within 60 days on the needs of cotton growers and to consider providing immediate assistance to dairy producers through the CCC.

Senate FY2018 Appropriations Bill (S. 1603, 115th Congress)

The cottonseed proposal was revised with a lower PLC reference price of $15.00 per cwt. but the same MAL loan rate of $8.00 per cwt. and was included two months later in the Senate committee-reported Agriculture appropriations bill for FY2018 (S. 1603, §728, 115th Congress, July 20, 2017).33 The new proposal was more specific in terms of how cottonseed producers would be allowed to designate generic base acres as cottonseed base acres and about the formula to be used to determine a producer's cottonseed program yields—both of which are needed to calculate PLC payments. In addition, the Senate bill included dairy program changes alongside the cottonseed proposal. The joint provisions would have authority for $1 billion in new baseline spending over 10 years but required no budget offsets, because they would not start until after FY2018. However, Congress was unable to reach agreement on an FY2018 appropriations bill for reasons unrelated to agricultural policy, and the cotton issue remained unresolved into fall 2017.

Emergency Supplemental Bill (H.R. 4667, 115th Congress)

Stakeholders in the agricultural sector were becoming increasingly concerned that leaving cotton and dairy policy fixes for the next farm bill would require new baseline spending that could lead to difficult debate over which programs—farm or domestic food programs—should make budget sacrifices to free up money for cotton and dairy. In December 2017, agricultural policy proponents in the House were able to include cotton and dairy proposals into an emergency appropriations bill (H.R. 4667) that was intended to provide assistance for victims of hurricanes and wildfires that had occurred during 2017.34 The cotton proposal was reshaped as a "seed cotton" program that uses a weighted average of both lint and cottonseed (described below). The House-passed supplemental appropriations bill, H.R. 4667, was not considered in the Senate.

Bipartisan Budget Act of 2018 (P.L. 115-123; BBA)

In February 2018, Congress agreed on a two-year budget deal that included the emergency supplemental bill provisions along with both the seed cotton and dairy program changes. On February 9, 2018, Congress passed the BBA (P.L. 115-123). Among its provisions, the BBA authorized supplemental appropriations for crop and livestock losses from the 2017 hurricane season and wildfires in the West.35 The BBA also included the seed cotton and dairy provisions that were in the House-passed supplemental appropriations bill (H.R. 4667). Both of these farm program changes have long-term policy implications because they change the 2014 farm bill statutes. In particular, Section 60101(a) of the BBA amends the 2014 farm bill to add seed cotton as a "covered commodity," making cotton eligible for the PLC and ARC programs.

Seed Cotton: Program Design

The BBA provision, Section 60101(a), includes seed cotton as a covered commodity, thus making it eligible for participation in PLC and ARC beginning with crop year 2018. Participating producers must make three decisions (for the one year remaining of the 2014 farm bill period): how to allocate their generic base acres, whether to update cotton program yields, and whether to participate in ARC or PLC.

Allocation of Generic Base Acres

Before producers make any decision regarding ARC or PLC, they must (within 90 days of enactment—that is, by May 10, 2018) decide how to reallocate their generic base36 to either seed cotton or to other program crops by the following formula:

No recent history of planting covered commodities: If the owner of a farm has not planted any covered commodities (including seed cotton) during the 2009 through 2016 crop years, then the generic base acres shall be allocated to "unassigned crop base" and no longer be eligible for ARC or PLC payments.

Recent history of planting covered commodities: The owner of a farm with a history of planting covered commodities during the 2009 through 2016 crop years shall allocate generic base acres between seed cotton and other program crops as follows:

- 1. To seed cotton base acres in a quantity equal to the greater of 80% of their generic base or the average upland cotton plantings (or prevented from being planted) during the 2009 to 2012 crop years (not to exceed the total generic base acres on the farm) or

- 2. To base acres for covered commodities (including seed cotton) in proportion to each crop's share of planted (or prevented from being planted) acreage during 2009 to 2012.37

Any residual or unassigned generic base acres (defined as any positive difference between generic base and the seed cotton base acres allocated under the first choice) are no longer eligible for program payments for any covered crop.

