Federal budget decisions express the priorities of Congress and reinforce its influence on federal policies. Making budgetary decisions for the federal government is a complex process and requires the balance of competing goals. The Great Recession adversely affected federal budget outcomes through revenue declines and spending increases from FY2008 through FY2013. The federal budget recorded a deficit of 9.8% of gross domestic product (GDP) in FY2009, the largest value since World War II.1 Subsequent improvement of the economy and implementation of policies designed to lower spending have improved the short-term budget outlook, though federal deficits remain at relatively high levels. In FY2017, the federal budget recorded a deficit of 3.5% of GDP, which was higher than the average deficit since FY1947 (2.7% of GDP).

Over the next several years, projections of a continued decline in discretionary spending are more than offset by increases in mandatory spending, increases in net interest payments, and reductions in revenues, leading to a rise in federal deficits. Increases in the long-term cost of federal retirement and health care programs and debt servicing costs each contribute to upward pressure on federal spending levels. Operating these programs in their current form may pass on substantial economic burdens to future generations. Revenues are projected to decline as a percentage of GDP over the next several years before increasing later in the 10-year budget window as provisions enacted by the 2017 tax revision (P.L. 115-97) are scheduled to expire. Congress and the President may consider proposals for deficit reduction if fiscal issues remain a key item on the legislative agenda.

This report summarizes issues surrounding the federal budget, examines policy changes relevant to the budget framework for FY2019, and discusses recent major policy proposals included in the President's FY2019 budget. It concludes by addressing major short- and long-term fiscal challenges facing the federal government.

Overview

Each fiscal year Congress and the President engage in a number of practices that influence short- and long-run revenue and expenditure trends. This section describes the budget cycle and explains how budget baselines are constructed. Budget baselines are used to measure how legislative changes affect the budget outlook and are integral to evaluating these policy choices.

Budget Cycle2

Action on a given year's federal budget, from initial formation by the Office of Management and Budget (OMB) until final audit, typically spans four calendar years.3 The executive agencies begin the budget process by compiling detailed budget requests, overseen by OMB. Agencies work on their budget requests in the calendar year before the budget submission, often during the spring and summer (about a year and a half before the fiscal year begins). The President usually submits the budget to Congress around the first Monday in February, or about eight months before the beginning of the fiscal year, although submissions are often later in the first year of an Administration.4

Congress typically begins formal consideration of a budget resolution once the President submits the budget request. The budget resolution is a plan, agreed to by the House and Senate, which establishes the framework for subsequent budgetary legislation. Because the budget resolution is a concurrent resolution, it is not sent to the President for approval.5 If the House of Representatives and Senate cannot agree on a budget resolution, a substitute measure known as a "deeming resolution" may be implemented by each chamber, which may give force to certain budget enforcement measures.6

House and Senate Appropriations Committees and their subcommittees usually begin reporting discretionary spending bills after the budget resolution is agreed upon. Appropriations Committees review agency funding requests and propose levels of budget authority (BA).7 Appropriations acts passed by Congress set the amount of BA available for specific programs and activities. Authorizing committees, which control mandatory spending, and committees with jurisdiction over revenues also play important roles in budget decisionmaking.8

During the fiscal year, Congress and OMB oversee the execution of the budget.9 Once the fiscal year ends on the following September 30, the Department of the Treasury and the Government Accountability Office (GAO) begin year-end audits.

Budget Baseline Projections

Budget baseline projections are used to project the future influence of current laws and measure the effect of future legislation on spending and revenues. They are not meant to predict future budget outcomes. Baseline projections are included in both the President's budget and the congressional budget resolution. It is important to understand the assumptions and components included in budget baselines. In some cases, slight changes in the underlying models or assumptions can lead to large effects on projected deficits, receipts, or expenditures.

The Congressional Budget Office (CBO) computes current-law baseline projections using assumptions set out in budget enforcement legislation.10 On the revenue side of the budget, the 2017 tax revision (P.L. 115-97; see additional discussion below) enacted several changes to individual and corporate income tax rates and to other tax policy provisions that are set to expire before the end of the 10-year budget baseline window. On the spending side, baseline discretionary spending levels are largely constrained by the caps and automatic spending reductions enacted as part of the Budget Control Act of 2011 (BCA; P.L. 112-25) and further modified on several occasions, most recently with the Bipartisan Budget Act of 2018 (BBA 2018; P.L. 115-123).11

Since the CBO baseline assumes that current law continues as scheduled, it incorporates policy provisions in current law that have historically been revised before taking effect. Specifically, the CBO baseline assumes that discretionary budget authority from FY2019 through FY2021 will be restricted by the caps as created by the BCA as amended, and that certain tax policy changes enacted in the 2017 tax revision and in other laws will expire as scheduled under current law.12 This leads to baseline projections of lower spending and higher revenue levels relative to a baseline that would reflect policy changes some would consider likely given past actions (sometimes referred to as a "current policy" baseline).

In addition to these elements of current law, macroeconomic assumptions, including those related to GDP growth, inflation, and interest rates, will also affect the baseline estimates and projections. Minor changes in the economic or technical assumptions that are used to project the baseline also could result in significant changes in future deficit levels.

A summary of budget outcomes in the latest CBO baseline is provided in Table 1. CBO's current baseline projections, released in April 2018, show rising budget deficits over the next several years.13 This represents a reversal from the significant declines in inflation-adjusted deficits experienced in the past few fiscal years. Those declines were primarily due to continued increases in employment (which increased revenues collected from income and payroll taxes) and reductions in discretionary spending. While the baseline projections include continued declines in discretionary outlays, those reductions are more than offset by increases in mandatory spending. Mandatory spending increases are largely due to the rising cost of Social Security and Medicare programs, and declines in federal revenues.

|

FY2017 (actual) |

FY2019 |

FY2023 |

FY2028 |

|

|

Budget Deficit |

3.5 |

4.6 |

5.2 |

5.1 |

|

Debt Held by the Public |

76.5 |

79.3 |

87.9 |

96.2 |

Source: Congressional Budget Office, The Budget and Economic Outlook: 2018 to 2028, April 2018, Summary Table 2.

