Figure 1. Dividends and Reinvested Earnings, U.S. Multinational Companies, Quarterly Flows

(in billions of dollars)

Source: CRS, with data from the Bureau of Economic Analysis.

Recent economic forecasts project a mild slowing in global economic growth in 2019, centered mostly in developed economies and Asia, according the International Monetary Fund (IMF) and the Organization for Economic Co-operation and Development (OECD), as indicated in Table 1. The IMF April 2019 forecast of global economic growth in 2019 and 2020 projects a growth rate of 3.3% and 3.6%, respectively, down about 0.2 percentage points (pp) from previous forecasts. It also forecasts global trade growth of about 3.4%, and a fall in energy prices of about 13%. IMF April 2019 forecast for global economic growth rates were lower by an additional 0.2 pp from earlier forecasts due to a slowing in the global economy during the second half of 2018. The OECD is forecasting that global growth will slow to 3.3% in 2019 and 3.4% in 2020, also a decline of about 0.2 pp from previous projections.

The OECD and IMF argue that various risks weigh on global economic growth. These risks include escalation in trade tensions, tightening financial conditions, monetary policy mismatches between central banks (some central banks are raising interest rates and reducing monetary stimulus while others are doing the opposite), high levels of personal and public debt, uncertainty over the potential impact of a no-deal withdrawal of the United Kingdom from the European Union (Brexit) and a slowdown in China's rate of growth.

The U.S. economy, which outperformed other developed economies in 2018 with an estimated 2.9% rate of growth, is projected by the OECD and the IMF to experience a slower growth in 2019 and 2020. Similarly, the Federal Reserve forecasted in March 20, 2019, the U.S. economy would grow by 2.1% in 2019, down from a previous forecast of 2.3%. Some economic indicators suggest the U.S. economy remains comparatively strong, but a deterioration in the economies of major trading partners could negatively affect the U.S. economy and alter these forecasts. Broad financial and economic linkages tie the U.S. and global economies, which means the United States affects and is affected by events in the global economy. These effects are reflected in capital flows, the international exchange value of the dollar, interest rates, and U.S. trade balances.

|

OECD Forecast |

IMF Forecast |

||||

|

2018 |

2019 |

2020 |

2019 |

2020 |

|

|

World Output |

3.7% |

3.3% |

3.4% |

3.3% |

3.6% |

|

Advanced Economies |

2.3 |

3.5 |

3.7 |

1.8 |

1.7 |

|

United States |

2.9 |

2.6 |

2.2 |

2.3 |

1.9 |

|

Euro Area |

1.8 |

1.0 |

1.2 |

1.3 |

1.5 |

|

Germany |

1.5 |

0.7 |

1.1 |

0.8 |

1.4 |

|

France |

1.5 |

1.3 |

1.3 |

1.3 |

1.4 |

|

Italy |

1.0 |

-0.2 |

0.5 |

0.1 |

0.9 |

|

United Kingdom |

1.4 |

0.8 |

0.9 |

1.2 |

1.4 |

|

Japan |

0.9 |

0.8 |

0.7 |

1.0 |

0.5 |

|

Asia |

6.5 |

NA |

NA |

6.3 |

6.3 |

|

China |

6.6 |

6.2 |

6.0 |

6.3 |

6.1 |

|

India |

7.3 |

7.2 |

7.3 |

7.3 |

7.5 |

|

Latin America |

1.1 |

NA |

NA |

1.4 |

2.4 |

|

Middle East |

2.4 |

NA |

NA |

1.5 |

3.2 |

Source: Organisation for Economic Co-operation and Development and International Monetary Fund.

Note: The OECD forecast for advanced economies constitutes the G-20 group of countries, which includes China.

Among developed economies, Germany, France, Italy, and the United Kingdom are projected to experience slower growth in 2019. The European Central Bank lowered its forecast for economic growth in Europe in 2019 to 1.1%, down from 1.7% forecasted in December 2018. Growth in European countries is expected to be affected by domestic political issues, slower economic growth in export markets, and continuing uncertainty over the economic impact of Brexit. Japan is projected to experience a more positive rate of growth in 2019 compared with 2018, but the rate is projected to fall by half in 2020 to 0.5%. Currency traders reportedly are concerned about a "flash crash" in the value of the yen in late April, when bond and equity markets in Japan will be closed for 10 days for a "Golden Week" holiday to observe the ascension of a new Emperor. The immediate impact on the yen is expected to be short-lived, but currency movements could increase long-term volatility in the yen.

Developing economies in Latin America and the Middle East are projected to sustain or slightly increase recent rates of economic growth in 2019. Economic sanctions on Iran and Venezuela, however, add to uncertainties about economic growth and price volatility in energy markets. Volatility in energy prices and risks in commodity markets associated with slower economic growth in Europe and Asia could negatively affect countries dependent on commodity exports. Of particular concern is the pace at which China's growth rate slows. China's growing role in the global economy means it has far-reaching influence through its trade and financial relations. As China's rate of growth slows, it likely will import fewer raw materials, with secondary and other effects on commodity exporters. These effects would be compounded by a slowdown in the rate of growth in Europe and the United States, which likely would reduce further China's rate of growth.

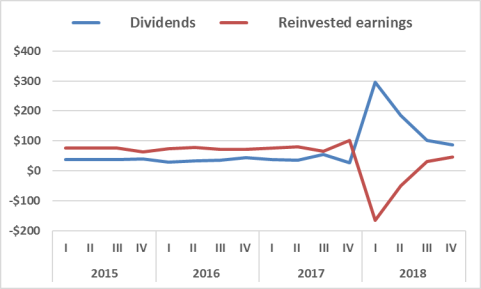

Uncertainties concerning the pace of global economic growth and the relative strength of U.S. growth rates and interest rates are reverberating through financial markets as investors seek safe returns. Over the past year, investors reportedly have moved out of Chinese and European stocks in favor of dollar-denominated assets. Also, the Bureau of Economic Analysis reports that U.S. multinational companies (USMNCs)

|

Figure 1. Dividends and Reinvested Earnings, U.S. Multinational Companies, Quarterly Flows (in billions of dollars) |

|

|

Source: CRS, with data from the Bureau of Economic Analysis. |

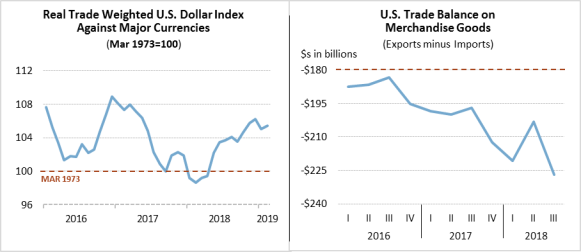

Increasing demand for the dollar and dollar-denominated assets supported an appreciation of the dollar of about 7% between the end of 2017 and early 2019, as indicated in Figure 2. In 2018, dollar appreciation and sustained demand for imports relative to external demand for U.S. exports widened the U.S. merchandise trade deficit to $891 billion in 2018.

|

|

Source: CRS, with data from the Federal Reserve Bank of St. Louis and the Census Bureau. |