Program Choice and Payment Parameters

For the 2018 crop year, producers have a one-time opportunity to elect ARC or PLC for seed cotton. If no election is made, PLC becomes the automatic choice. The seed cotton PLC reference price is 36.7 cents per pound. The seed cotton program yield is set at 2.4 times the historical upland cotton program yield (established by the 2008 farm bill [P.L. 110-246]). Producers have a one-time opportunity to update their farms' upland cotton payment yield based on 90% of the average yield on planted acres for the 2008 through 2012 crop years. Seed cotton payments are to be made on 85% of the seed cotton base.

Because seed cotton has never been a covered commodity, no price series exists and, thus, must be defined.38 The calculated seed cotton price (referred to as the "effective" price) is defined as the weighted annual price for upland cotton lint and cottonseed weighted by their share of combined production (lint plus cottonseed) measured in pounds. It is an artificial price that is computed only for purposes of the farm bill. If the effective price is less than the reference price of 36.7 cents per pound, payments are triggered under the PLC program.39 A producer's payment equals the product of the payment rate (i.e., the difference between the PLC reference price and the effective price) times the seed cotton program yield times 85% of the seed cotton base.

Upland cotton production remains eligible for the MAL program under the original 2014 farm bill with a loan rate that floats between 45 and 52 cents per pound of harvested cotton lint based on the simple average of the adjusted prevailing world price for the immediately preceding two market years. The new seed cotton provisions do not establish a nonrecourse MAL for seed cotton. However, for purposes of calculating the maximum potential seed cotton payment rate, seed cotton is deemed to have a MAL rate of 25 cents per pound. Finally, any farm that enrolls seed cotton base acres in either ARC or PLC is ineligible for STAX.

CBO Cost Projections

CBO scored the cost of seed cotton payments under the ARC and PLC programs at $1.270 billion over five years (2018-2022) and $2.961 billion over 10 years (2018-2027).40 However, according to CBO, the net costs of the seed cotton provision in the BBA would be reduced to $61 million over 10 years by associated budget offsets—including the reallocation of generic base and the removal of residual generic base from ARC and PLC program eligibility (-$2.188 billion over 10 years) and by repealing the eligibility for the STAX program for cotton producers that enroll their seed cotton base in either ARC or PLC (-$711 million over 10 years).

Potential Issues

Three issues that could figure into future policy debate as result of this program change include considerations surrounding the potential for re-opening of the WTO U.S.-Brazil cotton dispute, the potential for large budget costs if commodity markets weaken further, and the realignment of program payment acres.

WTO U.S.-Brazil Cotton Dispute

By designating seed cotton as a covered commodity, Brazil might argue that USDA has violated the terms of the U.S.-Brazil MOU, agreed to by both parties to resolve a WTO trade dispute concerning U.S. domestic cotton support programs. Under the WTO cotton case, the WTO granted Brazil authority to retaliate against U.S. goods and services, including copyright and trademark protections. By agreeing to a mutual MOU, trade retaliation was avoided. In particular, according to Section VI of the MOU—the Peace Clause—Brazil would refrain from retaliation prior to September 30, 2018, providing that the United States limits cotton payments to those programs specifically authorized by the 2014 farm bill such as STAX and MAL. With the addition of the seed cotton program, Brazil could potentially argue that the Peace Clause is no longer in effect and retaliation is once again an option under the WTO decision. Thus, designating seed cotton as a covered commodity might raise questions about adhering to the MOU and revive the WTO cotton trade dispute.