Baseline projections also include increases in debt held by the public (or debt held by all entities other than the federal government) throughout the 10-year budget window. Debt held by the public finances budget deficits and federal loan activity, and is a function of three things: (1) the size of existing debt, (2) economic growth, and (3) interest rates.14 Debt held by the public was 76.5% of GDP at the end of FY2017, and is projected to be 96.2% of GDP at the end of FY2028.

CBO also provides projections based on alternative policy assumptions, which illustrate levels of spending and revenue if current policies continue rather than expire as scheduled under current law. If discretionary spending increased with inflation after FY2018 instead of proceeding in accordance with the limits instituted by the BCA and tax reductions in the 2017 tax revision are extended, CBO projects an increase in the budget deficit of almost $2,400 billion relative to the current-law baseline, exclusive of debt servicing costs, over the FY2019 to FY2028 period. Beyond the 10-year forecast window, federal deficits are expected to grow unless major policy changes are made. This is a result of increases in outlays largely attributable to rising health care and retirement costs combined with little to no change in projected revenue levels over that timeframe.

Spending and Revenue Trends

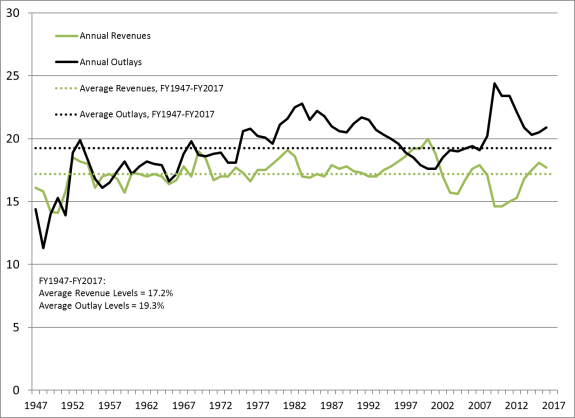

Over the last seven decades, federal spending has accounted for an average of 19.3% of the economy (as measured by GDP), while federal revenues averaged roughly 17.2% of GDP. Spending has exceeded revenues in each fiscal year since FY2002, resulting in annual budget deficits. Between FY2009 and FY2012, spending and revenue deviated significantly from historical averages, primarily as a result of the economic downturn and policies enacted in response to financial turmoil. In FY2017, the U.S. government spent $3,982 billion and collected $3,316 billion in revenue. The resulting deficit of $665 billion, or 3.5% of GDP, was higher than the average deficit from FY1947 through FY2017 of 2.1% of GDP. The trends in revenues and outlays between FY1947 and FY2017 are shown in Figure 1.

|

Figure 1. Total Outlays and Revenues, FY1947-FY2017 (as a % of GDP) |

|

|

Source: Congressional Budget Office and Office of Management and Budget. CRS calculations. |

Federal Spending

Federal outlays are often divided into three categories: discretionary spending, mandatory spending, and net interest. Discretionary spending is controlled by the annual appropriations acts. Mandatory spending encompasses spending on entitlement programs and spending controlled by laws other than annual appropriations acts.15 Entitlement programs such as Social Security, Medicare, and Medicaid make up the bulk of mandatory spending. Congress sets eligibility requirements and benefits for entitlement programs, rather than appropriating a fixed sum each year. Therefore, if the eligibility requirements are met for a specific mandatory program, outlays are made without further congressional action. Net interest comprises the government's interest payments on the debt held by the public, offset by small amounts of interest income the government receives from certain loans and investments.16

Federal Spending Relative to the Size of the Economy (GDP)

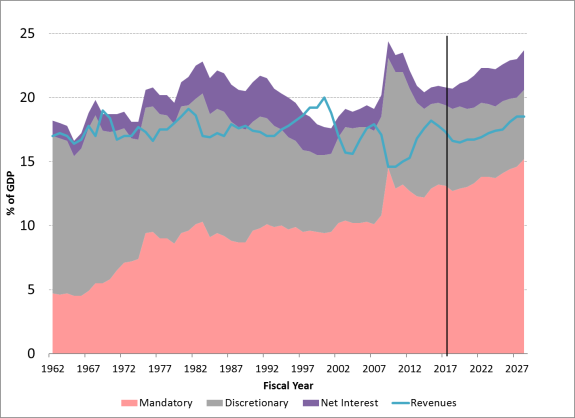

In FY2000, total outlays equaled 17.6% of GDP, the lowest recorded level since FY1966. In FY2009, outlays peaked at 24.4% of GDP. Outlays then fell steadily for the next few years, equaling 20.3% of GDP in FY2014, before rising to 20.8% of GDP in FY2017. Under the CBO baseline, total outlays are projected to continue rising and will reach 23.6% of GDP in FY2028. Figure 2 provides historical data and CBO projections of federal spending between FY1962 and FY2028.17

In FY1962, discretionary spending was consistently the largest source of federal outlays, peaking at 13.1% of GDP in FY1968. In the ensuing decades discretionary spending as a share of the economy underwent a gradual decline, and totaled 6.1% of GDP in FY2000. Discretionary spending increased in most years between FY2000 and FY2010, largely due to increases in security spending and federal interventions designed to stimulate the economy, and peaked in FY2010 at 9.1% of GDP.18 Discretionary spending fell from FY2010 through FY2017, due to both the wind down of stimulus programs and the implementation of restrictions established by the BCA. In FY2017, discretionary spending totaled 6.4% of GDP. CBO's most recent forecast projects short-term increases in discretionary spending, largely due to enactment of the Bipartisan Budget Act of 2018 (BBA 2018; P.L. 115-123). BBA 2018 allowed for large increases in discretionary spending in FY2018 and FY2019. Baseline forecasts subsequently include projections of lowered discretionary spending levels in FY2020 (the first year with spending caps unaffected by BBA 2018) and beyond. By FY2021, discretionary spending is projected to fall to 5.9% of GDP, which would be its lowest level ever; discretionary spending is projected to total 5.4% of GDP by FY2028. The projected decline in discretionary spending in the baseline over the next decade is largely due to the reductions under current law contained in the BCA.19

