Legislative text of the Coronavirus Aid, Relief, and Economic Security (CARES) Act, circulated on Sunday, March 22, 2020, proposes direct payments to individuals and families—"2020 recovery rebates." This Insight provides a brief overview of the proposed 2020 recovery rebates included in the text circulated on March 22, which differ from those included in the legislation introduced on March 19.

The proposed 2020 recovery rebates equal $1,200 per person ($2,400 for married taxpayers filing a joint tax return) and $500 per child. These amounts would phase down for higher-income taxpayers. These payments are structured as tax credits automatically advanced to households in 2020 if they filed a 2019 income tax return and would be received as a direct deposit or check by mail. If a 2019 return had not been filed, rebates would be advanced automatically based on 2018 return information. Seniors who did not file an income tax return would have the credit automatically advanced in 2020 based on their 2019 Social Security benefit statement.

The proposed credit equals $1,200 per person ($2,400 for married joint filers) for eligible individuals. Generally, an eligible individual is any individual excluding (1) nonresident aliens, (2) individuals who can be claimed as a dependent by another taxpayer, and (3) an estate or trust.

Individuals eligible for the credit would receive an additional $500 for each child that qualifies for the child tax credit.

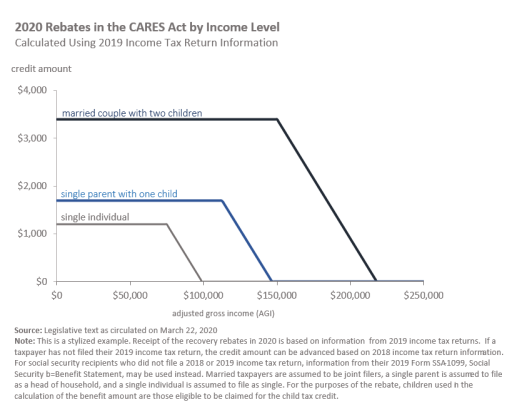

The total proposed credit phases out at a rate of 5% of adjusted gross income (AGI) above $75,000 ($112,500 for head of household filers and $150,000 for married joint returns). An illustration of the amount of the rebate by income level is provided in the figure below.

|

As with any tax refund, these payments would not count as income or resources for a 12-month period in determining eligibility for, or the amount of assistance provided by, any federally funded public benefit program.

The proposed credit would be a fixed amount until income reaches the phaseout level. Lower-income taxpayers with little or no income tax liability would be eligible for a tax credit equal in dollar value to that received by middle-income and upper-middle-income taxpayers. Hence, as a percentage of income, this rebate would be largest for the lowest-income recipients. The tax credit would phase out at the upper end of the distribution as shown in the figure above.

The bill would automatically advance the credit, which would be received as a direct deposit or a check by mail. Without this advancing provision, taxpayers would have to wait until they filed their 2020 income tax returns in early 2021 to claim this credit.

The advanced credit amount would be estimated by the Internal Revenue Service (IRS) using the same formula as the 2020 recovery rebates, but based on taxpayers' 2019 income tax return information (if the taxpayer did not file a 2019 income tax return, 2018 income tax return information could be used instead). For Social Security recipients, if neither a 2019 nor a 2018 income tax were filed, then information from their 2019 Social Security Benefit Statement (SSA-1099) could be used instead. If, when taxpayers file their 2020 income tax returns in 2021, they find that the advanced credit is greater than the actual credit, then they would not be required to repay the excess credit. In contrast, if the advanced credit is less than the actual credit, then taxpayers would be able to claim the difference on their 2020 income tax returns.

Taxpayers with gross income less than the standard deduction amount are not required to file a federal income tax return. In general, public cash assistance for low-income populations, such as Supplemental Security Income, is not considered gross income under a limited general welfare exclusion. Hence, many low-income individuals and families whose income is largely from public assistance may not have filed a 2018 or 2019 income tax return and as such, would not receive these rebates in 2020. A 2017 study found that "nonfilers" were more likely to be either seniors or recipients of public assistance compared to those who filed a tax return.