Introduction

The 2017 tax revision, P.L. 115-97, often referred to as the Tax Cuts and Jobs Act, and referred to subsequently as the Act,1 was estimated to reduce taxes by $1.5 trillion over 10 years.2 The Act permanently reduced the corporate tax rate to 21%, made a number of revisions in business tax deductions (including limits on interest deductions), and provided a major revision in the international tax rules. It also substantially revised individual income taxes, including an increase in the standard deduction and child credit largely offset by eliminating personal exemptions, along with rate cuts, limits on itemized deductions (primarily a dollar cap on the state and local tax deduction), and a 20% deduction for pass-through businesses (businesses taxed under the individual rather than the corporate tax, such as partnerships). These individual provisions are temporary and are scheduled to expire after 2025. The Act also adopted temporary provisions allowing the immediate deduction for equipment investment and an increase in the exemption for estate and gift taxes.3

The Congressional Budget Office (CBO) estimated in April of 2018 that the Act would result in a $65 billion reduction in individual income taxes, a $94 billion reduction in corporate taxes, and a $3 billion reduction in other taxes, for a total of $163 billion (after rounding) for FY2018.4

Numerous effects of the Act were projected during consideration of the law and shortly after, including

- an increase in output and investment;

- an increase in the debt to GDP ratio;

- possible benefits for workers from tax cuts for businesses;

- the repatriation of income held abroad by U.S. subsidiaries in the form of dividends; and

- a decreased likelihood of inversions (U.S. companies moving their headquarters abroad).

Some claimed that business investment would increase because of (1) the flow of investment from abroad due to the lower corporate tax rate and (2) no longer imposing a tax penalty on paying dividends from foreign subsidiaries would free up resources.5

This analysis examines the preliminary effects of the Act during the first year, 2018. In some cases it is difficult to determine the effects of the tax cuts (e.g., on economic growth) given the other factors that affect outcomes. In other cases, such as the level of repatriation and use of repatriated funds, the evidence is more compelling. This report discusses these potential consequences in light of the data available after the first year.

Effects on Output and Investment

Projections of Output Effects

During consideration of the Act and subsequently, various claims were made about the growth effects of the tax change. A variety of organizations, including private and government forecasters, projected economic growth rates that tended to be modest. In its April 2018 report on the budget outlook, CBO projected the tax change to increase GDP by 0.3% in calendar year 2018.6 Prorating the FY2019 revenue loss estimate indicated that the tax cut in calendar year 2018 accounted for about 1.2% of GDP. Assuming a tax rate on marginal output of around 20%, this projection would imply a feedback effect of 5%.7

The Joint Committee on Taxation (JCT) also projected the economic effects of the proposal, and while it did not report year-by-year estimates, its revenue feedback effect for calendar year 2018 was larger than that suggested by the CBO numbers—around 20%, which in turn indicates a projected increase in GDP four times larger, 1.2%.8 Given the baseline prior to the Act, that effect would have suggested a growth rate of 4.2% in 2018.

The CBO output estimate (i.e., the amount of GDP growth attributed to the tax change) was compared with projections by other forecasters and organizations. Of the seven other forecasts projecting the effects of the Act for 2018, five ranged from 0.3% to 0.5%, one was for 0.1%, and another for 0.8%.9

CBO also disaggregated its output effect into an increase in potential GDP of 0.2%, with the remaining 0.1% reducing the gap between output with and without full employment. The increase in potential output reflects increases in investment and in the labor supply. The 0.1% increase might be characterized as a demand-side effect and the remainder as a supply-side effect. Because the economy was at full employment and most of the tax cut went to businesses and higher-income individuals who are less likely to spend the increases, a small demand-side effect would be expected. Demand-side effects are transitory, whereas supply-side effects are permanent.

CBO and other organizations also produced longer-term forecasts. CBO projected output effects rising to 0.6% in 2019, then rising slightly and peaking in 2022, and finally declining, with an estimated 0.5% effect in 2028, the last year reported. The decline in later years might be partially traced to the expiration of some provisions. Compared with other forecasts for the average over the 10-year period 2018-2027, CBO's 0.7% effect was similar to other forecasts.10 For the 10th year, 2027, CBO projected an effect of 0.6%; there was considerably more divergence in the estimates for this year, with one organization projecting a negative effect by that time. This divergence presumably reflected competing views of the effects on capital formation due to lower tax rates on returns to investment and crowding out of private investment due to accumulating debt.11

During the debate, some argued for much larger growth effects, including arguments that the tax cuts would produce so much growth that they would largely or entirely pay for themselves, or even raise revenues.12 These statements, however, were not supported by most of the published analysis.