Figure 2 also shows mandatory spending as a share of GDP. Mandatory spending was a much smaller source of outlays than discretionary spending in earlier years, totaling just 4.7% of GDP in FY1962. Over time the share of mandatory spending has consistently grown, initially due to the increase in subscription in large mandatory programs such as Social Security and Medicare and then due to demographic and economic shifts that further increased the sizes of those programs.20 Mandatory spending totaled 13.2% of GDP in FY2016, up from 9.4% of GDP in FY2000. Mandatory spending peaked in FY2009 at 14.5% of GDP. Mandatory spending levels during the FY2009-FY2012 period were elevated mainly because of increases in outlays for income security programs as a result of the recession. The continuing economic recovery has resulted in lower mandatory spending on certain programs. Mandatory spending is projected to increase beginning in FY2019 due to growth in certain entitlement programs. Under current law, CBO projects that mandatory spending will total 15.2% of GDP in FY2028, greater than the FY2009 level.

Size of Federal Spending Components Relative to Each Other

It is also possible to evaluate trends in the share of total spending devoted to each component. In FY2017, mandatory spending amounted to 63% of total outlays, discretionary spending reached 30% of total outlays, and net interest comprised 7% of total outlays. The largest mandatory programs, Social Security, Medicare, and the federal share of Medicaid, constituted 48% of all federal spending in FY2017. CBO's baseline projections include a rise in net interest and a decline in discretionary spending as a share of total federal expenditures. In FY2028, the baseline projects that mandatory spending will total 64% of outlays, discretionary spending will total 23% of outlays, and net interest will total 13% of outlays.

Discretionary spending currently represents less than one-third of total federal outlays. Some budget experts contend that to achieve a long-term decline in federal spending, reductions in mandatory spending are needed.21 Budget and social policy experts have also stated that cuts in mandatory spending may cause substantial disruption to many households, because mandatory spending comprises important parts of the social safety net.22 Future projections of increasing deficits and resulting high debt levels may warrant further action to address fiscal health over the long term.23

Federal Revenue

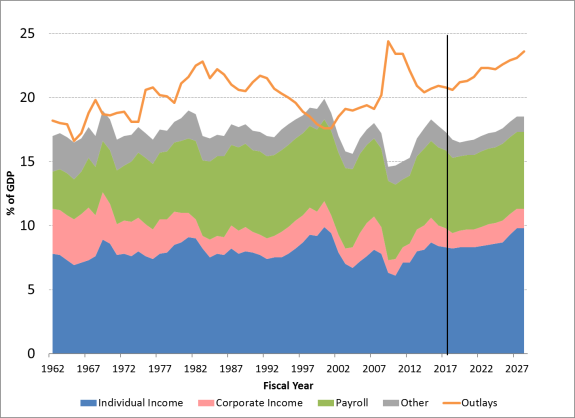

In FY2017, federal revenue collections totaled 17.3% of GDP, roughly equal to the historical average since FY1947 (17.2% of GDP). Real federal revenues have increased in recent years, due primarily to an improving economy. Between FY2009 and FY2013, revenue collection was depressed as the result of the economic downturn and certain tax relief provisions. In FY2009 and FY2010, revenue collections totaled 14.6% of GDP.

The 2017 tax revision (P.L. 115-97), enacted in December 2017, significantly altered federal receipt projections. Changes to the federal code implemented by P.L. 115-97 include a temporary reduction in individual income tax rates, a permanent reduction in the corporate income tax rate, permanent modification of the international tax system, and a number of mostly temporary modifications to income tax expenditures. Revenues are projected to decline from 17.8% of GDP in FY2016 to 16.5% of GDP in FY2019. Revenues are projected to gradually increase to total 18.5% of GDP in FY2028 under the CBO baseline. Increases toward the end of the baseline forecast are explained in part by the scheduled expiration of temporary provisions in the 2017 tax revision.

Figure 3 shows revenue collections between FY1962 and FY2028, as projected in the CBO baseline. Individual income taxes have long been the largest source of federal revenues, followed by social insurance (payroll) and corporate income taxes.24 In FY2017, individual income tax revenues totaled 8.3% of GDP. While individual income taxes as a share of the economy have remained relatively constant since the end of World War II, the share of federal revenues devoted to social insurance programs has increased from 2.9% of GDP in FY1962 to 6.1% of GDP in FY2017. That increase is largely attributable to growth in taxes that fund large entitlement programs. Shares devoted to corporate income and other outlays have declined, from 3.5% and 2.8% of GDP, respectively, in FY1962 to 1.5% of GDP and 1.4% of GDP, respectively, in FY2017. The CBO baseline projects that in FY2028 real individual tax revenues will be higher than current levels, other receipts will be lower than present levels, and corporate and payroll taxes will be roughly equivalent to FY2018 collections, though those projections would likely change if expirations of provisions in the 2017 tax revision do not proceed as scheduled.

Deficits, Debt, and Interest

The annual difference between revenue (i.e., taxes and fees) that the government collects and outlays (i.e., spending) results in either a budget deficit or surplus.25 Annual budget deficits or surpluses determine, over time, the level of publicly held federal debt and affect the level of interest payments to finance the debt.