Several economists have raised concerns about linking cotton program payments to cotton market prices.41 In particular, some economists contend that large government payments tend to mute market signals, and any incentive to produce more cotton than the market can support at current prices has potentially negative impacts on developing countries.42

Potential Budget Cost of Seed Cotton as a Program Crop

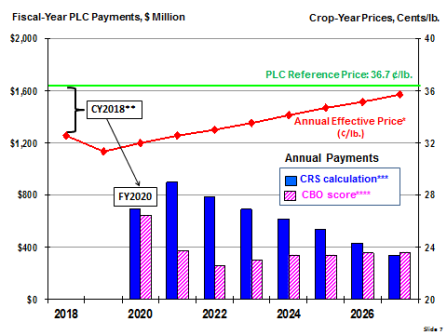

Projections for PLC payments on seed cotton base are sensitive to changes in market conditions. Figure 1 compares CBO projected payments (reported in February 2018 using a 2017 baseline) with CRS calculations based on the Food and Agriculture Policy Research Institute's (FAPRI) March 2018 baseline market projections for upland cotton and cottonseed prices, area, and yields. The CRS calculations illustrate how slightly lower projected farm prices could result in substantially higher program payments for seed cotton—with five-year aggregate payments reaching nearly $2 billion and 10-year payments of about $4 billion based on the FAPRI baseline projections.

|

Figure 1. Alternative Outlay Scenarios for Seed Cotton Under PLC |

|

|

Source: The PLC reference price for seed cotton of 36.7 cents per pound and the formula for calculating the seed cotton effective price is from the Bipartisan Budget Act of 2018 (P.L. 115-123, Section 60101(a)(2), BBA). The annual effective price for seed cotton is calculated by CRS according to the statutory provision using price projections for upland cotton and cottonseed, weighted by share of combined production in pounds, from the Food and Agricultural Policy Research Institute, University of Missouri, U.S. Baseline Outlook, FAPRI-MU Report #01-18, March 2018. Notes: PLC payments for a particular crop year are not made until after October 1 of the following year. Thus, there is a nearly two-year delay in payments associated with a crop. For example, PLC payments for the 2018 seed cotton crop year will not be paid out until after October 1, 2019 (i.e., FY2020), as seen in the chart. *The annual effective price for seed cotton is the average of the annual farm prices for upland cotton and cottonseed weighted by their share of total production measured in pounds. **The projected PLC payment rate equals the difference between the PLC reference price and the effective annual seed cotton price. ***The PLC payment equals the PLC payment rate times the seed cotton program yield (estimated at 1,384 pounds per acre) times seed cotton base acres (estimated at 80% of generic base or 14.1 million acres) times 85%. ****The CBO score for the BBA, Section 60101(a), "Treatment of Seed Cotton," February 8, 2018. |

Base Acres Reduction

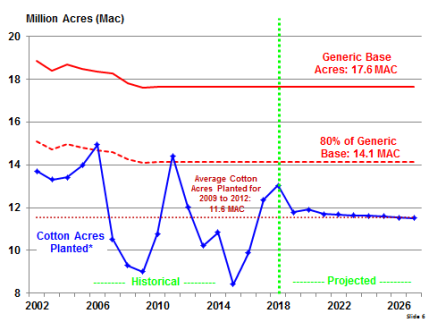

The reallocation of generic base to seed cotton or other covered commodities, combined with the elimination of payments to residual base (unallocated generic base), suggests that a significant portion of historical upland cotton base acres could become ineligible for revenue support payments. The likelihood of PLC payments to seed cotton base, as suggested in the previous section, could provide an incentive for reallocating generic base to seed cotton rather than to other program crops. Upland cotton producers planted an average of 11.6 million acres during the 2009-2012 period compared with 17.6 million acres of generic base (Figure 2). To obtain the highest seed cotton base possible, most cotton producers might opt to reallocate 80% of generic base to seed cotton per the statutory reallocation formula for farms with a recent history of covered crops. If so, national seed cotton base would be approximately 14.1 million acres. This, in turn, would imply that as much as 20% of generic base (or 3.56 million acres) would be residual generic base and thus be disqualified from receiving farm revenue support payments. This contributes to the size of the budgetary offset in the CBO score.

|

Figure 2. Upland Cotton: Generic Base versus Planted Acres (Under the Provisions of the Bipartisan Budget Act of 2018, P.L. 115-123, Section 160101(a)) |

|

|

Source: Historical data for 2002-2017 are from NASS; projected data for 2018 are from USDA, Office of the Chief Economist; projected data for 2019-2027 are from FAPRI 2018 baseline projections. Notes: Mac = million acres. |