Output Growth in 2018

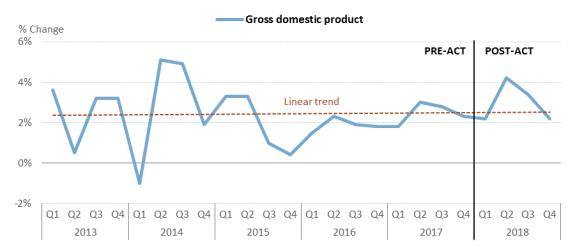

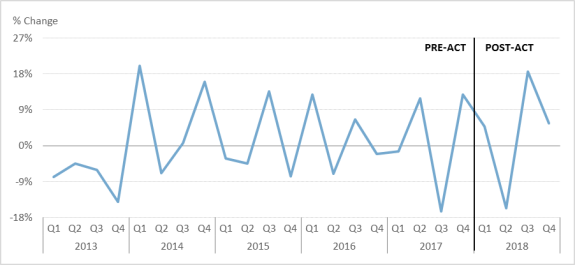

In April 2018, CBO projected real GDP growth for the calendar year 2018 of 3.3% (indicating a projected 3% growth rate without the tax cut). According to the National Income and Product Accounts (NIPA), actual growth rate was 2.9%, which is consistent with a small effect of the tax revision, perhaps even smaller than projected by most analysts. Quarterly growth rates are shown in Figure 1. The revenue loss from the tax cut without incorporated growth effects was estimated at about 1.2% of GBP in 2018.13

The 2.9% annual growth rate for 2018 was higher than the 2.2% growth rate in 2017 and the 1.6% growth rate in 2016. In previous years, output grew by 2.9% in 2015 and 2.5% in 2014, thus the increase in growth is in line with the trend in growth over the period examined in Figure 1. Forecasters had already projected an increase in growth rates in most cases that was similar to CBO's. In addition to the effect from the tax cuts, there was also some stimulus due to the increase in spending enacted in the Consolidated Appropriations Act of 2018 (P.L. 115-141) and the Bipartisan Budget Act of 2018 (P.L. 115-123). Growth may have also been negatively affected by tariffs.14

The high rate of growth in the second quarter of 2018 shown in Figure 1 may have been due to the demand-side stimulus of the tax cuts, which began to be reflected in withholding beginning in the first quarter, as well as the possibly delayed receipt of tax refunds.

On the whole, the growth effects tend to show a relatively small (if any) first-year effect on the economy. Although examining the growth rates cannot indicate the effects of the tax cut on GDP, it does tend to rule out very large effects in the near term.

The data appear to indicate that not enough growth occurred in the first year to cause the tax cut to pay for itself. Assuming a tax rate of 18% (based on CBO estimates), and estimating the tax cut to reduce revenue in calendar year 2018 by about 1.2% of GDP, a 6.7% GDP increase due to the tax cuts alone would be required.15 Rather, the combination of projections and observed effects for 2018 suggests a feedback effect of 0.3% of GDP or less—5% or less of the growth needed to fully offset the revenue loss from the Act.

Contribution of Consumption Growth

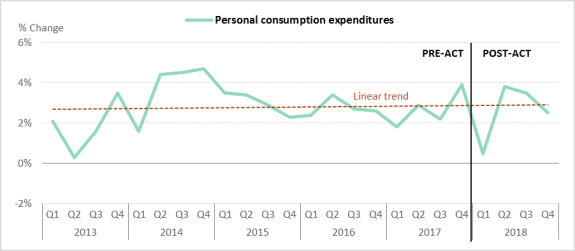

Consumption grew at 2.6% in 2018 in real terms, as shown in Figure 2, about the same as 2017 (which was 2.5%) and below 2014-2016 (although higher than 2013). As shown in Figure 2, there was a drop in the first quarter followed by a rise in the second quarter that was unexpected by most forecasters and may have reflected a delay in tax refunds.16 The initial effect of a demand side is likely to be reflected in increased consumption and the data indicate little growth in consumption in 2018. Much of the tax cut was directed at businesses and higher-income individuals who are less likely to spend. Fiscal stimulus is limited in an economy that is at or near full employment.