Budget Deficits

Between FY2009 and FY2012, annual deficits as a percentage of GDP were higher than deficits in any four-year period since FY1945.26 The unified budget deficit in FY2017 was $665 billion, or 3.5% of GDP. The unified deficit, according to some budget experts, gives an incomplete view of the government's fiscal conditions because it includes off-budget surpluses.27 Excluding off-budget items (i.e., Social Security benefits paid net of Social Security payroll taxes collected and the U.S. Postal Service's net balance), the on-budget FY2017 federal deficit was $715 billion.

Budget Deficit for FY2018

The April 2018 CBO baseline projected the FY2018 budget deficit to be $804 billion, or 4.0% of GDP. The rise in the estimated budget deficit for FY2018 relative to FY2017 is the result of decreases in real revenues more than offsetting a small decrease in real outlays. FY2018 outlays are projected to increase to 20.8% of GDP from 20.6% of GDP in FY2017; revenues are projected to fall to 16.6% of GDP in FY2018, down from 17.3% of GDP in FY2017.

Federal Debt and Debt Limit

Gross federal debt is composed of debt held by the public and intragovernmental debt. Intragovernmental debt is the amount owed by the federal government to other federal agencies, to be paid by the Department of the Treasury, which mostly consists of money contained in trust funds. Debt held by the public is the total amount the federal government has borrowed from the public and remains outstanding. This measure is generally considered to be the most relevant in macroeconomic terms because it is the debt sold in credit markets. Changes in debt held by the public generally track the movements of the annual unified deficits and surpluses.28

Historically, Congress has set a ceiling on federal debt through a legislatively established limit. The debt limit also imposes a type of fiscal accountability that compels Congress (in the form of a vote authorizing a debt limit increase) and the President (by signing the legislation) to take visible action to allow further federal borrowing when nearing the statutory limit.

The debt limit by itself has no direct effect on the borrowing needs of the government.29 The debt limit, however, can hinder the Treasury's ability to manage the federal government's finances when the amount of federal debt approaches this ceiling. In those instances, the Treasury has had to take extraordinary measures to meet federal obligations, leading to inconvenience and uncertainty in Treasury operations at times.30

A binding debt limit would prevent the Treasury from selling additional debt and could prevent timely payment on federal obligations, resulting in default. Possible consequences of a binding debt limit include (1) a reduced ability of Treasury to borrow funds on advantageous terms, resulting in further debt increases; (2) possible turmoil in global economies and financial markets; and (3) acquisition of penalties or fines from the failure to make timely payments. More broadly, a binding debt limit may also affect the perceived credit risk of federal government borrowing. Consequently, the federal government's borrowing capacity could decline.31

Net Interest

In FY2017, the United States spent $263 billion, or 1.4% of GDP, on net interest payments on the debt. What the government pays in interest depends on market interest rates as well as the size and composition of the federal debt. Currently, low interest rates have held net interest payments as a percentage of GDP below the historical average despite increases in borrowing to finance the debt. Some economists, however, have expressed concern that federal interest costs could rise if interest rates continue to increase, resulting in future strain on the budget. Interest rates are projected to rise in the CBO baseline, resulting in net interest payments of $915 billion (3.1% of GDP) in FY2028, a figure that well exceeds the historical average of 1.7% of GDP since FY1940.32

Recent Budget Policy Legislation and Events33

The 115th Congress has adopted legislation with short- and long-term effects on the federal budget. The 2017 tax revision included major changes to the federal tax code, including changes to individual and corporate income taxes, international taxes, and a variety of tax expenditures (deductions, exclusions, and credits available to taxpayers). BBA 2018 enacted a two-year revision to the discretionary spending caps imposed by the BCA and also suspended the statutory debt limit until March 2019. Congress has also enacted several pieces of legislation with ramifications for the appropriations process and statutory debt limit.

P.L. 115-97, the 2017 Tax Revision

The 2017 tax revision, signed into law on December 22, 2017, made extensive changes to the federal tax system. A comprehensive list of the modifications made in the 2017 tax revision is available in CRS Report R45092, The 2017 Tax Revision (P.L. 115-97): Comparison to 2017 Tax Law, coordinated by [author name scrubbed] and [author name scrubbed]. Changes made in the 2017 tax revision include the following:

- temporary modifications (scheduled to expire at the end of tax year 2025) to individual income tax brackets, with a reduction in the top rate from 39.6% to 37%, an increase in the income threshold for the top bracket, and a temporary increase in the individual alternative minimum tax (AMT) exemption;

- a permanent modification in corporate income tax rates from a graduated rate structure with a top rate of 35% to a flat rate of 21%, and a permanent repeal of the corporate AMT;

- numerous modifications, mostly temporary, to the tax expenditures available to individual and corporate income tax filers, which include changes made to the standard deduction, the mortgage interest deduction, and the deduction for state and local taxes paid;

- a temporary (scheduled to expire at the end of tax year 2025) increase in the federal estate and gift tax exclusion; and

- a permanent shift in the taxation of foreign income from a modified version of a worldwide basis (where all income from U.S. firms earned in other countries is subject to U.S. taxation) to a modified version of a territorial profits basis (where profits are taxed on the basis of the country where they are earned).

Summary data from the final cost estimate conducted by the Joint Committee on Taxation (JCT) for the 2017 tax revision are provided in Table 2. The law was estimated to increase deficits by a total of $1,456 billion from FY2018 to FY2027, with deficit increases from FY2018 to FY2026 and a small deficit decrease in FY2027 as many of the temporary provisions included in the act expire. That estimate excluded macroeconomic feedback effects: JCT estimated that such effects would reduce deficits by a total of $385 billion over the FY2018-FY2027 period.34

|

Tax Category |

FY2019 |

FY2023 |

FY2027 |

FY2018-FY2027 |

|

Individual |

-188.8 |

-144.0 |

83.0 |

-1,126.6 |

|

Business |

-133.8 |

-16.4 |

-49.4 |

-653.8 |

|

International |

42.6 |

22.5 |

-0.8 |

324.4 |

|

Total |

-280.0 |

-137.9 |

32.9 |

-1,456.0 |

Source: Joint Committee on Taxation, JCX-67-17, Estimated Budget Effects of the Conference Agreement for H.R. 1, https://www.jct.gov/publications.html?func=startdown&id=5053.

