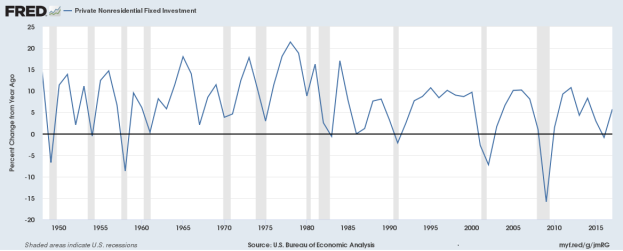

Figure 1. Annual Percentage Change in Business Investment

1948-2017

Source: Bureau of Economic Analysis, downloaded from FRED.

Business capital investment spending is composed of private spending on nonresidential structures (e.g., factories), equipment (e.g., machinery), and intellectual property products (e.g., software). Business investment is a key determinant of economic growth. When businesses add to the capital stock, the value of goods and services (i.e., gross domestic product [GDP]) the economy can produce increases. One reason that economic growth has been lower in the last decade is because business investment spending has grown more slowly. Boosting investment spending was one of the key goals of the 2017 tax cuts.

Average annual business investment spending from 2008 to 2017 was lower than the average for the previous six 10-year periods, going back to 1948. During the financial crisis, investment spending declined by 8.2% per year in 2008 and 2009, as shown in Figure 1. It has grown since then, but by a relatively low annual average of 4.5%, compared with about 6% from 1946 to 2000. In 2017, investment spending increased by 4.7%.

|

Figure 1. Annual Percentage Change in Business Investment 1948-2017 |

|

|

Source: Bureau of Economic Analysis, downloaded from FRED. |

The equipment category declined the most during the crisis, but has increased at the fastest pace in the recovery. The slowdown during the current expansion has been greatest within structures. Within the structures category, growth has recently been whipsawed from year to year by large swings in the subcategory "mining exploration, shafts, and wells," declining by 43% in 2016 and rising by 58% in 2017. This pattern reflects the sensitivity of investment spending for resource extraction to commodity prices, generally, and to the growth of U.S. shale production, in particular.

The investment slowdown is not limited to the United States; it has also occurred across advanced and developing economies, suggesting that plausible explanations for the slowdown are not U.S. specific.

Investment spending growth and economic growth are endogenous, meaning that at the same time that changes in investment spending cause changes in economic growth, changes in economic growth also cause changes in investment spending. Economists have debated whether the slowdown in business investment has exceeded what would be expected given the slowdown in growth. Economist Larry Summers attributes 48% of the decline in potential GDP to the decline in investment and 11% to the decline in productivity. One study, by contrast, argues that "weak investment…growth does not appear to have been an important independent contributor to weak [GDP] growth." The study attributes the investment slowdown to the slowdown in underlying economic growth, which stems from a structural slowdown in productivity growth and labor force growth, the latter due to the aging of the population. If capital and labor are complements instead of substitutes, a slowdown in labor force growth would reduce investment growth—as firms add fewer workers, less capital is needed for those workers to use.

Investment could be low because of low investment demand (firms' willingness to invest) or supply (a dearth of available savings to finance investment). The fact that real interest rates have been persistently low points to the former explanation. Therefore, most explanations for the slowdown focus on why investment demand has been low.

Cyclical and structural reasons are distinguishable for the slowdown in business investment and economic growth. Cyclical reasons relate to the business cycle—when overall business conditions are poor, as in a recession, firms are likelier to postpone investment spending, and when conditions are booming, firms are more likely to invest. From 2007 to 2009, the economy was in the longest and deepest recession since the Great Depression. From 2009 to 2013, the economic recovery was unusually sluggish, excess capacity remained elevated, and unemployment remained unusually high. One study attributes over 80% of the investment slowdown to weak demand across advanced economies. Beyond normal cyclical effects, the financial crisis may have temporarily disrupted some businesses' access to capital. The International Monetary Fund found that decreased credit availability limited investment during the recovery for euro-crisis countries, but not for the United States.

Cyclical factors have been less important since the economy recently returned to a more normal state. Given that the business investment slowdown predated the financial crisis—the annual average increase in investment from 2001 to 2007 was 2.5%—there are also a number of possible structural reasons for the slowdown. Hypotheses include the following:

The behavior of investment spending as the economic expansion progresses will shed more light on the relative merits of these various theories. If investment spending picks up as the economy reaches full employment, it would indicate that the weakness was mainly cyclical. If it does not, that would support the structural explanations.