Contribution of Investment Growth

Although it is difficult to determine the Act's overall first-year impact on GDP, other than to confirm that the evidence is consistent with a small projected first-year effect, it is possible to discuss supply-side effects on investment in more detail.

CBO estimated that the 0.3% increase in growth from the Act is the result of a 0.4% increase in GDP due to private consumption and a 0.2% increase due to nonresidential fixed investment (with a negligible effect on residential investment and government consumption and investment). This 0.6% increase was projected to be offset by a decrease in net exports of 0.3% of GDP (from both a decline in imports and an increase in exports). This decrease is expected as a consequence of net capital flowing in from abroad to finance the deficit or due to capital inflows used for investment in response to tax changes.

Given the shares of GDP that went to consumption (70%) and investment in nonresidential fixed investment (14%) in 2017, these growth contributions indicated an additional growth in consumption of 0.7% and in fixed nonresidential investment of 1.5%.

In 2018, consumption grew at 2.6% and nonresidential investment grew at 7%. Such numbers might suggest a supply-side effect. There are reasons, however, not to necessarily view that growth as a supply-side effect of the tax change.

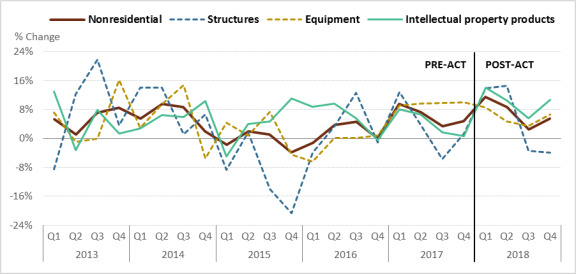

First, the growth rates of investment and its subcomponents are much more volatile than the growth rates of GDP, as shown in Figure 3, making it hard to assign causation.

Second, the largest effects occurred in the first and second quarters of 2018, which allowed very little time to be the result of investments that must be planned in advance (even if the tax cut was anticipated in late 2017). Furthermore, structures growth rates were negative in the last two quarters.

Third, real growth in the subcategories of equipment, structures, and intellectual property products is inconsistent with the incentive effects of the tax change. Over the entire year, intellectual property products grew at the fastest rate (7.7%), equipment at a slightly lower rate (7.5%), and structures at 5.0%. To assess the incentive effects of the tax changes (which included a lower tax rate and faster depreciation for equipment), consider the change in the user cost of capital (or rental price of capital). It is the equivalent of the "price" of capital as an input (just as the wage is the price of labor input). It includes two costs of using capital: the opportunity cost of using funds (i.e., the required pretax rate of return on the asset) and depreciation (i.e., the cost of using up the asset). The user cost reflects the required rate of return at the margin (i.e., for an investment that earns just enough to be worth making). Estimates indicate that the user cost of capital for equipment declined by 2.7% and the user cost of structures declined by 11.7%, but the user cost of R&D (intellectual property products) increased by 3.4%. (See the Appendix for details on the derivation of these results.) The user cost of capital for equipment declined by less than that of structures primarily because more of the cost for equipment is for depreciation.17 The decline in the required rate of return was somewhat smaller for equipment as well because it was already favorably treated (eligible for expensing half of the cost). The benefits of lower rates are also moderated by the use of debt-financed capital, where a lower tax rate reduces the subsidy (or negative tax rate) that applies to debt-financed investment because of the deduction of nominal interest by businesses.

Thus, while it is possible that the Act increased the investment due to supply-side effects, it would be premature to conclude that the higher rate of growth of nonresidential fixed investment was due to the tax changes. Looking at changes in the user cost of capital, effects of investments in structures would be expected to be largest, with small (or negative) effects on intellectual property. To date this pattern has not been observed.

Effects on Revenues

Overall revenue changes were close to projections, with revenues only $9 billion smaller than projected, due to a $45 billion increase in individual income tax revenues, but a $7 billion decrease in payroll taxes, along with a $40 billion decline in corporate revenues.