Notes: Column and row totals may not sum due to rounding. Estimate is not inclusive of macroeconomic feedback; see text for further discussion of those effects.

CBO included an estimated effect of the 2017 tax revision on the federal budget in its April 2018 baseline release, which incorporated an additional year (FY2028) and included the effects on debt servicing costs and of implementation details learned since the date of enactment. That estimate projected that exclusive of macroeconomic feedback, the 2017 tax revision increased total deficits by $2,314 billion from FY2018 to FY2028; including macroeconomic feedback, which reduced deficits by $461 billion, the act was estimated to increase deficits by $1,854 billion over the same period.

The Bipartisan Budget Act of 2018 (BBA 2018)

BBA 2018, enacted into law on February 9, 2018, is the latest modification to the deficit reduction measures imposed by the BCA. The BCA was enacted on August 2, 2011, and contained a variety of measures intended to reduce future deficits by at least $2,100 billion over the FY2012-FY2021 period. Most of the direct reduction in deficits imposed by the BCA was to be generated by caps on discretionary budget authority, with the remainder produced by a sequester on some types of mandatory spending.35

Before enactment of BBA 2018, the deficit reduction measures established by the BCA were amended by the American Taxpayer Relief Act of 2012 (ATRA; P.L. 112-240), the Bipartisan Budget Act of 2013 (BBA 2013; P.L. 113-67), and the Bipartisan Budget Act of 2015 (BBA 2015; P.L. 114-74). The specific changes made by each amending law differ, but all three laws provided for short-term increases in discretionary spending by raising the discretionary budget authority caps established by the BCA in certain years while reducing mandatory spending by extension of the sequester on mandatory programs. Unlike BBA 2013 and BBA 2015, the direct and indirect budgetary effects to the BCA made in BBA 2018 were not offset (according to standard legislative cost estimation procedures) by other changes included in the law.

Table 3 shows how the discretionary caps from FY2014 through FY2021 have changed since enactment of the BCA. BBA 2018 raised the discretionary caps in FY2018 and FY2019 by a combined $296 billion, a much greater increase than provided for in previous amendments to the BCA. FY2018 and FY2019 discretionary budget authority as provided for in BBA 2018 is projected to be a combined $114 billion higher than the initial caps established by the BCA, though the caps in FY2020 and FY2021 remain virtually unchanged since 2012.

Table 3. Discretionary Caps on Budget Authority Established by the BCA as Amended

(in billions of dollars)

|

FY2014 |

FY2015 |

FY2016 |

FY2017 |

FY2018 |

FY2019 |

FY2020 |

FY2021 |

|

|

Original limits established by the BCA |

||||||||

|

Defense |

556 |

566 |

577 |

590 |

603 |

616 |

630 |

644 |

|

Nondefense |

510 |

520 |

530 |

541 |

553 |

566 |

578 |

590 |

|

Revised limits following Automatic Enforcement Measures |

||||||||

|

Defense |

501 |

511 |

522 |

535 |

548 |

561 |

575 |

589 |

|

Nondefense |

472 |

483 |

493 |

505 |

517 |

531 |

545 |

557 |

|

Current limits following legislative changes and revised projections |

||||||||

|

Defense |

520 |

521 |

548 |

551 |

629 |

647 |

576 |

591 |

|

Nondefense |

492 |

492 |

518 |

519 |

579 |

597 |

542 |

555 |

Source: CRS Report R44874.

Notes: See CRS Report R44874, The Budget Control Act: Frequently Asked Questions, for more detail on the automatic enforcement measures established by the BCA. Legislative changes were enacted in ATRA, BBA 2013, BBA 2015, and BBA 2018. The BCA requires CBO and OMB to periodically revise future discretionary limits to ensure that the deficit reduction targets established by the BCA as amended are reached.

Appropriations and Debt Limit Legislation

Each year Congress enacts a set of laws providing for discretionary appropriations, which gives federal agencies the authority to incur obligations. Appropriations acts typically provide authority for a single fiscal year, and may come in the form of regular appropriations (providing authority for the next fiscal year), supplemental appropriations (providing additional authority for the current fiscal year), or continuing appropriations (providing stop-gap authority for agencies without a regular appropriation).36 Most recently, the Consolidated Appropriations Act, 2018 (P.L. 115-141) was signed into law on March 23, 2018, providing full-year appropriations for all federal agencies without a regular appropriation through the end of FY2018 (which ends September 30, 2018). Time periods for which no or incomplete appropriations are provided are known as funding lapses, and may result in partial or full shutdown of federal operations. Short-term funding lapses occurred in January and February 2018.37

Recent legislation has also modified the statutory debt limit. BBA 2018 suspended the debt limit until March 1, 2019, and dictated that the debt limit be increased upon reinstatement as needed to accommodate any additional federal borrowing undertaken up to that point.38 Before enactment of BBA 2018, Treasury had implemented extraordinary measures (which had been used in prior debt limit episodes) to prevent the debt limit from binding upon its reinstatement from a previous suspension on December 8, 2017.

Budget for FY2019

The Trump Administration submitted its FY2019 budget to Congress on February 12, 2018. The President's budget lays out the Administration's views on national priorities and policy initiatives. Congress has also begun consideration of the FY2019 budget.

Trump Administration's FY2019 Budget

President Trump presented his policy agenda in the Administration's FY2019 budget submission. If the policies are fully implemented, the Administration estimates that total FY2018 outlays would be $4,214 billion (21.0% of GDP) and revenues would be $3,340 billion (16.7% of GDP), resulting in a budget deficit of $873 billion (4.4% of GDP). The Administration estimates that deficits under the proposed budget would increase in FY2019 and then decline as a share of output over the course of the budget window, with the significance of the decline varying with how certain macroeconomic effects are applied to the forecast.

A summary of the total deficit effects of the budget's proposed changes is presented in Table 4. The budget proposes reforms that would reduce several types of outlays. The largest spending cut proposals are to (1) nondefense discretionary programs, with an outlay reduction of $1,669 billion from FY2019 through FY2028; (2) Medicaid and other mandatory programs (including Children's Health Insurance and welfare), with $1,074 billion in FY2019-FY2028 outlay reductions; (3) repeal and replacement of the Patient Protection and Affordable Care Act (ACA; P.L. 111-48), with $675 billion in FY2019-FY2028 deficit reductions; and (4) Medicare programs, with a $236 billion reduction in FY2019-FY2028 outlays.

The budget proposes increases in infrastructure spending, which would result in total outlays increasing by $199 billion over the FY2019-FY2028 period. Finally, the budget proposes increases to the total defense budget, with increases in base defense spending and decreases in Overseas Contingency Operations (OCO) spending resulting in an increase in discretionary defense outlays of $143 billion over the FY2019-FY2028 period.

The President's budget assumes that those policy changes produce additional indirect budgetary effects on net interest spending and through changes in economic output. The proposed policy changes are estimated to reduce net interest spending by $319 billion over the FY2019-FY2028 period. Moreover, the budget assumes those policies increase economic growth in a manner that reduces FY2019-FY2028 deficits by an additional $813 billion. The budget's economic forecast was based on information available in November 2017, and the budget states that this additional growth accounts for enactment of the 2017 tax revision.39 As noted earlier, the CBO and JCT included smaller deficit reduction estimates ($461 billion over the FY2019-FY2028 period and $385 billion over the FY2018-FY2027 period, respectively) resulting from such macroeconomic feedback.40

Table 4. Budgetary Effects of President's FY2019 Budget Proposals, FY2019-FY2028

(in billions of dollars)

|

Proposal (Major Budget Category) |

Increase (+) or Decrease (-) in FY2019-FY2028 Deficits from Policy Changes |

|

Infrastructure Investment (Mandatory Outlays) |

+199 |

|

Medicare (Mandatory Outlays) |

-236 |

|

Medicaid & Other Programs (Mandatory Outlays) |

-1,074 |

|

Defense (Discretionary Outlays) |

+143 |

|

Nondefense (Discretionary Outlays) |

-1,670 |

|

Net Interest (Net Interest Outlays) |

-319 |

|

Repeal and Replace Affordable Care Act (Unspecified) |

-675 |

|

Effect of Assumed Boost to Economic Growth (Unspecified) |

-813 |

|

Total |

-4,445 |

Source: OMB, Budget of the U.S. Government Fiscal Year 2019, Tables S-1 through S-3.

Notes: Indirect budgetary effects are italicized. For past budgets CBO has provided an independent analysis of proposals in the President's budget. That information has not yet been released.

The President's budget uses economic projections in its calculations that differ from those used in congressional budget operations. The budget projects that the real economic growth rate (measured as the percentage change in real GDP) will be 3.0% per year both in FY2018 and over the FY2019 through FY2028 period. That total is higher than the assumptions included in CBO's April 2018 forecast, which includes real economic growth projections averaging 1.9% per year from FY2019 through FY2028. Previous iterations of the President's budget have also included differences in economic projections with those produced by CBO, though such differences have typically been smaller than the projection gap in the FY2018 and FY2019 budgets.41 The United States last experienced real economic growth of greater than 3.0% in FY2005.42 The Administration estimated that assuming real economic growth to be 1% lower over the FY2018-FY2018 period would increase its projected budget deficits by $3,144 billion over the FY2018 to FY2028 window.

Deficit Projections in the President's FY2019 Budget

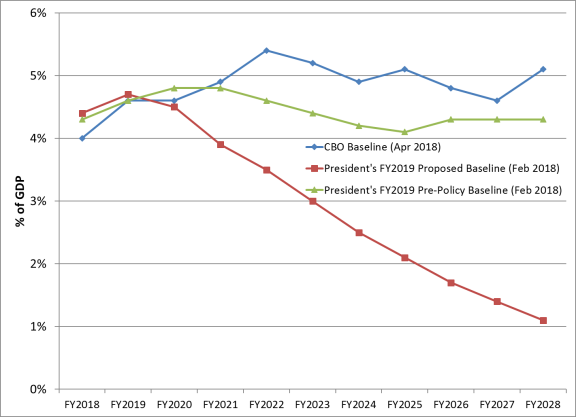

The Trump Administration provided two deficit projections in its FY2019 budget.43 First, OMB projected a Balanced Budget and Emergency Deficit Control Act (BBEDCA) baseline: the BBEDCA baseline, or "pre-policy" baseline, assumes that discretionary spending remains constant in real (i.e., inflation-adjusted) terms and revenue and mandatory (or direct) spending continue as under current law.44 Under this scenario, the FY2019 deficit is projected to total $0.969 trillion (4.6% of GDP), the FY2028 deficit is projected to be $1,378 billion (4.3% of GDP), and cumulative deficits are projected to be $11,540 billion over the FY2019-FY2028 period.