As noted above, data on GDP are not consistent with a large growth effect in 2018, and thus the tax cut is unlikely to provide enough growth to significantly offset revenue losses in 2018. Data from FY2018 suggest that the tax cut for corporations may have been larger than the $94 billion CBO projected in its April 2018 baseline. That baseline projected corporate revenues of $243 billion, but actual corporate revenues were $38 billion lower at $205 billion, 16% lower than projected. CBO's January 2019 report on the budget and economic outlook indicated that these lower corporate tax revenues could not be explained by economic conditions and stated that the causes will not be apparent until information from tax returns becomes available over the next two years.18 CBO also expected this decline in revenues to dissipate over time. With little evidence of whether the decline will actually be temporary or permanent, CBO may have relied on the historical tendency of unexplained changes to dissipate over time. It is also possible that estimated revenue losses from the corporate tax changes were too low in their earlier estimates.

The overall revenues were close to those projected as the lower corporate revenues were offset by gains from other taxes: a $45 billion increase in individual income tax revenues and a $7 billion decrease in payroll taxes. These differences, particularly for payroll taxes, are much smaller as a percentage of revenue, and CBO does not indicate any need for an explanation of these changes outside of economic forces.

Effects on Effective Tax Rates

Effective tax rates fell, with corporate effective tax rates declining significantly and individual effective income tax rates by a small amount.

Effective Corporate Tax Rate

Much of the tax revision was focused on corporations. Although the statutory corporate tax rate was reduced from 35% to 21%, the average effective tax rate decline (taxes divided by profits) would be smaller because of existing tax benefits (which lead to a smaller initial effective tax rate) and base-broadening effects. Such an effective tax rate can be calculated using aggregate data from the national income and products accounts, which attempt to measure economic income. The effective average tax rate for corporations was 17.2% in calendar year 2017, and fell to 8.8% in calendar year 2018.19 This estimate includes worldwide income, but not worldwide taxes. Although actual data on the division of domestic and worldwide income are not available for 2018, using the ratios projected by CBO to eliminate foreign-source income from the measure results in an average effective tax rate of 23.4% in 2017, falling to 12.1% in 2018.20 Either scenario suggests that the ratio of effective to statutory tax rate dropped following the tax revision. The statutory tax rate dropped by 40%, but the effective rate dropped by 48% (although the percentage point drop was smaller for the effective tax rate).

Another measure of effective rate is the marginal effective tax rate on income, a tax rate that is a component of the user cost of capital. These tax rates are prospective and capture the main elements of the tax code: tax rates, depreciation, and research credits. They also apply to domestic investment. Using a weighted average of equipment, structures, and intangibles, the effective marginal tax rate on equity investment was estimated to fall from 15.6% to 3.2% from 2017 to 2018.21 If the effects of reducing subsidies for debt-financed investment are accounted for, marginal tax rates are lower (actually slightly negative) and change less, from a -0.3% rate in 2017 to a -6.6% rate in 2018. Marginal tax rates are likely to be below average tax rates because they capture timing benefits (e.g., accelerated depreciation). Marginal effective tax rates are relevant to economic growth effects because they measure the incentive effects for investment.

Effective Individual Income Tax Rates

The individual income tax changes for 2018 were smaller than the corporate tax changes in absolute size and substantially smaller as a percentage of income. The effective individual tax rate for federal income taxes as a percentage of personal income is estimated at 9.6% in 2017 and 9.2% in 2018, based on data in the National Income and Product Accounts. This change constitutes a reduction in effective tax rate of 4%.22 The Treasury Department's Office of Tax Analysis estimates a larger reduction in effective tax rate as a percentage of adjusted family cash income, with the rate falling from 10.1% in 2017 to 8.9% in 2019, although this estimate is based on projected rather than actual data.23 Both of these declines are smaller than the corporate tax rate decline. As noted earlier, the increase in the standard deduction and child and dependent credit was roughly offset by the elimination of the personal exemption. Statutory rate reductions for individuals were relatively small compared with the corporate rate reduction (the top rate of 39.6% was reduced by 2.6 percentage points, compared with 14 percentage points for the corporate rate), and the benefits of rate reductions were offset by restrictions on itemized deductions. Business income was in some cases eligible for a 20% reduction, which was more significant (an additional 20% deduction at the 37% rate is 7.4 percentage points), but not all business income qualified.24

There are also effective marginal tax rates, although these are generally divided into rates on labor income and capital income. The marginal tax rate for labor income is typically above the average tax rates because of graduated tax rates and lack of timing benefits. CBO estimates that marginal tax rates on labor income fell from 29.4% to 27.2%.25 CBO also estimates the marginal tax rate for all capital income (which would include unincorporated businesses, owner-occupied housing, and taxes on interest, dividends, and capital gains, as well as corporate taxes). This value is estimated to fall from 16.5% to 14.7%.26 Although different from the marginal rates reported above for corporations, both estimated measures find small changes in marginal tax rates, which is consistent with an expected small behavioral response.

Effects on Wages

Distributional analyses of the tax change suggested that the tax revision favored higher-income taxpayers, in part because most of the tax cut benefited corporations and in part because the individual income tax cut largely went to higher-income individuals.27 During the debate about taxes, however, arguments were made that these corporate tax cuts would benefit workers due to growth in investment and the capital stock.

After enactment, CBO projected these effects to be relatively small, with increases in labor productivity (which should affect the wage rate) negligible in 2018 and growing to 0.3% of GDP after 10 years. CBO projected that the total wage bill would grow because of the increase in employment and hours per worker of 0.2% in 2018. The labor supply response would rise through 2024, peaking at 0.8% and then decline as the individual tax cuts expired.28

A Council of Economic Advisors (CEA) October 2017 study suggested a corporate rate reduction from 35% to 20%, if enacted, would eventually increase the average household's income by a conservative $4,000 a year.29 This was a longer-run estimate, but the study also estimated that workers would immediately get a significant share (30%) of the profits repatriated from abroad due to tax changes. Another CEA October 2017 report suggested wages could increase by up to $9,000 with such a corporate rate change using more optimistic assumptions.30 While the CEA study with respect to the $4,000 to $9,000 amounts referred to a long-term effect, the study was portrayed by the Administration as indicating an immediate effect.31 The amounts associated with repatriation were short term. A $4,000 to $9,000 effect per household, given the 126 million households that were estimated at that time, would produce a total effect ranging from $504 billion to $1,134 billion, or between 2.5% and 5.7% of GDP in 2018.32 The corporate rate cut from 35% to 21% cost about $125 billion over a full year, and it would cost about $133 billion with the additional percentage point rate reduction (to 20%) considered at that time. Thus, in these scenarios, the effects of the tax cuts would be many times (3.8 to 8.5) larger than the costs. The projections for long-run growth in the CEA study relied on a range of empirical economics literature, including the effects of changes in user cost on investment cost and corporate tax incidence. The econometric estimates of corporate tax incidence are problematic for a number of reasons,33 and the effects on investment considering user cost did not appear to take into account the direct effect of the tax rate change on the interest.

In the absence of the tax cuts, wages should grow with the economy and wage rates should grow as the capital stock grows. In addition, tight labor markets resulting from the approach to full employment should have put upward pressure on wage rates in any case. Evidence from 2018 indicated that labor compensation, adjusted to real values by the price indices for personal consumption expenditures, grew slower than output in general, at a 2.3% rate compared with a 2.9% growth rate overall. If adjusted by the GDP deflator, labor compensation grew by 2.0%. With labor representing 53% of GDP, that implies that the other components grew at 3.8%.34 Thus, pretax profits and economic depreciation (the price of capital) grew faster than wages.

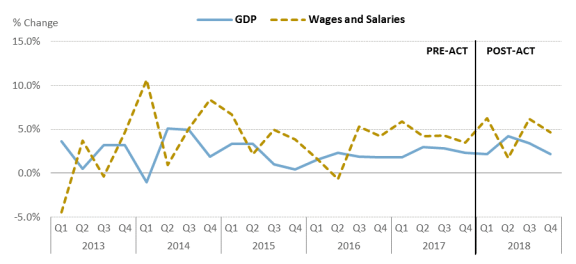

Figure 4 shows the growth rate of real wages compared with the growth rate of real GDP for 2013-2018, indicating that wage growth has sometimes been faster than GDP growth and sometimes slower. There is no indication of a surge in wages in 2018 either compared to history or relative to GDP growth. This finding is consistent with the CBO projection of a modest effect.

The Department of Labor reports that average weekly wages of production and nonsupervisory workers were $742 in 2017 and $766 in 2018.35 Wages, assuming full-time work, increased by $1,248 annually. But this number must account for inflation and growth that would otherwise have occurred regardless of the tax change. The nominal growth rate in wages was 3.2%, but adjusting for the GDP price deflator, real wages increased by 1.2%. This growth is smaller than overall growth in labor compensation and indicates that ordinary workers had very little growth in wage rates.