The other deficit projection, the proposed budget, illustrates the effect on the budget outlook if all of the policies proposed in the budget are implemented. In FY2019, the Administration projects that the deficit will reach $984 billion (4.7% of GDP). Under the proposed budget, deficits would steadily decrease from FY2021 through FY2028, producing a budget deficit of $363 billion (1.1% of GDP) in FY2028. The net budget deficit from FY2019 through FY2028 totals $7,095 billion in the proposed budget. Neither projection incorporates the budgetary effects of BBA 2018, which was enacted just prior to the budget release. CBO estimated that BBA 2018 would increase FY2018-FY2027 deficits by a combined $252 billion relative to current law, exclusive of debt servicing costs.45 Figure 4 illustrates how federal deficits in the President's pre-policy and proposed budgets compare to current law (CBO baseline) over the next decade.46 The proposals in the President's budget are projected to result in deficit reductions of $4,445 billion over the next decade relative to the pre-policy baseline.47

Adjustments to BCA Discretionary Caps

The President's budget proposes to adjust the caps on discretionary spending as originally established by the Budget Control Act (BCA). In August 2011, the BCA placed limits on discretionary budget authority and included provisions for additional spending cuts to be implemented through an automatic process that were eventually triggered by the absence of agreement from a committee tasked with passing deficit reduction legislation. Since enactment of the BCA, Congress and the President have modified the BCA several times, primarily to allow increases in discretionary spending (for more information, see the earlier section titled "Recent Budget Policy Legislation and Events").

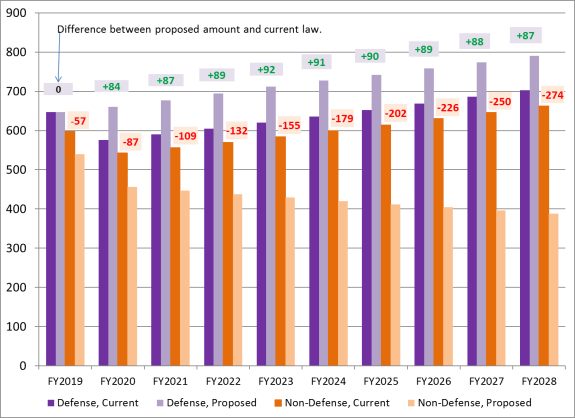

A summary of the changes to the discretionary caps in the President's budget is presented in Figure 5. In FY2019, the President's budget would leave the defense cap unchanged while decreasing the nondefense cap by $57 billion; both caps were recently modified by BBA 2018. The budget calls for increases to the defense caps by $84 billion and $87 billion in FY2020 and FY2021, respectively, and proposes decreases in the nondefense caps of $87 billion and $109 billion in FY2020 and FY2021.

While the caps on discretionary budget authority as established by the BCA are scheduled to expire after FY2021, the President's budget also proposes changes to discretionary spending in FY2022-FY2028 under the assumption that discretionary spending grows with current services growth rates. Over the FY2022-FY2028 period the Administration proposes increases to defense spending in each year ranging from $87 billion to $92 billion. The budget proposes decreases in nondefense spending that grow from $132 billion in FY2022 to $274 billion in FY2028.

FY2019 Congressional Budget Activity

Following passage of full-year FY2018 appropriations, Congress has turned its attention to the FY2019 budget. The budget committees in the House and Senate each may develop budget legislation as they receive information and testimony from a number of sources, including the Administration, the CBO, and congressional committees with jurisdiction over spending and revenues. Absent legislative action, the limits on discretionary budget authority for FY2019 are scheduled to be $647 billion for defense activities and $597 billion for nondefense activities, which is a combined $36 billion higher than the limits in FY2018 (see Table 3).

Considerations for Congress

Ongoing federal budgetary challenges remain which may lead to congressional action. Issues related to deficit reduction and the long-term budget outlook may continue to arise in policy discussions. Increased spending on entitlement programs, as currently structured, will likely contribute to rising deficits and debt, placing ever-increasing focus on how to achieve fiscal sustainability over the long term.

Ongoing Budget Issues

Various budget issues may feature prominently in near-term congressional debates. Discussions over FY2019 discretionary appropriations legislation may be held in advance of the beginning of the fiscal year (or afterwards in the case of supplemental or continuing appropriations). Congress may elect to revisit the deficit reduction measures imposed by the BCA as amended, which include discretionary caps on defense and nondefense budget authority through FY2021 and spending reduction measures on certain mandatory programs through FY2027. As discussed earlier, Congress has already lifted the discretionary caps (to allow for more spending) in each year from FY2013 through FY2019 relative to their values established in the BCA.48

Congress may also choose to modify the statutory debt limit. The debt limit is currently suspended through March 2019, at which time it is to be reinstated to accommodate federal borrowing levels. If faced with a nearly binding debt limit, Treasury may choose to enact extraordinary measures to postpone when the debt limit binds. Short-run budget surpluses in March and April of that year (primarily from the receipt of annual income tax returns) mean that extraordinary measures enacted in March will likely postpone a binding debt limit by several months.49 The latest CBO budget forecast projects a larger nominal budget deficit in FY2019 ($981 billion) than the federal deficit in FY2017 ($665 billion), which was the last year extraordinary measures were enacted in March. Such an increase may reduce the length of time extraordinary measures would postpone a binding debt limit relative to what was experienced in 2017.

Long-Term Considerations

The federal government faces long-term budget challenges. Occasional budget deficits are not necessarily problematic. Deficit spending can allow governments to smooth outlays and revenues to shield taxpayers and program beneficiaries from abrupt economic shocks in the short term, while also temporarily boosting GDP when the economy is underperforming. Persistent deficits, however, lead to growing levels of federal debt that may lead to higher interest payments and may also have adverse macroeconomic consequences in the long term, including slowing investment and lowering economic growth. Indefinite growth of real debt will eventually lead to a borrowing crisis, though the timing of such an event is subject to great uncertainty. Reducing large deficits will require increases in taxes, reductions in spending, or both.