Effects on Repatriation and International Investment Flows

One of the major sources of anticipated increased investment through supply-side effects is international capital flows, particularly in the short and medium term. Savings rates tend to be relatively unresponsive to changes in the rate of return and savings accumulate slowly. Thus the increased investment in the United States (in the aggregate) would need to come from abroad. Some expected foreign investment to flow due to the reduction in the user cost of capital.

Some also argued that eliminating the tax barrier to repatriating funds (as was done with the tax revision) would lead to reinvestment in the United States of unrepatriated earnings held abroad in U.S. subsidiaries.36 Under prior law, these earnings would have been taxed at 35%, adjusted for credits on foreign taxes paid, if paid as dividends to the parent company. The tax change exempted dividends from tax, imposed a transition tax on deemed repatriations of existing untaxed earnings at a rate lower than the new corporate rate of 21% (15.5% on liquid assets and 8% on illiquid assets), and imposed a global minimum tax on intangible income. These changes meant paying dividends resulted in no tax consequences. Although estimates varied, they indicated close to $3 trillion of unrepatriated earnings.37 There were a number of criticisms of the possibility that repatriation of these earnings would stimulate investment, considering the evidence that a repatriation holiday in 2004 had not affected investment.38

Not all of these amounts were held in cash, as some were earnings reinvested in physical assets (such as plant and equipment) and some might be invested in other assets that were not cash equivalents. A Federal Reserve study estimated that $1 trillion was held in cash.39

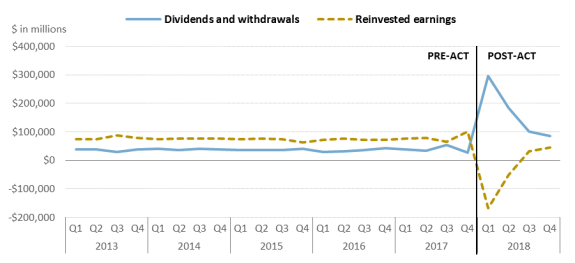

A significant amount of repatriations occurred in 2018, as compared both to history and 2017. Dividends in the previous three years ranged from $144 billion to $158 billion, as shown in Figure 5, whereas $664 billion was repatriated in 2018. Simultaneously, reinvested earnings declined sharply before returning to more normal levels in the 4th quarter of 2018.

|

Figure 5. Repatriations, First Quarter 2013 through Fourth Quarter 2018 |

|

|

Source: Table 4.1 Bureau of Economic Analysis. |

It is important, however, to measure international capital flows in true terms that reflect the inflow of resources for capital investment and not by financial transactions, such as repatriation of income earned abroad through dividend payments from foreign subsidiaries.40 Capital investment involves resources that reflect actual investment in the United States. It could involve imports of investment goods directly, or it could involve imports of consumption goods that free up other resources for investment. In either case, the true capital invested in the United States is largely measured by the excess of exports over imports, or more precisely by the current account, which can also include a small amount of net income payments. In more fundamental terms, investment from abroad occurs in a real sense only when the amount of imported goods exceeds the amount of U.S. exports.

To measure this aggregate change in net capital inflows, examine the balance on the current account, which is generally negative, indicating a net capital inflow (imports exceed exports, or a trade deficit). Adjusting these amounts by the GDP deflator and looking at the change, there was a small increase that amounted to 0.8% of private investment. This change is relatively small and is not out of line with historical fluctuations; see Figure 6.

|

Figure 6. Change in Net Capital Inflows, First Quarter 2013 Through |

|

|

Source: Tables 1.1.6 and 1.1.4 (NIPA); International Transactions 1.1. |

Again, many factors can affect net capital inflows, including domestic borrowing by the government and domestic saving, but the evidence does not suggest a surge in investment from abroad in 2018.

Use of Funds for Worker Bonuses and Share Repurchase

Increased funds, whether accessed from abroad or through tax cuts, could be used in several ways: investment, paying down debt, increasing wages, paying wage bonuses, paying dividends, or repurchasing shares.

During the passage of the tax revision and in the immediate aftermath, some argued that firms would use these funds to pay worker bonuses (as discussed in the previous section on wages). Subsequently, a number of firms announced bonuses, which in some cases they attributed to the tax cut. One organization that tracks these bonuses has reported a total of $4.4 billion.41 With US employment of 157 million, this amount is $28 per worker.42 This amount is 2% to 3% of the corporate tax cut, and a smaller share of repatriated funds.43 It is consistent with what most economists would expect that a small percentage of increased corporate profits or repatriated funds (if any) would be used to compensate workers, as economic theory indicates that firms would pay workers their marginal product, a result of fundamental supply and demand forces.44 The bonus announcements could have reflected a desire to pay bonuses when they would be deducted at 35% rather than 21% (in late 2017 for firms with calendar tax years but in 2018 for firms with different tax years). Worker bonuses could also be a result of a tight labor market and attributed to the tax cut as a public relations move.

Much of these funds, the data indicate, has been used for a record-breaking amount of stock buybacks, with $1 trillion announced by the end of 2018.45 A similar share of repurchases happened in 2004, when a tax holiday allowed firms to voluntarily bring back earnings at a lower rate.46

Effects on Inversions

During the discussion of corporate tax revision over a number of years, one important issue repeatedly raised was the effect of the current tax system on incentives for firms to relocate abroad, or "invert."47 Inversions involved firms relocating their headquarters to low-tax jurisdictions that generally had territorial taxes, allowing firms to shift profits out of their U.S. operations (so-called earnings stripping) as well as providing potential paths to repatriate earnings without taxes. The earliest of these inversions, beginning in the early 1980s, were called "naked inversions," where a company simply relocated its headquarters without otherwise changing its activities. A number of legislative and regulatory actions largely ended these types of inversions. In 2004, the American Jobs Creation Act (P.L. 108-357) required that any firm in which the former U.S. owners owned 80% or more of the new firm would continue to be treated as a U.S. firm. Firms with 60% to 80% ownership by former shareholders of the U.S. firm were considered inverted firms and subject to certain penalty taxes. This legislation allowed naked inversions in cases where the firm had substantial business activity in the new headquarters country, but regulations issued in 2012 tightened these requirements after a series of inversions used this rule to relocate.

In 2014, a new wave of inversions that involved mergers with smaller foreign firms began, with one of the most prominent being an announcement that Pfizer, the pharmaceutical company, would acquire Astra-Zeneca with a UK headquarters (although this merger never took place).

These inversions gave rise to a number of legislative proposals, but also led to numerous regulatory proposals, which were released in 2014, 2015, and 2016. These regulations addressed a number of issues, including restricting the use of serial inversions to allow a firm to fall under the ownership limits, limiting the ability to access earnings of subsidiaries abroad, and limiting earnings stripping through locating debt in the United States.

The 2017 Act contained several provisions that made inversions less attractive (aside from the lower corporate tax rate). One notable provision required firms that inverted in the next 10 years to pay a deemed repatriation tax at 35%, rather than at the lower rates of 8% for non-cash holdings and 15.5% for cash or cash equivalents.

The Act introduced a new minimum tax to address international profit shifting, the base erosion and anti-abuse tax (BEAT), which adds back payments between related domestic and foreign companies to base income and then taxes that base at a lower rate. BEAT excludes payments which reduce gross receipts with the result that payment for the cost of goods sold is not included under BEAT. An exception applies for firms that invert after November 9, 2017, where payments to a foreign parent or any foreign firm in the affiliated group for cost of goods sold is included in BEAT. The legislation also contained some other provisions making inversions less attractive.

The Act also modified asset attribution rules. The constructive ownership rules for purposes of determining 10% U.S. shareholders, whether a corporation is a Controlled Foreign Corporation (CFC), and whether parties satisfy certain relatedness tests, which can trigger certain tax provisions including restrictive ones, were expanded in the 2017 tax revision. Specifically, the new law treats stock owned by a foreign person as attributable to a U.S. entity owned by the foreign person (so-called "downward attribution"). As a result, stock owned by a foreign person may generally be attributed to (1) a U.S. corporation, 10% of the value of the stock of which is owned, directly or indirectly, by the foreign person; (2) a U.S. partnership in which the foreign person is a partner; and (3) certain U.S. trusts if the foreign person is a beneficiary or, in certain circumstances, a grantor or a substantial owner.

The downward attribution rule was originally conceived to deal with inversions. In an inversion, without downward attribution, a subsidiary of the original U.S. parent could lose CFC status if it sold enough stock to the new foreign parent so the U.S. parent no longer had majority ownership. With downward attribution, the ownership of stock by the new foreign parent in the CFC is attributed to the U.S. parent, so that the subsidiary continues its CFC status, making it subject to any tax rules that apply to CFCs (such as Subpart F and repatriation taxes under the old law, and Subpart F and Global Low-Taxed Income (GILTI) under the new law).