Some measures of fiscal solvency in the long term indicate that, under current policy, the United State faces major future imbalance, specifically as it relates to rising retirement and health care costs and the likely impact on government-financed health care spending. Existing deficit reduction policies like the BCA had improved recent and near-term deficits but do not make significant changes to the parts of the budget that are projected to grow the fastest in the long run. Therefore, many budget analysts believe that additional deficit reduction is required to put the budget on a sustainable path over the long term. CBO's current law baseline projects inflation-adjusted deficits (equal to 4.9% of GDP) from FY2019 through FY2028 despite a real economic growth rate averaging 1.8% per year over the same period: that combination of sustained economic growth and large federal deficits would be unprecedented in the postwar era.

CBO, GAO, and the Trump Administration agree that the current mix of federal fiscal policies is unsustainable in the long term. The nation's aging population, combined with rising health care costs per beneficiary, may keep federal health costs rising faster than per capita GDP. CBO projected in March 2017 that under current policy, federal spending on health programs (including Medicare, Medicaid, CHIP, and exchange subsidies) would grow from 5.5% of GDP in FY2017 to 8.8% of GDP in FY2047.50 A 2017 GAO report on fiscal health also cited health spending as a source of concern.51 Though these forecasts are highly uncertain, it seems probable that spending on these programs will rise as a share of GDP over time.

In addition, growing debt and rising interest rates are projected to cause interest payments to consume a greater share of future federal spending. CBO projects that under current law, spending to service the federal debt (net interest payments) will grow rapidly, from 1.4% of GDP in FY2017 to 5.2% of GDP in FY2047.52 GAO's recent long-term fiscal simulations, under an alternative policy scenario, projected that debt held by the public as a share of GDP would exceed the post-World War II historical high in the next 15 to 25 years.53

Keeping future federal outlays at 20% of GDP, or approximately at their historical average, and leaving fiscal policies unchanged, according to CBO projections, would require drastic reductions in all spending other than that for Medicare, Social Security, and Medicaid, or reining in the costs of these programs. Under CBO's extended baseline, maintaining the debt-to-GDP ratio at today's level (77%) in FY2047 would require an immediate and permanent cut in noninterest spending, increase in revenues, or some combination of the two in the amount of 1.9% of GDP (or about $380 billion in FY2018 alone) in each year. Maintaining this debt-to-GDP ratio beyond FY2047 would require additional deficit reduction. If policymakers wanted to lower future debt levels relative to today, the annual spending reductions or revenue increases would have to be larger. For example, in order to bring debt as a percentage of GDP in FY2047 down to its historical average over the past 50 years (40% of GDP), spending reductions or revenue increases or some combination of the two would need to generate net savings of roughly 3.1% of GDP (or $620 billion in FY2018) in each year.54

The alternative to decreased spending as a means of deficit reduction is to increase revenues through modifications to the federal tax system. The 2017 tax revision represented the latest major change to the federal tax code, and was estimated by CBO and JCT to reduce revenues over the FY2018-FY2027 period. CBO's latest budget and economic forecast projects that revenues as a percentage of GDP will be at or below their postwar average (17.2% of GDP) from FY2018 through FY2023 before reaching 18.5% of GDP in FY2028. Federal revenue levels toward the end of the 10-year baseline window will depend in part on whether the temporary tax provisions enacted as part of the 2017 tax revision expire as scheduled.

In the long run, increases in federal debt are constrained by the amount of remaining "fiscal space," which is the amount of government borrowing that creditors are willing to finance. The amount of fiscal space available depends on the current size of the debt, how fast it is increasing relative to GDP, and the attractiveness of federal debt to investors relative to other market instruments. Changes in debt relative to GDP depend on the size of deficits, the government's borrowing rate, and how quickly the economy is growing. With continuously increasing debt levels, at some point debt would become so large that investors would no longer be willing to finance deficits and fiscal space would be exhausted. Exactly when investors would stop financing federal borrowing is uncertain. Because interest rates are presently lower than their historical averages, there is little current concern that the federal government is in danger of running out of fiscal space in the short run.55

Appendix. Budget Documents

The Congressional Budget Office (CBO) provides data and analysis to Congress throughout the budget and appropriations process. Each January, CBO issues a Budget and Economic Outlook that contains current-law baseline estimates of outlays and revenues.56 In March, CBO typically issues an analysis of the President's budget submission with revised baseline estimates and projections. These documents can be delayed as a result of the legislative agenda or if the President's budget is off schedule. In late summer, CBO issues an updated Budget and Economic Outlook with new baseline projections.

In these documents, CBO sets a current-law baseline as a benchmark to evaluate whether legislative proposals would increase or decrease outlays and revenue collection. Baseline estimates are not intended to predict likely future outcomes, but to show what spending and revenues would be if current law remained in effect. CBO typically evaluates the budgetary consequences of most legislative proposals and the Joint Committee on Taxation (JCT) evaluates the consequences of revenue proposals.

CBO also releases other periodic publications focusing on the future fiscal health of the United States. In its publication The Long-Term Budget Outlook, CBO makes projections on the state of the federal budget over the next 30 years. CBO discusses spending and revenue levels and the related issues that it expects will arise under different policy assumptions. In its Budget Options volumes, CBO provides specific policy options and the impact they will have on spending and revenues over a 10-year budget window. CBO also provides arguments for and against enacting each policy.

The President's budget contains five major volumes: (1) The Budget, (2) Historical Tables, (3) Analytical Perspectives, (4) Appendix, and (5) Supplemental Materials.57 These documents lay out the Administration's projections of the fiscal outlook for the country, along with spending levels proposed for each of the federal government's departments and programs. The Historical Tables volume also provides significant amounts of budget data, much of which extend back to 1962 or earlier. Along with the Administration's budget documents, the Department of the Treasury also releases its Green Book, which provides further detail on the revenue proposals that are contained in the budget.58