The Act also contained other provisions affecting stockholders and stock compensation. These provisions were intended to discourage inversions. Dividends (like capital gains) are taxed at lower rates than ordinary income. The rates are 0%, 15%, and 20% depending on the rate bracket that ordinary income falls into. Certain dividends received from foreign firms (those that do not have tax treaties and Passive Foreign Investment Companies (PFICs)) are not eligible for these lower rates. Dividends paid by firms that inverted after the date of enactment of P.L. 115-97 are added to the list of those not eligible for the lower rates. Also, in 2004, an excise tax of 15% was imposed on stock compensation received by insiders in an expatriated corporation; the 2017 Act increased it to 20%, effective on the date of enactment for corporations that first become expatriated after that date.

These new laws did not change the definition of inverted firms but rather the consequences of inversions.

Although the legislative changes in the 2017 Act contributed to making inversions less attractive, announced inversions had already slowed substantially following the regulatory changes implemented in 2014, 2015, and 2016.48 In addition, data released by the Bureau of Economic Analysis indicated that foreign acquisitions of US companies, which rose substantially in 2015, fell by 15% in 2016 and 32% in 2017 (data not available for 2018). Some of the largest declines were in inversion-associated countries, such as Ireland, where acquisitions fell from $176 billion in 2015, to $35 billion in 2016, and to $7 billion in 2017.49

Appendix. The User Cost of Capital

The user cost of capital is the sum of the pretax required return for a marginal investment and the economic depreciation, or

(1) C = R/(1-t)+d

Where C is the user cost, R is the required after-tax return, t is the effective marginal rate, and d is the economic depreciation rate. Economic depreciation is the decline in the value of the asset in real terms, and belongs in the cost term because it compensates the investor for the wearing away, or using up, of the asset. The user cost calculations use a weighted pretax rate of return that reflects both debt and equity finance to simplify the analysis. The effective marginal tax rate, in turn, depends on the statutory tax rate, the present value of economic depreciation, the inflation rate, the return on equity, the share debt-financed, and the nominal interest rate.

Table A-1 reports the effective tax rate for corporate and non-corporate investment before and after the 2017 changes for the basic types of nonresidential fixed capital.

|

Asset Type |

Pre-2017 Law Corporate |

Pre-2017 Law Non-corporate |

Post-2017 Law Corporate |

Post-2017 Law Non-corporate |

||||||

|

Equity Financed |

||||||||||

|

Equipment |

13.4 |

|

|

|

||||||

|

Public Utility Structures |

14.2 |

|

|

|

||||||

|

Nonresidential Structures |

30.8 |

|

|

|

||||||

|

Intangibles |

-63.3 |

|

|

|

||||||

|

Debt and Equity Financed |

||||||||||

|

Equipment |

-0.9 |

|

|

|

||||||

|

Public Utility Structures |

-0.9 |

|

|

|

||||||

|

Nonresidential Structures |

19.2 |

|

|

|

||||||

|

Intangibles |

-116.3 |

|

|

|

Source: CRS calculations. For detail on method of calculations including economic depreciation rates and data on capital stocks, see CRS Report R44242, The Effect of Base-Broadening Measures on Labor Supply and Investment: Considerations for Tax Reform, by Jane G. Gravelle and Donald J. Marples.

Notes: Corporate tax rates of 34.14% in pre-2017 law (reflecting the production activities deduction) and 21% in new law; noncorporate tax rates of 37% in prior law and 30% in current law (based on information provided by the Congressional Budget Office). Real after-tax rate of return 7% for equity; interest rate 7.5%, inflation rate 2%. Debt weighted at 36%.

The overall user cost also depends on the economic depreciation rates and the relative sizes of each type of capital stock in the corporate and non-corporate sector. For equipment, the economic depreciation rate is 12.95% per year, and corporate equipment comprises 67% of all equipment. Structures are composed of two types: (1) public utility structures (accounting for 23% of the total) with a depreciation rate of 2.24% and (2) buildings with a depreciation rate of 2.8%. Within public utility structures, corporations account for 84%; within buildings, corporate structures account for 55%. Intangible assets have a depreciation rate of 17%, and corporations account for 86%. User costs and their percentage changes are shown in Table A-2.